Blockchain

Technology

Andreas Park

Part 3: Coins, Tokens, and Other Finance Applications

Cumulative sales since Jan 2016

Data: coinschedule

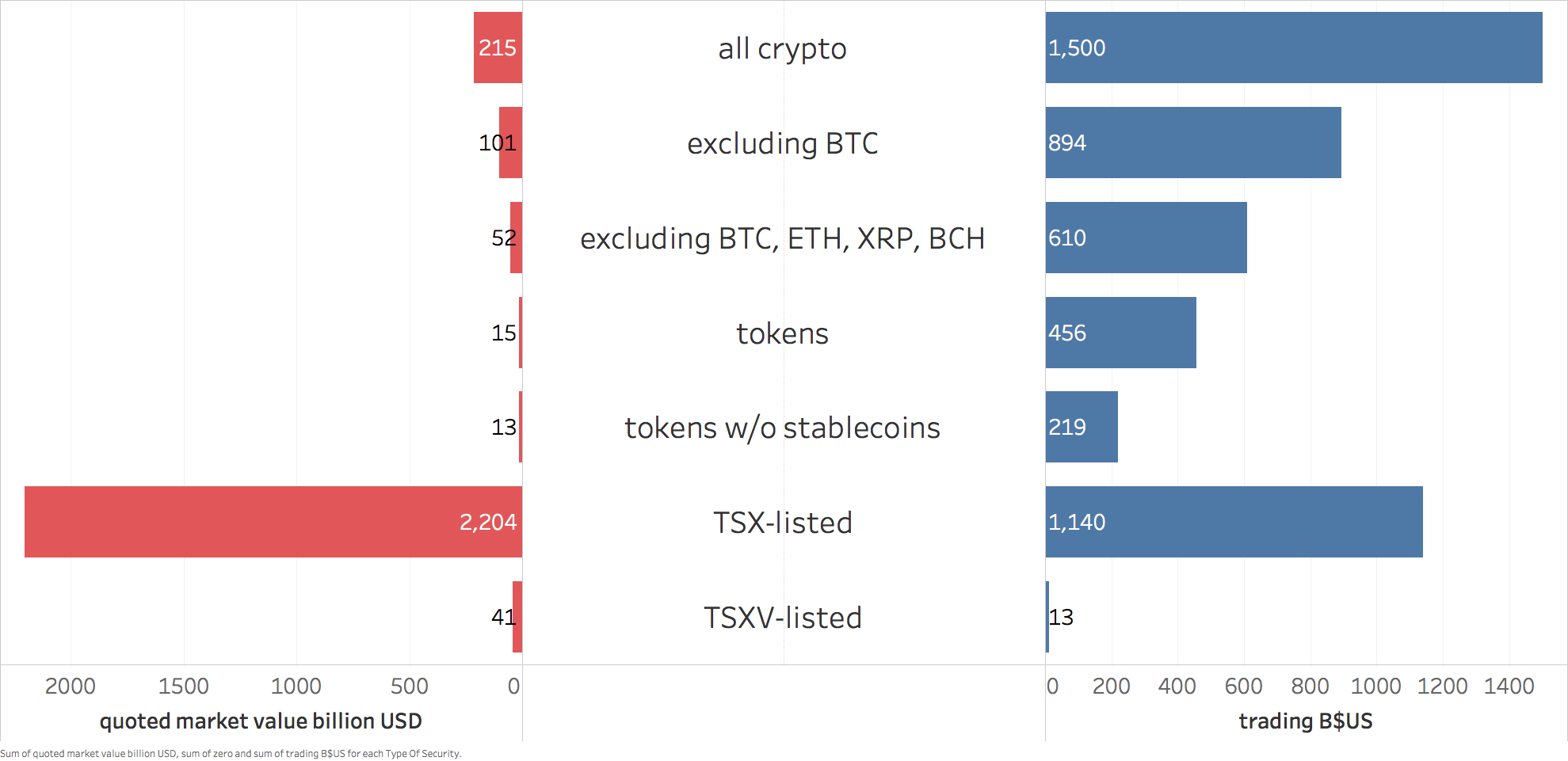

$25B total

$21B in 2018

for comparison: total size of

-

Toronto Stock Exchange: $2,200B

-

Toronto Venture Exchange: $41B

Why bother with Tokenomics?

from Forbes

Azure Blockchain Tokens [...] lets enterprises, or anyone really, design, issue and manage a wide range of assets,

Currently, the platform is a permissioned version of the ethereum blockchain that uses Microsoft’s Azure cloud computing.

In the future Azure Blockchain Tokens will interact with the public Ethereum blockchain or even at distributed ledgers created by some of Microsoft’s own competitors.

Some spectacular returns

Source: Tokendata

Why bother with Tokenomics?

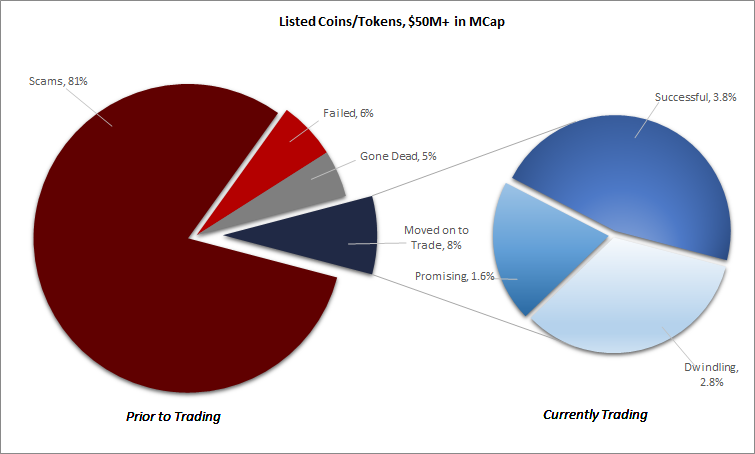

The Ugly Truth: Scams

Source: Satis Group LLC

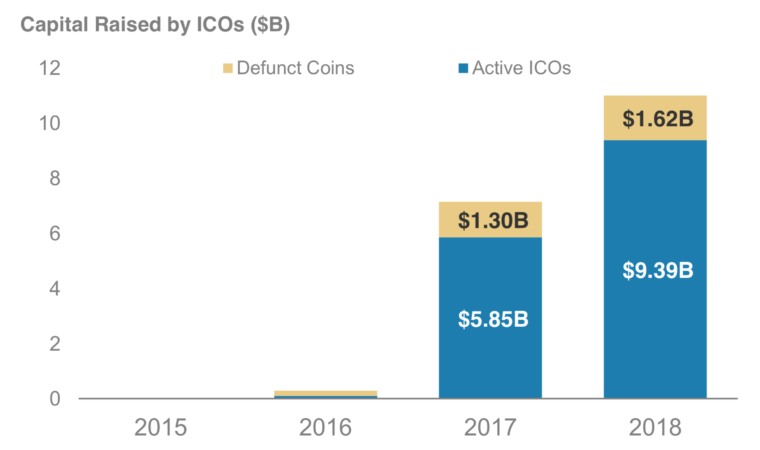

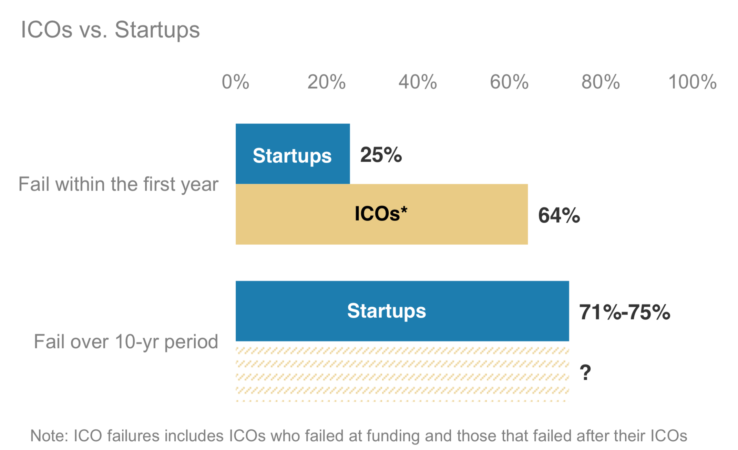

The Ugly Truth: Failure Rate

Source: Morgan Stanley (Nov 2018) “Update: Bitcoin, Cryptocurrencies and Blockchain”

Source: Tokendata

Why bother with Tokenomics?

Also: a real horrow show

Key: you cannot collect money from just anybody!

The Ugly Truth: Many tokens are securities

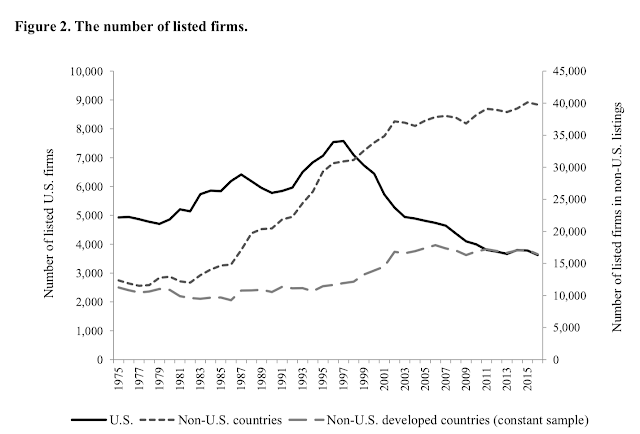

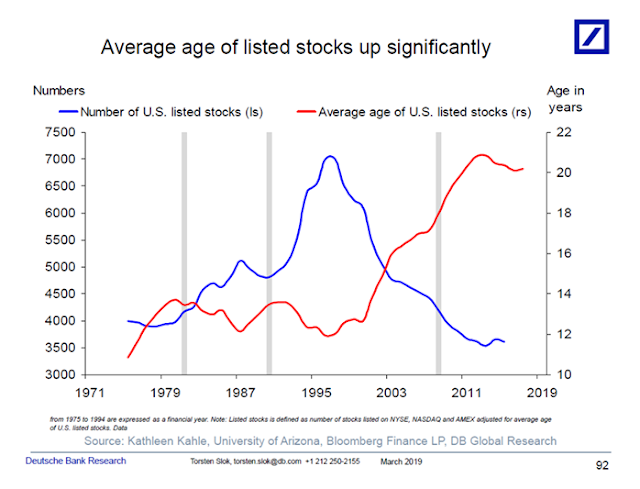

Small aside: public US markets are ailing

"Eclipse of the Public Corporation or Eclipse of the Public Markets?" by Craig Doidge, Kathleen M. Kahle, G. Andrew Karolyi, and René M. Stulz

Three Fallacies for Crypto Economics

crypto assets = traditional equities

crypto trading = traditional trading

crypto entities = traditional firms

Crypto

Exchange

Traditional

Internalizer

Wholeseller

Darkpool

Investor

Venue

Broker

Settlement

Investor

Venue

Settlement

On chain

Concerns

arbitrage requires capital commitment => expensive

exchanges = brokers? => single point of failure

decentralized: totally anonymous => easy price manipulation (e.g. wash trades)

Spirit of Blockchain: Fully decentralized

... 300 lines of code ...

standard trading rules practically impossible to enforce

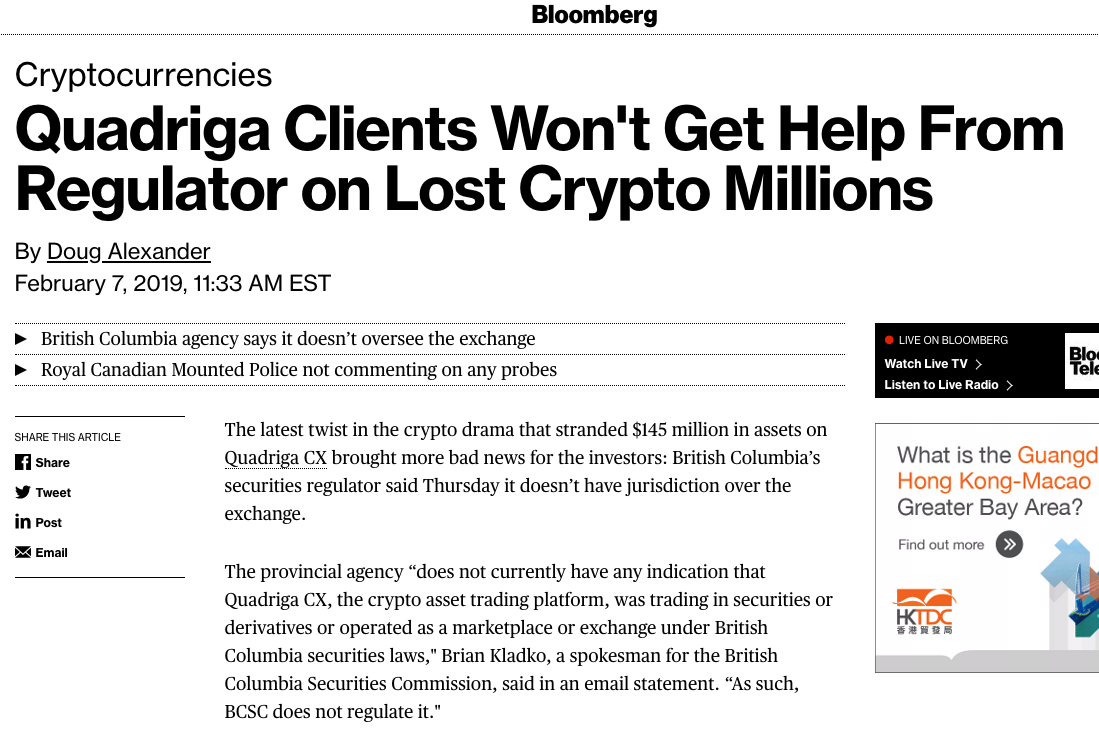

Crypto exchanges are a security risk

August 2016

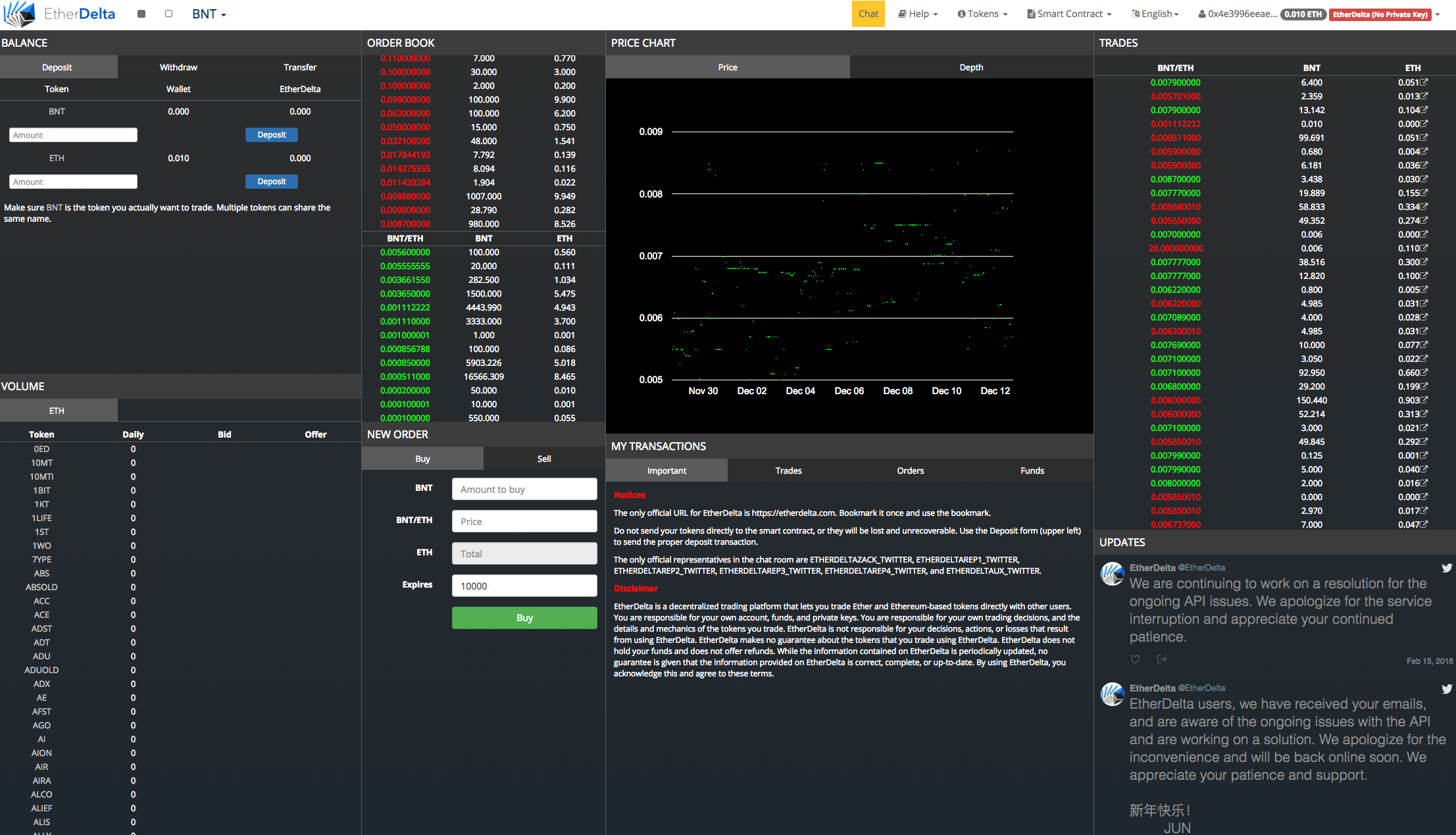

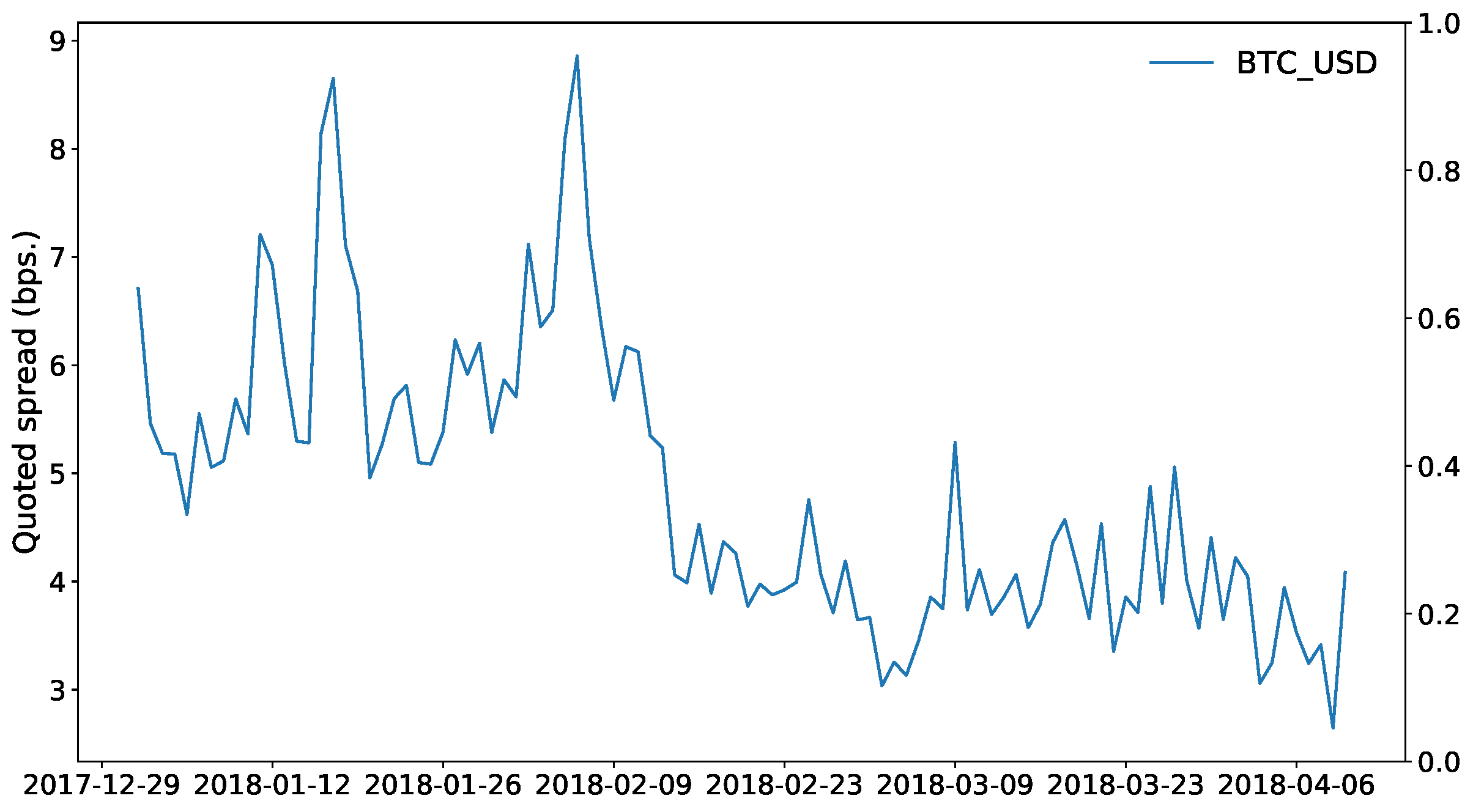

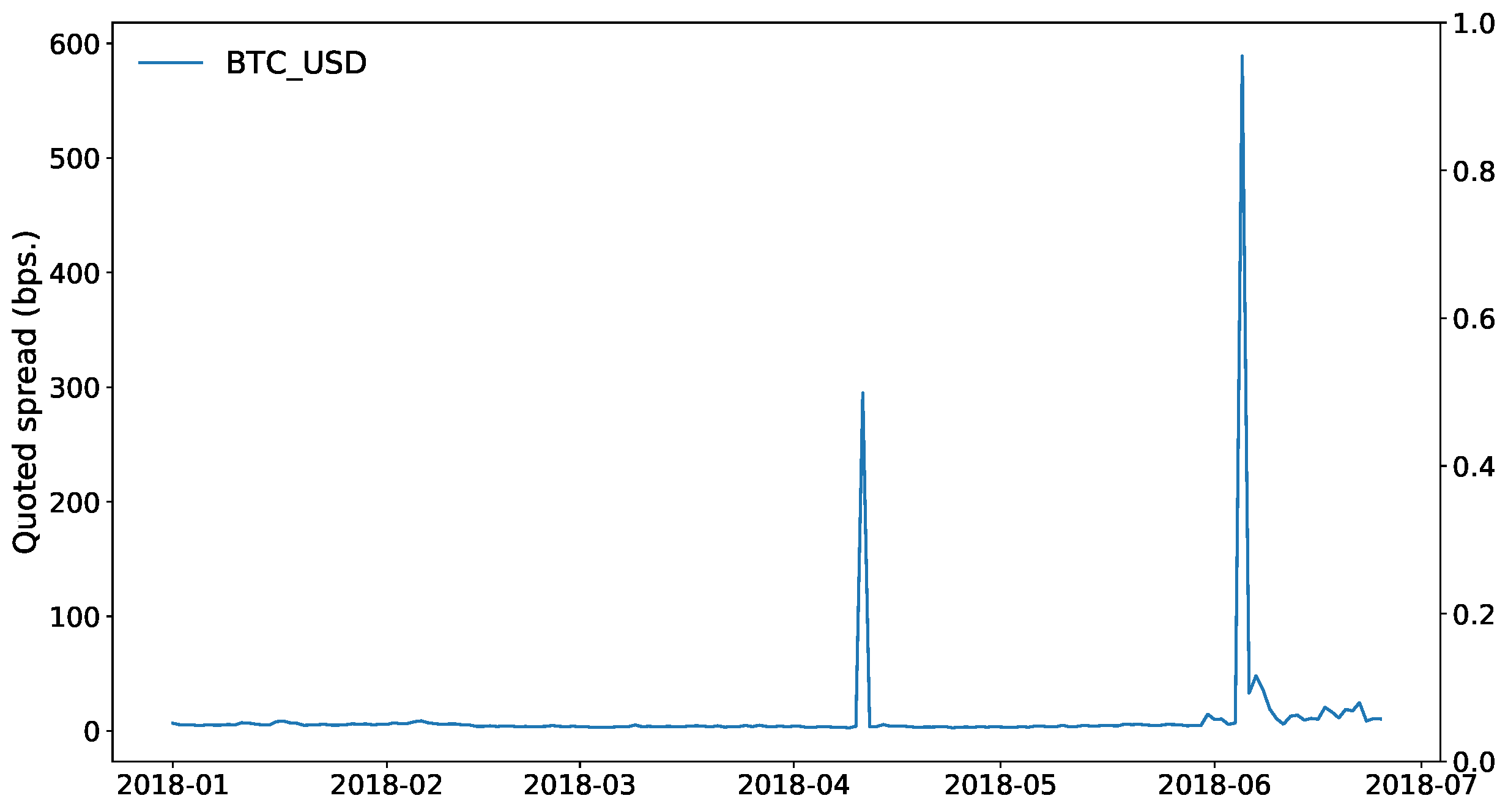

Some trading data

based on Khapko, Malinova, Park, and Zoican (2018)

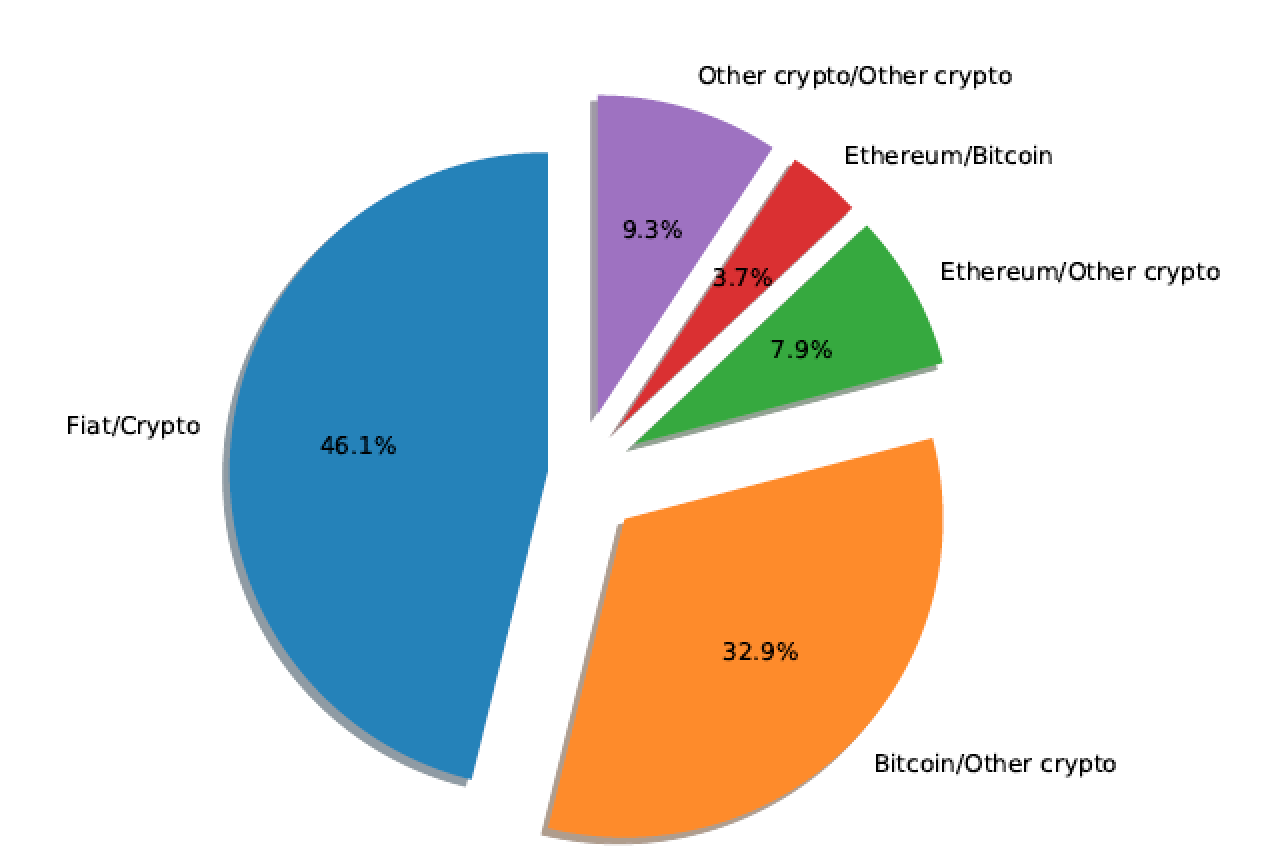

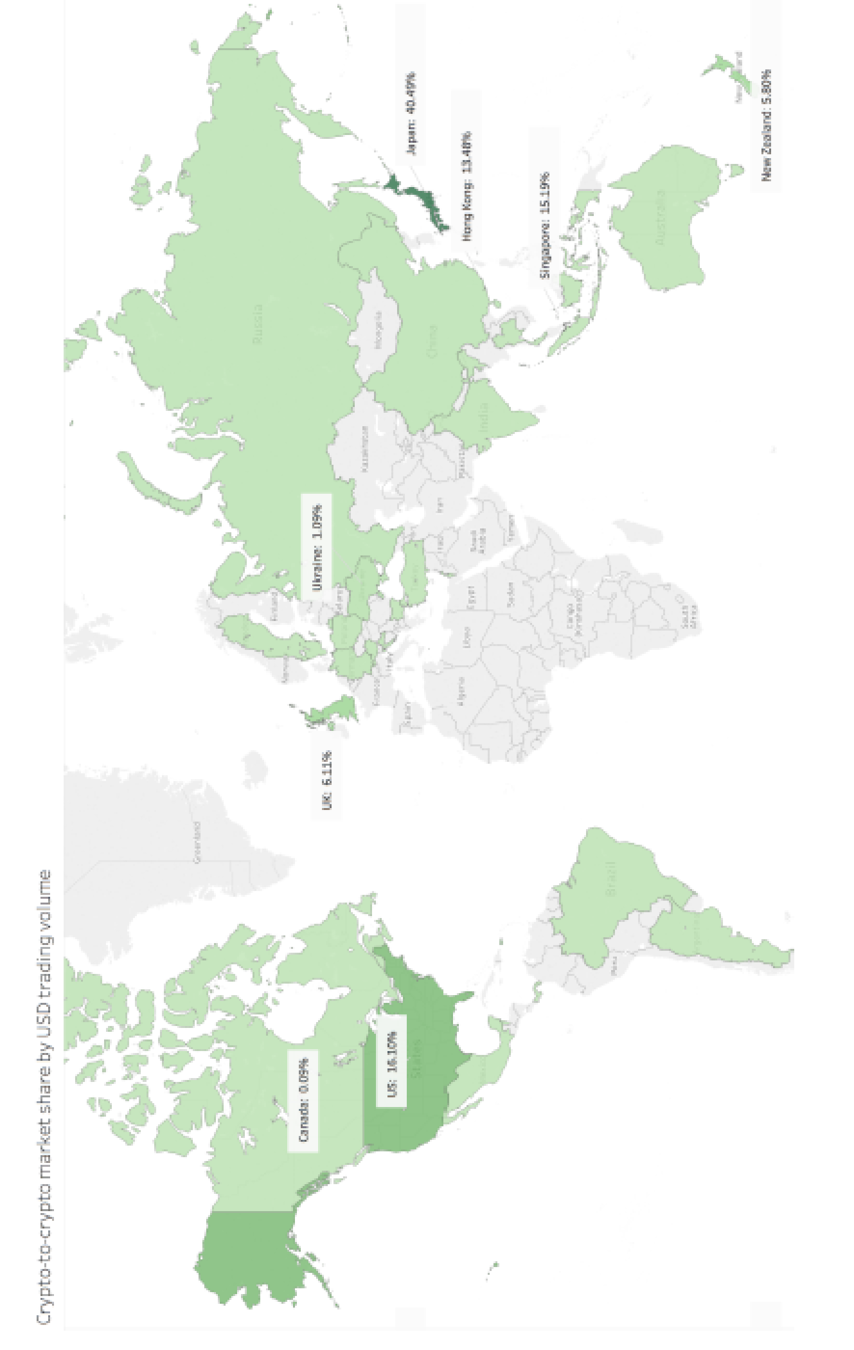

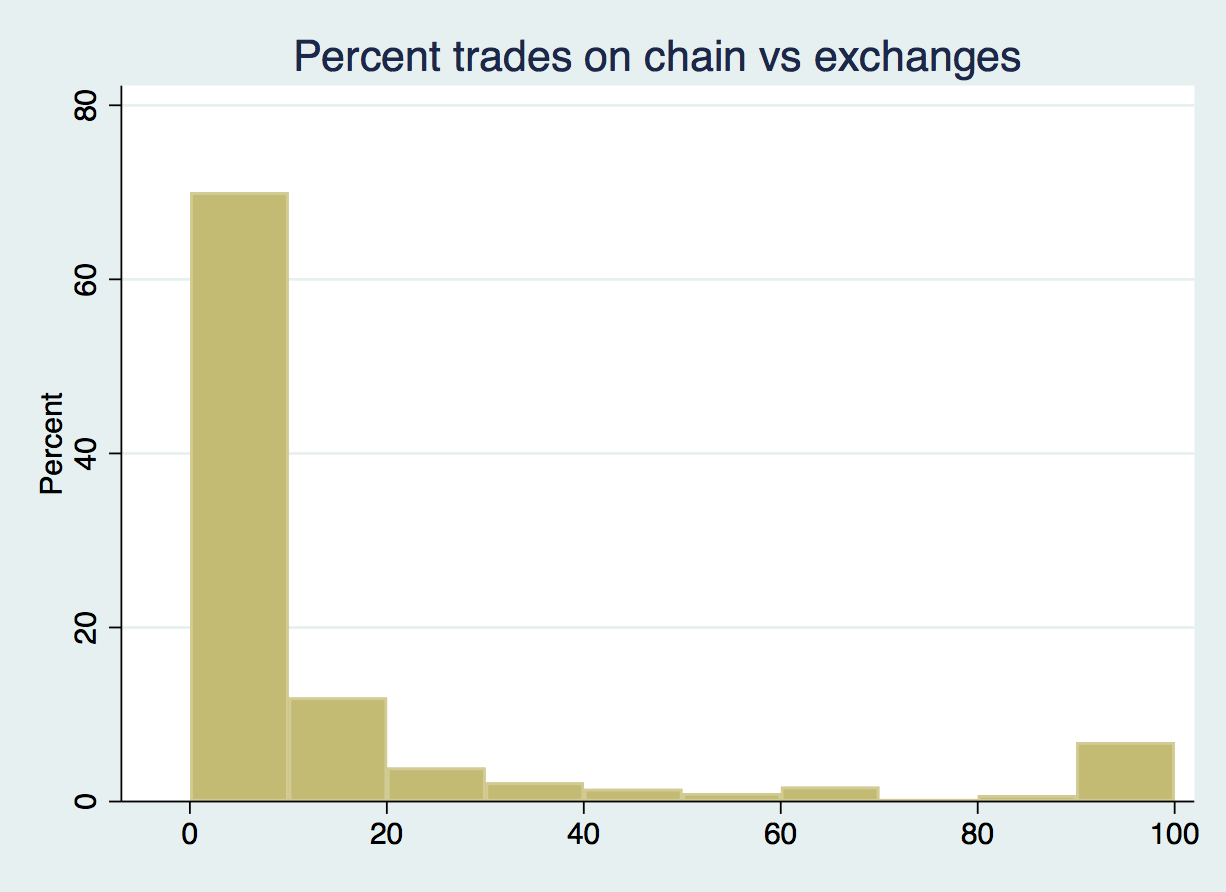

Where does trading take place?

Distribution of changes in beneficiary ownership

most tokens stay at exchanges and don't get settled on the blockchain

some usage tokens are "in use"

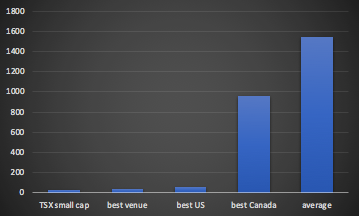

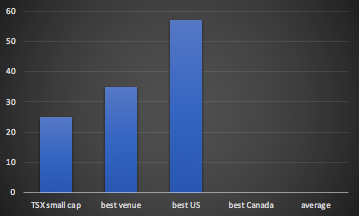

Compare Market Value vs Trading Crypto to TSX

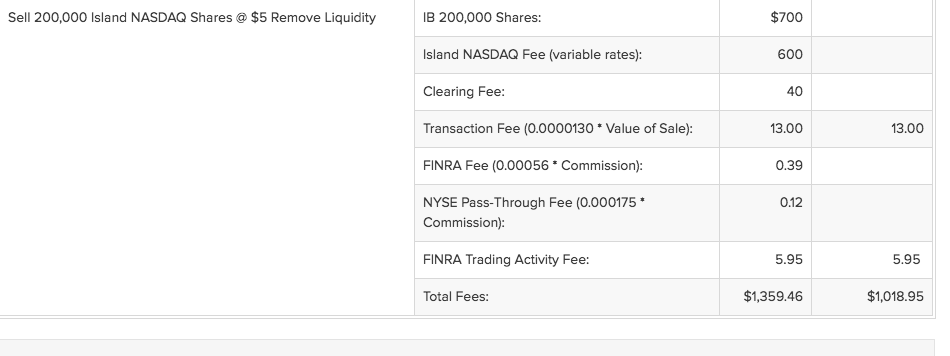

Transactions costs

Source: Interactive Brokers

Broker

Level

crypto exchange fees for $1,000,000 market order

account

wire/in-out

-

25 bps = 2,500 trading fee

-

in/out fee 0.1% - 3%

-

mining fee ($0.25)

Transactions costs

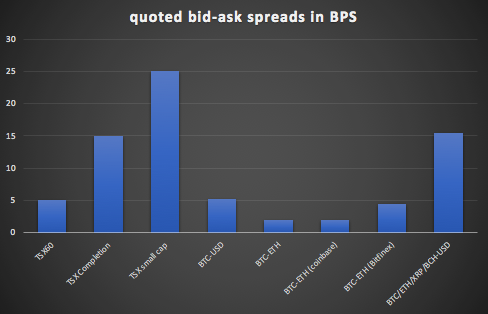

Bid-ask spreads

Transactions costs TOKENs

Summary: Crypto Trading

exchanges = brokers

exchanges = security risk

high exchange fees

tokens: large spreads

very active market

trading rules? => info(price)

decentralized trading possible and happening

What is a token?

Curious case of a utility token: KIN

- comments: from Raquel Jackson on Medium

- "Everything KIK wants to do can be accomplished with fiat currency or a simple payment integration with their app."

Do people understand utility tokens?

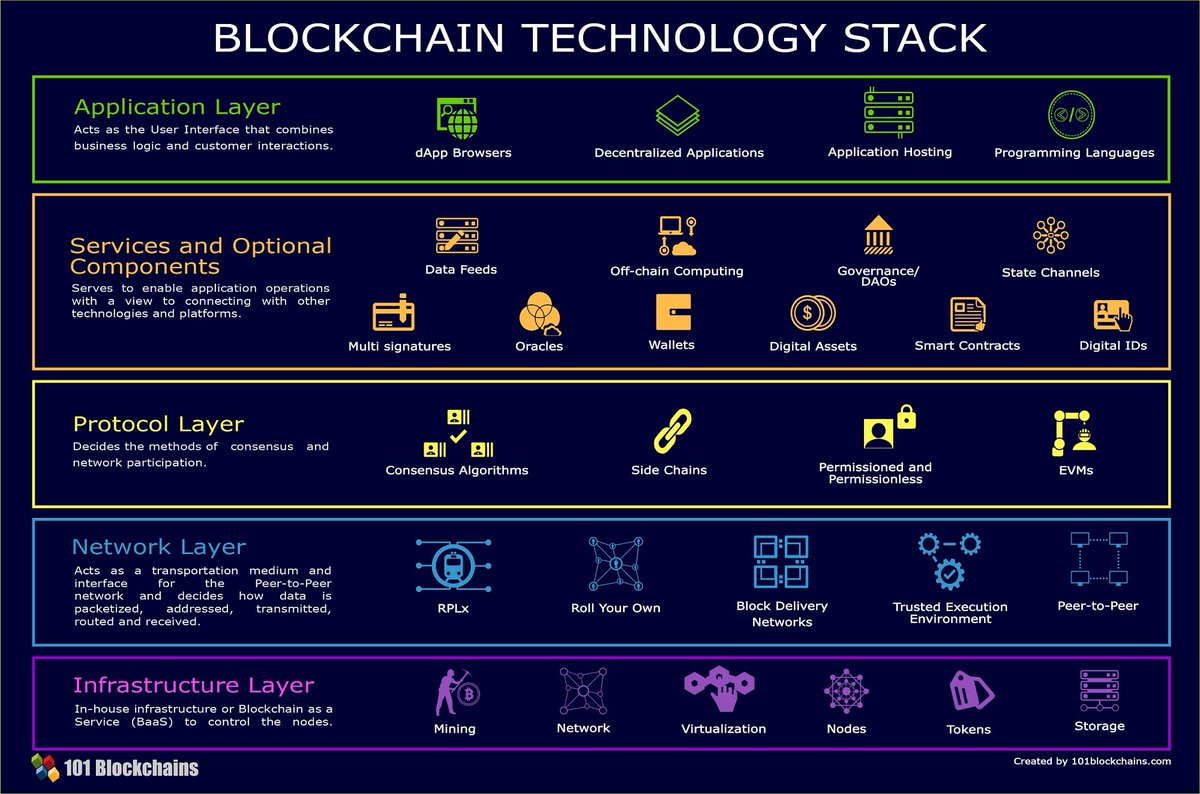

Blockchain Technology and Activity Layers

Infrastructure

Services

Network

Protocol

Application

dApps, application hosting, programming languages, browsers

oracles, wallets, smart contracts, digiIDs

consensus protocols,

sidechains

block delivery,

peer-to-peer

mining,

nodes

A taxonomy by function

-

native to a blockchain for payment

-

examples: Bitcoin, Bitcoin Cash, Ether, Lumens, Cardano

- build on top of or linked to an existing blockchain

- various uses, not just payments

Crypto-currency

link to on-chain activities

link to off-chain activities or assets

Stable coins

- blockchain is a value transfer infrastructure

- claims to revenues, cash flows, assets (e.g. real estate)

Cryptocurrencies

coinbase reward to miners

creation and redemption process as part of blockchain operation

examples: Bitcoin, Bitcoin Cash, Ether, Lumens, Cardano

native to a blockchain and essential for operation

Coins vs Tokens

- equity=ownership

- call option on company

- residual claim to all future cash flows (after debt an tax)

- => present value of future cash flows

\[\text{Fundamental Value}= \sum_{t=1}^\infty \frac{E(\text{cash flow}_t)}{(1+r)^t}.\]

- tricky stuff:

- forming expectations => estimating cash flows

- finding the right discount rate \(r\).

What is a stock and what is its value?

Money vs Financing

Time for some economics: systematic approach

- means of payment & mining reward

- value? => similar to fiat

- convenience

- cost of storage

- risk of loss

- volatility relative to usage need

- inflation and monetary policy vis-a-vis alternatives

What is a coin?

Time for some economics: systematic approach

- example of a model:

- Biais, Bisiere, Bouvard, Cadamatta, Menkveld (Oct 2018)

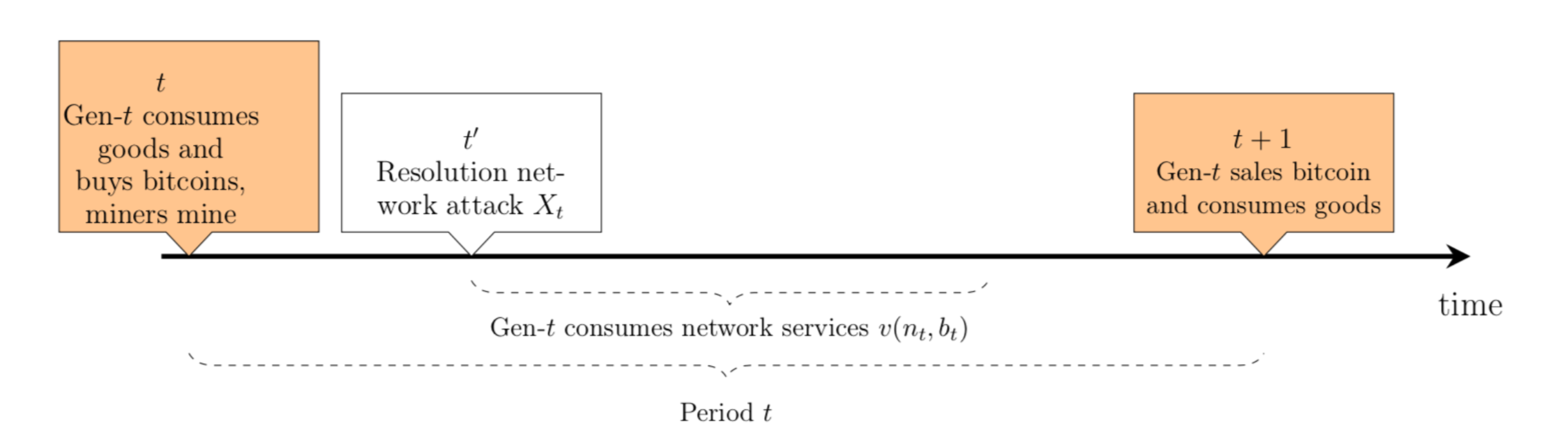

- Overlapping generations model of young and old investors who must push money across time to finance consumption

- three assets:

- cryptocurrency \(X_t\), fiat currency, risk free asset

- Miners mine at \(t\) and receive \(X_{t+1}-X_t\).

- Young have

- \(e_t\) of consumption good

- can buy \(q^c\) of crypto at price \(p^c_t \) and \(q^f\) of fiat at price \(p^f_t,\) rest \(s\) is saved.

- crypto involved mining fees \(F\)

- crypto has transaction benefits in the future \(\theta q^c p^c_{t+1}\)

What is a coin?

- consumption

- \(c^y=e_t-s-q^cp^c_t-q^fp^f_t-F(q^c)\)

- \(c^o=s(1+r)+q^cp^c_{t+1}+q^fp^f_{t+1}\)

- Young optimize

\[\max_{q^c,q^f,s}u(c_t)+\beta Eu(u_{t+1})\]

- Price for crypto must satisfy

\[p^c=\beta E\left[\frac{u'(c^o)}{u'(c^y)}\times\frac{1+\theta}{1+F'(X_t)}\times p^c_{t+1}\right].\]

Time for some economics: systematic approach

What is a coin?

- Define convenience yield \(T\) as \[1+T=\frac{1+\theta}{1+F'}\]

- transactional benefit \(\theta\) net of transactions costs \(F'\)

- The FOC w.r.t. savings (to get the relation of the discount rate and the interest rate) gives

-

\[\beta=\frac{1}{1+r}\frac{u'(c^o)}{Eu'(c^y)}.\]

- Then the price must satisfy

-

\[p^c=\frac{1}{1+r}E\left(\frac{u'(c^o)}{Eu'(c^y)}p^c_{t+1}(1+T)\right).\]

-

There could be multiple equilibria.

-

Price \(p=0\) at all dates is an equilibrium.

-

Further insights:

-

price of the cryptocurrency at time \(t=\) present value of

the expectation of the product of two terms

-

pricing kernel (captures correlation between marginal utility of consumption and the crypto price).

-

sum of the crypto price at time \(t+1\) and its

convenience yield.

-

-

- Pricing equation is standard and similar as with other assets ( e.g., stocks), except that the third term would be different.

Time for some economics: systematic approach

What is a coin?

-

convenience yield \(=\) scalar \(\times\) crypto price

-

Ceteris paribus \(p^c \nearrow \Rightarrow\) convenience yield \(\nearrow\).

-

Not so for stocks in perfect market

-

stock price at \(t\) reflects the \(E[p_{t+1}+d_{t+1}]\)

-

dividends at \(t+1\) do not depend on the \(t+1\) stock price.

-

\(\Rightarrow\) for stocks, dividends cause fundamental value and therefore prices

-

For the cryptocurrency, prices cause convenience yields

and therefore fundamental value.

-

- Further insights

- interpret convenience \(\theta\) as usefulness in e-commerce or illicit activities

-

Multiplicity: if a price sequence forms equilibrium, then sequence \(\times\) noise term with expectation \(=1\) is also an equilibrium.

-

=>large volatility for cryptocurrency prices!

(Even when fundamentals are not very volatile.)

-

-

large transaction costs for crypto => large expected returns on crypto

-

large benefits from crypto => small expected returns on crypto

-

Interpretation:

-

bitcoin prices reflect future stream of transactional benefits

-

In future, when the transactional services

of bitcoin will have become large, bitcoin prices will have further increased, but equilibrium expected returns will be low.

-

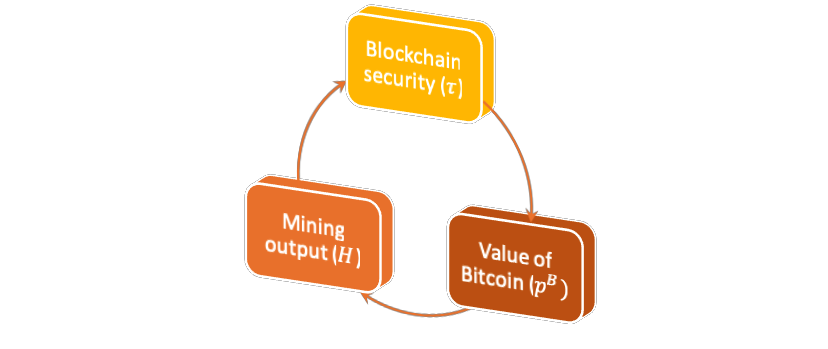

Model II: Emiliano Pagnotta

"Bitcoin as decentralized money"

- equilibrium model of demand and supply for decentralized money

- why hold it?

- transactional services

- and speculative value.

- might increase in value if network increases

- pros and cons of decentralized money

- censorship resistent

- hackable (affects both market value and usefulness)

- network security provided by miners

- enable transactions

- get paid in native currency

Key Concept: Unity

unity: token is means of exchange and incentive for miners

| Network | Multiple verifiers | Free entry for verifiers | Asset | Unity |

|---|---|---|---|---|

| DTCC | n | n | public equity | n |

| Bitcoin | y | y | bitcoin | y |

| Ethereum | y | y | ether | y |

| Ethereum | y | y | ERC-20 tokens | n |

| Ripple | y | n | XRP | n |

Model basics

- long-term miners

- overlapping generations model of users

- enjoy transaction benefits when young and network alive

- attacks may happen

- each period, network may get attacked and disappear

objective function user: \(\max \left(\text{transactional service}+\text{resale value}\right) \times \text{network security} -\text{cost}\)

Miner's problem

- Network security function of hash rate \(\tau\)

- long-term miners

- choose hash rate (at a cost) \(H\)

- get block reward if mining successful

- expected project proportional to hashing power

- don't keep block reward but cash in right away

General Equilibrium

equilibrium price is a function of

- network effects

- risk aversion

- technology

- money supply

- money regime

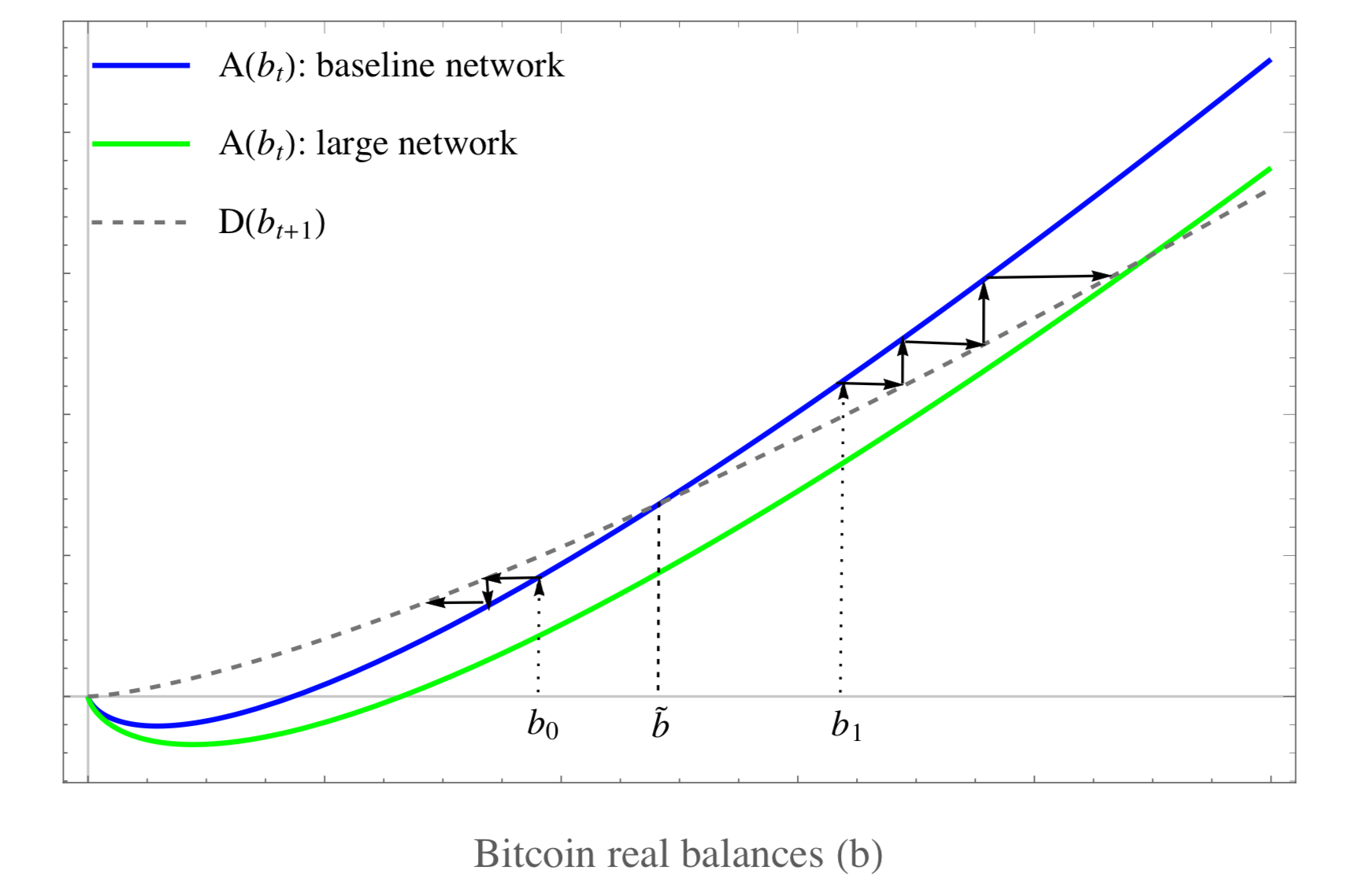

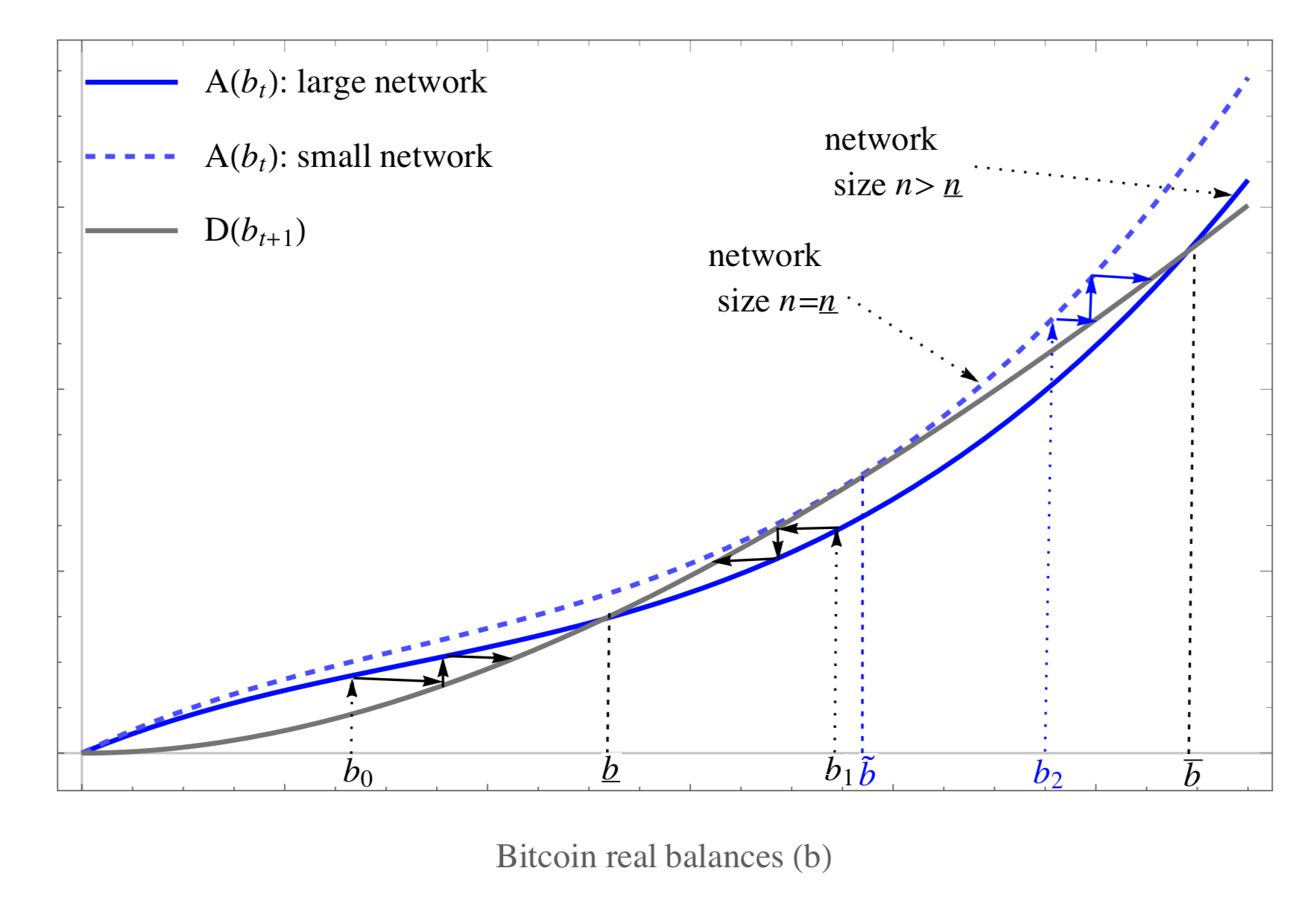

Benchmark: non-unity token

unstable equilibrium

unstable equilibria are also possible with unity tokens

Competitive mining for unity tokens

stable

equilibrium

Note: \(p=0\) is always an equilibrium!

unstable

=smallest network with positive price equilibrium; any smaller network has price=0

Comparative Statics Results

number of miners \(\nearrow\):

-

total hash rate \(\nearrow\)

-

price \(\nearrow\)

number of miners \(\to\infty\):

-

there is a finite limit price

-

there is a well-defined minting price

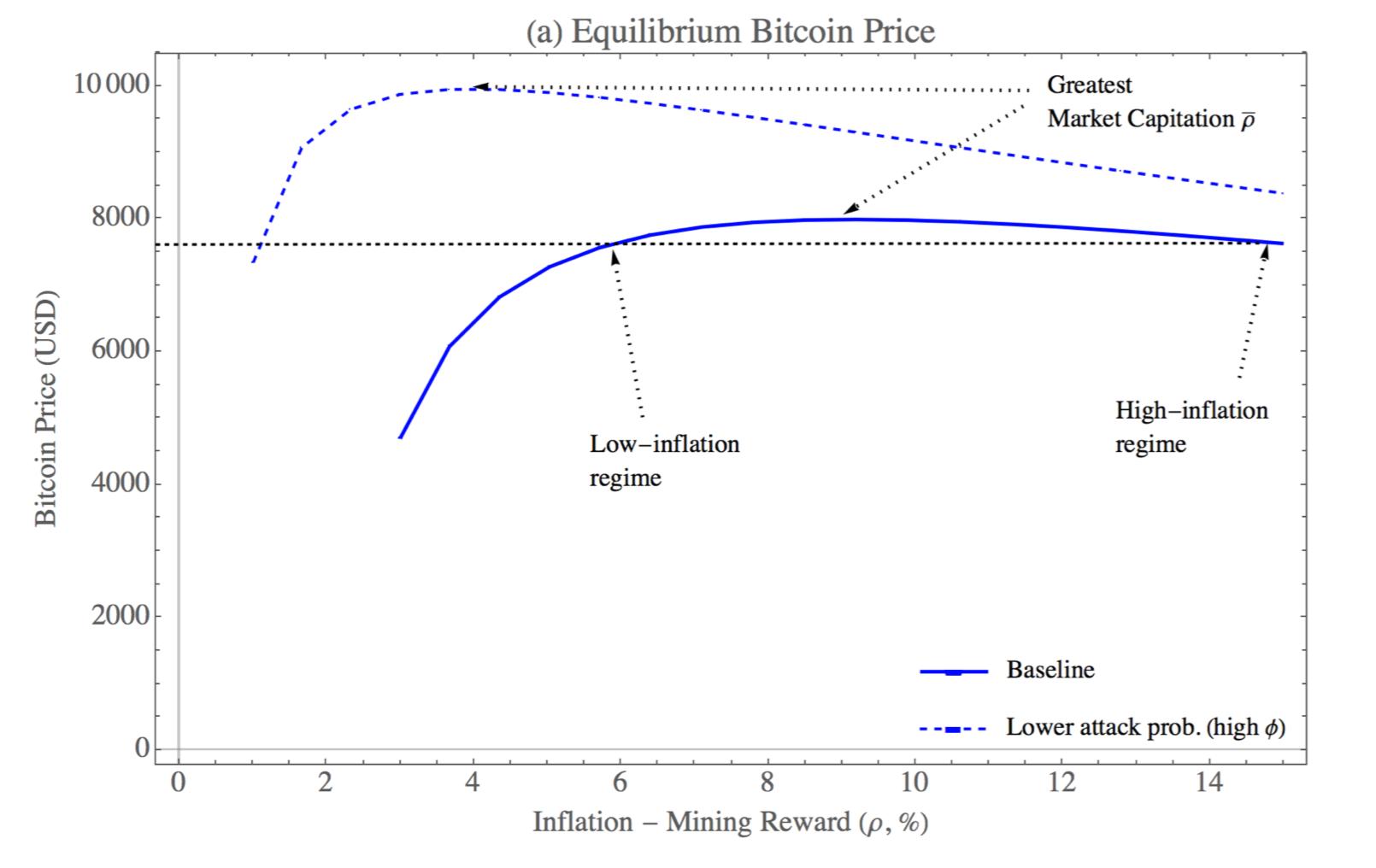

Optimal Monetary Policy

There is a threshold \(\bar{\rho}\) such that:

-

\(\rho<\bar{\rho}\): \(\frac{\partial\text{price}}{\partial\rho}>0\)

-

\(\rho>\bar{\rho}\): \(\frac{\partial\text{price}}{\partial\rho}<0\)

measured in growth rate of coinbase reward \(\rho\)

What is a Stablecoin?

Cryptocurrencies are volatile

- not a good store of value

- not a good means of payment

- => bad as money

Stablecoins try to solve this

- backed by an asset (to ensure confidence)

- pegged to a fiat currency

- available on the blockchain

- Fiat currency is

- a good store of value and

- a good means of payment

- not available on the blockchain

- => can't use it in smart contracts

other solution

- central bank digital currency

- government debt as tokens (in $1 denominations)

- corporate-tokens

BTC, ETH

fiat: USD, EUR

asset (gold)

fee-backed

Seigniorage

Crypto

Traditional

Algorithmic

Collateral-Backed

Taxonomy of Stablecoins

$174M

$33M

$144M

funding figures from Nov 2018; source: blockchain.com

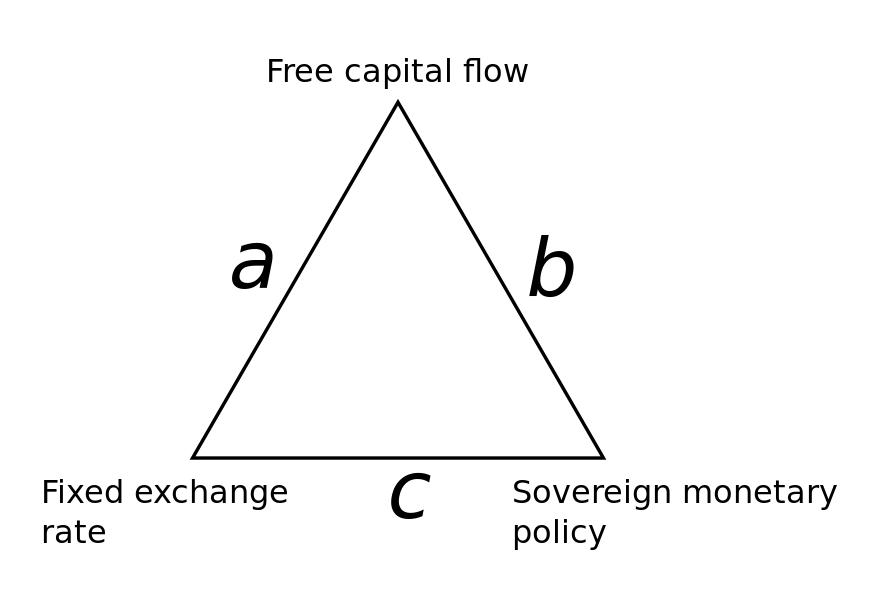

Basic insight from macro: you can have only two of the three!

The Impossible Trinity (macroeconomics)

State of the Token Debate

Is there economic merit to tokens?

Do tokens solve an economic problem?

Blockchain Tech Stack: Where would tokens matter?

Infrastructure

cryptocurrency

usage/incentive token

usage token

Service

Application

An Economic Model of ICO

- entrepreneur wants to produce a good or service

- Setup cost for production \(C_0\)

- marginal cost of producing \(c\)

- Demand is uncertain and only revealed after investment but pre-production. Inverse demand \(p(q)=x-q\)

- \( x\) is uniform on \([0,\theta]\).

\(x_i\)

\(x_j\)

\(x_k\)

Benchmark: Use own funds

- firm would maximize monopoly profits \[\max_q (x-q)\cdot q -cq.\]

- Benchmark: own funds \[q^m=\frac{x-c}{2}.\]

\(c\)

\(MR=x-2q\)

\(p(q)=x-q\)

\(q^m=(x-c)/2\)

Traditional Equity

- entrepreneur gives \(\alpha_e\) to equity investors to raise \(C_0\)

- investors fund as long as they break even

- entrepreneuer maximizes \[\max_q (1-\alpha_e)( (x-q)\cdot q -cq).\]

- Same as own funds \[q^e=q^m.\]

\(c\)

\(MR=x-2q\)

\(p(q)=x-q\)

\(q^m=q^e\)

ICO Financing

general idea: sell future output

two approaches for token sales

- sell a fraction of future revenue

- we call it revenue sharing

- formally: sell \(\alpha_t\) of \(T\) tokens

- produce \(q\) units a require \(T/q\) tokens per unit

- sell units of future output

- we call this output presale

- formally: sell \(t\) tokens

- produce \(q\) units and keep revenue from \(q-t\) tokens

Revenue Sharing

- entrepreneur chooses \(q^{rs}\) that solves \[\max_q (1-\alpha_t) q (x-q)-cq.\]

- Problem: entrepreneur pays full marginal cost and effectively solves \[\alpha \textit{MR}=c.\]

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^{rs}<q^m\)

- Solution \[q^{rs}=\frac{x-c/(1-\alpha_t)}{2}<q^m.\]

- Under-production!

\(\alpha_t MR\)

Output presale

- entrepreneur issues \(t\) tokens

- chooses \(q^{ps}\) that solves \[\max_q q (x-q-t)-cq.\]

- Entrepreneur effectively solves \[MR+t=c\]

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^{ps}>q^m\)

- Solution \[q^{rs}=\frac{x-c+t}{2}>q^m.\]

- The problem: over-production!

- Intuition: entrepreneur does not internalize that extra output unit affects revenue for tokenholders!

\(MR+t\)

Is token financing inferior?

- revenue sharing: underproduction

- output presale: overproduction

\(c\)

\(MR\)

\(p(q)=x-q\)

\(q^t=q^m\)

- "does not internalize" = externality

- address externality: TAX!

- here: tax future token income

- incremental token income gets shared

\(\alpha_tMR+t\)

- obvious answer: combine the two!

- issue \(t\) tokens ex ante

- share \(\alpha_t\) of new tokens

- Entrepreneuer solves \[\max_q (1-\alpha_t) (q-t)(x-q) - cq\] solution \[q^t=(x+t-c/(1-\alpha_t))/2\]

- token share \[\alpha_t=\frac{t}{c+t}\]

Token financing is NOT inferior!

Formal result: Optimal Token Contract

Presell \(t\) tokens.

Equivalence of Equity & Token Financing

If quantity produced \(q>t\), then share \(\alpha_t\) of revenue from incremental \(q-t\) tokens with tokenholders

As with equity, the entrepreneur receives the full NPV.

The entrepreneuer produces optimally at \(q^t=q^m\)

If \(q<t\) \(\Rightarrow\) redeem at rate \(t/q\) and tokenholders receive refund of \(c(t-q)\).

ICOs with Moral Hazard

- costs her \(0\)

- \(\theta\sim U(0,\theta_l)\)

- \(\theta_l<\theta_h\)

Idea:

entrepreneur can influence expected demand

- costs her \(C_e\)

- \(\theta\sim U(0,\theta_h)\)

with effort

without effort

- common topic in corporate finance

- very relevant in "decentralized" world where developers are scattered around the globe

- also applicable to, e.g. established firms that do something new

assume \[\textit{NPV}(\theta_h)>0>\textit{NPV}(\theta_l)\]

Equity Financing with Moral Hazard

equity holders

possibly break even

with effort

without effort

cannot break even

entrepreneur

earns \((1-\alpha_e)\ \frac{(\theta_h-c)^3}{12\theta_h} -C_e \)

with effort

without effort

earns \((1-\alpha_e) \frac{(\theta_l-c)^3}{12\theta_l}\)

\(>\) ?

exert effort iff

\[\textit{NPV}_h-C_e\ge \textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c}{\theta_h-c}\right)^3\]

Token Financing with Moral Hazard

token holders

possibly break even

with effort

without effort

cannot break even

entrepreneur

earns \(\frac{c}{c+t} \frac{2}{3\theta_h}\left(\frac{\theta_h-c}{2}-t \right)^3 -C_e \)

with effort

without effort

earns \(\frac{c}{c+t} \frac{2}{3\theta_l}\left(\frac{\theta_l-c}{2}-t \right)^3\)

\(>\) ?

exert effort iff

\[\textit{NPV}_h-C_e\ge \textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c-2t}{\theta_h-c-2t}\right)^3\]

Formal result

- With moral hazard,

- all projects that can be financed by equity can be financed by the optimal token contract but

- some projects that can be financed by optimal tokens contracts cannot be financed by equity.

Superiority of Token over Equity Financing

key math insight

\[\textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c}{\theta_h-c}\right)^3 >\textit{NPV}_h\times\frac{\theta_h}{\theta_l}\left(\frac{\theta_l-c-2t}{\theta_h-c-2t}\right)^3\]

Summary

- Simple model of ICO vs equity financing from the standard corporate finance toolbox

- Theorem 1: Without frictions,

- an optimal token contract finances the same projects as equity

- the entrepreneur earns the same rents under the optimal token contract

- Theorem 2: With entrepreneurial moral hazard,

- any equity-financeable project can be financed by an optimal token

- some token-financeable projects cannot be financed by equity

- \(\Rightarrow\) There is economic and conceptual merit to token financing

Another Model: Cattelini & Gans (2018)

- Gans and Cattelini (March 11, 2018)

- model as three stage process:

- Stage 1: offer

- Stage 2: first round of interaction

- Stage 3: possible additional issuance of tokens

- ICO used as a pre-sale mechanism

- "monetary policy" = possible future issuance

- Results:

- crypto tokens reveal consumer demand

- => "sometimes" entrepreneurial returns with crypto > with traditional equity financing.

- Lack of commitment in monetary policy can undermine saving

- model as three stage process:

What does a blockchain do?

only the first 1:16 min are relevant

What happened?

exchange needed TRUST

Jerry becomes trusted third party and enables the spot exchanges

What is the core message of the clip?

Jerry injects himself as an escrow

this is centralized trust

neither party trusts that the exchange happens

What Changes in Business Models can Blockchain Technology bring?

What does blockchain do?

peer to peer value transfers

self-powered platforms

contract execution

common outcome

Who do you dis-intermediate, and then who is your customer?

issuer

investor

broker-dealer

The challenge of dis-intermediation

investment advisor

Observation: many Decentralized Apps aim to create a platform to establish a two-sided, dis-intermediated market

Question 3: Do you need to incentivize the establishment of trust?

Question 2: What kind of incentives can you provide?

Question 1: What role does the intermediary play, what service does it provide?

-

Trust

-

Matchmaking

-

Time/size intermediation

-

marketing

What role does the token play?

What purpose does the token have?

What can tokens be used for?

What activities does the token incentivize?

bootstrap & enrich user engagement

internal economy

distribute payments

transaction

right to product/service, special functionality

internal currency

& value exchange

usage, voting, contribution, networking, connecting

rewards for work, creating

profit/benefit sharing

payment/transaction unit

Platform incentives are really iffy

-

is it worth it for me to engage at all

-

is the desired action of the platform the best for me

Not everything that can be measured matters and not everything that matters can be measured

-

must be aligned with long-run goal of platform

-

must be under the control of platform participant

What does the platform need people to do?

Is there a suitable performance metric

Utility tokens fail \(\Rightarrow\) not good platform tokens

Equity tokens fail too!

Key Challenges for the Blockchain/Crypto Community for 2019

Technology

Legal/Regulation

Economic functions

Key Technology Questions for Blockchain Design

interoperability

cybersecurity and privacy

functionality

scalability

smart contract features and verification

recently and unexpectedly: finality

Key Legal Questions for Blockchain Design

-

legal governance

-

what rules can and should a platform develop

-

-

legal contract/token design

-

Does the law have to change to accommodate new tech ? If so, how? What's dated?

-

How can token design and the law be married?

(the law should be tech neutral, but is it?)

Key Economic Questions for Blockchain Design

-

system governance

-

political economy

-

-

contract/token design

-

corporate finance

-

-

How does platform payment interactions with outside world

-

open-economy macro

-

-

How much do we have to pay operators to maintain the chain?

-

mechanism design

-

Summary for Future of Blockchain

allow new applications, new interactions, new business models

applications require (tech + economics) + business + legal background

understanding of economics on blockchain requires development

there is real economic value in tokens, when used properly

recording ownership on a blockchain is a no-brainer

blockchain tokens can be a lot more!

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/