Intertemporal Choice

Christopher Makler

Stanford University Department of Economics

Econ 51: Lecture 3

Today's Agenda

Part 1: Baseline Case

Part 2: Extensions and Applications

Modeling present-future tradeoffs

The intertemporal budget constraint

Preferences over time

Optimal saving and borrowing

Different interest rates for borrowing and saving

Credit constraints

Real and nominal interest rates

Beyond two time periods

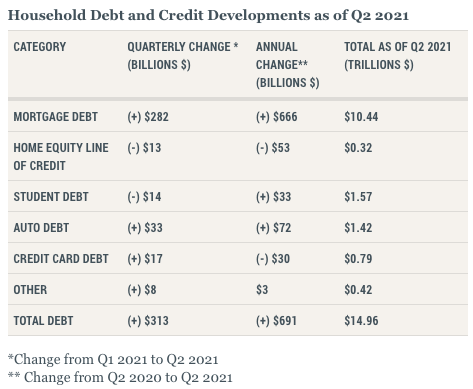

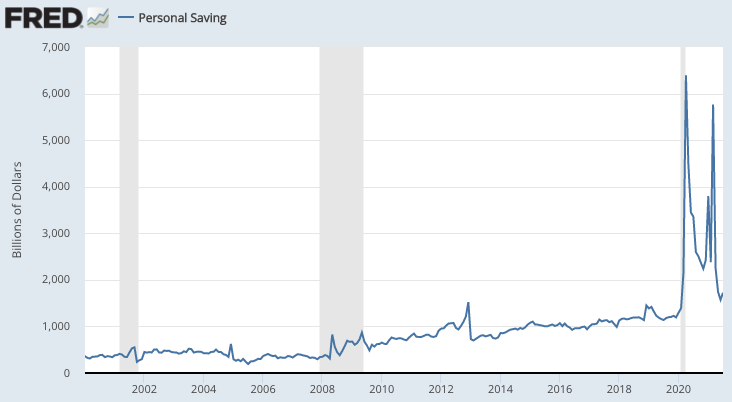

Saving and borrowing is a huge part of the U.S. economy.

Endowment of time and money.

Today: Present vs. Future Consumption

Endowment of money in different time periods (an "income stream")

Last time: Leisure vs. Consumption

Working = trading time for money

Saving = trading present consumption for future consumption

Borrowing = trading future consumption for present consumption

For Each Context:

Determine the budget line

Analyze preferences

Solve for optimal choice

Comparative statics: analyze net supply and demand

Do you have to spend all the money you earn in the period when you earn it?

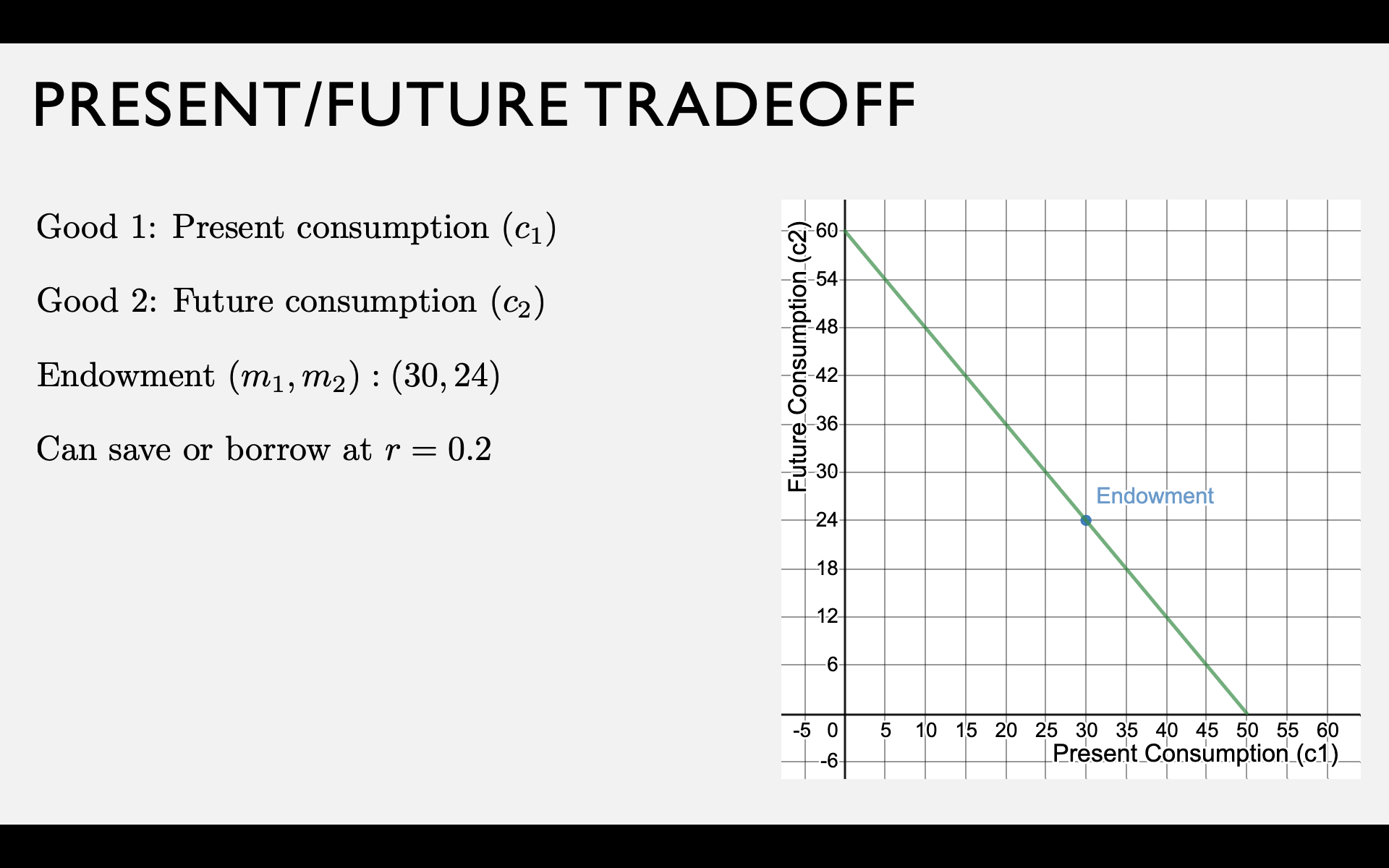

Present-Future Tradeoff

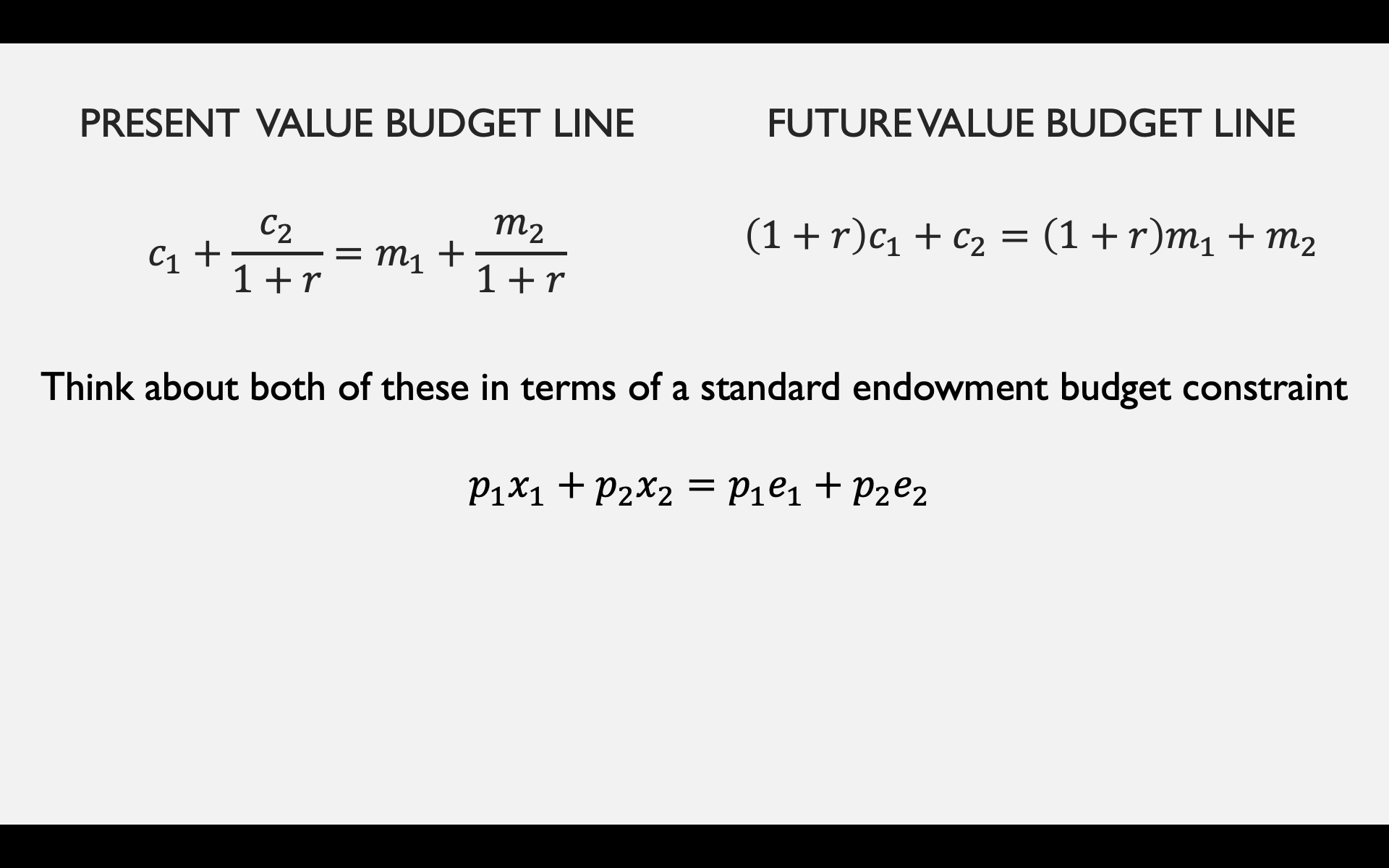

Your endowment is an income stream of \(m_1\) dollars now and \(m_2\) dollars in the future.

What happens if you don't consume all \(m_1\) of your present income?

Two "goods" are present consumption \(c_1\) and future consumption \(c_2\).

Let \(s = m_1 - c_1\) be the amount you save.

Saving and Borrowing with Interest

If you save at interest rate \(r\),

for each dollar you save today,

you get \(1 + r\) dollars in the future.

You can either save some of your current income, or borrow against your future income.

If you borrow at interest rate \(r\),

for each dollar you borrow today,

you have to repay \(1 + r\) dollars in the future.

"Future Value"

"Present Value"

pollev.com/chrismakler

Preferences over Time

Examples:

When to borrow and save?

Save if MRS at endowment < \(1 + r\)

Borrow if MRS at endowment > \(1 + r\)

(high interest rates or low MRS)

(low interest rates or high MRS)

If we assume \(v(c)\) exhibits diminishing marginal utility:

MRS is higher if you have less money today (\(m_1\) is low)

and/or more money tomorrow (\(m_2\) is high)

MRS is lower if you are more patient (\(\beta\) is high)

Borrow or Save?

pollev.com/chrismakler

Optimal Bundle

Tangency condition:

Budget line:

pollev.com/chrismakler

Supply of Savings and

Demand for Borrowing

In general, net demand is \(x_1^* - e_1\)

In this context, net demand is the demand for borrowing.

If it's negative, then it's the supply of saving.

Different Buying and Selling Prices

BUY MORE GOOD 1

BUY LESS GOOD 1

Sell good 1 and buy good 2 if your MRS at the endowment is less than the price ratio to sell good 1 / buy more good 2.

Either way, it all comes down to the relationship between your MRS at the endowment and the relevant price ratios.

Buy good 1 and sell good 2 if your MRS at the endowment is greater than the price ratio to buy more good 1 / sell good 2

Different Interest Rates

When a Budget Line Ends...

Inflation and Real Interest Rates

"Present Value" for two periods

"Present Value" for three periods

Why stop at two periods?

Net Present Value

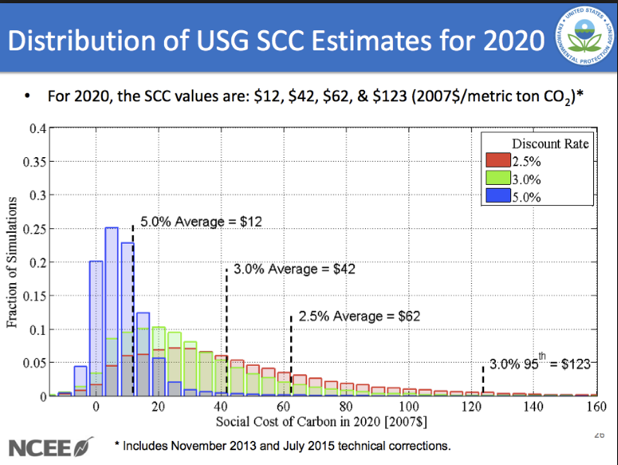

Application: Social Cost of Carbon

Obama Admin: $45

Uses a 3% discount rate; includes global costs

Trump Admin: less than $6

Uses a 7% discount rate; only includes American costs

PV of $1 Trillion in 2100:

$86B for Obama, $4B for Trump