Learning from DeFi: Would Automated

Market Makers Improve Equity Trading?

Katya Malinova and Andreas Park

Agenda

- Very brief overview of Automated Market Makers

- Liquidity supply and demand

- Research question: what if we used AMMs for equities?

- theory: liquidity provision & demand

- data: implementation & trading costs

Why did we write this paper?

- Current U.S. mindset: everything crypto-related is evil

- GG/S.E.C.: "We made up a new market institution that is so awesome that it'll save (retail) investors $1.5B per year"

Seriously?

0. Cynicism aside - big question: Can we improve liquidity for smaller listings?

Some Motivation

- Blockchain: borderless general purpose value and resource management tool

Basic Idea

- DeFi: financial applications that run on blockchains

- \(\Rightarrow\) brought new ideas and tools

- one new market institution: automated market makers

Trading Infrastructure

payments network

Stock Exchange

Clearing House

custodian

custodian

beneficial ownership record

seller

buyer

Broker

Broker

Broker

Exchange

Internalizer

Wholeseller

Darkpool

Venue

Settlement

Application: decentralized trading with automated market makers

AMM Pricing

- AMMs require liquidity deposits

- Deposits:

- \(a\) units of an asset (e.g. a stock)

- \(c\) units of cash

Constant Liquidity (Product) AMM

- Purchase \(q\) of asset

- Deposit cash \(\Delta c (q)\) into liquidity pool, extract \(q\) of shares

- Idea of pricing: liquidity before trade \(=\) after trade

\[L(a,c)=L(a-q,c+\Delta c)\]

- AMMs require liquidity deposits

- Deposits:

- \(a\) units of an asset (e.g. a stock)

- \(c\) units of cash

Key Components

- Our question:

- Can an economically viable AMM be designed for current equity markets?

- Would such an AMM improve current markets?

- pooling of liquidity

- pro-rated

- fee income

- risk

- Liquidity providers:

- use existing assets to earn passive income

- Liquidity demanders:

- predicatable price

- continuous trading

- ample liquidity

Liquidity Supply and Demand in an Automated Market Maker

The Pricing Function

Liquidity Deposit \(\Rightarrow\) slope of the price curve

- Most common form of AMM liquidity rule is Constant Product Pricing

\[L(a,c)=a\cdot c~\Rightarrow~a\cdot c= (a-q)\cdot (c+\Delta c).\] - Total cost of trading \(q\) \[\Delta c=\frac{cq}{a-q}.\]

- Price per unit \[p(q)=\frac{c}{a-q}.\]

- Average spread paid\[\frac{p(q)}{p(0)}-1=\frac{q}{a-q}.\]

- makes asset and cash deposit

- more deposits flatter price curve

- attracts more volume

- but larger "positional" loss when prices move

Basics of Liquidity Provision

\[\underbrace{F p_0 V}_{\text{fees earned on balanced flow}}+\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss when the return is \(R\)}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned from arbitrageurs}}~\phi(R)dR \ge 0.\]

\(q^* \) is what arbitrageurs trade to move the price to reflect \(R\)

- fundamental value up

- \(\Rightarrow\) price up

- \(\Rightarrow\) sell the asset for less than its worth

- \(\Rightarrow\) price up

- fundamental value down

- \(\Rightarrow\) price up

- \(\Rightarrow\) buy the asset for more than its worth

- \(\Rightarrow\) price up

Basic idea of liquidity provision: earn more on balanced flow than what you lose on price movement

\[\text{fee income} +\underbrace{\text{what I sold it for}-\text{value of net position}}_{\text{adverse selection loss}} \ge 0 \]

in AMMs:

protocol fee

in tradFi: bid-ask spread

Basics of Liquidity Provision

\[\int_0^\infty\underbrace{(\Delta c(q^*)-q^*p_t(R)}_{\text{adverse selection loss when the return is \(R\)}} +\underbrace{F \cdot \Delta c(q^*))}_{\text{fees earned from arbitrageurs}}~\phi(R)dR +\underbrace{F p_0 V}_{\text{fees earned on balanced flow}}\ge 0\]

\[\frac{1}{\text{initial deposit}}\int_0^\infty(\Delta c(q^*)-q^*p_t(R)+F \cdot \Delta c(q^*))~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

\[\int_0^\infty\left(\frac{\Delta c(q^*)-q^*p_t(R)}{\text{initial deposit}} +F \cdot \frac{\Delta c(q^*)}{\text{initial deposit}}\right)~\phi(R)dR +\frac{F p_0 V}{\text{initial deposit}}\ge 0\]

closed form functions of \(R\) only

(see Barbon & Ranaldo (2022))

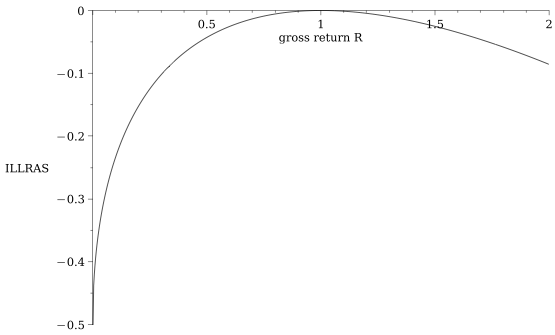

Sidebar: we can quantify how much a PASSIVE LP loses when the price moves by \(R\)

for orientation:

- If the stock price drops by 10% the incremental loss for liquidity providers is 13 basis points on their deposit

- \(\to\) total loss=-10.13%

- If the stock price rises by 10%, the liquidity provider gains 12 basis points less on the deposit

- \(\to\) total gain =9.88%

\[\frac{\text{adverse selection loss when the return is \(R\)}}{\text{initial deposit}}=\sqrt{R}-\frac{1}{2}(R+1)\]

see Barbon & Ranaldo (2022)

Basics of Liquidity Provision

Liquidity provision measured as "collective" deposit \(\alpha\) of firm's market cap as function of

- balanced volume

- asset volatility/return distribution

- fee

\[E[\text{IILRAS}(R)]+F\cdot E[\text{another function of }R]+F\cdot \frac{\text{dollar volume}}{\text{initial deposit}}\ge 0.\]

\[\text{what I sold it for}-\text{value of net position}+\text{fee income} \ge 0 \]

The Decision of the Liquidity Demander

- Wants to trade some quantity \(q\).

- Is better off with AMM relative to traditional market if

\[\text{bid-ask spread}\ge\text{AMM price impact} +\text{AMM fee}.\]

- two opposing forces for \(F\nearrow\) for liquidity demand

- more liquidity provision

\(\to\) lower price impact - more fees to pay

- more liquidity provision

- Finding: There is an optimal fee:

\[F^\pi=\frac{1}{E[|\sqrt{R}-1|/2]+V}\left(-2q\ E[\text{ILLRAS}]+ \sqrt{-2qV\ E[\text{ILLRAS}]}\right).\]

Model Summary

- Have: equilibrium choice for liquidity provision.

Useful feature: measure by % market cap

- Measure: benefit for liquidity demanders to use AMM.

- Know: fee that maximizes liquidity demander benefit (\(\not=0\))

- Next: Calibrate to stock markets

- Optimal fees?

- Feasible?

- Empirical benefits?

How we think of the Implementation of an AMM for our Empirical Analysis

Approach: daily AMM deposits

- AMMs close overnight.

- Market: opening auction \(\to\) \(p_0\)

- Determine: optimal fee; submit liquidity \(a,c\)

at ratio \(p_0=a/c\) until break even \(\alpha=\overline{\alpha}\)

- Liquidity locked for day

- At EOD release deposits and fees

- Back to 1.

Background on Data

Special Consideration 1: What volume?

-

some volume may be intermediated

- with AMMs: no need for intermediation

- \(\to\) intermediate volume should disappear

- \(\to\) use volume/2

Special Consideration 2: What's \(q\) (the representative order size)?

- use average per day

- take long-run average + 2 std of daily averages

- (also avg \(\times 2\),\(\times 4\), depth)

All displayed data CRSP \(\cap\) WRDS

- CRSP for shares outstanding

- WRDS computed statistics for

- quoted spreads (results similar for effective)

- volume

- open-to-close returns

- average trade sizes, VWAP

- Time horizon: 2014 - March 2022

- Exclude "tick pilot" period (Oct 2016-Oct 2018)

- All common stocks (not ETFs) (~7550).

- Explicitly not cutting by price or size

- All "boundless" numbers are winsorized at 99%.

AMMs that's true to the "model"

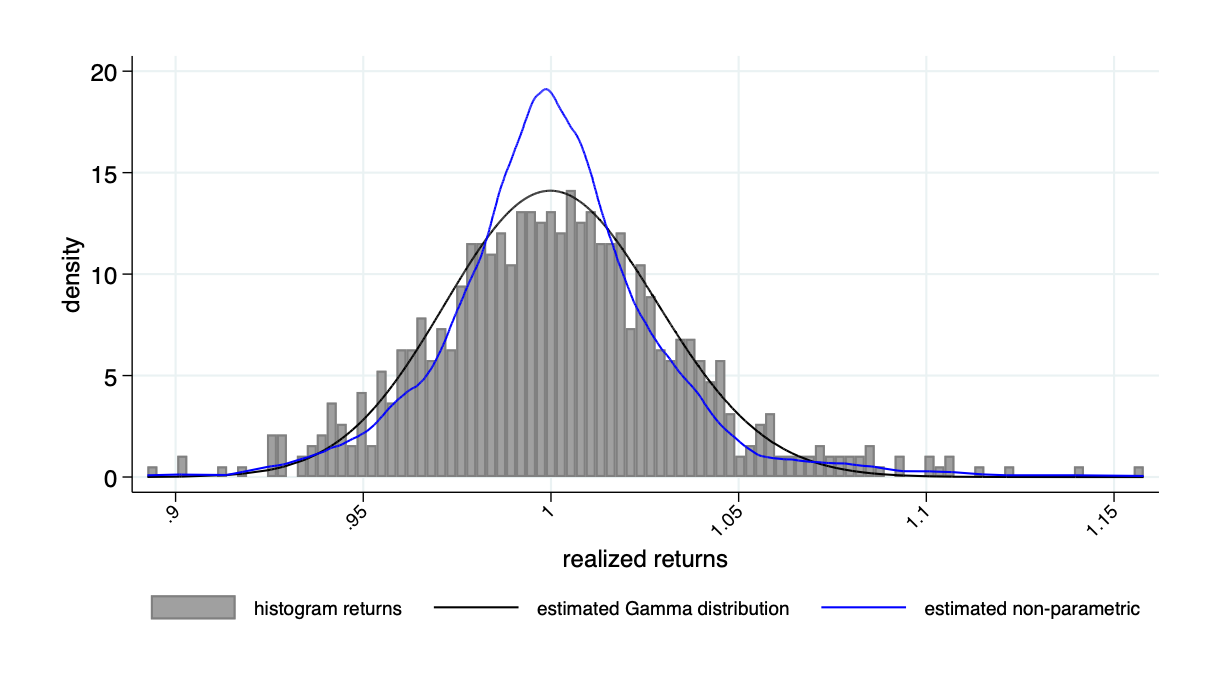

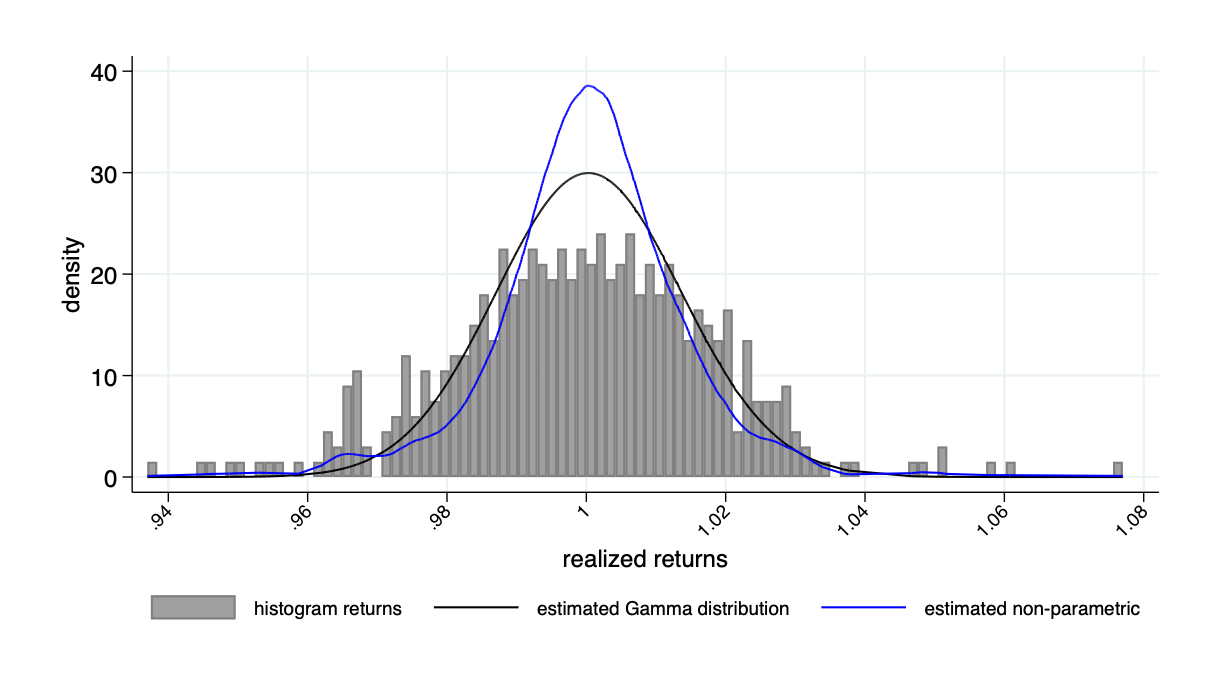

Return distribution example: Microsoft

Return distribution example: Tesla

- average \(F^\pi=11\)bps

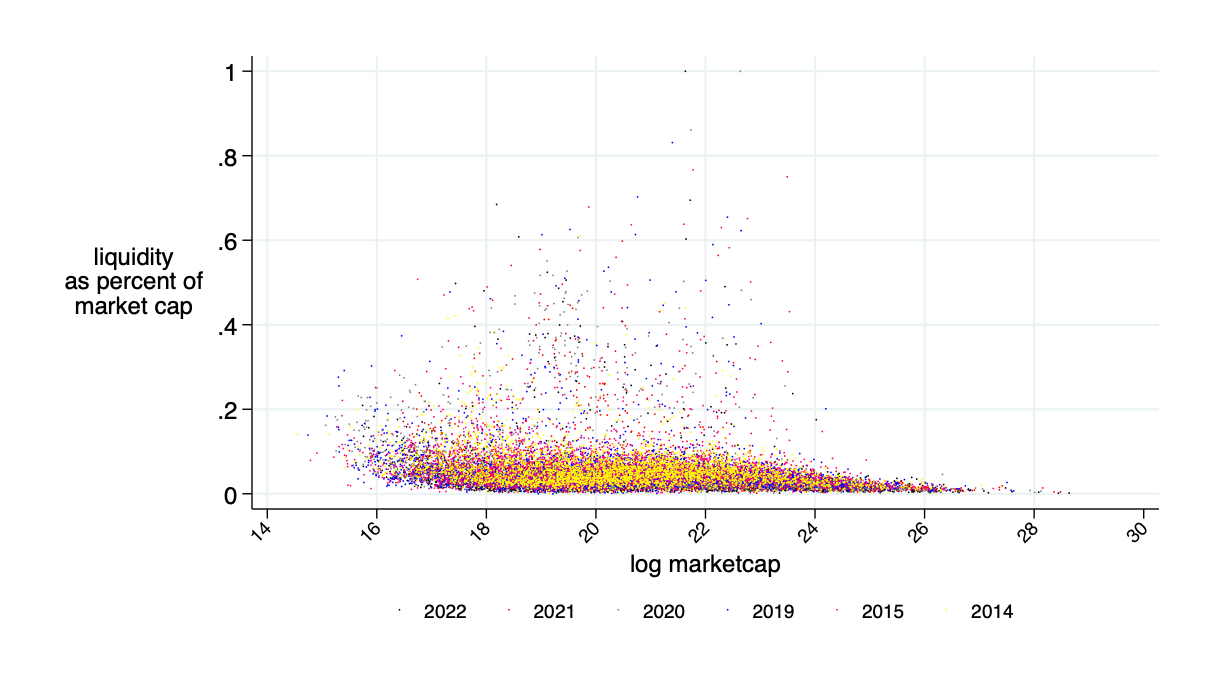

\(\bar{\alpha}\approx 2\%\)

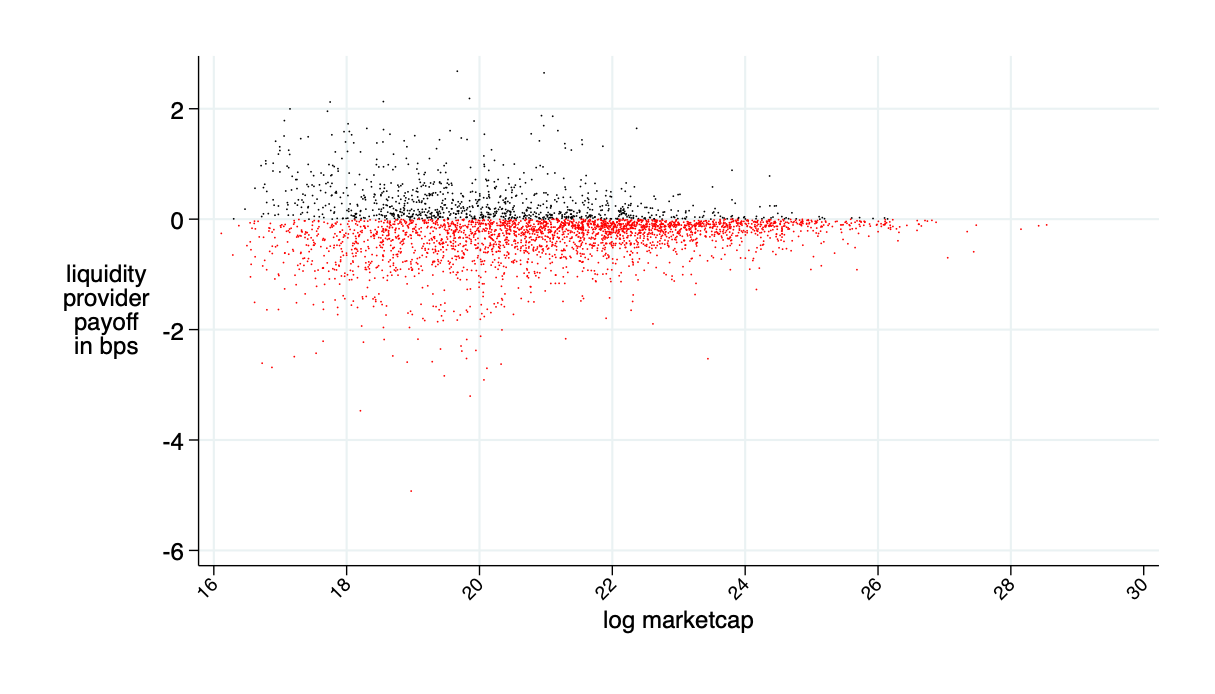

almost break even on average (average loss 0.2bps \(\approx0\))

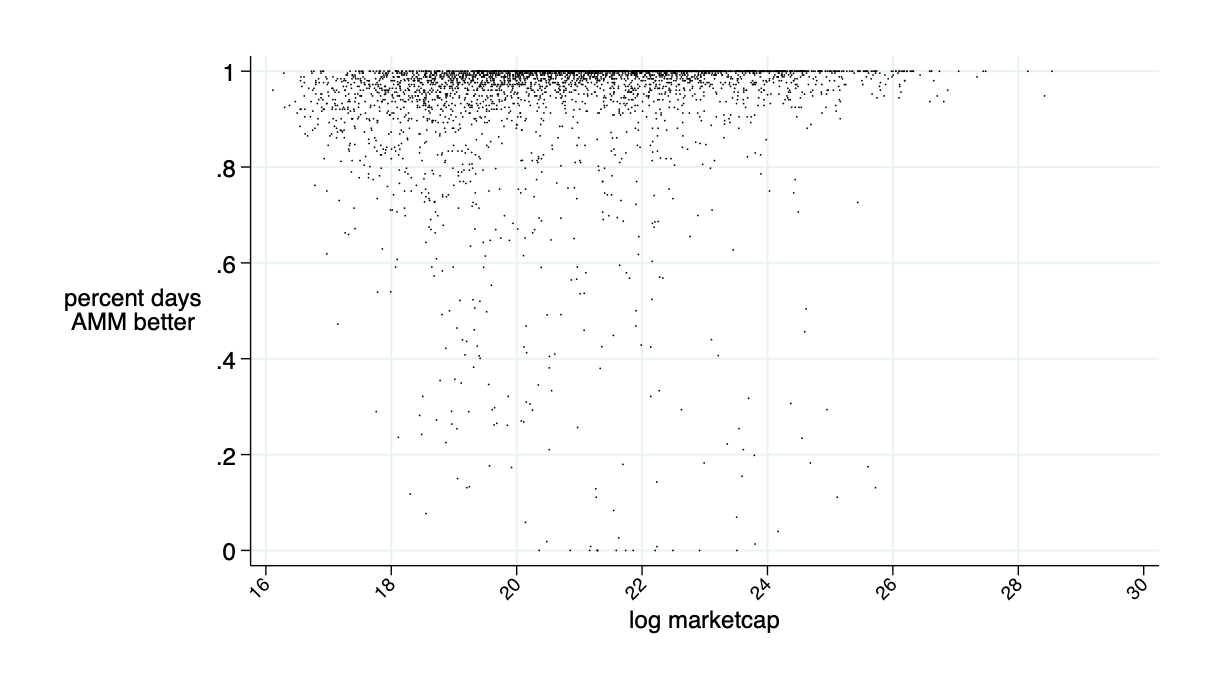

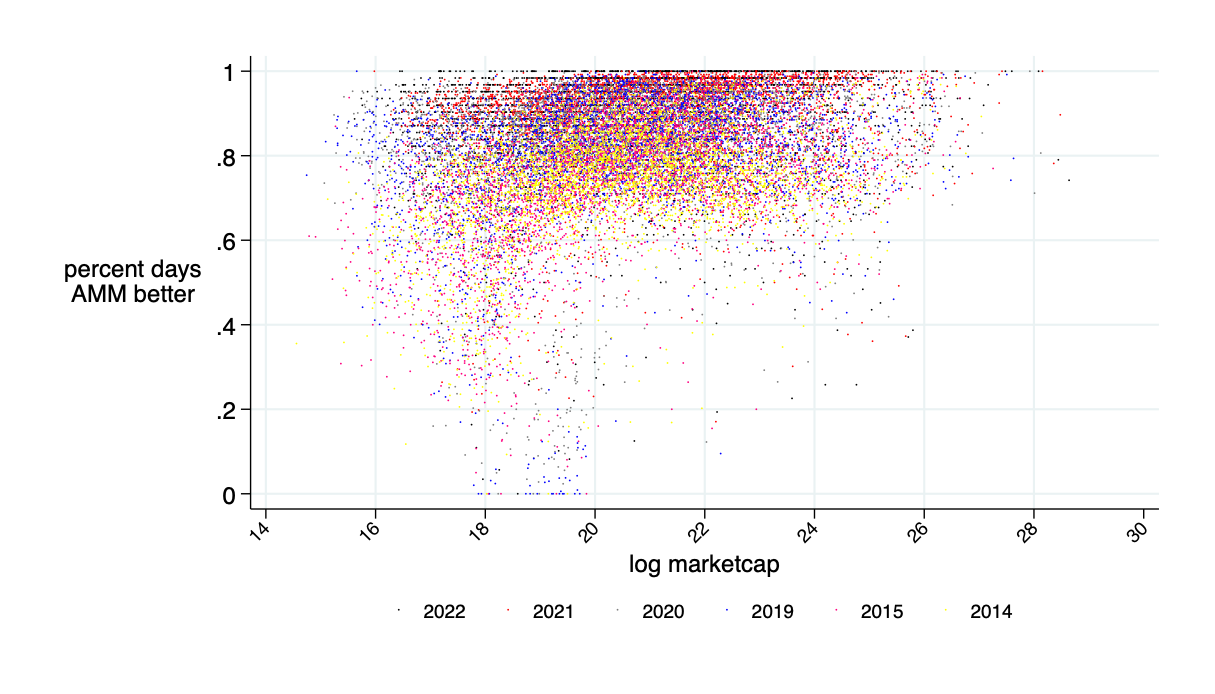

average: 94% of days AMM is better than LOB

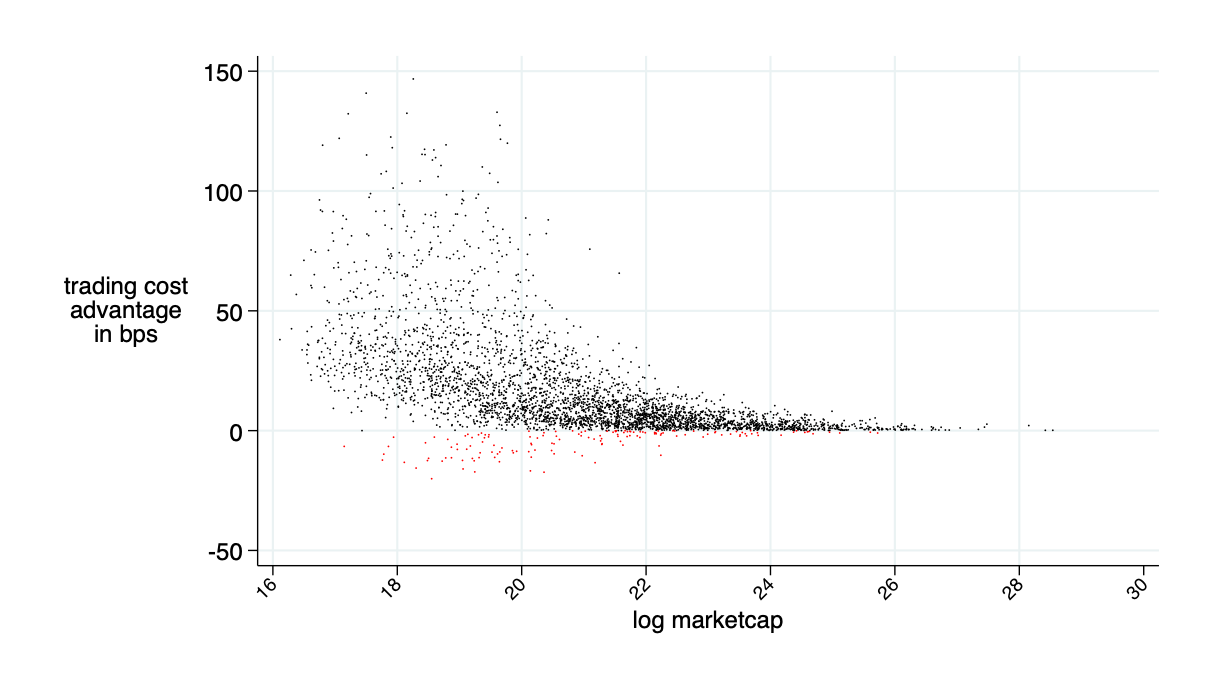

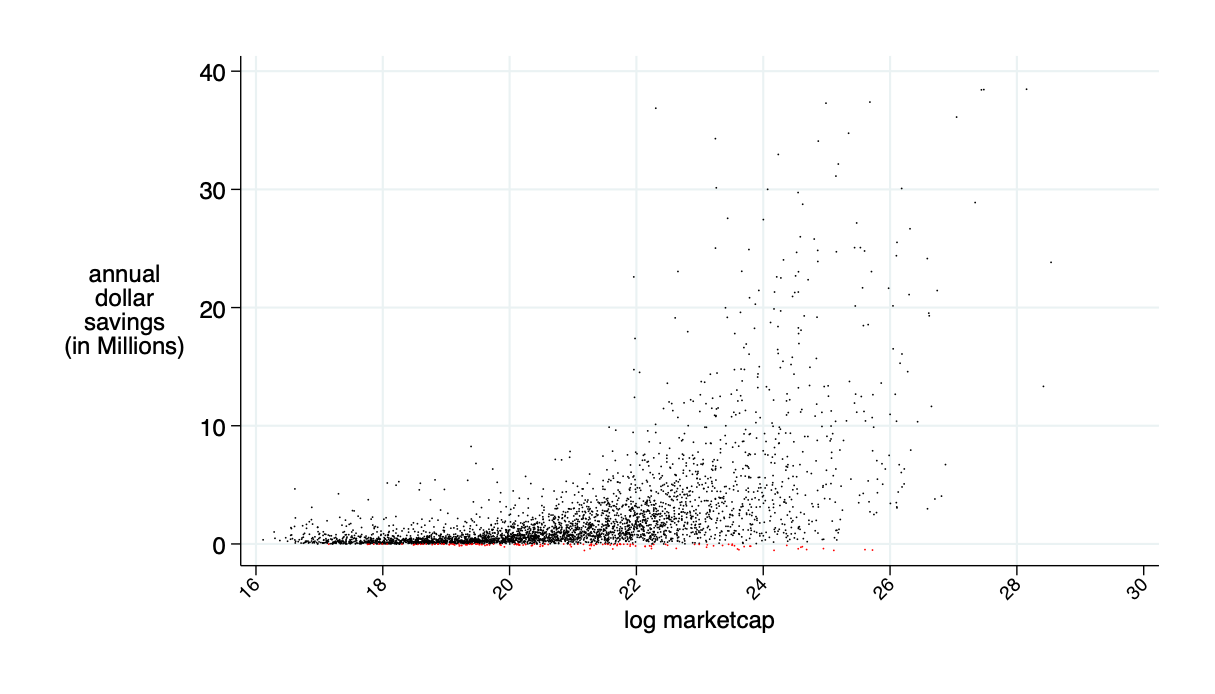

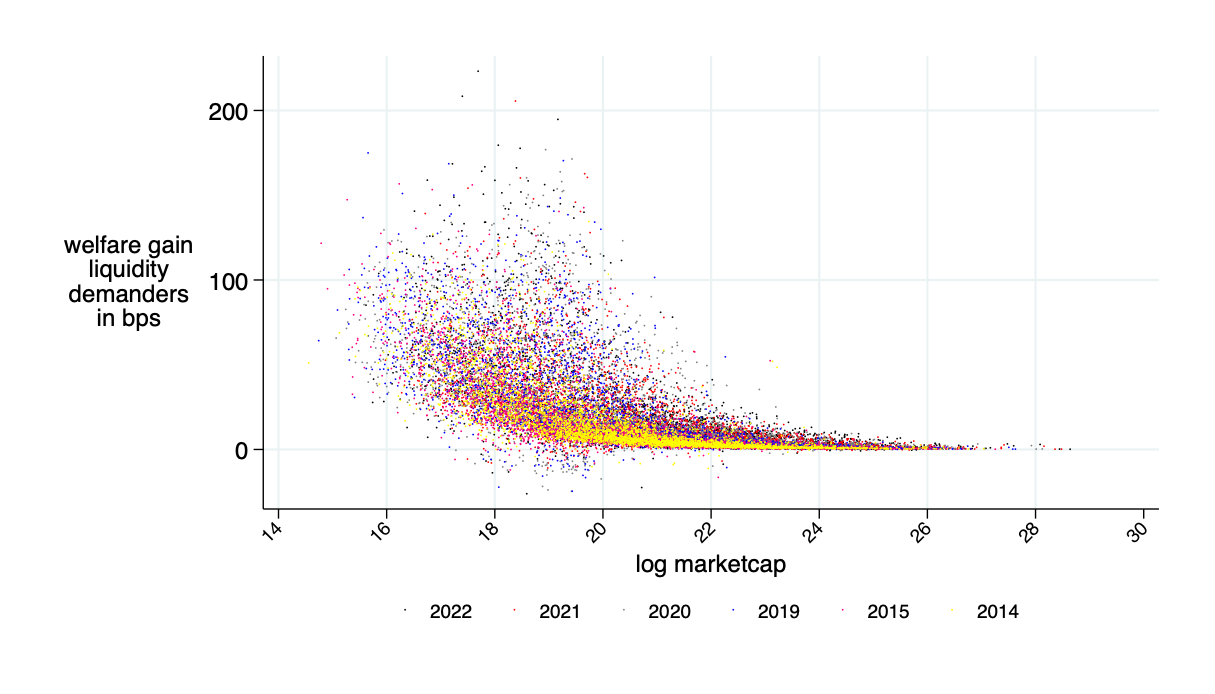

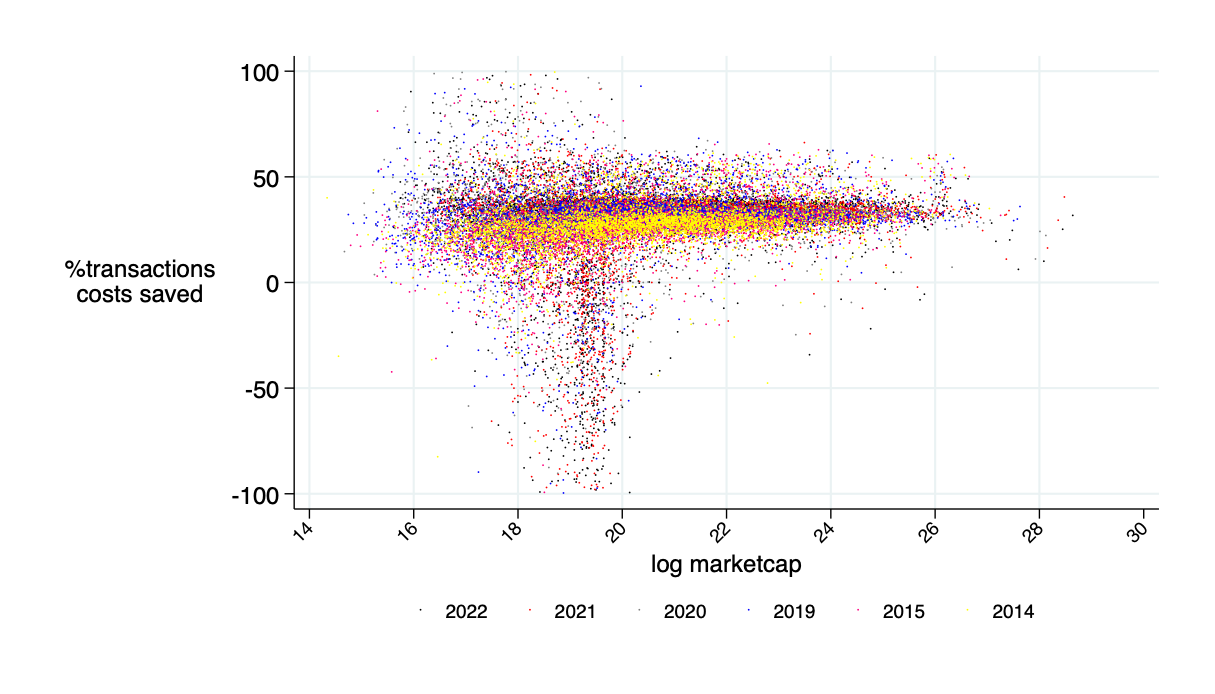

average savings: 16 bps

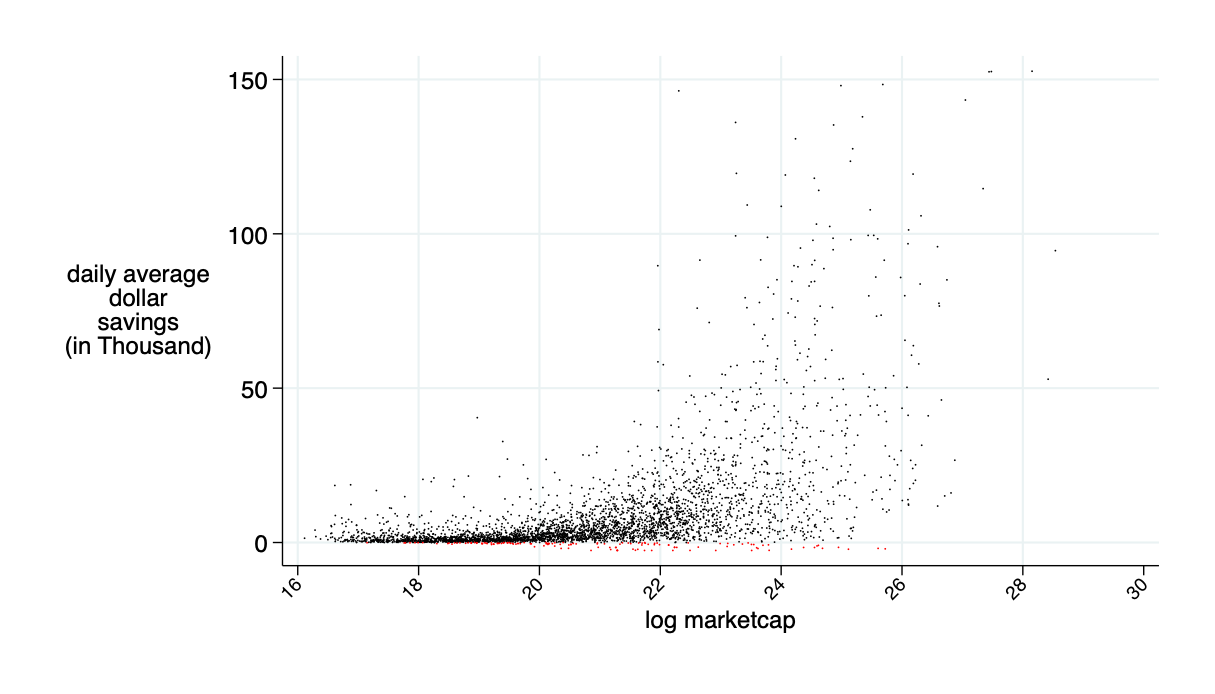

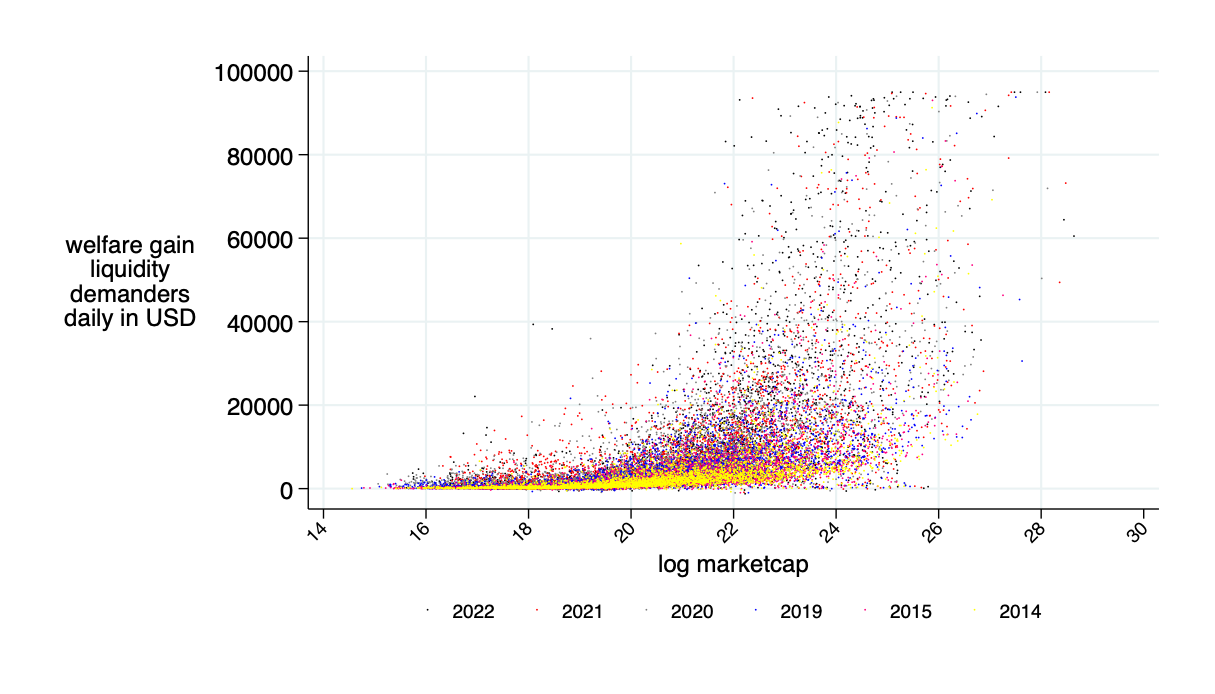

average daily: $9.5K

saves around 45% of transaction costs (measured in bid-ask spread)

average annual saving: $2.4 million

Optimally Designed AMMs with

"ad hoc" one-day backward look

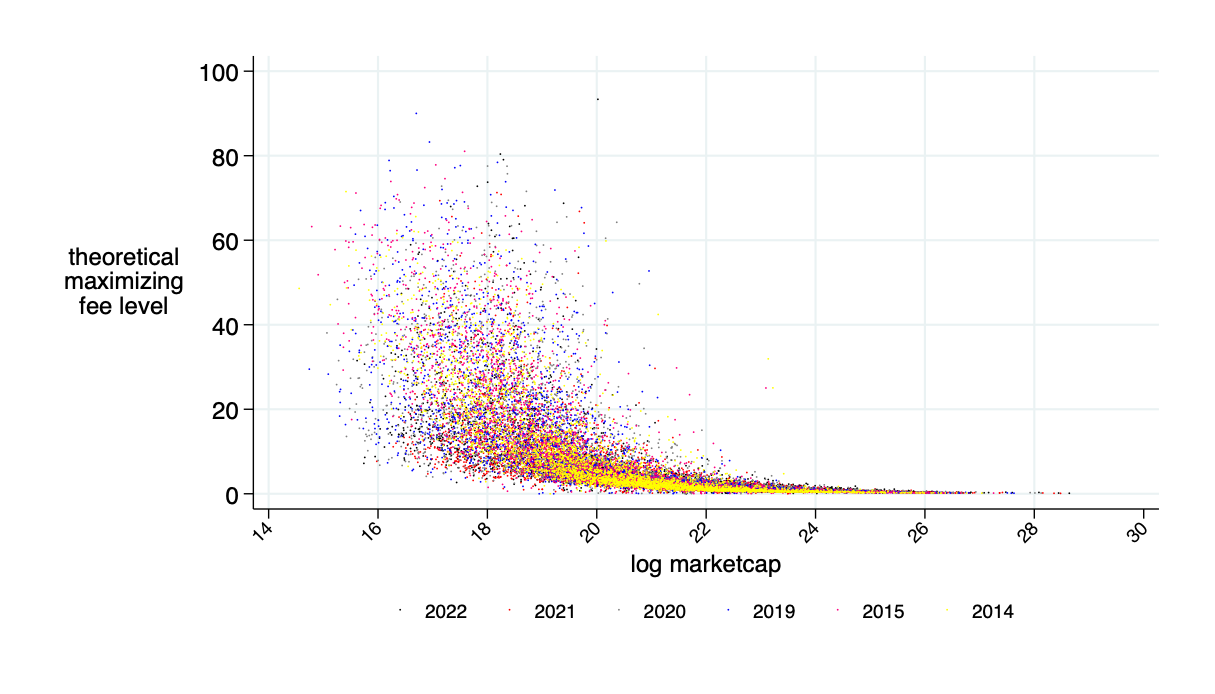

Optimal fee \(F^\pi\)

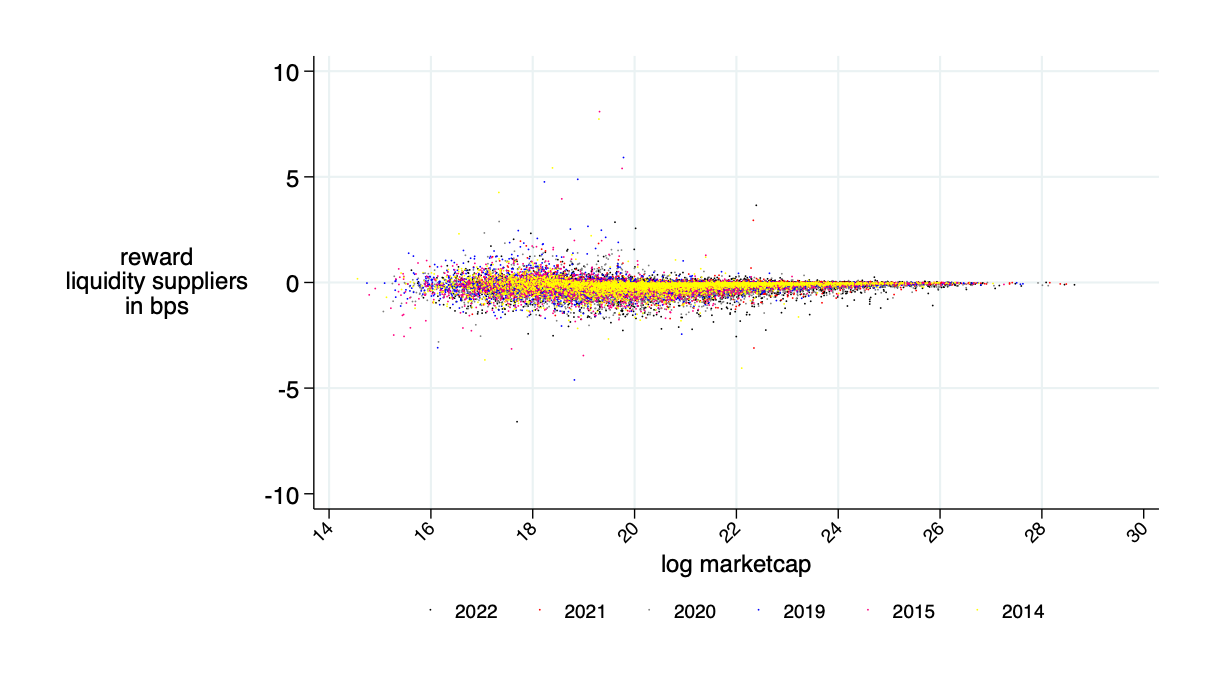

average benefits liquidity provider in bps (average=0)

Insight: Theory is OK - LP's about break even

\(\overline{\alpha}\) for \(F=F^\pi\)

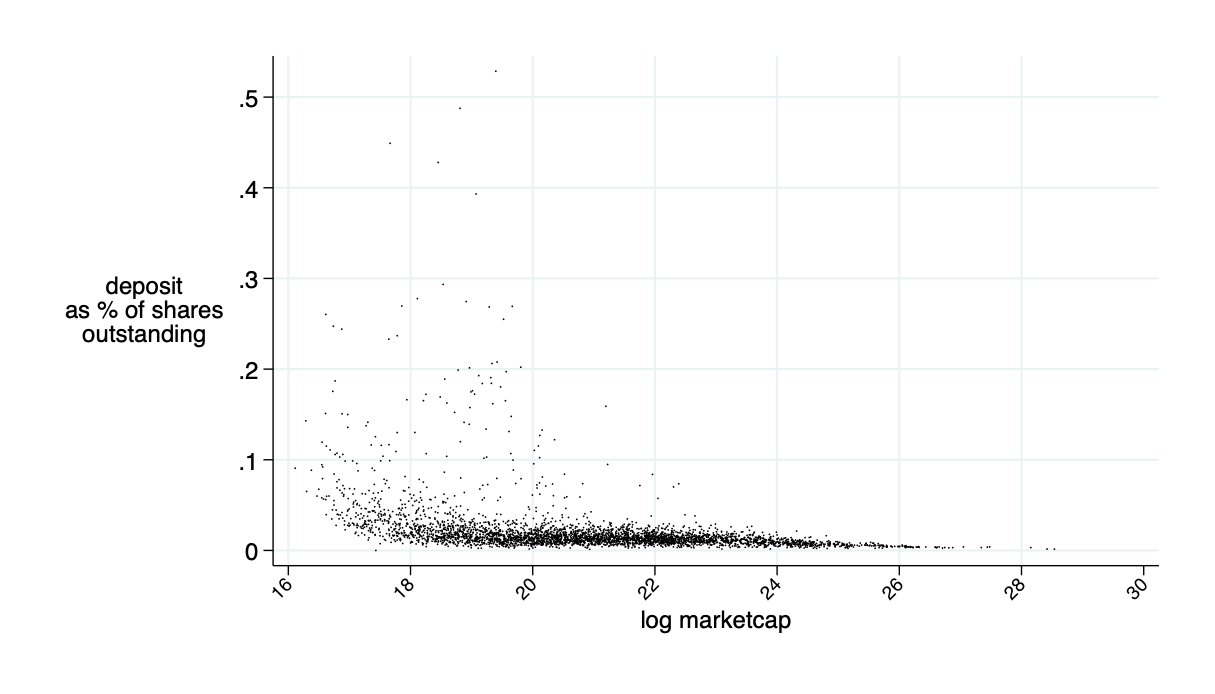

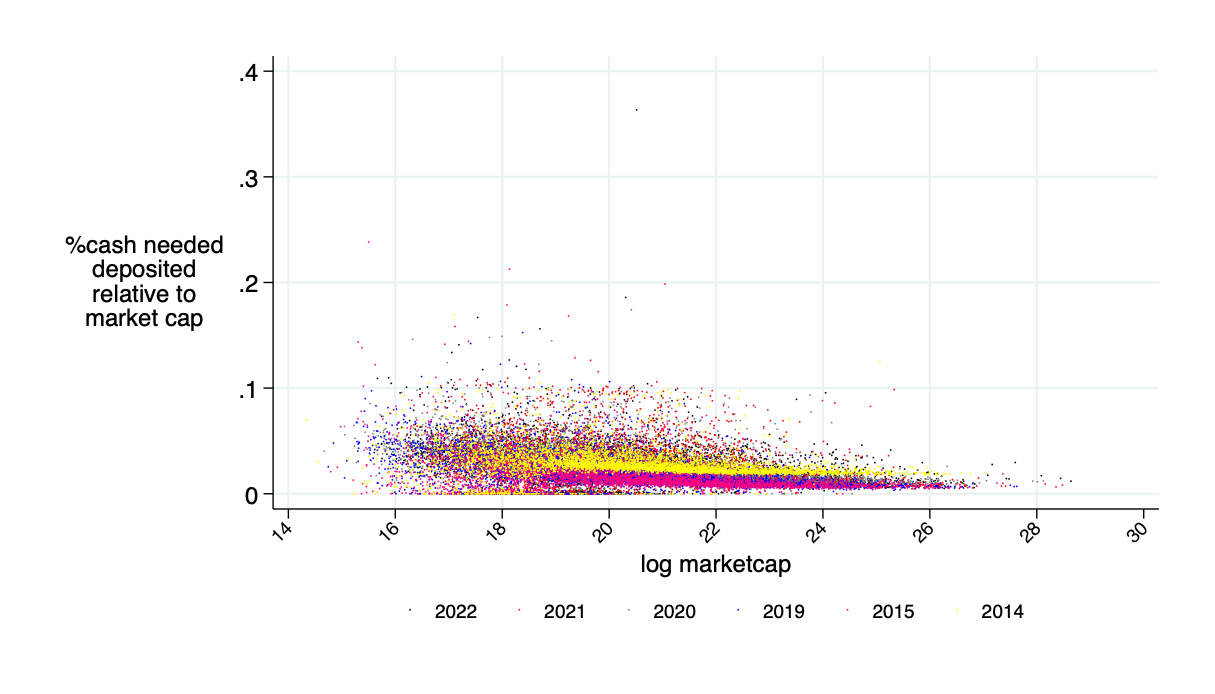

Need about 10% of market cap in liquidity deposits to make this work

actually needed cash as fraction of "headline" amount

Only need about 5% of the 10% marketcap amount in cash

AMMs are better on about 85% of trading days

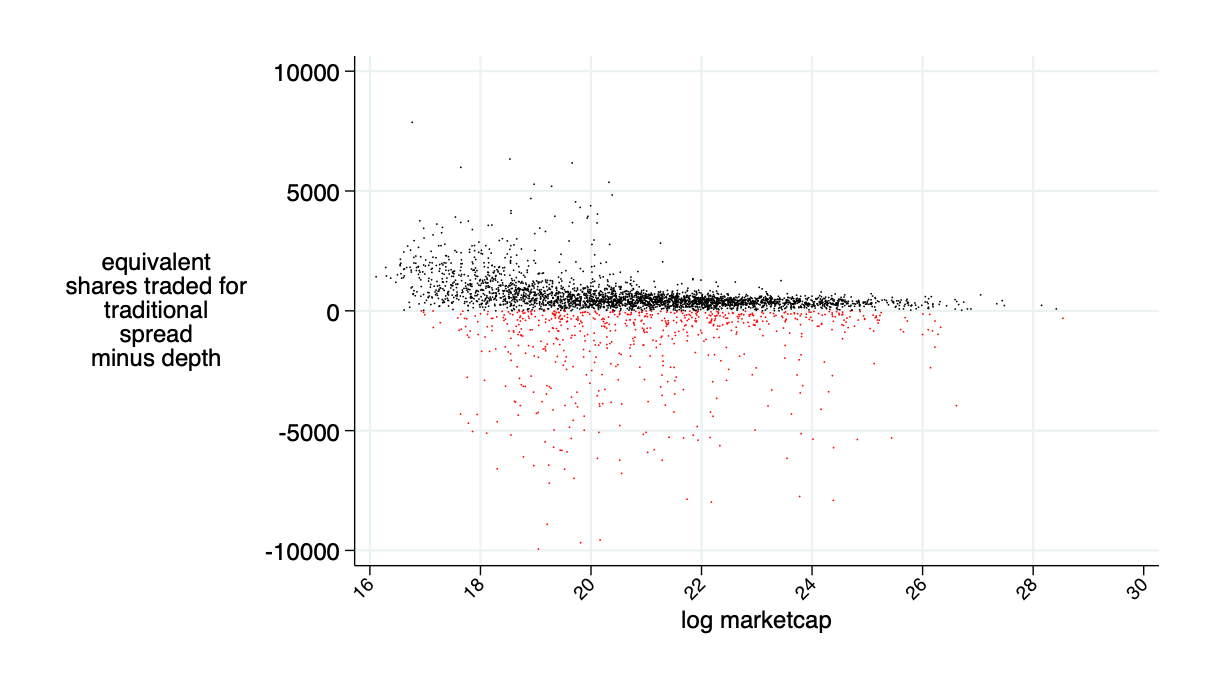

quoted spread minus AMM price impact minus AMM fee (all measured in bps)

relative savings: what fraction of transactions costs would an AMM save? \(\to\) about 30%

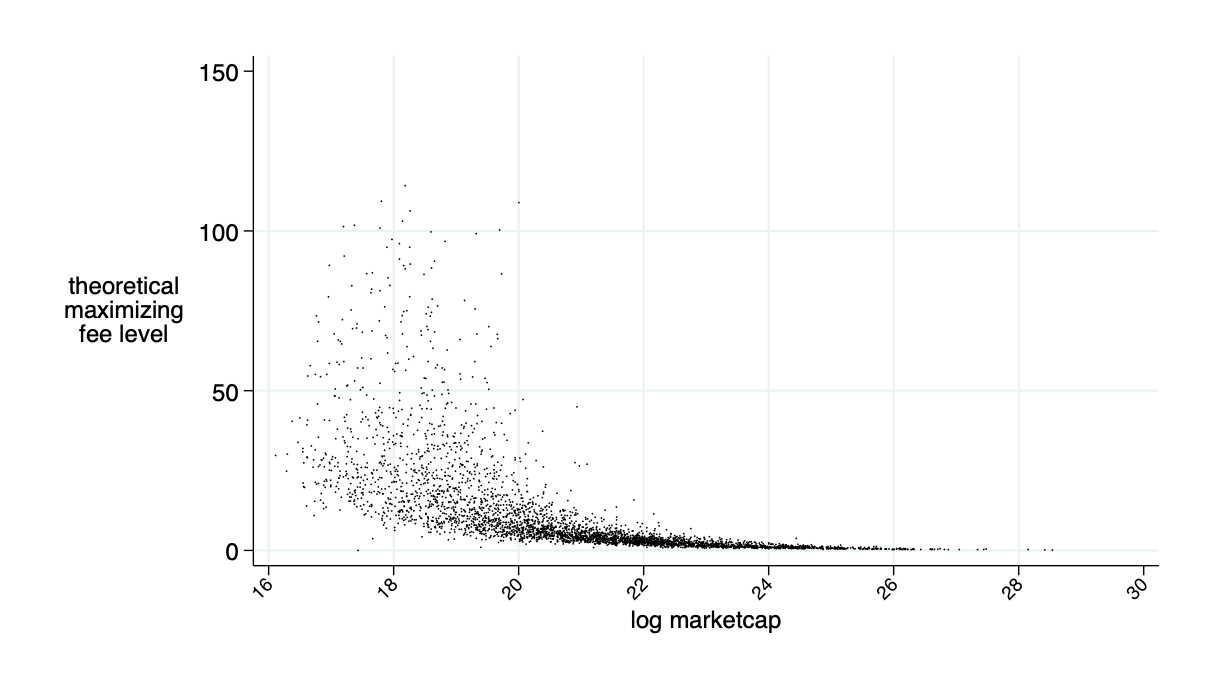

theoretical annual savings in transactions costs is about $15B

Sidebar: Capital Requirement

Deposit Requirements

- Our approach: measure liquidity provision in % of market cap

- Share-based liquidity provision is trivial: the shares are just sitting at brokerages.

- But: requires an off-setting cash amount

- Cash is not free:

- at 6% annual rate, must pay 2bps per day.

- Would need to add to fees

- But: do we need "all that cash"?

- No.

- (hand-waving argument)

- 2nd gen AMMs have liquidity provision "bands": specify price range for which one supplies liquidity

- Here: specify range for \(R\in(\underline{R},\overline{R})\)

- Outside range: don't trade.

- Inside range: "full" liquidity with constant product formula.

- Implication: only need cash and shares to satisfy in-range liquidity demand.

- For return \(R\), the following number of shares change hands: \[q=a\cdot(1-\sqrt{R^{-1}}).\]

- Fraction of share deposit used \[\frac{q}{a}=1-\sqrt{R^{-1}}.\]

- Fraction of cash used \[\frac{\Delta c ("R")}{c}=\frac{1-\sqrt{R^{-1}}}{\sqrt{R^{-1}}}.\]

- Example for \(R=.9\) (max allowed price drop \(=10\%\)) \[\frac{\Delta c ("R")}{c}=-5\%.\]

- \(\Rightarrow\) "real" cash requirements \(\not=\) deposits

Literature

AMM Literature: a booming field

- Theory

-

Lehar and Parlour (2021): for many parametric configurations, investors prefer AMMs over the limit order market.

-

Aoyagi and Ito (2021): co-existence of a centralized exchange and an automated market maker; informed traders react non-monotonically to changes in the risky asset’s volatility

-

Capponi and Jia (2021): price volatility \(\to\) welfare of AMM LPs; conditions for a breakdown of liquidity supply in the automated system; more convex pricing \(\to\) lower arbitrage rents & less trading.

-

Capponi, Jia, and Wang (2022): decision problems of validators, traders, and MEV bots under the Flashbots protocol.

-

Park (2021): properties and conceptual challenges for AMM pricing functions

-

Milionis, Moallemi, Roughgarden, and Zhang (2022): dynamic impermanent loss analysis for under constant product pricing.

-

Hasbrouck, Rivera, and Saleh (2022): higher fee \(\Rightarrow\) higher volume

-

-

Empirics:

-

Lehar and Parlour (2021): price discovery better on AMMs

-

Barbon and Ranaldo (2022): compare the liquidity CEX and DEX; argue that DEX prices are less efficient.

-

-

Math Literature: large number of papers that study AMMs in applied maths

- e.g. Cartea, Drissi, Monga (2023): closed form solution to IPL and optimizing strategy

The Bigger Picture and Last Words

Summary

- AMMs do not require a blockchain - just a concept

- could be run in the existing world (though there are institutional and regulatory barriers)

- Our question:

- Can an economically viable AMM be designed for current equity markets?

- Would such an AMM improve current markets?

- Answers:

- Yes.

- Massively.

- Source of Savings:

- Liquidity providers \(\not=\) Citadel!

- \(\to\) passive liquidity provision

- \(\to\) use idle capital

- \(\to\) + better risk sharing

- pooling of liquidity

- pro-rated

- fee income

- risk

- Liquidity providers:

- use existing assets to earn passive income

- Liquidity demanders:

- predicatable price

- continuous trading

- ample liquidity

@financeUTM

andreas.park@rotman.utoronto.ca

slides.com/ap248

sites.google.com/site/parkandreas/

youtube.com/user/andreaspark2812/