Phase-Type Models in

Life Insurance

Dr Patrick J. Laub

Université Lyon 1

Work

Work

Coffee

Coffee

Lunch

Home

Chat

A typical work day

Work

Work

Coffee

Coffee

Lunch

Home

Bisous

Pause Café

Paperwork

Déjeuner

Il y a un pot

Une petite pinte

Paperwork

Sieste

(Talk)

A typical French work day

Work

Work

Coffee

Coffee

Lunch

Home

Chat

1/3

1/3

1/3

1

1

1

1

1

2

5

1

4

3

7

6

1/3

1/3

1/3

1

1

1

1

1

From Markov chains to Markov processes

- Coffee

- Work

- Lunch

- Coffee

- Work

- Chat

- Work

- Home

| State | Time in State |

|---|---|

| Coffee | 5 mins |

| Work | 2 hours 3 mins |

| Lunch | 26 mins |

| Coffee | 11 mins |

| Work | 1 hour 37 mins |

| Chat | 45 mins |

| Work | 2 hours 1 mins |

Chain

Discrete Time

Process

Continuous Time

Example Markov process

The Markov property

Markov chain State space

Markov process at times

Sojourn times

Sojourn times are the random lengths of time spent in each state

Transition rate matrices

2

5

1

4

3

7

6

1/3

1/3

1/3

1

1

1

1

1

Phase-type definition

Markov process State space

- Initial distribution

- Sub-transition matrix

- Exit rates

Example

Markov process State space

Phase-type distributions

Markov chain State space

Phase-type quiz...

Phase-type generalises...

- Exponential distribution

- Sums of exponentials (Erlang distribution)

- Mixtures of exponentials (hyperexponential distribution)

When to use phase-type?

When your problem has "flow chart" Markov structure.

E.g. mortality. Age is a deterministic process, but imagine that the human body goes from physical age \(0, 1, 2, \dots\) at random speed.

("Coxian distribution")

Class of phase-types is dense

S. Asmussen (2003), Applied Probability and Queues, 2nd Edition, Springer

Class of phase-types is dense

Why does that work?

Can make a phase-type look like a constant value

More cool properties

Closure under addition, minimum, maximum

... and under conditioning

Phase-type properties

Matrix exponential

Density and tail

Moments

Laplace transform

Guaranteed Minimum Death Benefit

Application

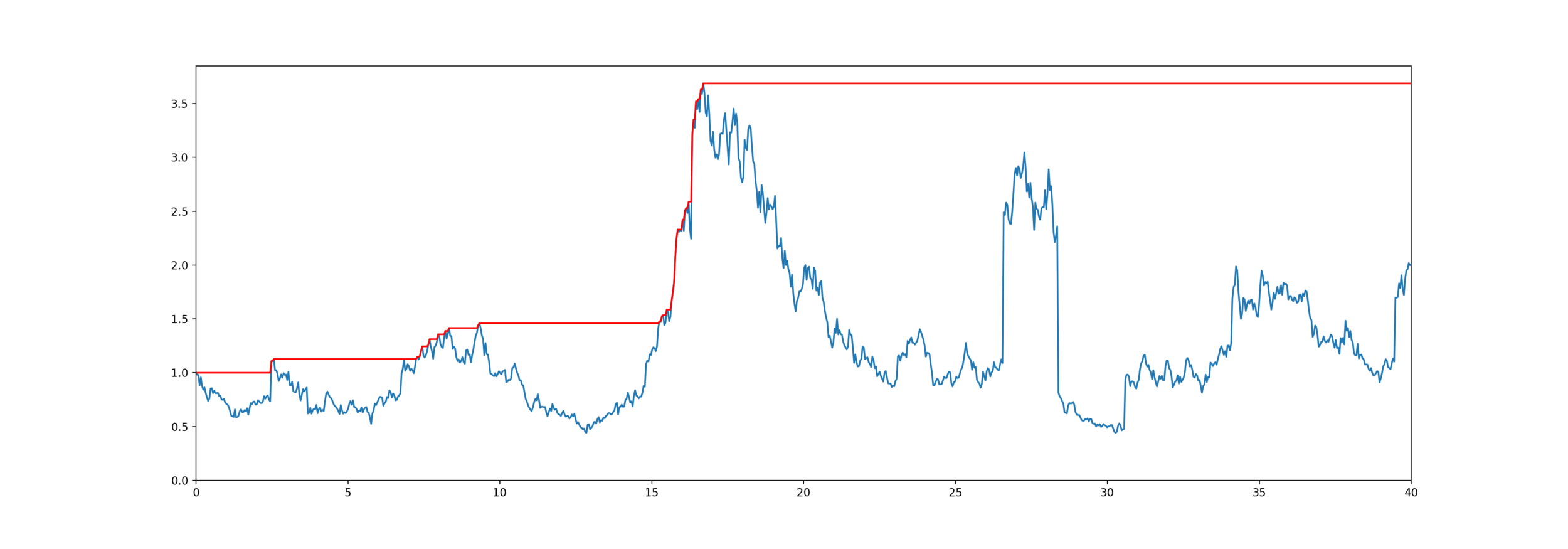

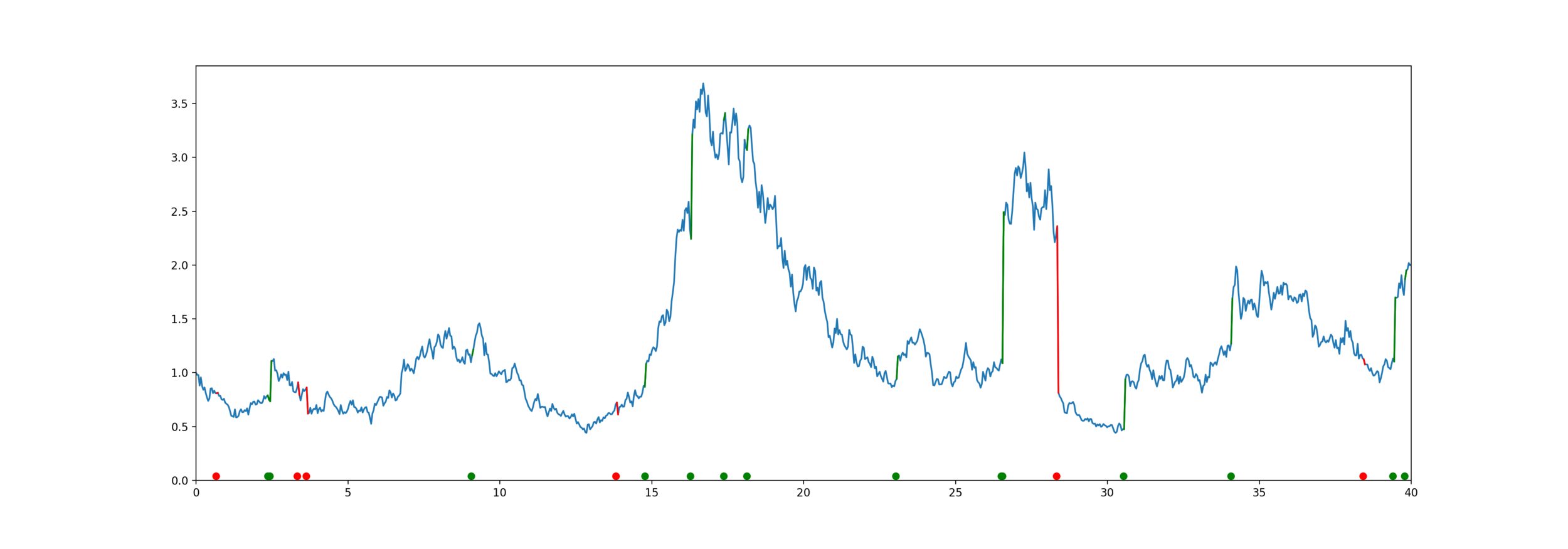

Equity-linked life insurance

High Water Death Benefit

Equity-linked life insurance

Model for mortality and equity

The customer lives for years,

Equity is an exponential jump diffusion,

Exponential PH-Jump Diffusion

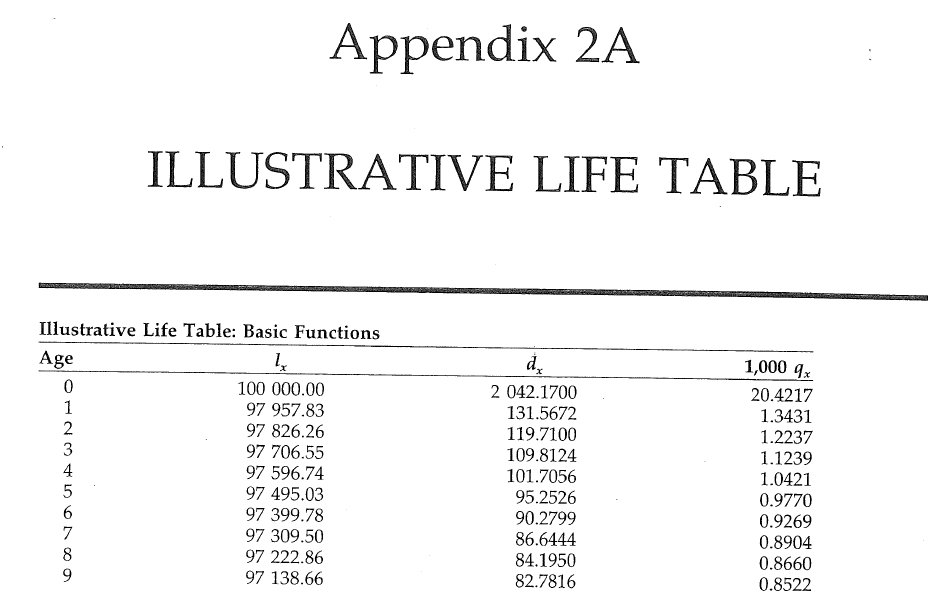

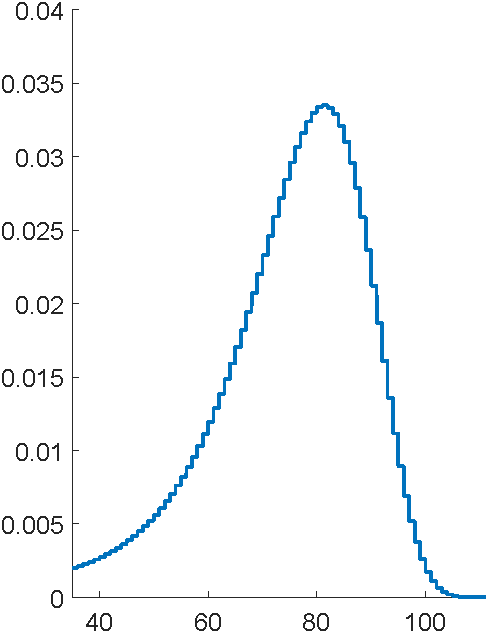

Problem: to model mortality via phase-type

Bowers et al (1997), Actuarial Mathematics, 2nd Edition

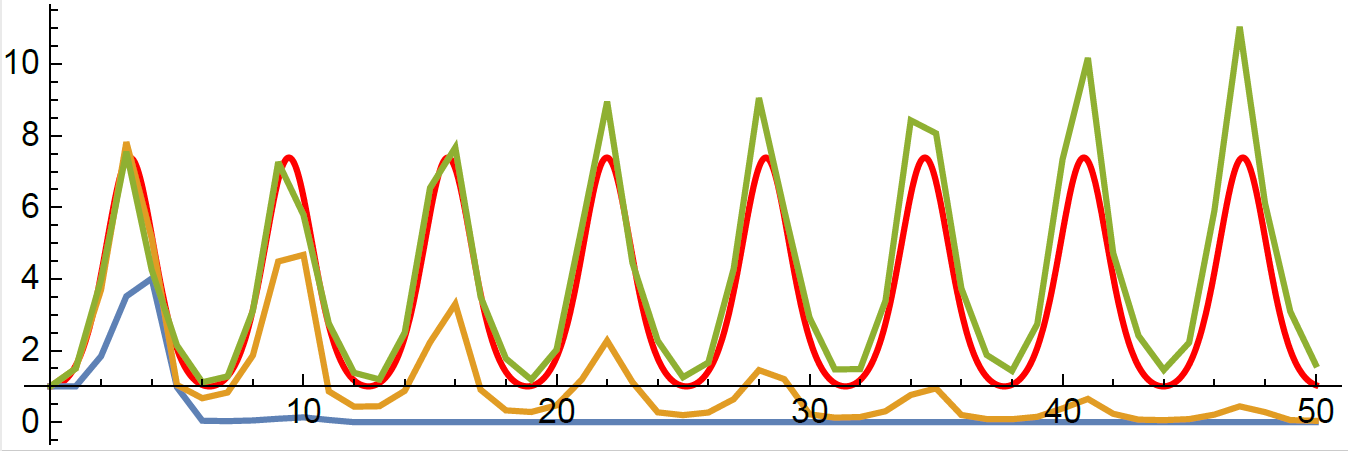

Fit General Phase-type

Representation is not unique

Also, not easy to tell if any parameters produce a valid distribution

Lots of parameters to fit

- General

- Coxian distribution

Fit Coxian distributions

General vs Coxian

Rewrite in Julia

void rungekutta(int p, double *avector, double *gvector, double *bvector,

double **cmatrix, double dt, double h, double **T, double *t,

double **ka, double **kg, double **kb, double ***kc)

{

int i, j, k, m;

double eps, h2, sum;

i = dt/h;

h2 = dt/(i+1);

init_matrix(ka, 4, p);

init_matrix(kb, 4, p);

init_3dimmatrix(kc, 4, p, p);

if (kg != NULL)

init_matrix(kg, 4, p);

...

for (i=0; i < p; i++) {

avector[i] += (ka[0][i]+2*ka[1][i]+2*ka[2][i]+ka[3][i])/6;

bvector[i] += (kb[0][i]+2*kb[1][i]+2*kb[2][i]+kb[3][i])/6;

for (j=0; j < p; j++)

cmatrix[i][j] +=(kc[0][i][j]+2*kc[1][i][j]+2*kc[2][i][j]+kc[3][i][j])/6;

}

}

}

This function: 116 lines of C, built-in to Julia

Whole program: 1700 lines of C, 300 lines of Julia

# Run the ODE solver.

u0 = zeros(p*p)

pf = ParameterizedFunction(ode_observations!, fit)

prob = ODEProblem(pf, u0, (0.0, maximum(s.obs)))

sol = solve(prob, OwrenZen5())https://github.com/Pat-Laub/EMpht.jl

DE solver going negative

Coxian with uniformization

A twist on the Coxian form

Canonical form 1

Et voilà

using Pkg; Pkg.add("EMpht")

using EMpht

lt = EMpht.parse_settings("life_table.json")[1]

phCF200 = empht(lt, p=200, ph_structure="CanonicalForm1")How to fit them?

Observations:

Derivatives??

How to fit them?

Hidden values:

\(B_i\) number of MC's starting in state \(i\)

\(Z_i\) total time spend in state \(i\)

\(N_{ij}\) number of transitions from state \(i\) to \(j\)

Fitting with hidden data

EM algorithm

Latent values:

\(B_i\) number of MC's starting in state \(i\)

\(Z_i\) total time spend in state \(i\)

\(N_{ij}\) number of transitions from state \(i\) to \(j\)

- Guess \( (\boldsymbol{\alpha}^{(0)}, \boldsymbol{T}^{(0)} )\)

- Iterate \(t = 0,\dots\)

- E-step

- M-step

EM algorithm:

Questions?

https://slides.com/plaub/phase-type-lecture