The Value of a Millisecond:

Harnessing Information in Fast, Fragmented Markets

paper by Chen, Foley, Goldstein, and Ruf

discussion by Andreas Park

Research Question

Who benefits from a speed bump on marketable orders that provides a speed advantage to some limit orders?

Answers

- HFTs liquidity providers: larger profits on the speed-bump venue.

- Aggregate liquidity worsens.

- Liquidity providers: lower profits on remaining venues.

Speed Bumps

The famous case: IEX's Speed Bump

- main idea: orders into IEX are slowed down by 350 milliseconds but updates SIP data (=NBBO) faster.

- => NBBO pegged orders trade at "fresh" prices

- Chicago Exchange proposes “Liquidity Taking Access Delay"

- Incoming marketable orders get delayed by 350 microseconds, limit order cancellations do not

Speed Bumps

- all orders send to TSX Alpha Exchange are randomly delayed, between 1-3 milliseconds

- the exception are "post-only" orders which are not subject to the delay

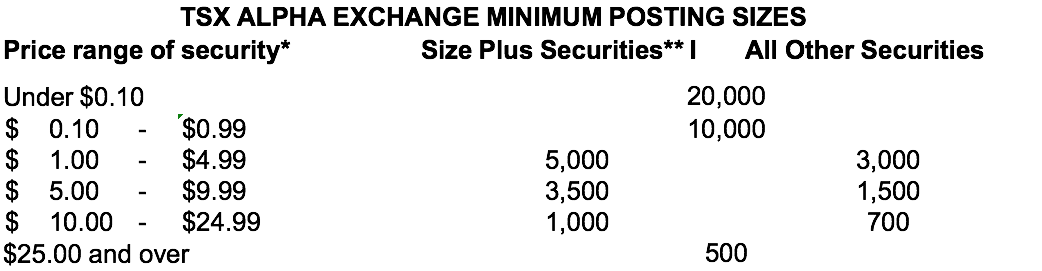

Here: TSX Alpha Exchange

- higher maker fee:

- 16 cents per 100 shares vs

- 14 cents per 100 shares

- minimum posting size

Cost of using post-only?

How do you benefit from post-only?

market event

expect market orders

200 shares

100 shares

500 shares

before

at the ask

How do you benefit from post-only?

market event

expect market orders

200 shares

100 shares

500 shares

after

cancels

Comment 1:

Many things happened at the same time

- TMX Select was closed

- Alpha fees became inverted

- Alpha introduced a speed bump

- Alpha became "unprotected"

- Brokers/marketplaces could "trade-through" Alpha's prices

1 event = 4 changes

Comment 2: Endogeneity of Adverse Selection measures in the paper

General Idea:

- the speed bump protects liquidity provider against adverse selection

- => avoid posted orders to become stale and can cancel ahead of market orders

Defining an informed order

- Step 1: Collect strings of trades

- = trades within 50 milliseconds

- Step 2: Informed = displaced/absorbs entire NBBO (i.e. across multiple markets)

- accounts for

- the trade itself

- plus trades by others

- plus cancellations!

- What if the NBBO is only 100 shares?

- Creates an endogeneity when speed bumps are introduced!

- accounts for

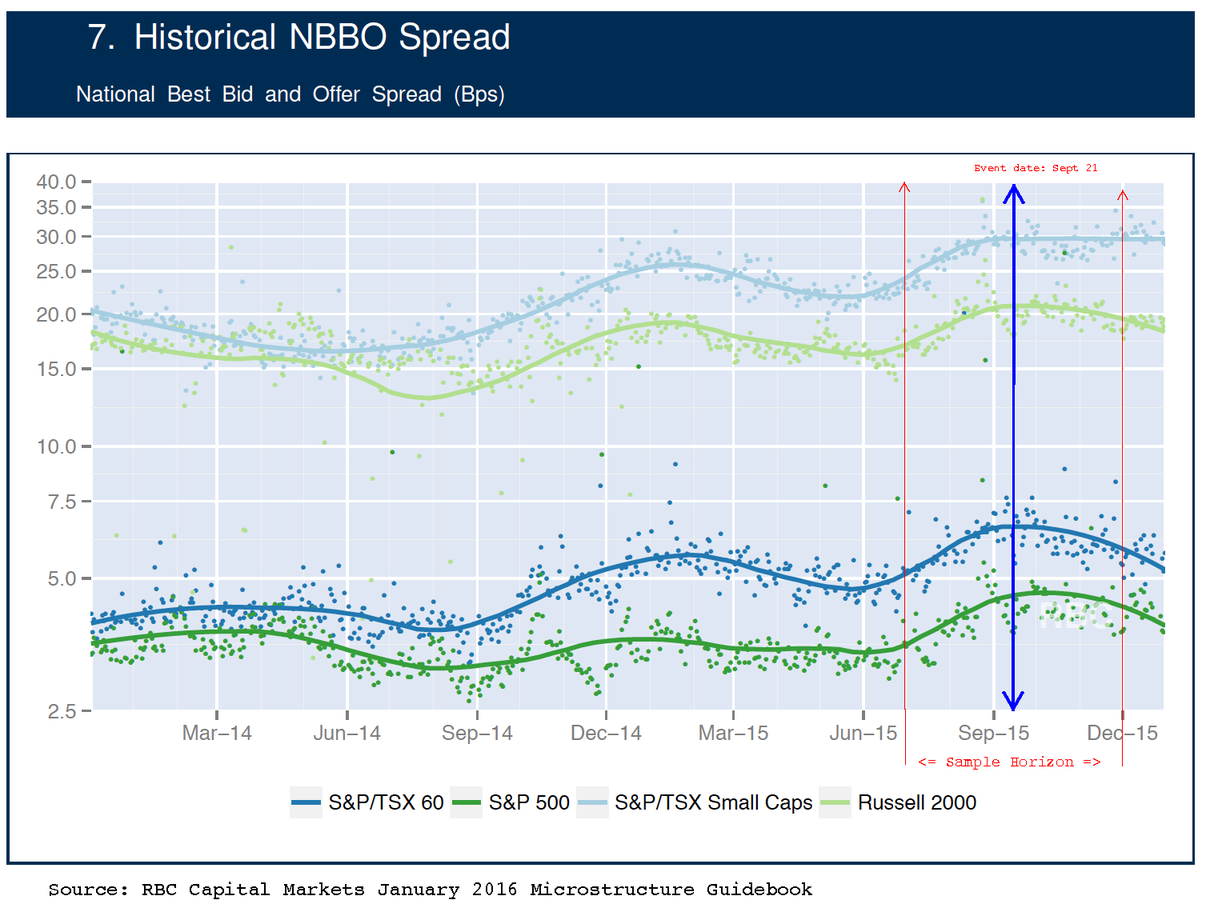

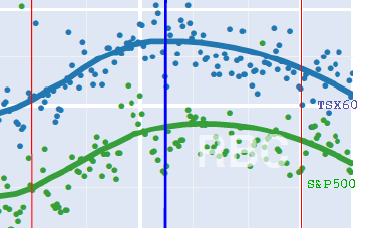

Comment 3: Did spreads change?

Comment 4: Beware of retail orders

Retail Myth 1:

(not this paper, but generally)

"retail trades are small"

| Price level | retail | non-retail |

|---|---|---|

| $1-$5 | 1,486 | 697 |

| $5-$10 | 791 | 413 |

| $10-$25 | 422 | 266 |

| >$25 | 275 | 203 |

average volume for single-market marketable orders

Retail Myth 2:

"retail trades are single-market and small"

| Price level | retail | non-retail | %retail | minimum size Alpha |

|---|---|---|---|---|

| $1-$5 | 5,100 | 5,797 | 26% | 5,000 |

| $5-$10 | 2,134 | 2,378 | 17% | 3,500 |

| $10-$25 | 1,032 | 1,128 | 27% | 1,000 |

| >$25 | 664 | 719 | 17% | 500 |

average volume for multi-market marketable orders

=> retail trades are neither small nor trade on only one market

HANDLE WITH CARE: "retail orders, on average, are unlikely to need to execute quantities larger than the 5 board lot minimum Alpha enforces"

Smaller Comments on Results and Interpretation

- "[The change] increase[s] profits for liquidity providers on [...] Alpha but [...] liquidity suppliers’ profits [are] reduced across remaining venues."

- Often these will be the same entities: do they just cross-subsidize and costs/benefits net to zero?

- NBBO Computation for Alpha trades - does it include Alpha?

- would explain quote-fade/fill rate result

overall I like many of the results, and I believe that they make intuitive sense, but I think the construction of measures requires work

Results and Interpretation

- informed=consume all liquidity

Tight spreads: 50-80% of trade-strings consume all liquidity

Wide spreads: significantly lower levels of informed.- I am sympathetic to the measure

- BUT: Way too much informed trading! If depth is low, too much will be absorbed

- The fill-rate measure has to be explained more thoroughly, e.g., by using examples.

overall I like many of the results, and I believe that they make intuitive sense, but I think the construction of measures requires work

Broker Activities

| Broker | %Vol |

|---|---|

| Anonymous | 24% |

| CIBC | 13% |

| TD | 11% |

| RBC | 9% |

| BMO | 5% |

| Scotia | 5% |

| National Bank | 4% |

| Merrill | 4% |

| Instinet | 2% |

| Morgan Stanley | 2% |

Source: RBC Marketstructure Guidebook Jan 2016

Who are the retail brokers? RBC & TD?

- are the largest retail brokers

- have many institutional clients

Comment on Results on Adverse Selection

- Result: Adverse Selection on Alpha declines

- => makes perfect sense to me

- hard to show in the data, but apparently one retail broker send all its flow there first.

- lower realized spreads for non-HFT liquidity provision on Alpha also makes perfect sense

- => only get to trade once the HFTs stepped out of the way

Effects on other venues

- "Section 4 establishes that Alpha’s systematic order processing delay against marketable orders enables the segmentation of uninformed order flow"

- statement much too strong!

- Question: with minimum post size, what is the ratio of depth Alpha/depth rest when Alpha at NBBO?

- Feature of TSX Composite:

- around 180 of 250 have 1-2 cent spreads

- rest has very wide spreads

- Suggestion: split sample!

my view: take with huge grain of salt due to the many simultaneous changes

Conclusion

- Paper has a lot of good stuff/ideas

- Interesting event

- Need to tighten data collection:

- What is a string? What is informed?

- Good call to move away from retail segmentation (old version) as it's too speculative

- Personal and subtle note: your results on retail flow segmentation contradict your findings in your recent JFE...