Discussion of "Stablecoin Runs and the Centralization of Arbitrage"

Paper by Ma, Zeng, and Zhang

Discussion by: Andreas Park

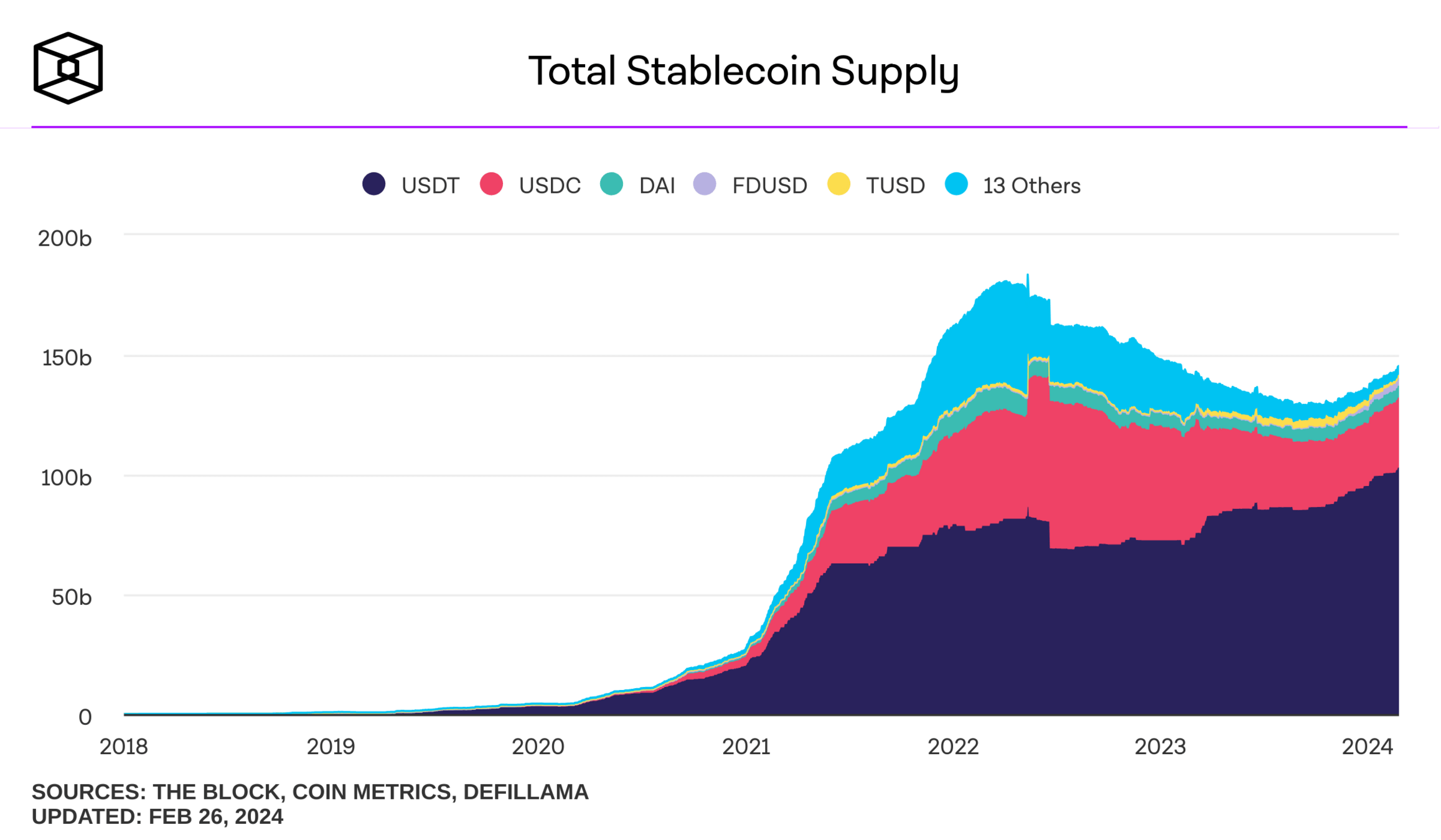

What is a stablecoin?

digital representation of a unit of a fiat currency on a blockchain

pulled from Nick Carter's talk on "Will stablecoins serve or subvert U.S. interests?"

stablecoins are crypto's/blockchain's first "killer" use case

BTC, ETH

HQLA: USD, EUR

asset (gold)

fee-backed

Seigniorage

Crypto

Traditional

Algorithmic

Collateral-Backed

Taxonomy of Stablecoins

DEPOSITS

other assets

JPM coin

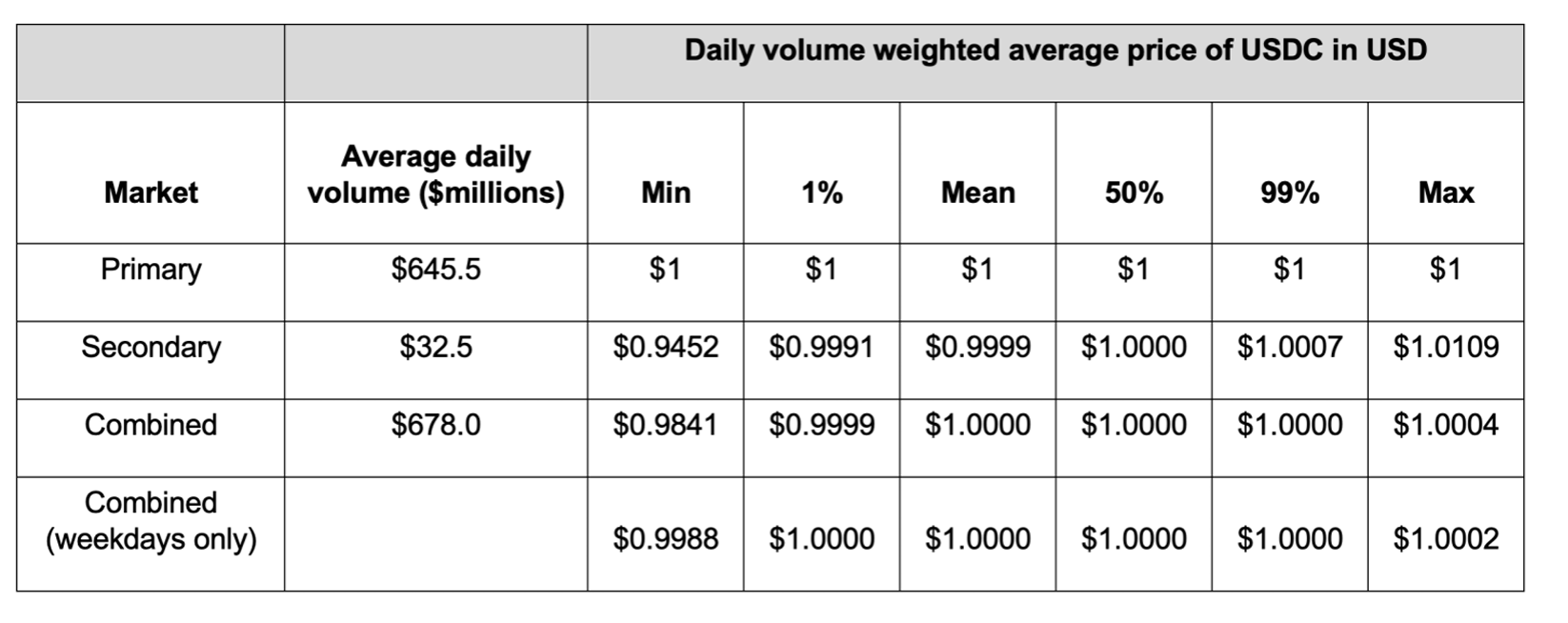

USDC

USDT

UST, Basis, Neutrino

DAI, FEI

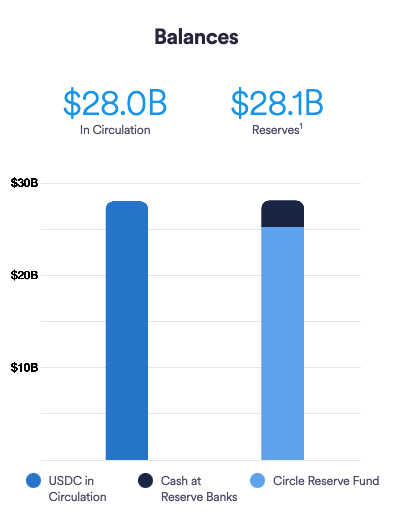

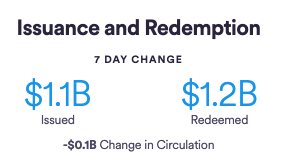

Collateral Backed Stablecoins: USDT & USDC

\(\Rightarrow\) 5% over-collateralized

primary market acces: 6 entities only

Collateral Backed Stablecoins: USDT & USDC

- "Cash at Reserve Banks" once was SVB

- Reserve fund = short-date US treasuries & overnight repos

primary market acces: 560+ entities

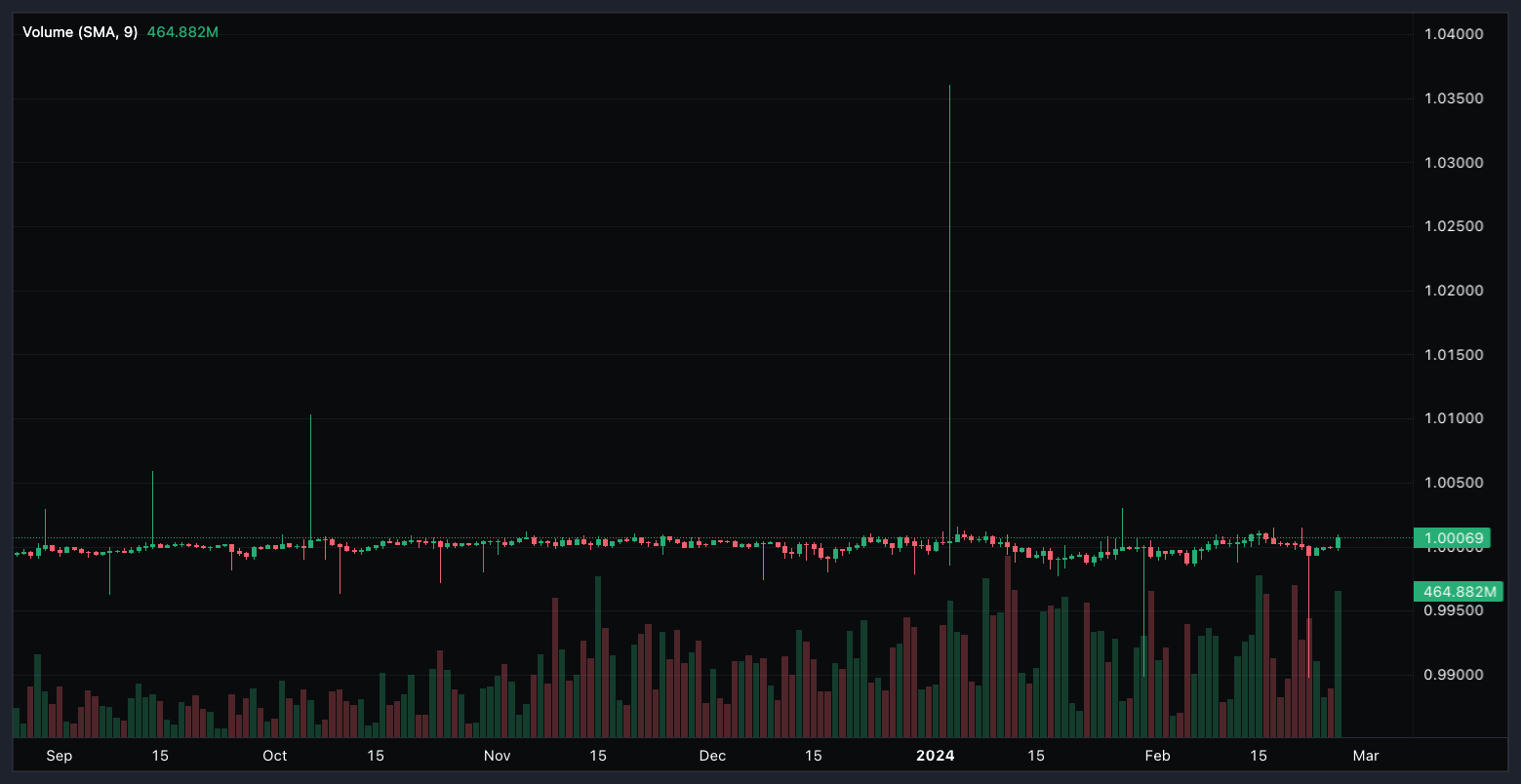

What makes a Stablecoin stable?

USD-USDT (6 months)

\(\Rightarrow\) need a primary/reference market mechanism to allow for forces of arbitrage to align prices

- stablecoins are issued

- by a single entity or

- a blockchain-based algorithm (smart contract)

- they trade in a secondary market

- on crypto-exchanges against fiat

- on crypto-exchanges against cryptos

- on-chain against other tokens

- \(\Rightarrow\) stablecoin price fluctuates

Arbitrage when price(stablecoin)>$1

arbitrageur

issuer/ primary market

secondary market

What makes a Stablecoin stable?

Arbitrage when price(stablecoin)<$1

arbitrageur

issuer/ primary market

secondary market

This paper: Runs!

Key Model Ingredients and what they do

1. stablecoin with primary and secondary market

2. liquidity transformation by stablecoin issuer \(\to\) Diamond-Dybvig bank run model

3. Morris-Shin-style global game

- secondary market trading creates price dislocations

- requires arbitrage related liquidations in the primary market

- arbitrage related primary market liquidations require early sale of illiquid asset

- prospect of early sale creates run risk

- primary assets subject to fundamental risk

- global games creates unique equilibrium for run

- run threshold is the key variable of interest

What's the Key Tension

- price drop stablecoin to USD prompts arbitrageurs to

- buy stablecoins for USD in secondary market

- sell stablecoins for USD at parity in primary market

-

to exchange stablecoins for USD at parity issuer needs to

-

find cash or

-

sell illiquid assets

-

Issues in the Secondary Market

Issues in the Primary Market

What's the Key Tension

What's the Key Mechanism

- running has costs

- you lose future convenience yield

- you sell when the price is below parity

- you have price impact

- (fire-)sale of illiquid assets is costly and reduces value of stablecoin backing

- highly illiquid backing makes costly sale more likely

- increases run risk

key implication:

less liquid backing \(\to\) more run risk

- price drop stablecoin to USD prompts arbitrageurs to

- buy stablecoins for USD in secondary market

- sell stablecoins for USD at parity in primary market

-

to exchange stablecoins for USD at parity issuer needs to

-

find cash or

-

sell illiquid assets

-

Issues in the Secondary Market

Issues in the Primary Market

key implication:

more liquidity \(\to\) more run risk

Intuition for Key Result

key implication:

more liquidity \(\to\) less price impact

less price impact \(\to\) more run risk

more abitrageurs \(\to\) more secondary market liquidity

Model Implications

- less liquid backing \(\to\) more run risk

- more arbitrageurs \(\to\) more run risk

- less liquid backing \(\to\) choose fewer arbitrageurs

- more liquid backing \(\to\) may have higher run risk (than expected)

Comments

Comment 0: all OK with the theory?

- theory model is fine (and well thought out)

- big question: is it true and does it capture what's going on?

Comment 1: What brings prices back to parity?

1. primary market arbitrage

2. secondary market arbitrage

Arbitrage when price(stablecoin)<$1

arbitrageur

issuer/ primary market

secondary market

arbitrageur

issuer/ primary market

secondary market

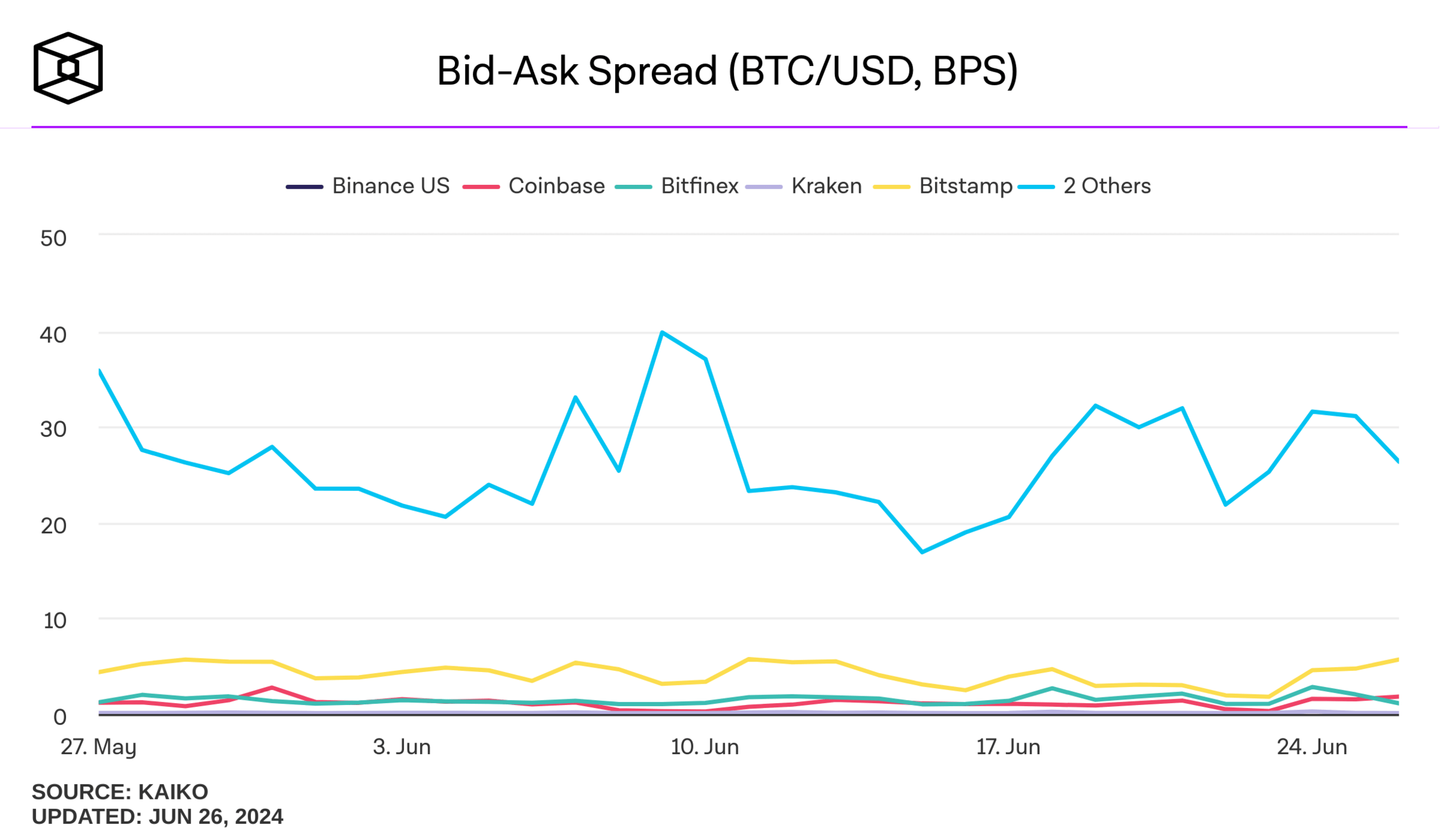

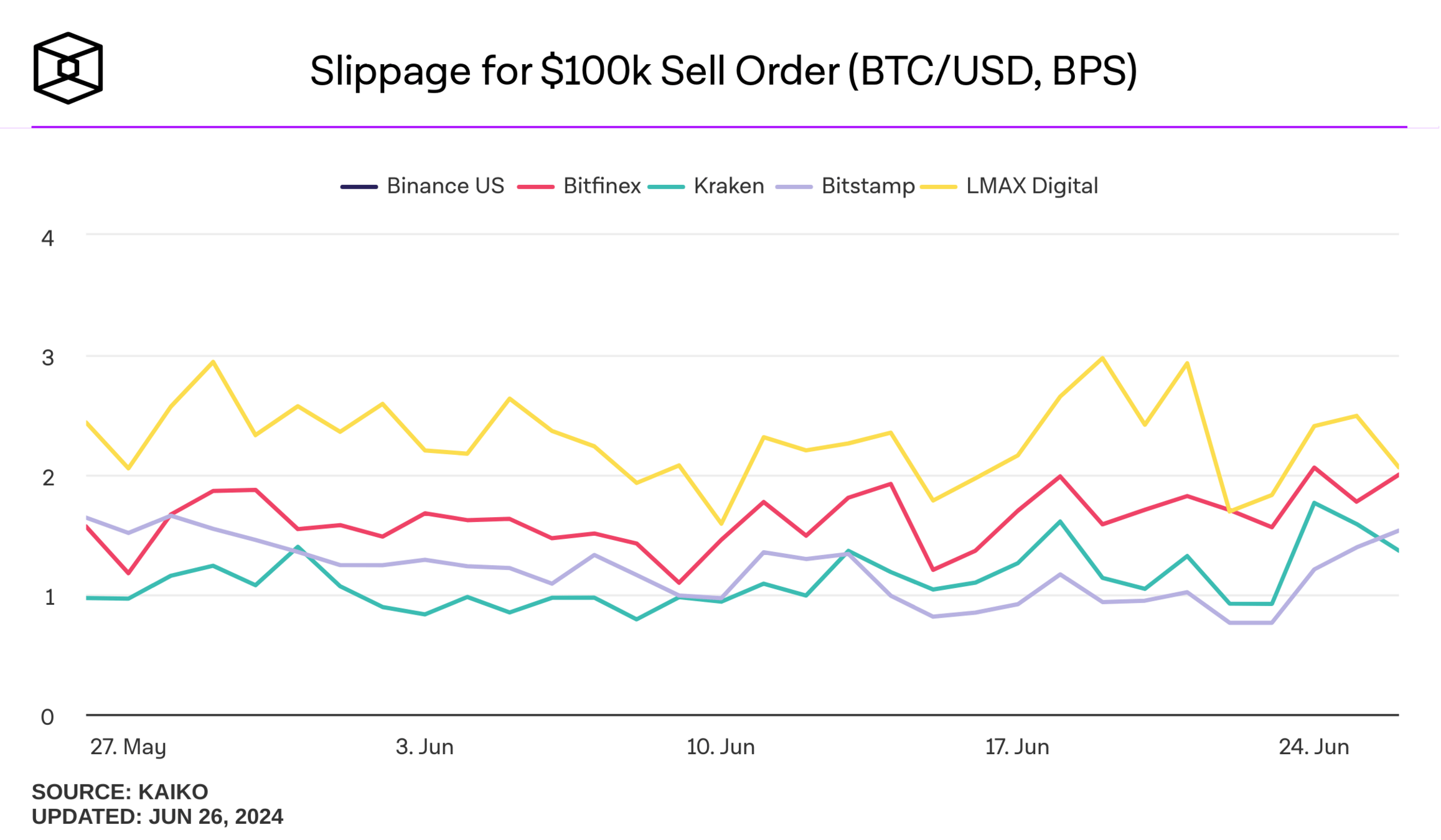

Cost on Kraken: .1 bps

Source: Liao (2023) "How to preserve the singleness of money for tokenised forms of money? "

Does secondary market activity justify primary market flows?

Comment 2: Price impact argument for infinitesimal investors

- secondary market liquidity does a lot of heavy lifting in the model

- concern about price impact is the cited reason for run aversion

- but: investors (prospective runners) are infinitesimal and have no price impact.

- So ... ?

Comment 3: cranky referee #2

censored ;-)

Comment 4: issuers optimize over #of arbitrageurs?

- key variable: # of arbitrageurs for primary market.

- Tether: 6

- Circle: 500+

- In the grand scheme of things, the choice of \(\phi\), the assets to back with seems much more salient.

- Appendix D is not convincing.

- alternative explanation: Tether has bad access to banking network

- \(\to\) cannot enable more arbitrageurs

Comments 5: odds and ends

- concentration measure for arbitrage

- fraction of top 5?

- why not Hirshman-Herfindahl Index (or 1/HHI)

-

institutions of Tether and Circle operations

-

Tether:

- large discrete chunks traditionally issued via Bitfinex

- banking connection in the Carribean \(\to\) cannot redeem for \(r\)

-

Circle:

- strong connection banking network

- high redeem-issuance frequency \(\to\) redeem USDC for \(r\)

-

Tether:

-

Calibration

- CDS spread \(\not=\) CDS price (since 2009), so Appendix G requires some work (see ISDA's pricing model or Augustin, Saleh, Xu (JEDC 2020))

Comment 3: cranky referee #2

- The formulation of theorems requires work.

-

Proposition 2: "The run threshold, that is, run risk, is increasing in \(\phi\) if and only if \(g(\phi) > K\), where \(g(\phi)\) is continuous and strictly decreasing in \(\phi\) , and satisfies \(\lim_{\phi \to 0} g(\phi)>0\)."

- Proposition 3: "When the stablecoin engages in a higher level of liquidity transformation, the stablecoin issuer optimally designs a more concentrated arbitrageur sector, that is, \(n\) decreases in \(\phi\) when \(\phi\) is not too large and the cumulative distribution function \(G\) is close to linear."

- same for other propositions

-

- comparative statics results are static but are described in text like they are dynamic