Externalities

Christopher Makler

Stanford University Department of Economics

Econ 50: Lecture 22

pollev.com/chrismakler

What color shirt am I wearing?

Reminder: A's and A+'s

The cutoff for an A really is 95. This is because I essentially give you 100 points for 1/3 of your grade if you do the homeworks and come to class; so to earn an A in the class, you need a 93 or above on the exam portion.

There is no cutoff for an A+, but I will give out a limited number of A+'s. The way to earn an A+ is to submit a question for Exercise 9.1 on the homework. A+ grades will be given to people who are both at the top end of the grade distribution and demonstrate the nuance of their knowledge through writing an incisive exam problem.

Public Economics

Climate change is an equilibrium phenomenon.

Inequality is an equilibrium phenomenon.

Housing is an equilibrium phenomenon.

Health is an equilibrium phenomenon.

For 8 weeks, we have studied

the gravitational forces that drew systems towards equilibrium, and kept them there.

To what end, if not to find

a way to a better equilibrium?

Public Economics

Some goods are underprovided or overprovided in equilibrium.

Some goods will never be provided in equilibrium

Market equilibria occur when all agents try to maximize their own utility/profit/payoff.

These are known as market failures.

The field of public economics studies how public policy

can (usually partially) correct those failures.

EXTERNALITIES

(TODAY)

PUBLIC GOODS

(AFTER THANKSGIVING)

Externalities

- Situations in which the actions of agents affect the payoffs of others

- Often caused by "missing markets"

- Markets (or more generally, everyone acting in their own self interest) will not generally solve the problems — equilibria are inefficient or inequitable

Externalities

- Market Externalities

- Lots of buyers and sellers

- The overall quantity of the good produced has an external cost

- Individual Exernalities

- Two agents

- One agent's actions affects the other

Externalities

- Market Externalities

- Lots of buyers and sellers

- The overall quantity of the good produced has an external cost

- Individual Exernalities

- Two agents

- One agent's actions affects the other

Not as much a "one size fits all" model,

but more of an approach:

- identify a "social welfare function" that tell us what the "socially optimal" outcome is

- model the incentives agents face, and understand why the "market equilibrium" outcome differs from the "socially optimal" one.

- try to find a way to adjust the incentives to achieve the socially optimal outcome

- usually involves getting the agents to internalize the externality they are causing others

Market Externalities

What happens when there are too many people to contract?

Pigovian tax:

Internalize the externality so that private marginal cost equals social marginal cost.

Competitive equilibrium:

consumers set \(P = MB\),

producers set \(P = PMC \Rightarrow MB = PMC\)

With a tax: consumers set \(P = MB\),

producers set \(P - t = PMC\)

Problems and Complications

- What if not all firms generate the same externality?

- Some firms will be overtaxed, others undertaxed

- No incentive to switch to less polluting production processes

- Better solution, if possible: measure and tax the externality itself

(tax on pollution/emissions), not the good that generates it as a byproduct- Carbon tax vs. steel tax

- Tradeable pollution quotas ("cap and trade") incentivize cost minimization and innovation

Q: Makler, what do you think about taxes?

A:

It depends. What model are we in?

Individual Externalities

Individual Externalities

- Individuals solving their own optimization problem

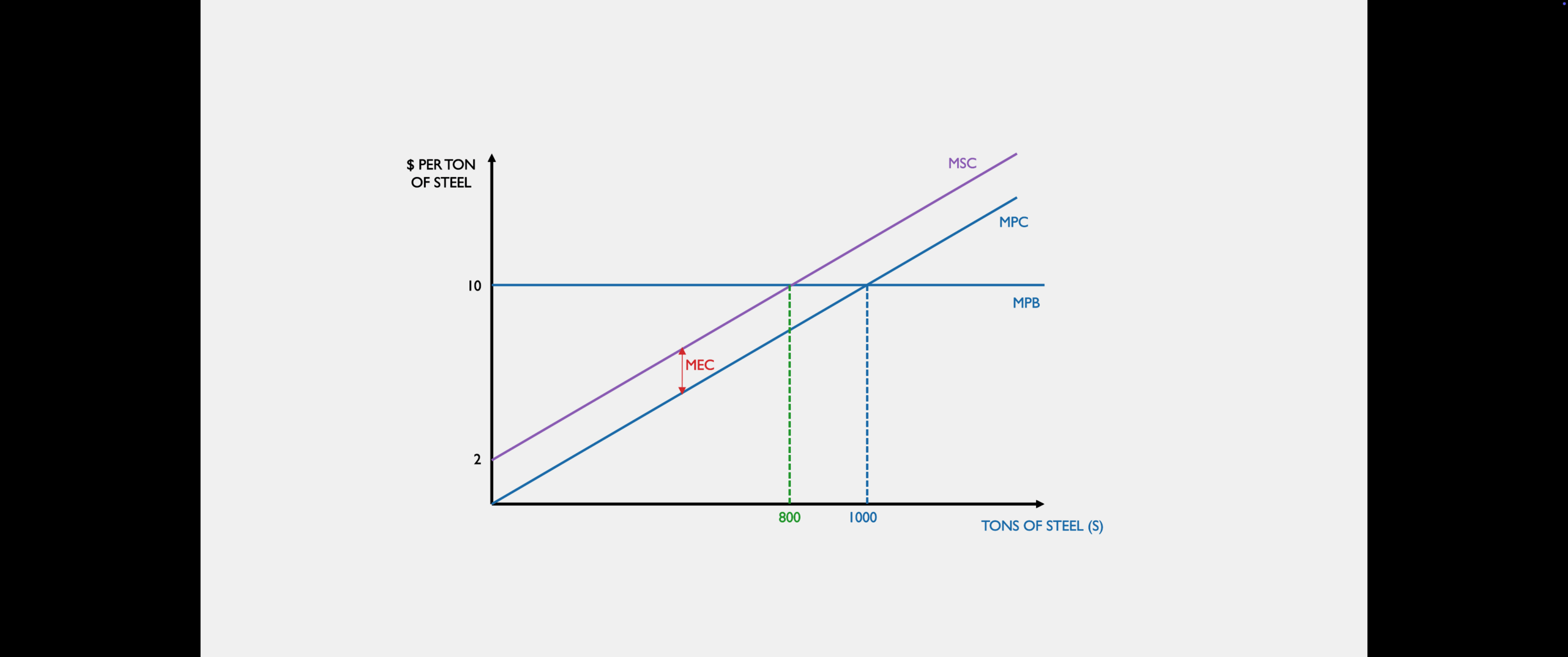

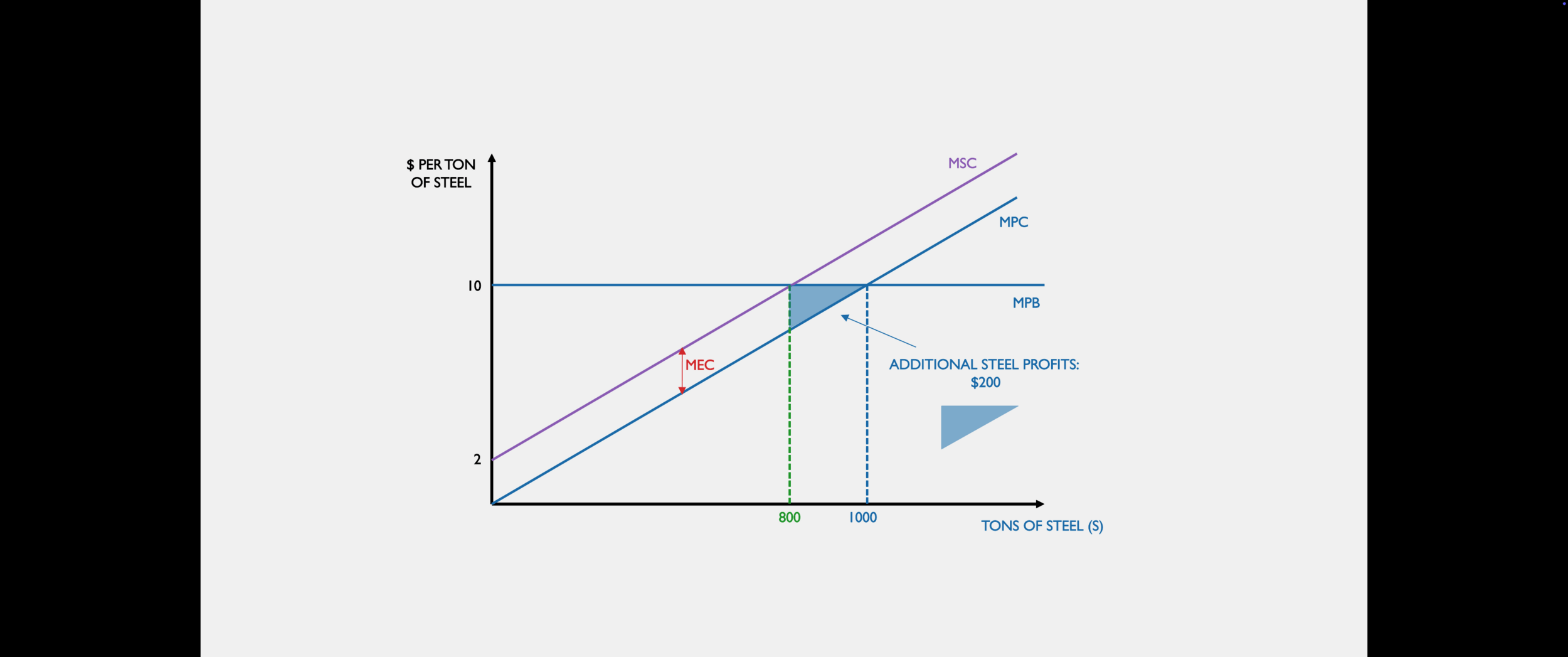

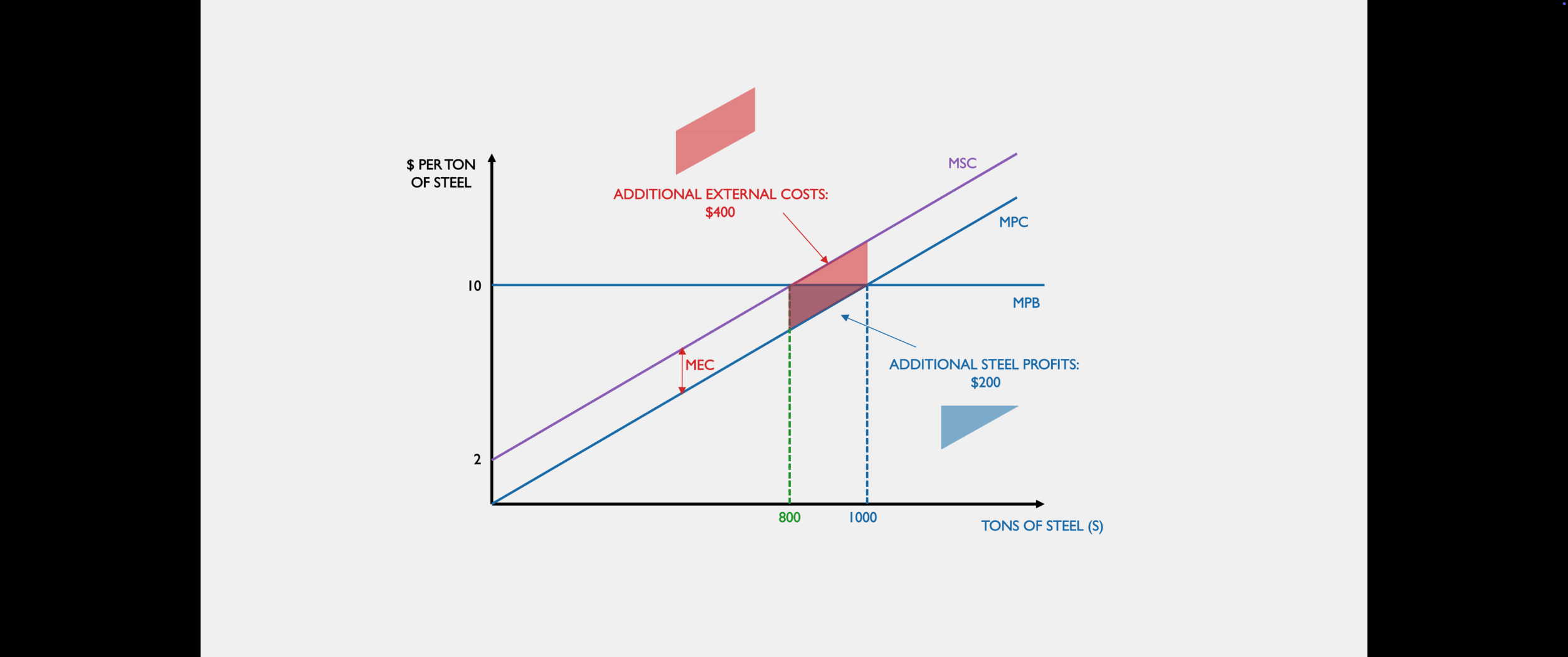

disregard the external effects they have on others - Marginal social cost (MSC) = marginal private cost (MPC) + marginal external cost (MEC)

- Market equilibrium will occur where MB = MPC

- Social optimum is where MB = SMC

Note: I'm trying to switch from "private marginal cost (PMC)" and "social marginal cost (SMC)" to "marginal private cost (MPC)" and "marginal social cost (MSC)" ... in the meantime I'm super inconsistent. You can use either, and you'll see both used in this presentation.

Steel Mill and Fishery

Base Model: Profit Maximization

Extension: Production choices affect other's profit

Conflict: Steel mill only takes into account its own cost,

not impact on the fishery.

Who does better under each scenario?

Which scenario is overall more profitable?

How can we get the steel mill to produce the socially optimal amount?

- Government solutions

(imposed by a third party) - Negotiated solutions

(achieved by the agents themselves)

[ GOVERNMENT SOLUTIONS ]

Policy I: Direct regulation

Dictate that the firm must produce

exactly 800 units of steel.

- Good if the government knows exactly how much is optimal

- Not so good otherwise

[ GOVERNMENT SOLUTIONS ]

Policy II: Impose a "Pigovian tax" equal to the amount of the negative externality.

- Good if the government knows exactly how much damage producing steel occurs

- Not so good otherwise

[ PRIVATE SOLUTIONS ]

Ronald Coase's insight: we can achieve the optimal quantity via negotiation if we assign property rights to the firms.

- Give the steel mill the "right to pollute" and let the fishery pay them to not pollute.

- Give the fishery the "right to clean water" and let the steel mill pay them to pollute.

Coase Theorem

Absent "transaction costs,"

private bargaining reaches the efficient outcome,

for any allocation of initial property rights.

Possible "transaction costs"

Costs of measuring/contracting on the relevant externalities

Incentives for each agent to pretend that the costs are greater than they are

Lawyers' fees

Monitoring

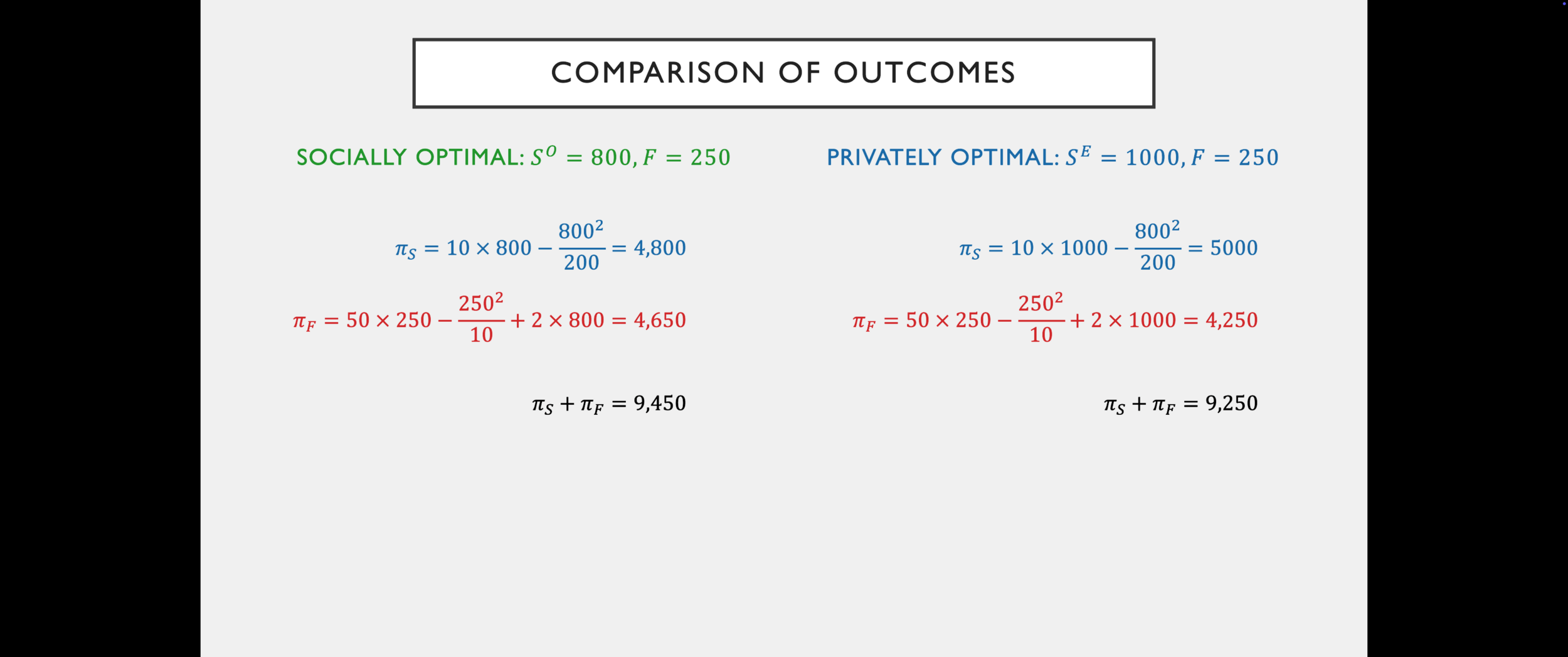

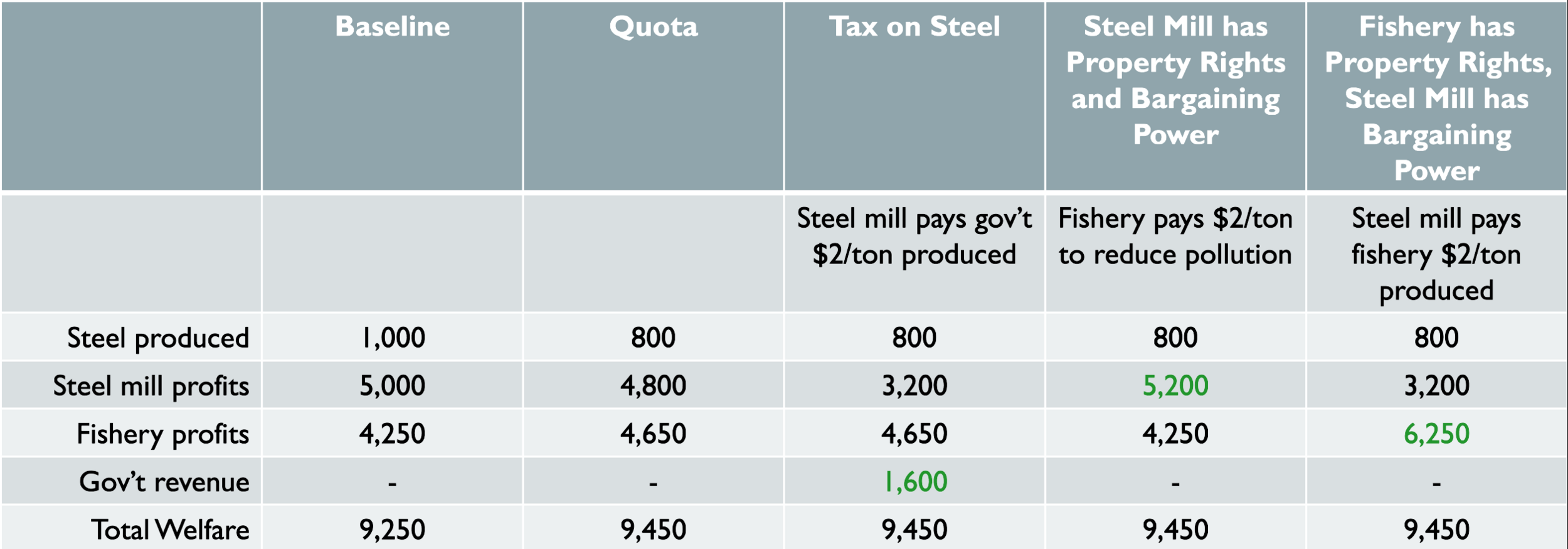

Comparison of outcomes

The allocation of property rights doesn't affect the amount of steel produced...

but it does determine winners and losers!

Conclusion: Externalities

In the presence of externalities, personal decisions affect others.

If everyone just balances their own personal marginal benefits and costs,

it can have a negative (or positive) external effect on others.

Markets will not, in general, result in an efficient outcome on their own —

there is a role for government intervention.

Broader conclusions: markets don't always result in the optimal result;

but understanding the market mechanism can allow you

to shape public policy that gets closer.

In certain cases, it's possible that private (non-government) solutions can also achieve an efficient outcome.