DeFi Lending and Borrowing

Instructors: Andreas Park

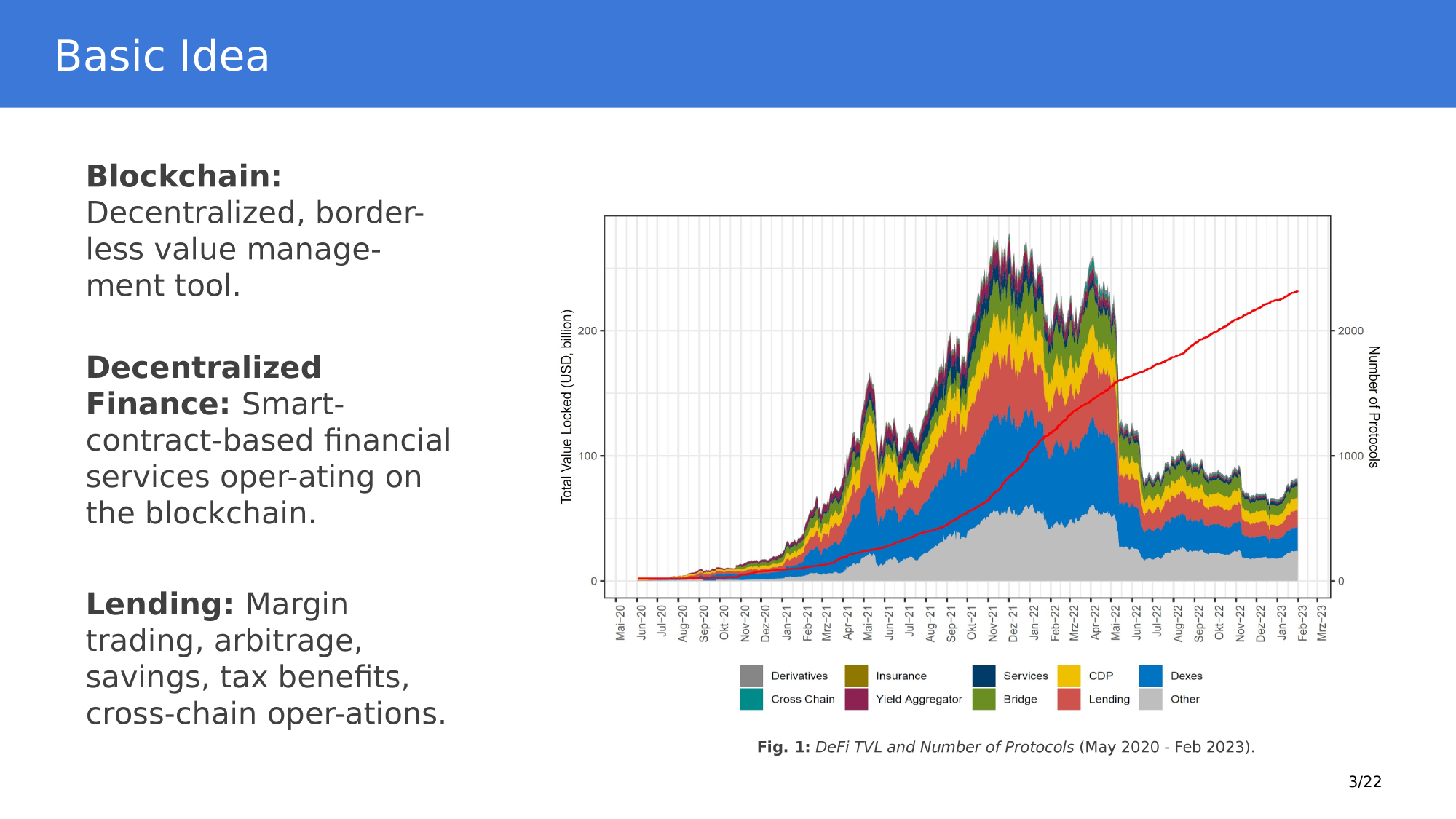

What's interesting about Defi Lending?

2021

the empirical part will focus on this episode

What are the core functions that a DeFi Ecosystem must cover?

- creation of assets

- trading of assets

- borrowing and lending

- creation of derivative assets

What are the core functions that a DeFi Ecosystem must cover?

- creation of assets

- trading of assets

- borrowing and lending

- creation of derivative assets

Liquidity transformation

- convert an "illiquid" asset into cash temporarily

- = borrow against some form of collateral

Credit

- obtain cash temporarily for a fee

- = borrow against your good name

Comparative advantage

- borrow an asset

temporarily because you can use it better

MakerDAO/Sky

Maple Finance

AAVE/Compound/Morpho

MakerDAO

user perspective

4 ETH

(1 ETH = $375)

(Oct 15, 2020)

\(\approx\) $1,500

\(\vdots\)

1,500 DAI

(1 DAI = $1)

formally: this smart contract is a collateralized debt position (CDP)

Prerequistes

Key Components for Defi

borrowing/lending

on-chain ability to exchange arbitrary value

(last class)

Borrowing/Lending & Unit of Account creation

Idea:

- create fiat money on chain with borrowing

- mechanism

- a collateralized loan with ETH in escrow

- DAO-managed monetary policy (=creation or destruction of tokens)

Sidebar: what is a DAO?

- DAO=decentralized autonomous organization

- \(\to\) entity without management

- governance decided by token holders essentially by vote

- We'll devote a class to DAO governance

user perspective

fractional collateral \(\to\) collateralization factor \(=\) 150%

total collateral = $1,500

maximum loan = $1000

overcollateralization = $500

actual loan (example) = $500

buffer = $500

user perspective: what happens if the price of ETH rises?

ETH \(\nearrow\) $500

value of ETH collateral = $2,000

maximum loan = $2,000/150%=$1,333

total collateral = $2,000

maximum loan = $1,333

overcollateralization = $667

actual loan (example) = $500

buffer = $500

overcollateralization = $667

new loan capacity= $333

user perspective: what happens if the price of ETH falls?

ETH \(\searrow\) $187.5

value of ETH collateral = $750

maximum loan = $750/150%=$500

total collateral = $750

maximum loan = $500

overcollateralization = $250

actual loan (example) = $500

buffer = $0

for reference: former value of collateral

user perspective: what happens if the price falls & max loan is exceeded?

Maker DAO

ETH \(\searrow\) $150

value of ETH collateral = $600

maximum loan = $600/150%=$400

total collateral = $600

maximum loan = $400

required overcollateralization = $200

actual loan (example) = $500

buffer = -$100

for reference: former value of collateral

\(\Rightarrow\) triggering of liquidation auction by "keeper"

sell 3.33 ETH=$500=500 DAI

repay $500=500 DAI loan

retain incentive

return remainding ETH to vault owner

Maintaining the Peg: monetary policy

Maker DAO

- How works:

- 1 USDC=1.01 DAI

- use USDC to mint new DAI

- supply (DAI) \(\nearrow\)

- price (DAI) \(\searrow\)

- use USDC to mint new DAI

- 1 USDC=0.99 DAI

- Swap Dai for USDC (more below)

- demand (DAI) \(\nearrow\)

- price (DAI) \(\nearrow\)

- 1 USDC=1.01 DAI

\(\Rightarrow\) all relies on behavioral assumptions

\(\Rightarrow\) But: there are also real incentives & mechanisms

Maintaining the Peg: monetary policy

Maker DAO

- stability fee

- DAI savings rate (DSR)

- debt ceiling

borrowers of DAI need to pay interest \(\to\) stability fee

- if too much minting (=too much DAI) then

- \(\to\) interest \(\nearrow\) \(\to\) cost of DAI \(\nearrow\)

- \(\to\) minting \(\searrow\) \(\to\) supply DAI \(\searrow\)

DSR paid on "locked" DAI

- DAI deposited to specific contract (demand \(\nearrow\))

- funded by stability fees

- \(\to\) SF>DSR

total amount of debt (or DAI) outstanding is limited

Sidebar: how is this decided?

\(\to\) special "governance" token MKR

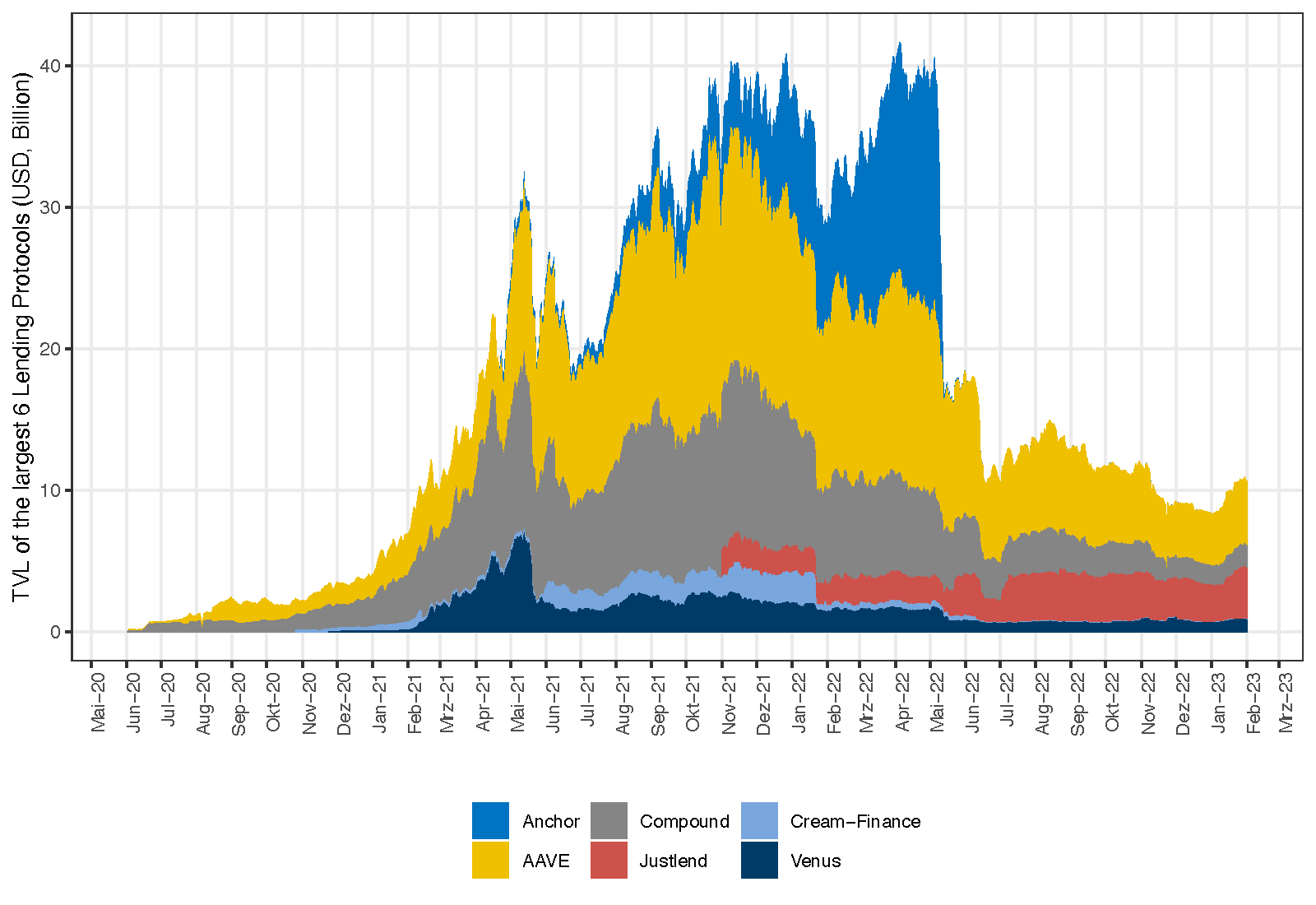

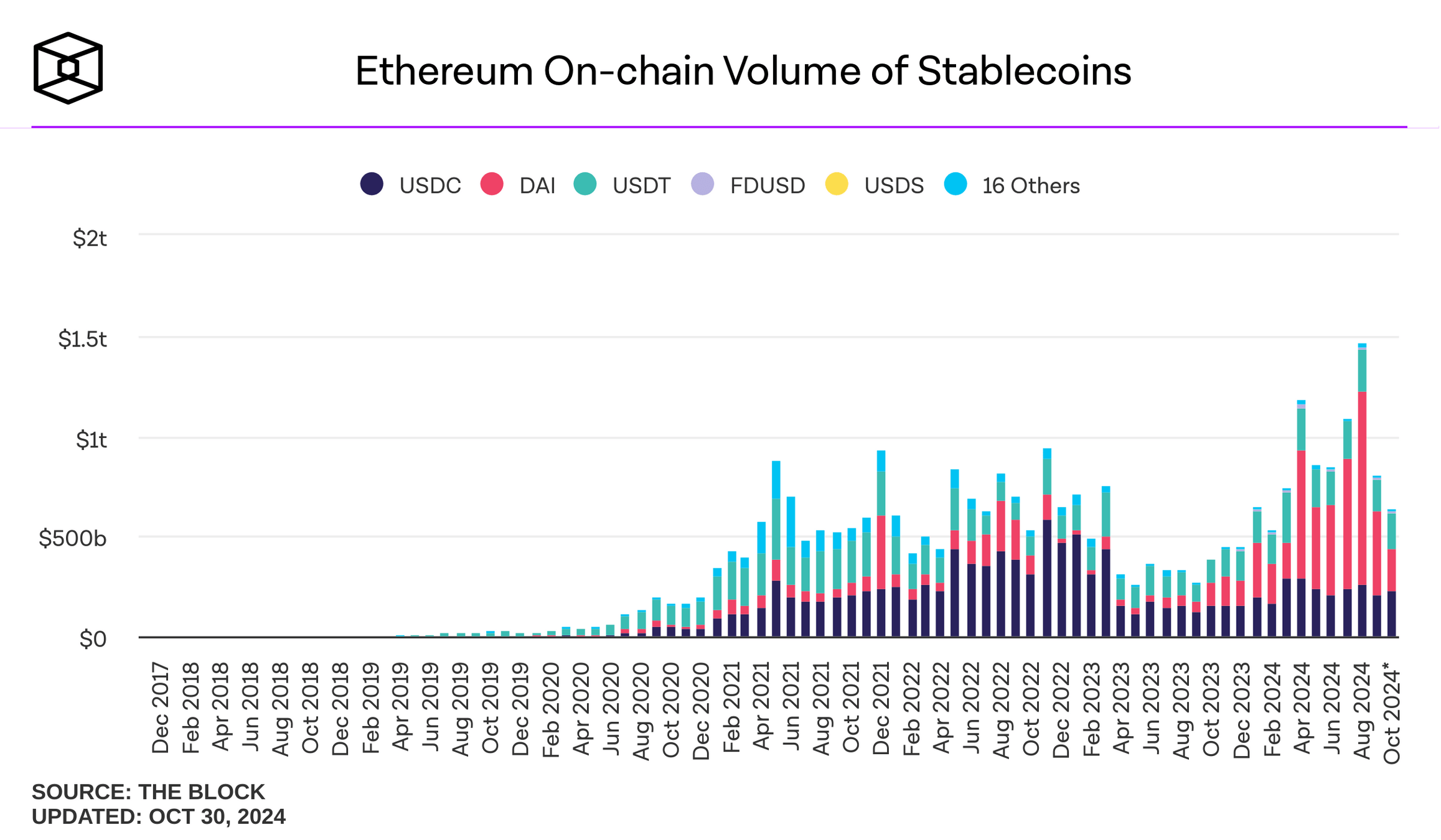

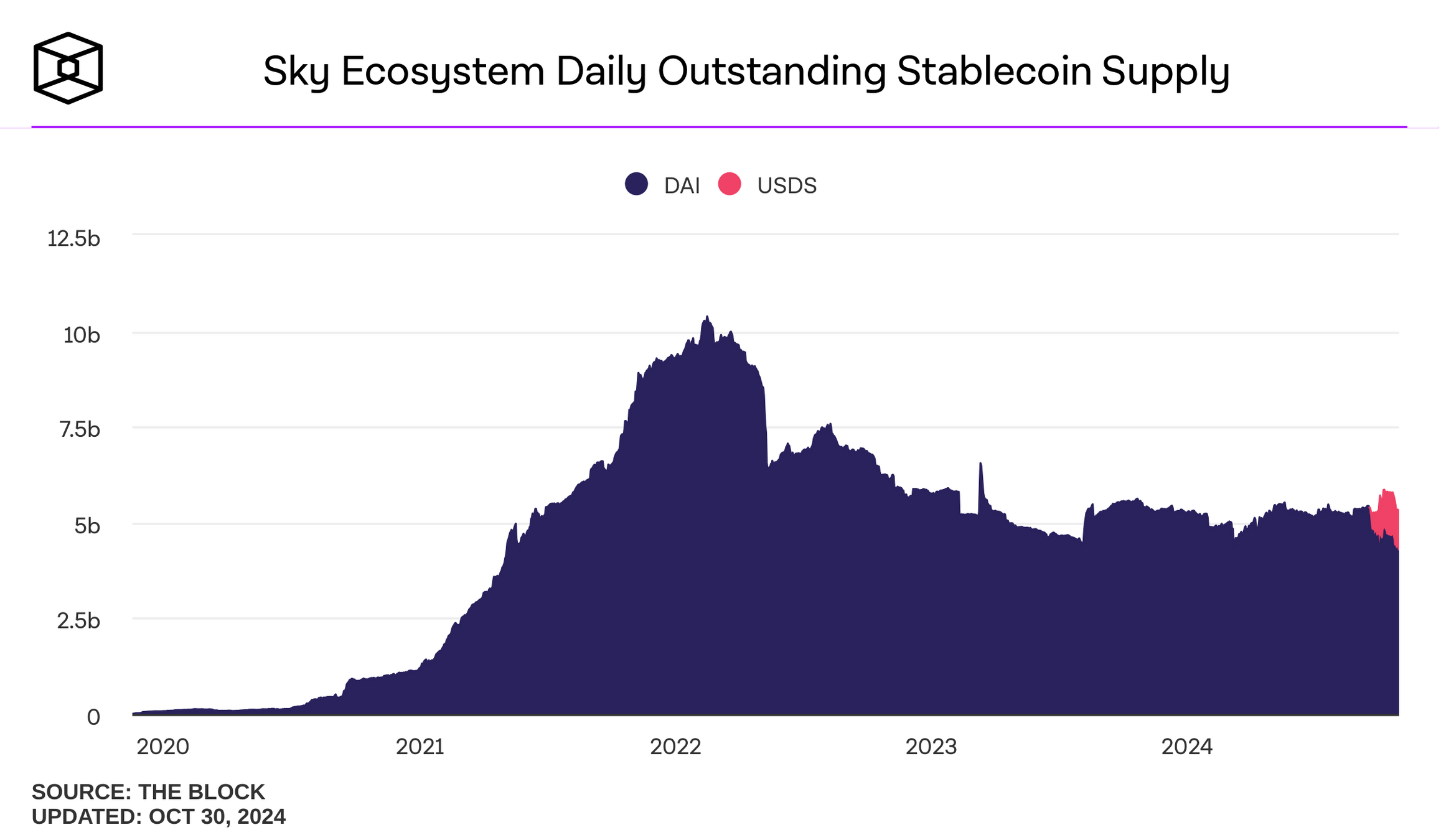

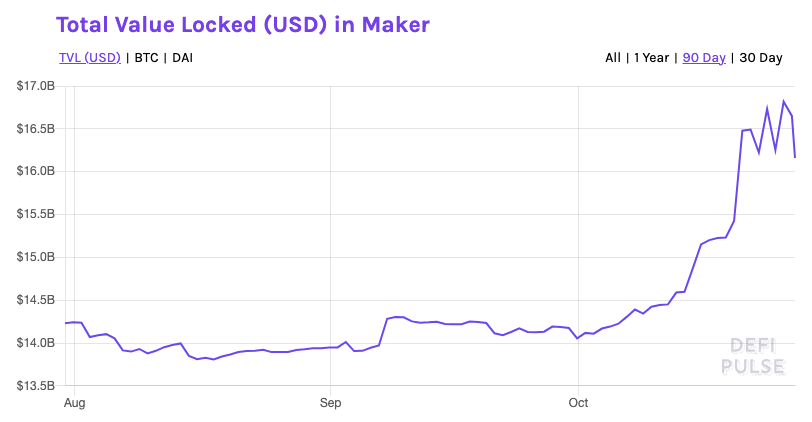

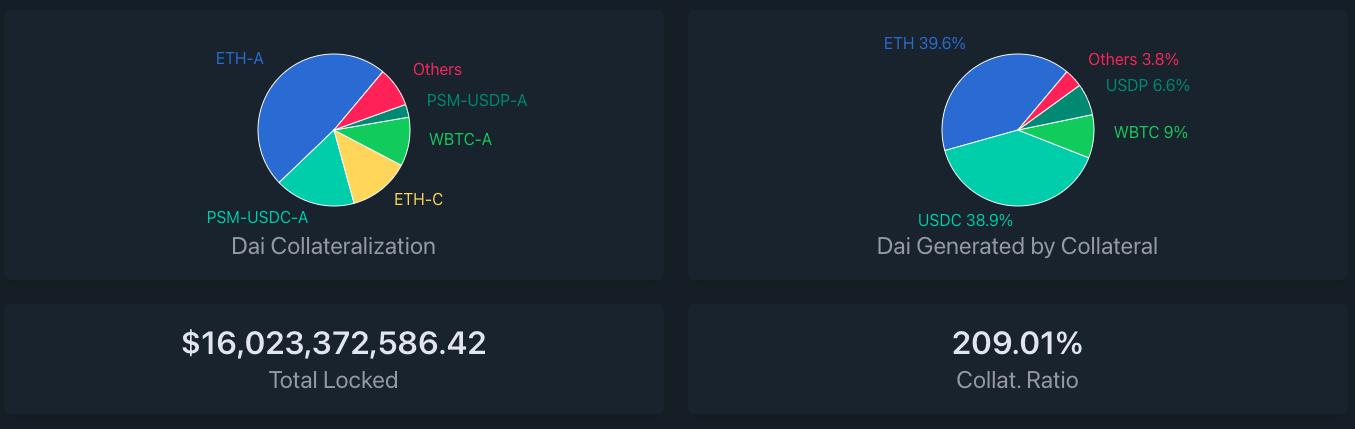

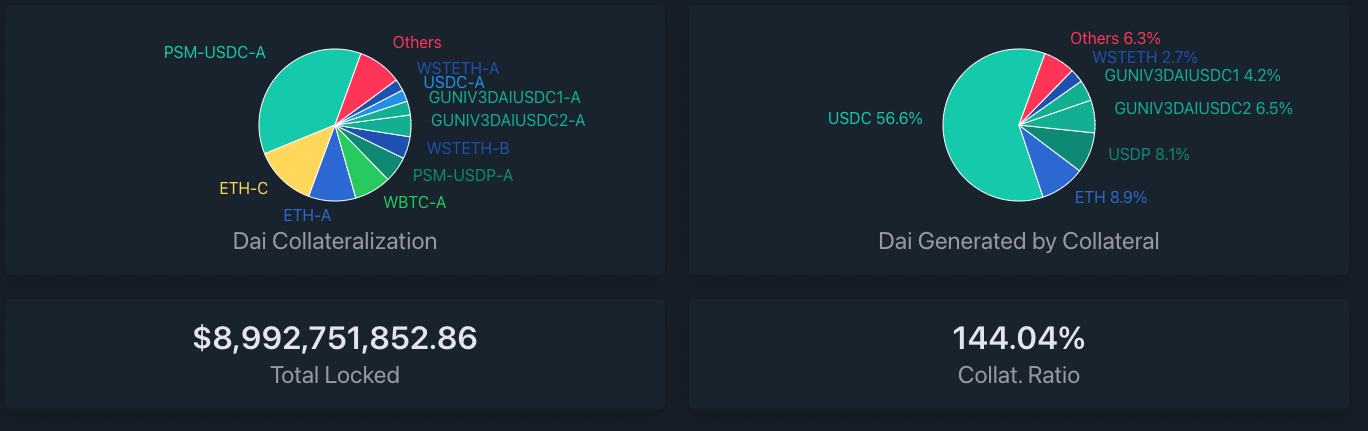

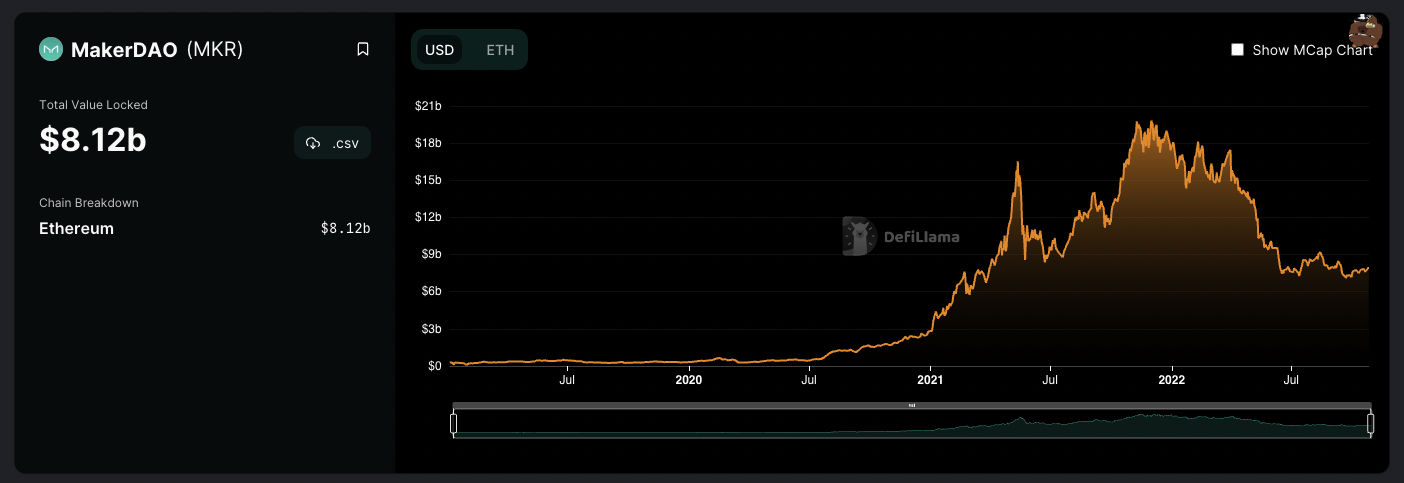

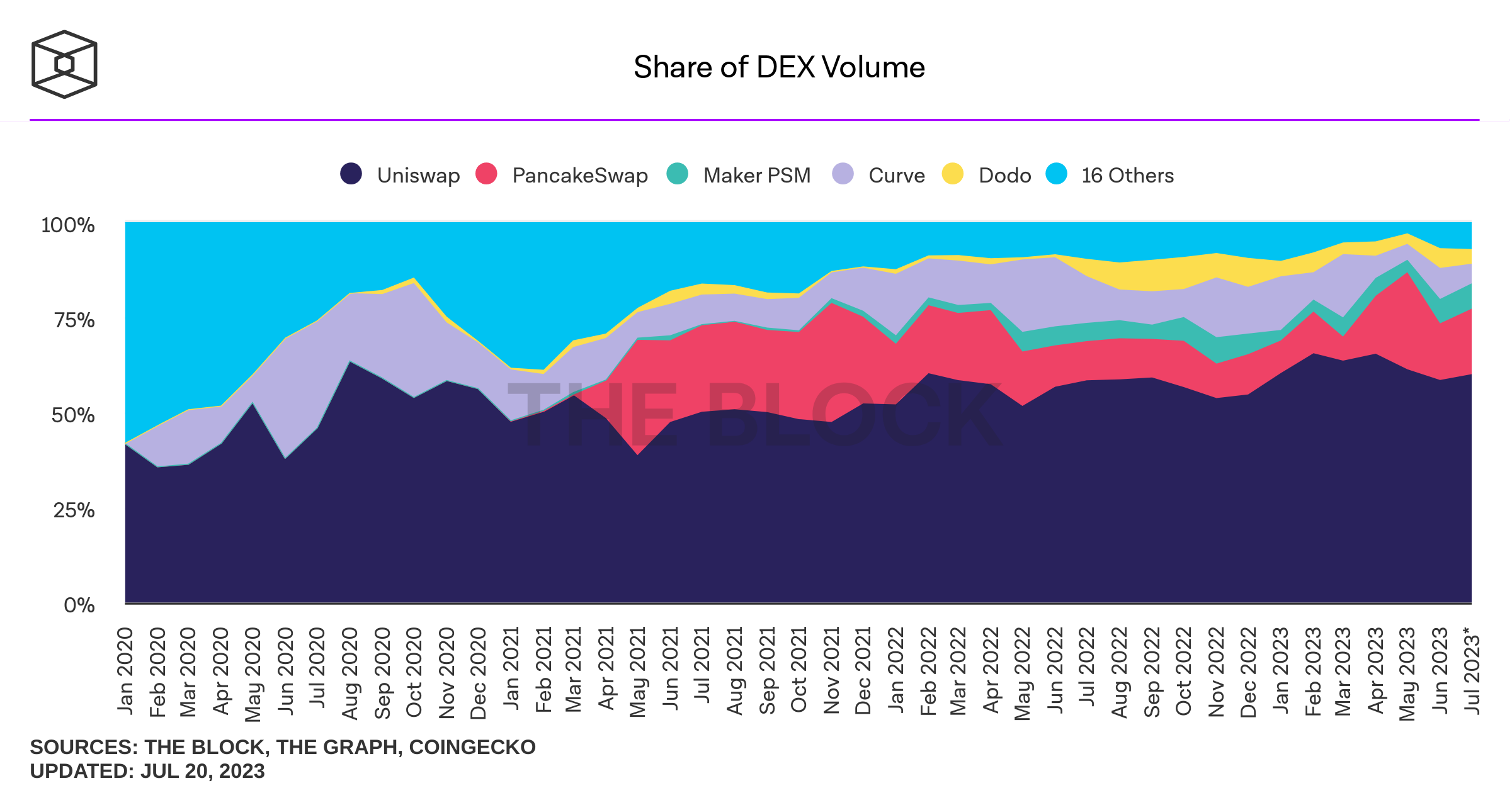

Value locked Oct 27, 2021

Maker DAO

Source: daistats.com (Oct 27, 2021)

Source: daistats.com (Oct 26, 2022)

The March 12, 2020 "BlAck Thursday" Drama

Maker DAO

- some crypto prices dropped more than 50%

- cascading liquidations in leveraging platforms

- network congestion: some liquidations done at near-zero prices

- collateral shortfall in DAI

- MakerDAO sold new DAO tokens to collect collateral

- odd: DAI became riskier but high demand for DAI to trigger liquidations!

PEG stability module (PSM)

Maker DAO

The Problem:

- in extreme bull/bear runs, the peg may no longer work

- example: March 2020

- ETH dropped significantly and suddenly

- a rush occurred to (a) get out of ETH into save assets and (b) to collect DAI to get keeper fee

- upward pressure on price of DAI

The Solution:

- Peg stability module

- swap a given collateral type directly for DAI at a fixed rate (no minting/borrowing)

- like regular vault type with a zero stability fee and a liquidation ratio of 100%

- accessed through a user-facing smart contract containing the relevant swap functions (no ownership, just straight swap)

Note: In May 2021, ETH prices dropped again by >30% but no drama in DAI

MakerDao's Peg Stability Module as an AMM

categories and assessment for defi

assessment of makerdao

Interest rates influenced by the FED, access to loan products controlled by regulation and institutional policies

MakerDAO platform is openly controlled by the MKR holders.

Difficulty of obtaining loans for large majority of population

Open ability to take out DAI liquidity against an overcollateralized position in any supported ERC20 token. Access to a competitive USD denominated return in DSR.

Costs of time and money to acquire a loan

Instant liquidity with minimal transaction costs.

Can't seamlessly use the same USD across many platforms

Issuance of DAI, a permissionless USD-tracking stablecoin backed by cryptocurrency. DAI can be used in any smart contract or DeFi application.

interoperability

inefficiency

centralized control

limited access

opacity

Unclear collateralization of lending institutions.

Transparent collateralization ratios of vaults visible to entire ecosystem

legacy finance

MakerDAO

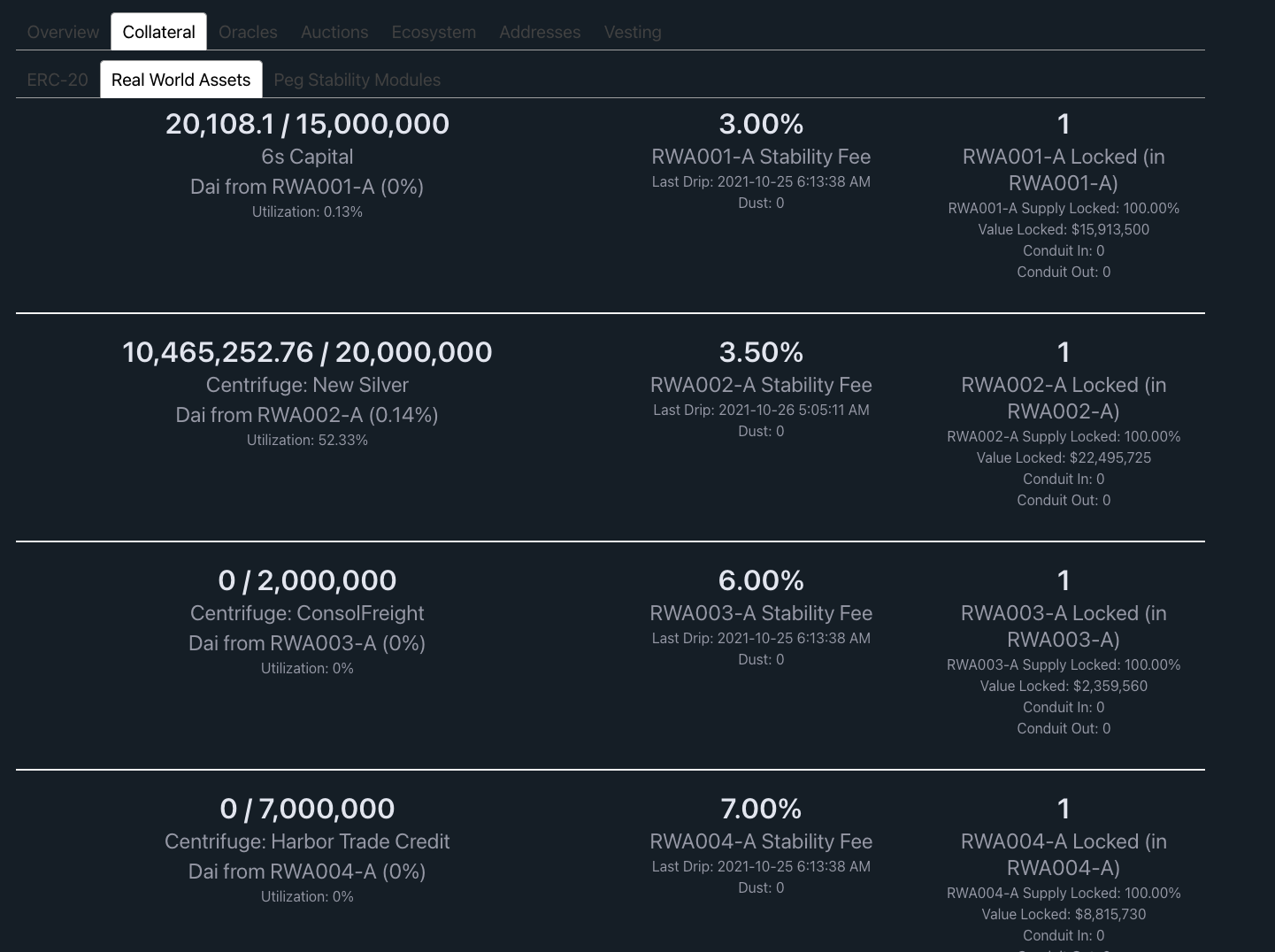

The frontier: DAI loans for real-world assets

Maker DAO

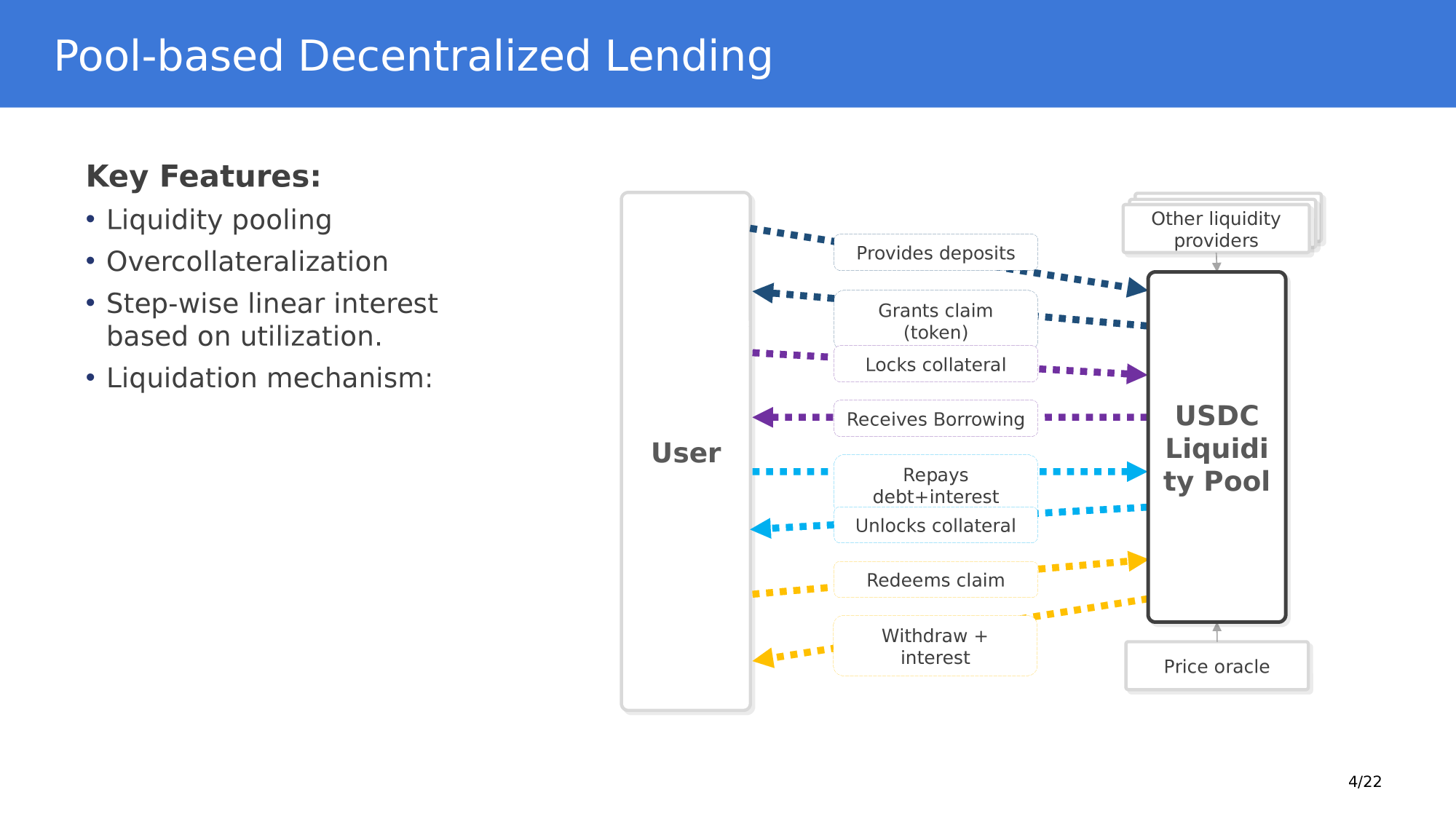

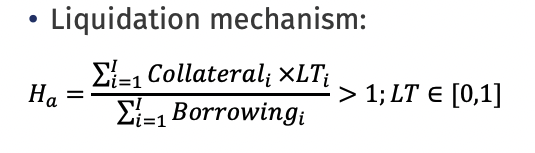

Pool-based lending principles

collateral

compound Finance

- Collateral ratio \(\in[0,90]\)

- =0 \(\to\) not usable

- =90 \(\to\) stablecoin

- post 100 DAI

- factor 90

- \(\to\) for each $1 borrow, deposit $100/90=$1.11

- can borrow up to $90

- post 1 ETH=$300

- factor 60

- \(\to\) for each $1 borrowed, deposit $100/60=$1.67

- can borrow up to $180

Example 1

Example 2

Example 3

- post 1 ETH=$300 and 100 DAI \(\to\) $400

- factor 60 and 90

- \(\to\) for each $1 borrowed, deposit

$100/(.75\(\cdot\)60+.25\(\cdot\) 90)=$1.48 - can borrow up to $270

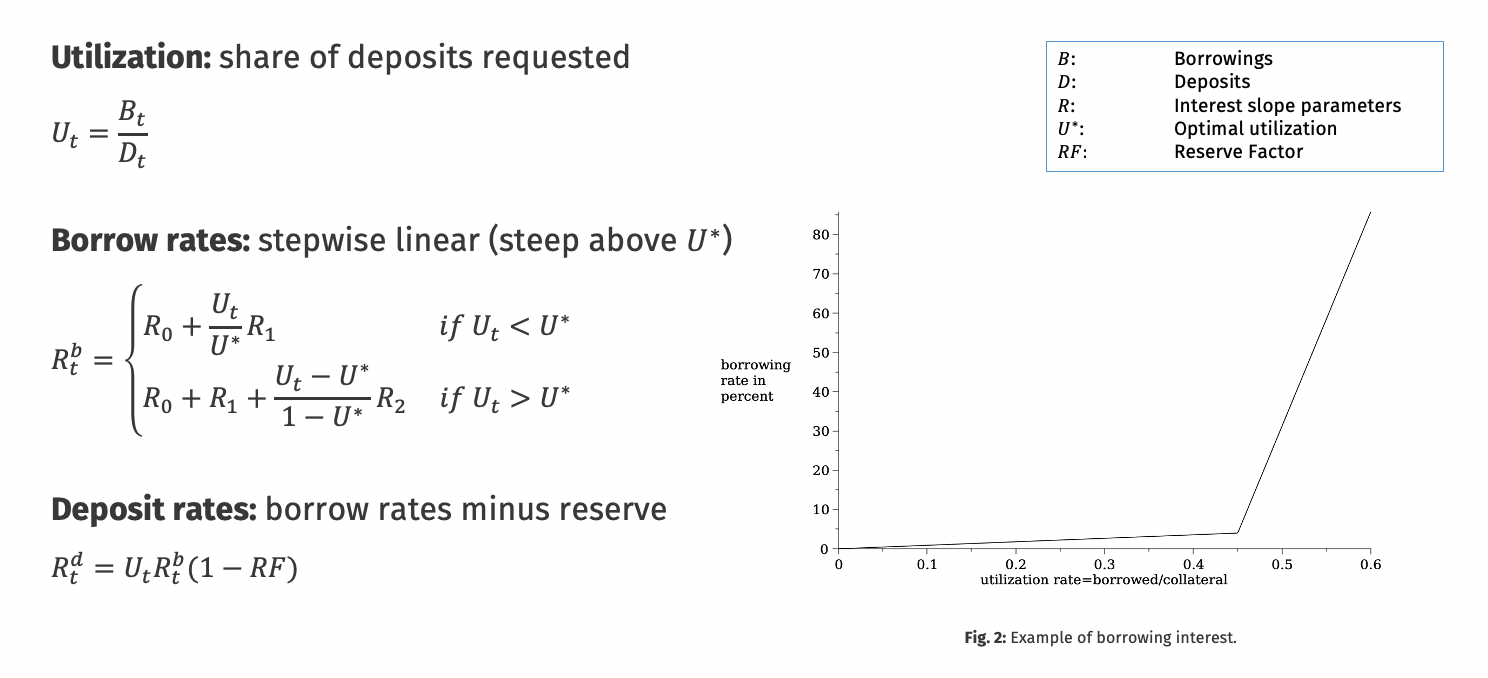

borrowing and lending rates compounded per block

Pool-based Defi Lending: Theory

Riviera, Saleh, Vanderweyer (2025)

Pool-based Decentralized Lending: economic function = the price

- price function is ad hoc

- but can it work well = achieve the most efficient outcome?

- How do they measure "good"?

- loosely:

- higher volume

- = better capital use

- = most efficient

- best = like competitive market

- loosely:

Riviera, Saleh, Vanderweyer: Results

Without uncertainty over how many people may enter the market, welfare can be made arbitrarily close to competitive equilibrium welfare.

For any admissible borrower interest rate function, there exists a unique stationary equilibrium in utilization

With uncertainty users worry about excessive rates (borrowers) or low income (lenders) => they "internalize and use the lending protocol less"

Economic Intuition

-

no uncertainty: Users’ informed actions reveal the market state via utilization; DLP can set rates close to competitive levels.

-

With uncertainty: Random shocks to credit market conditions create rate volatility; risk-averse users reduce borrowing/lending ex-ante to avoid bad outcomes, lowering utilization.

Riviera, Saleh, Vanderweyer: Translating Econ-Speak to Practice: what do we learn?

Practical Implications

-

Design: Interest rate functions should heavily penalize utilization near 100% and set low rates when far below it.

-

Limits: No interest rate function can fully remove inefficiency if users face uncertainty.

-

Oracle problem: Overrated in this context — user uncertainty is the real constraint.

Token Accounting:

tracking ownership

Compound

AAVE

Token Accounting: TWO Types

- track ownership of pool holdings with receipt tokens

- continuous updating of wallet balances

How does compound finance work?

Lending

Fundamentally, what does a bank do?

- size intermediation

- term intermediation

- risk intermediation

And how is this done?

- pooling deposits

- issuing loans based on deposits

- loan rates based on collateral or credit rating

on blockchain

- short-term loans

- pseudo-anonymous

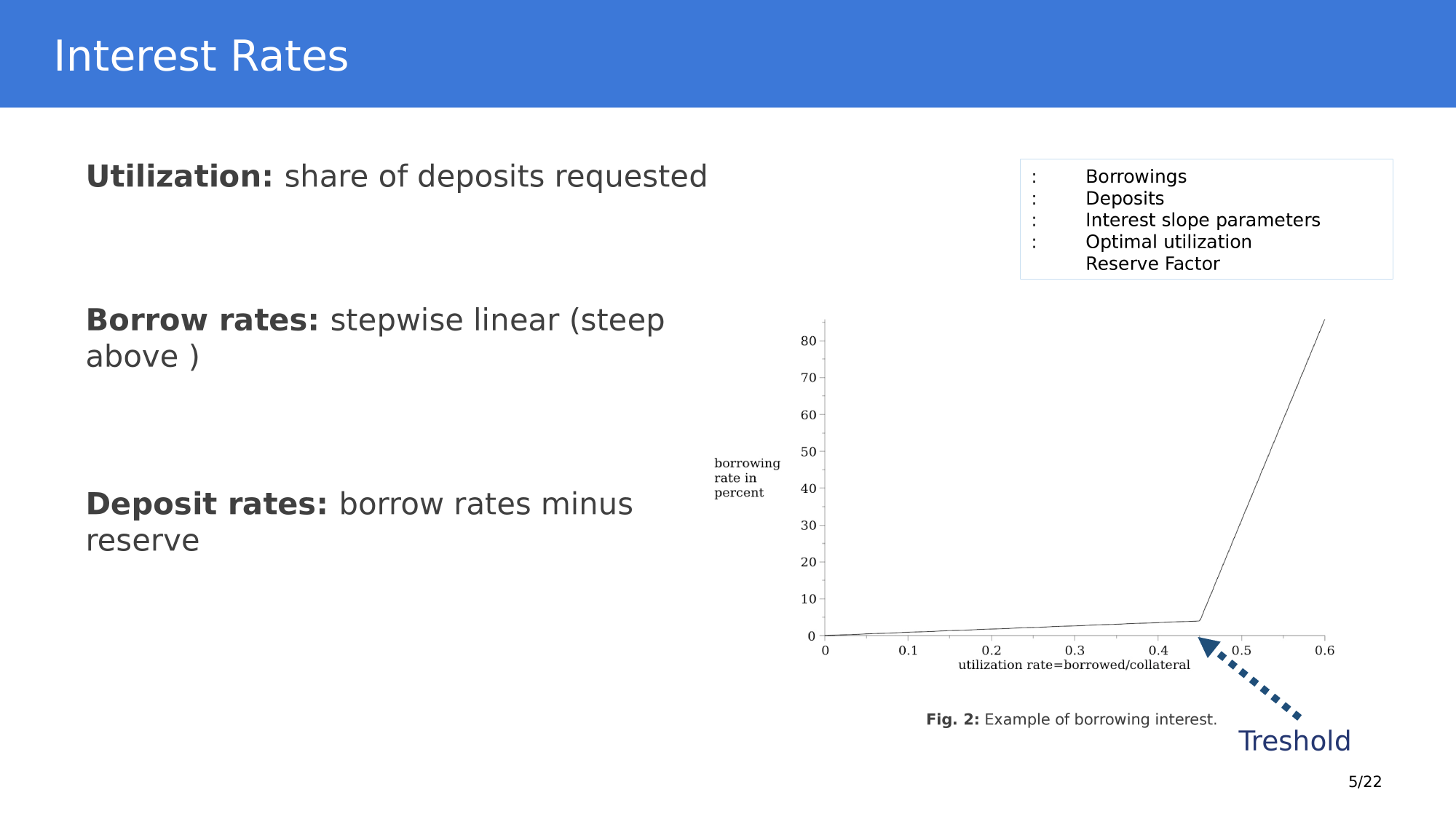

how are the rates determined? - a function

compound Finance

100%

fraction of supplied that's been borrowed

base rate

borrow rate

token accounting

Compound

- deposit: add \(q_0\) units of \(A\)-tokens into a pool that contains \(Q_0\)

- assume: \(Q^c_0\) units of the \(cA\)-receipt tokens outstanding already

- User receives \(q^c\) receipt \[ \frac{q^c}{Q_0^c+q^c}=\frac{q_0}{Q_0+q_0}.\]

- Exchange rate: \(z_t=\frac{Q_t}{Q_t^c}\) of \(A\) to \(cA\)-tokens.

- Interest accrues so that pool contains \(Q_T>Q_t\) of the \(A\) token after time \(T\)

- When withdrawing, users sends \(q^c\) tokens to the contract

- Receives \(q_T>q_0\) of the \(A\)-token at exchange rate \(z_t>z_0\) where \[q_{T}=Q^c \times z_{T}\]

compound Finance

- Compound escrows tokens

- must account for % ownership

- \(\to\) tokenized user share

- \(\to\) use the c-token

- cDAI

- cETH

- minted/burned based on funds added/removed from underlying

- seamless movement of these shares (reduced transactions costs!)

- ability to use the ctokens in other protocols

Tracking ownership - How do you reclaim a deposit?

Tracking ownership - Example

compound Finance

In Compound

translated

new deposit

1,000 DAI

100 cDAI

500 DAI

add 50 new cDAI

Tracking ownership - Example

compound Finance

In Compound

translated

new deposit

1,000 DAI

150 cDAI

500 DAI

1 year later: 10% interest on compound

150 DAI

(same cDAI, ownership shares don't change, just each cDAI is worth more)

(accrues per block per deposit)

AAVE

Differences to Compound

Aave

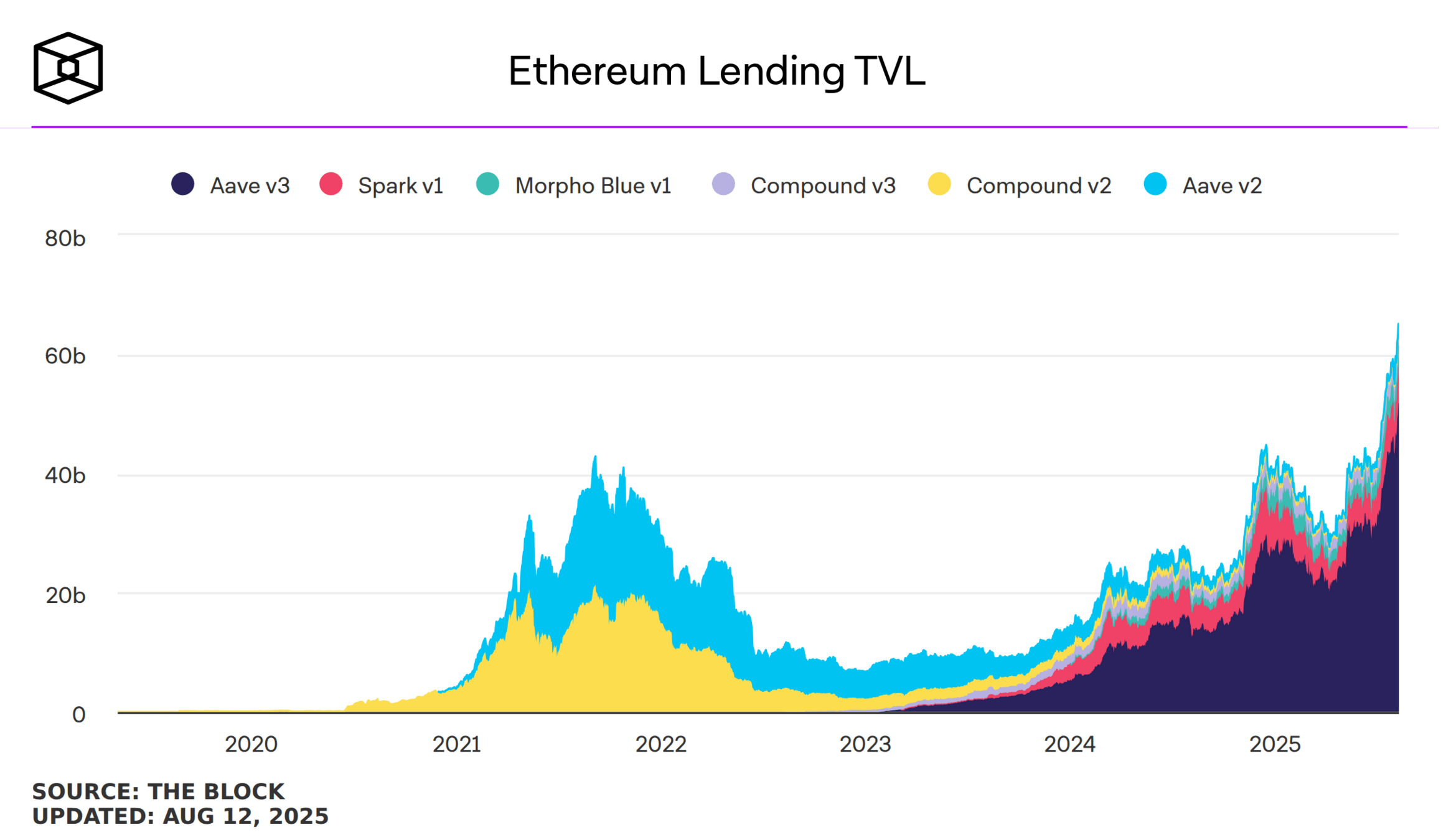

- Aave is the now the largest lending protocol

- has many features that are similar to Compound

- offers more assets

- offers flash loans (rate ~7bs)

- token accounting done by continuous updating of token balance

token accounting

Aave

- User makes a deposit continuously receives "a-tokens"

- Supply:

- \(Q_0\) units of an asset \(A\) token to the Aave pool obtains

- \(Q_0\) units of \(aA\)-tokens

- balance updates continuously (\to\) claim on more \(aA\) tokens

- To withdraw after \(T\) interest periods: sends her \(Q_T\) \(aA\)-tokens to the contract, where

\[Q_T= Q_0\prod_{t=1}^{T}{(1+r_t)}\] - \(t\) measured in blocks

- \(r_t=\) interest allocated per block \(t\)

Morpho

Liquidity Mining

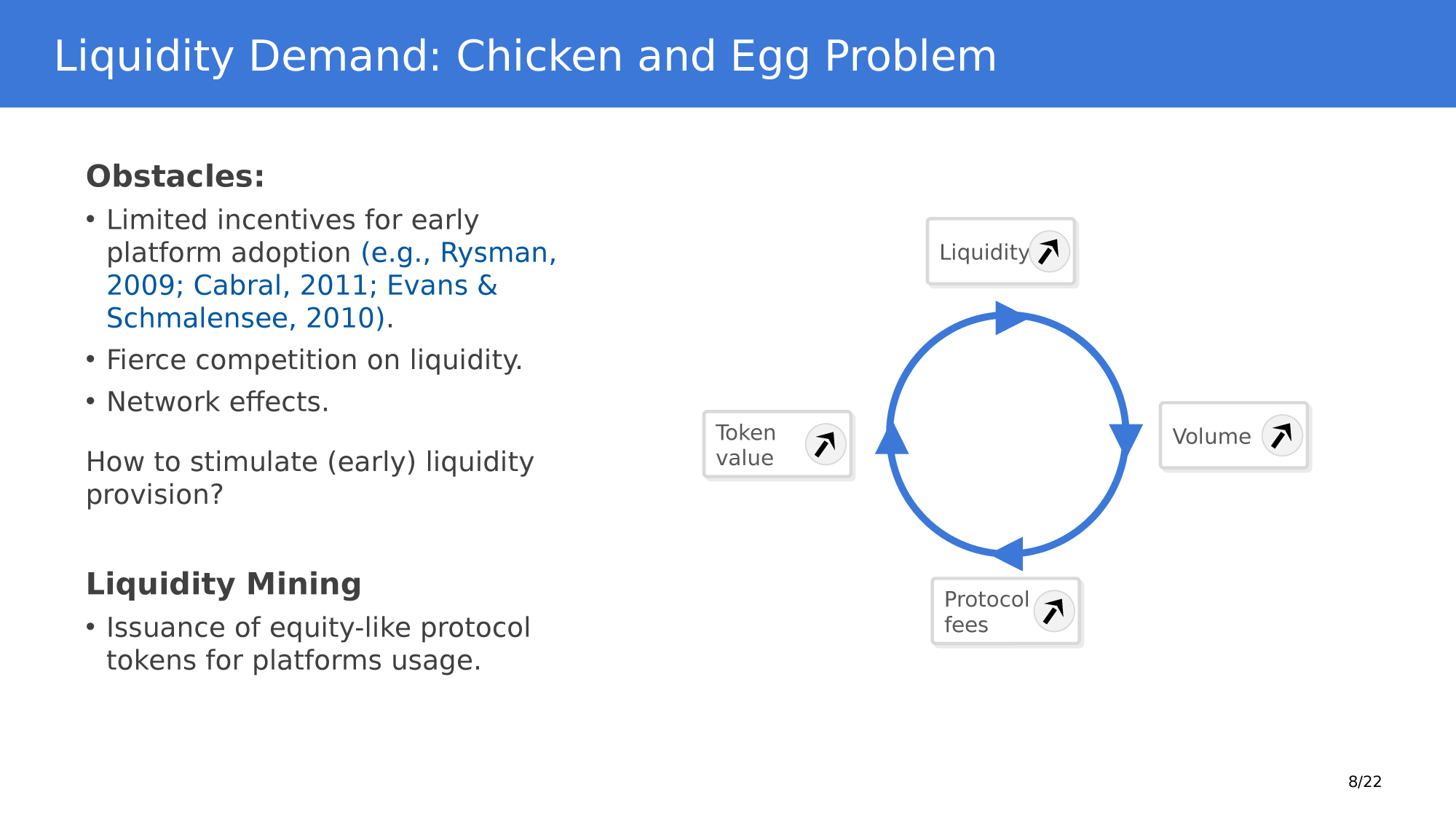

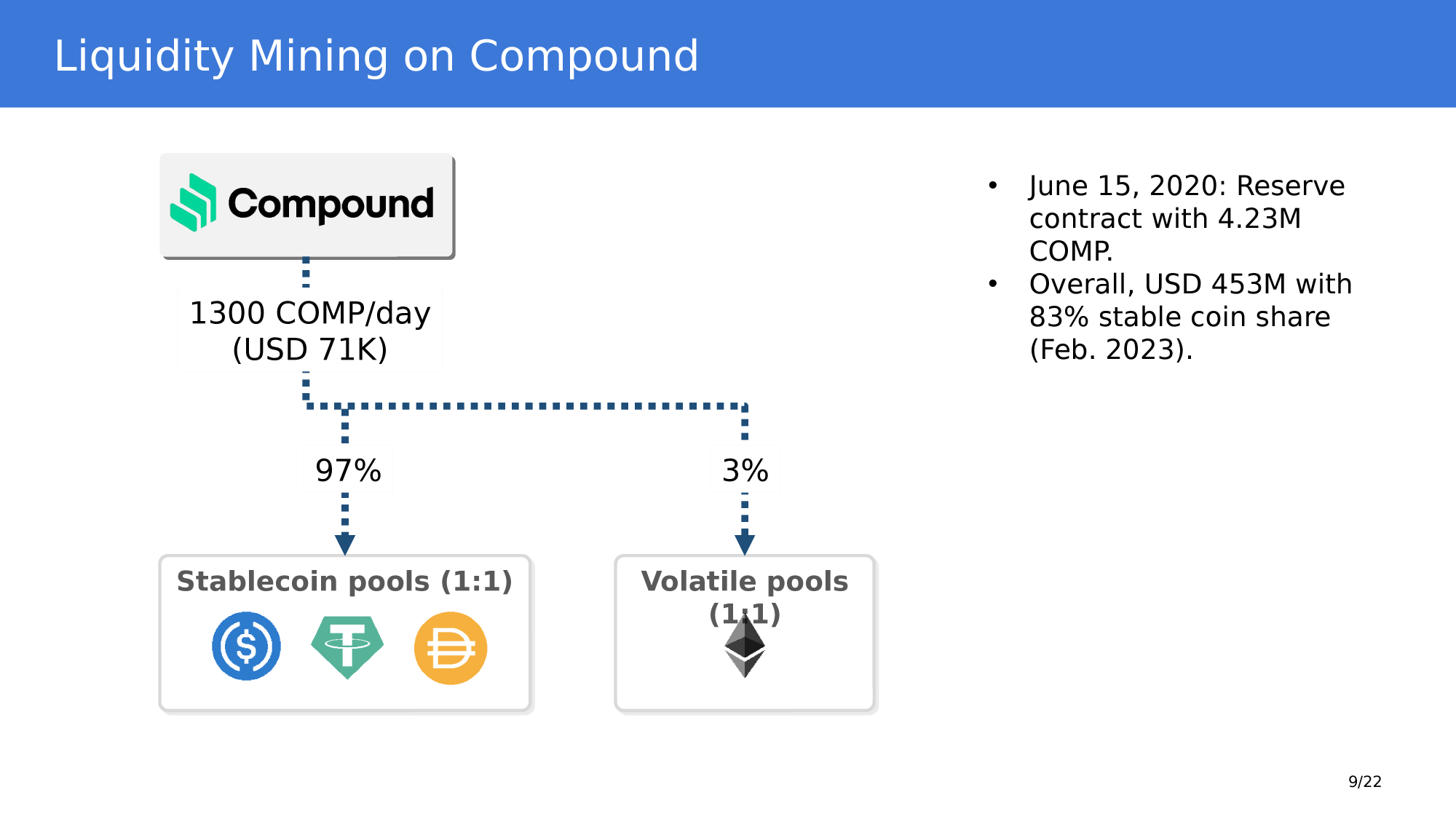

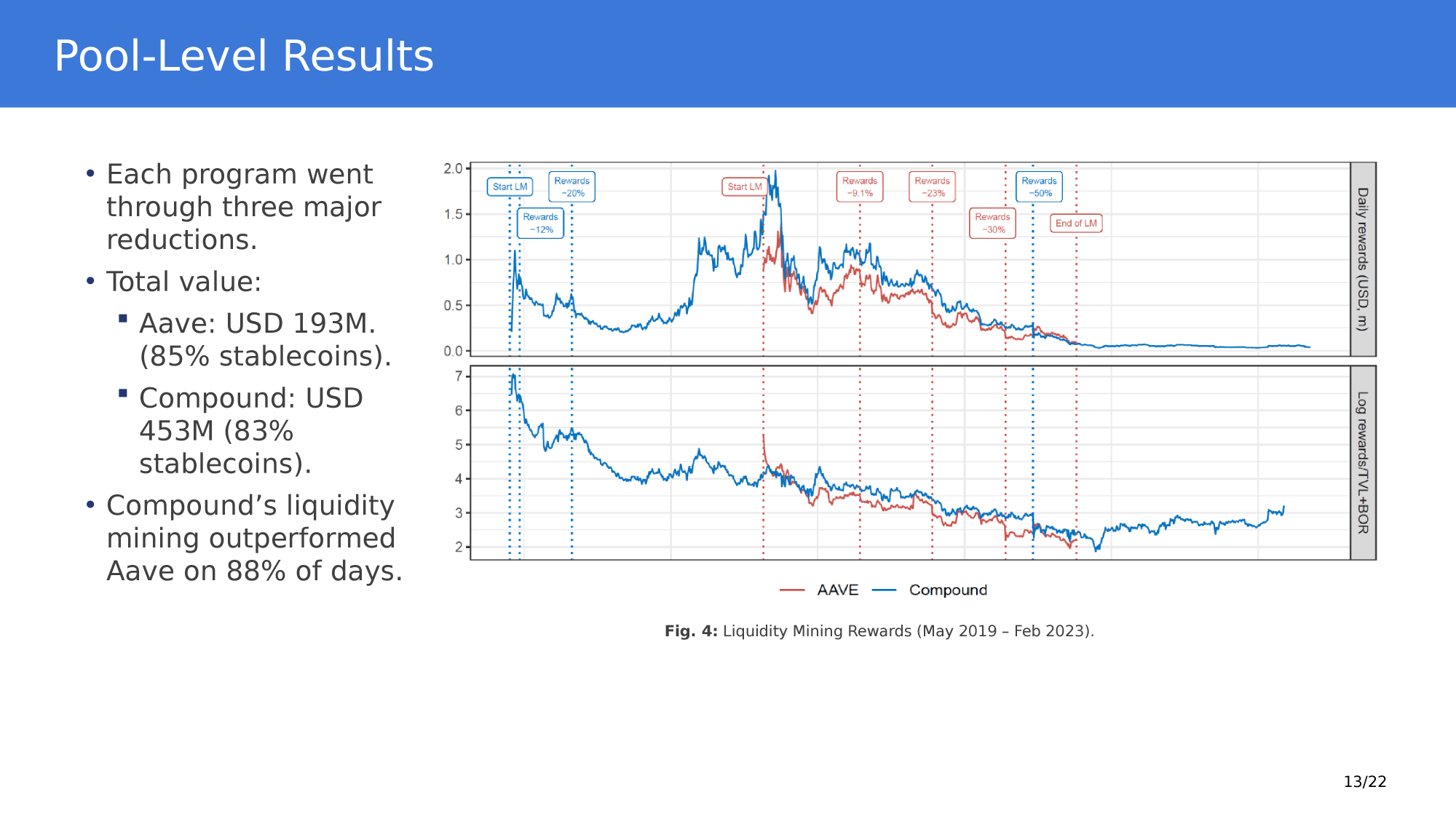

Park & Stinner (2025): Solving the Chicken and Egg Problem: Liquidity and Activity Incentives

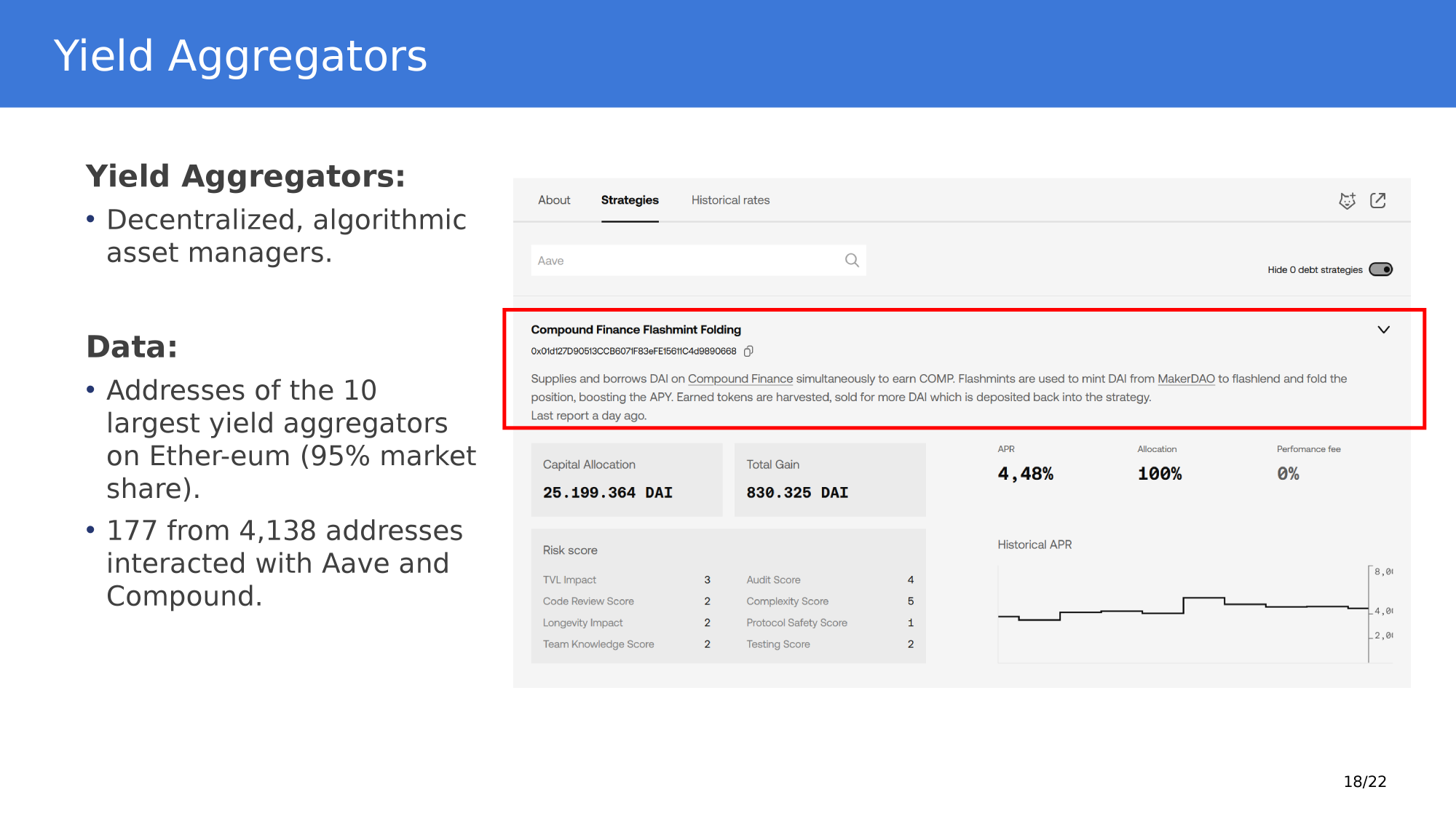

Yield Aggregators

Flash Loans

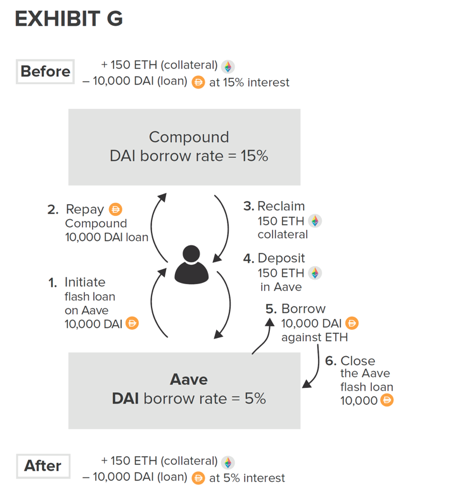

common theme in DeFi: jumping between dApps

-

Assume

- 1 ETH = 200 DAI

- supplied 100 ETH in Compound

- borrowed 10,000 DAI to lever up and purchase an additional 50 ETH

- \(\to\) also supplied to Compound

-

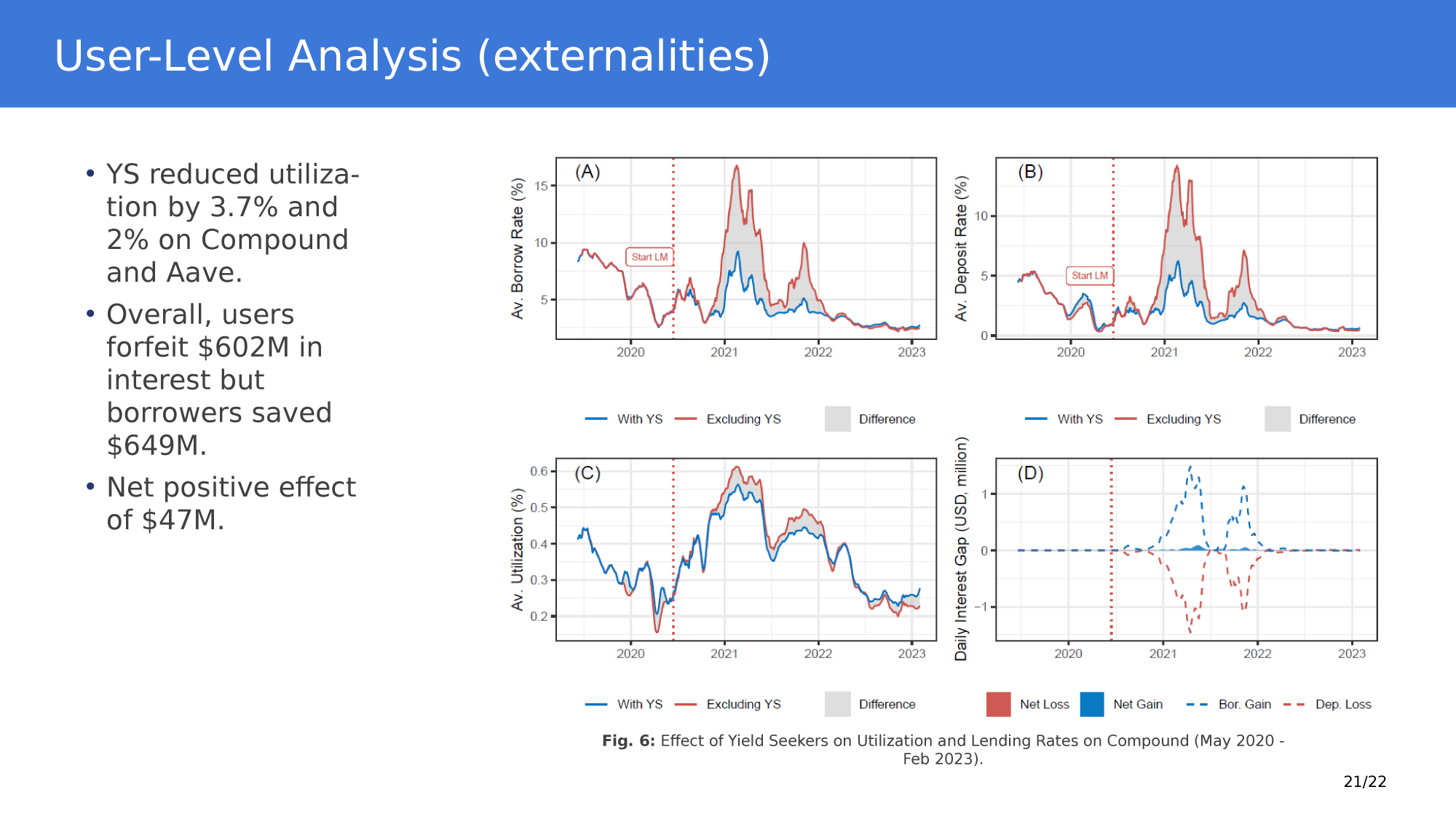

Borrow interest rate in DAI

- Compound: 15%

- Aave: 5%.

- Can you refinance your borrowing?

dapp-linking

Defi is like real "high" finance

Source: Harvey, Ramachandran, and Santoro (2020)

Dapp composability & Flash loans

1. flash-borrow DAI

5. repay DAI

3. receive ETH

4. convert ETH to DAI

2. liquidate ETH loan with DAI

Loan liquidation opportunity

- Use collateral repeatedly to lever up:

- Deposit ETH as collateral.

- Borrow USDC against it up to some LTV.

- Swap borrowed USDC to ETH.

- Deposit new ETH as collateral.

- Repeat 2–4 until near the LTV limit.

- End state: larger ETH exposure, USDC debt in the lending protocol.

Using Flash Loans for Leverage

- Has 10 ETH

- wants 22 ETH exposure

Naive Solution: Spiral Borrowing

- deposit ETH

- borrow DAI

- sell DAI

- buy ETH

- deposit ETH

- borrow DAI

- sell DAI

- buy ETH

- deposit ETH

- borrow DAI

- Price: 1 ETH = 2,000 USDC

- Collateral factor (max LTV) on ETH: 70%

- Start: 10 ETH → value = 20,000 USDC

Loop 0

- Deposit 10 ETH (20,000 USDC value)

- Borrow 14,000 USDC (70% of 20,000)

- Swap 14,000 USDC → 7 ETH

- Deposit 7 ETH → total collateral = 17 ETH (34,000 USDC)

Loop 1

- Max debt now = 0.7 × 34,000 = 23,800 USDC

- Current debt = 14,000 → can borrow 9,800 more

- Borrow 9,800 USDC, swap → 4.9 ETH, deposit

- Total collateral = 21.9 ETH (43,800 USDC), total debt = 23,800 USDC

Toy example

Result

- Start: 10 ETH, no debt

- End: ~21.9 ETH collateral, 23,800 USDC debt

- Achieved via multiple transactions and intermediate risk states

-

Flash loan: borrow with no collateral, do operations, then repay principal + fee within the same transaction; otherwise everything reverts.

-

Use it to “jump” directly to a target leveraged state:

- Flash-borrow USDC.

- Swap USDC → ETH.

- Deposit all ETH as collateral.

- Borrow USDC from the lending protocol.

- Use that USDC to repay the flash loan.

-

End state after one transaction:

- Large ETH collateral in the protocol

- USDC debt in the protocol

- No flash-loan debt

now with a flash loan

- Has 10 ETH

- wants 22 ETH exposure

Clever (gas-efficient) solution: flash loan

- flash-borrow DAI

- deposit ETH

- borrow DAI

- sell DAI

- buy ETH

- repay DAI flashloan

- Same parameters as before:

- Price: 1 ETH = 2,000 USDC

- Collateral factor: 70%

- Target: ~21.9 ETH collateral, 23,800 USDC debt

Inside a single transaction

- Flash-borrow 23,800 USDC.

- Swap 23,800 USDC → 11.9 ETH.

- Add your 10 ETH → 21.9 ETH total; deposit all as collateral.

- Collateral value = 21.9 × 2,000 = 43,800 USDC

- Max debt at 70% LTV = 30,660 USDC (we only need 23,800 + fee)

- Borrow 23,800 USDC from Aave.

- Repay the flash loan (23,800 + fee).

Toy example with flash loan

Result

- Collateral: 21.9 ETH in Aave

- Debt: ~23,800 USDC to Aave

- Flash loan fully repaid

- Same economic position as the spiral, created atomically in one transaction

Commercial Paper/T-Bill like securities

YIELD Protocol

- basic idea: zero-coupon loans

- You have:

- target asset

- collateral

- y-token trading at discount price

- examples: yDAI

- expires in 1 year

- price: $.92

- backed by ETH

- buying = you earn 8/92 cents=8.7% RoR

YIELD example

1 ETH = 150 DAI

collateralization ratio 125%

seller

buyer

Assumptions

supplies 1 ETH collateral today

mints (=borrows) 100 yDAI to be repaid in 1 year

y

receives 92 DAI today

pays 92 DAI today

y

receives 100 yDAI

repays loan with 100 DAI

deposits yDAI and receives 100 DAI

YIELD example: scenarios

seller

buyer

Scenario 1: ETH \(\ge\)125 DAI

deposits 100 yDAI

withdraws 100 DAI

receives balance of 1 ETH - 100 DAI

What does the seller own (ignore keeper fee)?

- 92 Dai (the loan)

- 0.2 ETH x price(ETH)=25 DAI (assume price=125)

seller

buyer

Scenario 2: ETH falls to <125 DAI

keeper

closes undercollateralized position \(\to\) sells 0.8 ETH for 100 DAI

receives 100 DAI early

receives balance

of 0.2 ETH

categories of finance

What do banks/financial institutions do?

disclaimer: an incomplete list

Bitcoin,

stablecoins, etc.

"higher layer"

lending

payments processing

financial

advice

trading

services

funding

services

prop trading to manage risks

too early, but projects are underway

as it turns out, these items are often directly related

what could defi do?

Five key problems in finance

Defi vs Legacy finance

interoperability

inefficiency

centralized control

limited access

opacity

interchange (=VISA) fees, settlement times, microtransactions, physical infrastructure

between-institution or transfers, reconciliation process, international remittances, various securities custody and trading systems

information for users, health of deposit taker, what-happens-behind-the-scenes, counterparty risk

local monopolies/switching costs, central banking, deposit concentration, control vs. competition

1.7B unbanked in the world, 24M in the US, many services or products not available based on location etc, lack of SME support, inability to collateralize

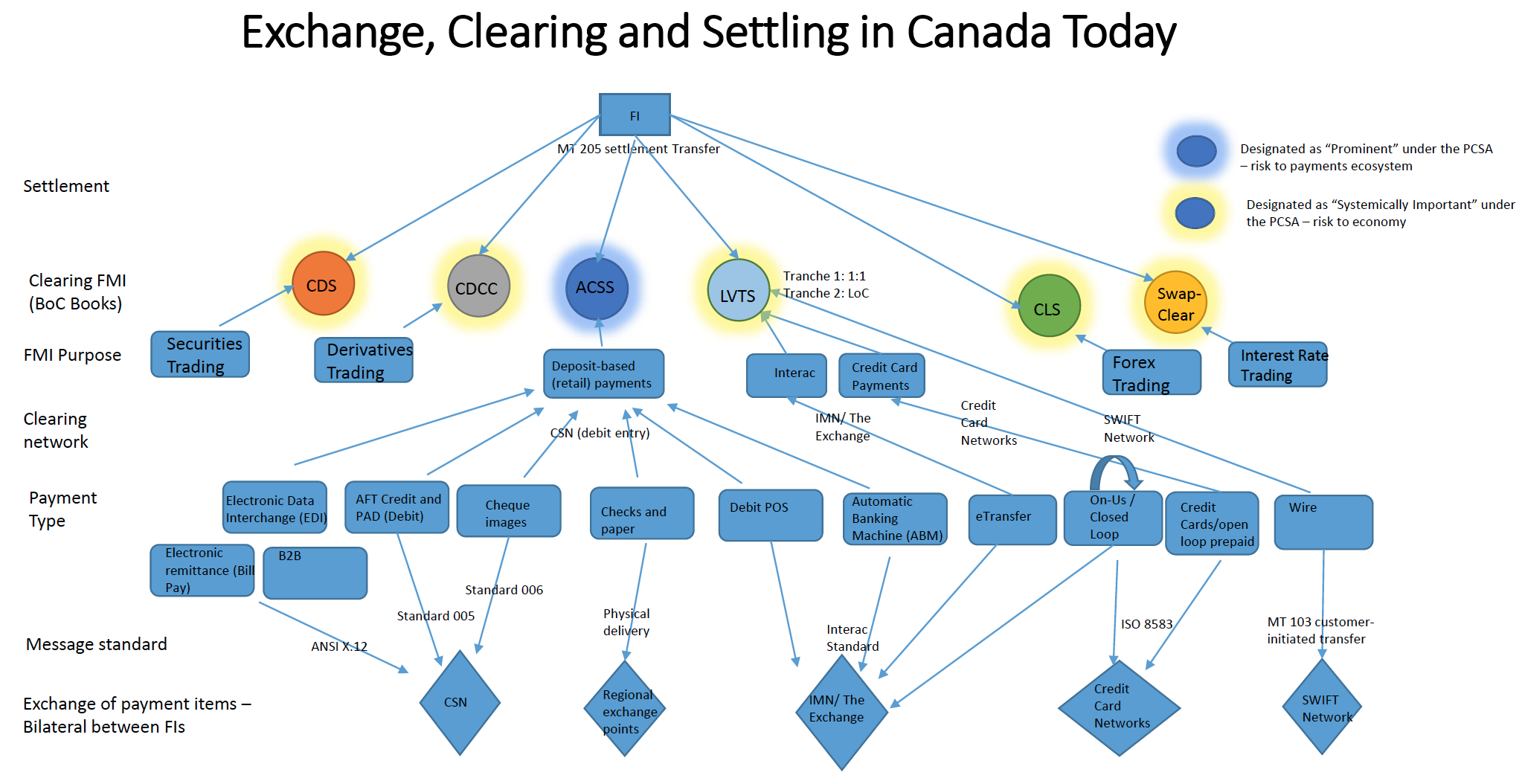

Source: Wendy Rotenberg's Payments lecture

payments pieces

simplified view

CDS

ACSS

LVTS

Cheques

Debit at POS

e-transfer

Credit Card/

open loop

ATMs

Wire

Interac

Credit

Card

deposit based retail

Interac standard

credit card network

SWIFT

CSN

Settlement

Clearing process

Underlying network

Type of payment

Financial market infrastructure purpose

Securities Trading

why blockchain?

a common resource

e-transfer

Wire

deposit based retail

CDS

Securities Trading

derivatives

swaps

property registry

interoperability

inefficiency

centralized control

limited access

opacity

siloed legacy system

is interoperable by design

reduces frictions and separates service from "commodity"

decentralized control and common operation

fewer barriers\(\to\) broad access

is/can be highly transparent

common infrastructure system

categories and assessment for defi

Our focus

interoperability

inefficiency

centralized control

limited access

opacity

- What do the projects do?

- How do these projects improve on legacy limitations?

payments

lending

trading

services

funding

services

prop trading

manage risks

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/