Dissertation Overview

Brandon John Williams

May 4, 2026

Dissertation Overview

Dissertation Chapters:

- Constrained Delegation in Veto Bargaining

- Perfecting Performance: A Gendered Perspective

- Segmented Markets and Moral Preferences

Constrained Delegation in Veto Bargaining

with Richard Van Weelden and Alistair Wilson

Project Summary

- We investigate an environment of constrained delegation: an uniformed party delegates some of their decision power to an informed party

- The delegating party can impose limits (constrained)

- The informed party has veto power (outside option)

- Theory identifies constrained delegation as an optimal mechanism, but do people use it efficiently, and how much power do they cede?

- We experimentally investigate using a buyer-seller framework

Results

- Constrained delegation greatly increases efficiency, to levels roughly equivalent with pre-play communication

- Proposers concede a large amount of bargaining power and efficiency gains are captured by the responders

- Additional treatments allow us to identify:

- Ceding power not driven by other-regarding behavior

- Mechanism framing plays a large role in the distribution of the gains (evidence of optimization failure)

- Constraining power of the veto threat, and that without a veto, delegation hurts the proposer

- Participants are reasonably well-calibrated to the value of the delegation mechanism

- Majority of responders reveal their true value in chat and are more honest in delegation

Status and Next Steps

- Data collection complete: 6 treatments (2x2 plus 2 modified treatments)

- Additional analysis:

- Chat logs

- Addendum treatments

- Next steps

- Manuscript draft

- Journal submission

Perfecting Performance: A Gendered Perspective

with Lester Lusher and Lise Vesterlund

Project Summary

- We observe that women outperform men academically

- Do men and women have different standards of performance?

- Are standards for women expected to exceed those of men?

- Use administrative data from the University of Pittsburgh to identify performance differences across grade distributions and course retakes

- Intro to micro course gives us insight into gender differences at the highest (A- to A) grade margin

- Survey and experimental evidence for performance standards and expectations

Experiment

- We ask participants: who do you think is more likely to perform better on an economics quiz?

- We then elicit second-order beliefs: who do you think other participants selected?

Preliminary Results

- First-order evidence with mixed-gender pairs

- Women more likely to be chosen

- Women experience stronger returns to GPA than men

- With single-gender pairs, men experience higher returns to GPA than women

- Even conditioning on GPA, women's worst grade is indicative of their probability of being selected (blemish effect)

Status and Next Steps

- Data collection complete: N=202

- A considerable amount of analysis needed:

- Second-order elicitation

- Condition on participant characteristics

- Timeline

- Additional data analysis

- Present results for feedback

- Write first draft

Segmented Markets and Moral Preferences

There is not one banking sector. There are two—one for the poor and for the rest of us—just as there are two housing markets and two labor markets.

- Matthew Desmond, Poverty by America

Segmented Markets

- Large, traditional markets that serve the majority of people, with small, peripheral markets designed to serve those excluded from the traditional market

- Consumers in peripheral markets may be defined by vulnerability through weak outside options

- Often viewed as exploitative—predatory inclusion as attributed to historian Keeanga-Yamahtta Taylor—because search frictions and weak outside options lead to limited bargaining power and one-sided surplus extraction

- Examples of segmented markets:

- Housing rental vs renting with an eviction

- Labor market vs labor as an undocumented immigrant or with a criminal conviction

- Traditional lending vs payday, auto title, or pawn loans

Research Question

Do consumer moral concerns/repugnance maintain segmented markets and exclude some consumers from the standard market?

Commercial banks could offer payday loans with fees up to eight times less than the standard market price and still turn a profit.... But getting into the payday loan business would mean offering financial products designed specifically for a down-market clientele, loans that would come with APRs between 40 and 80 percent and serious reputational baggage. So far the suits at JPMorgan Chase and Citigroup have decided it is not worth it.

-Matthew Desmond, Poverty by America

Research Approach

- Model of segmented markets, using payday loans as a guide

- What forces would be sufficient to keep markets and consumer groups segmented?

- Identify behavioral or policy changes that could reduce or eliminate peripheral market power

- Document empirical structure and response to market changes

- Bank entry into small-market loans (US Bank 2019)

- Policy changes to cap interest (Illinois 2021) or other policy changes (Ohio 2018: more time to repay, repayment schemes)

- Experimentally identify repugnance that constrains firms

- To what extent do people respond to perceived exploitation when choosing to transact and do firms react accordingly?

- Estimate welfare changes via a reduction in the distance (or unification) between markets

About Payday Loans

- Payday loans began in the 1990s as a response to:

- Deregulation of the banking industry

- Elimination of interest rate caps

- Absence of small loan providers for short-term credit (UNC School of Law, 2001)

- The payday loan process:

- Consumer needs a source of income and a checking account, to allow access or a dated check

- Typically no credit check (and no benefit to credit score) and no collateral

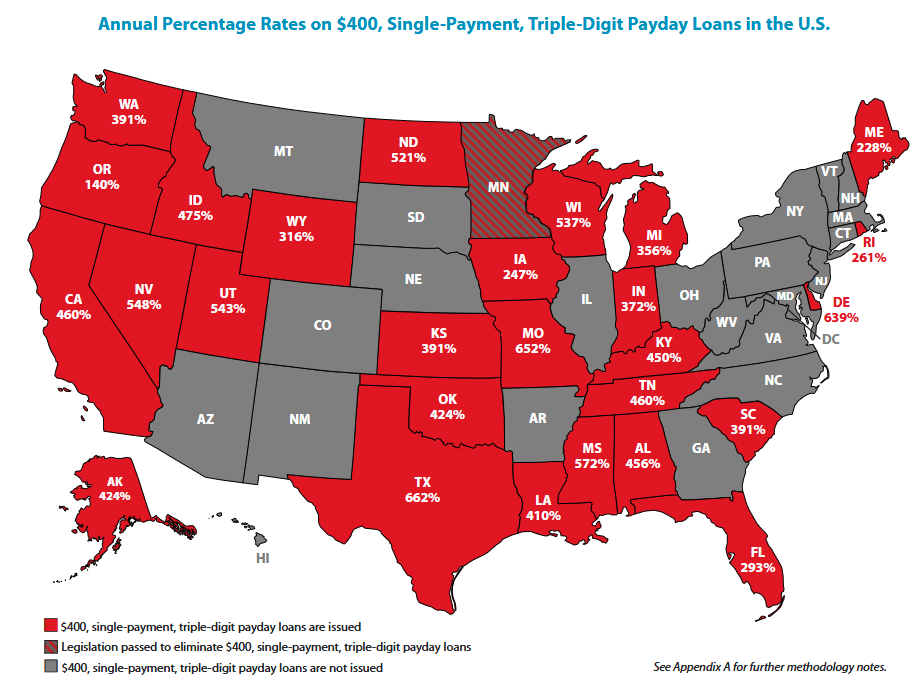

- Small dollar amount (<$1000) with high interest or fees (ranging from $10 to $30 per $100 borrowed in two weeks, or 260% to 780% annualized percentage rate)

Data from Pew unless otherwise noted

About Payday Loans

- 12 million borrowers annually

- Approximately 5.5% of adults have borrowed in the last 3 years

- The average borrower takes out 8 loans, each lasting 18 days, of $375 each per year and pays $520 in interest

- $15 in fees on $100 equals 391% APR on the loan

- 4 in 5 loans are rolled over or renewed

- 1 in 5 loans end up costing more than initially borrowed

- Borrowers are: those without a four-year college degree; home renters; black; those earning below $40,000 annually; and those who are separated or divorced

- 81% of borrowers said they would cut back on food or clothing if a payday loan was unavailable (or use over-draft as alternative)

- 20% default at some point (many after renewing more than 5 times)

Data from Pew unless otherwise noted

Center for Responsible Lending

Alabama, Idaho, South Carolina, Utah and Wisconsin have no cap except for "unconscionable" loans

Exploitative Market?

- Payday lenders are widely criticized: 3% of voters hold a favorable view of payday lenders (GBA Strategies 2016)

- But the regulatory landscape is somewhat more complicated:

- 71% of Illinois payday borrowers supported a 36% rate cap (Lake Research Group 2024)

- Nearly all payday loan borrowers say that the loan was useful to them (96%) and that they used them to pay bills (46%), avoid overdraft (23%), or pay for emergency expenses (57%). (Community Financial Services Association of America 2016)

- 74% said they have no other option than to take out a loan. (CFSAA 2016)

- 2/3 of general public support more regulation, while 2/3 of borrowers oppose regulation (CFSAA 2016)

Why would(n't) a bank enter this market?

Interest rates in the payday sector considerably exceed typical maximum credit card APR (26%) or personal loan APR (21%)

What could explain the segmented market structure?

Why would(n't) a bank enter this market?

- It is not profitable for a bank to loan at short-term, small dollar amounts with high default risk

- Payday loans operate at considerable profit margins, even when taking default risk into account (Flannery and Samolyk, 2005)

- A sizable cost for many payday lenders is physical infrastructure that banks already have

- Payday loans already require a bank account, so banks already have access to information on borrowers

- Regulations do not allow it

- Banks are exempt from usury laws and have "exportation power" to lend at the cap of their home state (Section 85 of the National Bank Act)

- There would be reputational harm to the lender

Literature Review: Payday Lending

- Moral hazard (Karlan and Zinman 2009) and adverse selection (Stiglitz and Weiss 1981) may mean that lenders compete on factors other than price

- Access to credit is essential for smoothing income or responding to shocks, so payday loans may provide needed liquidity; however, payday loan access leads to increased difficulty paying other bills (Melzer 2011)

- Time inconsistency might explain borrowing at extremely high interest rates (Laibson 1997), but experienced borrowers reveal themselves to be sophisticated about their future borrowing (Allcott et al., 2021), suggesting that prohibiting payday loans may be welfare reducing

- Contribution: literature has largely focused on payday loans or traditional lending as their own separate market or product

Literature Review: Morals and Repugnance

- Repugnance can constrain markets for things that are considered taboo or problematic to exchange for money (Roth, 2007)

- Usury has a long history of being repugnant (Aristotle, 350 BCE)

- Markets can undermine moral values (Falk and Szech, 2013), while at least some firms and consumers have a preference for social responsibility (Bartling et al., 2015)

- Contribution: Repugnance that constrains only some actors and becomes a market-separating force that confines some types to repugnant markets alone

Model: Conceptual Framework

A model of traditional loans vs payday lending captures:

- Consumers, with a true risk of default and some signal of type

- Outside options vary by consumer type

- Search frictions that vary by market type, such that they are higher in the peripheral market

- At least some consumers care about the ethical practices of the firm in addition to the price

- Firms, who compete over prices for the loan interest rate

- Firms choose to offer in an interest rate interval, where choosing to omit a high interest rate removes them from the corresponding market

- Consumers have some way of detecting which market(s) the firm is operating in

Model

- Model could use assumed search frictions to generate differences in markets

- I use an auctions approach which has some nice properties:

- Perceived exploitative profit margins can be generated without assuming directly predatory markups

- Fewer entrants into the peripheral market lead to higher prices

- Firm technology determines interpretation of signal, where payday lenders have a weaker signal than banks

- The key separating condition is derived from moral repugnance

Model

Consumers have types defined by their market access and riskiness

with outside options

High-type consumers care about the brand reputation of a firm. For consumer k looking at firm i:

is a exploitation-aversion (repugnance tolerance or moral disutility) parameter that penalizes exploitation by the firm with heterogeneity at the individual level drawn from

and share

is an increasing and weakly convex function (some exploitation might be okay)

Model

Firms are indexed

Each firm observes a private signal about the transaction value:

The high market has many well-informed competitors while the low market has fewer firms and signals are weaker

Model

Firms observe the signal and submit a bid (rationally anticipating a winner's curse):

which accounts for winner's curse discount, which is increasing in the weakness of the signal and decreasing in the number of firms:

Model

The winner's curse discount:

gives a nice measure of perceived exploitation without assuming predatory behavior on behalf of the firms in the low market:

More firms reduces perceived exploitation while less informative signals increase it.

Note: I believe the model can accommodate additional perceived exploitation not owing solely to a winner's curse markup, but I have not proven this yet and it is possible it would require additional assumptions.

Model

The winner's curse discount:

also allows for some positive profit to banks in the primary market.

The firms in the high market then face a trade-off:

- Stay only in the high market

- Enter and participate in both markets (potentially losing some high-market consumers)

Note: I start under the assumption of a segmented market. I have not yet shown if my model primatives can accommodate starting there.

Model

The firm choice becomes to stay clean:

And lose some share of consumers who would find their entry into the low market to be repugnant, determined by

Or to enter into the low market and extract a share of the premium using the better assessment technology:

Model

Model predictions:

- The clean firm will only enter the peripheral market if the gains to doing so will outweigh the loss from consumers who find it repugnant

- A high enough perceived risk of losing those customers will keep the markets separate

- Markets remaining separate means:

- Competitive costs for high-type consumers

- Much higher costs to the low-type consumers, even with respect to their true riskiness type

Model

Things currently not addressed:

- Additional profit margin not explained by risk / winner's curse

- General equilibrium outcomes and asymmetric winner's curse

- Existing goodwill or heterogeneous repugnance by firm type (e.g. credit unions)

- Adverse selection concerns in the low-market

- Policy changes that set a max annual interest rate

Data and Policy Changes

- Use empirical data to show that there is a segmented market with a discontinuity in the riskiness profile

- Data limitations that would need to be overcome include the availability of information on:

- Loans from traditional banks (especially US Bank or Credit Unions that offer small-dollar loans)

- Payday loans (public filing in some states might help)

- Policy changes can validate model predictions, especially if data is available in states with:

- Recent cap limits (Illinois, Minnesota)

- Structural changes (Ohio)

Experiment

An ideal experiment would answer:

- Do people see extremely high prices for some people (e.g. payday lending) as exploitative / repugnant? Does the source of the high prices matter?

- Do they respond and punish as a result?

- Can we identify the approximate shape of ?

- Do firms identify and respond to the trade-off, maintaining the segmented market?

Experiment

Possible design 1:

- Simple trade-off between price and supporting a firm that charges much higher prices to others

- Easy to design, implement, and understand

- We already have some evidence that firm ethics matter to some degree and people will consider that in their prices

Experiment

Possible design 2:

- A full market trading design the mirrors the model setup

- Sellers choose market entry

- Buyers have real, exogenous risk profiles and market access

- Trade over many rounds, observing market entry and prices

- Vary price setting by treatment

- Exogenously imposed to capture observed rates and profitability

- Set by firms in response to signal and signal strength

- Much more complicated, and learning the winner's curse is slow / incomplete

Timeline

- Summer 2026:

- Data feasibility and experimental design

- Brown bag and feedback

- Fall 2026:

- Continued feedback, second brown bag

- Data collection

- Winter / Spring 2027:

- All data, initial results

- Weak draft ready and present for feedback

- Summer 2027: outside conferences and draft online

- Fall 2027: finished product with lots of input