Make Dat Money

TDF

By Jason Dobry

Problem #1

Need Clean Data

Inconsistent intervals,

crazy numbers in off ours, etc.

Solution

Clean it

Gathered data every hour on the hour from operational hours

Problem #2

Predicting Returns

Predict next hourly data point?

Or predict opening value?

Closing value?

Um, how?

Attempt #1

L2 Regression

Example

Fail

Heavily affected by outliers,

non-linearity,

too many variables, etc.

Attempt #2

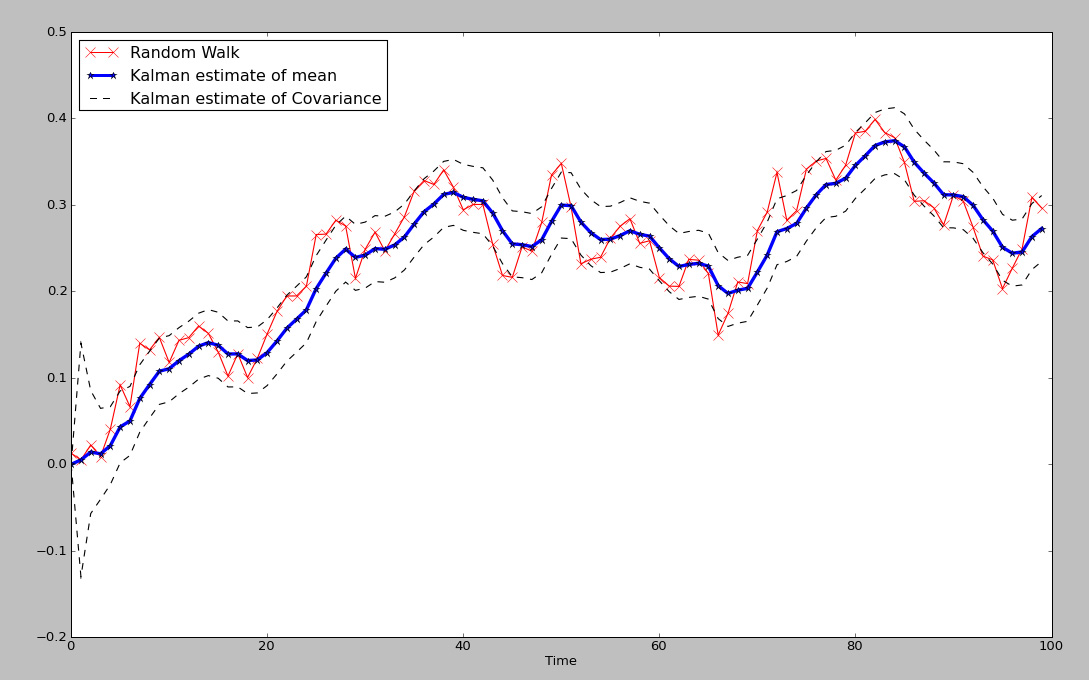

Kalman Filter

What's that?

The Gist

The Kalman filter operates recursively on streams of noisy input data to produce a statistically optimal estimate of the underlying system state.

Applications

Autopilot

Tracking and Vertex Fitting of charged particles in Particle Detectors

Tracking of objects in computer vision

Economics, in particular macroeconomics, time series, and econometrics

Inertial guidance system

Orbit Determination

Radar tracker

Dynamic positioning &

Navigation systems

Seismology

Simultaneous localization and mapping

Speech enhancement, Weather forecasting, 3D modeling

Example

How does it work?

xt = A * (xt - 1) + w

xt -

hidden variable we're trying to estimate

A - state transition matrix

(xt - 1) -

current state

w -

noise of model

zt = H * xt + v

zt - noisy measurement

H -

observation model

xt -

xt from above

v -

noise of model

How does it work?

xt = A * (xt - 1) + w

xt -

hidden variable we're trying to estimate

A - state transition matrix

(xt - 1) -

current state

w -

noise of model

zt = H * xt + v

zt - noisy measurement

H -

observation model

xt -

xt from above

v -

noise of model

Quadratic Filter

xk | k-1 = 3 (xk-1 - xk-2) + xk-3

assumes that every four consecutive trend values fit a quadratic curve

xk = xk | k-1 + ( Gk * (yk - xk | k-1) )

final estimate combines observation and state change estimate

Problem #3

Risk

Solution

Force Diversification

Restrict Maximum amount of wealth invested per stock

Experiments

Restrict investment per stock to:

1% of wealth

5% of wealth

20% of wealth

Solve LP for Optimal Portfolio

Trade = Optimal Portfolio - Current Portfolio

Experiments

Trade:

Every Hour

At Opening

At Closing

Most successful agents had diverse portfolios and traded once a day