The surprisingly fun topic of CORPORATE tax avoidance:

who is to blame?

Javier García-Bernardo

The University of Amsterdam

Sept 29th, 2017

Javier Garcia-Bernardo, Jan Fichtner, Frank Takes, Eelke Heemskerk

episode IV: conduits and sinks

``Uncovering Offshore Financial Centers: Conduits and Sinks in the Global Corporate Ownership Network''

https://www.nature.com/articles/s41598-017-06322-9

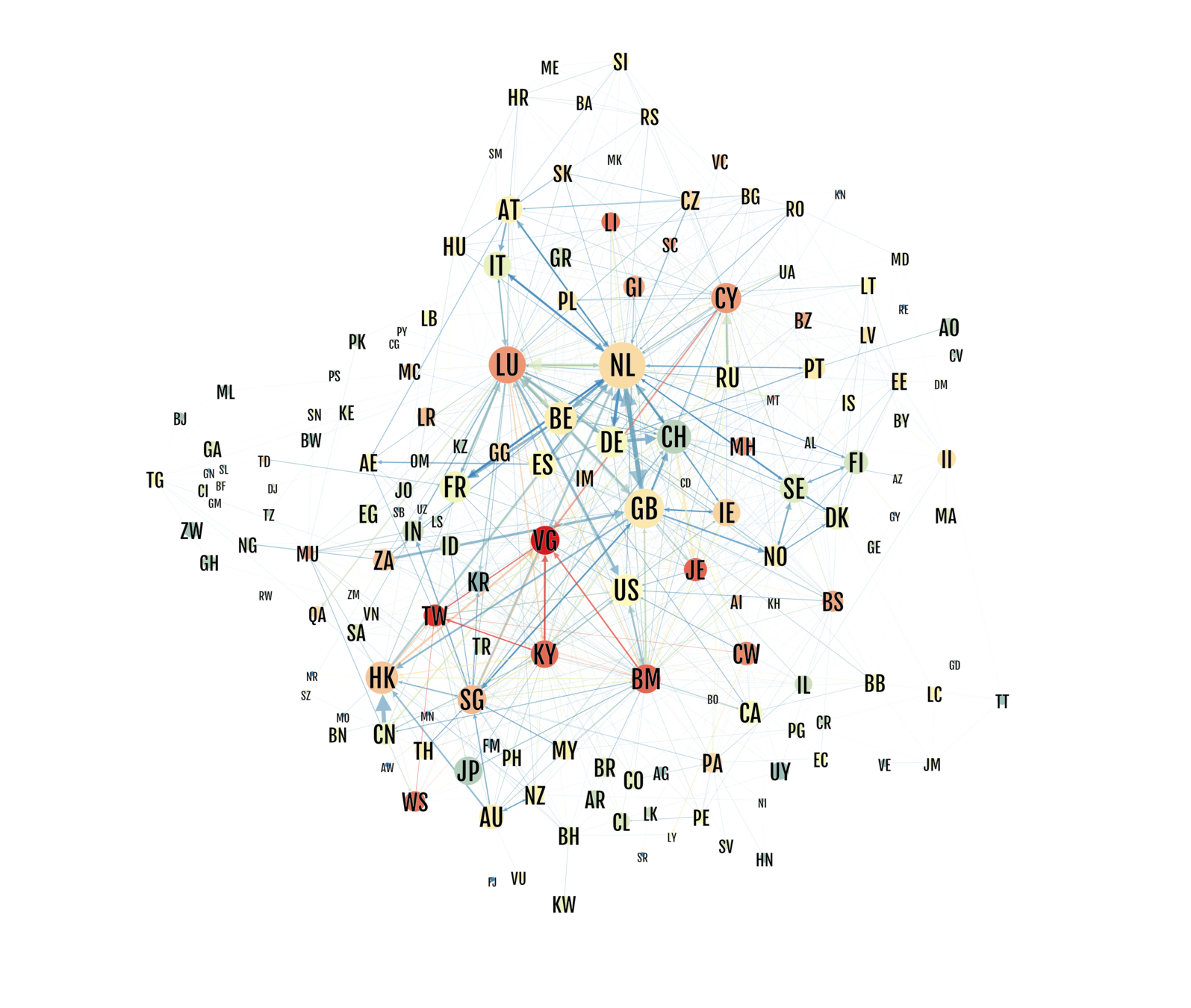

sinks and conduits

We look at which countries are used disproportionally in transnational ownership chains.

ORBIS

- 200 million companies

- 70 million ownership relationships

- 10 million transnational chains

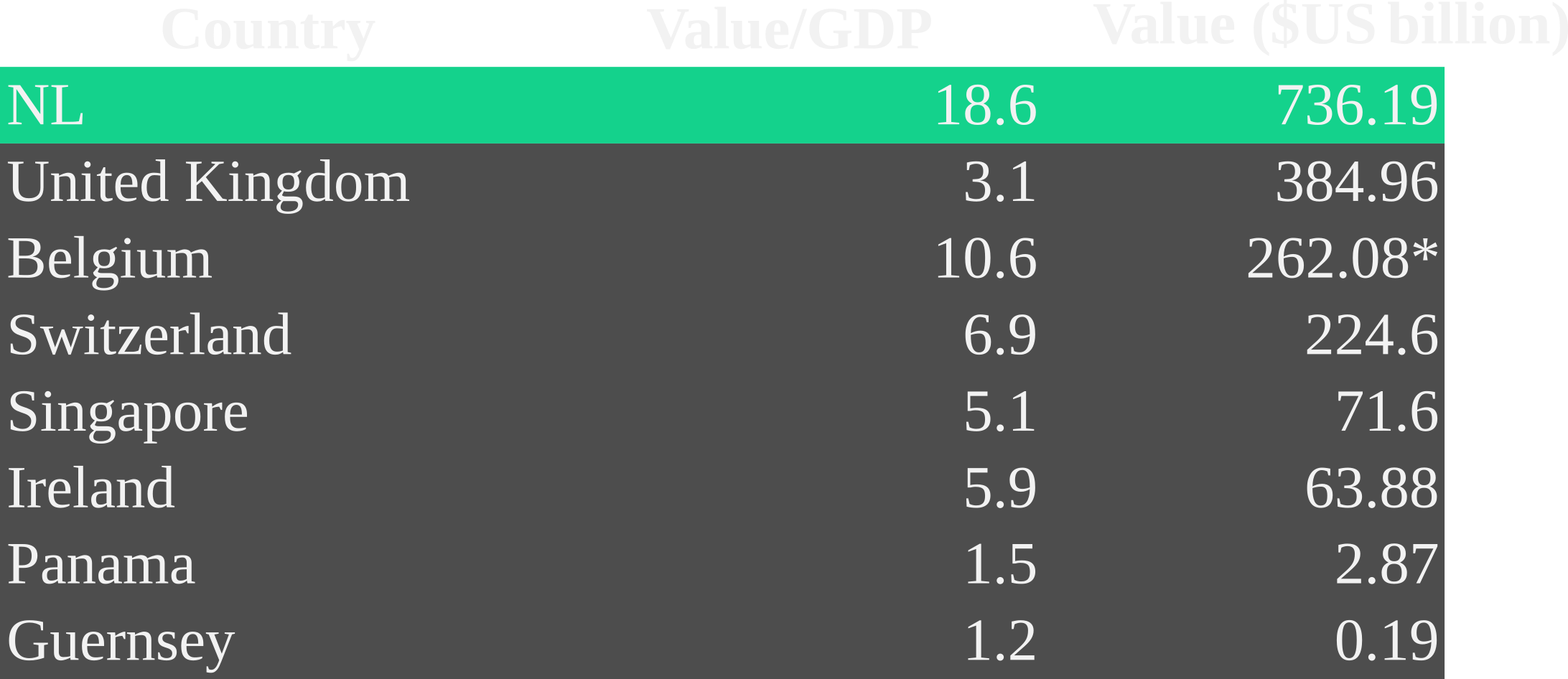

finding 1: sink-OFFshore financial centers

Blue: (Former) Colony/Territory of the UK

aka The empire strikes backParadisacal beach in Luxembourg

finding 2: conduit-OFFshore financial centers

sink

conduit

some country

18% of all flow to sinks

23% of all flow to sinks

episode V: tax treaties

`The erosion of sovereignty and race to the bottom'

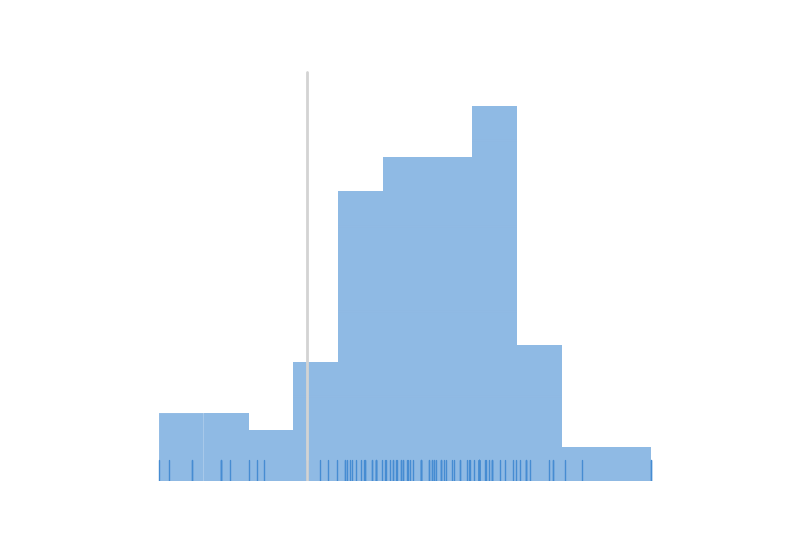

Data: Yearly snapshots (2008-2017) for dividend, royalties and interest withholding taxes.

TAX TREATIES

Agreements between two countries, in which they clarify who has the right to tax what in order to avoid double taxation.

Corporations move profits to conduits and sinks using tax treaties.

why they matter

Theory:

- Provide security and protection to MNEs

- Increase investment between two countries

why they matter

Theory:

- Provide security and protection to MNEs

- Increase investment between two countries

why they matter

However:

- The investment can be only in paper (treaty shopping), which would drive a race to the bottom.

- Reflect the imbalance of power and experience between countries.

- Potential for loopholes.

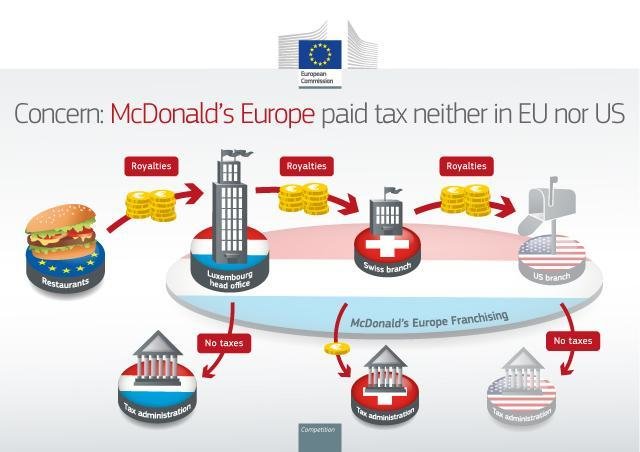

- Tax treaty US-LU: Royalties should pay taxation in US, and McDonald's needs to show the receipt.

- Loophole: US law states that branches should pay tax in Luxembourg.

- Lux tax ruling: McDonald's does not need to show the receipt.

EPISODE V: TAX TREATIES

PART 1: treaty shopping or real investment?

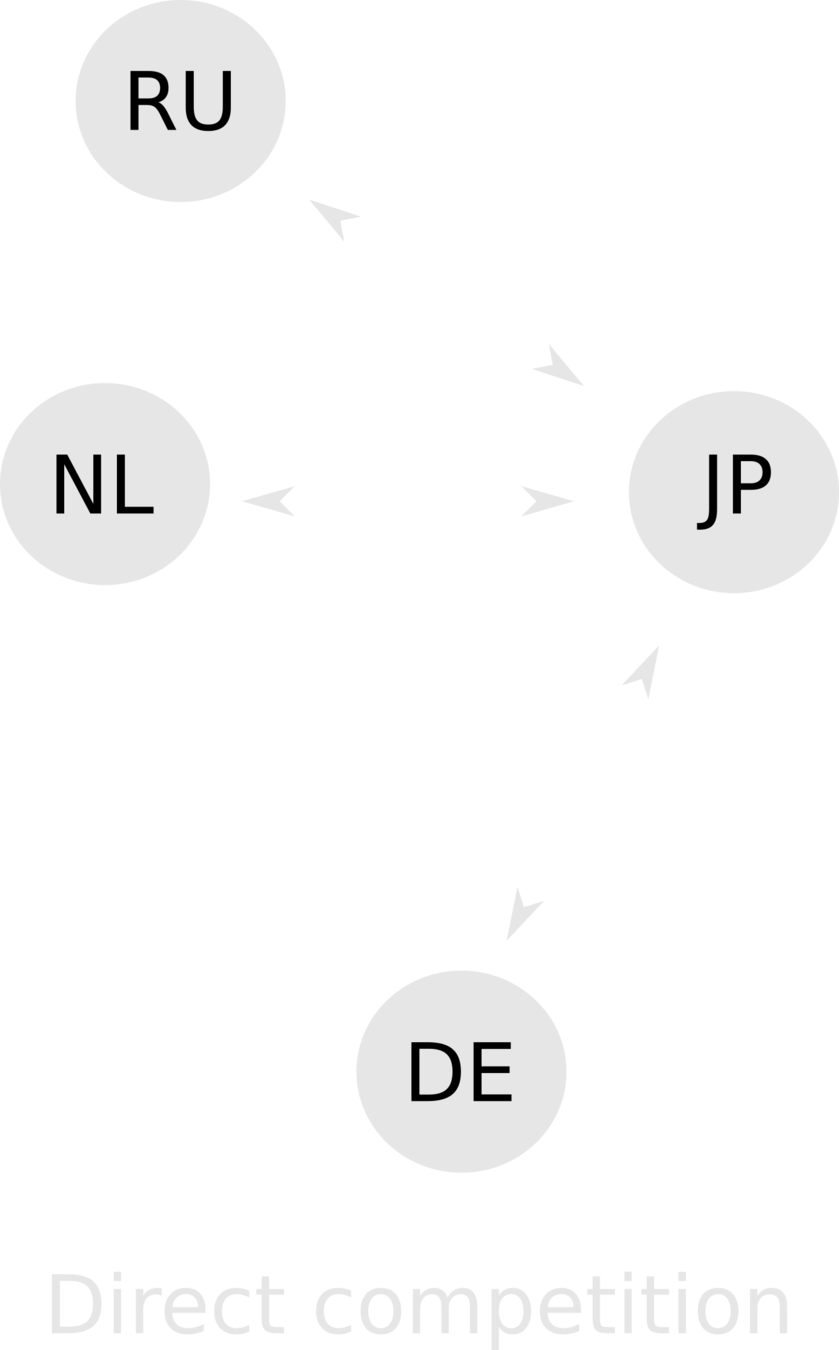

Part 1: direct or indirect competition?

If treaty shopping is real:

- MNEs move if indirect routes are cheap

- Small countries have a first-mover advantage

- Sovereignty eroded: Other countries are forced to reduce taxes.

Method:

- Test if investment after a tax treaty is associated with a decrease in investment in neighbor countries.

Part 1: direct or indirect competition?

EPISODE V: TAX TREATIES

PART 2: who drives the process?

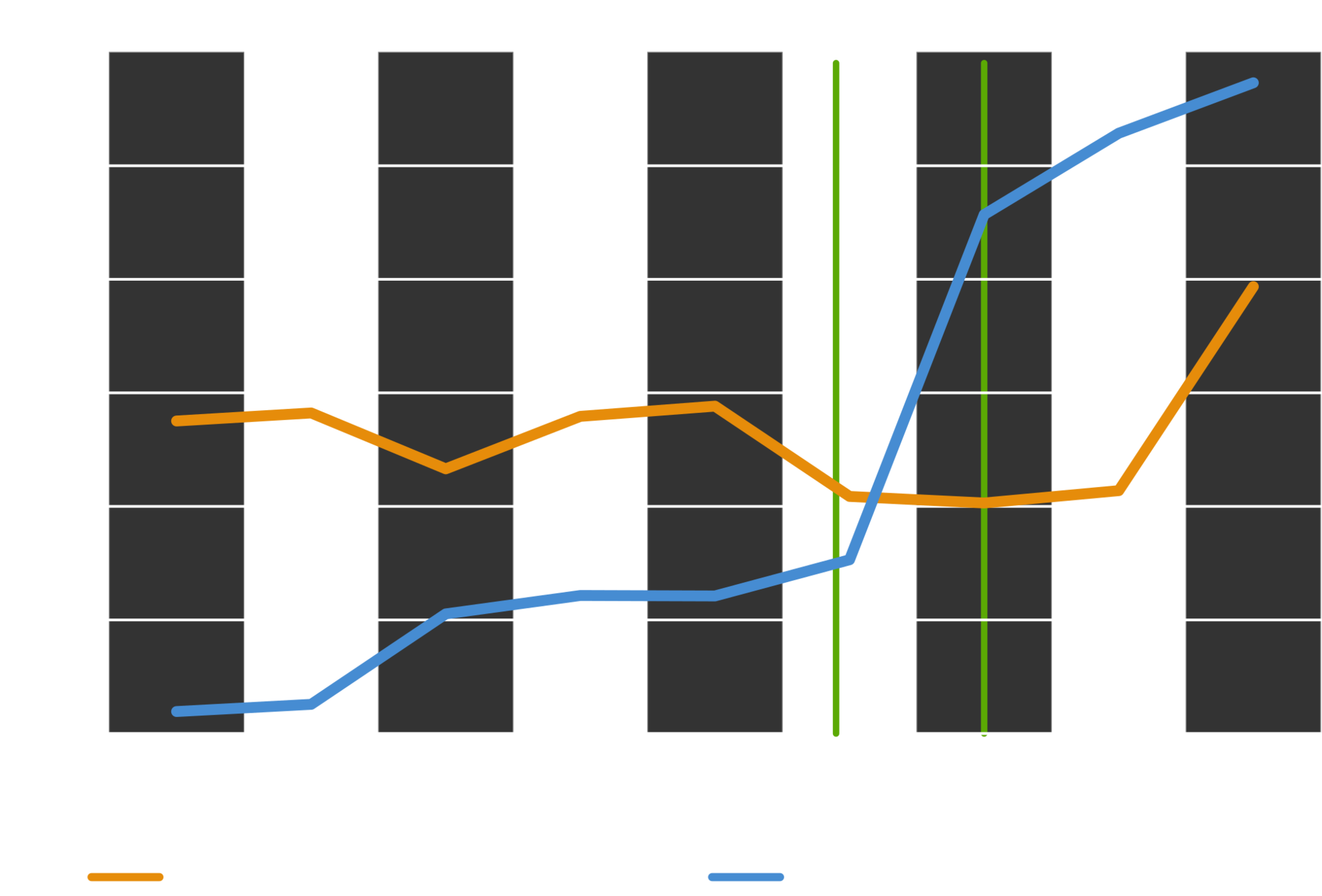

Part 2: who drives the process?

- Use transfer entropy or cross-correlation times.

Part 2: who drives the process?

- Use transfer entropy or cross-correlation times.

Part 2: who drives the process?

- Use transfer entropy or cross-correlation times.

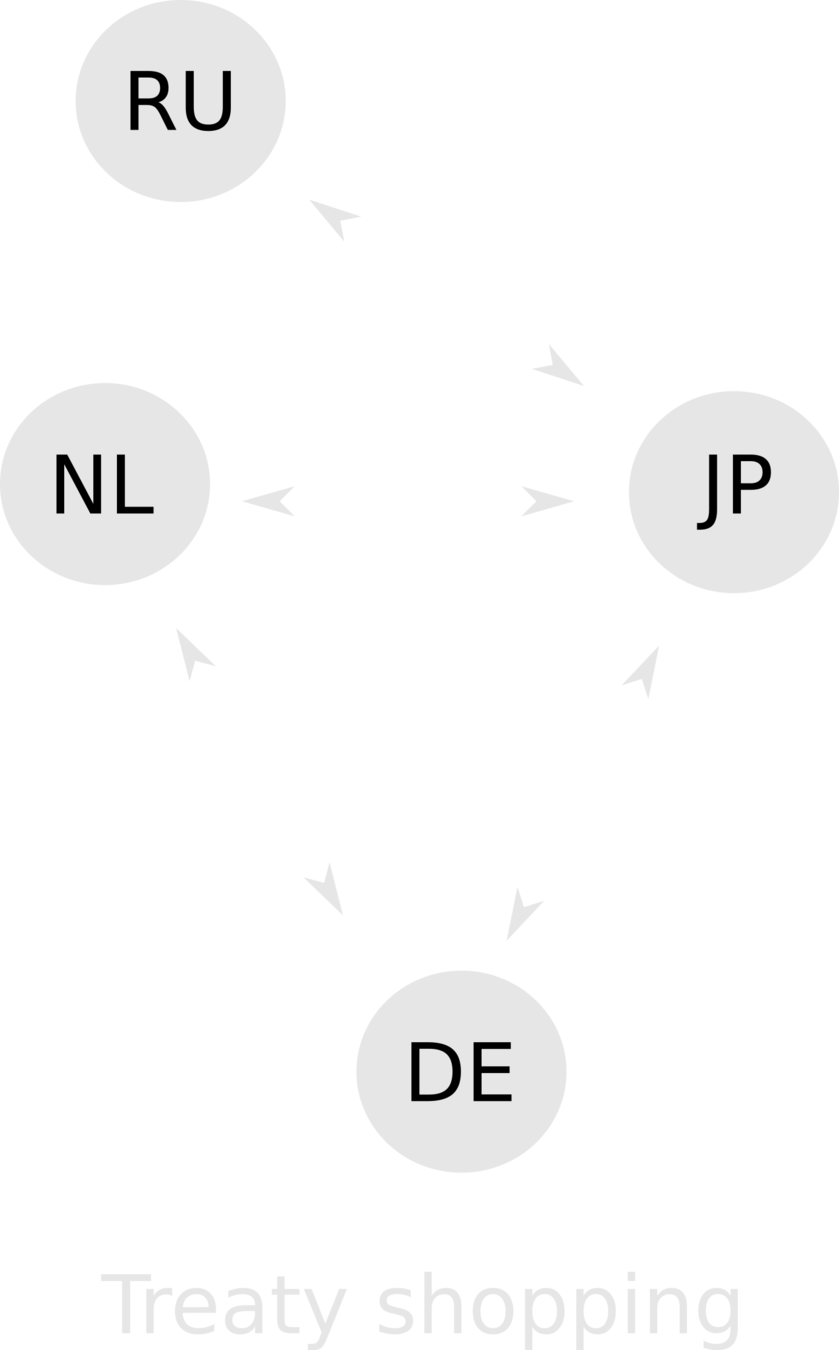

- Order the hierarchies (in the example above NL > DE)

- Find main drivers (on top of hierarchies) and which features are important (e.g. dividends, interests or royalties rates)

expectations

- Treaty shopping:

- Real, increase in investment in country A correlated with decrease in investment in neighbor countries.

- Only for conduits.

- Drivers of the race to the bottom:

- United Kingdom and Netherlands are the main actors.

- Royalties are the most important feature.

corpnet.uva.nl

This presentation: slides.com/jgarciab/eusn

@javiergb_com

@uvaCORPNET

javiergb.com

corpnet@uva.nl

garcia@uva.nl