Background info for FI Trading Cases

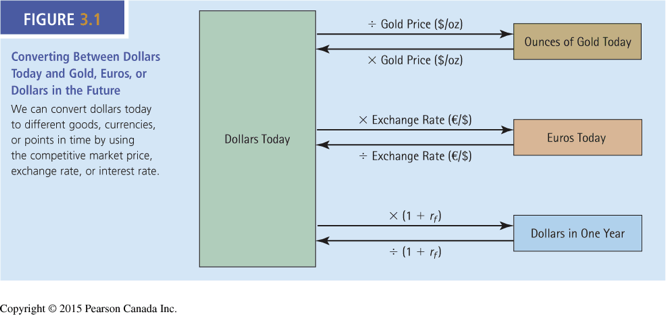

No arbitrage \(=\) what pays the same must cost the same

-

Example 2 one good for another

- Jeweler offer 400 ounces of silver for 5 ounces of gold

- Prices per ounce:

- gold: \(\$1,108.79\)

- silver: \(\$14.46\)

- Good deal?

- Dollar value 400 ounces silver = \(\$5,784\)

- Dollar value 5 ounces = \(\$5,543.95\)

-

Example 1 one financial product for another

- Offer 5 Bitcoins for \(\$300,000\)

- Price (Feb 21, 2021): 1 BTC = \(\$ 57,618\)

- Good deal?

- 5 BTC = \(\$288,090\)

-

Example 3 money today vs money tomorrow

- Offer: exchange \(\$100,000\) today for \(\$105,000\) in 1 year

- Interest rate for safe investment \(r\)

- Good deal?

- \(\$100,000=\frac{\$105,000}{1+r}?\)

The quick and dirty on FI1

New symbol?

What's notable about the security?

TB6M

T-Bill that pays a guaranteed $100 six months after beginning of the case

What do you have to do?

decide whether or not to buy or sell the T-Bill

Anything special?

- there is a risk-free rate that pays 7% p.a.

- interest is paid every week.

Things to explain

- there is a risk-free rate that pays 7% p.a.

- interest is paid every week \(\to\) every 12 s

-

Payments: receive $100 per owned bond, pay $100 per owed bond

-

Your task is to beat the risk-free rate!

Time value of money calculations: T-Bills

- Annual interest rate \(r\)

- Terminal cash flow \(C\)

- Price for the investment \(P\)

- Payment periods per year \(T\)

- Time till terminal cash flow \(t\)

in case: \(T=52\), \(C=\$100\)

The quick and dirty on FI2

New symbol?

What's notable about the securities?

TB6M, TB12M, 1YCP

- Two T-Bill that pays a guaranteed $100 after six and twelve months respectively

- Semi-annual coupon-paying bond

What do you have to do?

decide whether or not to buy each of the securities

Anything special?

- saving account rate changes after 6 months

- must pay accrued interest on bond

Time value of money calculations: T-Bonds

- Annual interest rate \(y\)

- Face value \(F\)

- Coupon rate \(c\)

- Coupon frequency \(f\)

- Years till maturity \(Y\)

- Coupon payment \(\frac{c}{f}F\)

- Price for the bond \(P\)

- Interest payment periods per year \(f\)

- Total payment periods: \(T=f\cdot Y\)

Special case: everything annual

- The annual rate is implied by the amount that people are willing to pay for the cash flow.

- Its name is yield to maturity.

Clean vs dirty prices

Oddity of bonds: when you buy a bond between two coupon dates, then the seller is entitled to the portion of the coupon payments that pertains to the holding period. Economically, this is total nonsense, but here we are. Formally:

clean price = does not contain accrued interest

dirty price = contain accrued interests

RIT quotes clean prices (so you need to add accrued interest to your cost)

\(t=\) Time till terminal cash flow

Time value of money calculations: T-Bonds

- Annual interest rate \(r\)

- Face value \(F\)

- Coupon rate \(c\)

- Coupon frequency \(f\)

- Coupon payment \(\frac{c}{f}F\)

- Price for the bond \(P\)

- Interest payment periods per year \(T\)

- Years till maturity \(Y\)

- Time till terminal cash flow \(t\)

in case:

- \(T=52\) (weekly)

- \(F=\$100\)

- \(f=2\) (semi-annual)

- \(Y=1\)

- prices = clean

present value of cash flows

=

note that you have to pay accrued interest so your willingness to pay for the cash flow is diminshed by this exact amount (which is why it is economic nonsense to charge it)

Note: the formulae two slides up were based on the beginning of a time period; in RIT, there are "interim" interest payments; hence the different formulation

The quick and dirty on FI2-B

New symbol?

What's notable about the securities?

no, same as FI2

there is no savings account/savings account rate is 0%

What do you have to do?

exploit arbitrage opportunities among the three securities

Anything special?

revisit your knowledge from bond pricing from MGT330

A special type of bond: Zero Coupon Bonds

- Annual interest rate \(y_t\) for year or time interval \(t\)

- Face value \(F\)

- No coupon (hence "zero")

- Years till maturity \(t\)

- Price for this zero-coupon bond \(S_t\)

Interpretation:

- \(y_t\) is the interest rate for a \(t\) year investment.

- Can also thing of \(y_t\) as the discount rate for a \(t\) year investment

No-Arbitrage

Thought experiment:

- Assume the zero-coupon bonds are for $1 each.

- You want

- annual payments of \(cF\) for \(Y\) years and

- a single payment of \(F\) after \(Y\) years.

- Which products do you need to buy?

Option 1: Buy the coupon bond

Option 2: Buy the \(cF\) zero-coupon bonds for years \(1,\ldots,Y\) and \(F\) of the \(Y-\)year zero coupon bond

for no arbitrage:

\(=\)

No-Arbitrage with two T-Bills and a bond

- Ignore the savings interest rate!

- Suppose you have 20 bonds.

- What's the payment stream?

- 20 x $5 = $100 in 1/2 year

- 20 x $5 + 20 x $100 = $2,100 in 1 year

- Is there another way to get this payment stream?

- Yes!

- 1x 6-month T-Bill

- Pays $100 in 1/2 year

- 21x 12-month T-Bill

- Pay 21 x $100 = $2,100

- 1x 6-month T-Bill

Recap on Arbitrage: payments of the instruments illustrated

For FI2-B: ignore the fair values!

today

today

+6 months

today

+12 months

coupon payment by 1YCP

1YCP face value payment

TB12M payment

TB6M

payment

coupon payment by 1YCP

A more detailed recap on arbitrage to help you better understand FI2-B

Recap on Arbitrage: now some more background

-

No arbitrage conditions can be formulated in various ways,

for instance-

A portfolio that costs you ZERO today cannot provide you with a guaranteed POSITIVE payoff in the future

- A portfolio that provides you with a guaranteed payoff of ZERO in the future cannot cost you a NEGATIVE amount today.

-

A portfolio that costs you ZERO today cannot provide you with a guaranteed POSITIVE payoff in the future

We will use the second formulation in case FI2-B

Recap on Arbitrage: what is it? what have we learned so far?

- The idea of arbitrage: what pays the same must cost the same.

- Note: Arbitrage does not mean that an asset is cheap or expensive relative to an estimate of a fundamental value (like in EV1 and EV2)

- What have we looked at so far:

- The same asset, but traded on two markets

- Two assets: a T-Bill and a savings account.

- Investing in either should give you the same payoff

- Or: they must be priced "correctly" relative to one another

Now: arbitrage portfolios

- Idea: Trade portfolios of securities

- Combinations of assets have to be priced correctly relative to one another

- \(\to\) the core of what you do in finance!

Recap on Arbitrage: payments of the instruments illustrated

For FI2-B: ignore the fair values!

today

today

+6 months

today

+12 months

coupon payment by 1YCP

1YCP face value payment

TB12M payment

TB6M

payment

coupon payment by 1YCP

Recap on Arbitrage: this case

- The problem here:

- The assets have very different payoffs:

- How can we say that they are priced correctly relative to one another?

- (I repeat: you need to forget about pricing it relative to the "savings account"!)

- The solution:

- Construct portfolios that give you the same payoff profile.

- Mathematically, this is a bit like solving a system of equations

(sorry!!! But this is actually how finance works...)

You have seen this before in your finance courses:

- Zero-coupon bonds vs. coupon bonds

- Arbitrage Pricing Theory (APT)

Recap on Arbitrage: how does it work

- Let's say the coupon rate is \(c\) and all instruments have face value \(F\)

- Mathematical formulation:

- \(x\) investment in T6M

- \(y\) investment in T12M

- \(z\) investment in 1YCP:

- Conditions. There are two payment times in 6 months and 12 months

- \(x\cdot F=z\cdot cF\) \(\Leftrightarrow\) \(x=zc\)

- \( y\cdot F=z\cdot cF+z\cdot F\) \(\Leftrightarrow\) \(y=z(c+1)\)

- Tiny snag:

- Conceptually, there is now an indeterminacy because we have three variables \((x,y,z)\) but only two constraints.

- Also: \(x,y\) and \(z\) have to be integers.

- No problem though: we can just "pick" a value for, say, \(x\) and then see if the solutions for \(y,z\) are integers.

Recap on Arbitrage: how does it work (part II)

- So let's pick \(x=1\)

- \(1=z\cdot c\) \(\Leftrightarrow\) \(z=1/c\)

- Insert in \( y=z(1+c)\) \(\Leftrightarrow\) \(y=\frac{1+c}{c}\)

- In the case, we have \(c=5\%\):

- \(z=1/0.05=20\)

- \(y=1.05/0.05=21\)

- \(\to\) so it works out.

- Note that we could have used other values for \(x\), this is not meant to have a unique solution

In fact, for \(c=0.05 \to 1/c=20\) and any integer value \(x=i\), we have:

- \(z(i)=20\cdot i\)

- \(y(i)=i\times (1+.05)/0.05=21\cdot i\)

Recap on Arbitrage: how does it work (part III)

- OK, but we have only matched payoffs.

- \(\to\) That says nothing about arbitrage or lack thereof!

- Recap: what does payoff matching say?

- Portfolio A: \(z\) 1YCP and

- Portfolio B: \(x\) T6M and \(y\) T12M

- Portfolios A & B create the same payoffs

- Economically, they are the same asset!

- No arbitrage: the portfolios must cost the same!

- Mathematically:

- \(P_{TB6m},P_{TB12M},P_{1YCP}\) are the prices then

Note: Now we have three constraints \(\to\) we could solve for \(x,y,z\)

Recap on Arbitrage: back to the case

For any integer value \(x=i\) (the number of TB6M that we buy)

- \(z(i)=20\cdot i\)

- \(y(i)=i\times(1+.05)/0.05=21\cdot i\)

So it must hold that

- \(i\cdot P_{TB6m}+21 i\cdot P_{TB12M}=20i\cdot P_{1YCP}\)

Recap on Arbitrage: back to the case

- In trading there is no one "price", there are bids and asks.

- We must now translate that into a trading strategy.

- If the condition does not hold then you would go long in one portfolio and short in the other

- So we have two conditions that must hold for no arbitrage

- \(i\cdot ask_{TB6m}+21 i\cdot ask_{TB12M}\ge 20i\cdot bid_{1YCP}\)

- \(i\cdot bid_{TB6m}+21 i\cdot bid_{TB12M}\le 20i\cdot ask_{1YCP}\)

Recap on Arbitrage: back to the case

- Let me explain with the first equation

- The portfolio

- buying \(i\) TB6M and \(20i+1\) TB12M

- selling \(20i\) 1YCP

- has exactly the same payoffs.

- The portfolio

- The portfolio

- costs you \(i\cdot ask_{TB6m}+21 i\cdot ask_{TB12M}\) for the T-bills but

- gives you a cash flow of \(20i\cdot bid_{1YCP}\)

- So if \(20i\cdot bid_{1YCP} - (i\cdot ask_{TB6m}+21 i\cdot ask_{TB12M})>0\) then you make money out of nothing!

Note: you sell at the bid and buy at the ask \(\to\) selling at bids lead to positive cash-flows, buying at asks to negative cashflows

Recap on Arbitrage: numerical example for the case

- Take the following prices

- \(bid_{1YCP}=103.85\)

- \(ask_{TB6M}=98.6\)

- \(ask_{TB12M}=92.4\)

- Cash flows in 12 months:

- \(20\cdot -5=-100\) from paying for the coupons

- \(20\cdot -100=-2000\) from paying face value

- \(+21\cdot100=2,100\) from TB12M

- \(\to\) net is ZERO

- Cash flows today:

- 2,077 from 1YCP

- -98.6 from TB6M

- -1,940.4 from TB12M

- Total: +38

- Now you trade as follows

- buy: 1 TB6M and 21 TB12M

- sell: 20 1YCP

- Cash flows in 6 months:

- \(20\cdot -5=-100\) from paying for the coupons

- \(+1\cdot100=100\) from TB6M

- \(\to\) net is ZERO

Recap on Arbitrage: payments of the instruments illustrated

today

TB12M payment

TB6M

payment

outflows

inflows

sell 20 1YCP for 2,077

buy 1 TB6M for 98.6

buy 21 TB12M for 1,940.4

net gain:

$38

after

6 months

after

12 months

receive $100 for 1 TB6M

pay 20 \(\times\) $5\(=\)$100 for coupons of 1YCP

pay 20 \(\times\) $5\(=\)$100 for coupons of 1YCP

pay 20 \(\times\) $100\(=\)$2,000 for face value of 1YCP

receive 21 \(\times\) $100\(=\)$2,100 for face values of TB12M

net gain:

$0

net gain:

$0

Why is this arbitrage?

Because you make an instantaneous profit for a portfolio that is payoff neutral in the future (creates no losses nor benefits)

One last snag: accrued interest

- The strategies I presented so far are for the beginning of the case.

- At any point "in the middle" you need to pay accrued interest for the bond.

- Therefore, you need to adjust as follows

- \(i\cdot ask_{TB6m}+21 i\cdot ask_{TB12M}\ge 20i\cdot (bid_{1YCP}+\) accrued interest)

- \(i\cdot bid_{TB6m}+21 i\cdot bid_{TB12M}\le 20i\cdot (ask_{1YCP}+\) accrued interest)