By

The

Numbers

Benchmarking Progress Toward Financial Inclusion

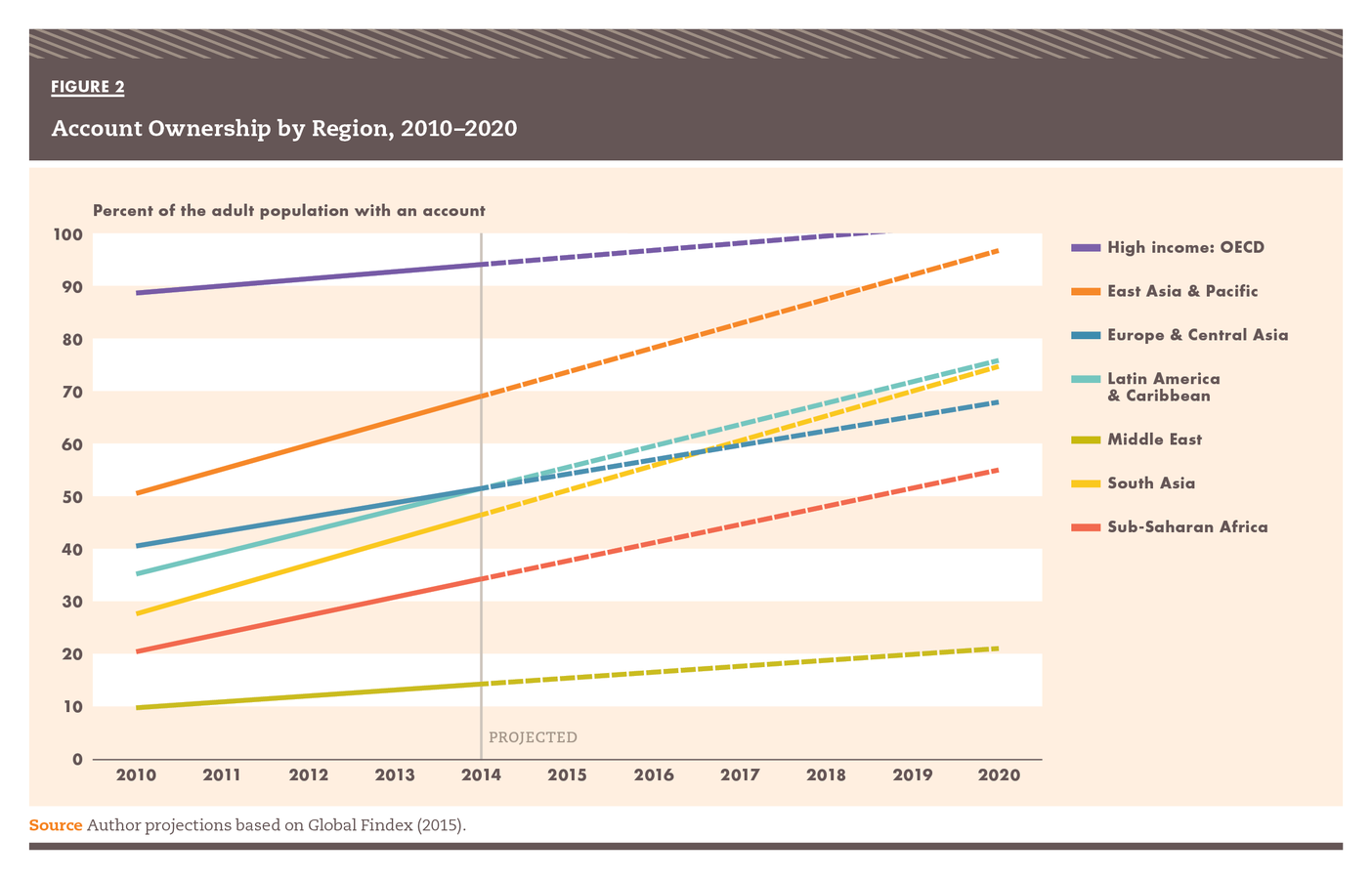

The world – every region, income level, and “slice” of the global population – is moving toward greater financial access.

But some regions are growing faster than others.

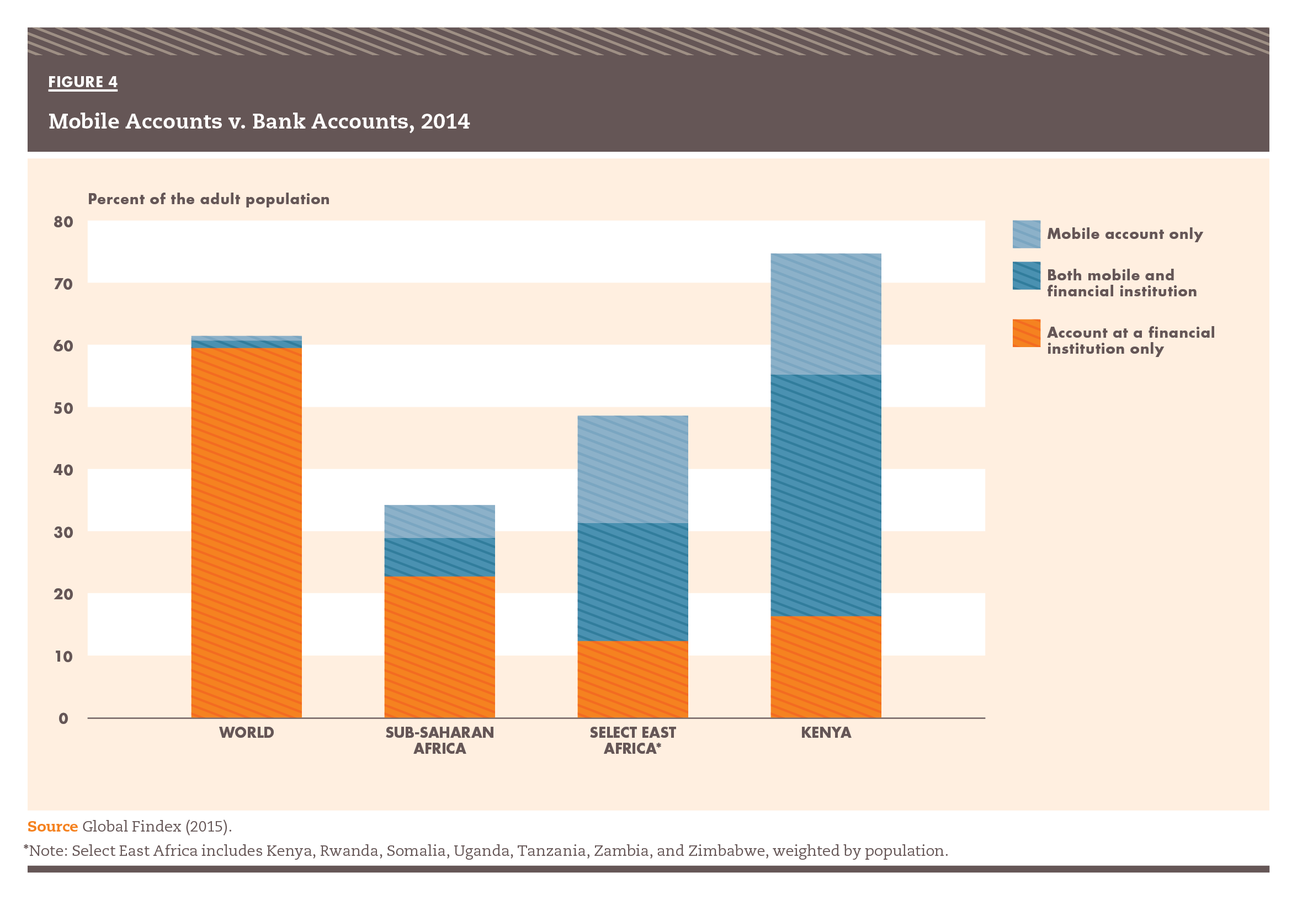

The mobile phone is a big story in Africa, especially East Africa, but not elsewhere.

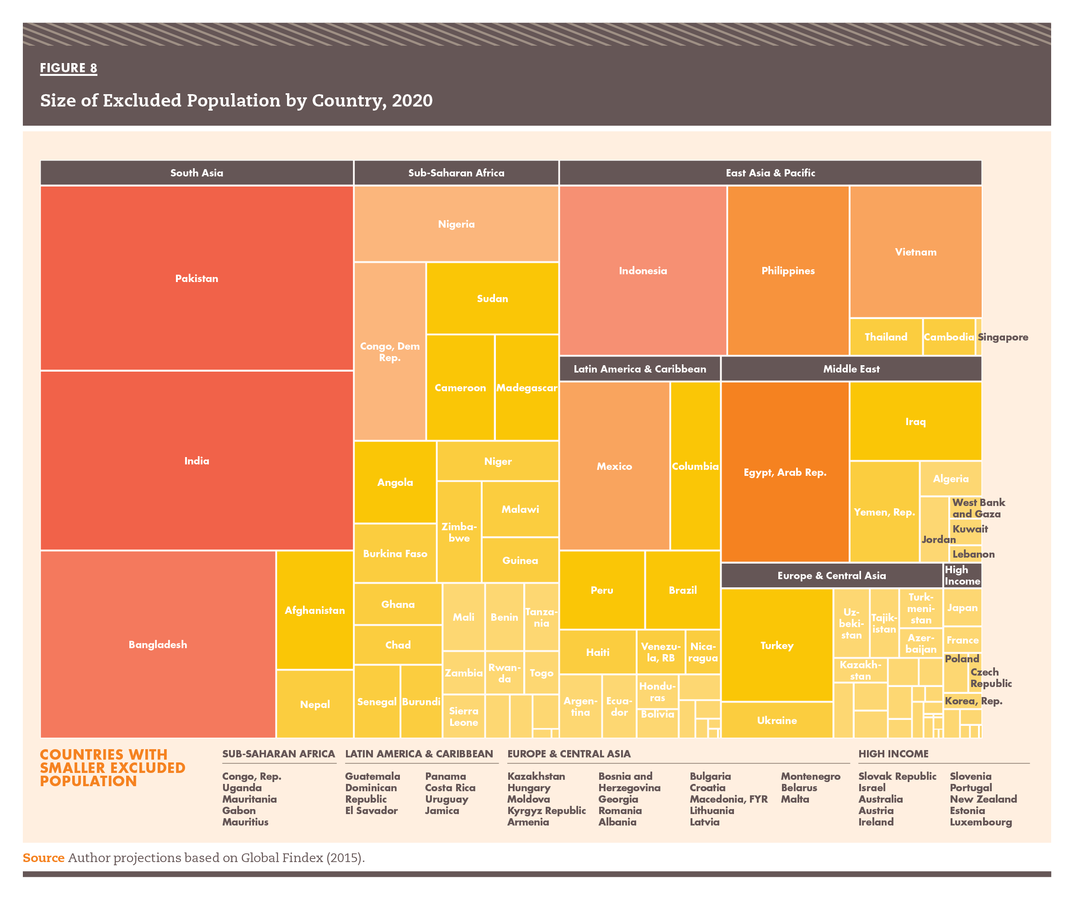

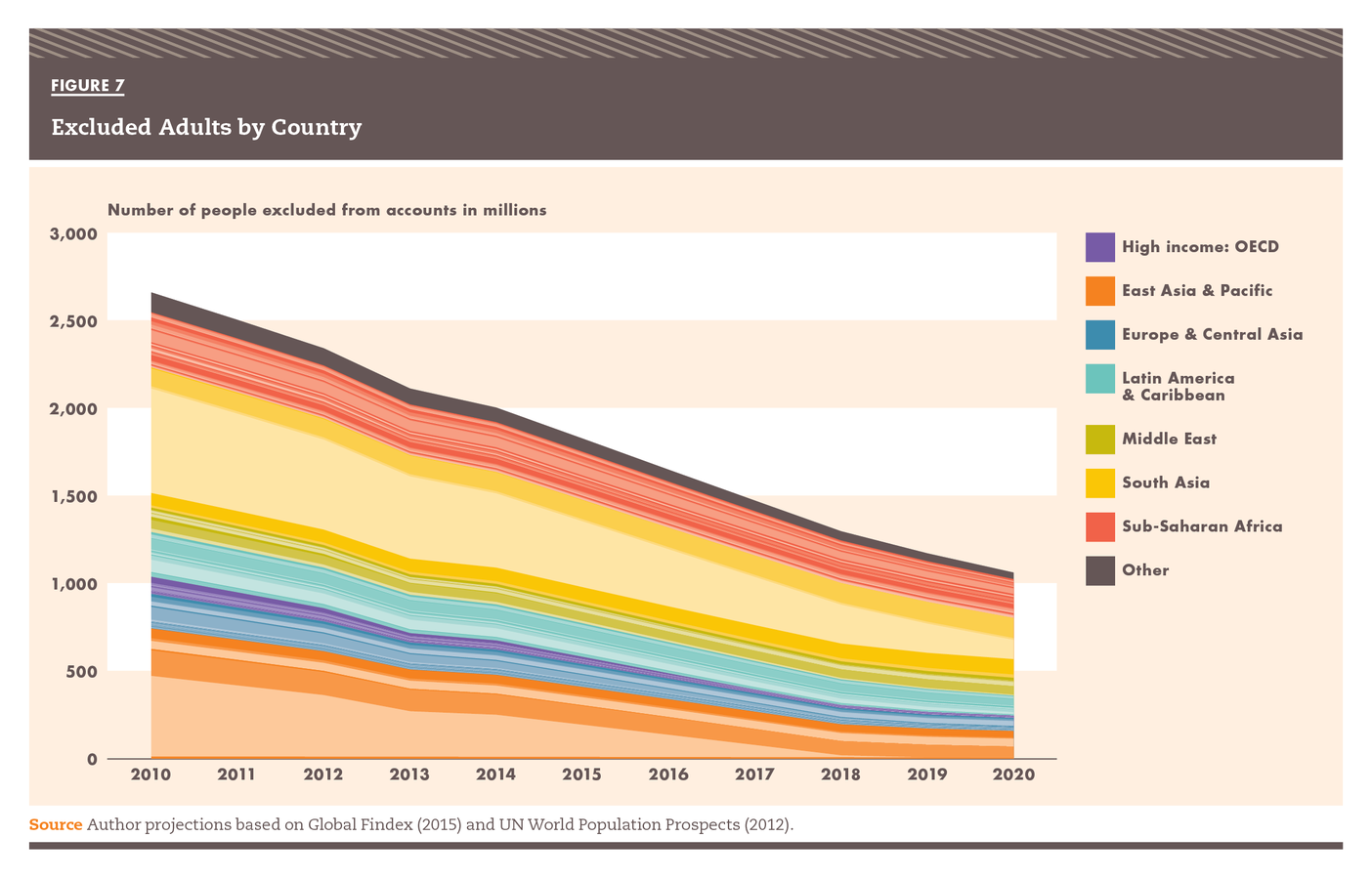

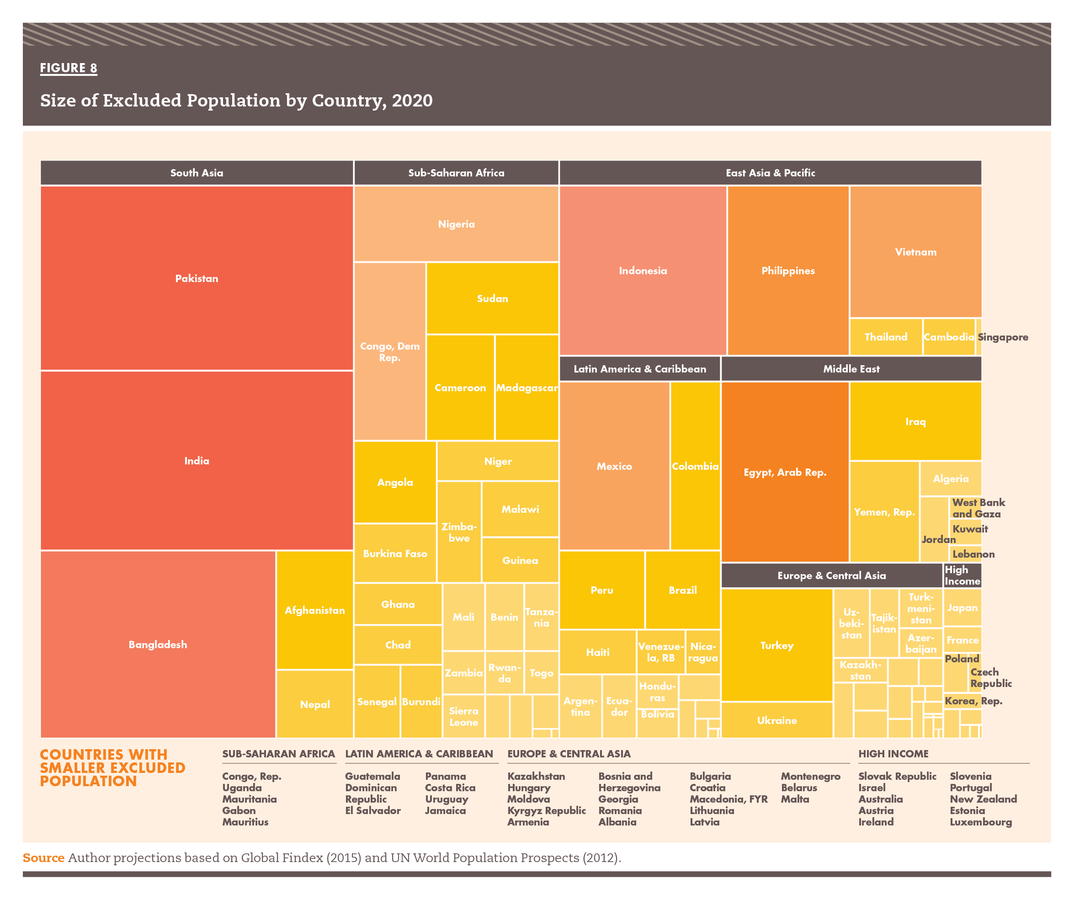

In absolute numbers of excluded, India and China dominate today, but by 2020 remaining exclusion will be broadly distributed among many countries.

As universal access approaches, addressing remaining exclusion will require attention to every country.

As large international organizations and foundations commit to ushering in financial inclusion in a select larger and more critical countries, smaller and harder to reach countries may be left behind. With current trends, exclusion in 2020 may not be largely dominated by countries like China and India, but spread broadly across the world.

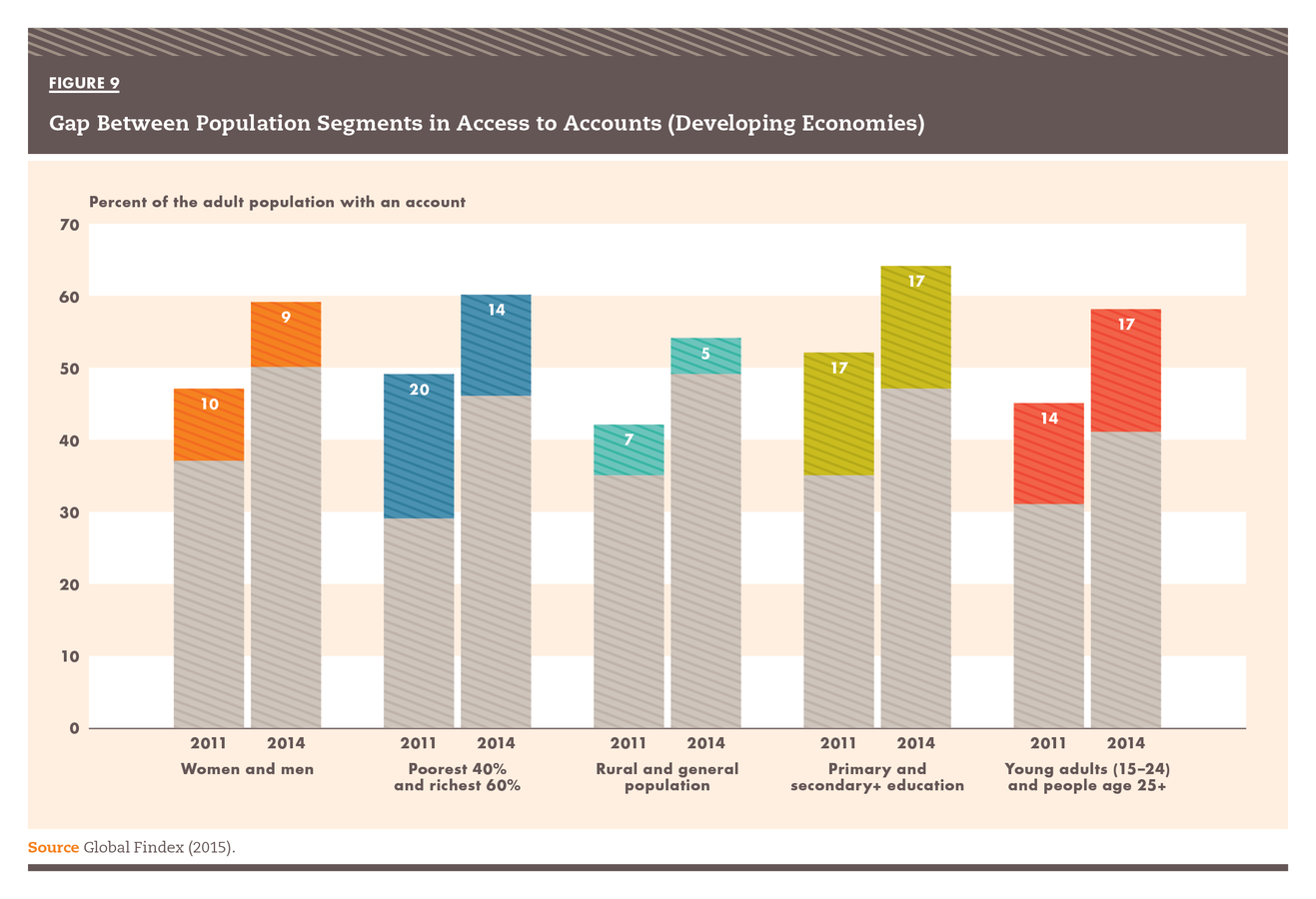

The more-excluded population segments are gaining, but access gaps persist.

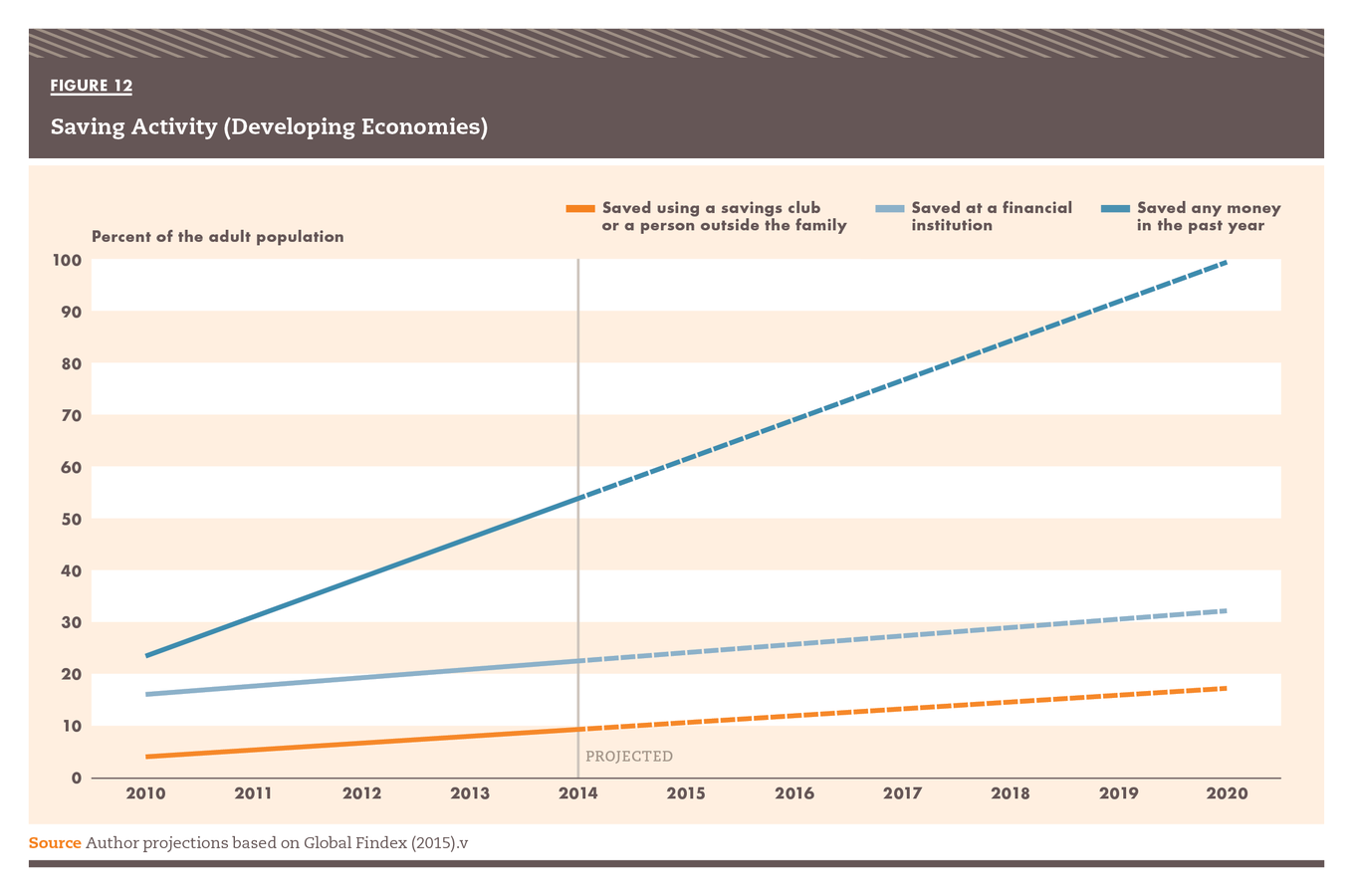

Saving is increasing fast, but not so much in financial institutions.

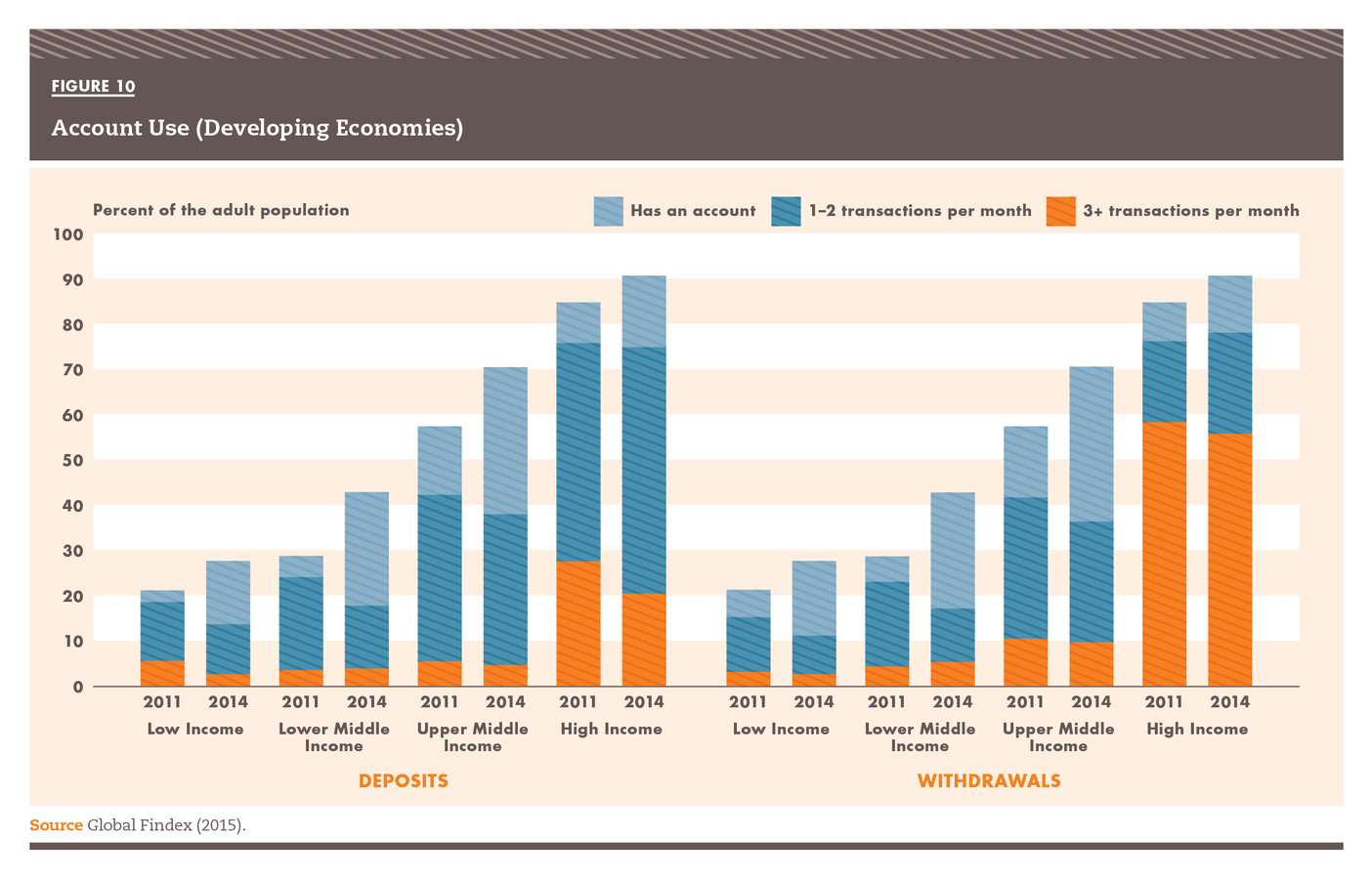

Account access has grown, but usage lags.

What are people doing with their accounts?

Borrowers use multiple sources, both informal and formal.

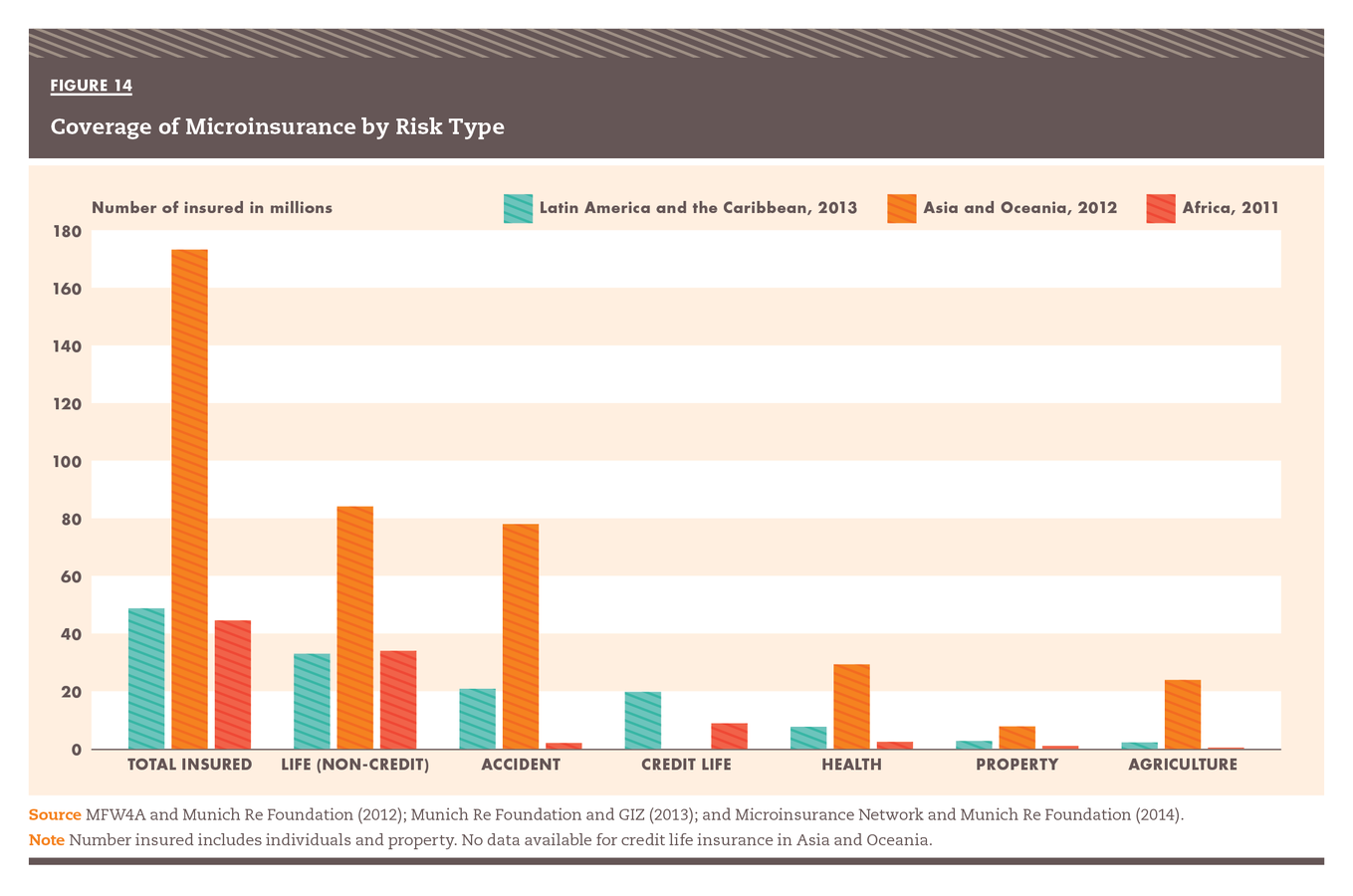

While the total number of people with microinsurance is significant, distribution across the world is highly skewed.

Progress on inclusion requires building and maintaining an enabling ecosystem including policy, regulation, and industry infrastructure.

In recent years the world has made strides on technology change, solidified government commitment and action, and increased quality and use of public goods like credit reporting systems, physical infrastructure, and digital infrastructure. These improvements increase both access and ease of use of financial services.

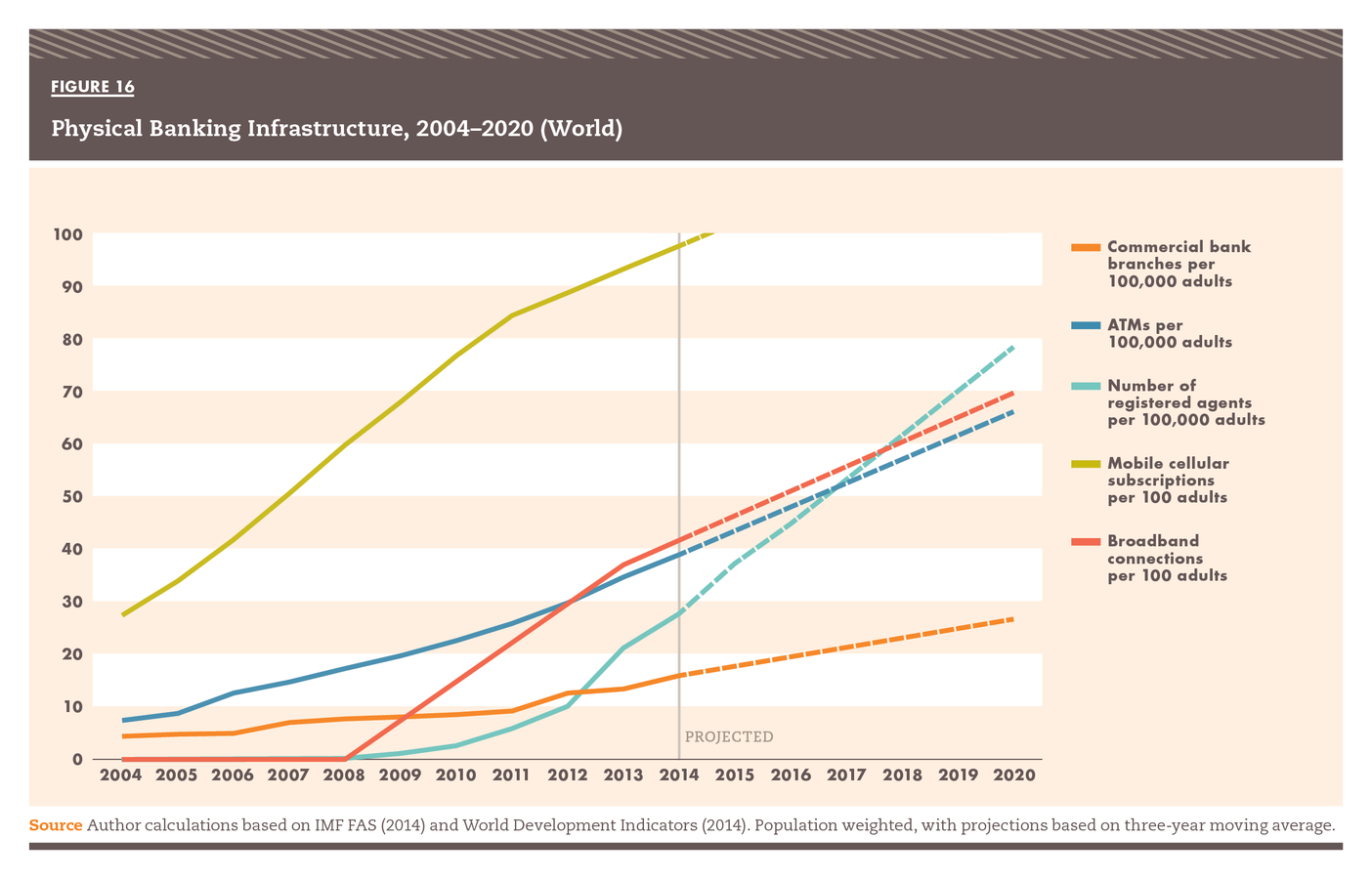

Mobile phones, ATMs, agents, and bank branches are rapidly moving the world toward ubiquitous access.

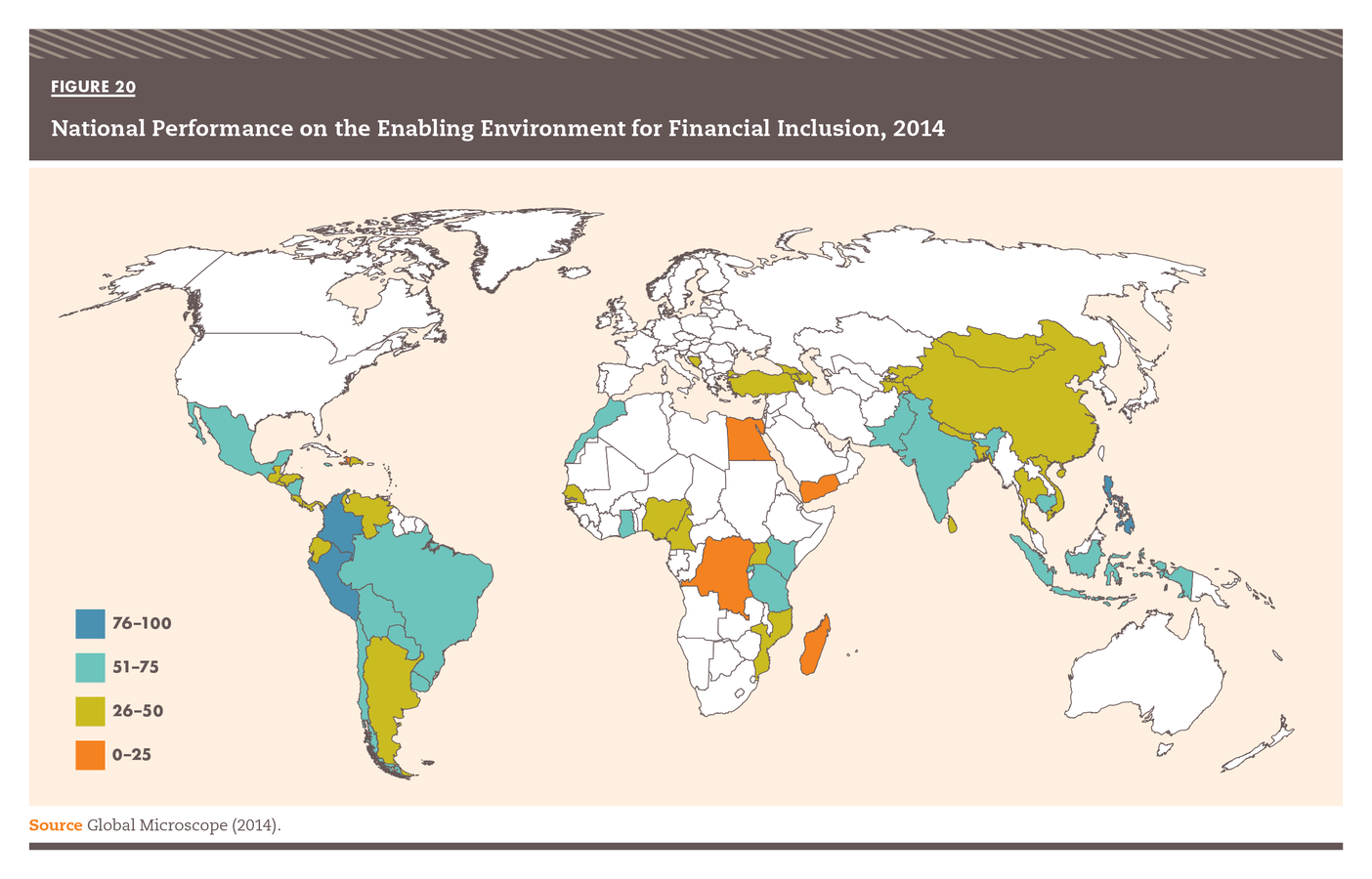

Policy performance across the world ranges from excellent to very poor.

This map shows scores from the 2014 Microscope. A higher score indicates higher inclusiveness of a county’s financial sector by considering best practices in the national regulatory environment and institutional support in the safe provision of a wider range of financial products and services to low income populations.

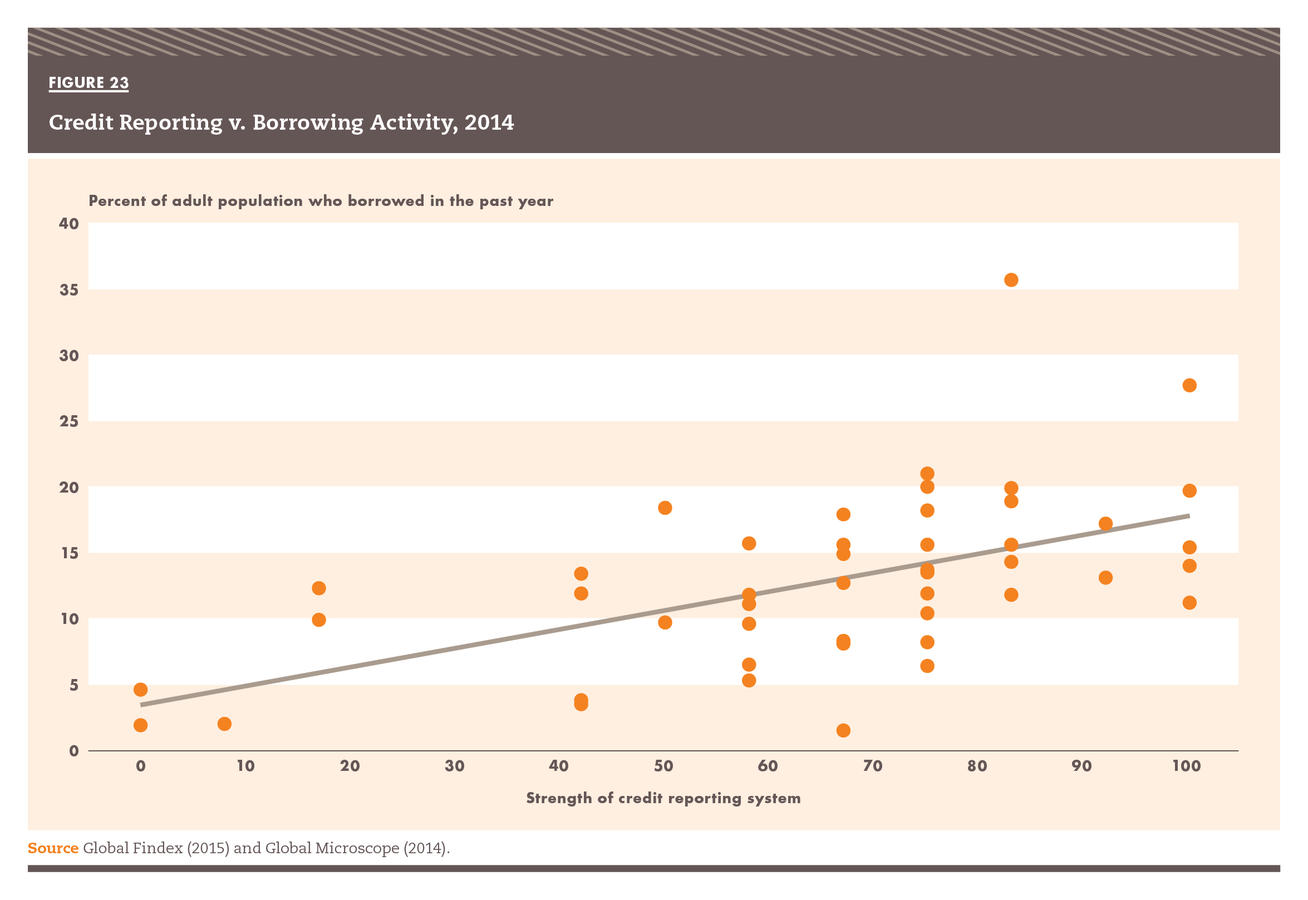

Where effective credit reporting exists, more people borrow.

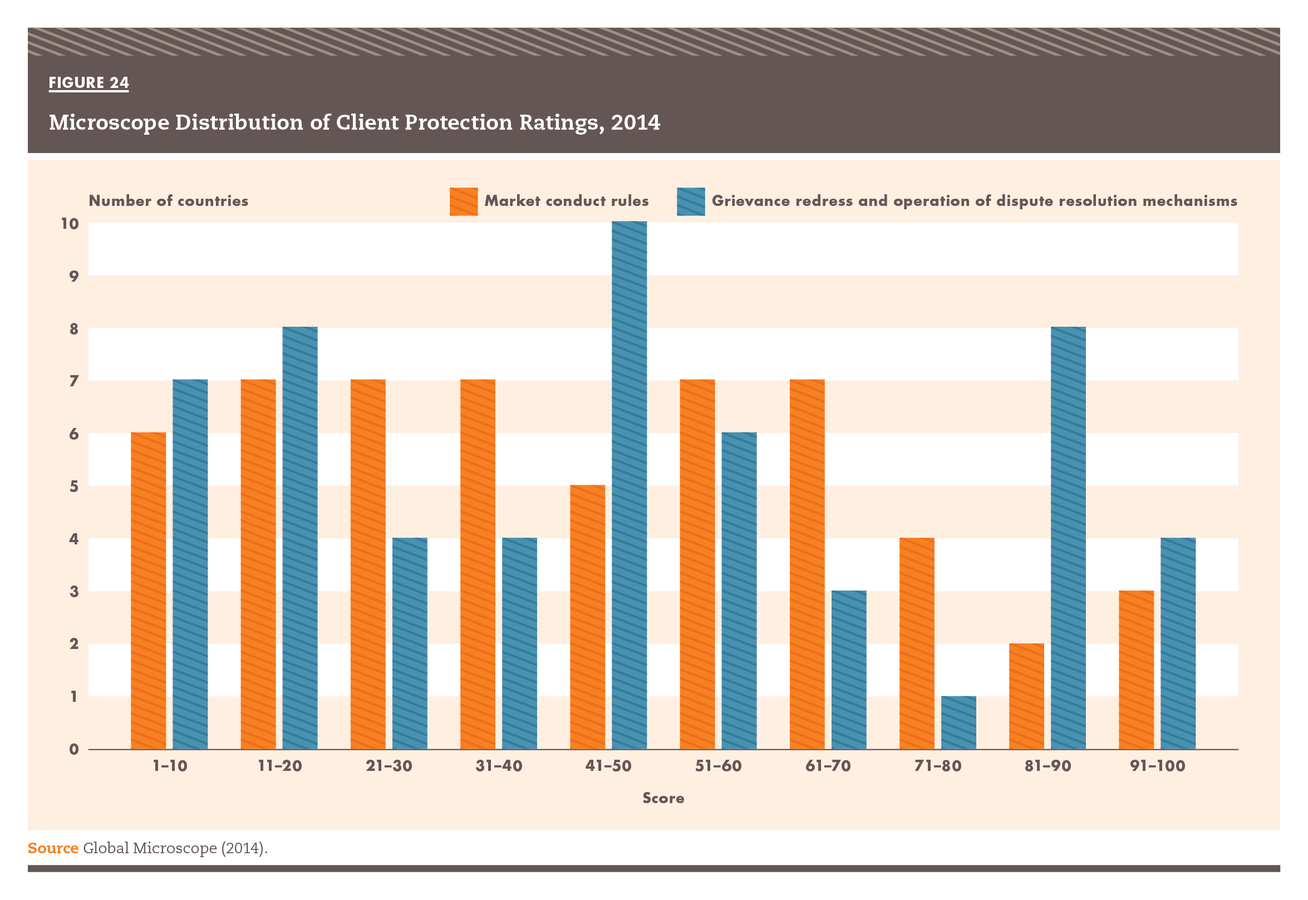

Consumer protection regulation ranges from extremely weak to quite comprehensive.

Client protection has gained traction, especially since the global financial crisis, both from national governments and from portions of the financial inclusion industry. However, building an effective client protection infrastructure takes time, and many countries have started from a low base. When the EIU rated regulatory frameworks for client protection as part of the Global Microscope, it found a broad distribution of performance as seen here.

Universal financial access is just a first step toward full financial inclusion.

According to CFI, financial inclusion is a state in which everyone who can use them has access to a range of quality financial services at affordable prices, with convenience, dignity, and consumer protection, delivered by a range of providers in a stable, competitive market to financially capable clients

The purpose of promoting financial inclusion is to enable people to use financial services to better manage their lives.

A fully included person is an active user of quality financial services that bring significant value to their lives.

Progress on access to an account must be accompanied by further efforts to achieve deeper inclusion.

Our hope is that this report provokes further questions.

Which regions are advancing faster than others and why?

Which countries are moving quickly, slowly, or not at all?

How significant is the contribution of mobile phones to increasing account access?

Who will still be excluded in 2020, and where will they be located?

How can the push to financial inclusion retain a focus on quality and value for the customer?

The Center for Financial Inclusion is grateful for the generous support we have received from our founding partner, Credit Suisse, in support of By the Numbers, a project of Financial Inclusion 2020.

For the full report, visit www.centerforfinancialinclusion.org/bythenumbers