Crypto-Economics, Blockchains, and Tokenomics

based on a paper by Katya Malinova and Andreas Park

Cumulative sales since Jan 2016

Data: coinschedule

$25B total

$21B in 2018

for comparison: total size of

-

Toronto Stock Exchange: $2,200B

-

Toronto Venture Exchange: $41B

Why bother with Tokenomics?

Some spectacular returns

Source: Tokendata

Why bother with Tokenomics?

What is a token?

A taxonomy of coins vs tokens

Coin

Token

-

native to a blockchain for payment

-

examples: Bitcoin, Bitcoin Cash, Ether, Lumens, Cardano

- build on top of or linked to an existing blockchain

- various uses, not just payments

Payment

Utility

Security

Stable coins

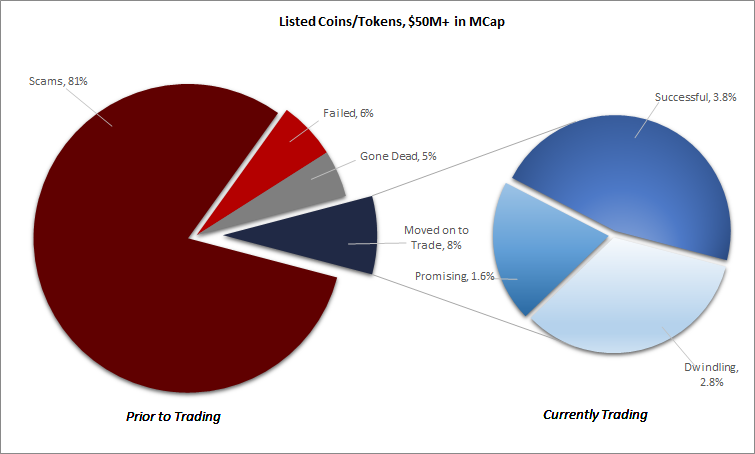

The Ugly Truth: Scams

Source: Satis Group LLC

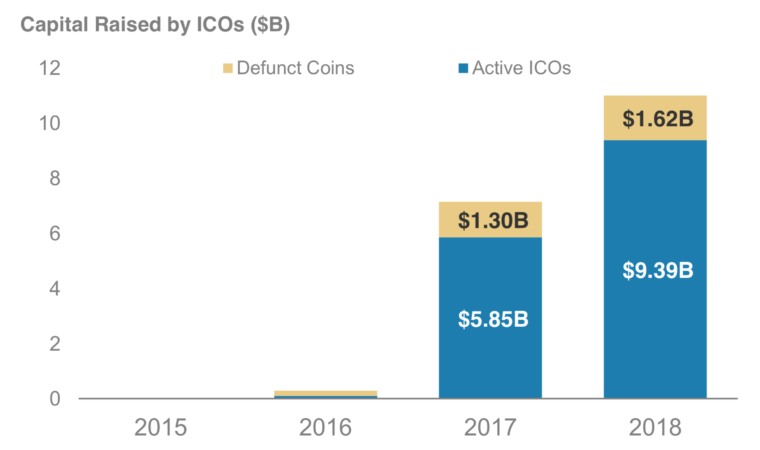

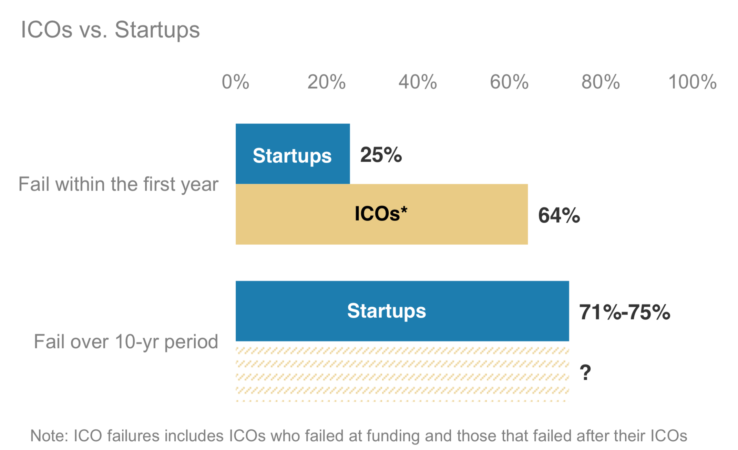

The Ugly Truth: Failure Rate

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

Source: Tokendata

Why bother with Tokenomics?

Also: a real horrow show

Key: you cannot collect money from just anybody!

The Ugly Truth: Many tokens are securities

Key Challenges for the Blockchain/Crypto Community for 2019

Technology

Legal/Regulation

Economic functions

Key Technology Questions for Blockchain Design

interoperability

cybersecurity and privacy

functionality

scalability

smart contract features and verification

recently and unexpectedly: finality

Key Economic Questions for Blockchain Design

-

system governance

-

political economy

-

-

contract/token design

-

corporate finance

-

-

How does platform payment interactions with outside world

-

open-economy macro

-

-

How much do we have to pay operators to maintain the chain?

-

mechanism design

-

Three Fallacies for Crypto Markets

crypto assets = traditional equities

crypto trading = traditional trading

crypto entities = traditional firms

My beef with the non-crypto world

State of the Debate on Tokens

Is there economic merit to tokens?

Do tokens solve an economic problem?

price

An Economic Model of ICO

- entrepreneur wants to produce a good or service

- Demand is uncertain and only revealed after production.

- \(\Rightarrow\) maximizes monopoly profits

demand

marginal cost

marginal revenue

ICO/Token Financing

general idea: sell future output

two approaches for token sales

- sell a fraction of future revenue

- = revenue sharing

- sell units of future output

- = output presale

price

demand

marginal cost

marginal revenue

Revenue Sharing

\(\Rightarrow\) shifts marginal revenue for entrepreneuer left because get only fraction of revenue

Result: underproduction

NB: Chod and Lyandres (2018) have the same result

price

demand

marginal cost

marginal revenue

Output presale

Entrepreneur does not internalize that extra output unit affects revenue for tokenholders!

Result: overproduction

Is token financing inferior?

- revenue sharing: underproduction

- output presale: overproduction

\(c\)

\(MR\)

- "does not internalize" = externality

- address externality: TAX!

- here: tax future token income

- incremental token income gets shared

- obvious answer: combine the two!

- issue \(t\) tokens ex ante

- share \(\alpha_t\) of new tokens

- token share \[\alpha_t=\frac{t}{c+t}\]

Token financing is NOT inferior!

ICO/Token Financing

general idea: sell future output

two approaches for token sales

- sell a fraction of future revenue

- = revenue sharing

- sell units of future output

- = output presale

Problem: leads to overinvestment

But: if you first pre-sell and then share revenue, then tokens are economically superior to equity financing

Problem: leads to underinvestment

ICOs with Moral Hazard

Common result in the literature: only debt guarantees effort

Idea: entrepreneur can influence expected demand with "effort"

effort is costly

- common topic in corporate finance

- very relevant in "decentralized" world where developers are scattered around the globe

- also applicable to, e.g. established firms that do something new

Is it worth it for the entrepreneur?

Optimal contract looks like debt:

- get nothing if demand is low (only original tokenholders get anything)

- benefit if demand is high

Formal result

- With moral hazard,

- all projects that can be financed by equity can be financed by the optimal token contract but

- some projects that can be financed by optimal tokens contracts cannot be financed by equity.

Superiority of Token over Equity Financing

Summary

- Simple model of ICO vs equity financing from the standard corporate finance toolbox

- Theorem 1: Without frictions,

- an optimal token contract finances the same projects as equity

- the entrepreneur earns the same rents under the optimal token contract

- Theorem 2: With entrepreneurial moral hazard,

- any equity-financeable project can be financed by an optimal token

- some token-financeable projects cannot be financed by equity

- \(\Rightarrow\) There is economic and conceptual merit to token financing

The Problem: Crypto-Schizophrenia

libertarian view of markets & regulation

rejection of economics and finance

My beef with the crypto community

blockchain

=

technology + economics

Hiccups vs. End-games

Feb 2000

Aug 2014

Nasdaq recovered ...

Hiccups vs. End-games

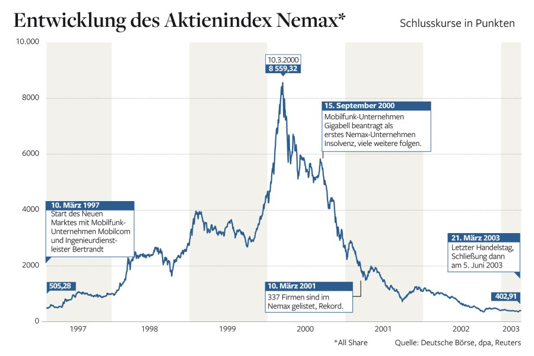

The German "New Market" did not - it closed for good

Summary for Future of Blockchain

blockchain only useful with applications

applications require (tech + economics) + business

understanding of economics on blockchain requires development

our paper: \(\exists\) real economic value in tokens, when used properly

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/