DeFi Derivatives

Instructors: Andreas Park

Commercial Paper/T-Bill like securities

YIELD Protocol

- basic idea: zero-coupon loans

- You have:

- target asset

- collateral

- y-token trading at discount price

- examples: yDAI

- expires in 1 year

- price: $.92

- backed by ETH

- buying = you earn 8/92 cents=8.7% RoR

YIELD example

1 ETH = 150 DAI

collateralization ratio 125%

seller

buyer

Assumptions

supplies 1 ETH collateral today

mints (=borrows) 100 yDAI to be repaid in 1 year

y

receives 92 DAI today

pays 92 DAI today

y

receives 100 yDAI

repays loan with 100 DAI

deposits yDAI and receives 100 DAI

YIELD example: scenarios

seller

buyer

Scenario 1: ETH \(\ge\)125 DAI

deposits 100 yDAI

withdraws 100 DAI

receives balance of 1 ETH - 100 DAI

What does the seller own (ignore keeper fee)?

- 92 Dai (the loan)

- 0.2 ETH x price(ETH)=25 DAI (assume price=125)

seller

buyer

Scenario 2: ETH falls to <125 DAI

keeper

closes undercollateralized position \(\to\) sells 0.8 ETH for 100 DAI

receives 100 DAI early

receives balance

of 0.2 ETH

Futures-like securities

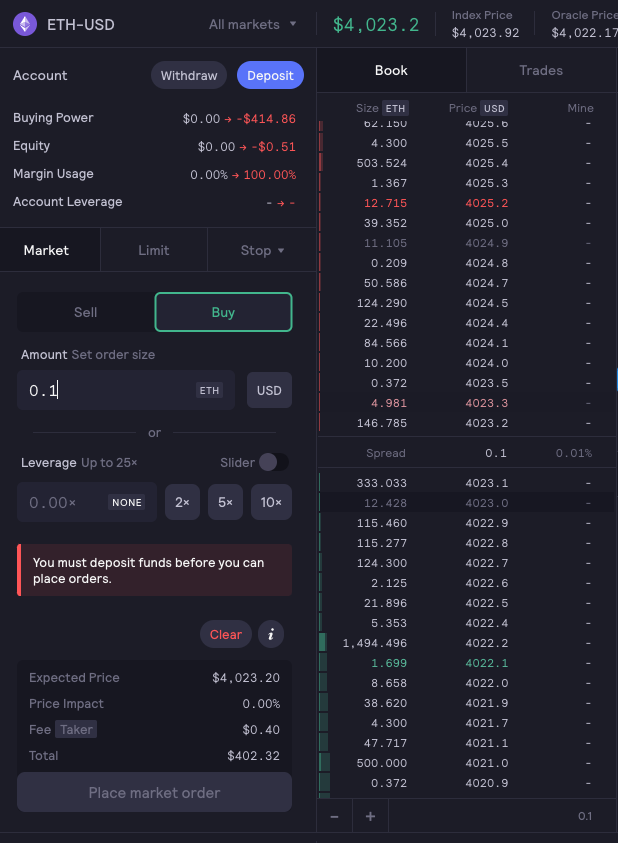

Perpetual futures on Bitcoin on dYdX

- perpetual future = futures contract without a settlement date

- can be long or short

- index price based on Binance, Bitfinex, Bitstamp, Bittrex, Coinbase Pro, Gemini, and Kraken

- dYdX:

- decentralized exchange with L2 solution

- stores signed orders off-chain

- liquidates underwater positions transparently on-chain

Perpetual futures on dYdX

- Why? Access returns on non-native assets (Bitcoin, Solana) on the Ethereum blockchain

- Goal of perpetual futures: keep price close to index

- funding fees:

- futures price>index: long pay short

- futures price<index: short pay long

- two margins:

- initial: 10%

- maintenance: 5%

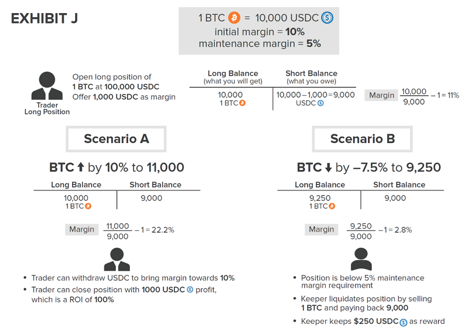

Example

Date: Oct 27, 2021

Example

- 1 ETH = 2,000 USDC

- open long of 1ETH when 2,000 USDC with 200 USDC margin

Scenario: ETH \(\downarrow\) 7.5% to 1,850

1 ETH=

1,850 USDC

1,800 USDC

\(\frac{1,850}{1,800}-1=2.78\%\)

Scenario: ETH \(\uparrow\) 10% to 2,200

1 ETH=

2,200 USDC

1,800 USDC

\(\frac{2,200}{1,800}-1=22\%\)

Options for the trader

- Withdraw up to 200 USDC to bring margin to 10%

- Close the position with a 200 USDC profit = 100% return

What will happen

- position is below 5% maintenance margin

- keeper liquidates position: sells 1 ETH and pays 1,800 to contract

- keeper keeps $50 as reward

long balance

(what you will get)

short balance

(what you owe)

margin

1 ETH=

2,000 USDC

2,000-200

=1,800 USDC

\(\frac{2,000}{1,800}-1=11\%\)

Beginning

Smart Contract Derivatives with Synthetix

- creations of Synths

- tokens linked to underlying price feed provided by a Chainlink Oracle

- long asset: sToken (sETH, sBTC)

- short asset: iToken (iMKR, iAAV)

Note: this screenshot is from June 2021; the equity synths have since been removed

Smart Contract Derivatives with Synthetix: how does it work?

- single collateral asset SNX \(=\) utility token

- you first need to buy SNX tokens and stake them using Mintr

- you can mint sTokens against SNX holdings (over-collateralization: 750%) (fluctuations in SNX and Synths both matter!)

- you incur debt as proportion of total debt of the system

Example for Synthetix

assets

price

quantity

fraction of debt

BTC

ETH

USDC

10,000

1,000

1

2

20

20,000

total debt: 60,000

33% of 60,000=20,000

33%

33%

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

Example for Synthetix: prices for ETH and BTC up

assets

price

quantity

fraction of debt

BTC

ETH

USDC

20,000

5,000

1

2

20

20,000

total debt: 160,000

33%=53,333

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

33%=53,333

33%=53,333

40,000-53,333

=-13,333

100,000-53,333

=46,667

20,000-53,333

=-33,333

you effectively bet that your position outperforms the pool

Example for Synthetix: prices for ETH and BTC down

assets

price

quantity

fraction of debt

BTC

ETH

USDC

5,000

500

1

2

20

20,000

total debt: 40,000

33%=13,333

2 sBTC

20 sETH

20,000 sUSDC

minted

gain/loss

10,000-13,333

=-3,333

20,000-13,333

=7,777

33%=13,333

33%=13,333

10,000-13,333

=-3,333

what is dydx?

main product:

BTC perpetual futures contract

initial margin =

amount of collateral needed to be posted

maintenance margin =

amount of price movement after which collateral needs to be replenished

Source: Harvey, Ramachandran, and Santoro (2020)

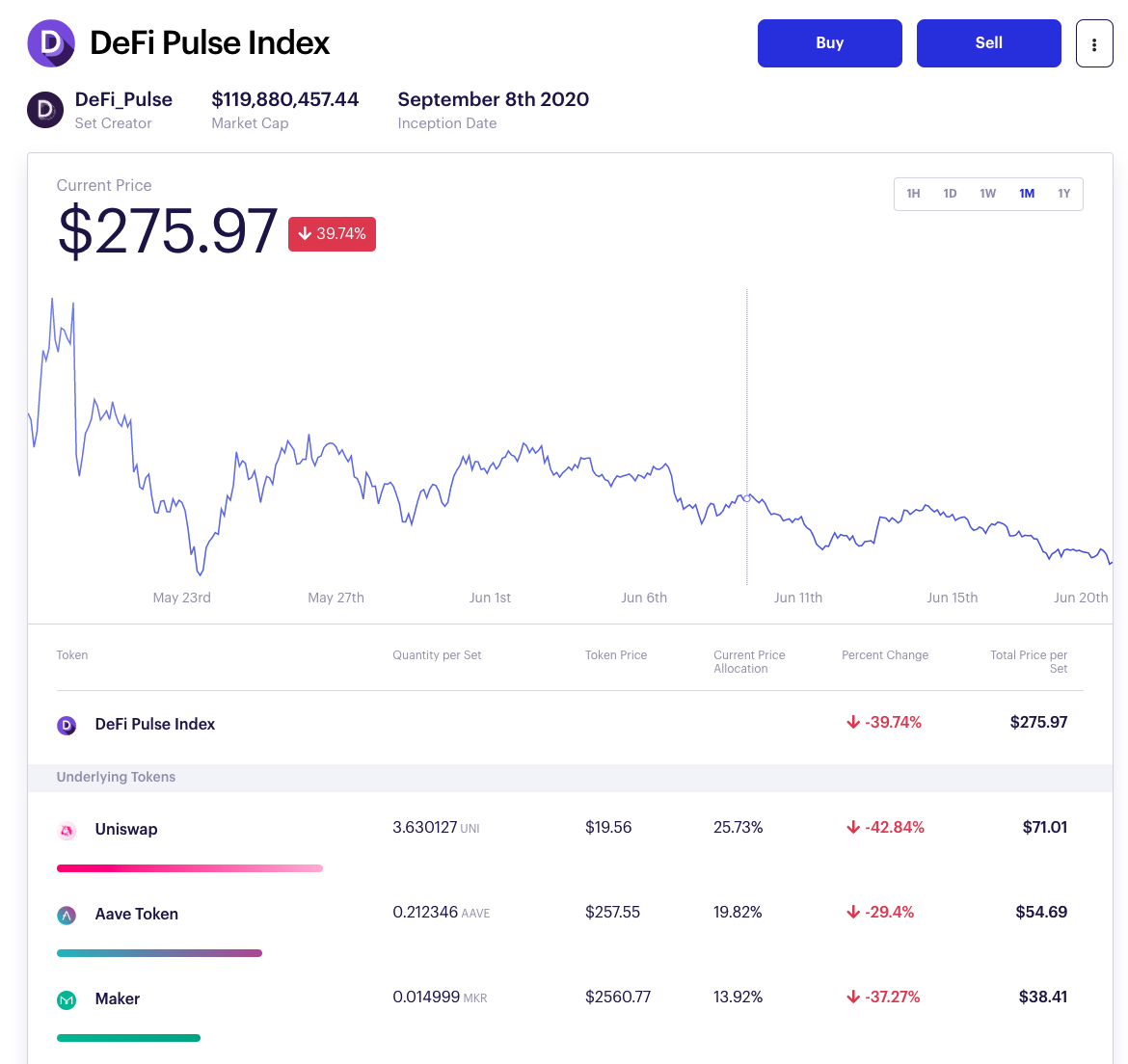

ETF-like securities

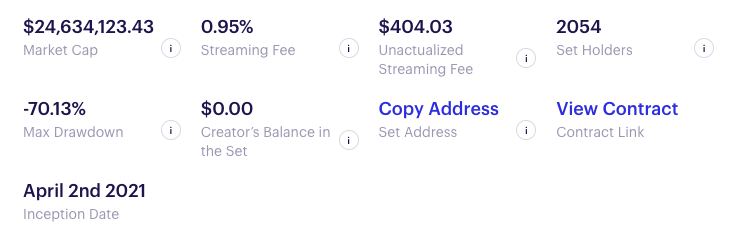

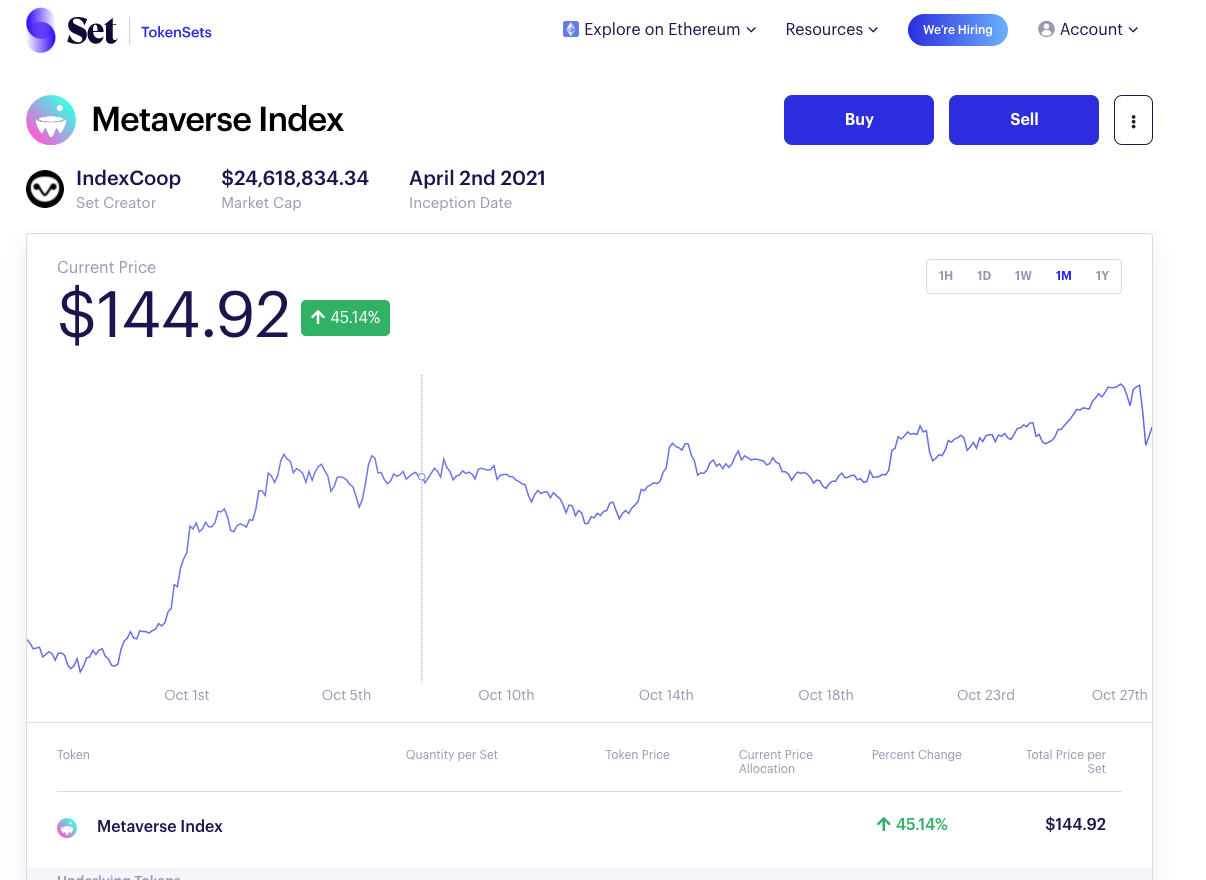

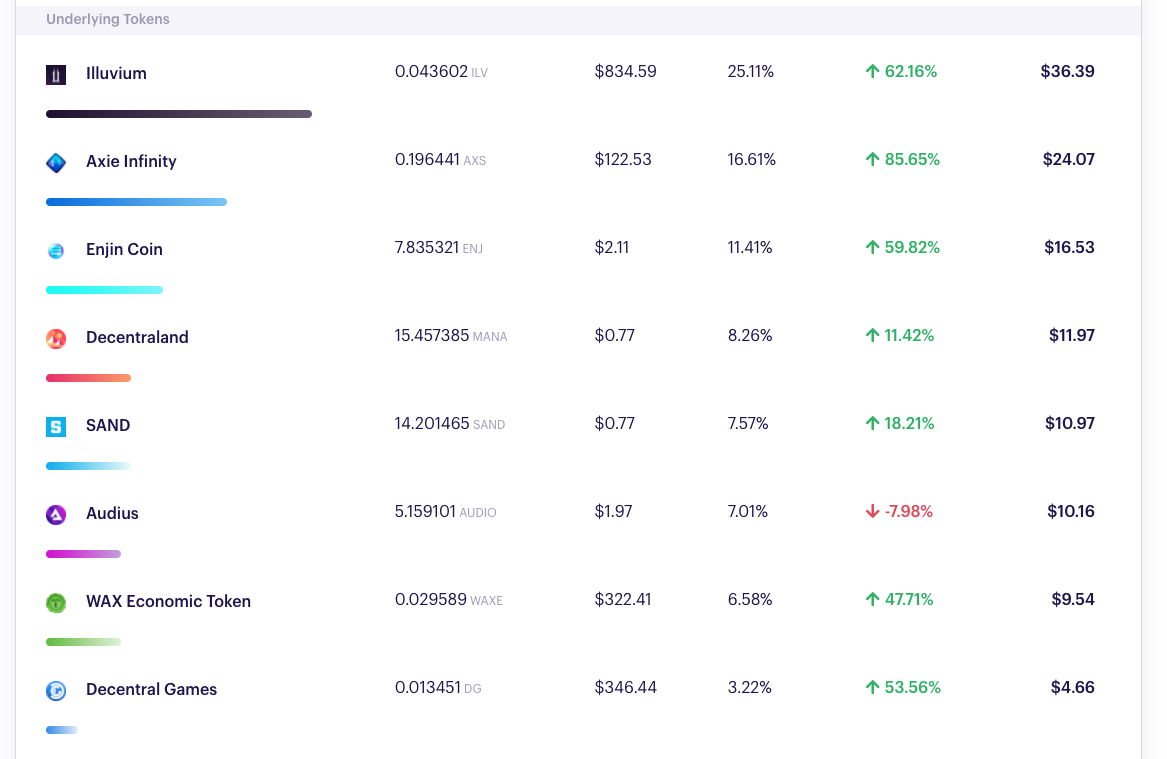

Securities Creation: Tokensets

idea: create new mutual fund like asset

Securities Creation: Tokensets