Blockchain Disruption and Smart Contracts

paper by William Cong and Zhiguo He

discussion by Andreas Park

2018 American Economic Association Meeting in Philadelphia

Research question:

How do

blockchain-registered

smart contracts

affect economic interactions?

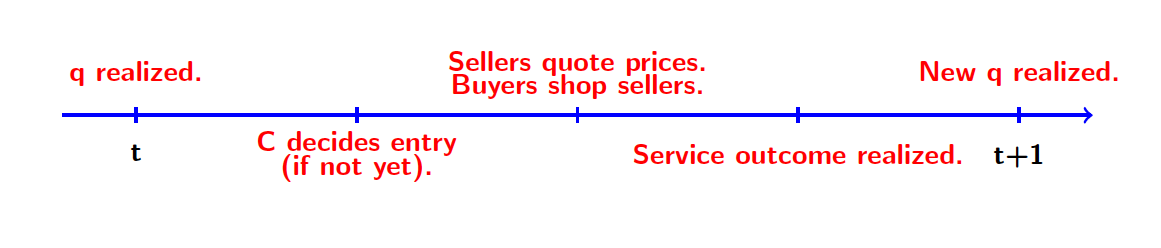

Basic Setup

- suppliers post prices via smart contracts

- customers arrive and transact/place order

- blockchain verifiers confirm delivery and record transaction

- smart contract: delivery-contingent payment => trust for unknown entrant

- blockchain: observing competitors activities => collusion easier

Results

Economic Insights/Mechanism

- blockchain = escrow/trusted party

- blockchain changes information environment

Model Mechanism Review (simplified):

no blockchain = benchmark

- no verification => no entry

- incumbents play a la Green & Porter (ECTA 1984)

- dynamic game with imperfect monitoring

- tacit collusion on price-gauging

- deviations from price-gauging get punished

-

sometimes punishment unnecessary/inefficient

- A had no customers not because B cheated

- but because there were no customers

Model with Blockchain and smart contract

Idea

- supplier is unknown/new

- may not deliver a product

- => pay for nothing

- if consumers believe that new entrant may be unreliable:

- => no entry.

Role of blockchain: escrow account that releases payment upon delivery confirmation

Model Mechanism Review (simplified):

with blockchain

- with verification => entry happens (if entrant is competitive)

-

activities/transactions are recorded on/visible through the blockchain and they are visible to suppliers

- improved monitoring

- more tacit collusion

- no inefficient punishments

- improved monitoring

Welfare Results (simplified):

with blockchain

- entry => average quality higher

- 2 incumbents only: tacit collusion space expands

-

2 incumbents + entrant: when collusion possible

- any collusion equilibrium has surplus < any eq. from traditional world

- exist equilibria with surplus >,=,< any eq. from traditional world

Comment: What is the right benchmark?

But: there are other established market solutions!

- intermediaries or escrows

- e.g., marketplaces as certifiers such as Amazon, Apple's App store

Currently:

- w/o blockchain = no verification

- w blockchain = verification

Why not:

- intermediary verifies vs.

- blockchain verifies

Why important?

- getting info from outside on the blockchain is a hard problem

- requires essentially trusted third party

Comment: is entry vs collusion the key trade-off when thinking about blockchain-registered smart contracts?

- Main message: blockchain presents trade-off

- verification => trust => entry (good)

- visible activities => better monitoring => more collusion (bad).

- Applicability and assessment of surplus trade-offs depend on choice of benchmark.

- Delivery verification can obtain with intermediaries

- => Key feature of blockchain is non-intermediated decentralized interaction

Comment 1: Key question reg. smart contracts in this setting is/should be the trade-off that non-intermediated decentralized interactions bring.

Model Ingredient Review (simplified): product market

what are the buyers' decision rules?

what's the role of qualities? why needed?

how do I interpret this in finance?

for most of the paper: truthful verification

Model Ingredient Review (simplified): verifiers

- Four items of interest:

- the truth: w

- the info about w: x

- the vote on w: y

- the bias in the vote

-

Q: How do we interpret a bias?

- For price quotes that are fed by an oracle?

- For UPS delivery information?

Comment 2 (part 1): the main results in the paper don't use the verifier and instead assume perfect revelation.

Review of model extensions

- imperfect consensus may still lead to entry (unless bias is large)

- privately observed quality can be included

- only these two extensions exploit the lengthy consensus modelling and the qualities

Comment 2 (part 2): These results have an appendix-like/robustness-check feel. Why not simplify the model and shift all the complex material to an online appendix?

Broader Thoughts

- Collusion (or accusation thereof) is a genuine concern

- highlighted in Bank of Canada's Jasper II experiment.

- In practice, tacit collusion is difficult to establish, in particular with many players

- competitors have an interest to be able to plausibly deny collusion

- => can they take active steps to create plausible deniability?

- state channels, multi-IDs, or Zk-snarks?

- Paper does talk about the design: permissioned vs. public (Sec 4.3 vs 4.4), regulatory nodes, who sees what (Sec 5.1), but the discussion is dispersed throughout the paper.

Comment 3: Does the paper address a question on blockchain design question? If so, organize the paper as such.

Conclusion

- Blockchain:

- decentralized ledger that allows peer-to-peer transfers of value

- smart contracts on blockchain

- automated execution of contracts with verifiable parameters

-

This paper:

- smart contracts expand the contracting space relative to world without any verification

-

blockchains change the information environment and affect behavior

- follows Yermack (2016) and Malinova & Park (2016).

Summary Main Comments

- Welfare/surplus results depend on benchmark

- IMO,more suitable benchmark would be setting with intermediary

- should bring out trade-off from core blockchain feature (= enabling non-intermediated transactions)

- Many model ingredients aren't used except for results with appendix-feel

- If there is a market design question, need to bring it out clearer.