MGT444: Fintech

FinTech Lending

Topic:

- What is FinTech lending?

- Why does it matter?

- What is different about FinTech lending?

- Why do we see it?

- SME lending?

FinTech Lending: questions we want to answer

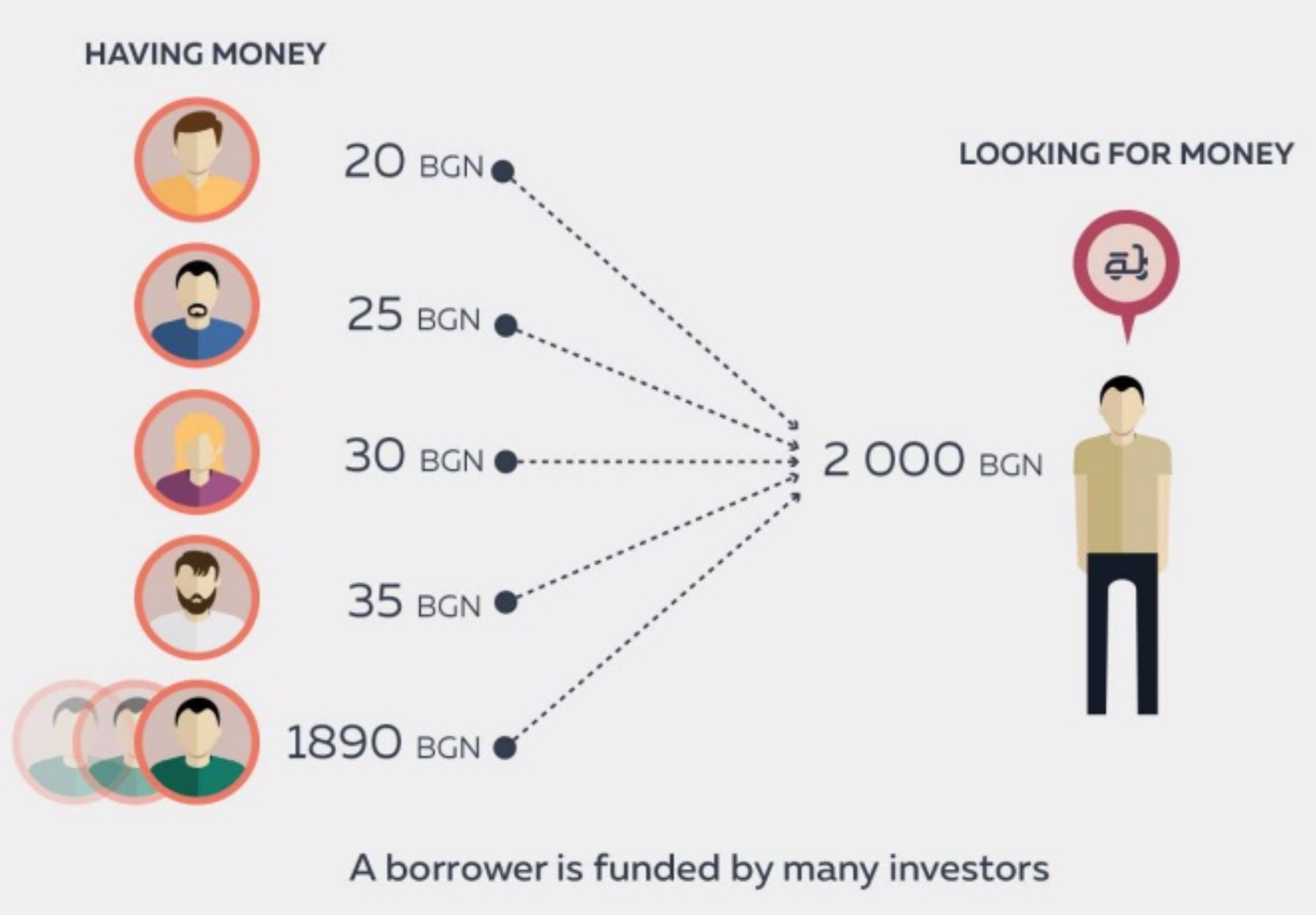

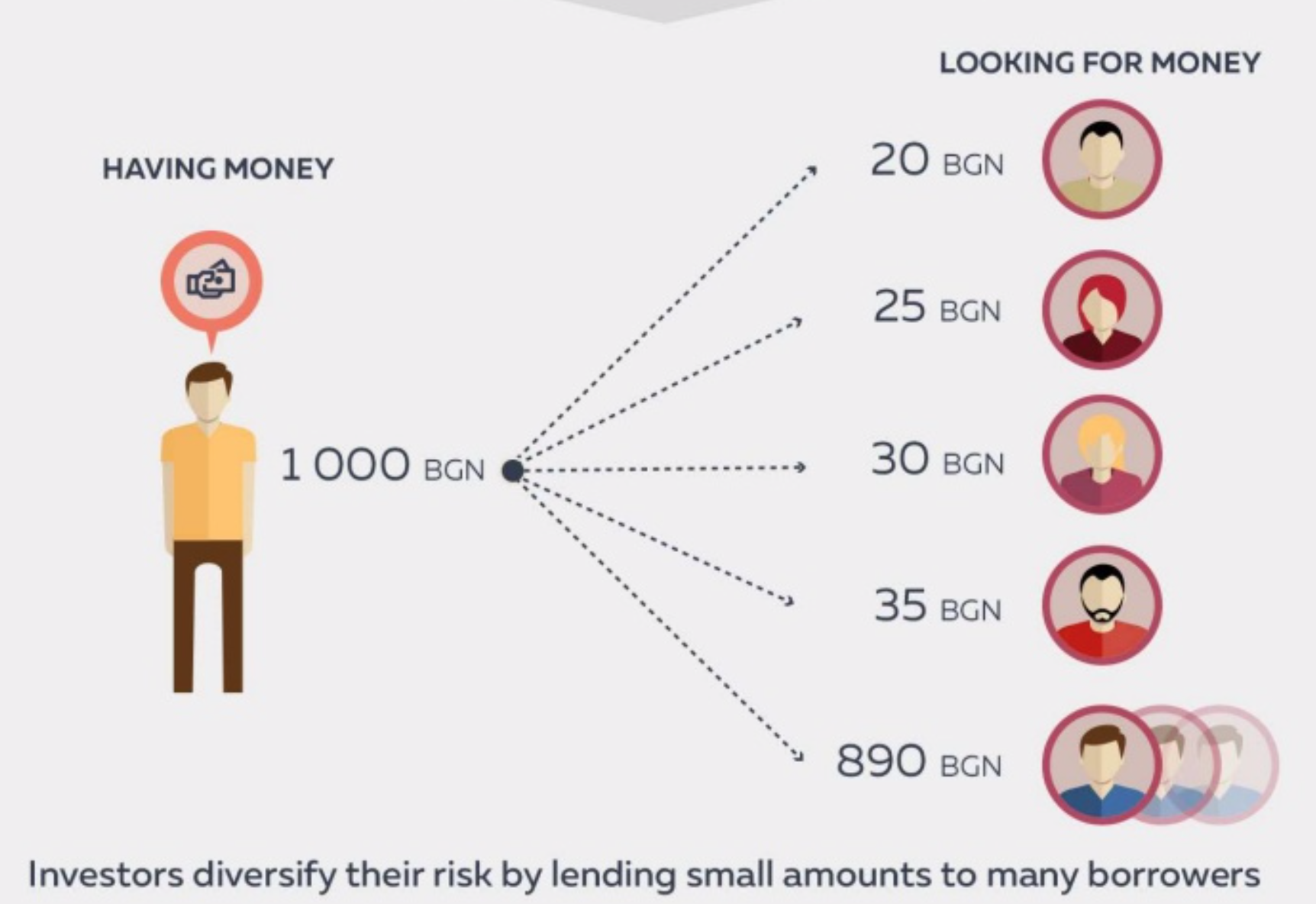

What is FinTech Lending?

Original Idea: Peer-to-peer (P2P)

Original Idea/Pitch?

Good timing to pitch the "sharing"?

-

Borrowers would post

- financial information

- maybe a picture

- how much they want to borrow, maximum interest rate

- why they wish to borrow

- hope that their peers will loan at a better rate than the card issuer (why might they?)

- Peers:

- review the loan requests

- can choose the loans & amounts to invest

Sidebar: on the usage of photos

From Ravina, Enricetta. 2018. “Love & Loans: The Effect of Beauty and Personal Characteristics in Credit Markets.” Working Paper

- Borrowers whose beauty is rated above average

- are 1.41 percentage points more likely to get a loan and, given a loan,

- pay 81 basis points less than an average-looking borrower with the same credentials.

- Black borrowers pay between 139 and 146 basis points more than otherwise similar White borrowers, although they are not more likely to become delinquent.

- personal characteristics are not, all else equal, significantly related to subsequent delinquency rates -

- with the exception of beauty, which is associated with substantially higher delinquency probability

Original Idea: Peer-to-peer (P2P)

Over time ...

Over time ...

- Lending platforms became more involved in the decisions

- Make a credit risk evaluation and set an interest rate

- Investors: can only decide if they want to be a part of it or not

- Over the years:

- information provided to lenders has gone down

- most "peer" lenders now are institutions (95%(?))

Over time ...

- Institutional investors automatically buy loans based on the platform’s risk assessment and pricing

- Loans are securitized

- Assemble a pool of loans, issue securities backed by that pool

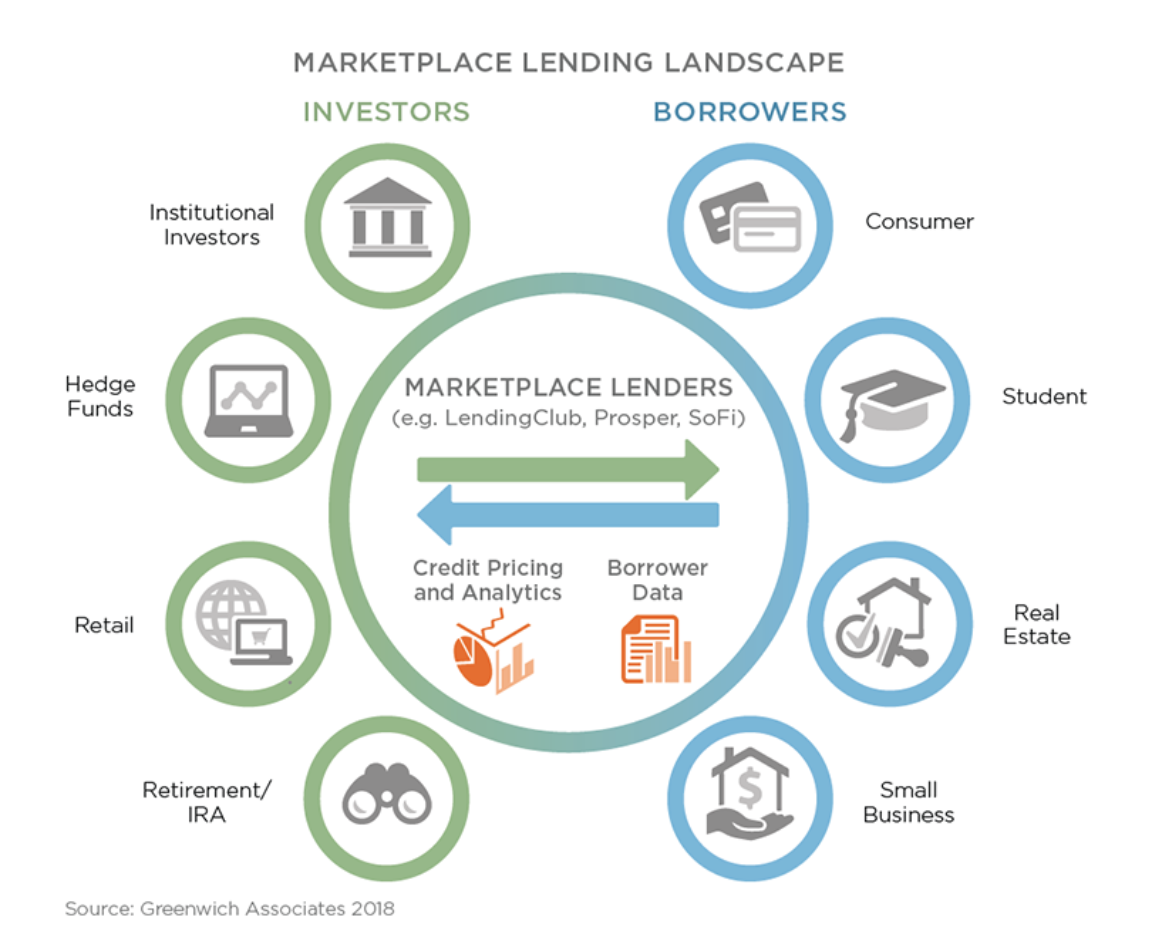

Marketplace Lending (formerly P2P)

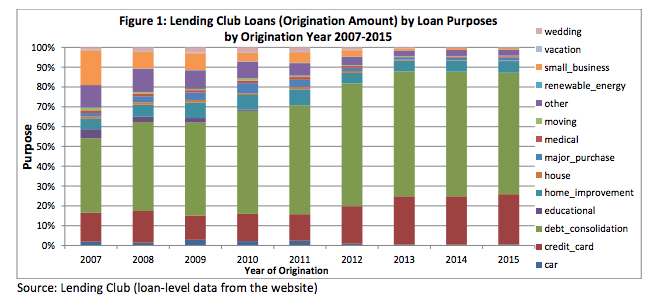

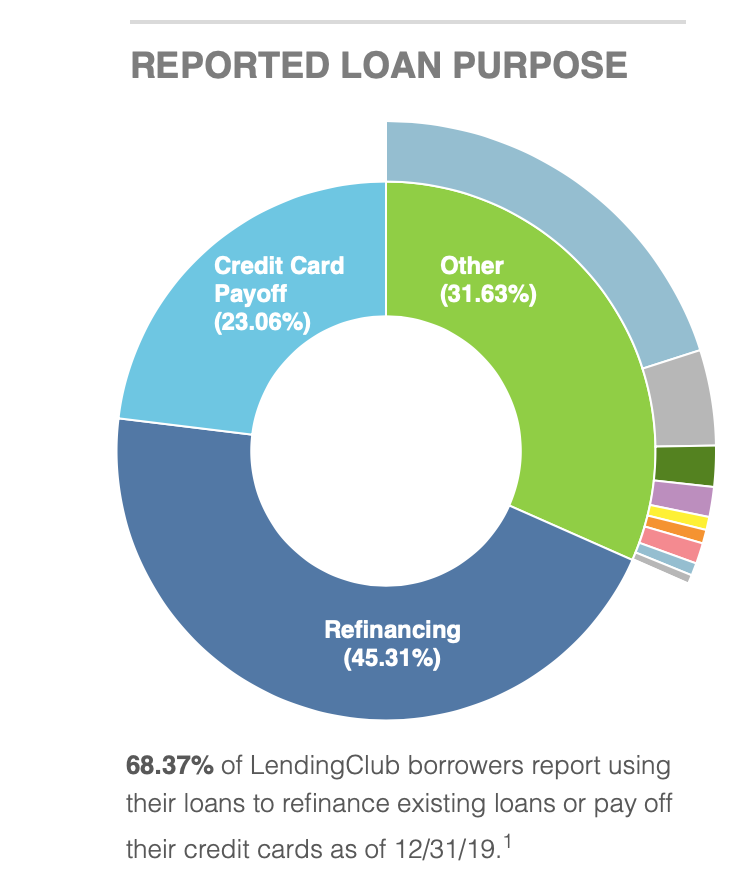

What do people use FinTech Lending for?

price for loan

effort required to get loan

What do people use the online lenders for?

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

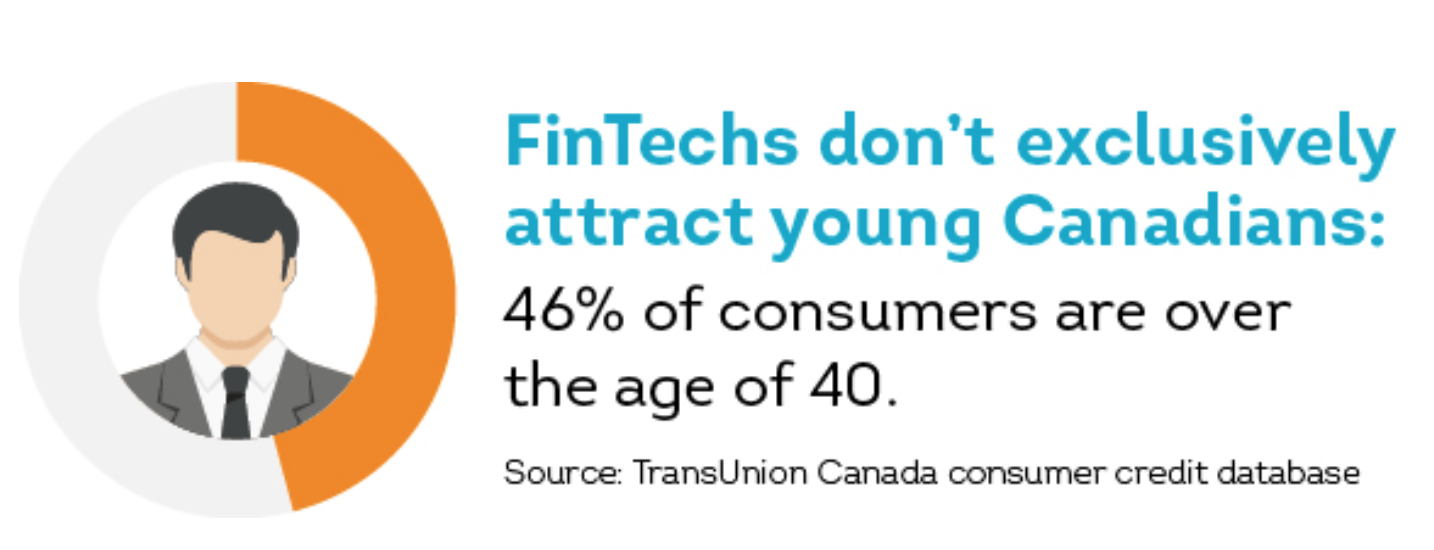

Who uses FinTech lenders? (Canada)

compared to 53% for consumers with personal loans from traditional banks

NB: this data/picture is a few years old. At the time, people under 40 were "millennials"

Who uses FinTech lenders? (Canada)

Why does it matter?

- Unsecured loans #1

- $3.7 trillion purchase volume in 2018

-

Debt has fallen from 64.7 percent in 1996 to 26.5 percent in 2018

- $900 billion in balances at the end of 2018

- $4.3 trillion total credit lines, APR >20%

- Balance vs payment:

- ~60% pay balance in full

- ~40% do not pay in full and keep a balance

- Interest rates: >20%

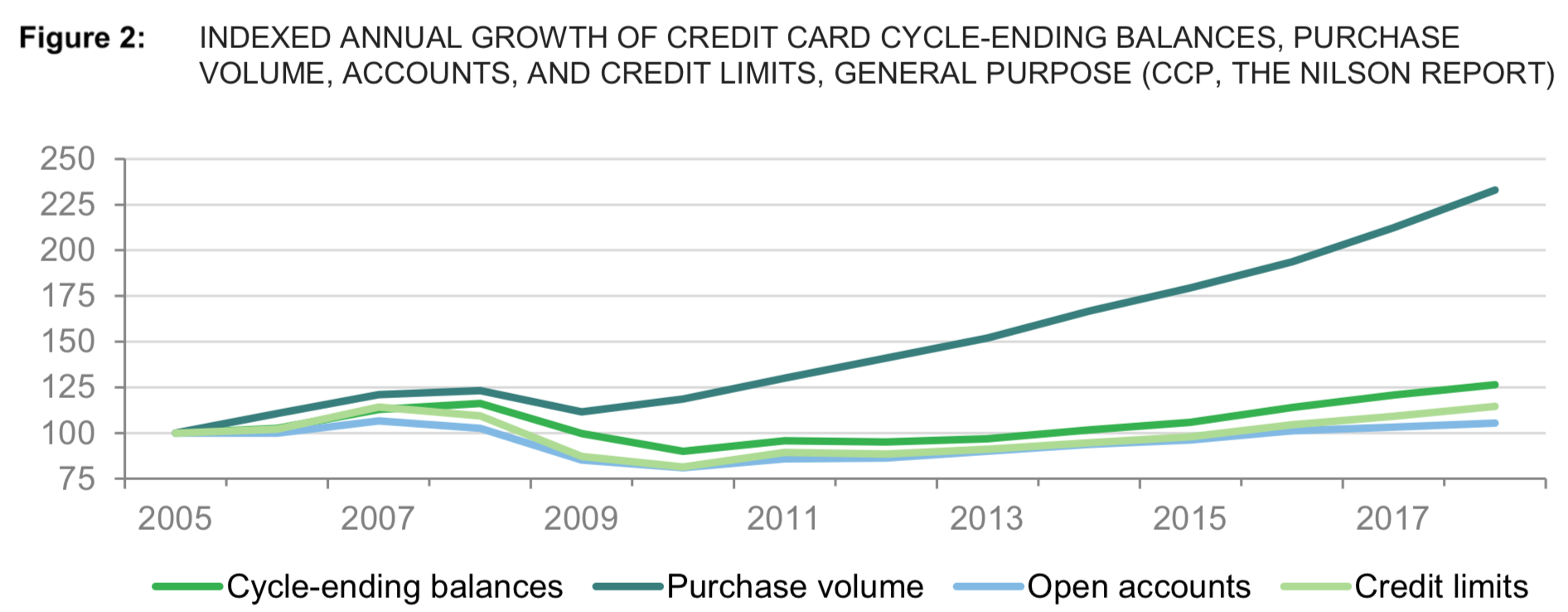

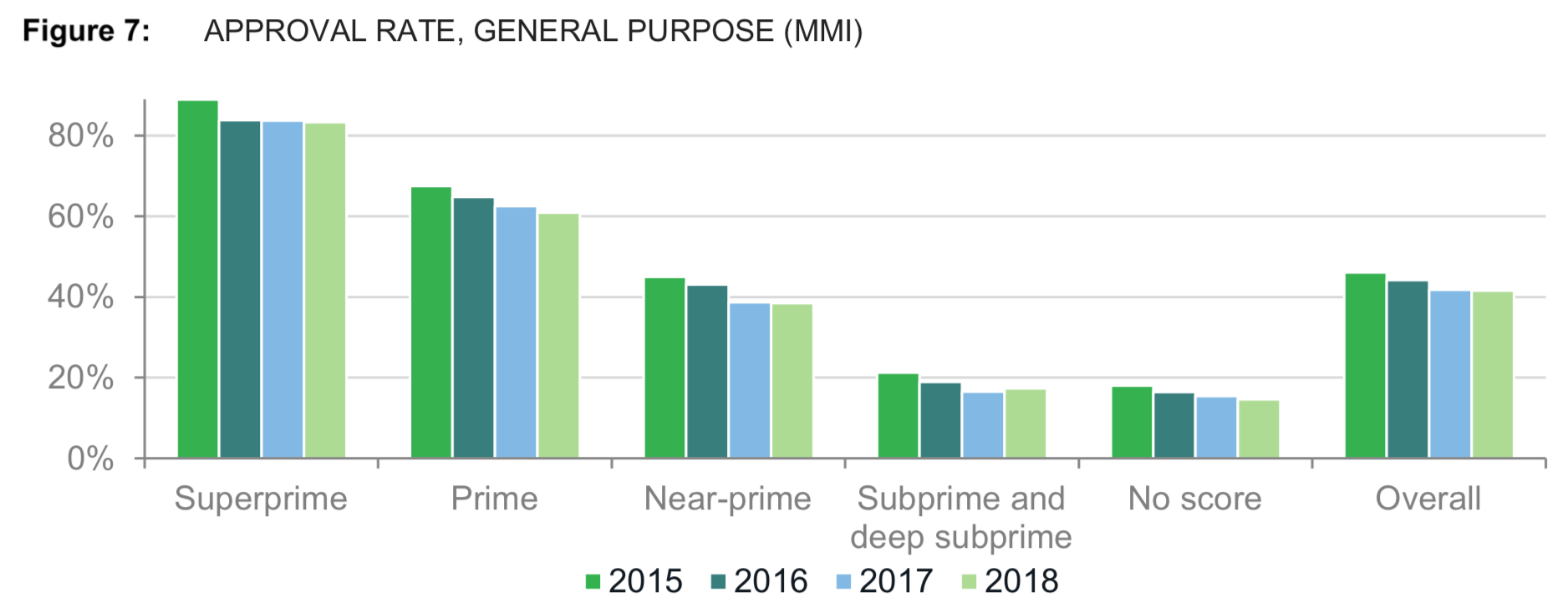

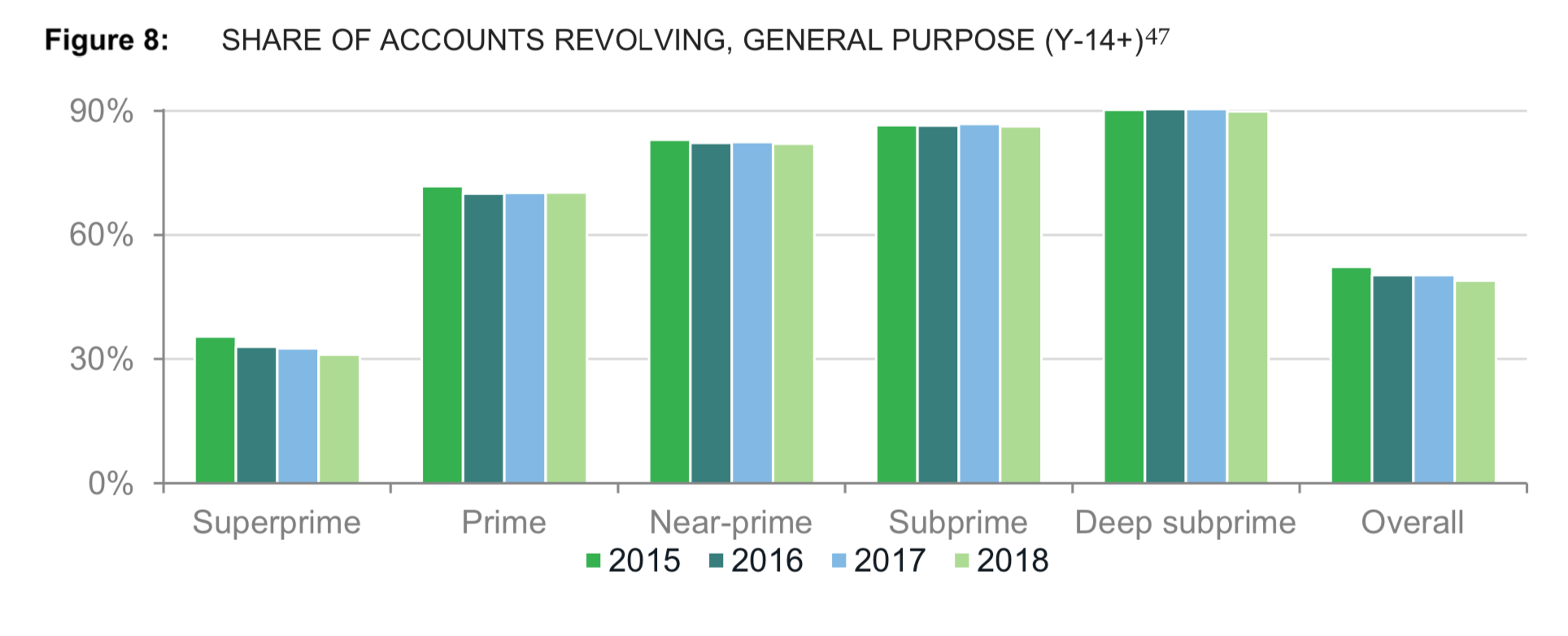

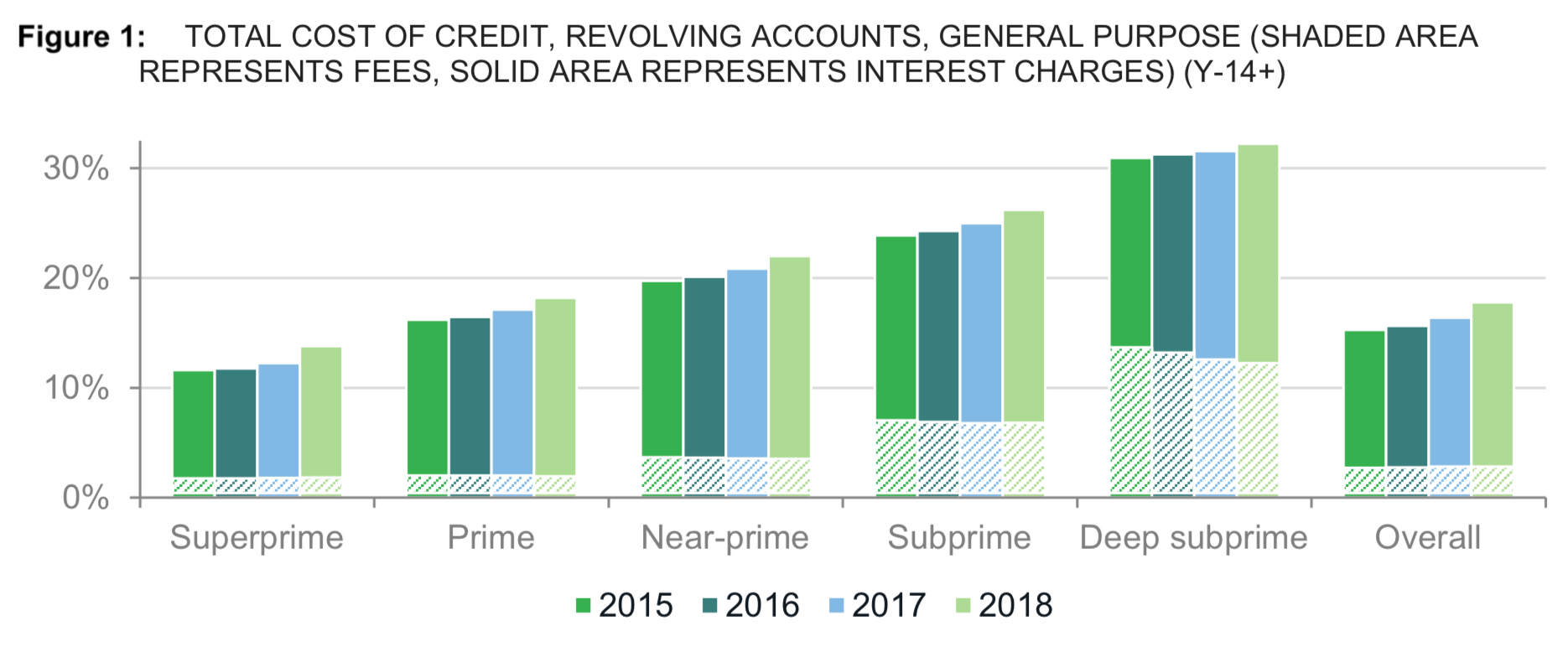

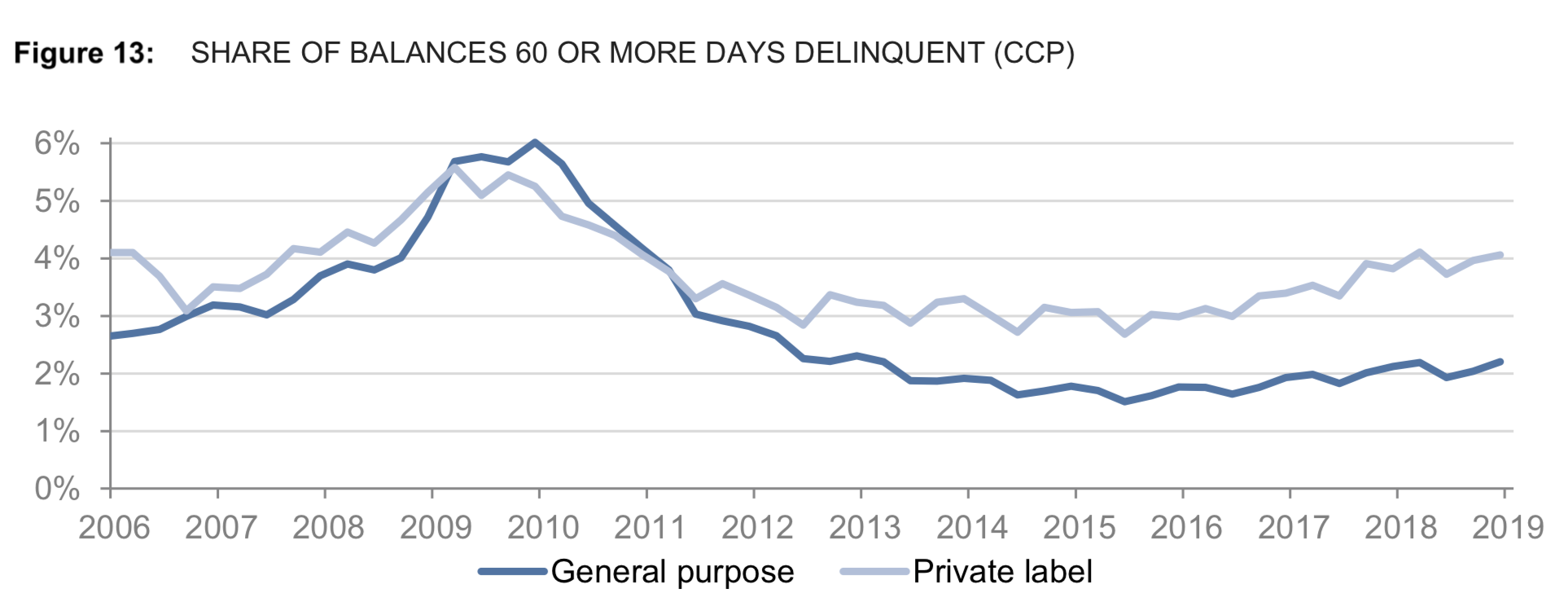

Existing Credit markets: Credit Cards

(U.S. Stats)

Canadian Bankers Association:

- 70% of Canadians pay back credit card in full

- \(\Rightarrow) 30% hold a balance

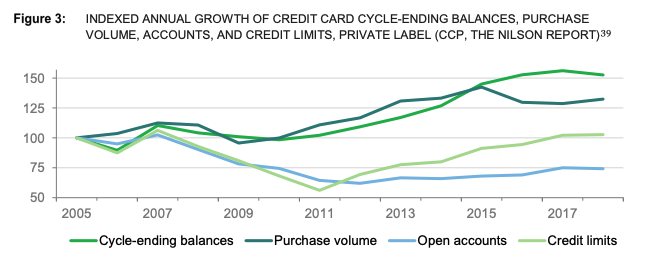

Existing Credit markets: Decreased use as "credit"

small caveat: high balances for "private label" cards (e.g., store cards)

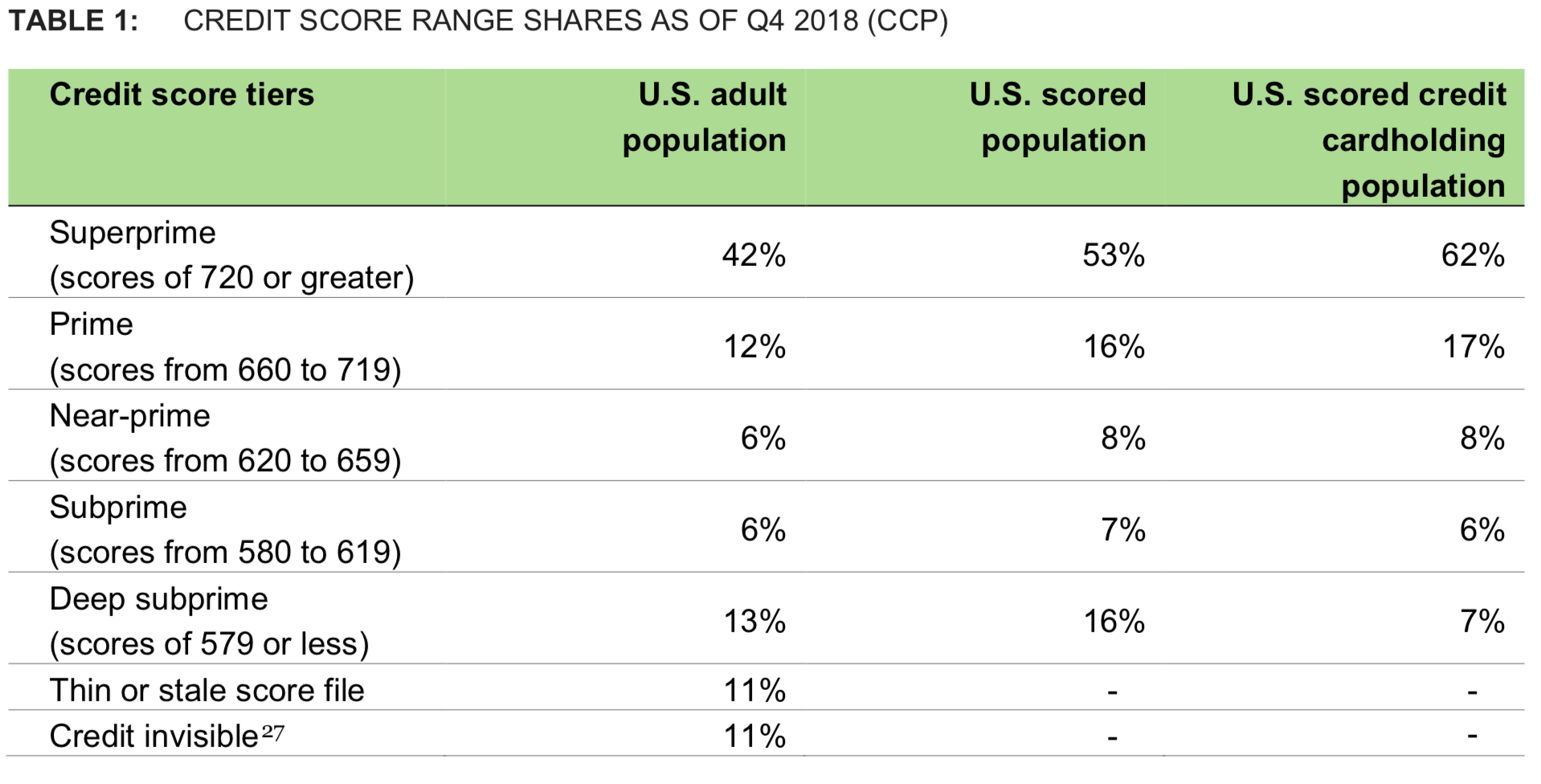

Existing credit markets: who is "scored"?

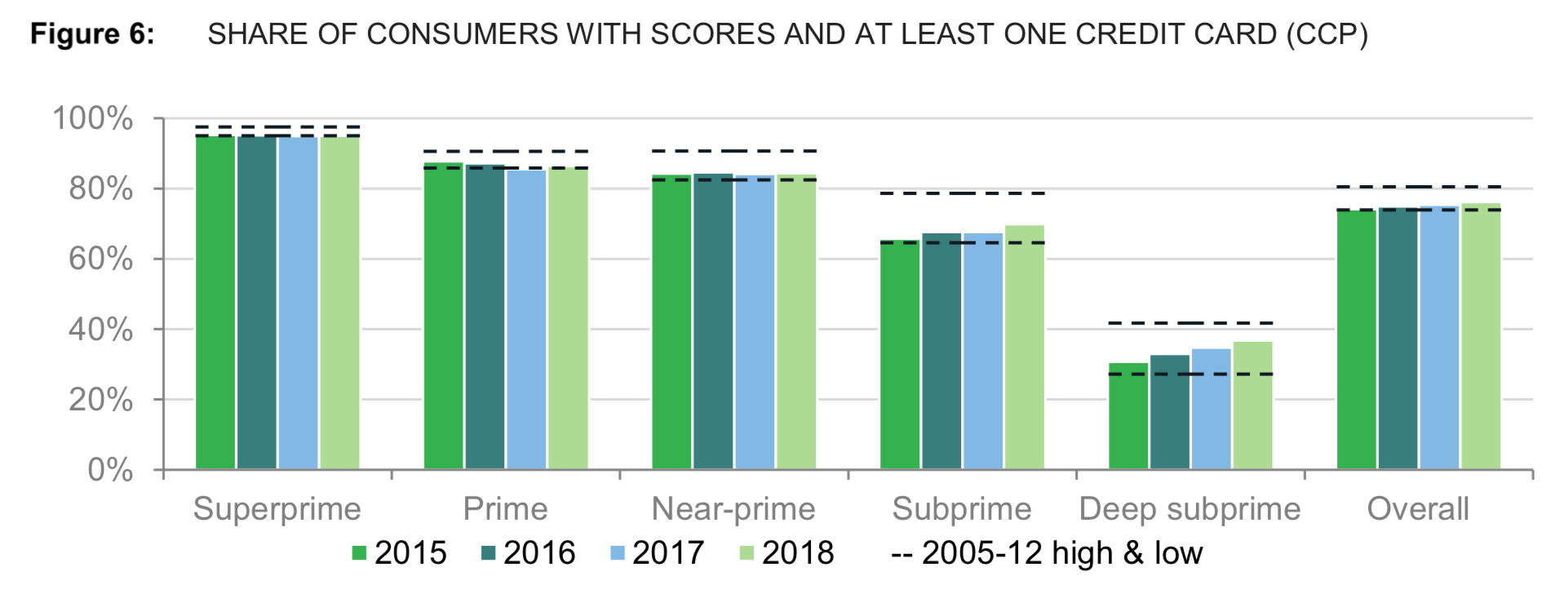

Credit cards: who uses them?

Credit cards: how easy to get?

Credit cards: usage as "credit" (revolving) vs. "payments"

Credit cards as "credit": costs

Credit cards as "credit": delinquency losses

basic portfolio math

- average rate earned per consumer: 13-15%

- average losses on portfolio: 2-4%

- => average return on portfolio: 9-13%

Is this market ripe for disruption?

Is this market ripe for disruption?

- high returns on the portfolio

- everyone offered the same APR => not a lot of risk-based differentiation

- alternative loans (e.g., personal loans) are hard to get

Why is there an opportunity?

All types of consumer credit are ripe for disruption!

Example: student loans. Very low hanging fruit!

All students within a cohort get the same interest rate.

\(\to\) Find the graduates that do well & "cream-skim"!

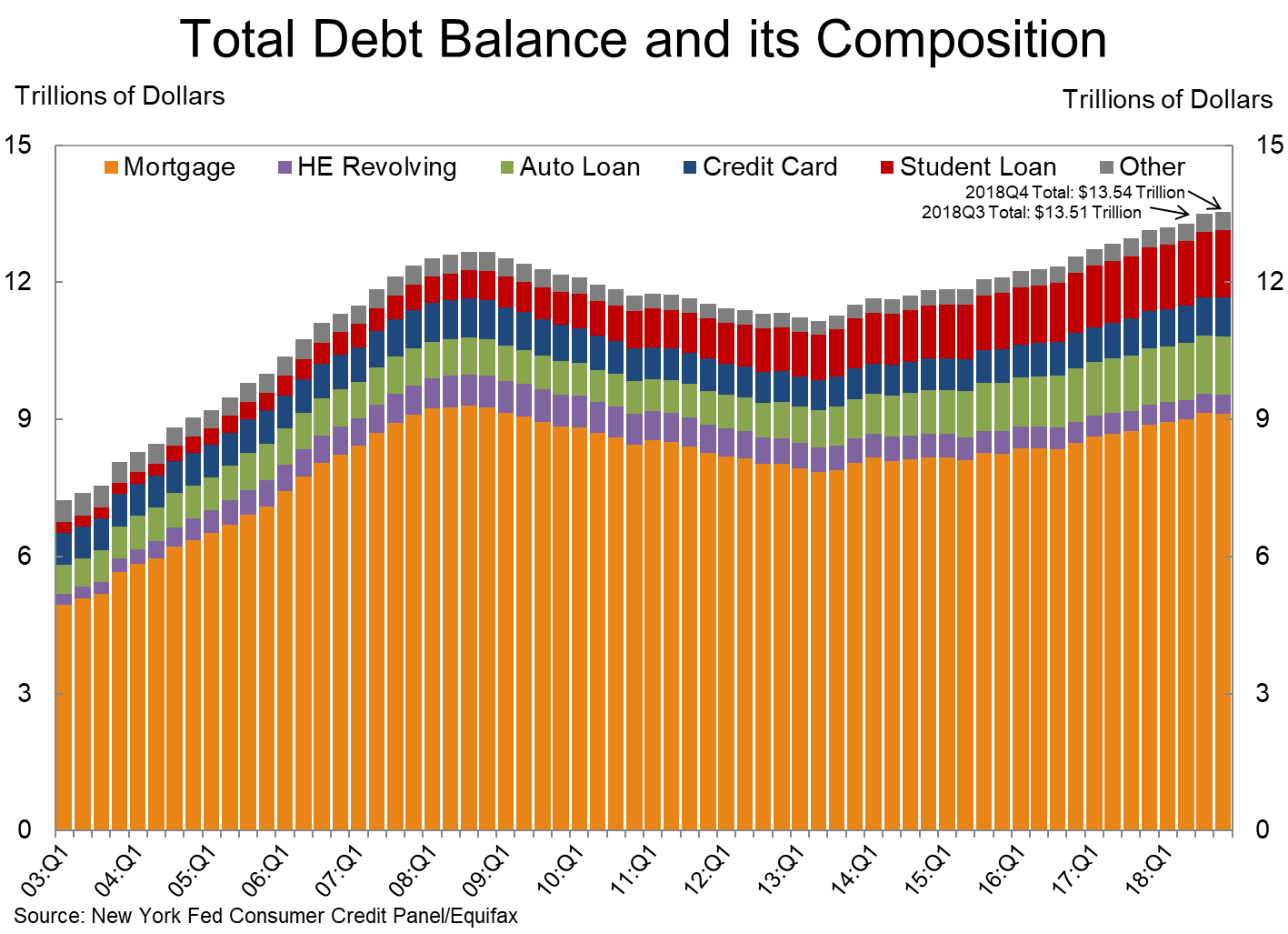

Example: home equity loans

*

*HELOC=home equity line of credit

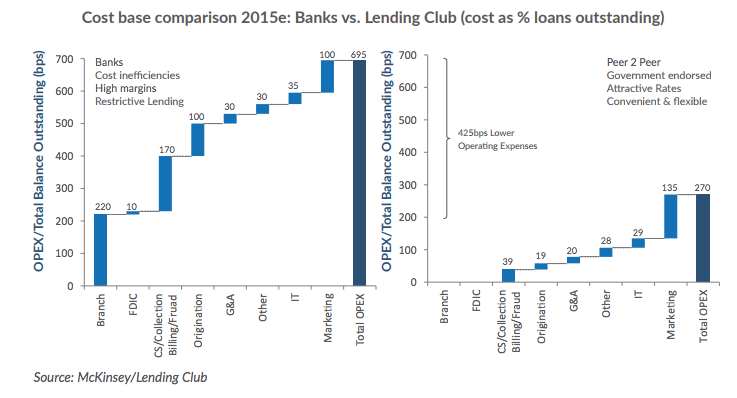

Why do we see it?

425bps!

Costs: Lending Club vs. A Bank

G&A=general administrative expenses

OPEX=operational expenditures

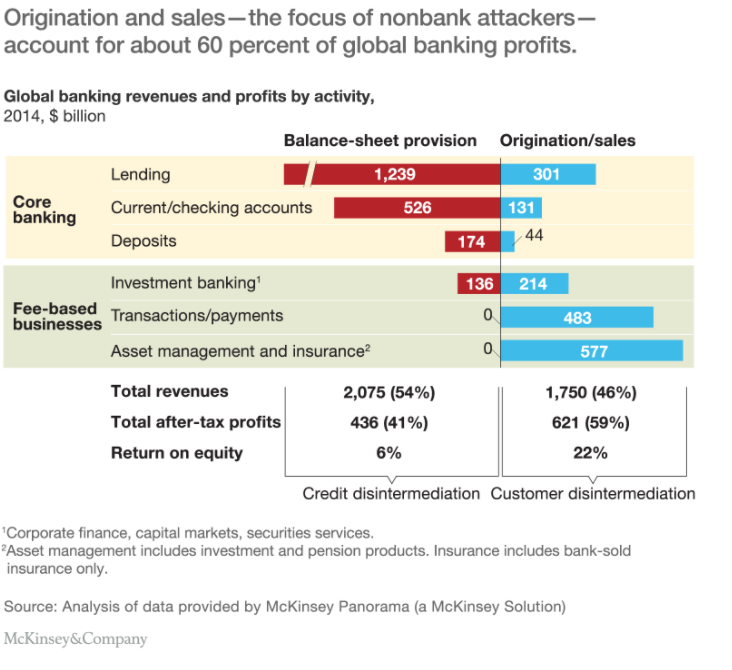

McKinsey: 59% of the banks’ earnings flow from pure fee products as well as the origination, sales, and distribution

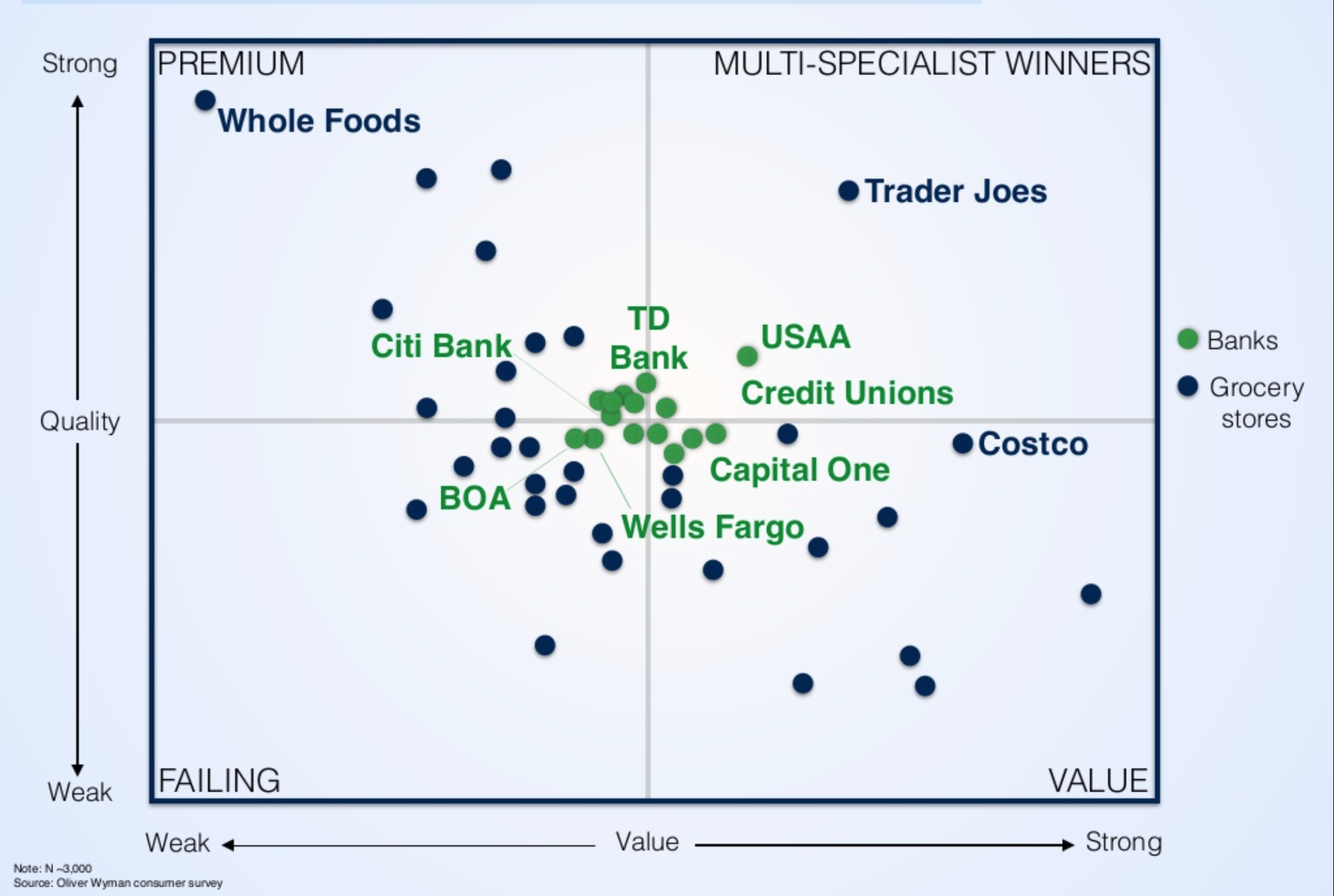

Costs aside, there is very limited differentiation among banks!

Banks even look the same!

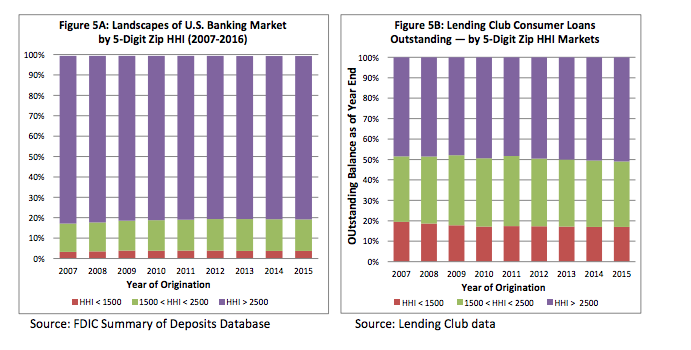

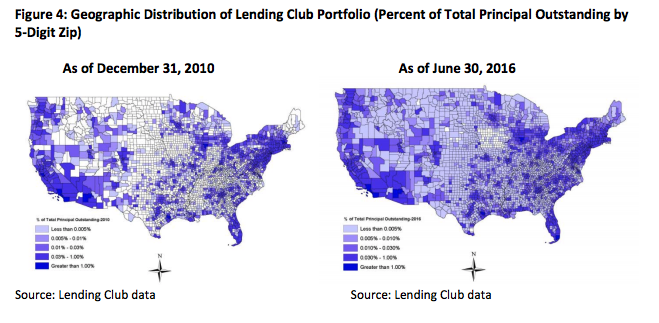

Lending Club filled a niche: went to ZIP codes where competition was low!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Critically: they did scale up!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

FinTech lenders aim to find a niche ....

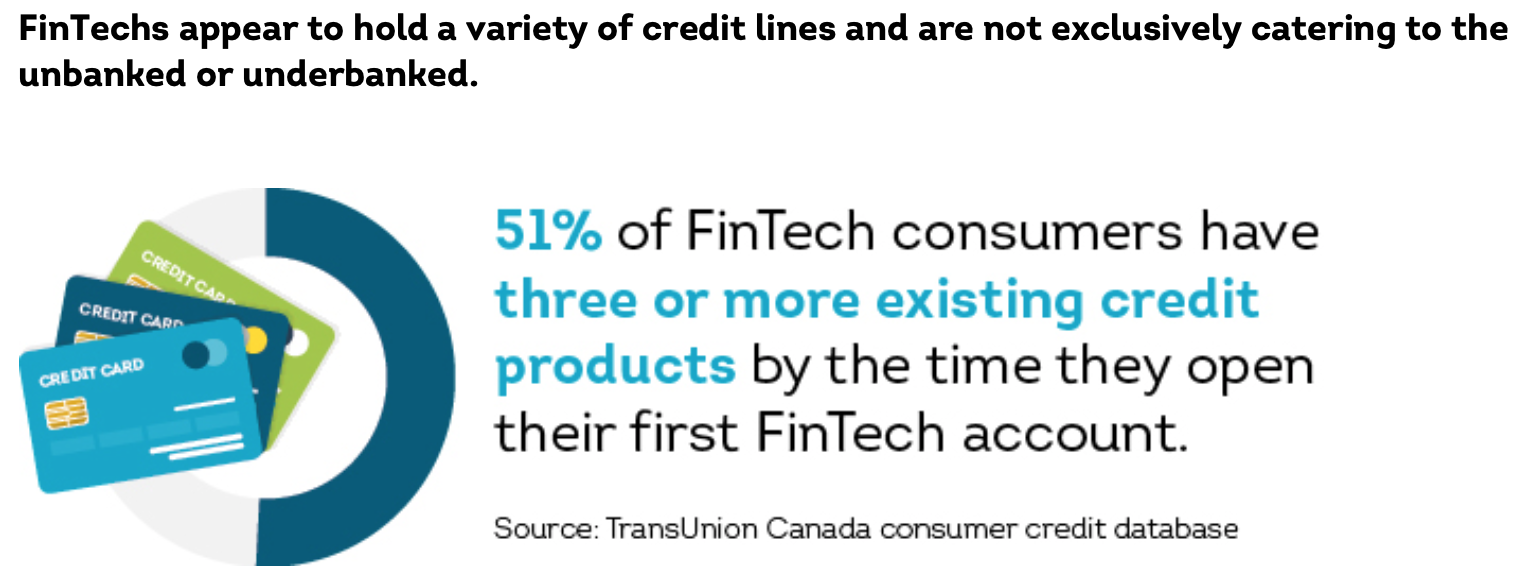

TransUnion study in Canada:

- FinTech portfolios are comprised of riskier consumers

- significantly higher consumer base within the subprime space.

- higher delinquency rates across all risk tiers

- higher interest rates for personal loans

- These lenders seek to satisfy market demand among consumers who may not have access to traditional lending sources.

Here's a view from Canada (less positive than for the U.S.)

FinTech lenders aim to find a niche ....

TransUnion study in Canada:

- FinTechs are focused on technology over risk management

- Limited evidence of a risk-based strategy for pricing risk or assigning loan size based on a consumer’s risk profile

- A one-size-fits-all approach

- similar loan sizes and interest rates being issued regardless of a consumer’s credit score.

https://www.transunion.ca/blog/fintechs-in-canada

Word of caution: I haven't been able to find the study (released Feb 25, 2020). Take the TransUnion blog conclusion with a grain of salt.

(Many FinTechs do their own credit scoring!)

FinTech lenders aim to find a niche ....

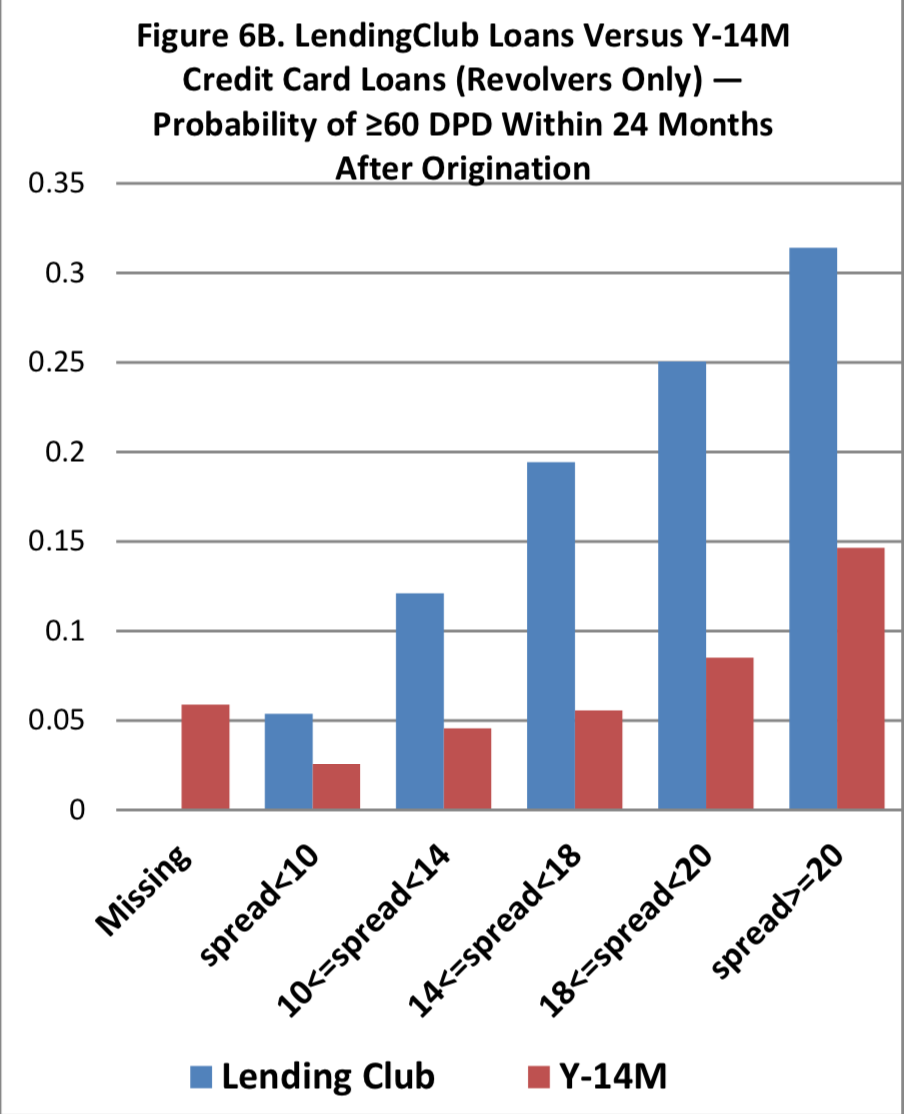

[Lending Club's] model attempts to identify applicants with FICO scores that do not reflect their true credit quality, and thus the risk could have been mispriced based on FICO scores alone.

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

What is different

about FinTech Lending?

- about 33% of borrowers with FICO scores below 620 default

- \(\to\) 67% do not default!

(Upstart’s Paul Gu)

Why are they better?

What do FinTech lenders do differently?

FinTech lenders: Better data and better techniques

Old days:

- FICO/Vantage scores

- work only with credit history

- 26 million people in the US have "thin" credit history

- \(\to\) ask Canadian immigrants if they can get a loan...

"FinTech lenders use technology to obtain new kinds of data that can make lending decisions more efficient and informed."

Goldstein, I., J. Jagtiani, and A. Klein. 2019. “Fintech and the New Financial Landscape.” Bank Policy Institute (BPI): Banking Perspectives, Q1:7, March 2019.

Sidebar: academic insights from how data can be used well

New Days: Alternative data and machine learning

-

Soft information (Iyer, R., A. Khwaja, E. Luttmer, and K. Shue. 2016. “Screening Peers Softly: Inferring the Quality of Small Borrowers.” Management Science 62(2): 1554‒1577)

- whether the borrower posts a picture

- the number of words used in the listing text descriptions,

- friend endorsements

- social networks

example 1

New Days: Alternative data and machine learning

Flavour of the month: text-based analysis

- Gao, Q., M. Lin, and R. Sias. 2017. “Word Matters: The Role of Texts in Online Credit Markets.” Working Paper:

- use natural language processing (NPL)

- analyze textual information from borrowers’ writing on online lending platforms.

- quantify the informational content of lengthy personal text descriptions, linguistic style

- lenders tend to bid more aggressively, are more likely to grant credit, and charge lower interest rates to borrowers whose writing is more readable, more positive, and contains a lower level of deception cues.

- Note: Lenders are required to demonstrate that the use of alternative data does not result in biased credit decisions against certain segment of the borrowers, such as race and gender.

example 2

New Days: Alternative data and machine learning

Berg, T., V. Burg, A. Gombovic, and M. Puri. Year? “On the Rise of Fintech — Credit Scoring Using Digital Footprints.” Working Paper:

-

email contains their real name

-

make purchases at night time

-

number of typing mistakes

-

even the simple, easily accessible digital footprint variables as good as the Equifax Risk Score in predicting loan outcomes.

-

together with the Equifax Risk Score \(\nearrow\) model’s predictive power

example 3

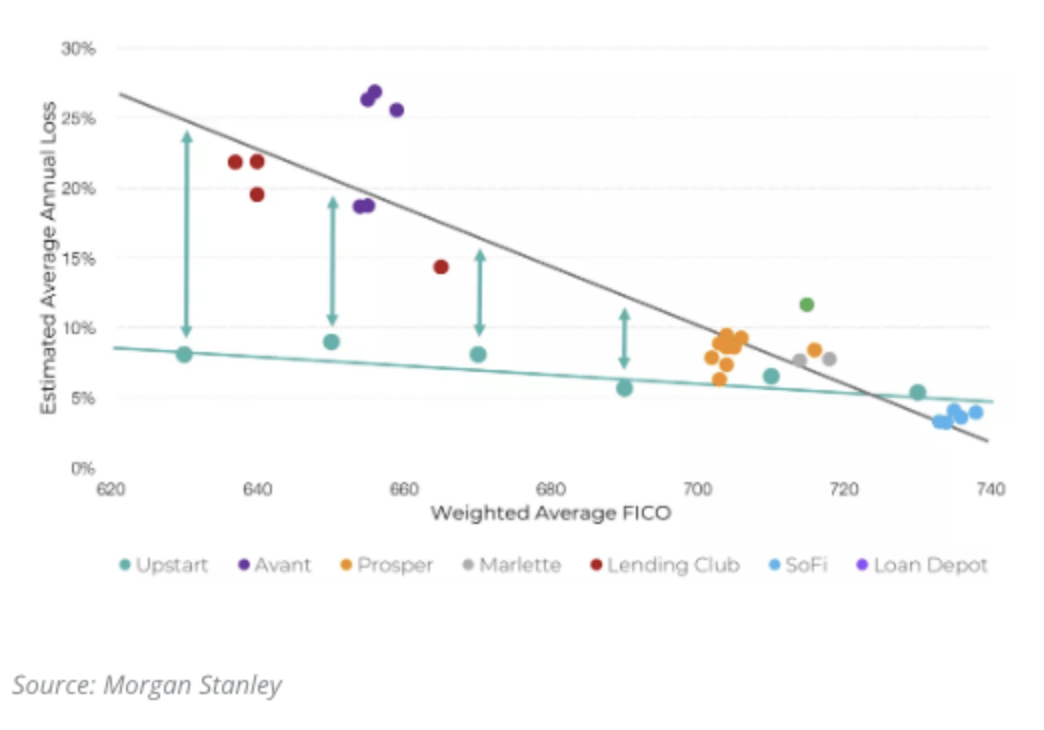

How do better data and better data analysis help FinTech Lenders?

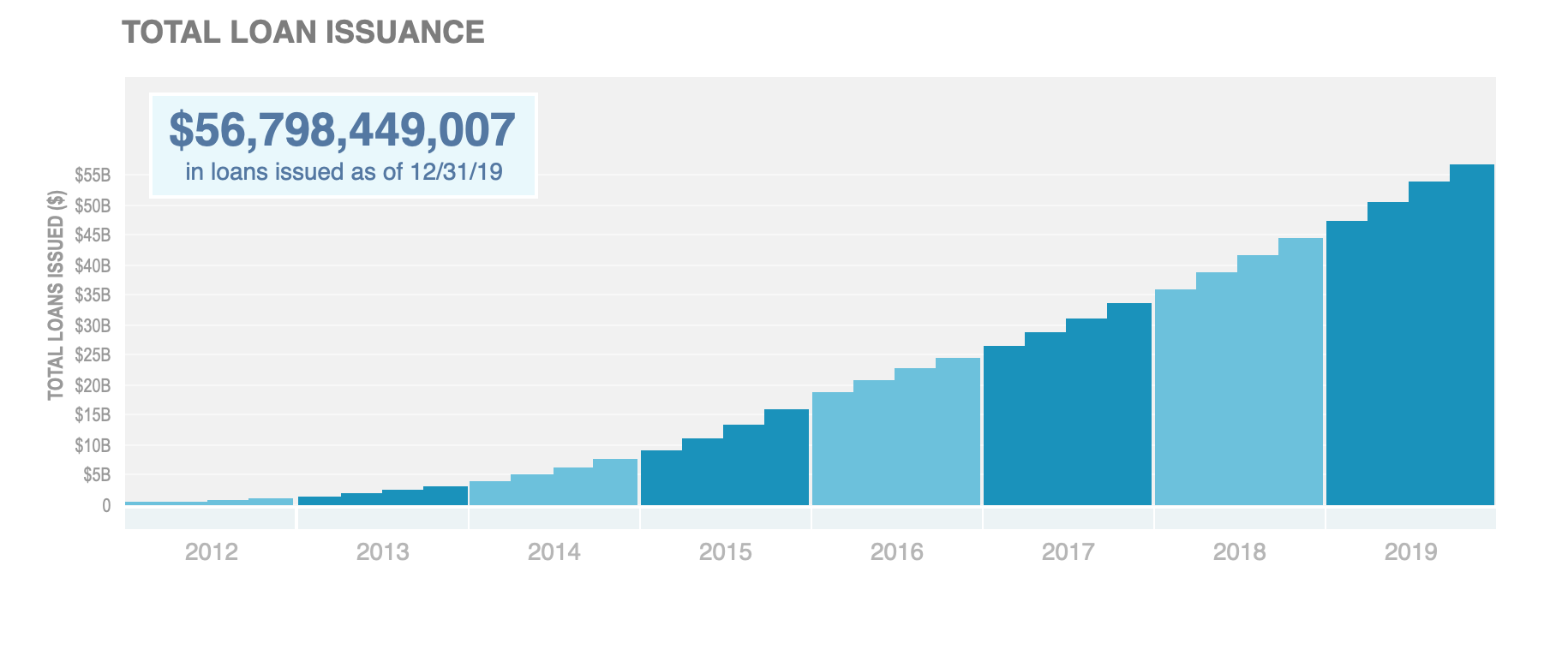

Lending Club: steady growth of loans!

What are key components to their success?

quick note: Lending Club posts a ton of data on its website \(\to\) that's why there is a lot of research on it

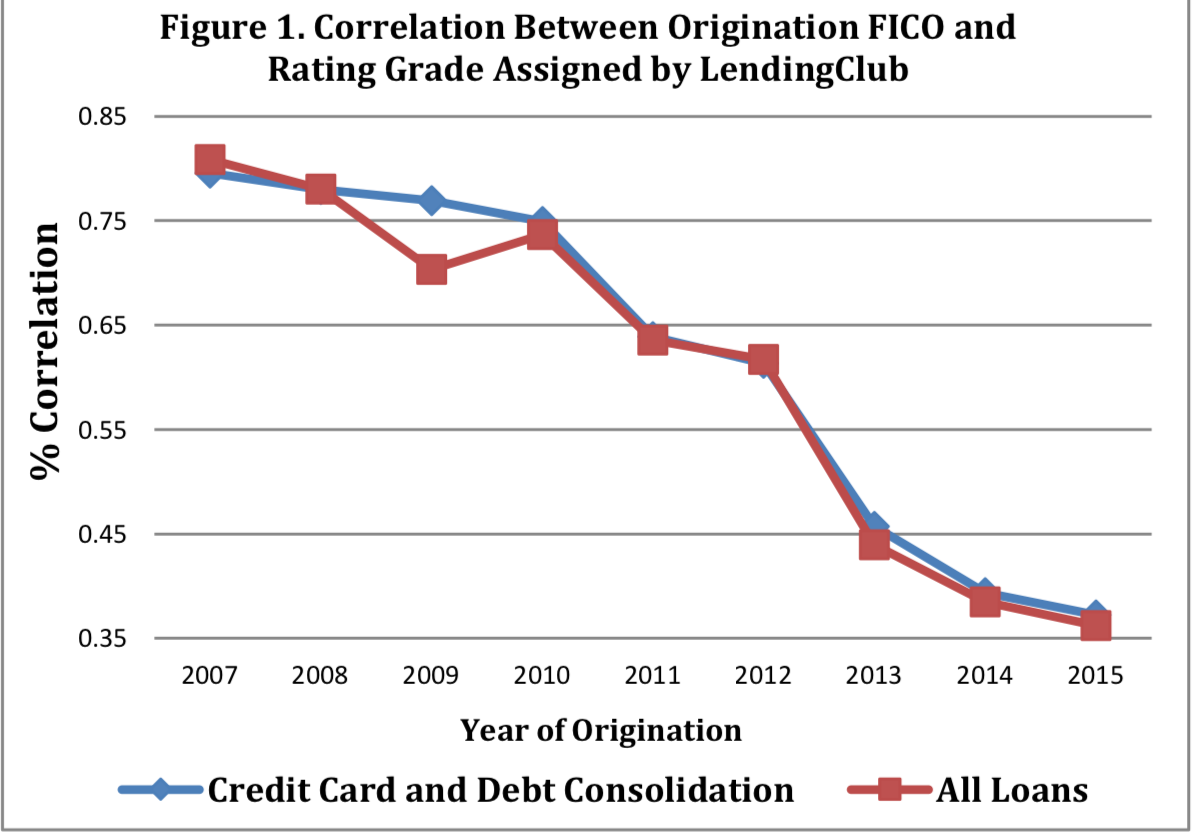

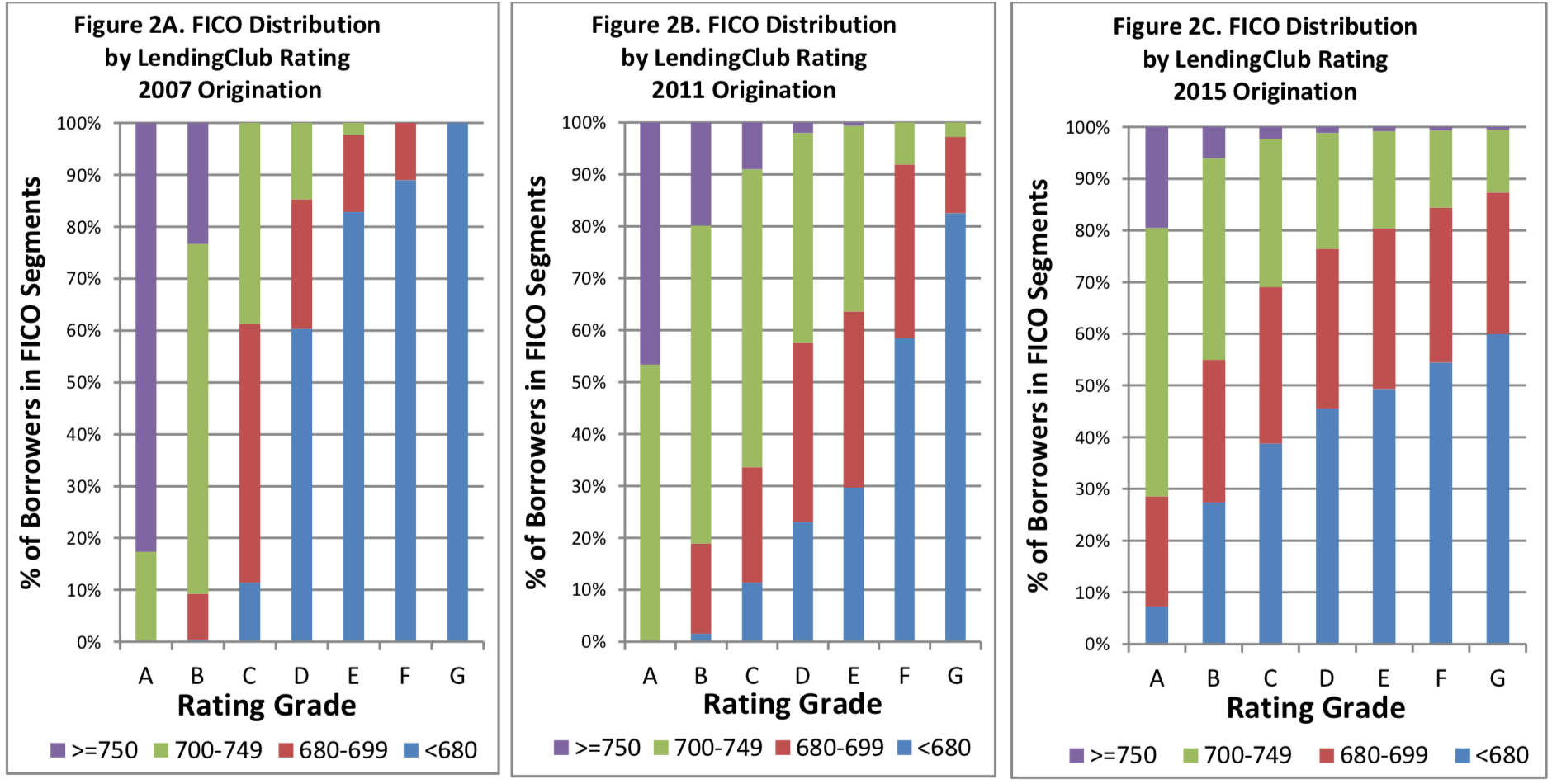

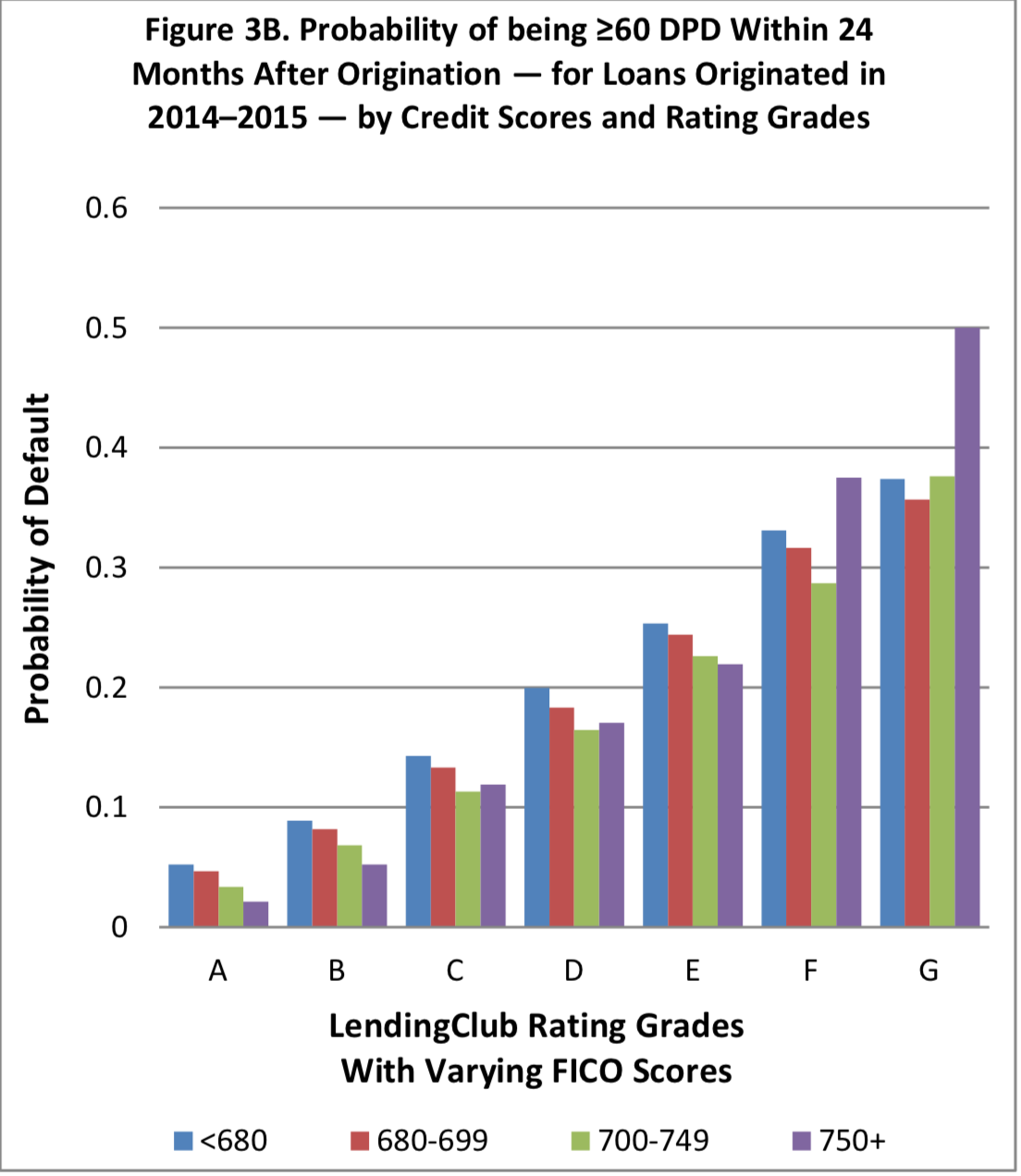

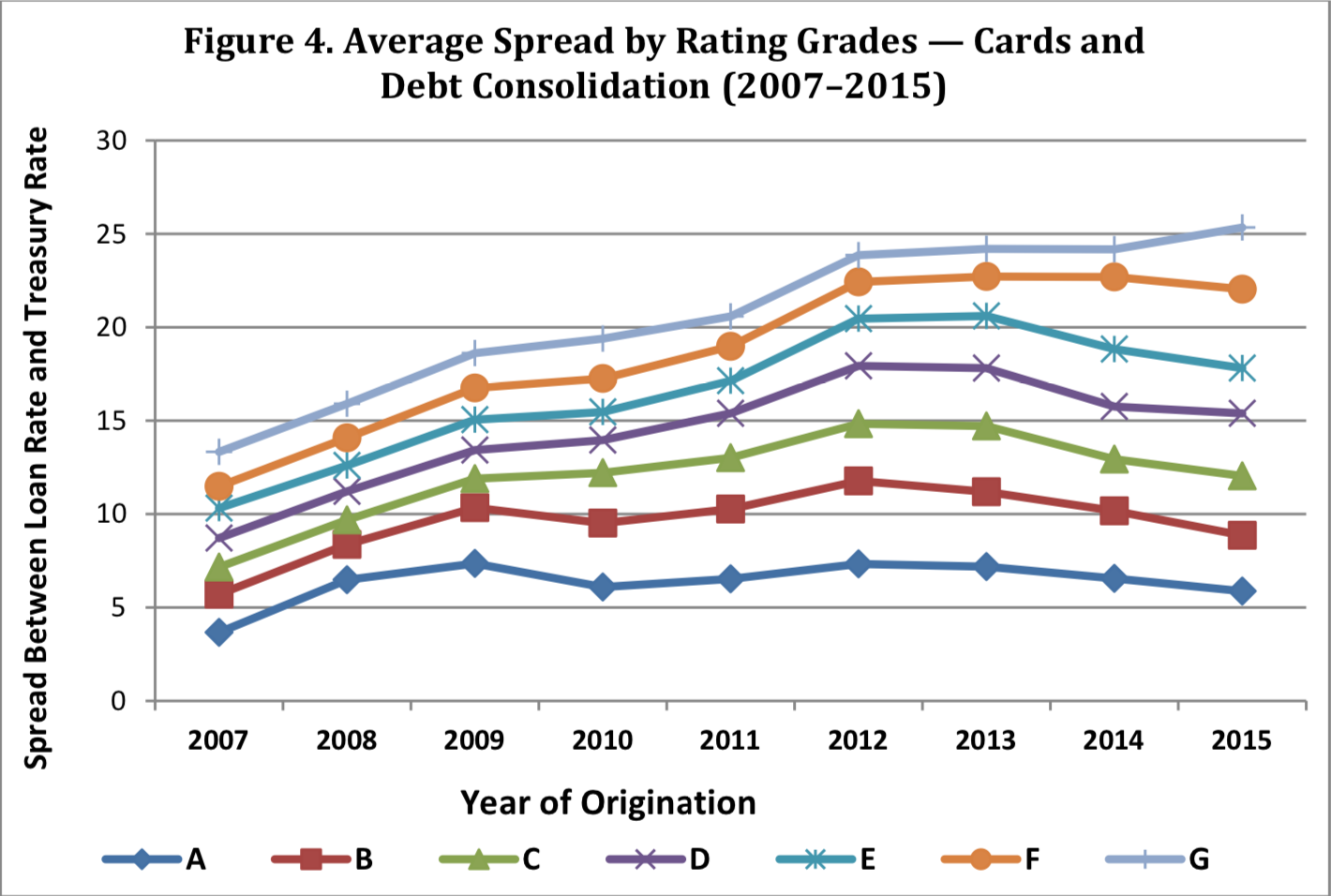

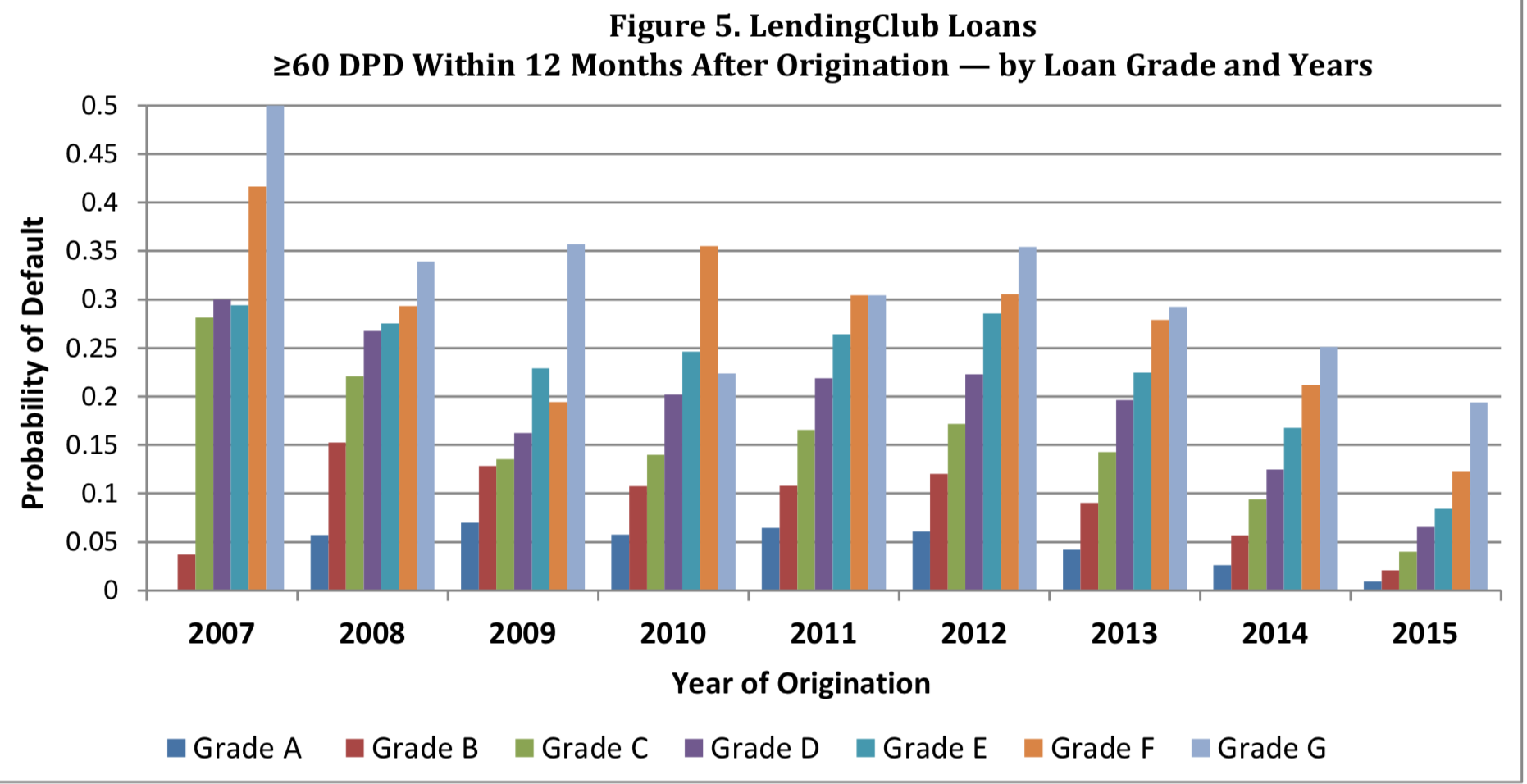

Lending Club: better credit scoring and product differentiation!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

\(\Rightarrow\) They learn!

Better credit scoring and product differentiation!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Better credit scoring and product differentiation!

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

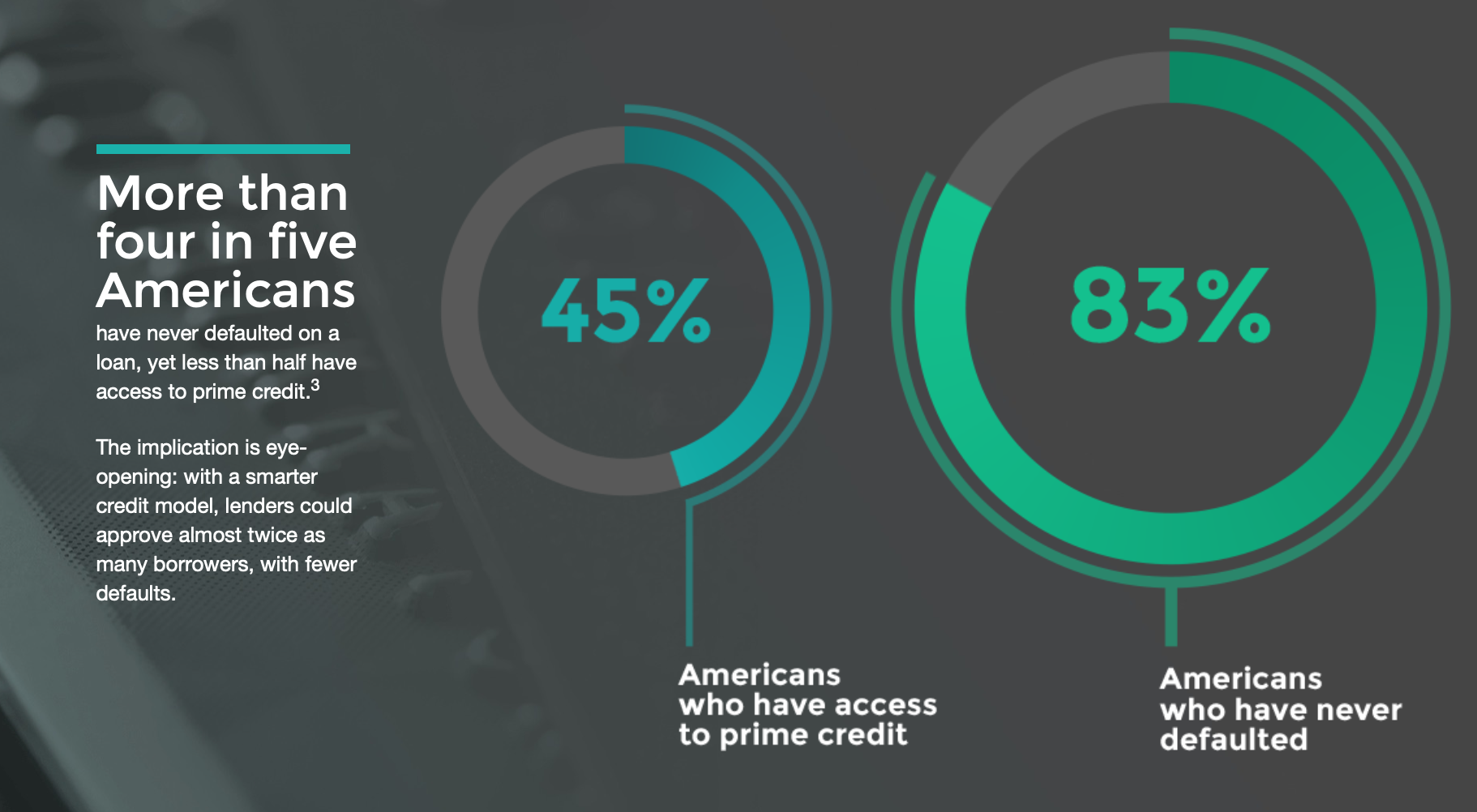

The results show that given the same credit risk (i.e., for borrowers with the same expected delinquency rate), consumers would be able to obtain credit at a lower rate through the Lending Club than through traditional credit card loans offered by banks.

Source: Jagtiani & Lemieux, 2017, Philly Fed Working Paper 17-17

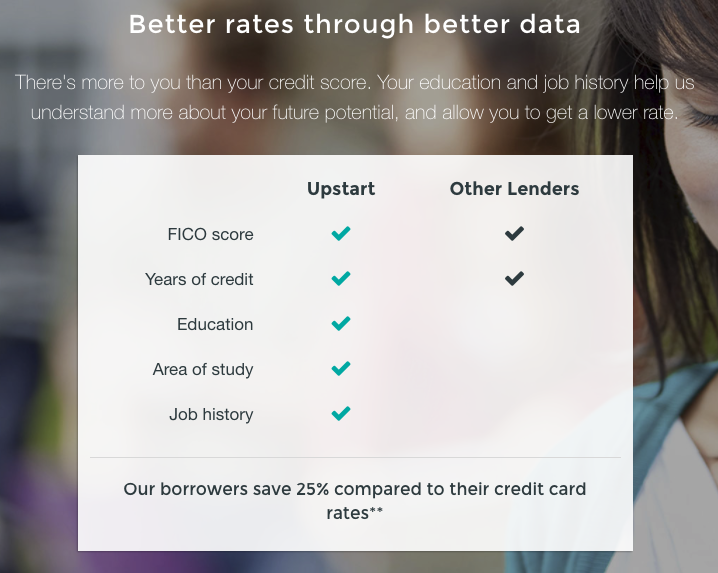

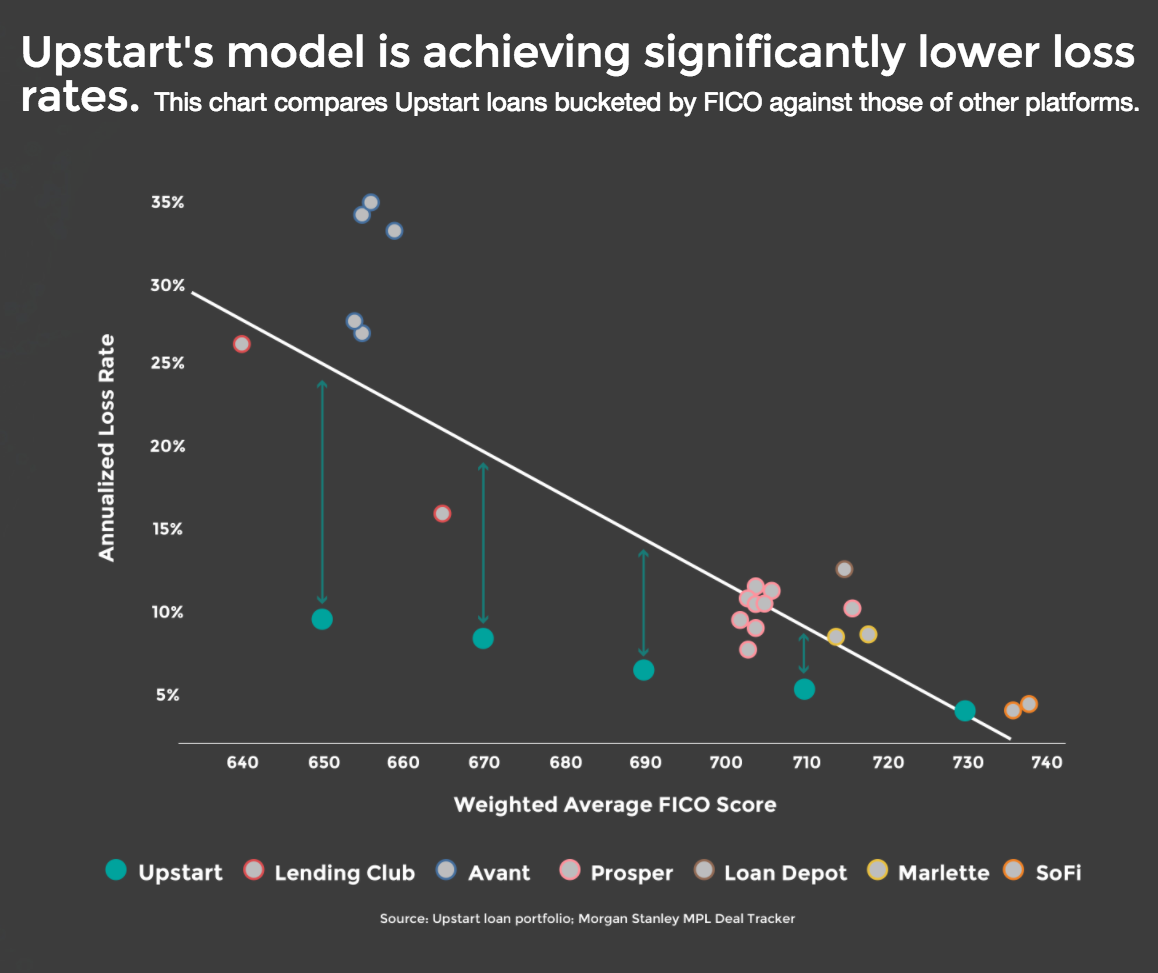

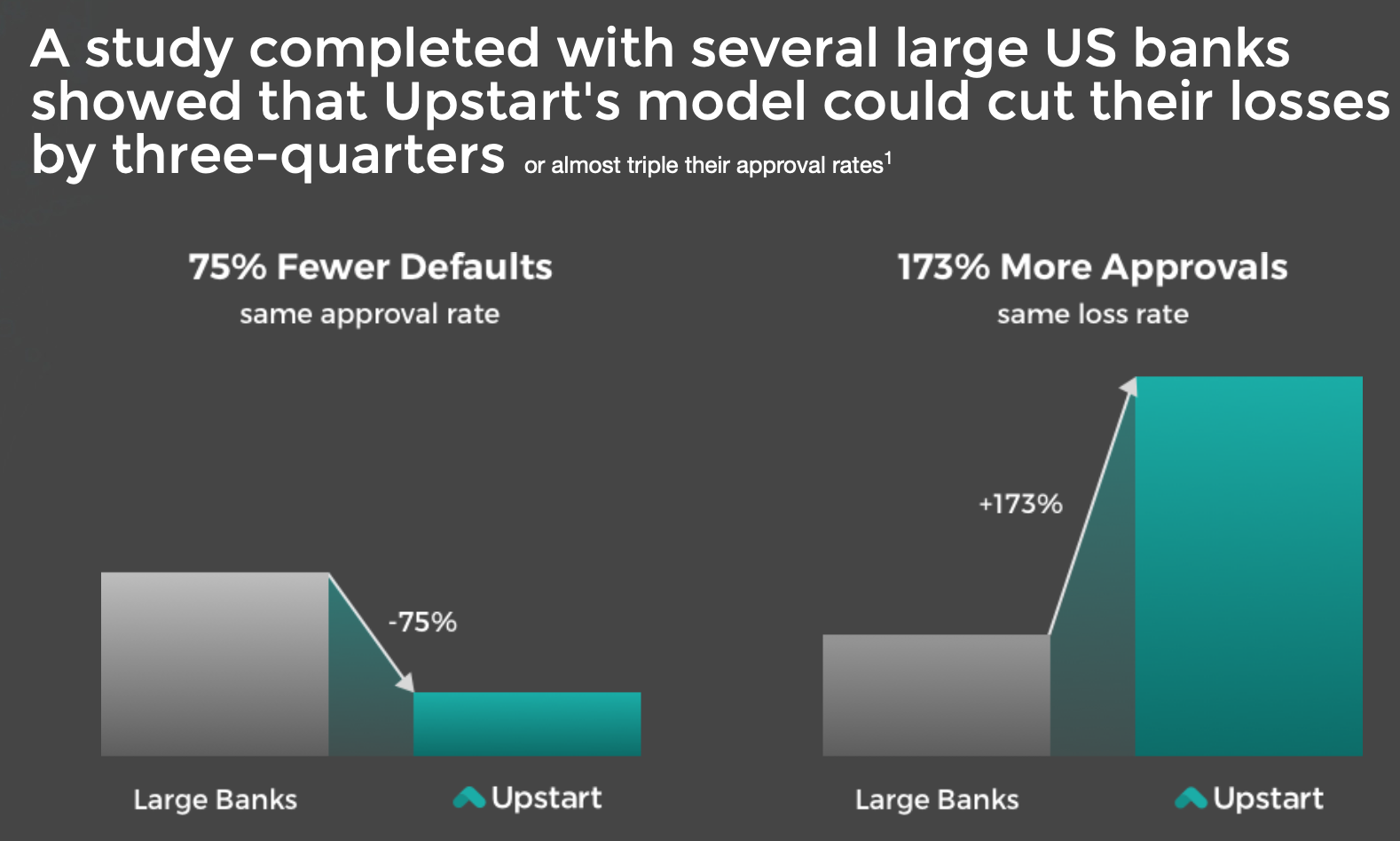

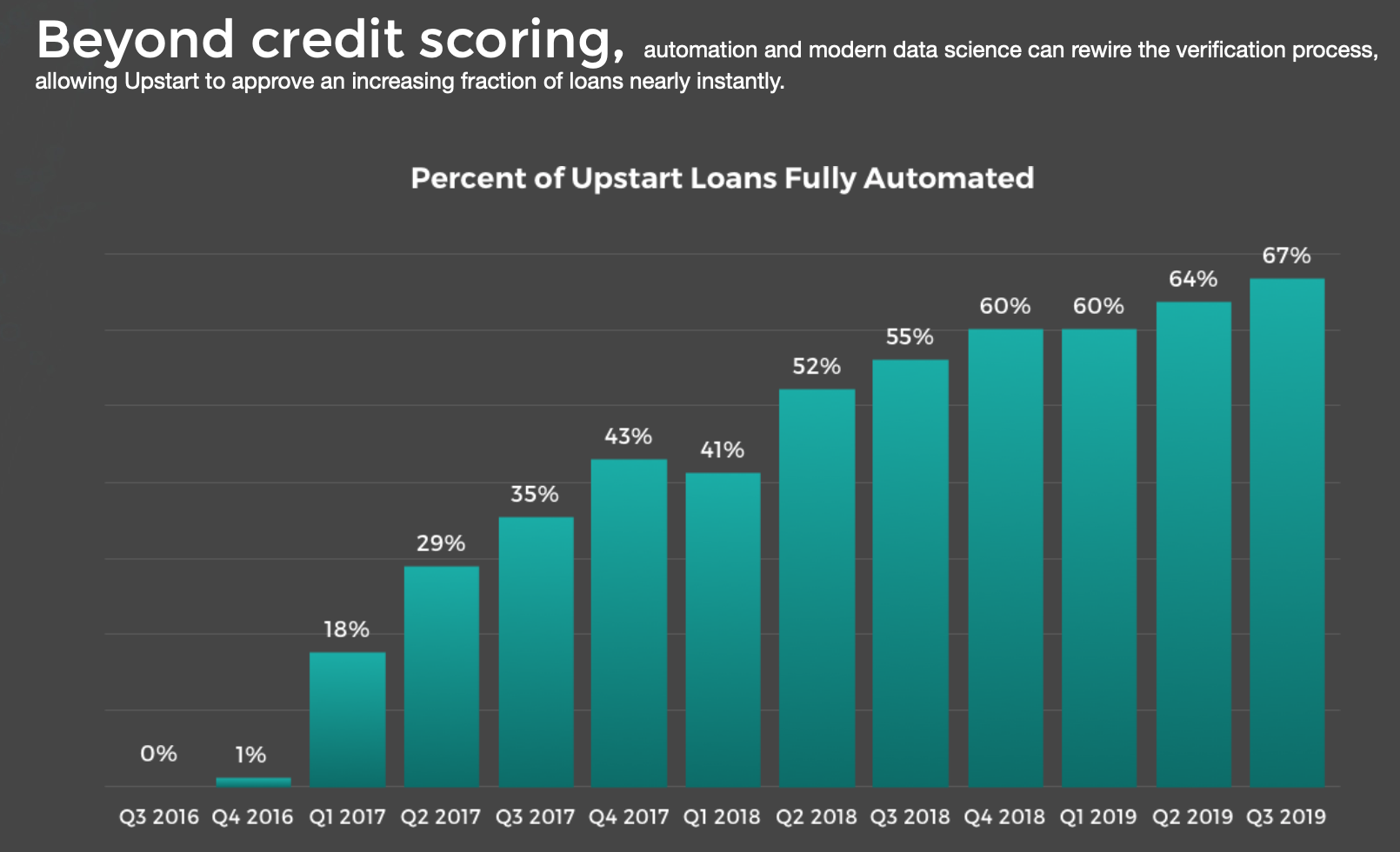

https://www.upstart.com/about#credit-limits-2

Example: UpStart

Example: Upstart

Source: upstart.com

Upstart

Source: upstart.com

Source: upstart.com

Source: upstart.com

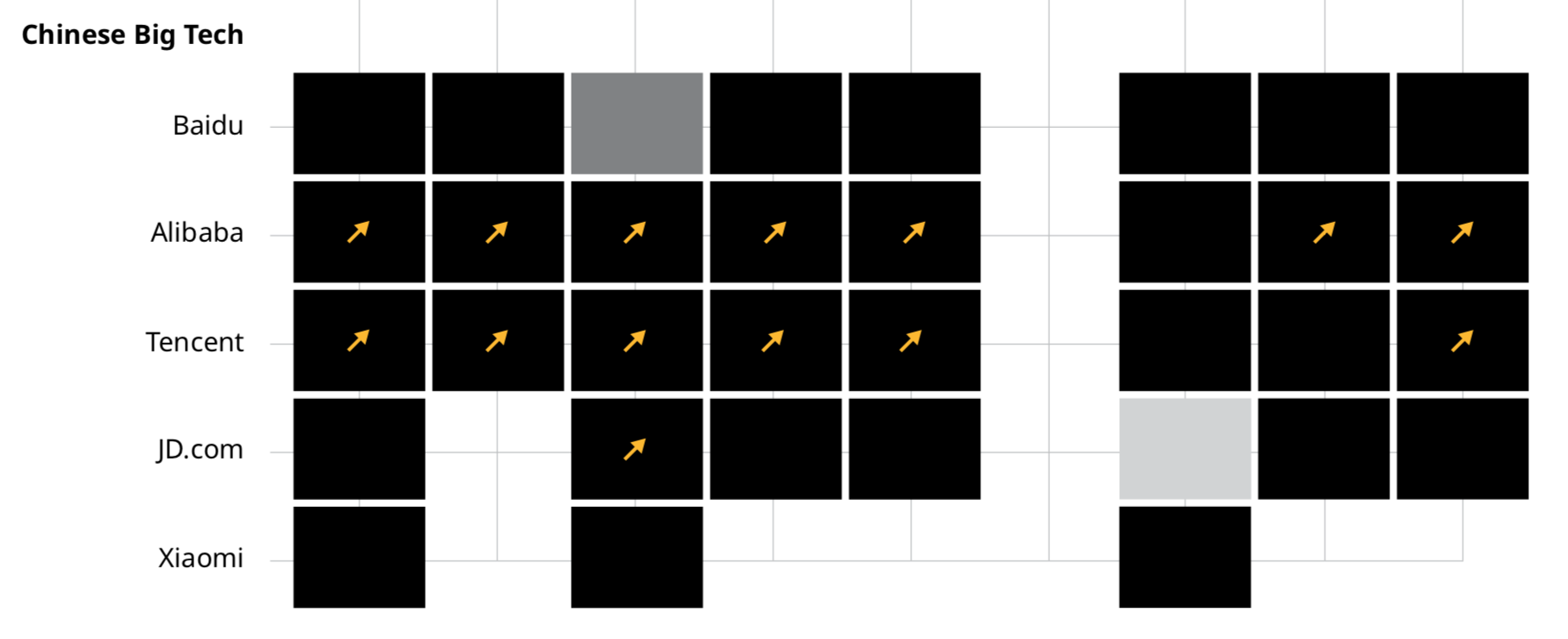

Other types FinTechs in the consumer lending space

Other Niches? (In consumer lending?)

- leverage cryptocurrency for loans.

- loans available for Bitcoin, Ether, Litecoin and Dogecoin.

- smart contracts to ensure the crypto is safely transferred.

- Available in most U.S. states for business and personal loans & internationally in New Zealand, Brazil, Switzerland and the U.K.

Other Niches? (In consumer lending?)

Lending and Financing

in the SME space

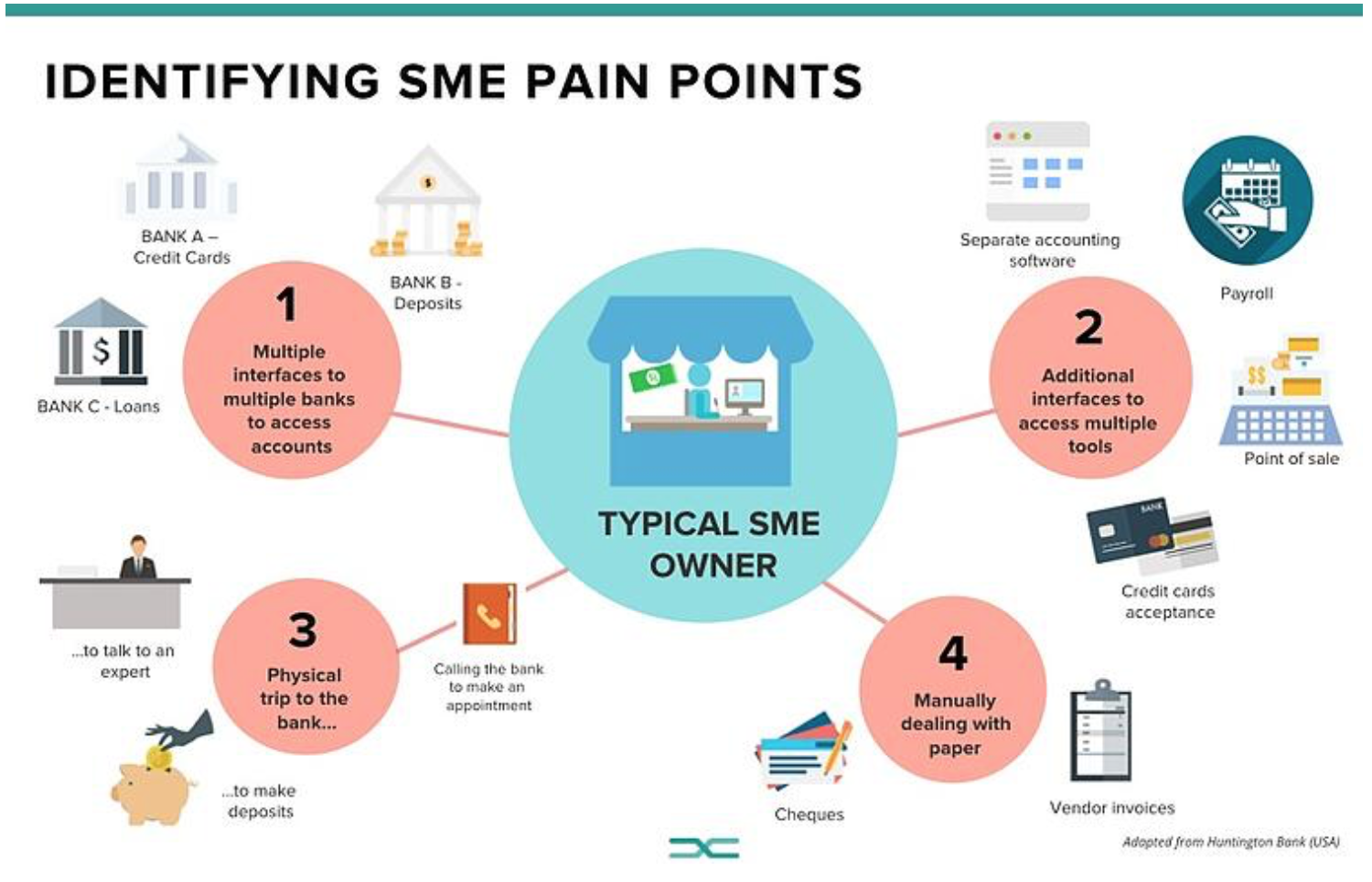

Next big gap: Small and Medium Enterprise Financing

- Problem: starting with the 2008 financial crisis, difficult for SME to get loan

- processing costs for $50K and $1M loan are the same!

- Banks require collateral/securing

- most SME loans are secured by personal wealth!

Next big gap: Small and Medium Enterprise Financing

- Approval percentages of small business loan requests made at big banks (defined as having assets of $10 billion+) dropped to the single digit range during the ensuing credit crunch.

- In June 2011, small business financing approval rates at big banks was a paltry 8.9%.

Today, big banks are granting 25.9 percent of the funding requests

This means that they decline 74.1% of applications!

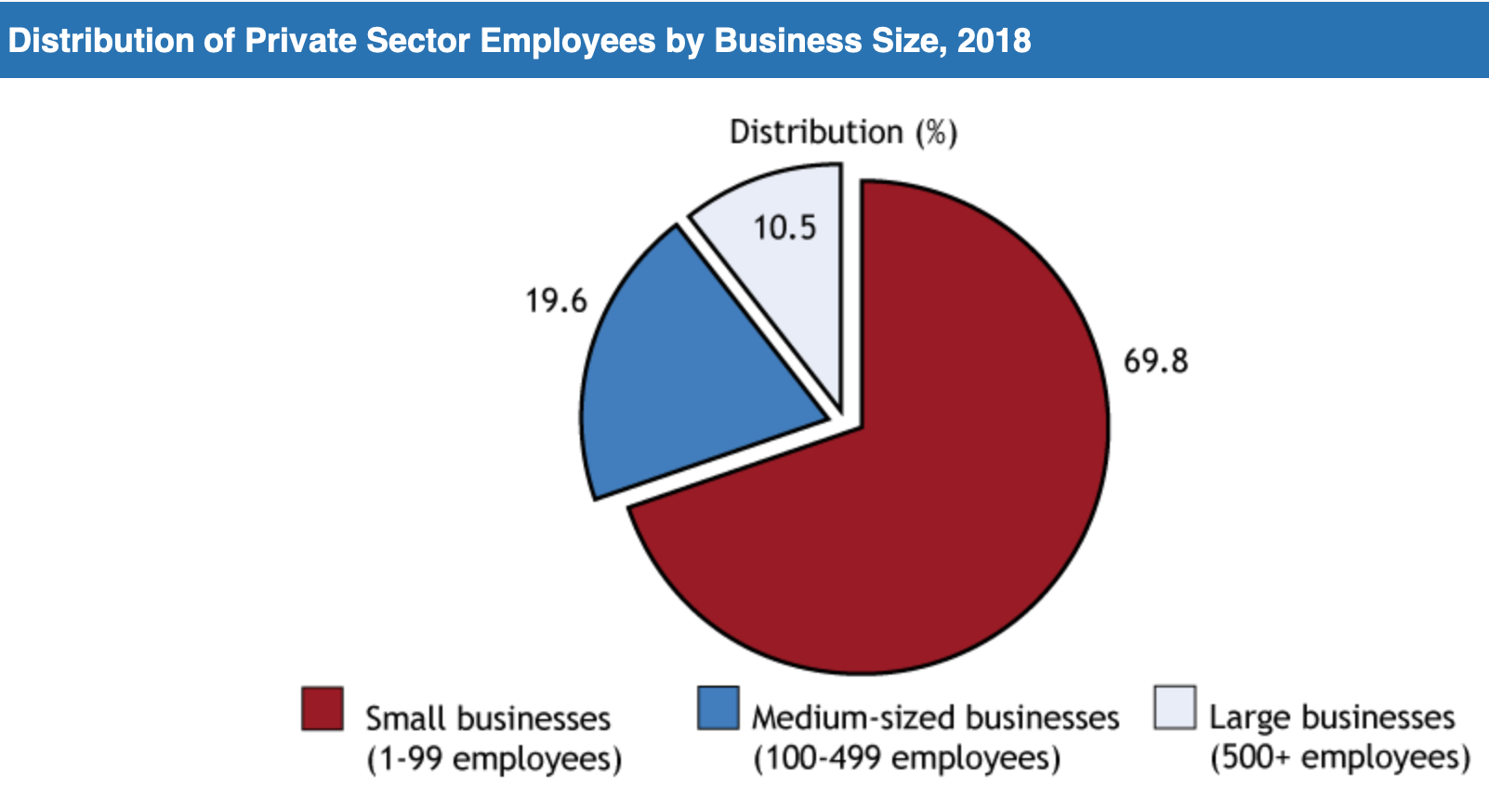

Small Businesses in Canada (2018)

- 1.2 million employer businesses

- 1.18 million (97.9%) are small

- 22,266 (1.9%) are medium-sized

- 3,010 (0.2%) are large

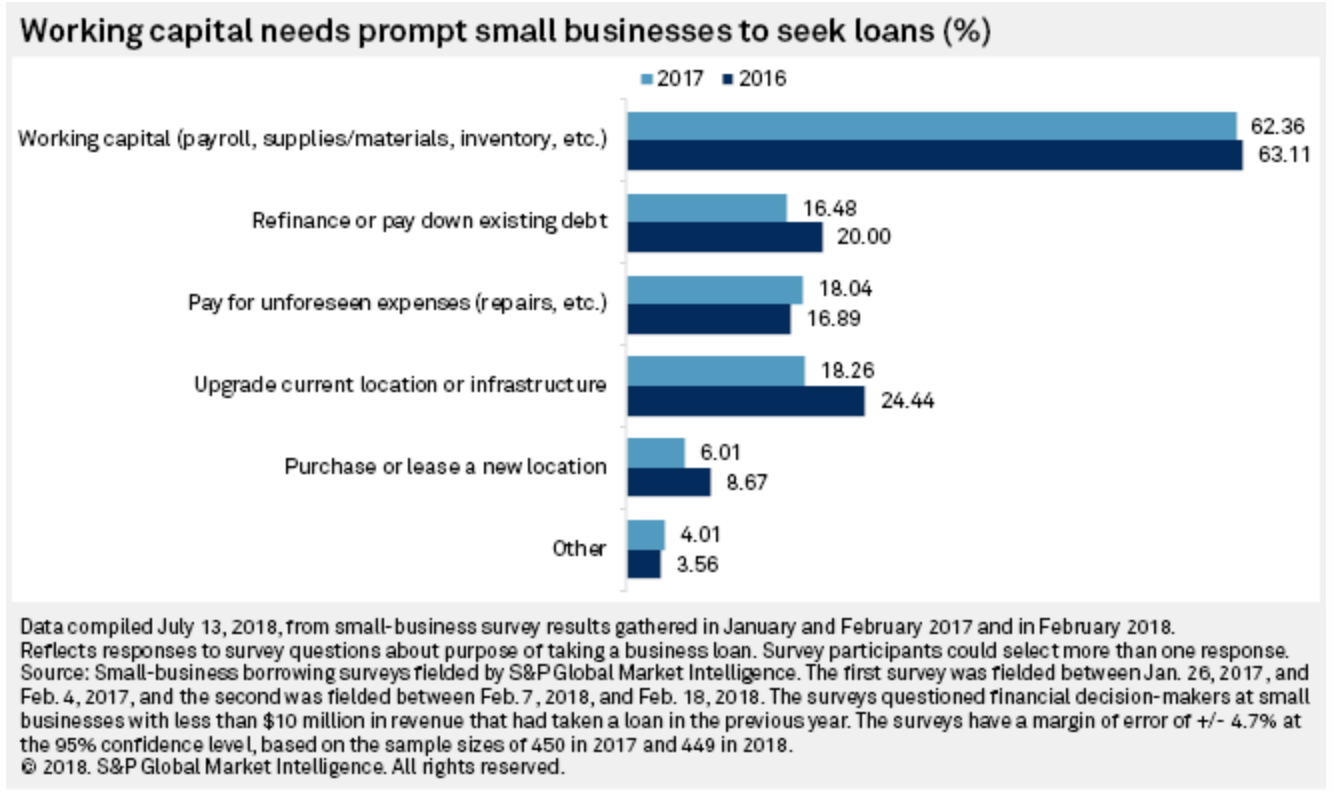

SME: why do they need the money?

Types of SME loans? (Lending Club)

Market segment challenges?

- Personal loans:

- homogenous

- \(\Rightarrow\) lots of data

- SME:

- highly heterogenous

- \(\Rightarrow\) hard to learn (even with data!)

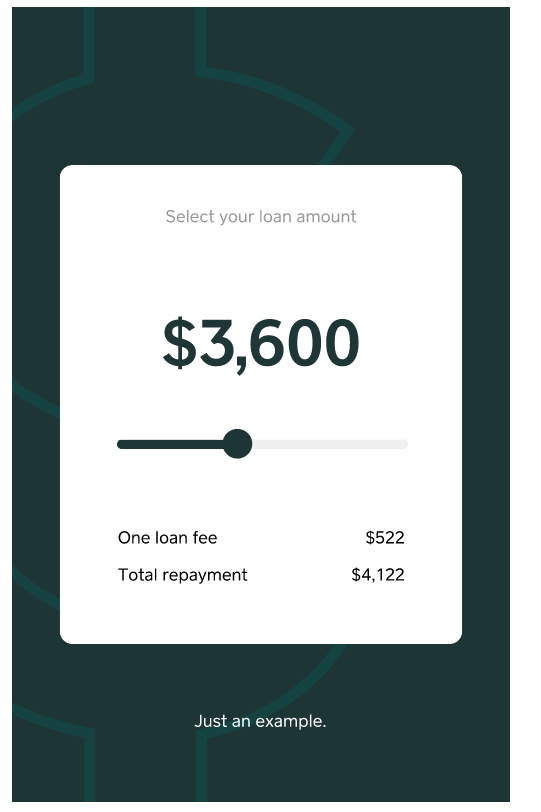

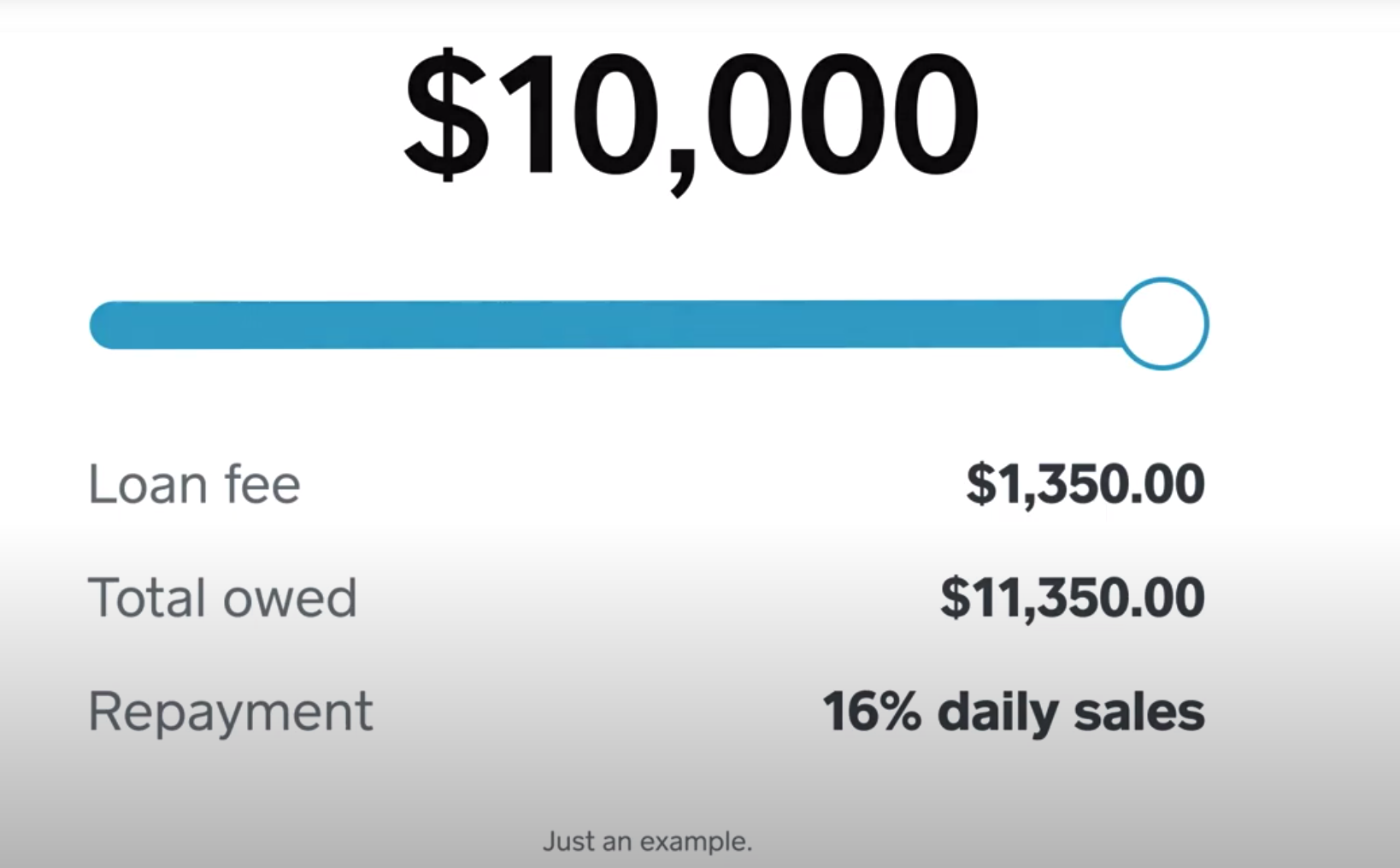

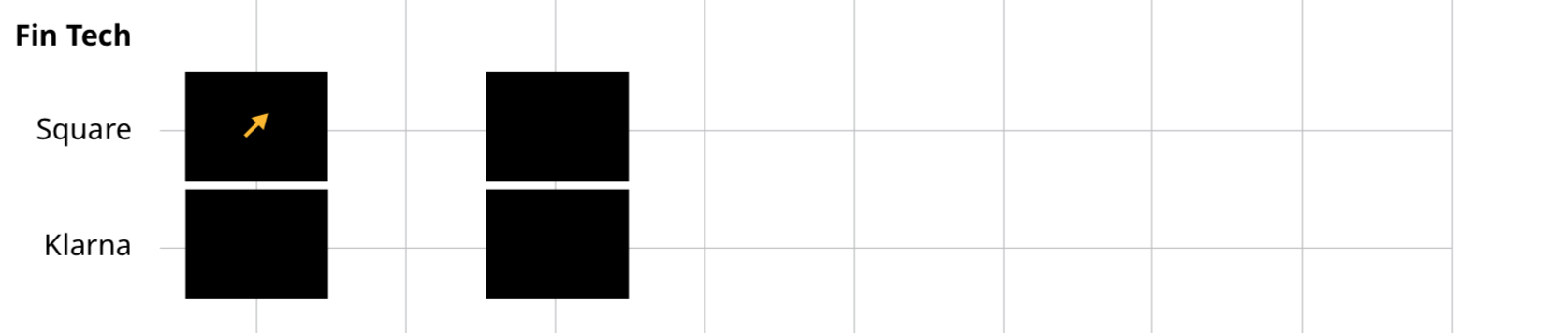

Payments and Lending

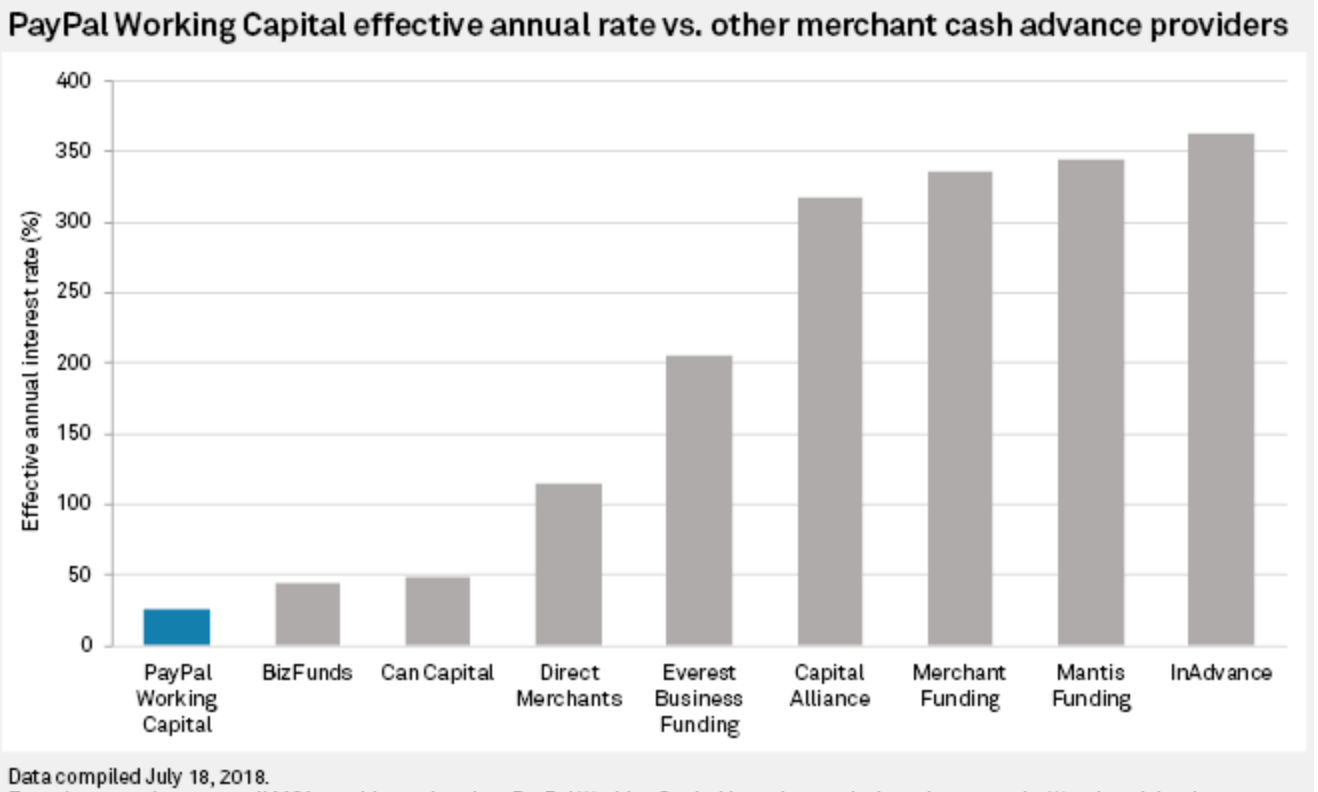

- Payment Fintechs (PayPal and Square)

- use their access to clients' real-time cash flow data to provide them with financing.

- Merchant cash advances (MCA)

- Establish a fixed total repayment amount

- The payment company deducts a percentage from every card transaction until the full amount is paid.

Payments and Lending

Alternative (?): look at customers' credit!

- Invoices are bought by FundThrough, which advances funds directly into the client’s bank account.

- The client’s customer in turn pays the original invoice when it’s due

The flip side of online lenders?

- Lenders vary in the amount of information provided, especially on costs

- challenging to identify interest rates or estimate cost

- Personal and business information

- policies permit user-provided data to be used by third parties

- \(\to\) bothersome sales calls

- policies permit user-provided data to be used by third parties

-

Personal and business information

- unclear whether these data are used to underwrite and price offers of credit

- Crucial component of SME traditional loans: asset-based.

- SME: leverage assets as collateral, incl. goods, equipment, etc.

- The lender: reserves the right to inspect the “asset” of the borrower (and also the right to seize that asset)

- Goods in Amazon’s warehouses \(\to\)

- Mixed with other sellers'

- No access for anybody

- Amazon lending

- secretive

- MCA, double-digit interest rates

- single purpose: build up/ restock inventory on products sold on Amazon!

Speaking of Amazon, data, etc

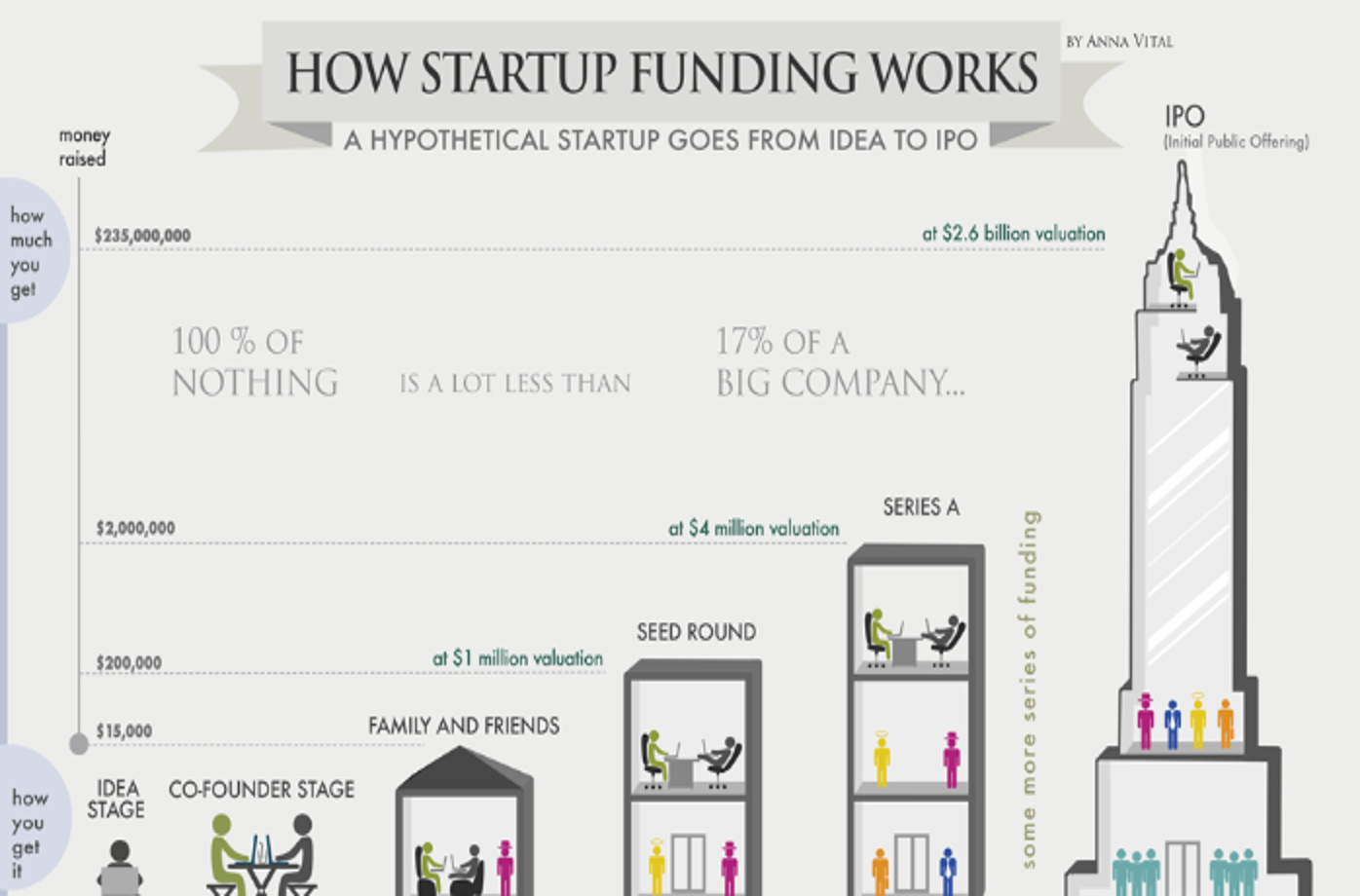

Alternative sources of funding for SME?

- Personal credit (owner)

- own funds (\(\to\) own equity)

- external equity

- Angels, VC (later stage)

- friends and family

- \(\ldots\)

Traditional sources of private equity funding

- Friends and Family

- Angel Investors

- Individuals; must be ”accredited investors” (income of at least $200K, and/or high wealth).

- Venture Capital Firms

- A limited partnership that specializes in raising money to invest in the private equity of young firms

- General Partners = Venture Capitalists

- A limited partnership that specializes in raising money to invest in the private equity of young firms

- Private Equity Firms

- Invest in existing firms rather than start-ups. Often participate in LBOs.

- Typically more mature; larger amounts than VCs.

- Invest in existing firms rather than start-ups. Often participate in LBOs.

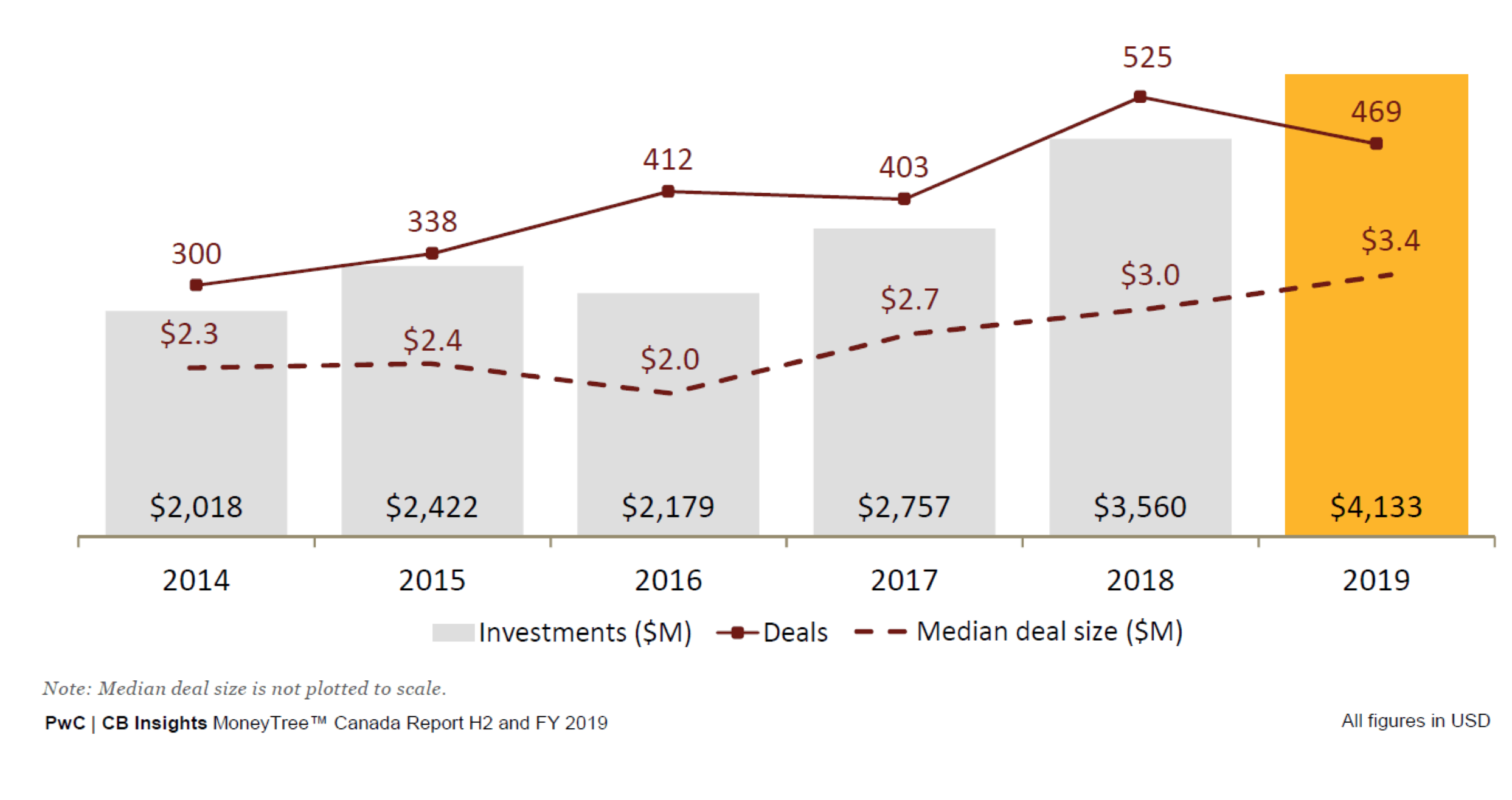

Venture Funding in Canada

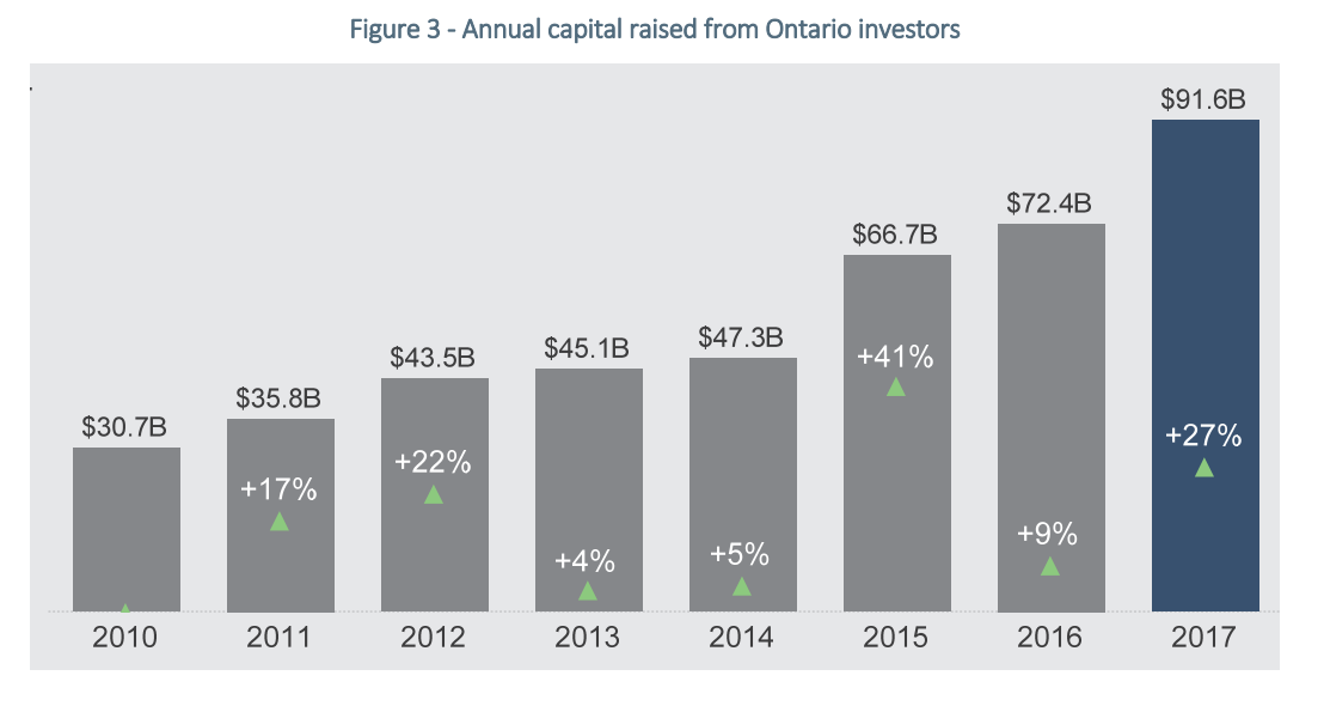

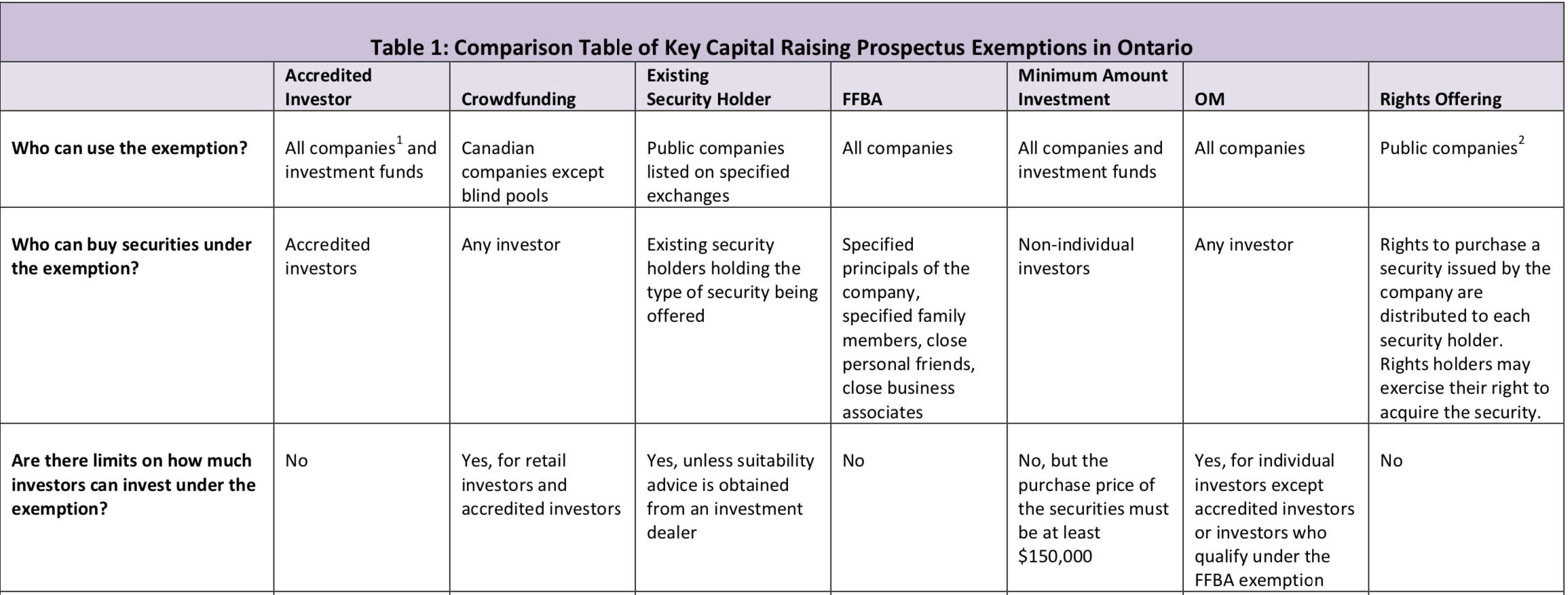

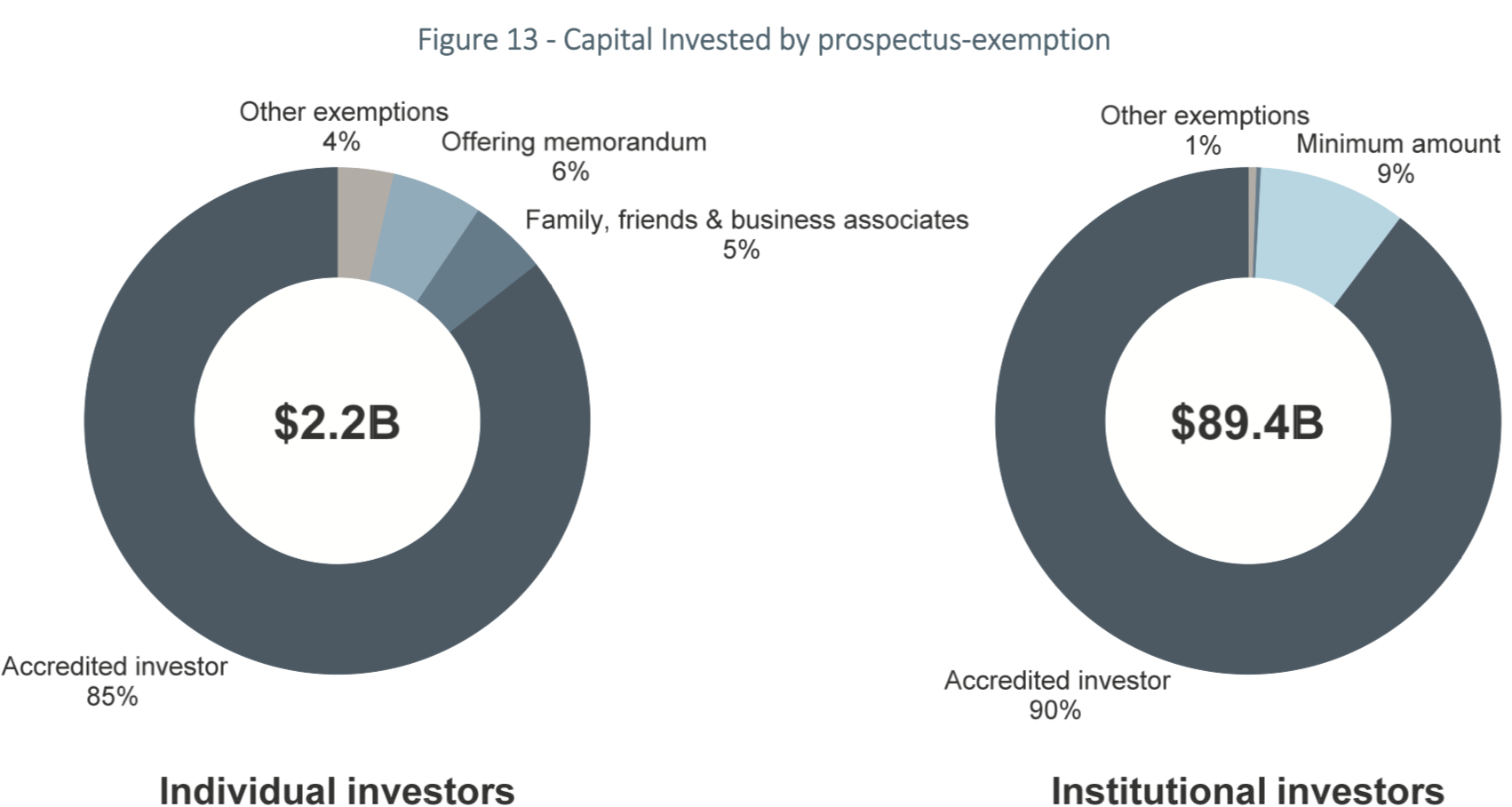

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Private markets in Canada (Ontario investors)

Data: coinschedule

$5B in 2017

$2.2B in 2018

$2.3B in 2019

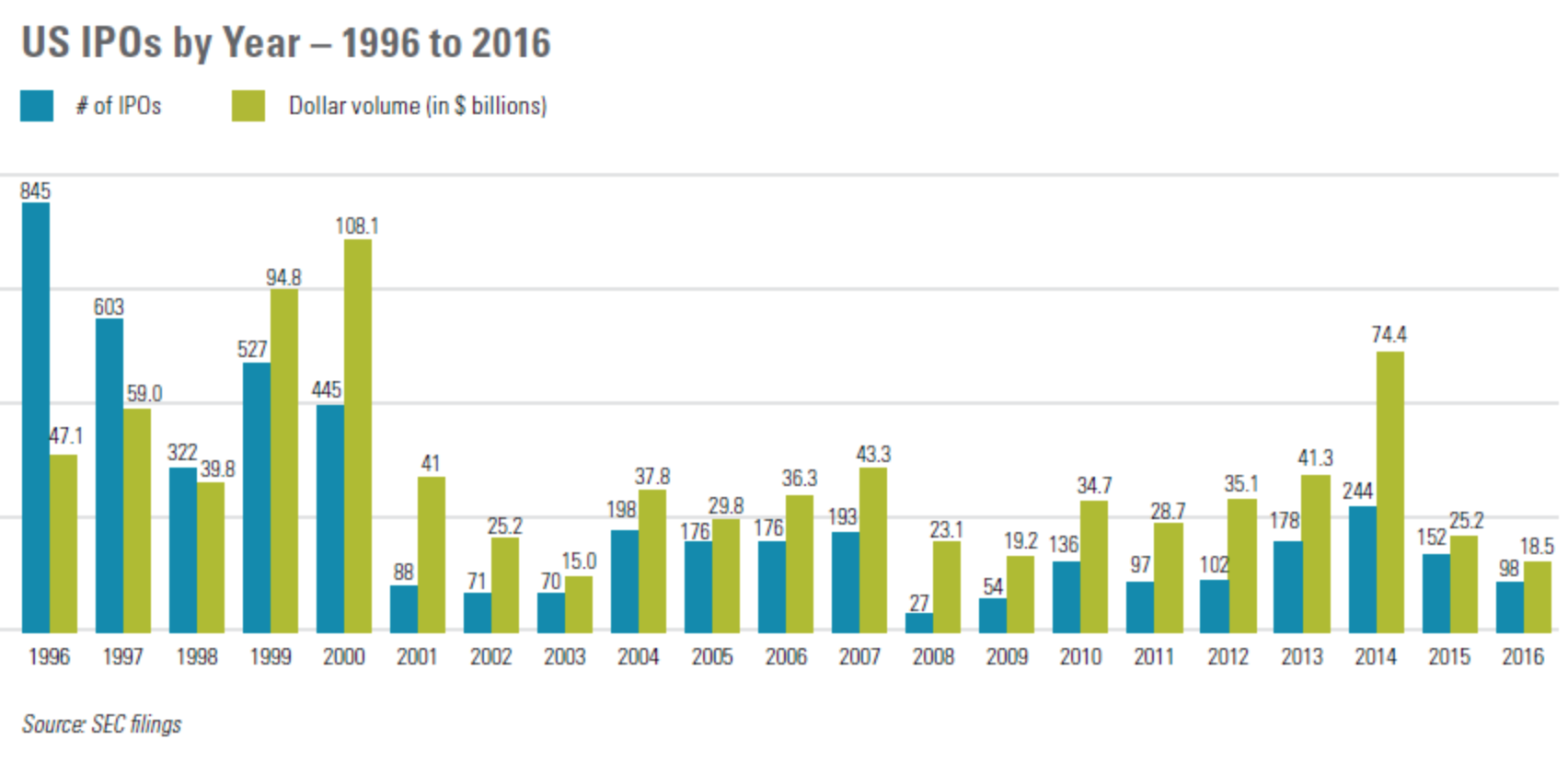

For comparison: publics markets in Canada (IPO)

Data: coinschedule

IPOs: expensive, difficult, and also the # is declining

Data: coinschedule

Why decline in IPOs?

- Various reasons

- Expensive to go public => want to stay private for as log as possible

- Became easier to stay private for longer

- More money in private markets

- Additionally: regulation change in 2012: The US Jumpstart our Business Startups (JOBS) Act

- the maximum number of shareholders a company can have before it must disclose financial statements went from 500 to 2000 shareholders

Alternative Sources of Funding?

- Recently permitted by the SEC in the US and the CSA in Canada (JOBS Act Title III in the U.S.; provincial regs in Canada)

- Restrictions (among others):

- Must be done on a registered platform

- Limits for entrepreneurs ($1 million in a 12 month period in the U.S.)

- Limits for investors (per firm&total; income-dependent). U.S. numbers:

- >$100K => 10%

- <$100K => 5% or $2K

Crowdfunding

Alternative Sources of Funding?

Crowdfunding: Canada

- Restrictions (Ontario)

- Must be done on a registered platform

- Limits for entrepreneurs ($1.5 million in a 12 month period (?)

- Limits for investors

- $2,500 in any one deal, max $10K in total per year

- $25,000 if accredited & $50K (per year) total

- The CSA promises a new harmonized set of rules for Canada out for comment by May 27, 2020.

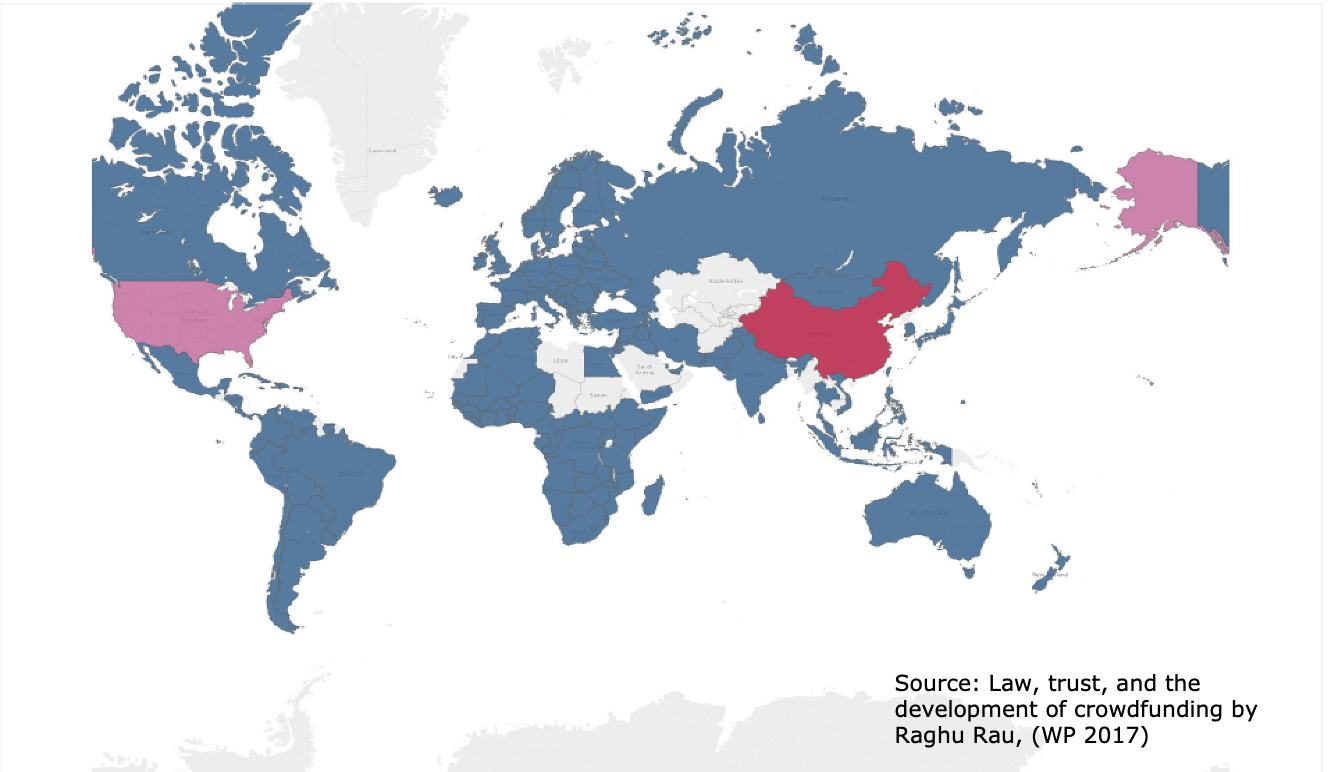

Global Volume of Crowdfunding (2015)

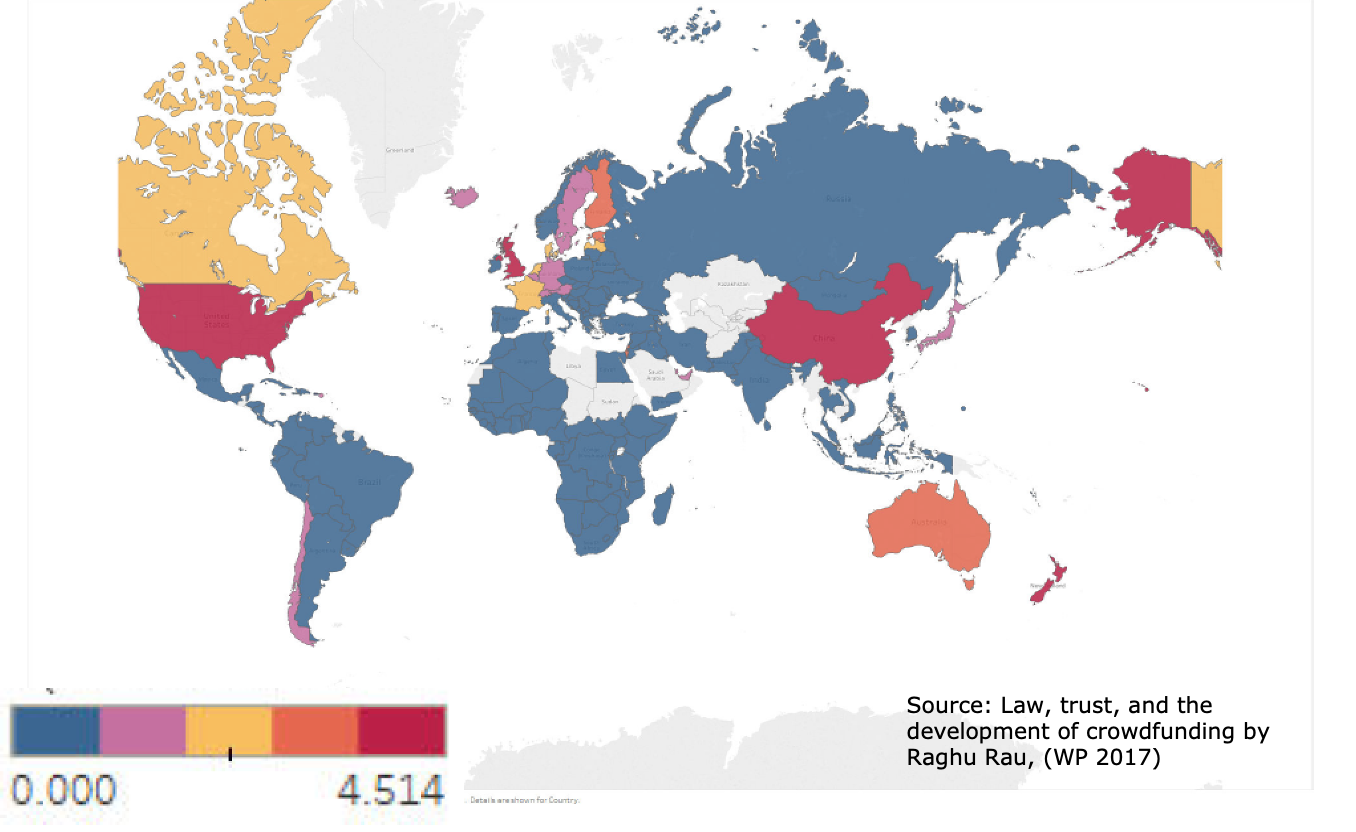

Log Volume Per Capita (Crowdfunding, 2015)

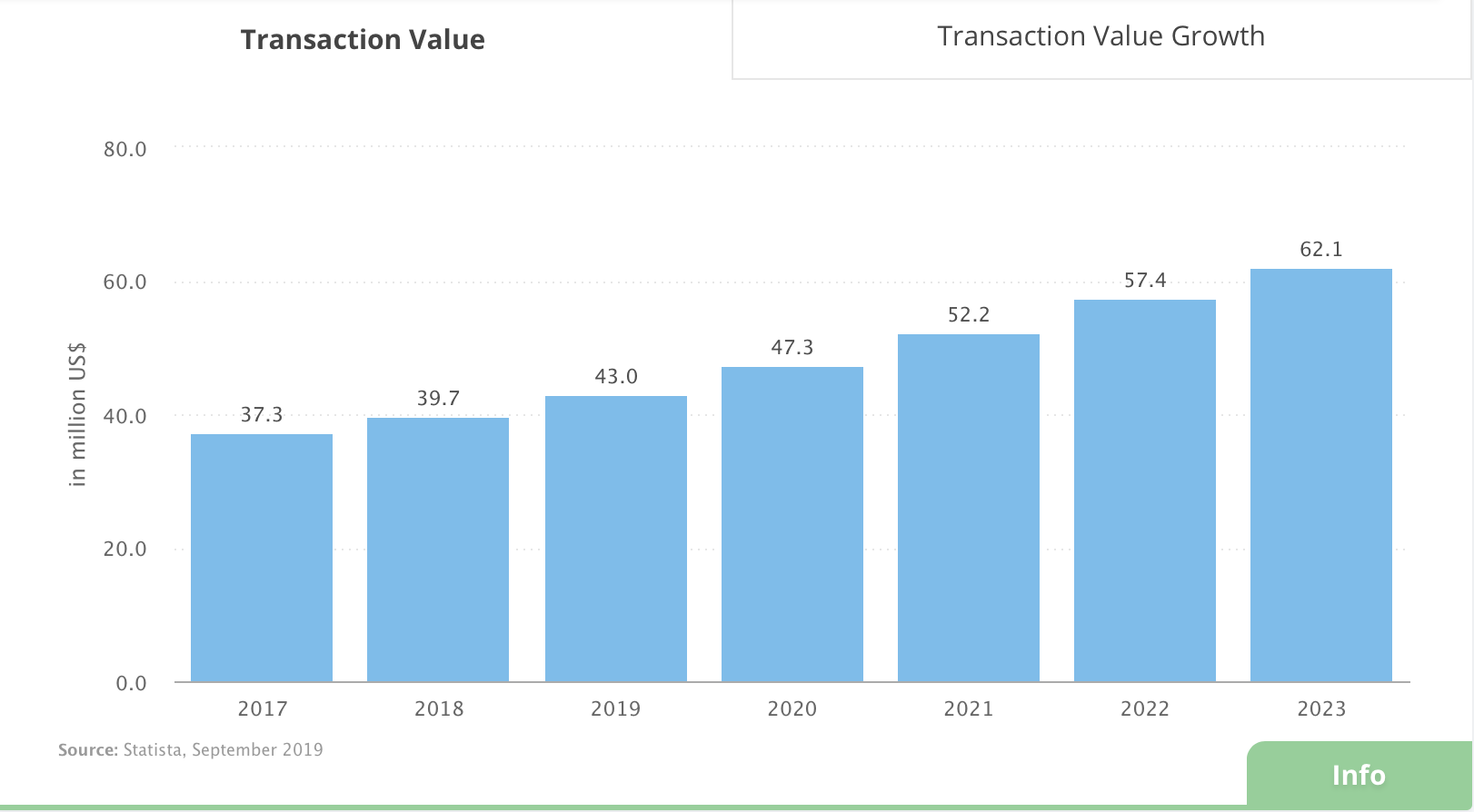

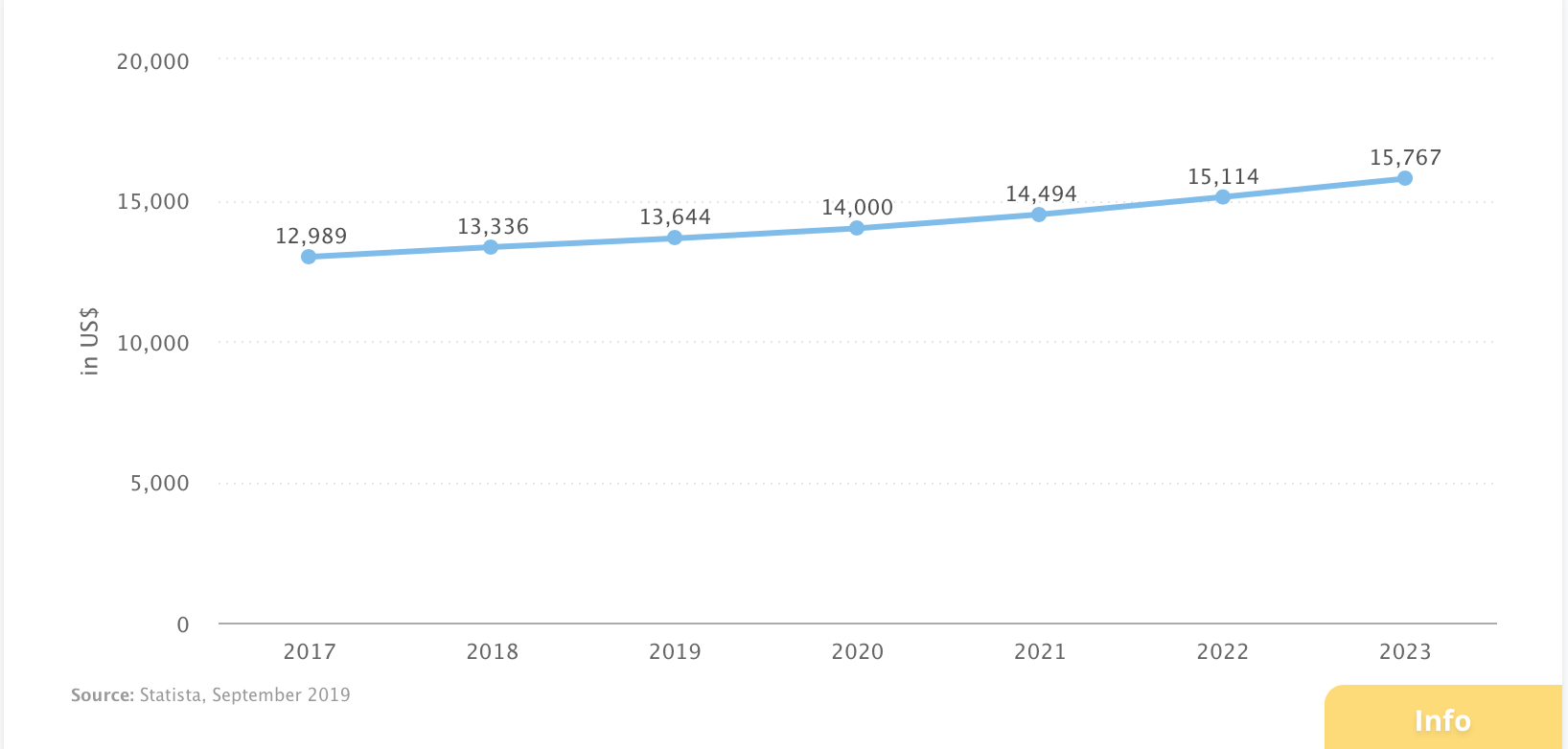

Crowdfunding in Canada (statistic.com projections)

Average deal now is USD13.5-14K

Future of crowdfunding?

Pros and Cons?

Costs of crowdfunding?

-

Professional time (Lawyers, accountants, etc.)

- $500/hour

- 100 hours? => $50K in costs?

- Platform Fee

- SEC 2016 study: 5%

- Wefunder: 7%

- U.S.: max allowable amount is $1 million

- 10% in costs?!

- Plus advertising, management time, promos, etc

Costs to investors?

- If you are making $100K, then about $50 per hour.

- How many hours did you spend "researching" the companies for your $2,500K to invest?

- Opportunity cost ....

- Wisdom of the crowd?

- Criminal juries and pivotal votes

- Impact Investing?

- Supporting socially responsible/impactful start-ups?

From Wefunder website:

New frontier: revenue-based lending

14.5% interest - over what horizon?

New frontier: revenue-based lending

- paid back as fraction of revenue

- \(\to\) uncertain horizon

- \(\to\) uncertain APR

- (max horizon 18 months)

- linked to Square system (so no shirking)

Some Core Functions of Financial Institutions/Banks affected by FinTechs

Lending and Borrowing

Wealth Management

Payments

Investment Banking Services

Six "Markers of Success" (McKinsey):

- Advantaged modes of customer acquisition

- Point-of-Sale

- Merchant acquisition through payments

- Step-function reduction in the cost to serve

- no branches

Six "Markers of Success" (McKinsey):

- Innovative uses of data

- college attended and majors

- social networks

- Managing risk and regulatory stakeholders

- Leveraging existing infrastructure

- software-as-a-service/lending-as-a-service

- bank partners/acquisitions

- Apple Pay

- Segment-specific propositions

- Young people, underbanked, small businesses