Use of Hypothetical Data in

Machine Learning Trading Strategies

Disclosures: All investments carry risk. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.

Ankit Awasthi

Quantitative Portfolio Manager

What will we cover today

Evolution in trading and machine learning

Data Augmentation in Deep Learning

How to generate hypothetical data for trading strategies ?

Stylized facts of time series of asset returns

Improving deep learning models for Finance

Future Testing Strategies

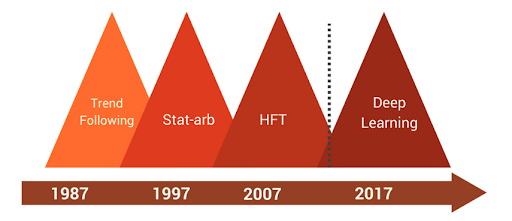

Ten Year Cycles of Innovations in Trading

Source : May 2017 Research, qplum

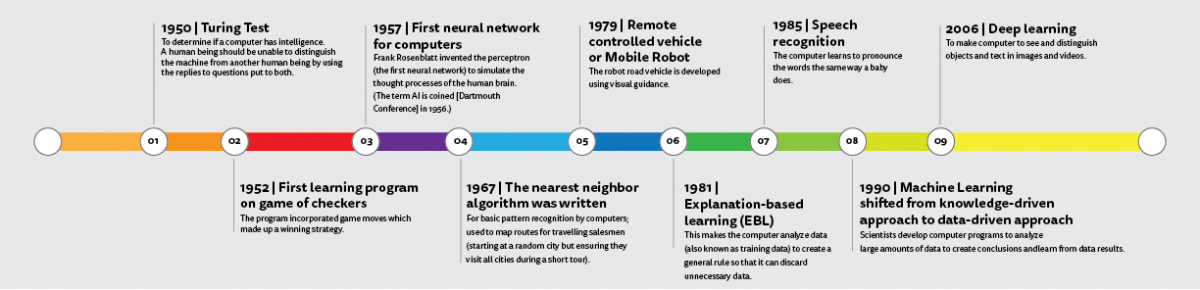

Evolution of Machine Learning

Tremendous Success of Deep Learning

Image

Text

Speech

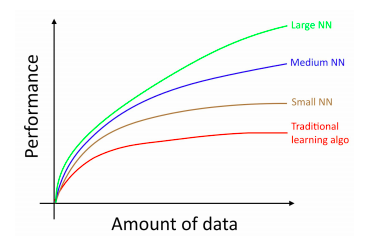

Abundance of Data!

Deep learning scales with data

Source : Andrew Ng, Coursera Deep learning specialization

Data Augmentation for Deep Learning

Even more data!

Source : Bharat Raj, Data Augmentation | How to use Deep Learning when you have Limited Data

Much harder in Finance!

Generating Hypothetical Data for Trading

-

Adding noise or transformations

- Data generated is similar to original so doesn't lead to great generalization

- Higher magnitude noise can distort properties of financial time series

-

Theoretical models

- Hard to estimate and sample from

- Multi-variate distributions are problematic

- Hard to account for all empirical properties of financial time series

-

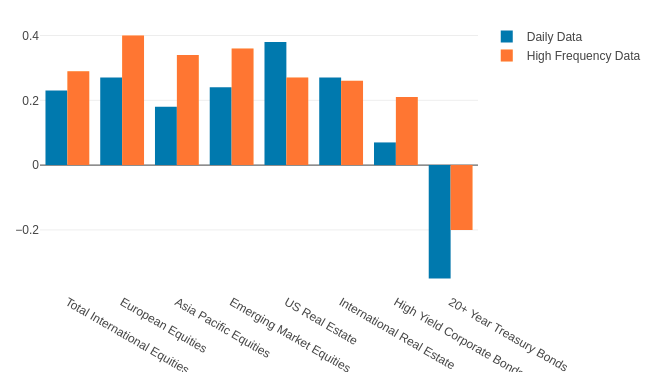

Appropriating High Frequency Data

- Shows remarkable similarity to Daily Data

- Data acquisition is hard and costly

Using High Frequency Data as Daily Data

Step 1 : Generate 15-minute contiguous non-overlapping samples from high frequency tick-data

Step 2 : Compute Mean and Variance for daily returns as Daily_Mean and Daily_Variance

Step 3 : Transform High Frequency Data to have the mean as Daily_Mean and variance as Daily_Variance

Stylized Effects of Financial Time Series

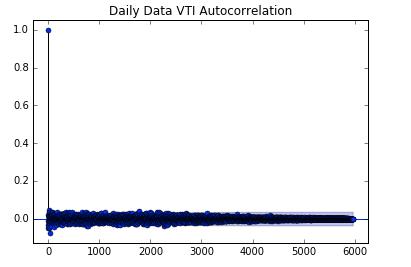

Absence of Autocorrelations

Heavy Tails

Volatility Clustering

Leverage Effect

Cross Correlation vs Volatility

Absence of Autocorrelations

Autocorrelation of returns is low both in daily and high frequency data

Autocorrelation

Autocorrelation

Lag

Lag

Source : qplum Research

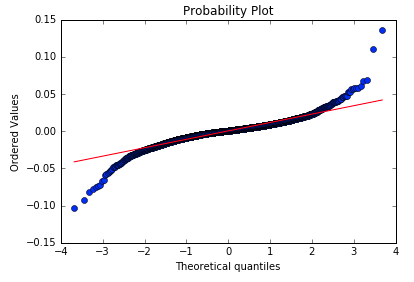

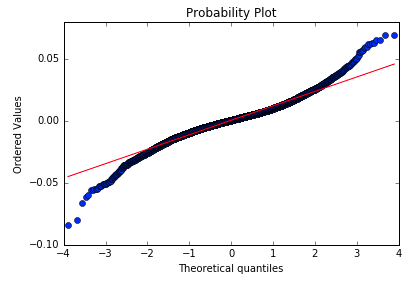

Heavy Tails

High frequency data exhibits divergence from normal similar to daily returns

The magnitude of the divergence, however, is much more pronounced for daily returns

Source : qplum Research

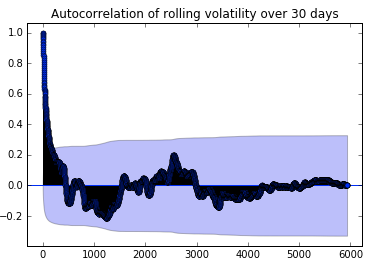

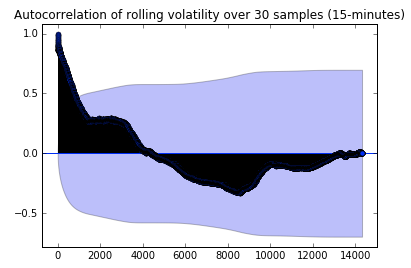

Volatility Clustering

As opposed to returns, volatility of daily returns shows significant autocorrelation, which is retained in high frequency data as well

Autocorrelation

Autocorrelation

Lag

Lag

Source : qplum Research

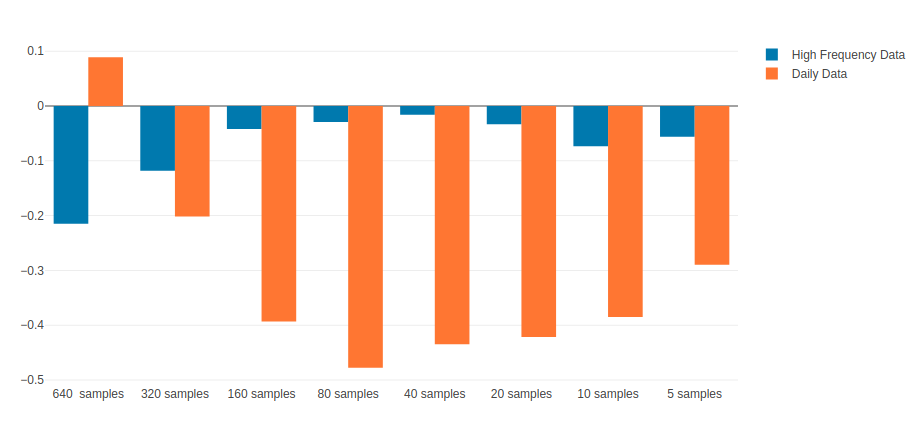

Leverage Effect

...refers to the observed tendency of an asset's volatility to be negatively correlated with the asset's returns

Correlation of volatility with returns for US Total Market Index (VTI)

Leverage effect is also exhibited by high frequency data but to a smaller extent

Correlation

Source : qplum Research

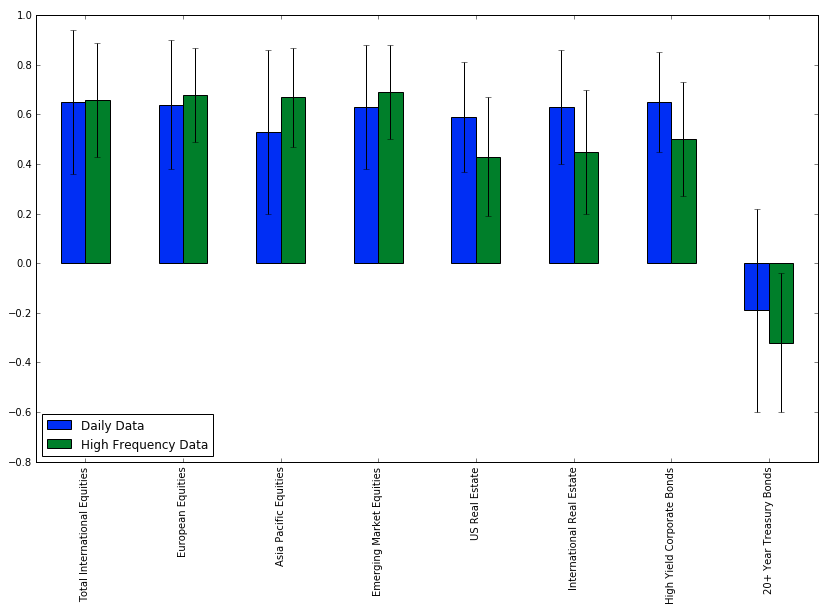

Cross-Correlation Vs Asset Volatility

Mean of 30-day rolling correlation of different assets with US Total Stock Market (VTI)

Standard Deviation is shown as error bars.

Correlation ( Mean and Variance )

Source : qplum Research

Correlation increases with volatility

Correlation of 30-day rolling correlation of log returns of different assets vs US Total Stock Market against the volatility of US Total Stock Market.

Correlation

Source : qplum Research

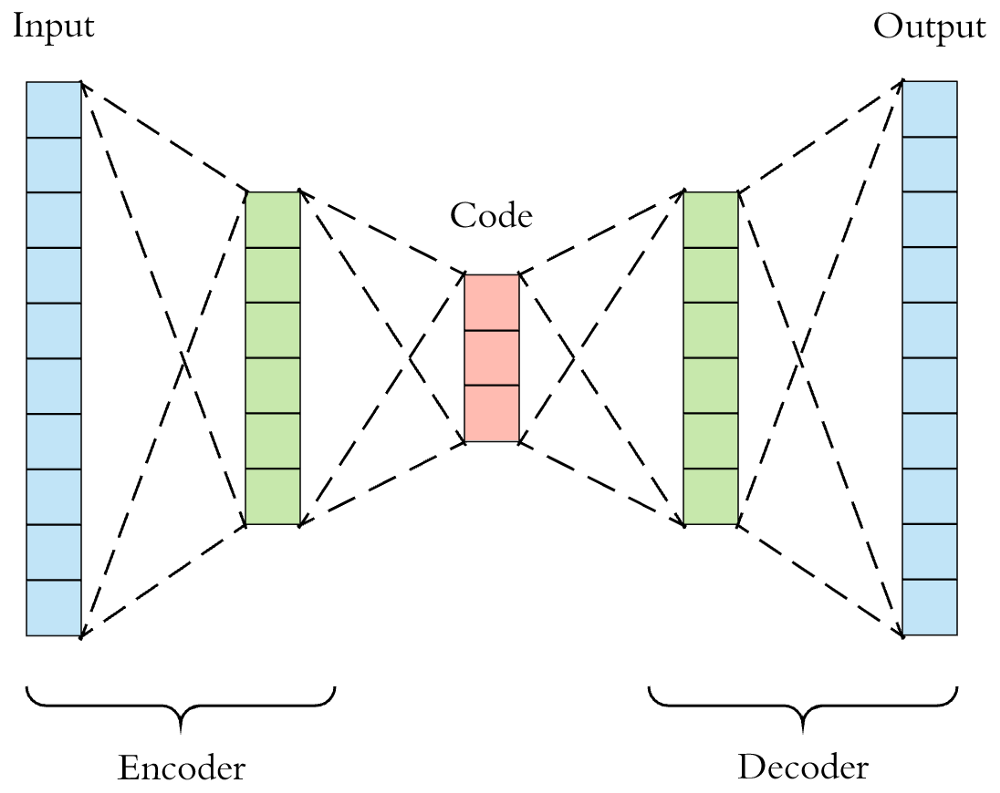

A simple example - Autoencoders

Source : Arden Dertat, Applied Deep Learning

Feature Learning

Source : Arden Dertat, Applied Deep Learning

- Factorization of price-volume features across multiple securities

- Unsupervised - It is not used to predict returns, or maximize performance metric

- Information bottleneck forces the network to learn the most important factors

- Captures non-linearities across time and cross section of securities

Experiment

Daily EOD Data

Training

3000 pts

Validation

1000 pts

Testing

1000 pts

Large High Frequency Data Corpus

( 32000 pts )

Training

(High Frequency + Daily)

Validation

Out of Sample

Evaluation

Source : qplum Research

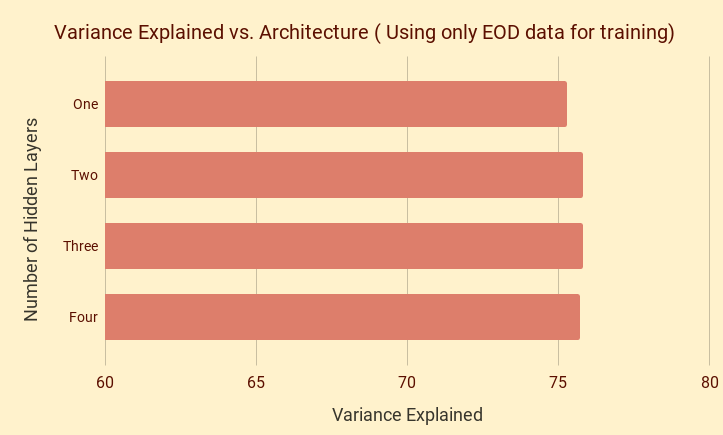

Model complexity alone doesn't help much!

One Hidden Layer : 62 -> 3 -> 62

Two Hidden Layers : 62 -> 10 -> 3 -> 10 -> 62

Three Hidden Layers : 62 -> 20 -> 10 -> 3 -> 10 -> 20 -> 62

Four Hidden Layers : 62 -> 100 -> 20 -> 10 -> 3 -> 10 -> 20 -> 100 -> 62

Source : qplum Research

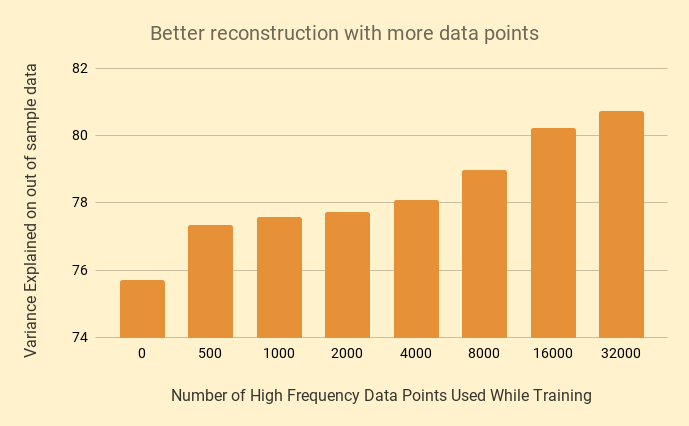

However....more data does!

Architecture Used : 62 -> 100 -> 20 -> 10 -> 3 -> 10 -> 20 -> 100 -> 62

Source : qplum Research

Scenario Analysis

Helps to be data-driven with more data!

- Multiple instances of 'market crashes'

- Easy to find custom scenarios e.g., fixed income positively correlated to equities

- Periods of high or low divergence across different sectors in equity markets

- Multiple inflationary/deflationary periods as measured through commodity prices

Cross-Validating Hyper-parameters

Helps to be data-driven with more data!

-

Risk model parameters

- Sensitivity to lookback duration

- Combinations of different metrics like expected shortfall, current drawdown

-

Regularization constants

- Soft constraints in multi-objective portfolio optimization - constraining active risk and risk of the portfolio

-

Tax Optimization parameters

- Thresholds for deferring gains, booking losses as a function of volatility

Future Testing Strategies

" It is far better to forsee even without certainty than not to forsee at all " - Henri Poincare

-

Collect different capital market assumptions

- Qplum's Internal Expected Returns

- JP Morgan Capital Market Assumptions

- Research Affiliates Capital Market Assumptions

- ....

-

Transform high frequency data

- Set mean of returns such that annualized returns match the respective capital market assumptions

- Set variance of returns such that annualized volatility matches the respective capital market assumptions

- Evaluate performance of strategies under different capital market assumptions

Key Takeaways

Deep learning works best when you have lots of data

Adapting high frequency returns is one of the easiest ways of augmenting daily returns data

Hypothetical data can be used to stress test strategy performance

Hypothetical data can be used to develop better and more robust strategies

Questions?

contact@qplum.co

Disclosures: All investments carry risk. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.