Payment Tech:

From Pain Points to Innovation

Instructor: Andreas Park

Rotman School of Management & FinHub, Rotman's Financial Innovation Lab

Date: June 2023

Business of Payments Executive Ed

A quick survey, before we even start

please navigate to

My agenda

Topic: Innovations in payments: Why and how?

- Understanding payments-related pain points

- Study solutions from around the world

Goal: Convey solutions and competitive developments to payments-related challenges of consumers & businesses

HOW Part 1: Innovation WITHIN the current institutional arrangements

HOW Part 2: Innovation OUTSIDE the current institutional arrangements

- blockchain and decentralied finance

- Central Bank-issued Digital Currencies

Part 1

Innovation WITHIN the current institutional arrangements

Where are we?

Big Picture

Small Businesses

Consumers and Merchants

Some totally unscientific evidence

sending money peer-to-peer

help with budgeting

mortgage

loans for car

payment card

Recent in-class discussion assignment (50 students)

What do you need a bank for? (in this order)

in many countries, this space is FinTech

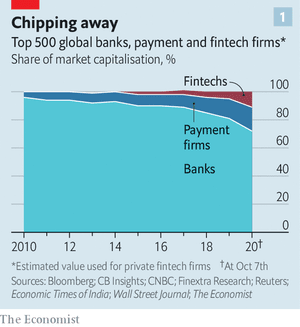

Why Payment Innovation?

Source: CNBC Jan 15, 2021, https://www.cnbc.com/2021/01/15/jamie-dimon-says-jpmorgan-chase-should-absolutely-be-scared-s-less-about-fintech-threat.html

Why? Highest touchpoint between customer and bank

"Payments is the hill for banks to die on"

"JPM should absolutely be scared s**tless about the FinTech threat"

Why Payment Innovation?

payments is a profitable line of business

payments data is very valuable

payments \(=\) clunky and full of frictions

payments is the entry level drug to all things FinTech

Legacy institutions are most likely attacked where the greatest sources of customer friction meet the largest profit pools

Giancarlo Bruno, Senior Director, Head of Financial Services Industry, World Economic Forum

payments matter a lot more to people than we might think

fritctionless

fast

open & expandable

cheap

secure

How would a perfect payment system look like?

Big Picture

Small Businesses

Consumers and Merchants

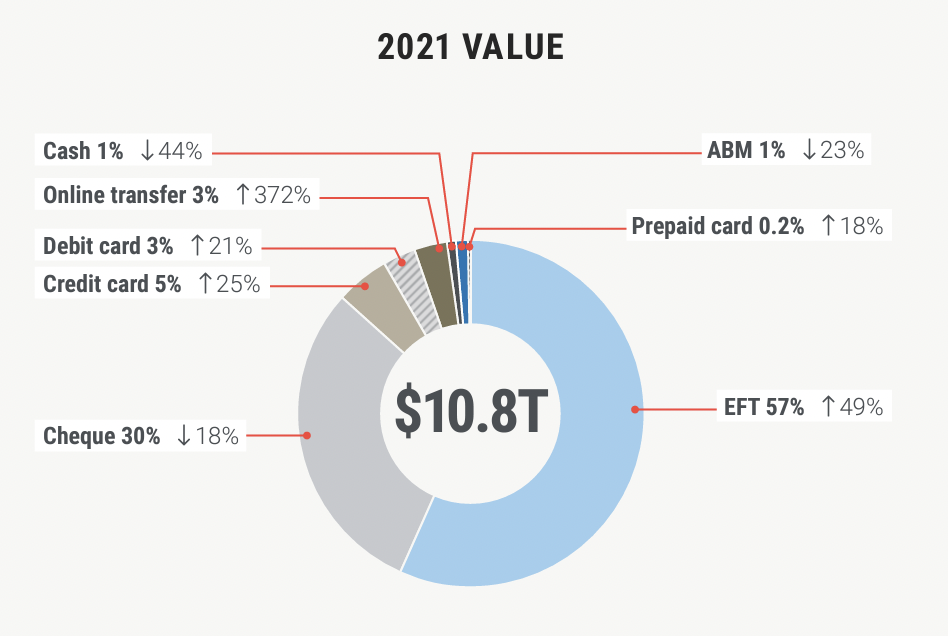

Are people well serviced? A provocative review

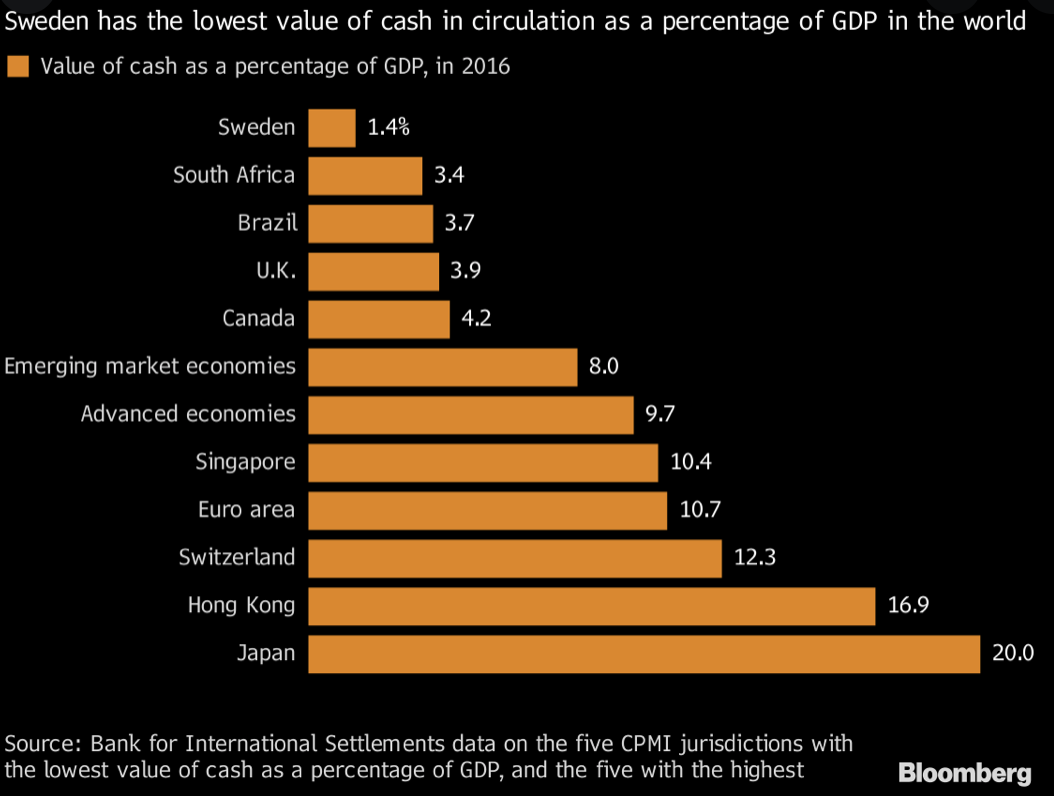

Who pays with dead trees and why?

Not who you think:

- The young: 18–34

- rent payment

- payments or gifts to other people

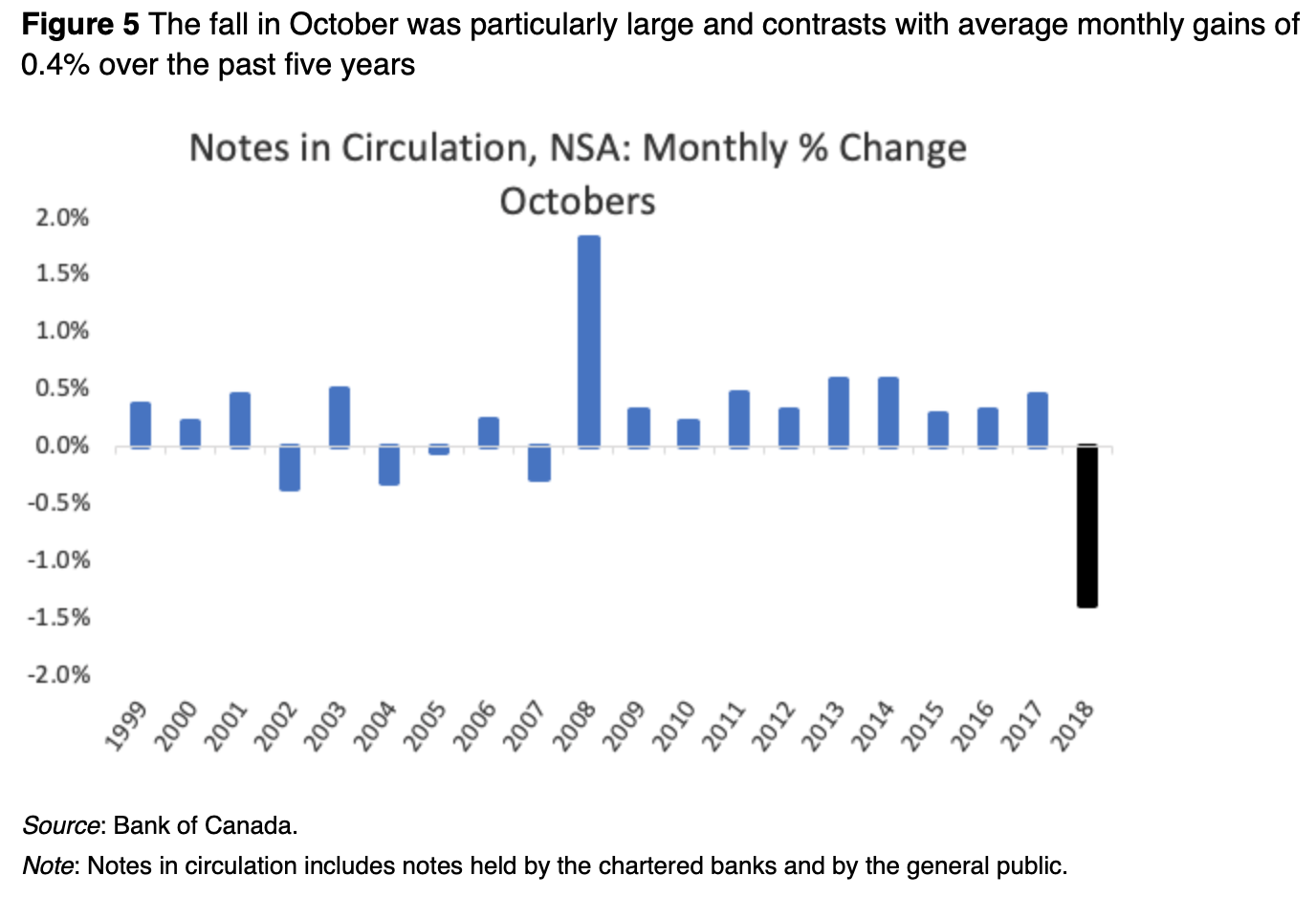

%change is for past 5 years

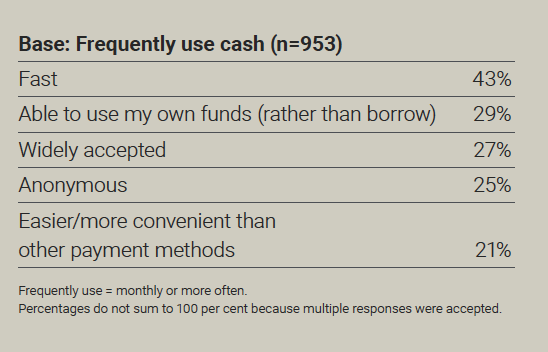

Are people well serviced? A provocative review

Why do people use cash?

- Fast 45%

- Able to use my own funds (rather than borrow) 32%

- Widely accepted 29%

- Anonymous 25%

- Easier to keep track of expenses 24%

Fun Fact: cash is probably the only day-to-day item that you have to get in-person

2020 Survey

2021 Survey

An alternative view of cash: it is still necessary

... it's just 9 steps away!

- Open banking website

- enter account number

- enter password

- enter 2FA

- navigate to e-transfer

- add contact with name and email/phone => add

- fill transfer info

- possibly add password and message

- review and send

But you can interac e-transfers!

?

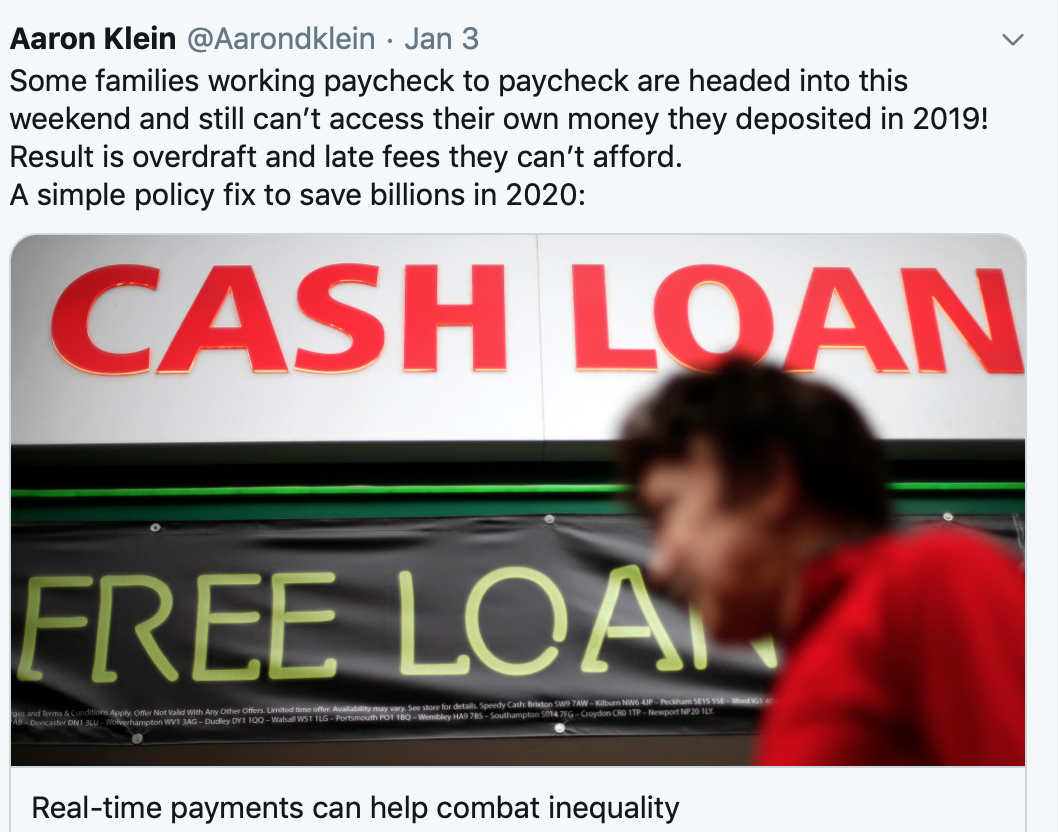

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

Speed matters

https://www.brookings.edu/opinions/real-time-payments-can-help-combat-inequality/

How is it that Amazon delivers same day but merchants receive their payment two days later?

Are people served well? U.S. data on why speed matters

- In 2015, underserved consumers spent $140.7 billion on fees and interest across five financial product categories that serve the "under-banked"

- Slow payments drives individuals to use

- high cost check cashers $2 billion

- small dollar ‘pay day’ lenders $7 billion

- bank overdraft fees $24 billion

- Not all but some of this stems from slow payments - why?

- Get paid on the 30th by cheque

- rent is due on the 1st

- cheque clears on the 2nd or 3rd

Source: Schmall & Wolkowitz (2016), Center for Financial Services Innovation (2016) "Financially Underserved Market Size Study"

A little detail the deserves attention: push vs pull

- Sue needs to provide critical information

- doesn't know when funds will be taken

- difficult to have real-time information on all obligations

- incentive for some creative intra-day "transaction re-ordering"

Pull

Push

- Sue in control of her funds at all times

- real-time information on holdings

- \(\Rightarrow\) easier to avoid accidental overdrafts

- NB: Realtime rails are typically PUSH

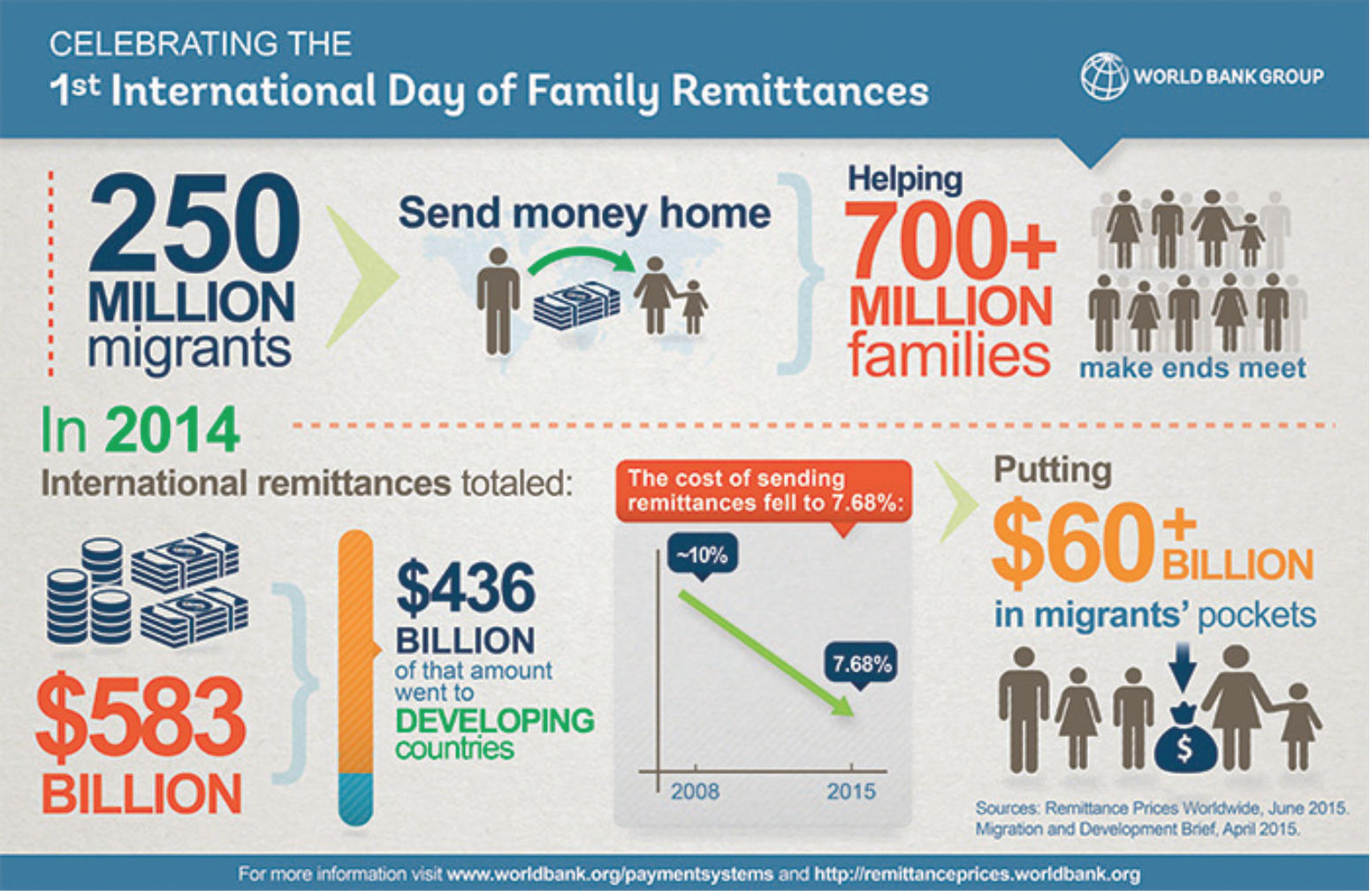

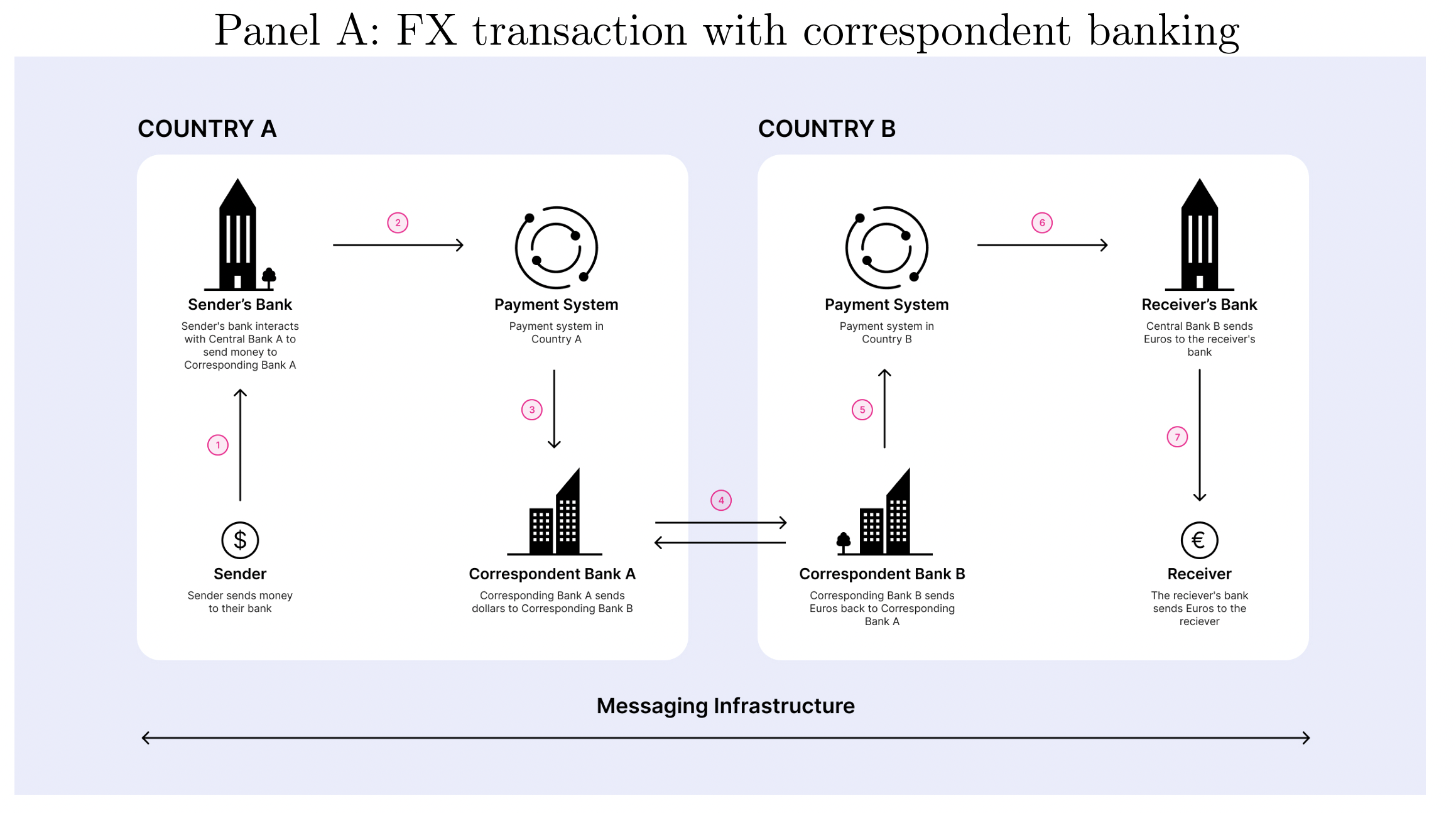

- Remittance cost estimates:

- https://remittanceprices.worldbank.org/

- Statcan report: https://www150.statcan.gc.ca/n1/pub/89-657-x/89-657-x2019007-eng.htm

- For perspective:

- fee for $200: 10.7% for bank, 9.8% for agent

- annual: \(\approx\) USD250

- for comparison:

- 1kg rice costs USD2.50

- \(\oslash\) adult consumes 120 kg rice p.a.

- assume kid consumes \(\frac{1}{2}\times\) adult

- \(\Rightarrow\) fees > annual rice for 1 kid

- Payments Canada: 15% of Canadians sent money overseas in 2020

- In 2017: $10B in remittances to East Asia and the Pacific.

- Often: new immigrants support their families at home

- Statcan: 56% use money transfer stores, only 14% use a bank. Main argument: ease of user for sender & receiver

- Most amounts are small and costs high.

Canada is a country of immigrants

- Canada has 800,000 international students

- admits around 300,000-400,000 annually

- Government of Canada: "We estimate that in 2017 and 2018 respectively, international students in Canada spent $18.4 billion and $22.3 billion on tuition, accommodation, and discretionary spending."

- Most of these funds are transferred from foreign countries to Canada in large sums.

- Students regularly get harrassed by tellers/banks about the source of their funds.

Canada is a country of international students

- To get admitted & get a visa you need to

- make a sizeable deposit

- prove that you have funds for tuition and sustaining your life

- How??? \(\to\) expensive brokers and other shady arrangements

Big Picture

Small Businesses

Consumers and Merchants

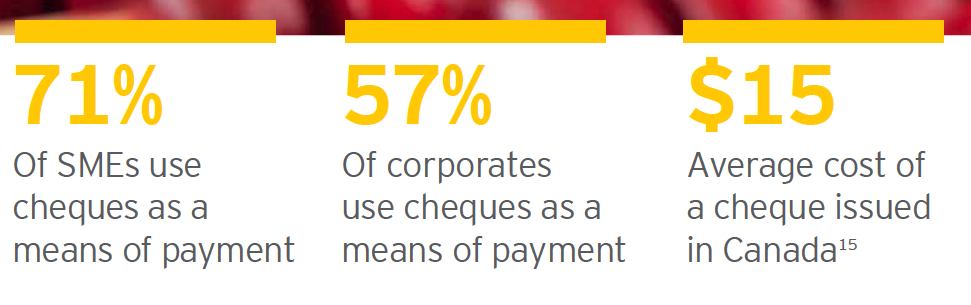

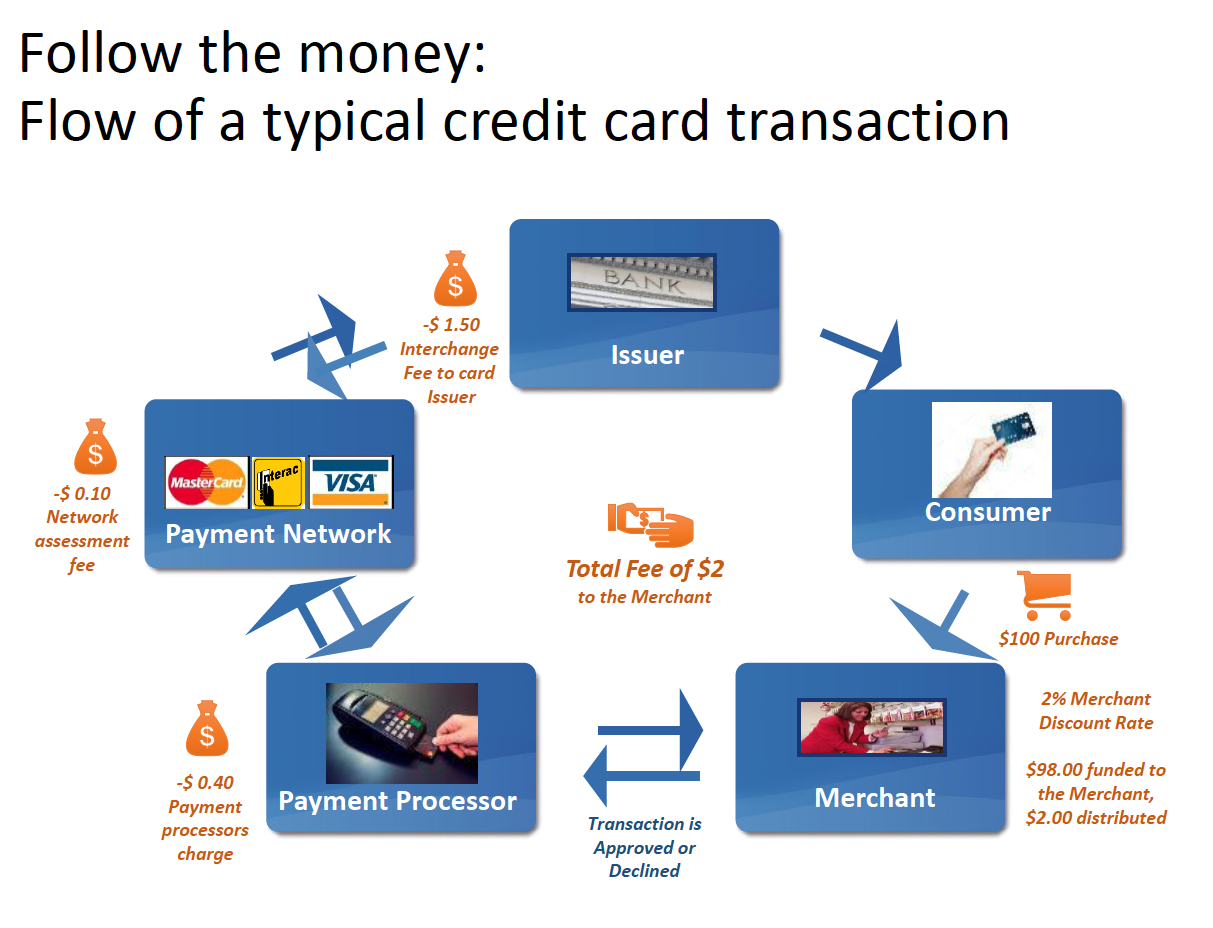

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

From Wendy Rotenberg: 734 Million Cheques for $4 Trillion

Undue Risk Aversion:

Financial institutions often won't offer payment solutions to small business, due to their credit risk profile.

B2B payments:

most financial institutions charge base fee + transaction fees

Payroll:

Need for payroll solutions for SME that are integrated with accounting systems.

Credit cards:

SMEs need to use owner's personal card which affects their personal credit score

Accounting/corporate finance

Small businesses have to integrate payment activities to accounting platforms themselves.

:$1 per transaction

Small Business Grievances: Anecdotal Evidence

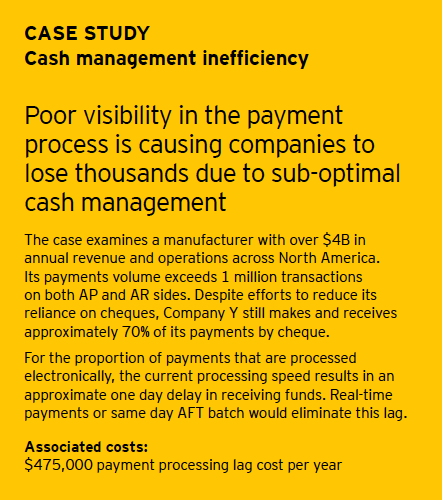

Business: Better Data and Faster Processes?

Manual/Excel-based, stand-alone cash need forecasts

\(\Rightarrow\) inadequate cash management

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

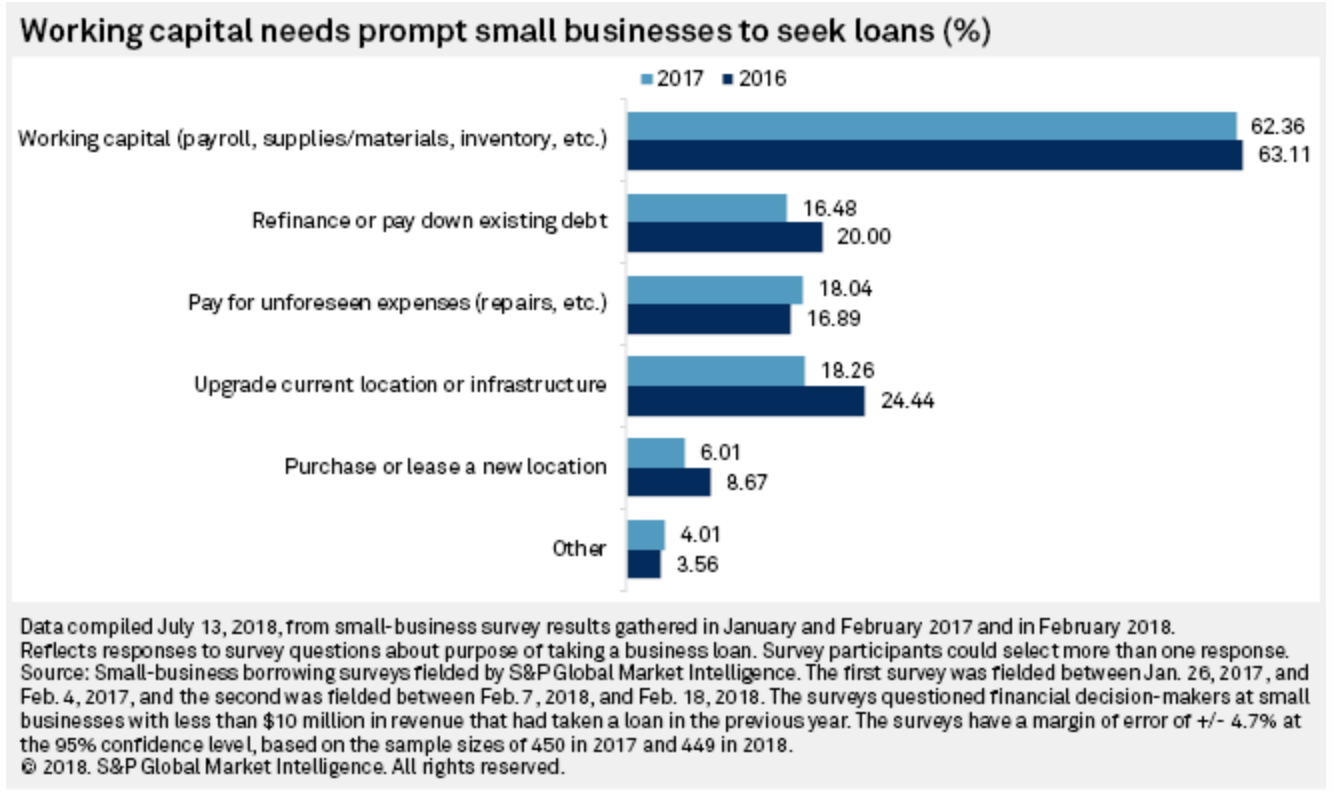

SME: why do they need the money?

Summary: sub-optimal payment processing costs Canadian businesses $2.9 to $6.5 billion annually

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

So: Where are we?

We're not there yet ...

Can we get there with FinTech and PayTech?

Can innovation get us there?

gig economy instant pay

fast vendor payment and B2B & inter-company real time payments

PayTech firms fill the void within their platforms

What are the risks for customers?

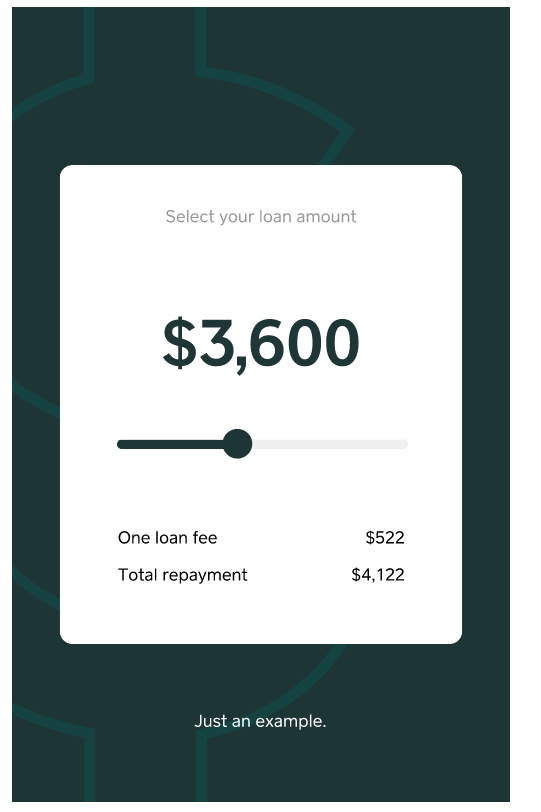

Examples of PayTechs

-

credit card issuer

-

easy reward point redemption

-

in-app loan application

-

buy now pay later

-

Pitch: $16 billion of rewards left unredeemed each year by Canadians.

-

Why? Cumbersome, not relevant or have been devalued.

-

With Brim, points accrue at market fare because user purchase first and then redeem rewards. No redeeming at a marked-up value. The platform makes earning and redeeming simple.

Examples of PayTechs

-

enable businesses to make deposits in real-time directly to an account in seconds, not days

-

payments usually take 4-5 days

-

Companies such as Borrowell provide on-demand loans for businesses and consumers. Without Pungle, businesses that need cash instantly, whether to settle up with a supplier or pay for an unexpected expense, must wait several days to receive the money.

-

Gig economy: employees expect to be paid instantaneously or at shift-end. We’ve found that the more frequent payment of wages has had a direct correlation with lower turnover.

Will interac for business

solve all these issues?

Innovations in Non-physical Payments around the world

Danish Mobile Pay

4+ million users (population 5.7M)

235+ million transactions, 8.6Bn EUR value

launched by Danske Bank, but bank-neutral

instant payments based on mobile phone numbers

Critical component: "digital" ID

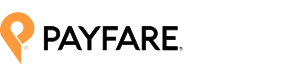

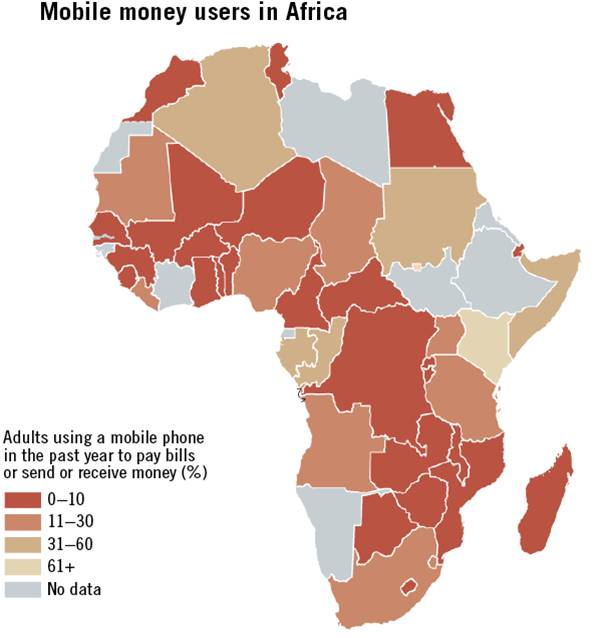

Mobile Money in the Developing World

Mobile Payment

Mobile Money

Cash-In

agent

Cash-Out

agent

Mobile Apps in Emerging Economies

and almost every other 905 tourist mall

- 900M WeChat Pay Users

- 84% market penetration

Mobile Apps in Emerging Economies

These apps offer more financial services than payment

Real Time Retail Payments in Emerging Economies

- launched in Nov 2020

- 365/7/24 system

- Process:

- user generates a PIX key through its bank stored in central database DCIT.

- Key=address on PIX network added on top of the existing bank account

- Oliver Wyman prediction:

- 22% of electronic payments by 2030

-

reality:

- 72% of electronic transactions in Oct 2021

- uptake: 62% of Brazilian population

Key institutional facts

- forced development by central bank to improve competition in payments

- built time: 9 months

- cost: $5M

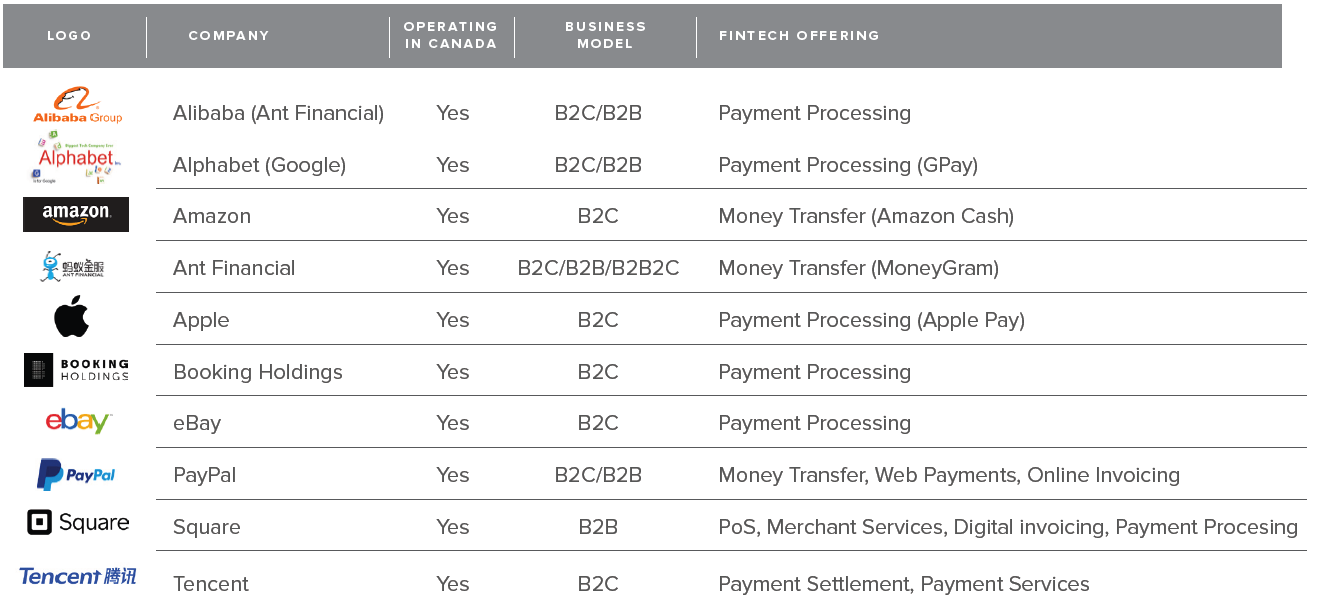

The Threat of Big Tech

Innovations by BigTech

BigTechs operating as FinTechs in Canada

New frontier: revenue-based lending

14.5% interest - over what horizon?

Government Intervention

Basic Idea: Allow external party access to your bank account information

\(\Rightarrow\) information/data sharing

Future Services

-

360-degree analysis

-

transfers among various accounts

-

product integration and linking

-

payment initiation

-

linking of reward services

-

immediate credit assessment

Current FinTech solution: data scraping

may require legal & technological changes

Open banking - what is it?

Open banking - learning from the UK

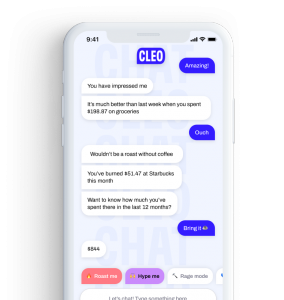

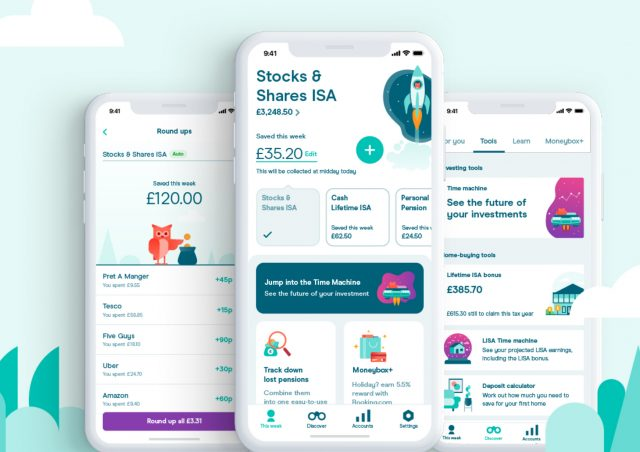

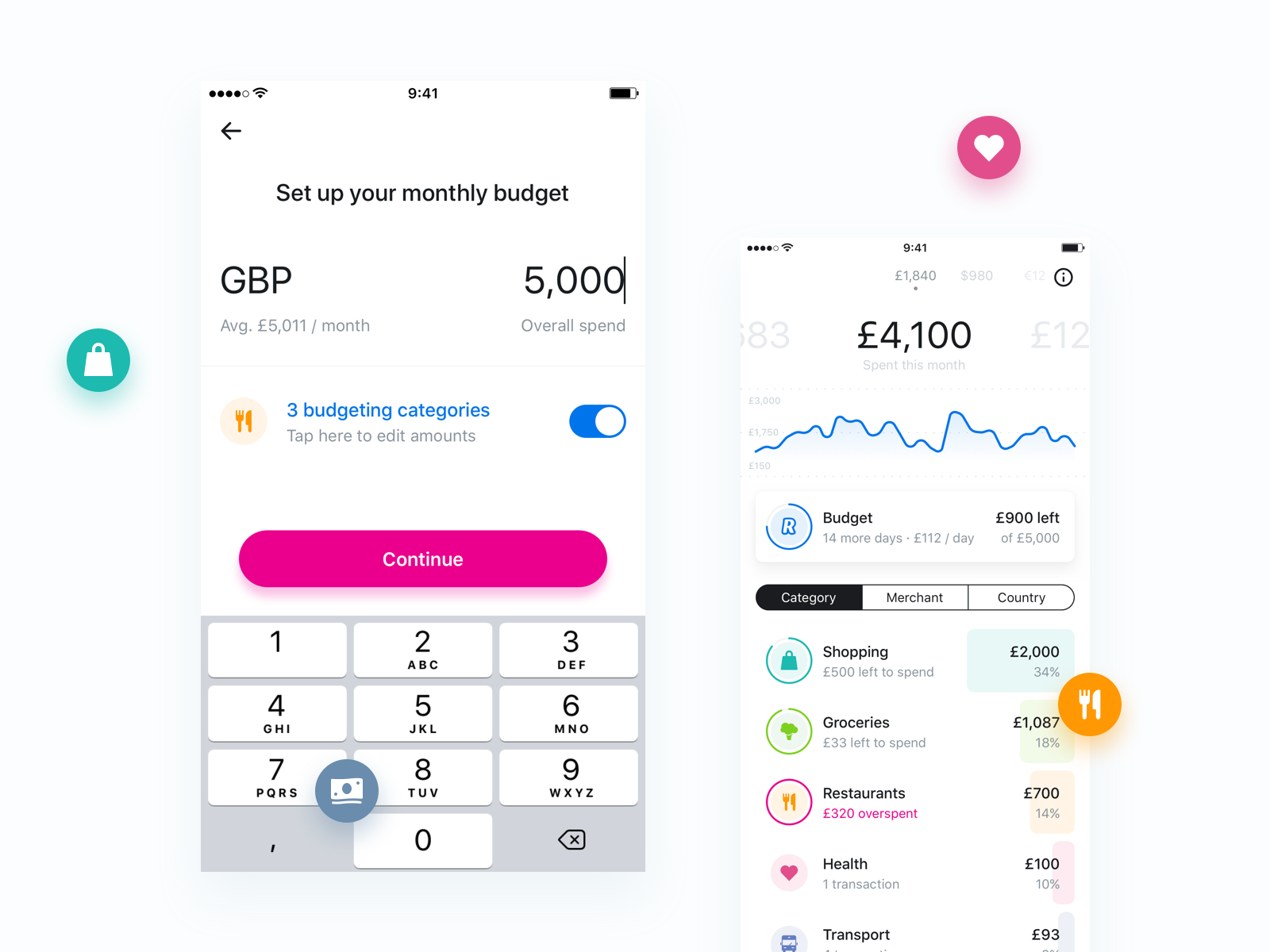

AI chatbot that chides you if you overspend and that advises you if an expense fits your budget

allows you to redesign your salary pay structure (make monthly weekly etc)

get alerts for suspicious transactions of elderly parents

Moneybox

aggregates all your banking related services

- advanced budgeting and planning

- manage all subscriptions and bills

What do people in Canada think?

59% only trust their bank with their financial data.

75% are not interested in open banking

91% worry about the privacy

Source: Accenture Consulting Open Banking in Canada: Opportunity Knocks

71% say their concerns can be addressed with technology

20-30% would share significant personal information with a non-bank in exchange for better pricing on products and services.

End of Part 1 survey

please navigate again to

End of Part 1 debate

Discussion topic: "Canadian Banks are well-positioned to serve its customers '(consumers and businesses) payments needs"

Setup: Random sorting into TWO groups

- Group 1: Agrees and defends this statement with this statement.

- Group 2: Disagrees

Format

- Each group presents its arguments (3 min each)

- Each group presents a rebuttal (1 min each)

- Vote on who had the better argument.

Your task for the next 10 minutes

- prepare your arguments and rebutals of the arguments that you think the other side will present

Part 2

Innovation OUTSIDE the current institutional arrangements

Outside Force #1: Decentralized Finance

What is a Cryptocurrency?

Conceptually: What is a Blockchain?

payments

stocks, bonds, and options

swaps, CDS, MBS, CDOs

insurance contracts

A blockchain is a

- general purpose

- open access

- value management

- infrastructure

- that is communally run

What makes DeFi different from TradFi

decentralized finance =

provision of financial service functionality without the necessary involvement of a traditional financial intermediary like a bank or broker-dealer*

digital media =

provision of information service functionality without the necessary involvement of a traditional information intermediary like a publisher, library, or newagency

*my take: applies to only commoditizable services

trading Infrastructure

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

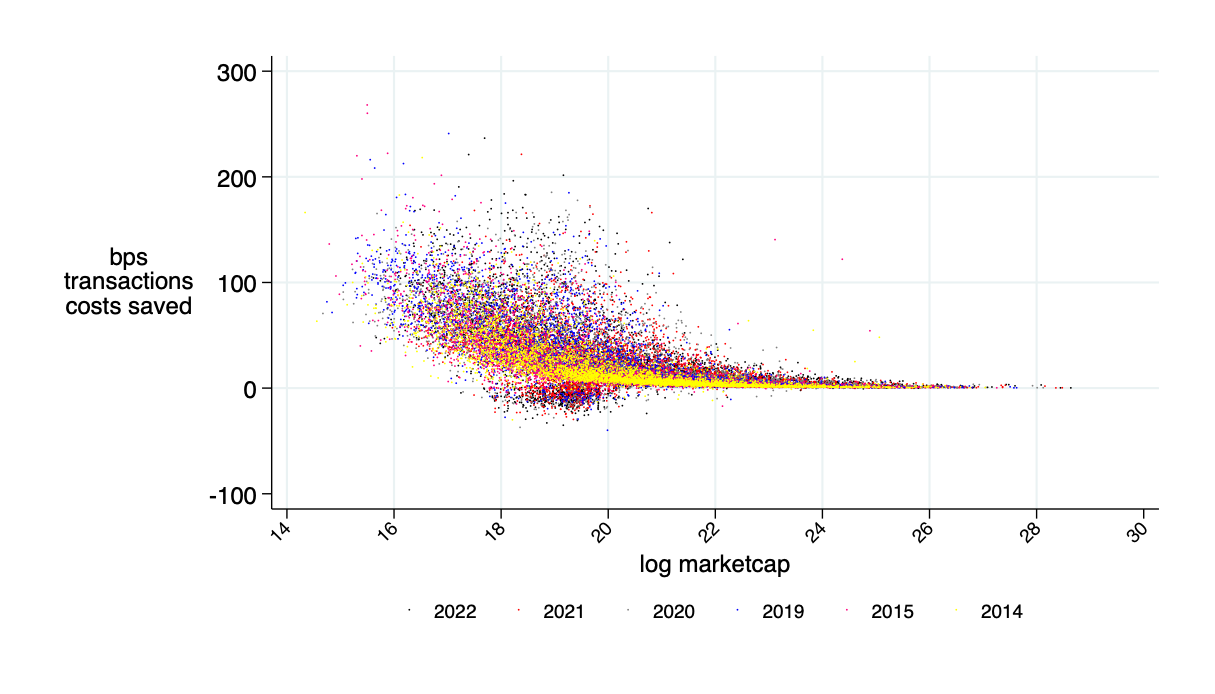

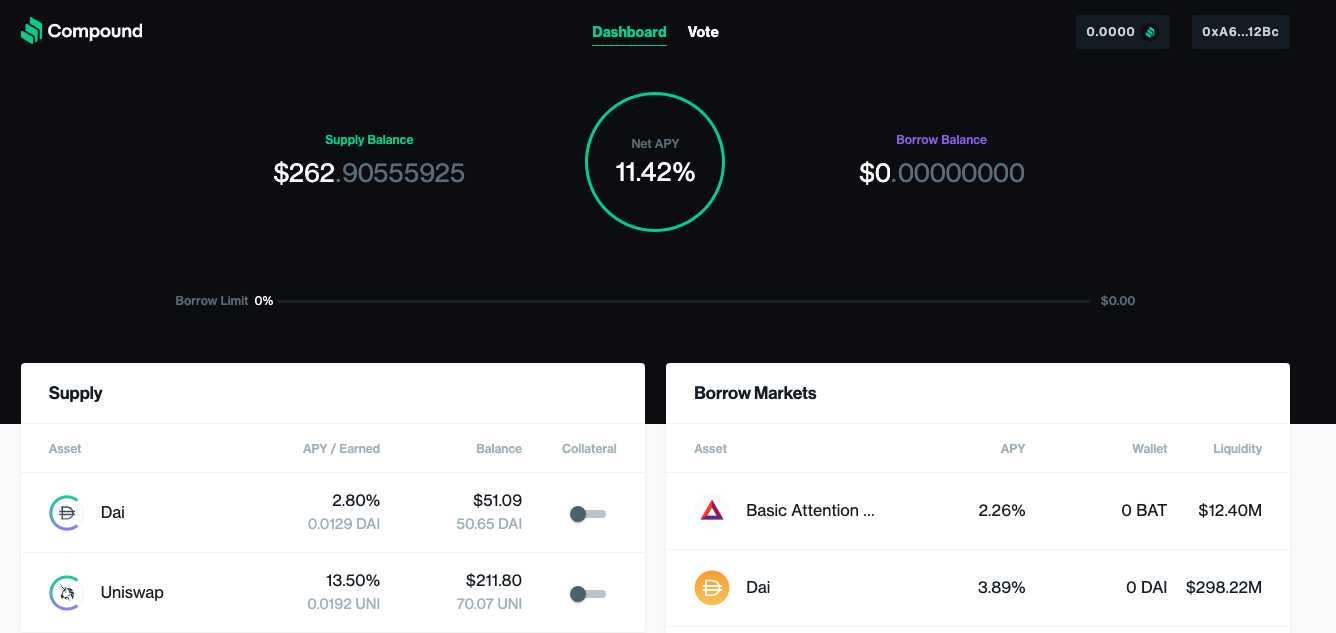

Application: decentralized trading with automated market makers

Source of savings:

- better risk sharing among liquidity providers

- better use of capital

Possible transaction cost savings: \(\approx\) 30%

Source: "Learning from DeFi: Would Automated Market Makers Improve Equity Trading?" working paper, Malinova & Park 2023

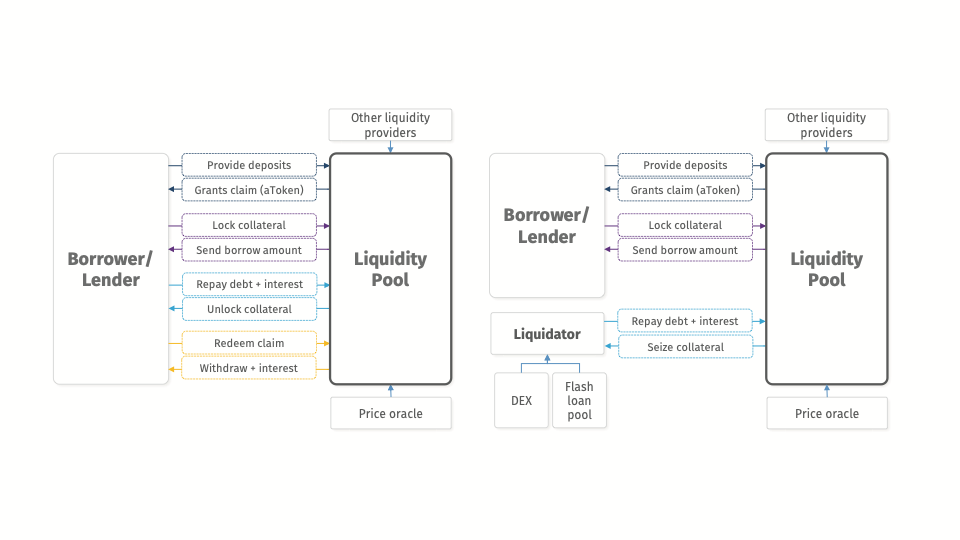

Application: Decentralized Borrowing & Lending

borrow

provide collateral

The Flow of Event: Normal Times

The Flow of Event: Collateral Liquidation

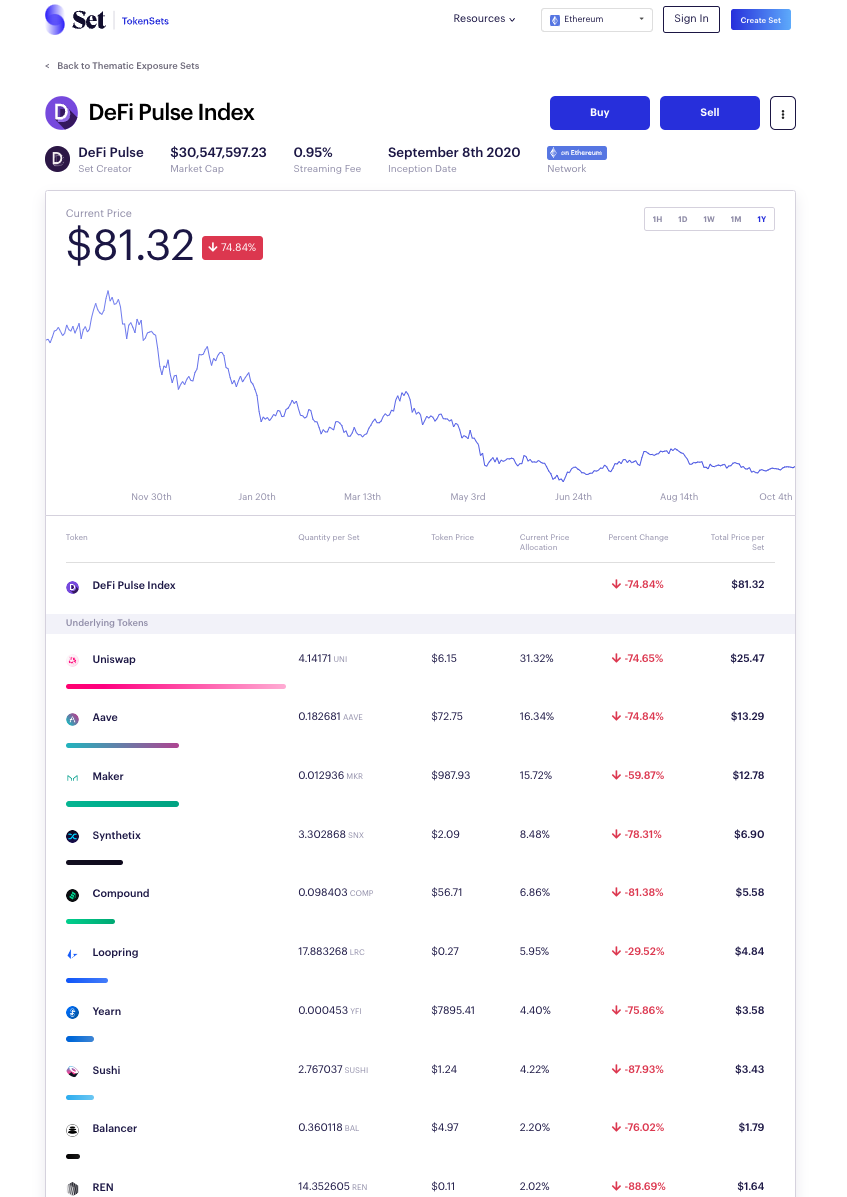

Obvious Smart Contract Application: Automate Investment Strategies

idea: create new mutual fund like asset

"yield aggregator:" push capital where rate of return is highest

Peer-to-peer \(\Rightarrow\) Platforms

liquidity \(\nearrow\)

volume \(\nearrow\)

protocol fees \(\nearrow\)

token value \(\nearrow\)

Platform economics is tricky:

- What's the product?

- How do you get it started?

- How do you get people to contribute?

- How do you earn money?

it works!

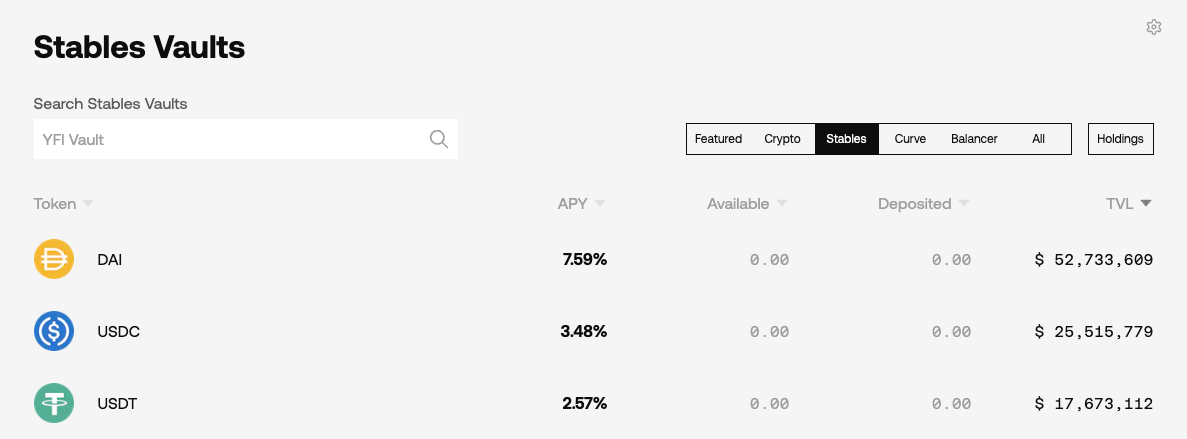

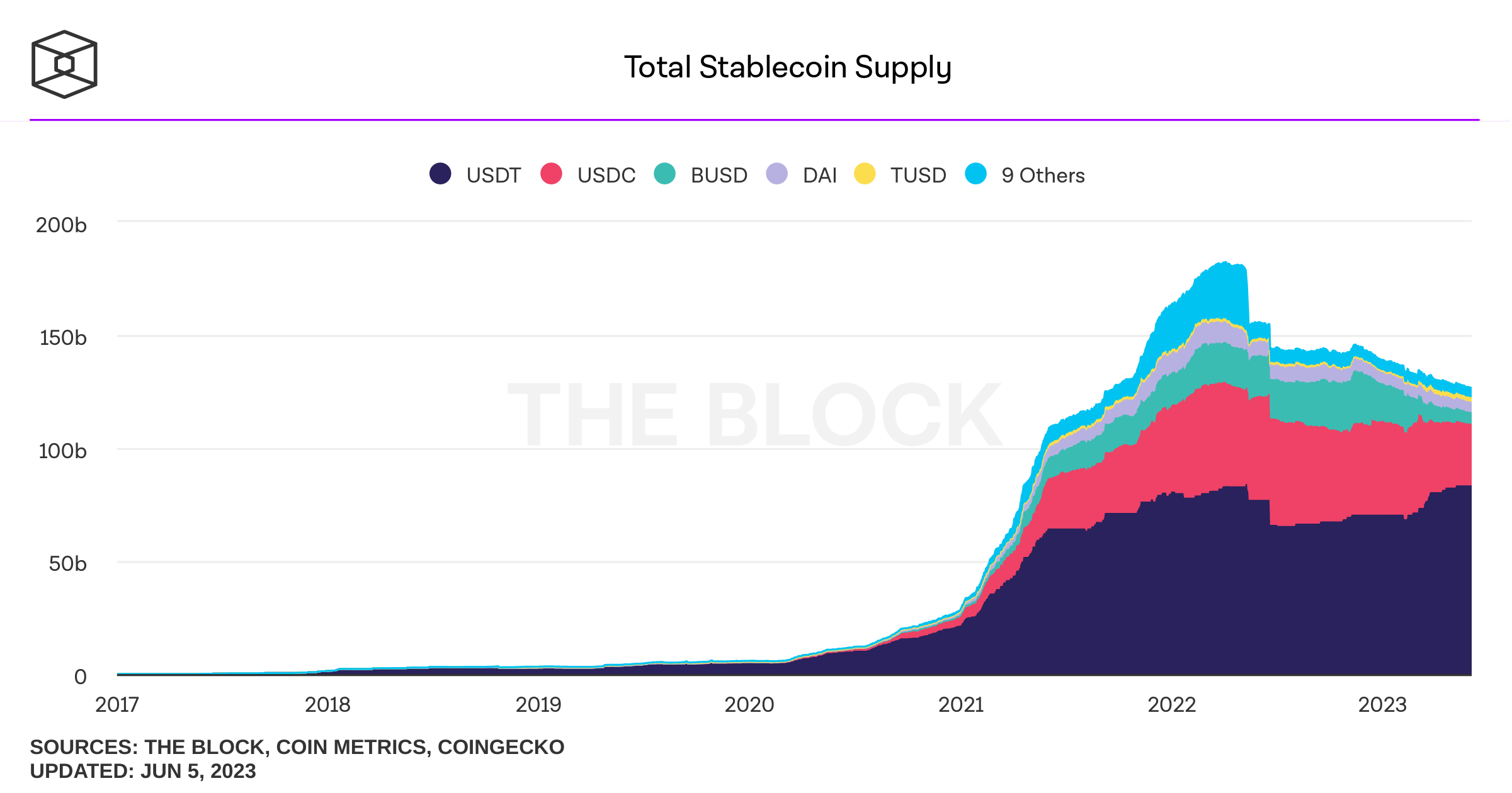

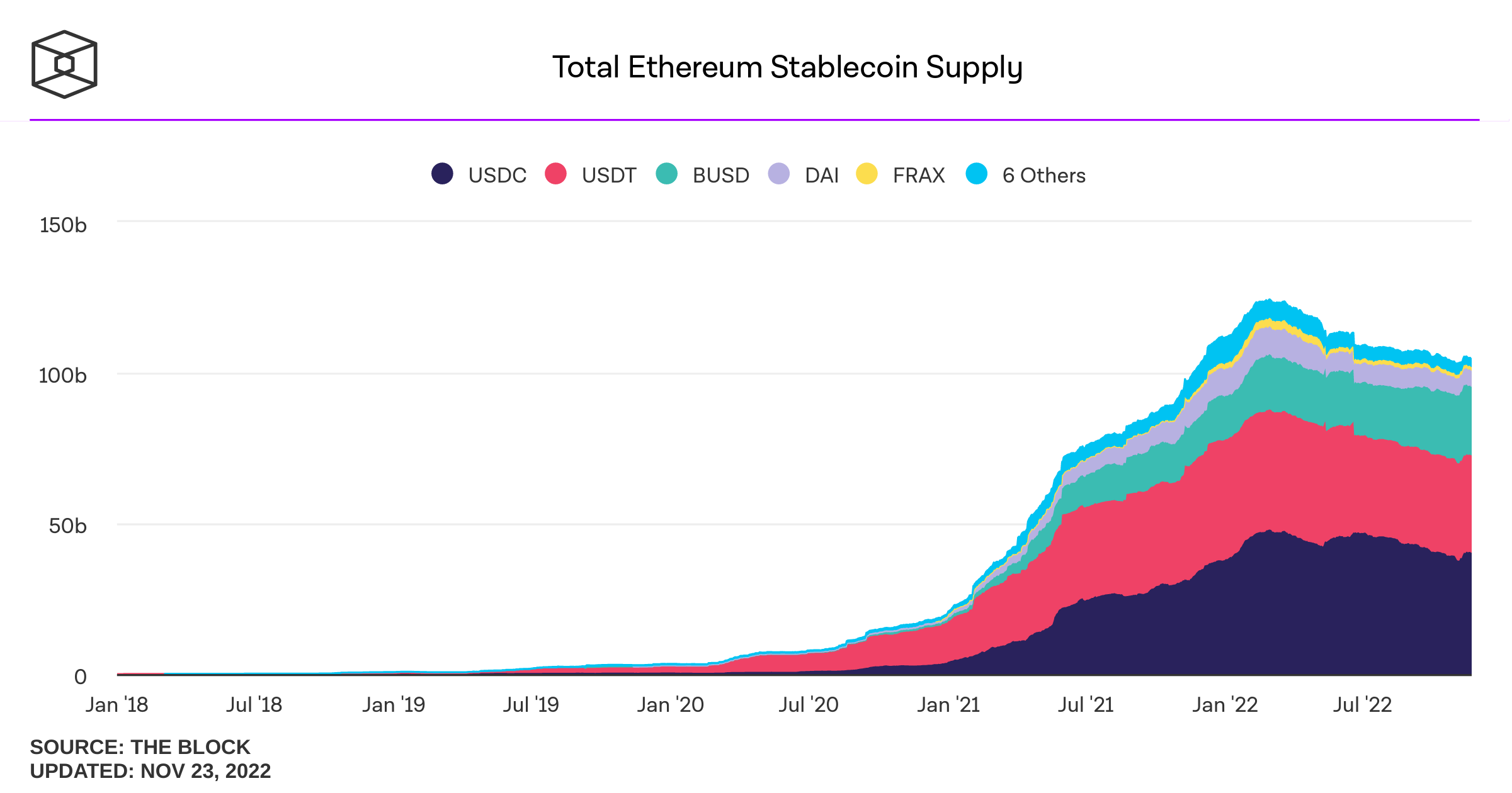

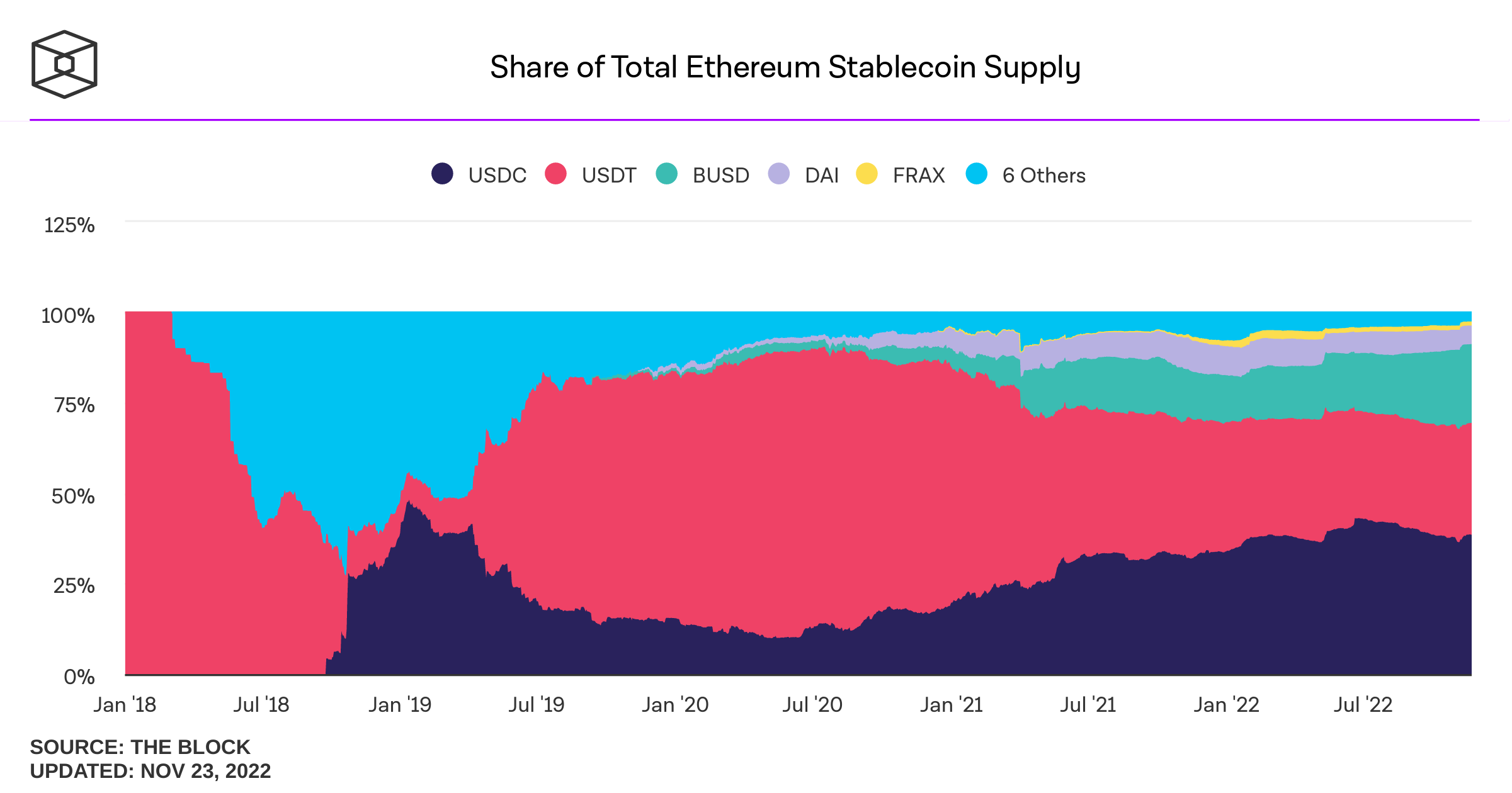

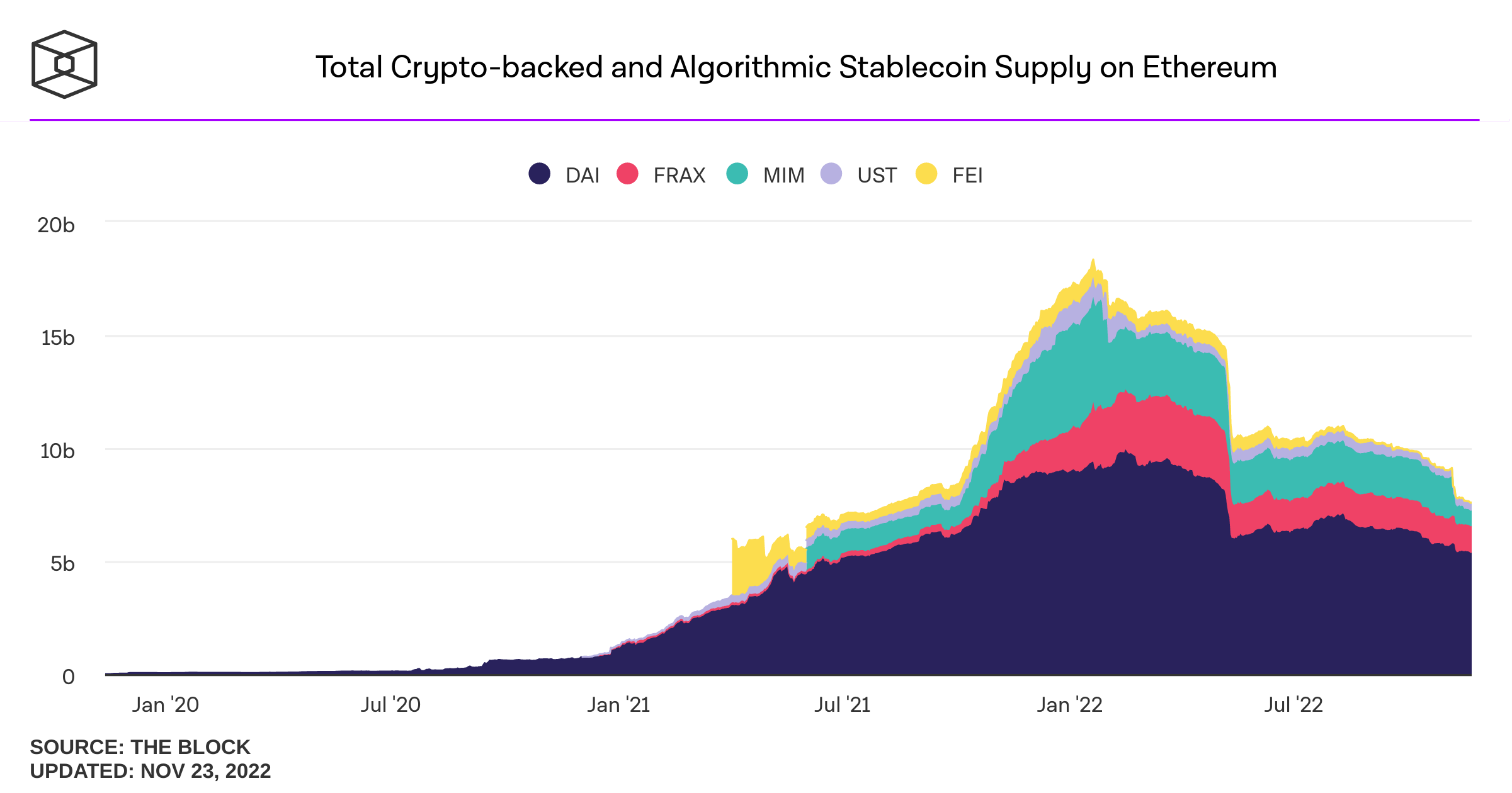

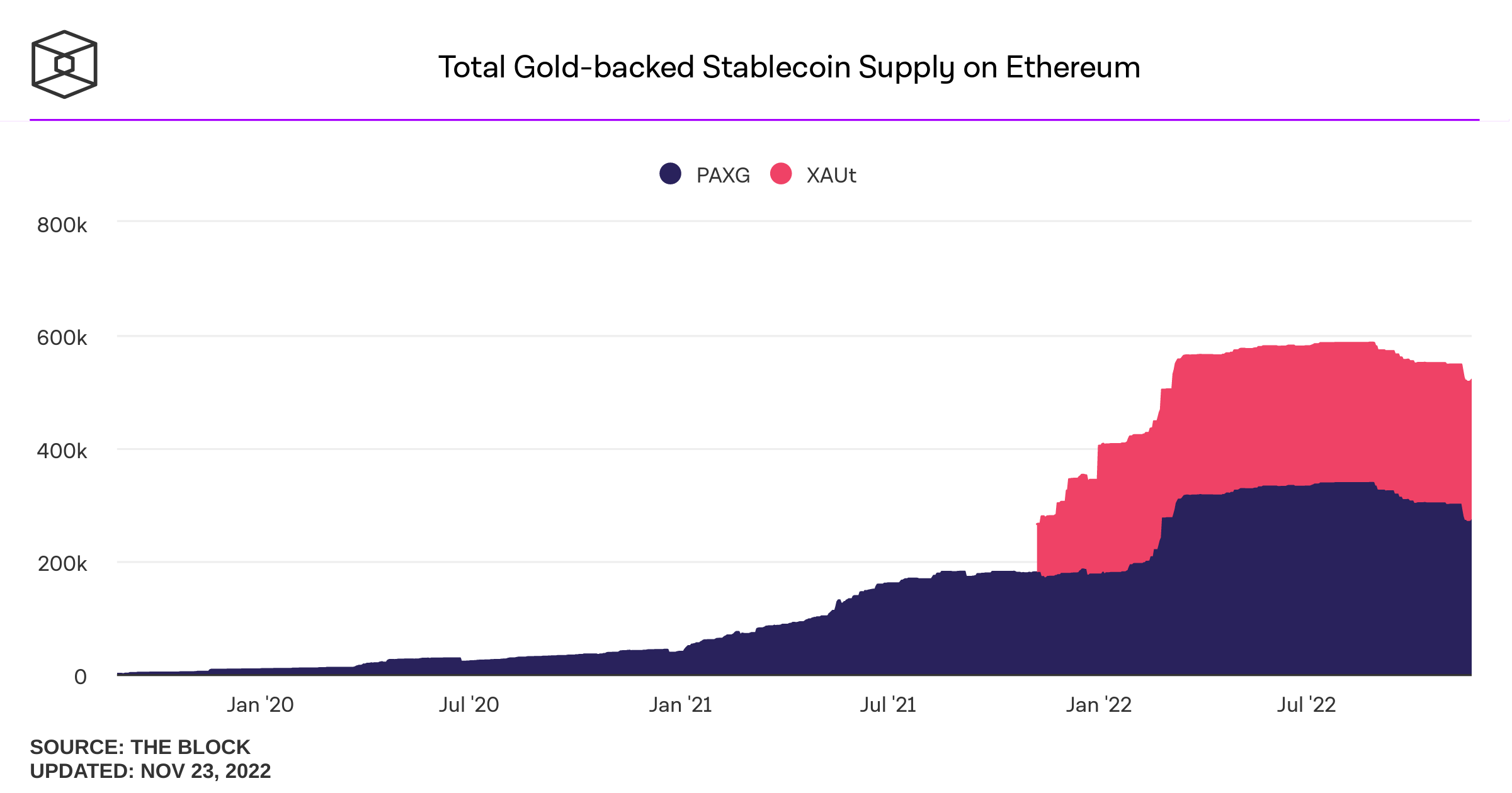

Stablecoins

BTC, ETH

fiat: USD, EUR

asset (gold)

fee-backed

Seigniorage

Crypto

Traditional

Algorithmic

Collateral-Backed

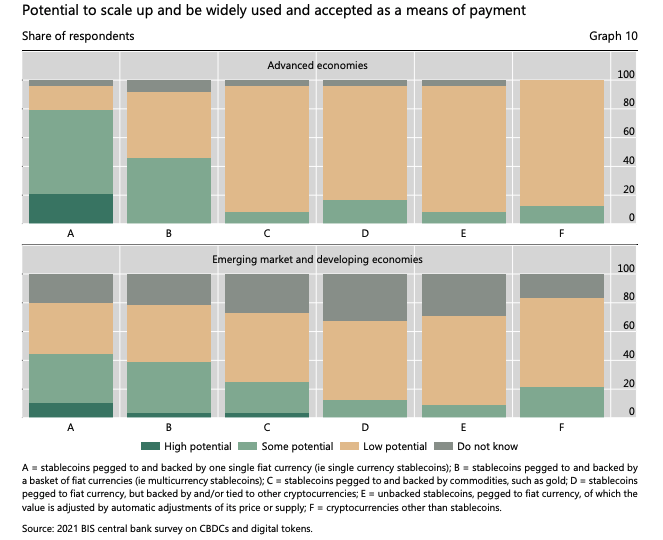

Taxonomy of Stablecoins

Stablecoins: Digital Representations of the USD

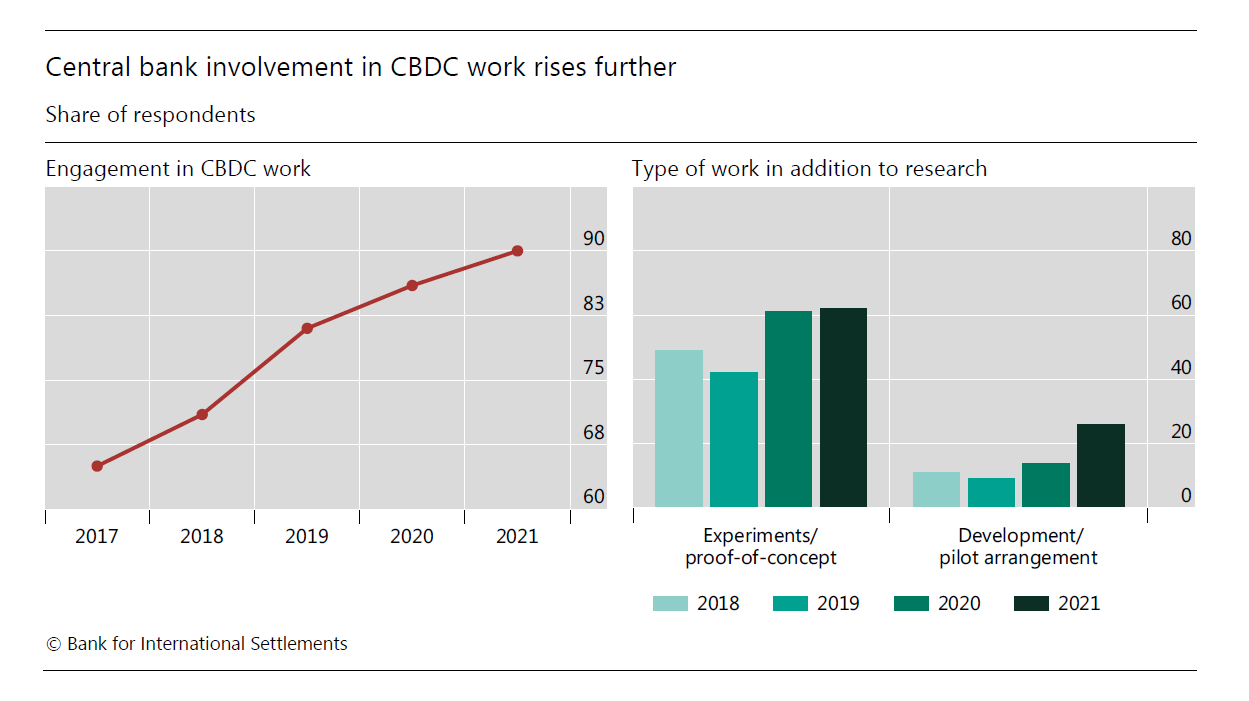

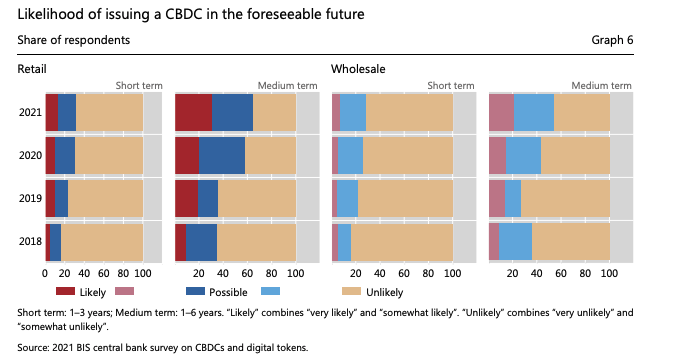

BIS Survey of Central Banks:

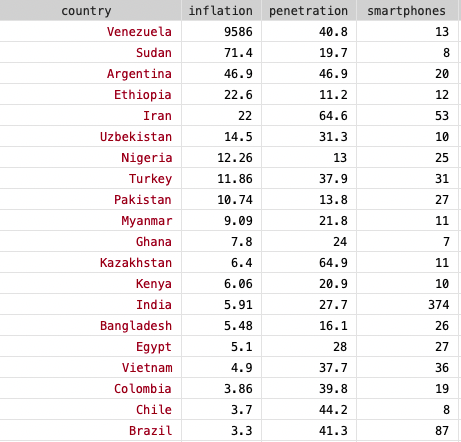

Some data

cellphone data from 2018 (NewZoo), inflation from 2020 (World Population Review)

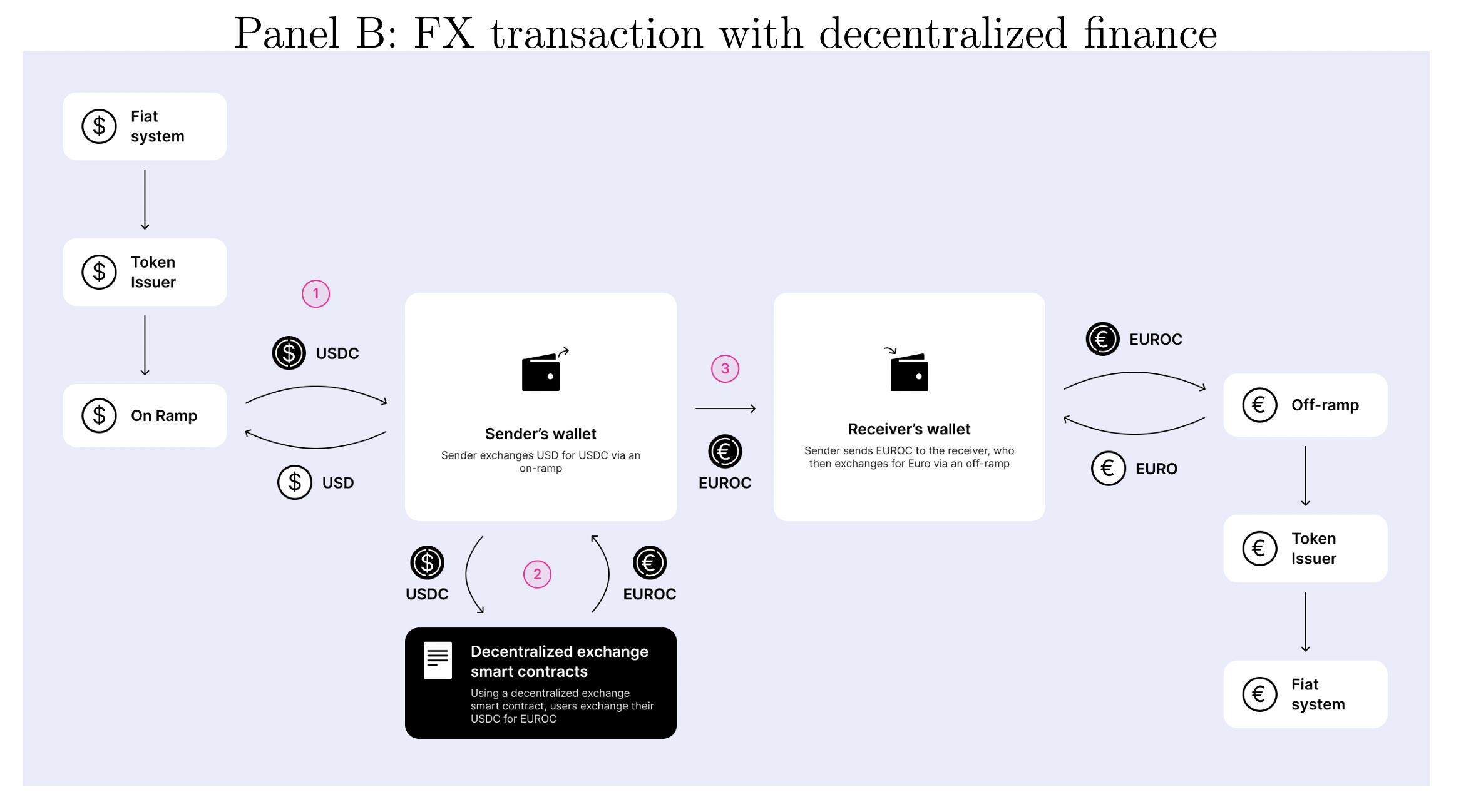

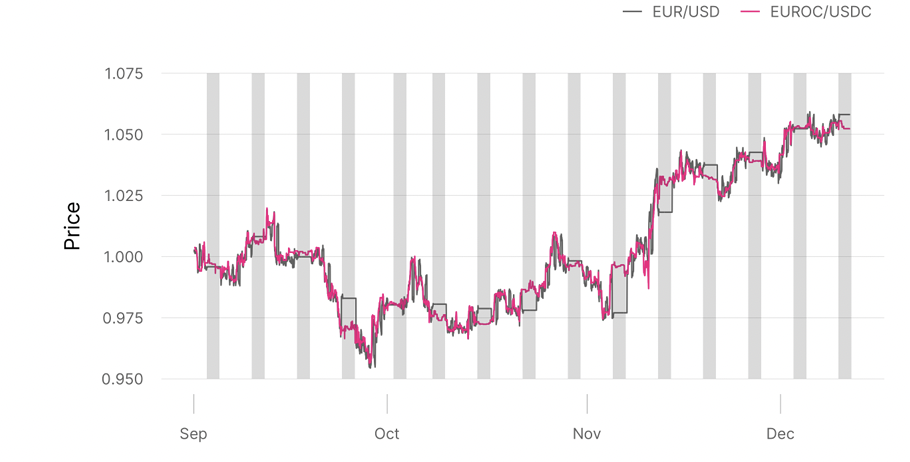

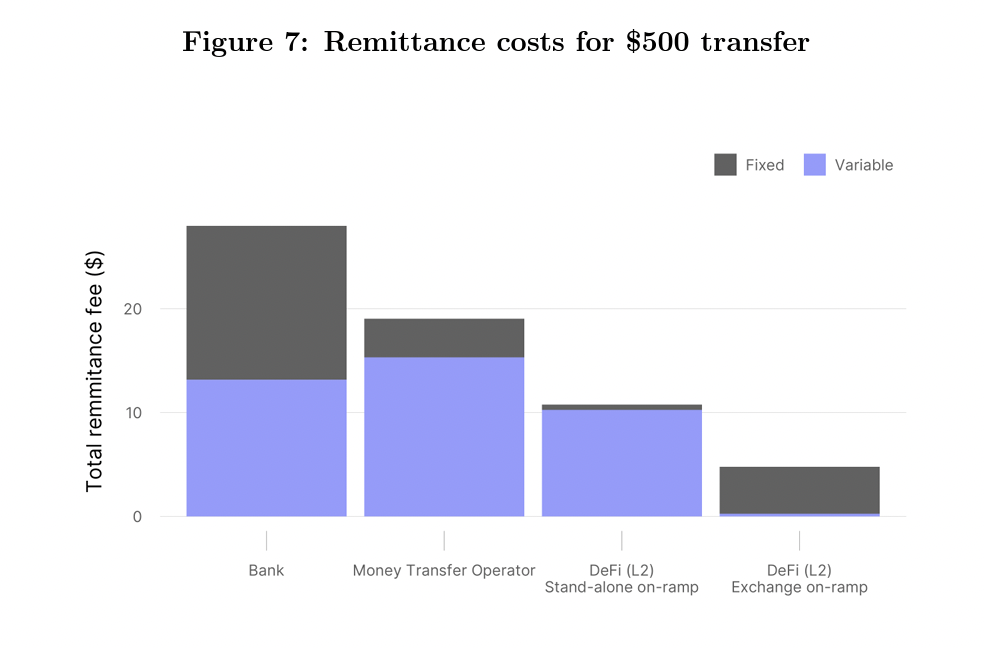

Source: On-chain Foreign Exchange and Cross-border Payments by Austin Adams, Mary-Catherine Lader, Gordon Liao, David Puth, Xin Wan (2023) [team from UniSwap Labs]

DeFi fees:

- fiat to crypto on ramp: 0%-1%

- exchange fees 1-5bps

- network fee: $0.001-5$

- off-ramp fee: 0%-1%

- total: from close to 0 to 2%+$5

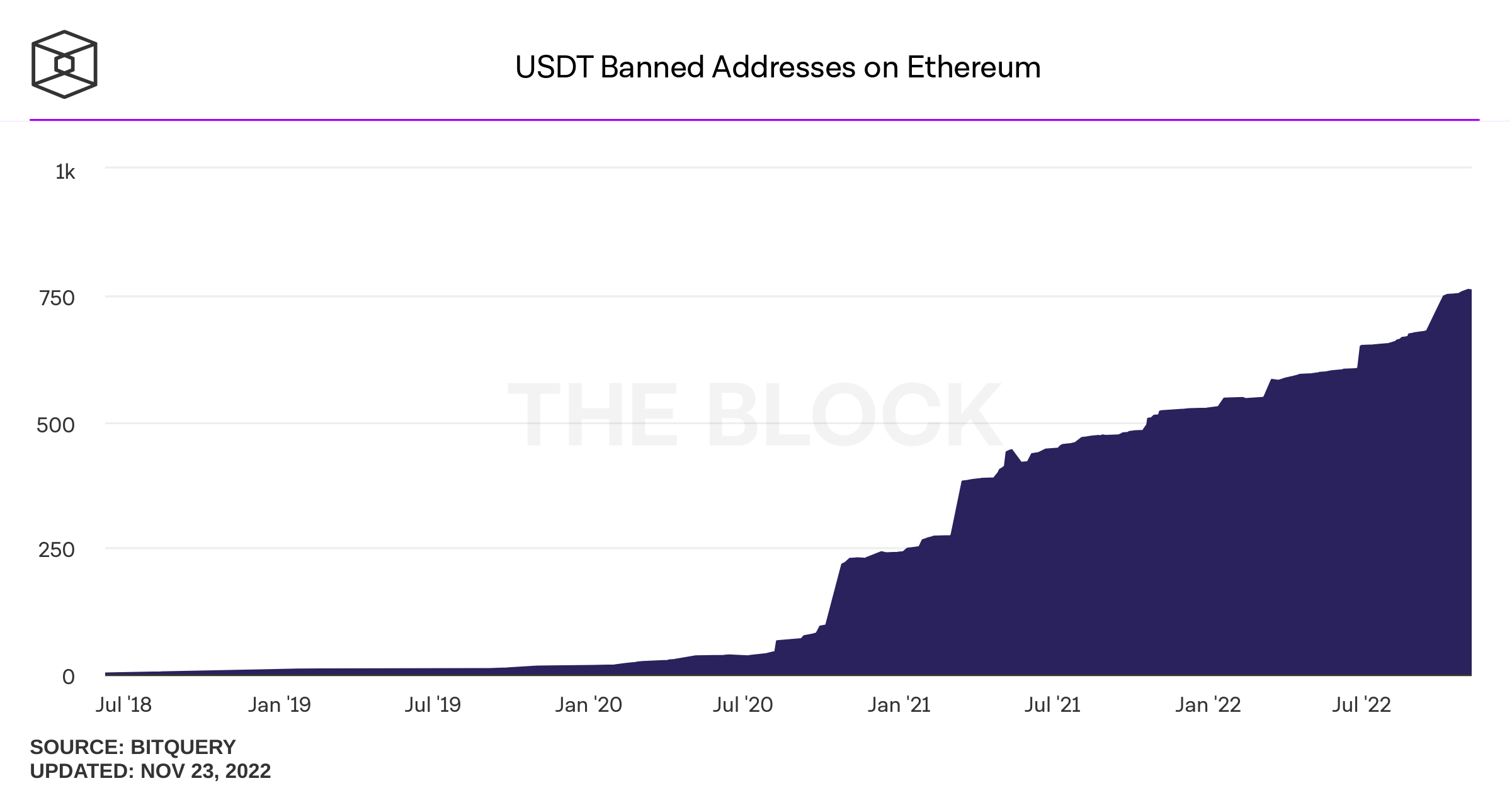

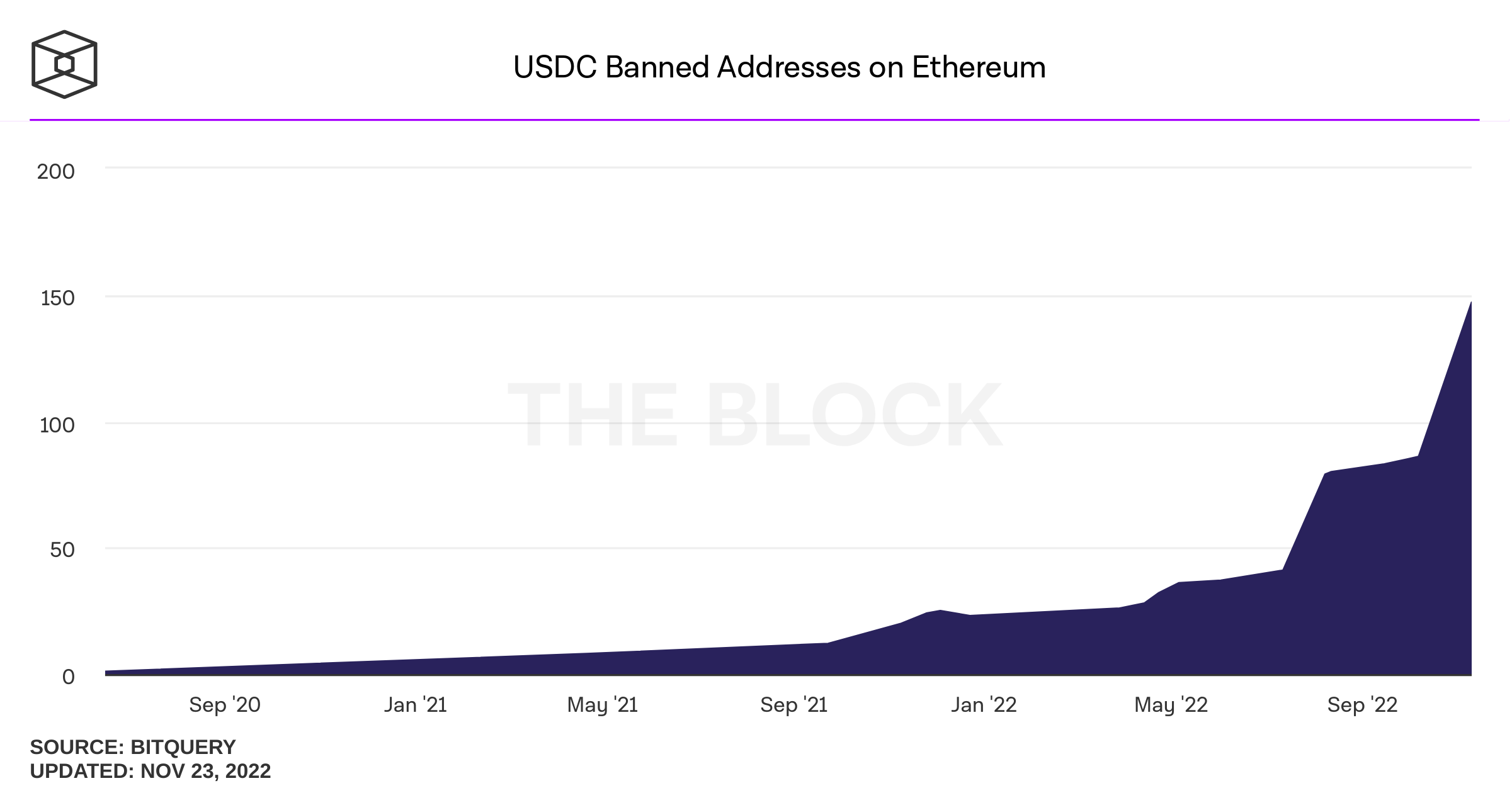

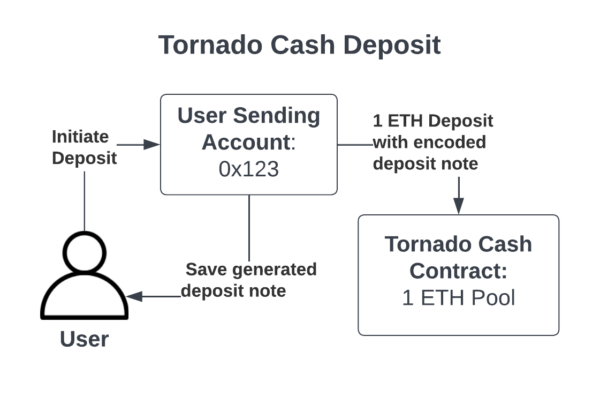

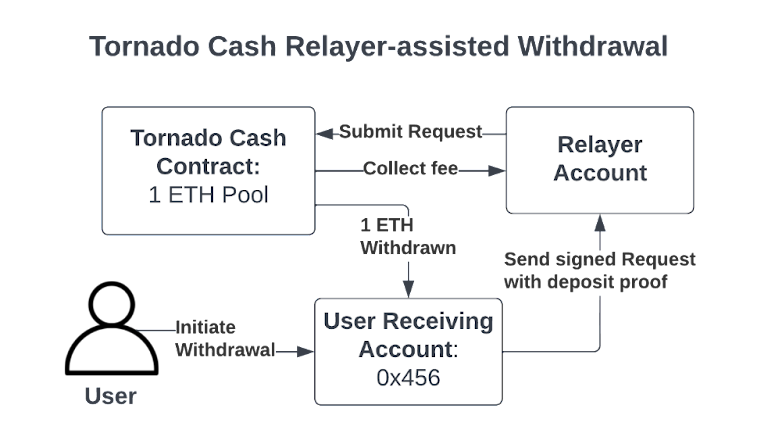

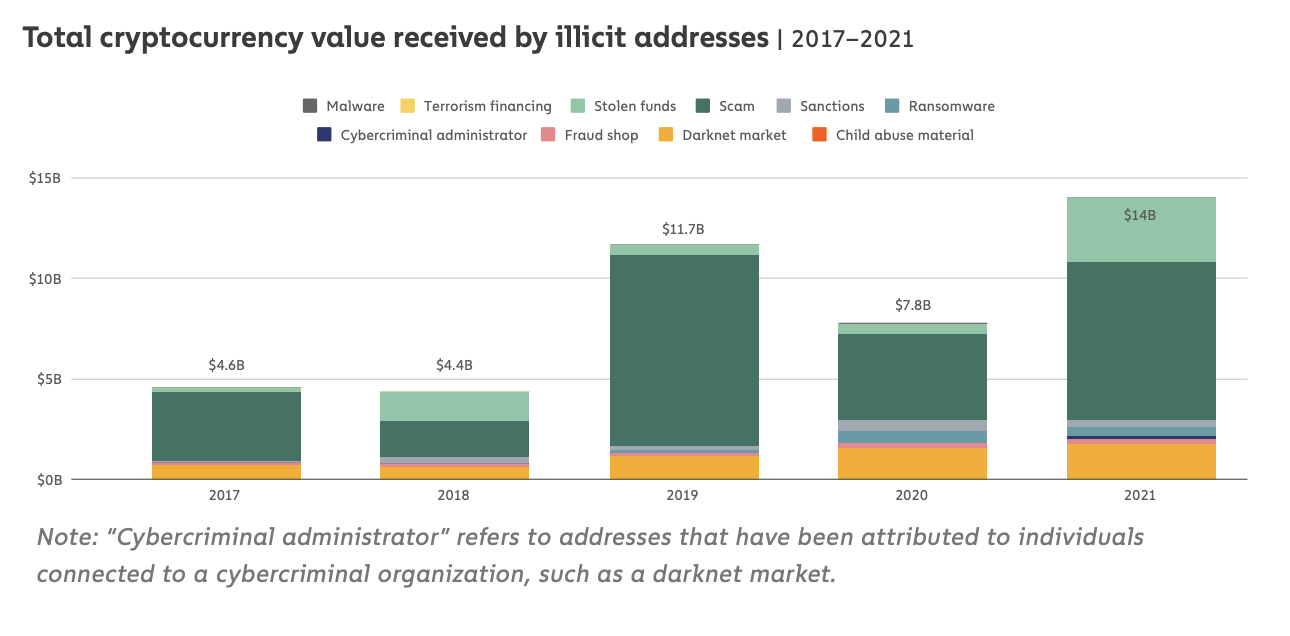

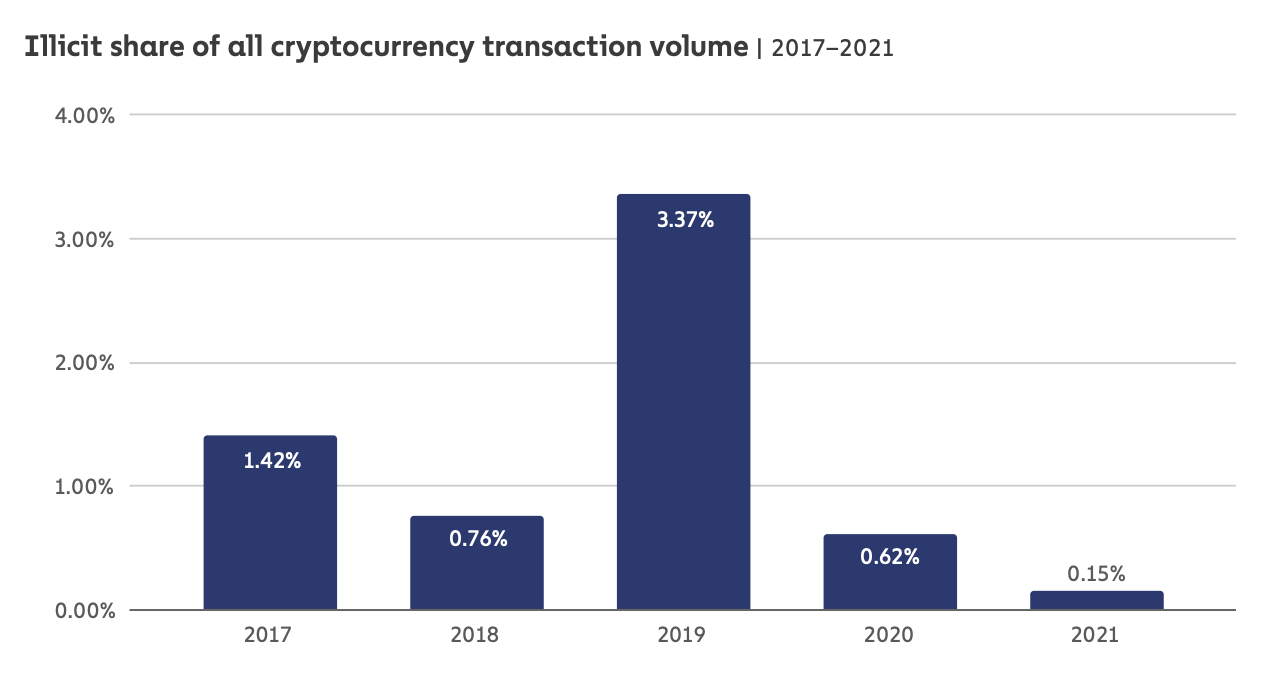

Money Laundering and Crime

Banned addresses

Tornado cash

Chainalysis Crime Report

extra info:

- 2019: PlusToken Ponzi scheme

- numbers depend on known addresses, e.g., 2021 report listed ~.3% for 2020 and upped to .65 now

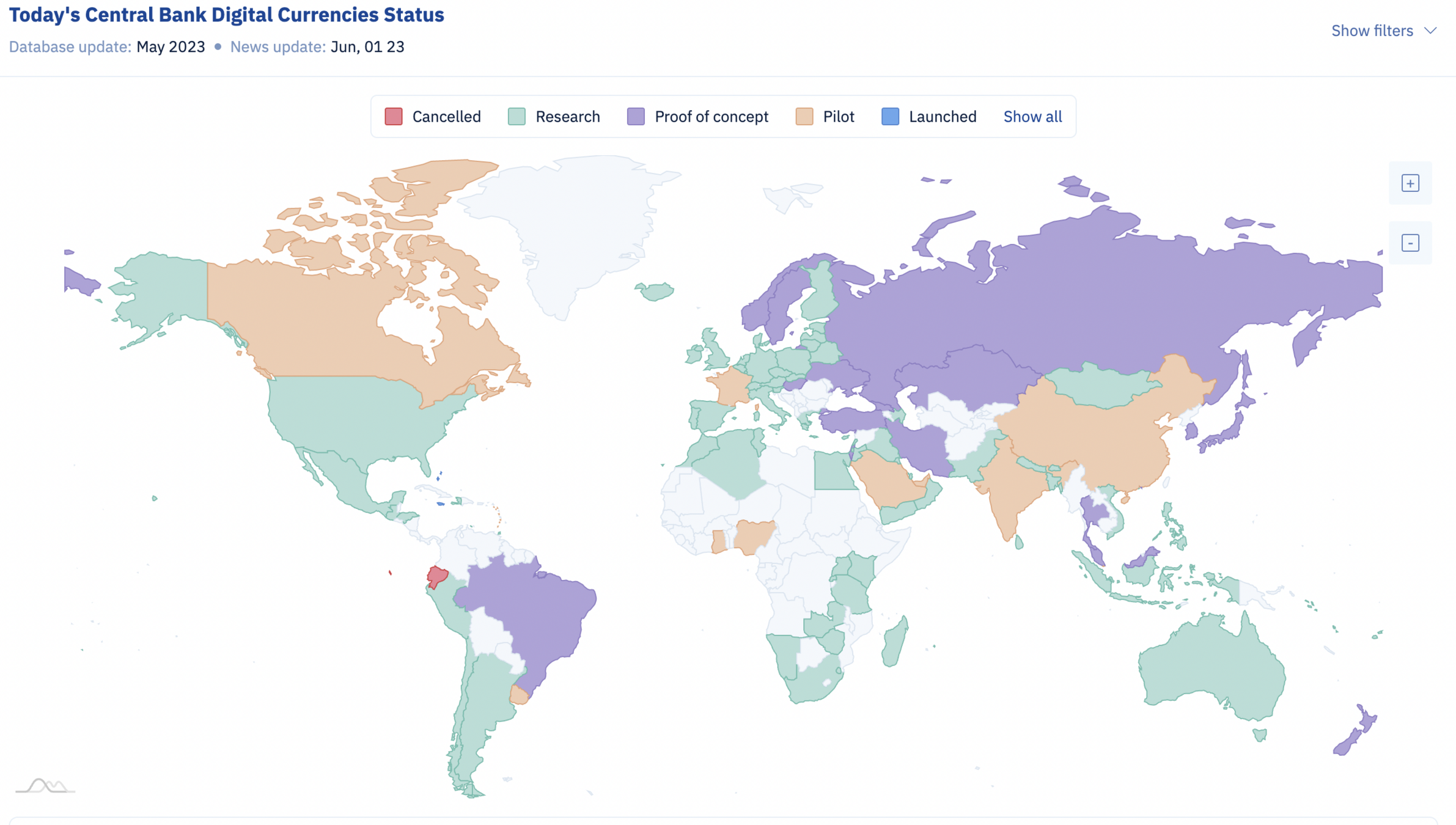

Outside Force #2:

Central Bank-Issued Digital Currencies

Evolution

(now defunct)

CBDCs are on their way

Chrystia Freeland Justin Trudeau

of all things crypto and digital in Canada

A CBDC in Canada ... ?

What has happened in the CBDC space in the past 12 months?

- Canada related:

- Bank of Canada research: works with MIT

- Toronto Star article for DoF: "significant impact for financial sector"

- BIS Innovation Hub Toronto for North American CBDC work, Ripple Labs in TO

- Budget 2022: $17M to DoF/BoC for CBDC work over 4 years

- Worldwide (incomplete list)

- US: Executive order to study intro of CBDC

- China: deployment during Olympics

- Project Dunbar (AUS, Malaysia, Singapore, SA)

- Group of Seven report

- Hoover report on China \(\leftrightarrow\) US & CBDCs

What digital money?

fast money

real time rails run by chartered banks

CBDC

run by

chartered banks

run by

Bank of Canada

new communually run system

Stablecoin

private firm (e.g. Facebook)

CBDC on public blockchain

chartered bank-issued on public blockchain

Can and will the Bank of Canada issue a CBDC?

The Bank of Canada's Contingency Plan (Feb 2020):

Consider Issuing CBDC if:

- Cash becomes unusable, and/or

- An alternative digital money starts taking over

Will they?

Veneris, Park, Long, Puri (2021): BoC is in a legal position to issue a CDBC and there are several legal paths to do so

Can they?

What's Next?

CBDCs

- regulatory action

- FIs to provide some services

- continued evolution

- major disruption for FIs

- DefFi => Diem

- new finance brands

- "CBDC as service"

- few "real" CBDCs

End of Part 2 survey

please navigate again to

End of Part 2 debate

Discussion topic: "Decentralized Finance on public blockchains will play a bigger role in the future of finance and property than CBDCs, Diem, or a banking-sector solution"

Setup: Random sorting into TWO groups

- Group 1: Agrees and defends this statement with this statement.

- Group 2: Disagrees

Format

- Each group presents its arguments (3 min each)

- Each group presents a rebuttal (1 min each)

- Vote on who had the better argument.

Your task for the next 10 minutes

- prepare your arguments and rebutals of the arguments that you think the other side will present

Conclusion

digitization of payments is advancing

innovation in the sector indicates that there are unfilled customer needs

traditional players are well set up for now, but there are significant pain points

traditional players have difficulty innovating (lack of need, compliance, cannibalization fears)

DeFi creates new ideas and opportunities, CBDC use case is still unclear

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/

$16B for transactions costs?

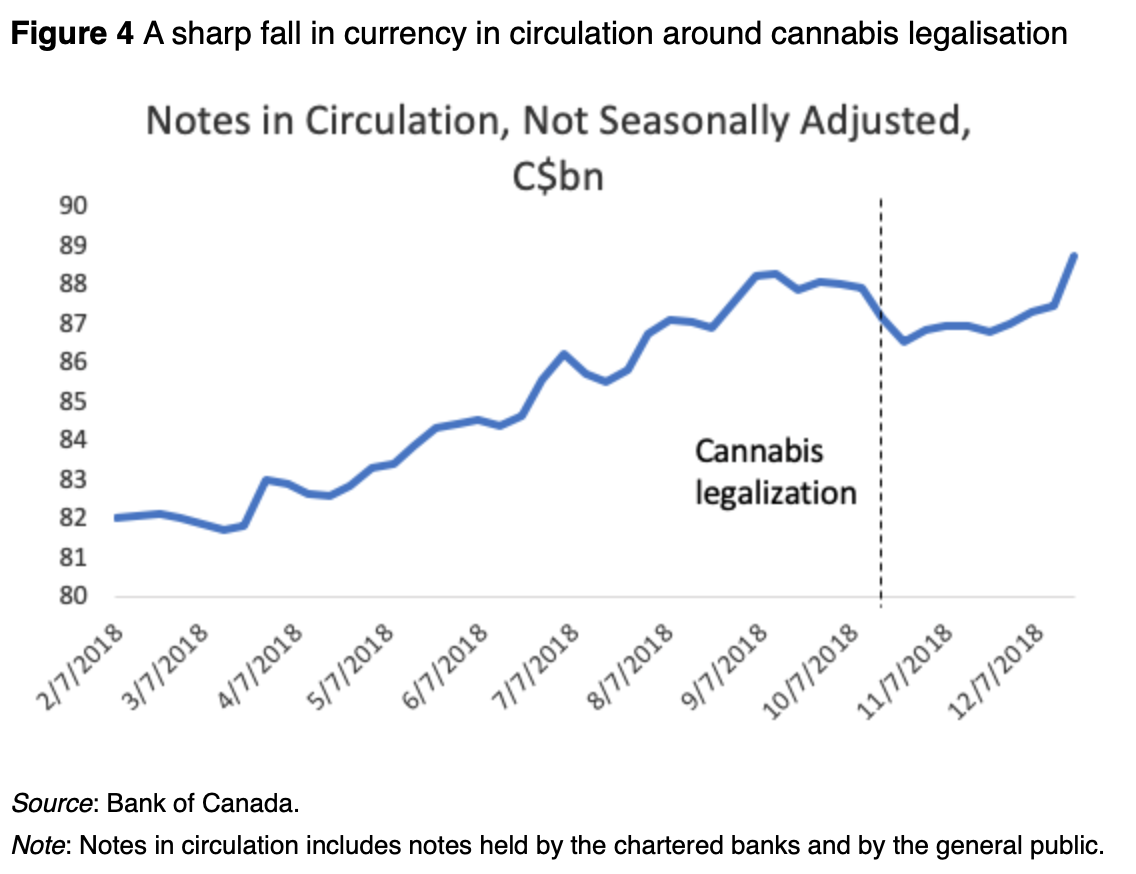

Cash and drugs: Cannabis legalization in Canada

Obstacles & Hurdles

PayTech

banking and payments activity require a banking license

need approval of the Finance Minister and the Office of the Superintendent of Financial Institutions (OSFI)

Hurdle #1: Current Law

Pain Points & Adoption Hurdles

providing any financial service

acting as a financial agent

providing investment counselling or portfolio management services

issuing payment, credit, or charge cards,

operating a payment, credit, or charge card plan in co-operation with others (including other financial institutions)

Wide Reach of the Law

Hurdle 1: Current Law

Existing banks protected from (too much) competition

granting of bank license has extensive list of regulatory criteria (subject to political interpretation)

takes 2 to 5 years to successfully acquire a banking license in Canada

Rogers applied in 2011 and was granted a Schedule I bank license in 2013

most FinTechs and PayTechs do not have the time or money to acquire a banking license

High Regulatory Adoption Hurdle

Hurdle 1: Current Law

-

PayTech demonstrated use and purpose of prepaid card to regulator

-

OSFI rep had never seen one, not had any experience in dealing with the regulatory implications of this product.

-

OSFI and others do not have Fintechs and PayTechs in scope (not yet threat to the safety and soundness of the financial system).

Lack of Knowledge by Regulators

EXAMPLE #1

Hurdle 1: Current Law

-

regulatory compliance = lawyers

-

lawyers = second line of defence teams at FI

-

\(\Rightarrow\) decision makers have very little access to clients and the frontline.

EXAMPLE #2

good at general service and infrastructure

banks have very rigid ways of engaging with their clients, “they push information, they don’t take it”

\(\Rightarrow\) poor at customization and customer service

Banks & the Last Mile Problem

Banks' Modus Operandi

Premise of FinTech

start with customer needs and then build platforms

Hurdle 1: Current Law

Current Development

New Framework To Regulate Canadian Retail Payment Ecosystem was in the 2019 budget

foundation for broader, risk-based access to Canada’s retail payments ecosystem

Payments Canada: "level the playing field"

Mentioned safeguards:

-

safeguarding end-user funds

-

implementing operational risk-management standards

-

minimum disclosure requirements

-

dispute resolution mechanisms

-

liability rules.

Is PayTech a thing in Canada?

Yes!

42+ PayTechs in the GTA

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

Yes!

42+ PayTechs in the GTA

Source: Seizing The Opportunity: Building The Toronto Region Into A Global Fintech Leader; TFI/Deloitte/McMillian 2019

Is PayTech a thing in Canada?

Remittances

Consumer PayTech

loyalty

Payment financing

mobile payment integration

mobile payments + rewards

connect advertising directly with immediate mobile purchasing option

personal payment management app

Payment financing + loyalty

PayTech & Accounting Platforms

Overall idea: increase visibility of payments across the supply chain and across internal business operations

Specialized SME Products

property management and rent payments

B2B & inter-company real time payments

gig economy instant pay

fast vendor payment

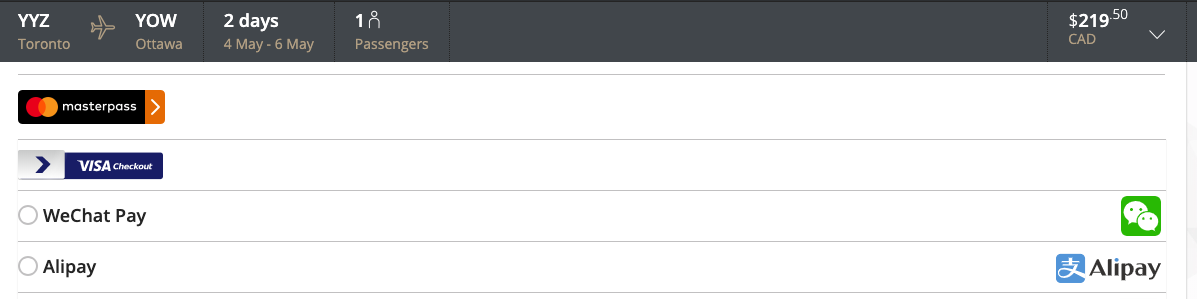

Services to Cater to Chinese Customers

North American merchants connect to Chinese consumers who use WeChat & Alipay

Why do PayTech solutions emerge?

people want mobile, frictionless, and immediate

Reduced payment

risks

new customer-business relationships (data collection)

Business integration and accounting simplification

expansion of merchant and user base

Innovations in Non-physical Payments around the world

Scandinavian Digital Payments

Mobile

Money

Mobile Apps in Emerging Economies

Critical PreReq for Danish Mobile Pay

government issued digital ID

available to anyone with a SIN

common login for:

civic services

banking

taxes

other businesses, e.g. telcos

Components of Danish Mobile Pay

a mobile app

links to existing bank account

uses trusted infrastructure and authentication

cleverly leverages what you have

adoption rate shows the value of form factor/frictionless experience

Mobile Money in the Developing World

bank account

access to saving vehicles and safe storage & transfers

better economic future

Mobile Money: M-Pesa

https://www.youtube.com/embed/g1IqjY88YuM?enablejsapi=1

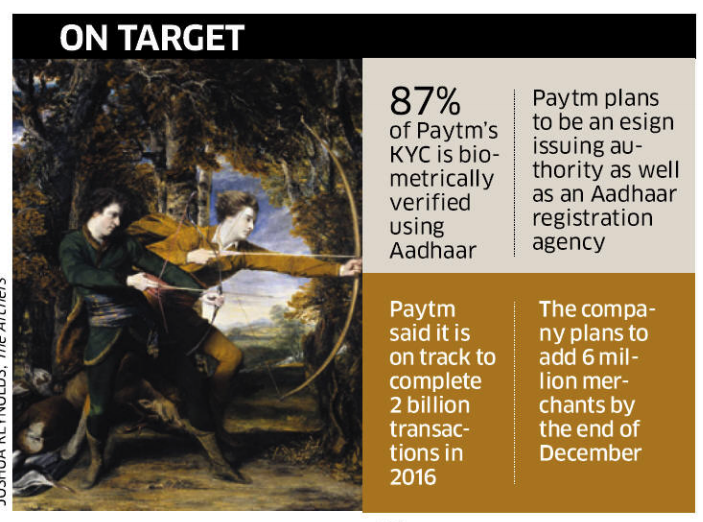

Component of : digital identity + Unified Payments Interface

"To empower residents of India with a unique identity and a digital platform to authenticate anytime, anywhere."

- "[PayTM] want[s] to become the universal payments layer on every bank account"

- "something that was going to take 3-6 years now takes 3-6 months"

UPI puts multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments under one hood.

some stats for India

-

300 million users

-

5 million transactions per day

-

over 7 million merchants

-

over $4 billion per month

Why is WeChat etc already relevant for Canada?

Will new students ...

-

get a bank account?

-

or just choose merchants by whether they can use WeChat pay?

How about new immigrants?

-

At what point will they simply stop using Canadian banks?

- and almost every other 905 tourist mall

- >150K WeChat Pay users @GTA

1. Visit Agent

2. Deposit Cash by phone or bar code

3. Use online

Customers use Amazon login ...

... to pay at other merchants sites!

Why we should be skeptical of untethered AI

Application: Decentralized Lending

\(\vdots\)

Smart Contract Derivatives with Synthetix

- creations of Synths

- tokens linked to underlying price feed provided by a Chainlink Oracle

- long asset: sToken (sETH, sBTC)

- short asset: iToken (iMKR iAAV)

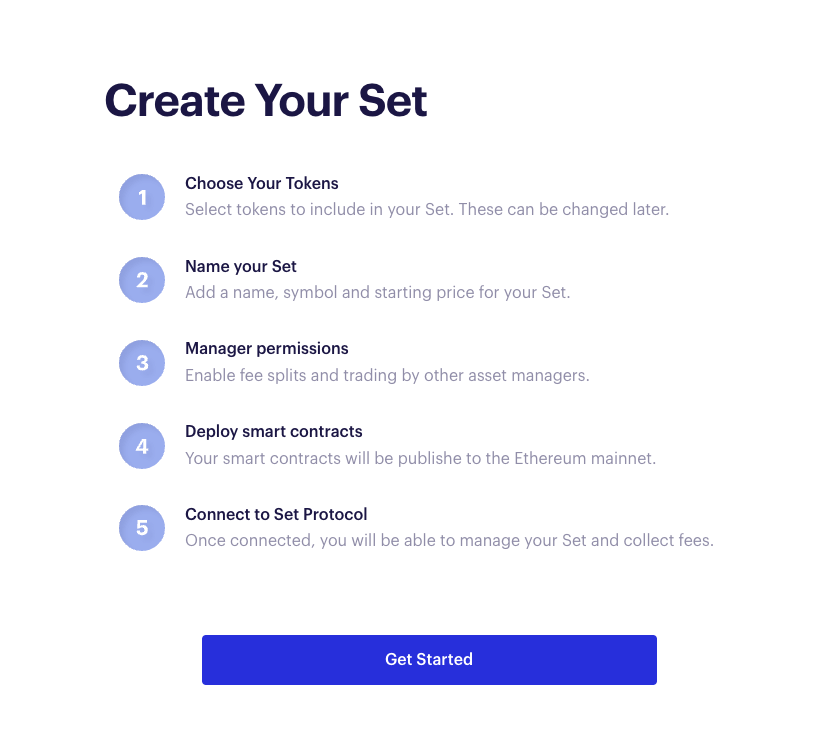

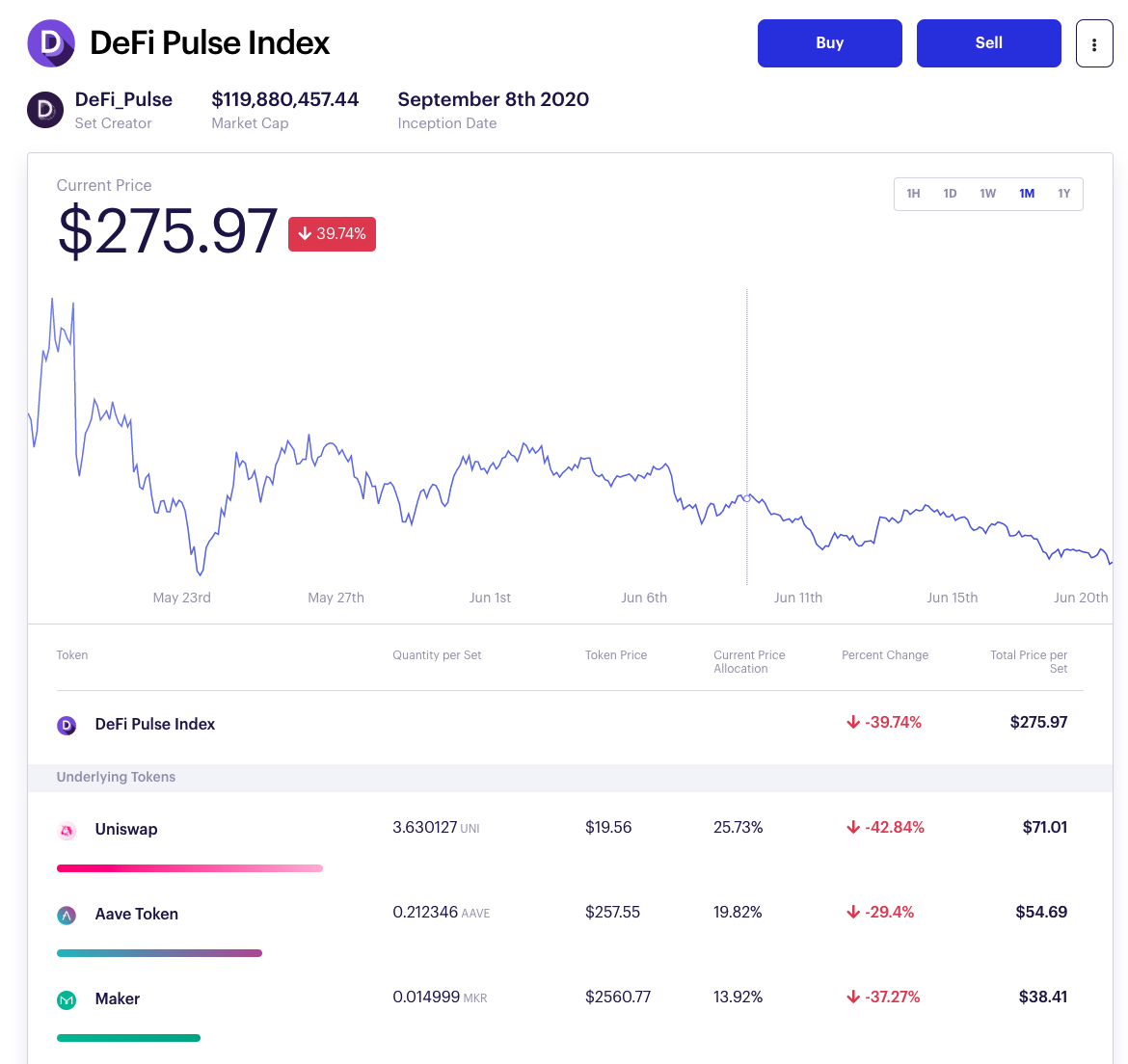

Securities Creation: Tokensets

idea: create new mutual fund like asset

Risks and open problems

- many apps are still experimental, many kinks need ironing, and tech progress is needed

- smart contract risk:

- detecting problems with code

- detecting problems with economic incentives

- foreseeing unforeseen contract contingencies

- contract contagion risks

- governance of decentralized organizations

- role of regulators

Who's in it?

Partnerships

"new financial infrastructure"

When it goes live, it will come with extensive "layer two" functionality

Why is payments data valuable?

How much money is coming into and out of the account each month

If you had a full view of payments, what would you learn?

Spending habits: what you spend money on and where you spend it

Payment habits: Are you paying bills way ahead of deadline or tardy?

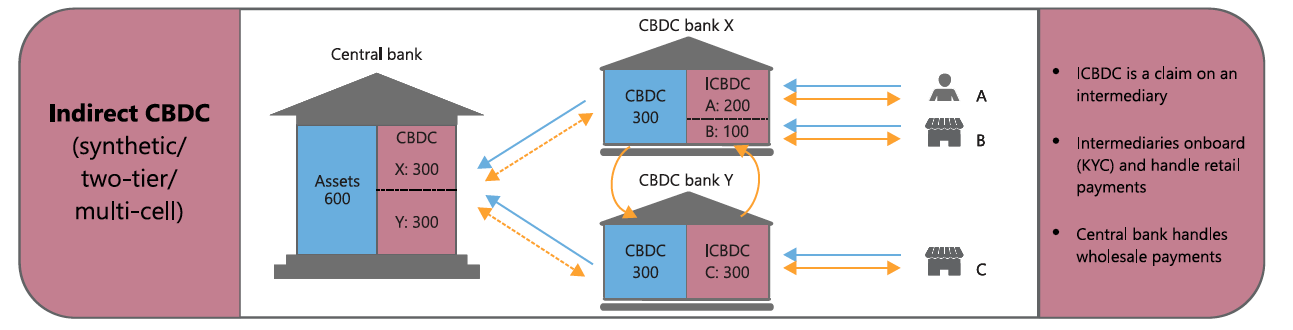

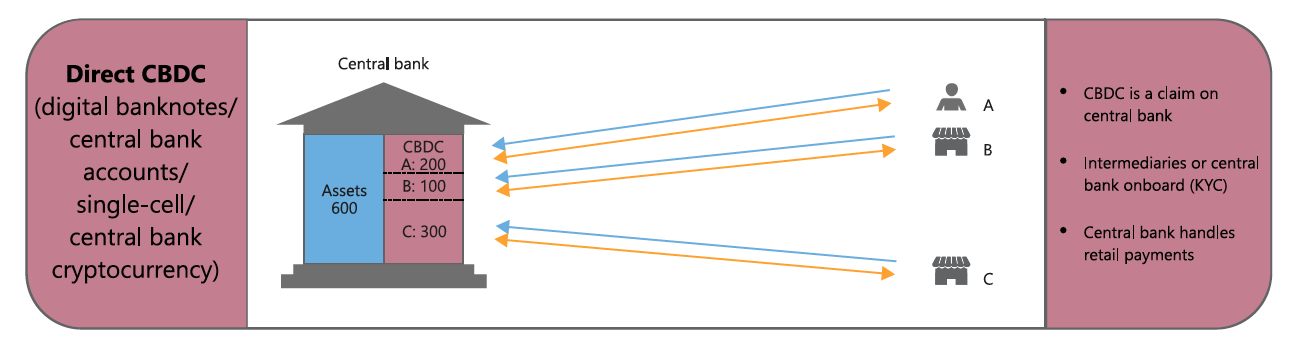

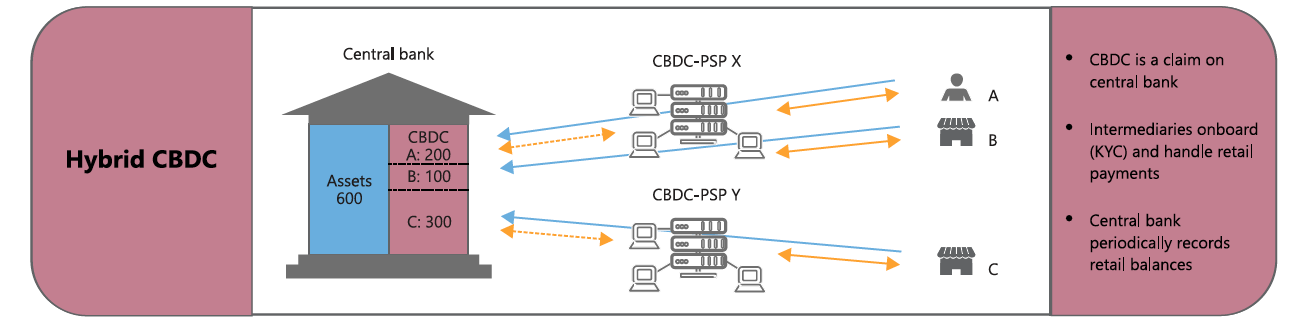

Possible CBDC architectures

Source: BIS Quarterly Review, March 2020

Would a CBDC destabilize the banks?

BoC analysis (August 2020):

- [banks] are well-positioned to absorb potential temporary negative effects on profitability and liquidity

- Banks[can] absorb the shock under plausible adoption scenarios.

- [No] threat to the stability of the financial system or to banks’ competitiveness in terms of ROE.

- banks will maintain healthy liquidity levels, and liquidity could become a concern only in the most extreme scenario.