Debt Instruments

Government bonds and Corporate bonds

Learning Outcome

5

Analyse which bond is suitable for different investors.

4

Understand the role of credit ratings and regulations.

3

Compare bonds based on risk, return, and liquidity.

2

Identify the key features of both types of bonds.

1

Understand the meaning of government and corporate bonds.

What is a Government Bond?

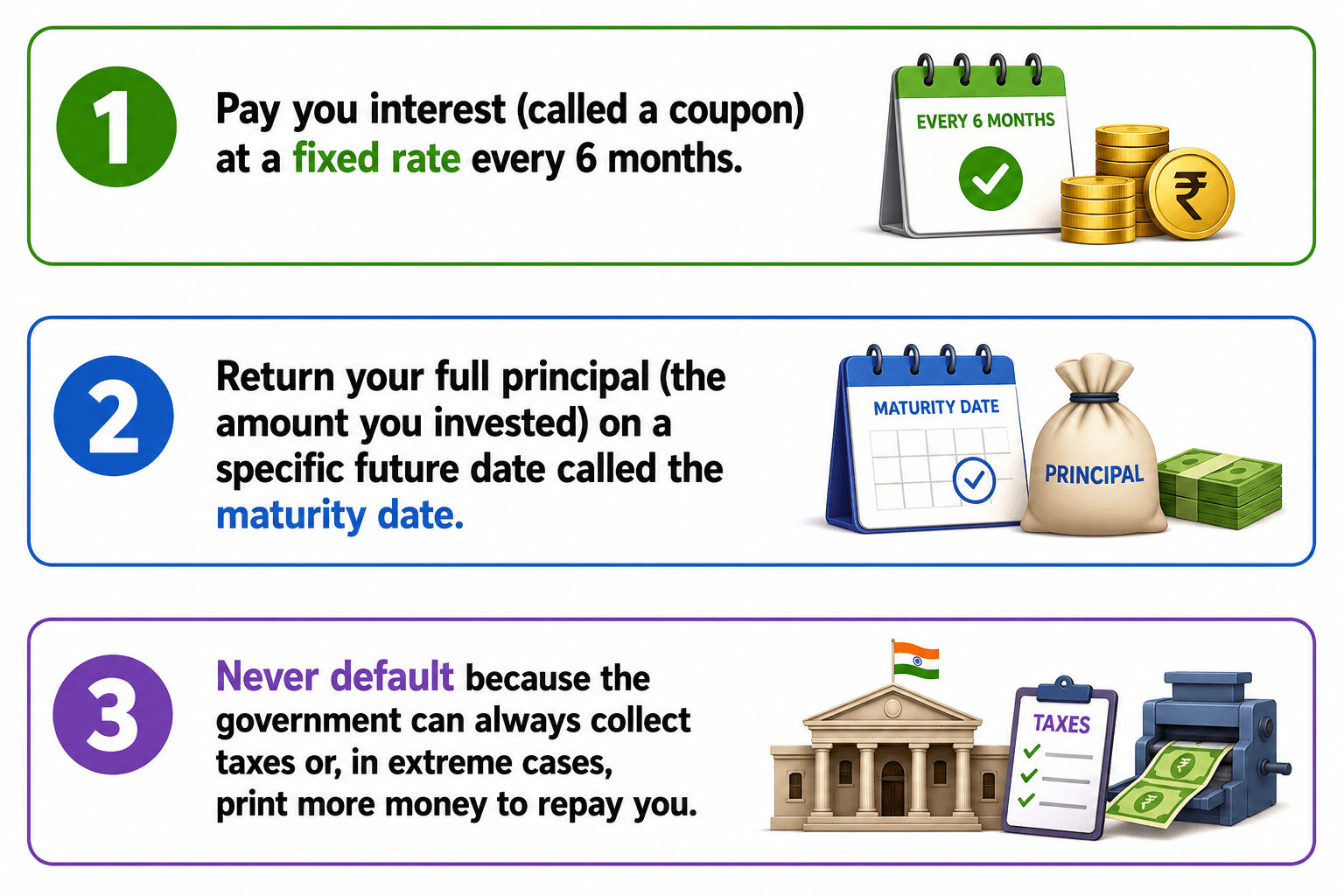

A Government Bond is a loan you give to the Government of India (or a state government). In exchange, the government promises to:

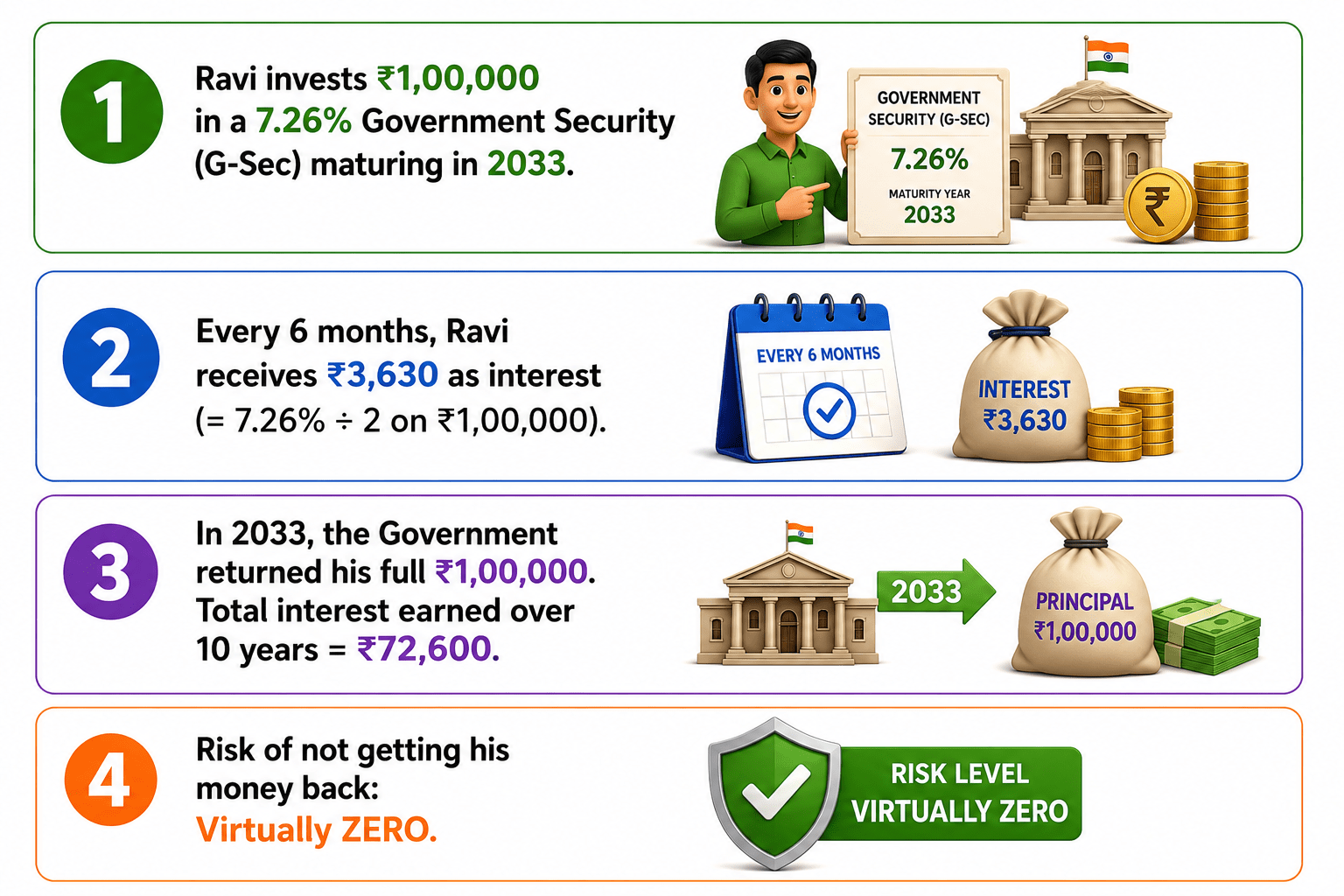

Eg- Ravi invests ₹1,00,000 in a 7.26% Government Security (G-Sec) maturing in 2033.

Every 6 months, Ravi receives ₹3,630 as interest

(= 7.26% ÷ 2 on ₹1,00,000).

In 2033, the Government returned his full ₹1,00,000. Total interest earned over 10 years = ₹72,600.

Risk of not getting his money back: Virtually ZERO.

Types of Government Bonds in India

1. G-Secs (Government Securities)- Long-term bonds issued by the Central Government. The most common type. Maturities from 5 to 40 years. Pays interest twice a year.

2. T-Bills (Treasury Bills)- Short-term borrowing by the government. Lasts only 91, 182, or 364 days. No interest payments — you buy at a discount and get full face value back. Example: Buy at ₹97,000, get ₹1,00,000 back in 91 days.

3. State Dev. Loans (SDLs) - Same as G-Secs but issued by state governments (Maharashtra, Gujarat, etc.) instead of the Central Government. Slightly higher interest than G-Secs.

4. Inflation-Linked Bonds- Special bonds where your interest and principal grow with inflation. Protects your purchasing power. Ideal for long-term investors worried about rising prices.

5. RBI Floating Rate Bonds- Interest rate changes every 6 months based on small savings rates. Good when interest rates are rising.

6. Sovereign Green Bonds- Government bonds where money is used only for green/environment projects like solar energy or clean water. Launched in India in 2023.

What is a Corporate Bond?

A Corporate Bond is a loan you give to a company. In exchange, the company promises to:

-

Pay you interest (coupon) at a fixed rate usually higher than a government bond.

-

Return your principal at the maturity date.

-

But here’s the key difference, the company may fail. If it goes bankrupt, you may lose some or all of your money.

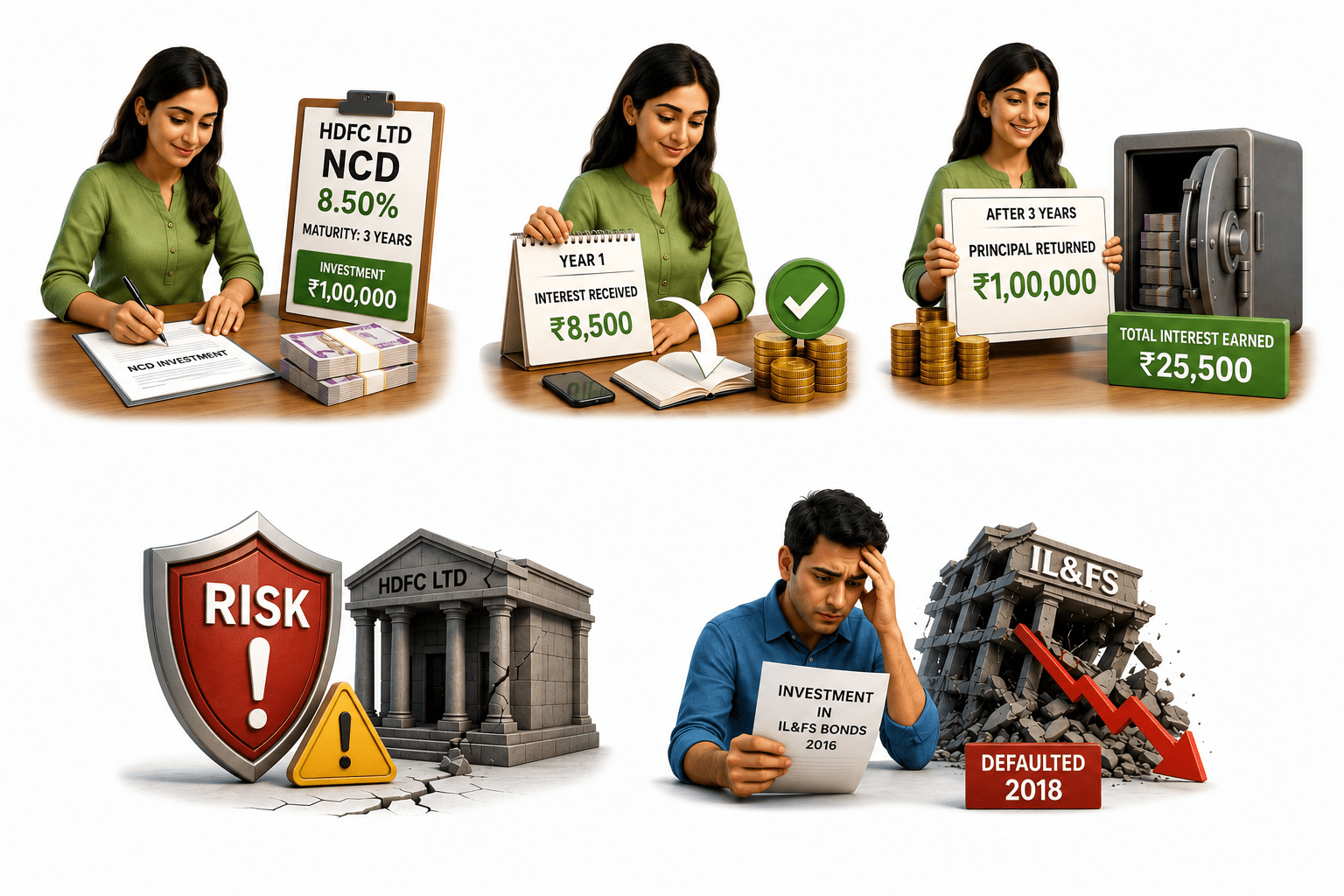

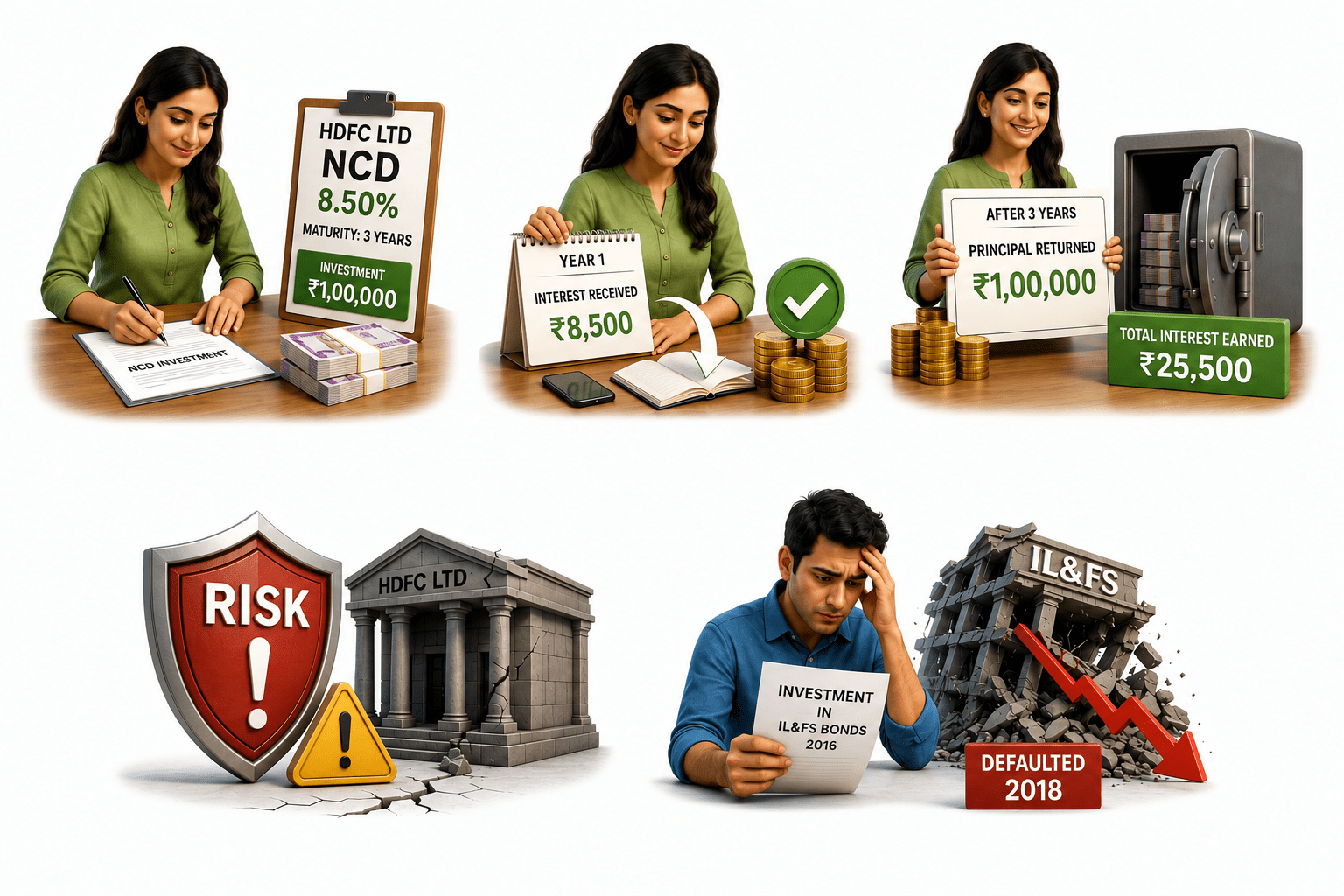

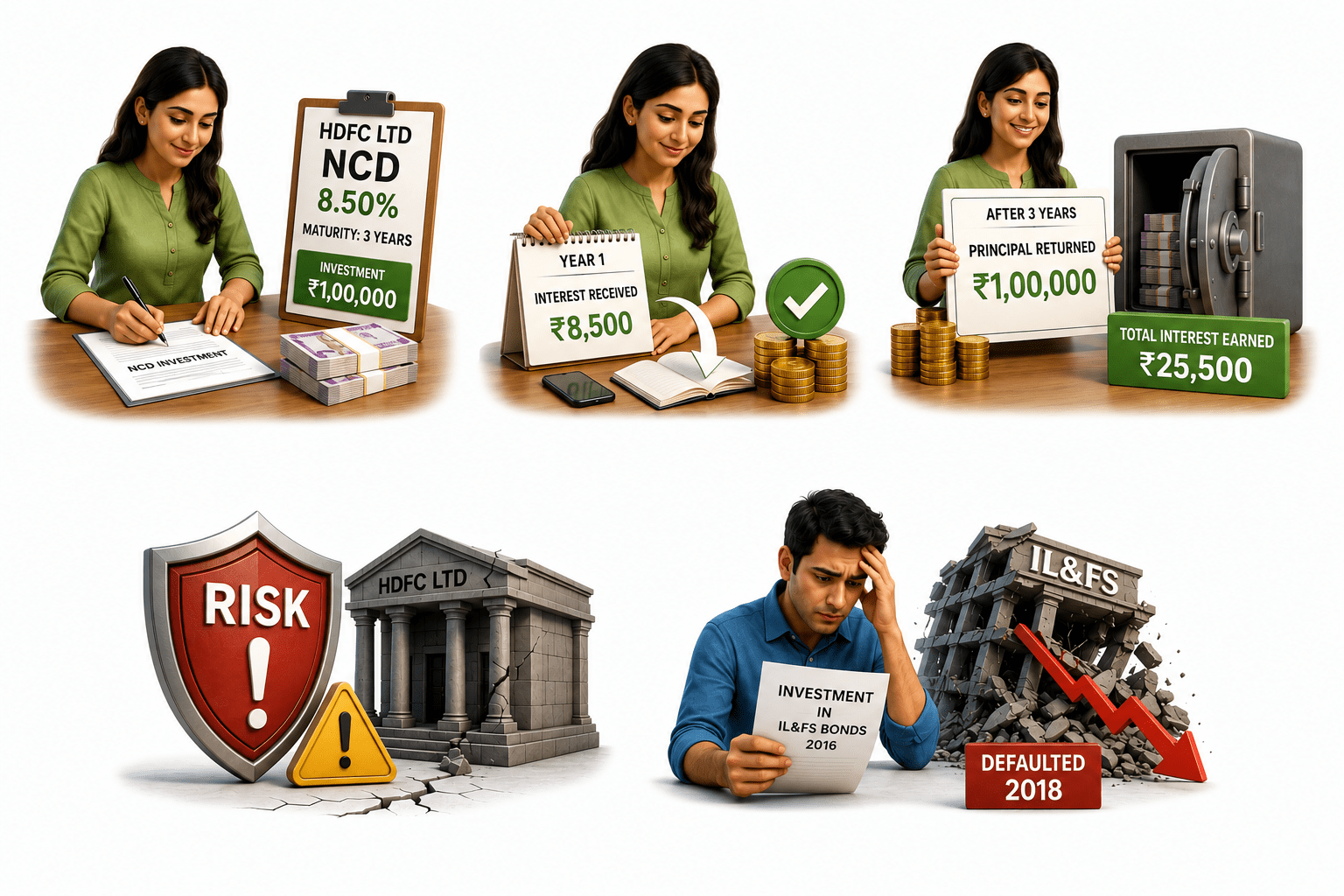

Example: Priya invests ₹1,00,000 in an HDFC Ltd NCD (Non-Convertible Debenture) at 8.50%, maturing in 3 years.

Every year, Priya receives ₹8,500 as interest.

By 2018, IL&FS defaulted and Amit lost a significant portion of his investment.

A reminder that even AA-rated corporate bonds can fail.

Risk: If HDFC Ltd faces financial trouble (very unlikely for AAA-rated), her principal could be at risk.

Counter-Example: Amit invests in IL&FS bonds rated AA in 2016.

In 3 years, HDFC Ltd returns her full ₹1,00,000.

Total interest earned = ₹25,500.

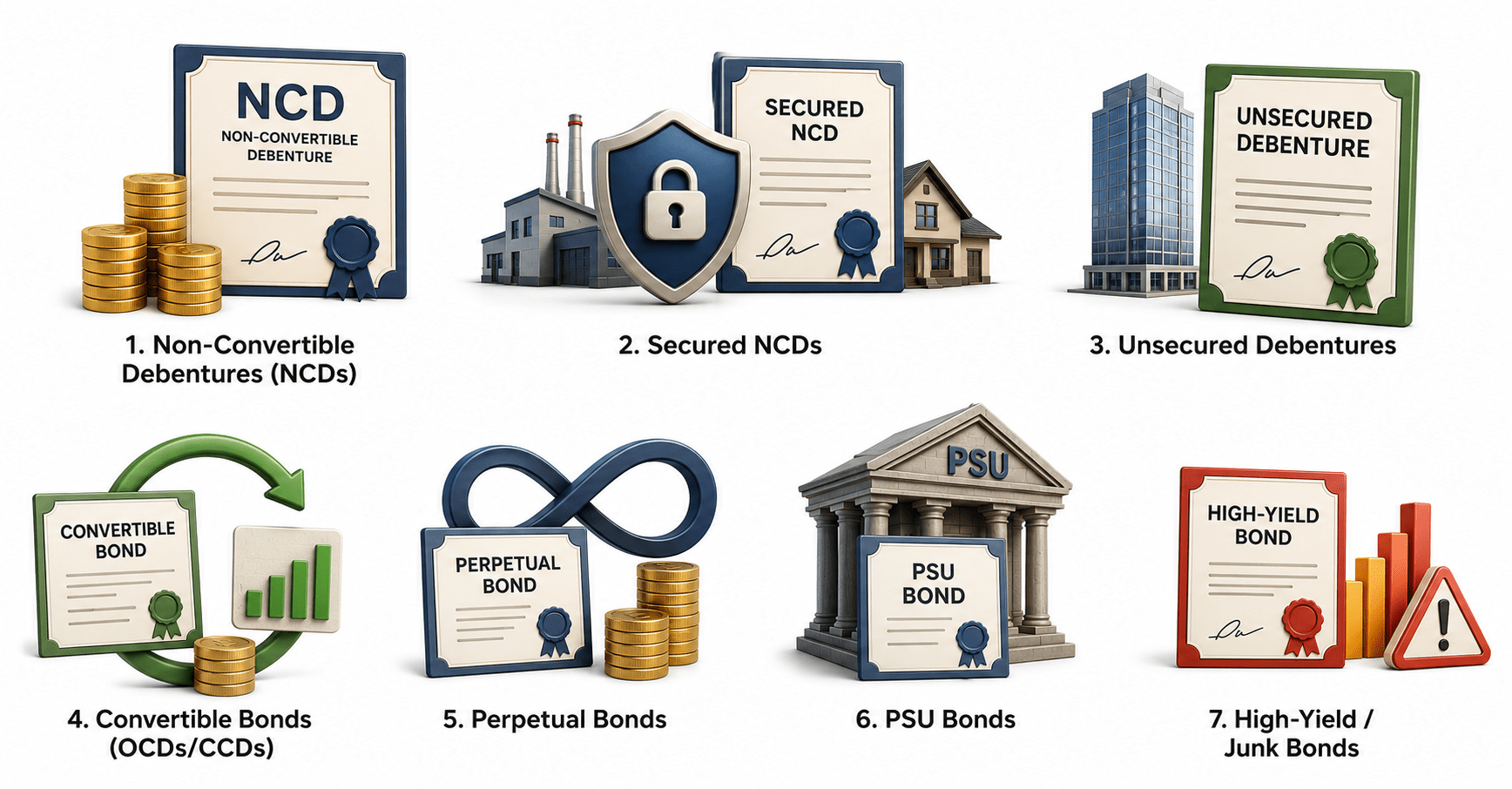

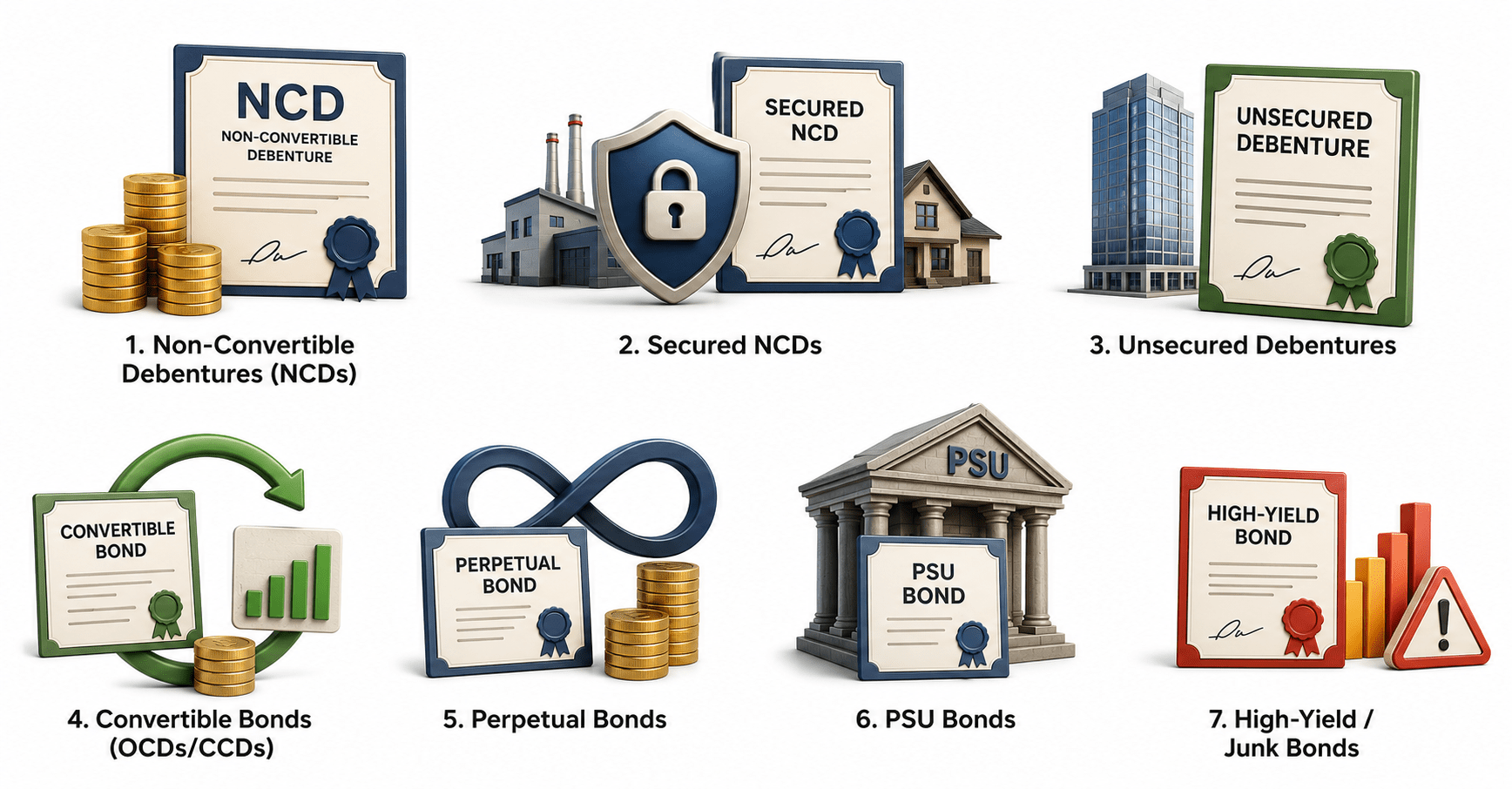

Types of Corporate Bonds

1. Non-Convertible Debentures (NCDs)- The most common corporate bond in India. Simply put — you lend to a company, it pays interest, returns your money. Cannot be converted to shares. Can be secured (backed by assets) or unsecured.

2. Secured NCDs- The company pledges specific assets (property, plant) as collateral. If it defaults, these assets are sold to repay you first. Safer than unsecured.

3. Unsecured Debentures- No collateral. You rely purely on the company’s ability to repay. Higher yield to compensate for higher risk.

Types of Corporate Bonds

7. High-Yield / Junk Bonds- Issued by companies with low credit ratings (BB or below). Very high interest (12–16%+) but very high risk of default. Not for ordinary investors.

6. PSU Bonds- Bonds issued by government-owned companies like NTPC, IRFC, NHAI. Safer than private corporate bonds because the government is the ultimate owner.

5. Perpetual Bonds- Issued by banks. No fixed maturity — the bank pays you interest forever (in theory). Very high risk — can be written to zero if the bank faces a crisis. Eg: Yes Bank AT1 bonds written down in 2020.

4. Convertible Bonds (OCDs/CCDs)- These bonds can be converted into equity shares later. You start as a lender and may become a shareholder. Attractive in growing companies.

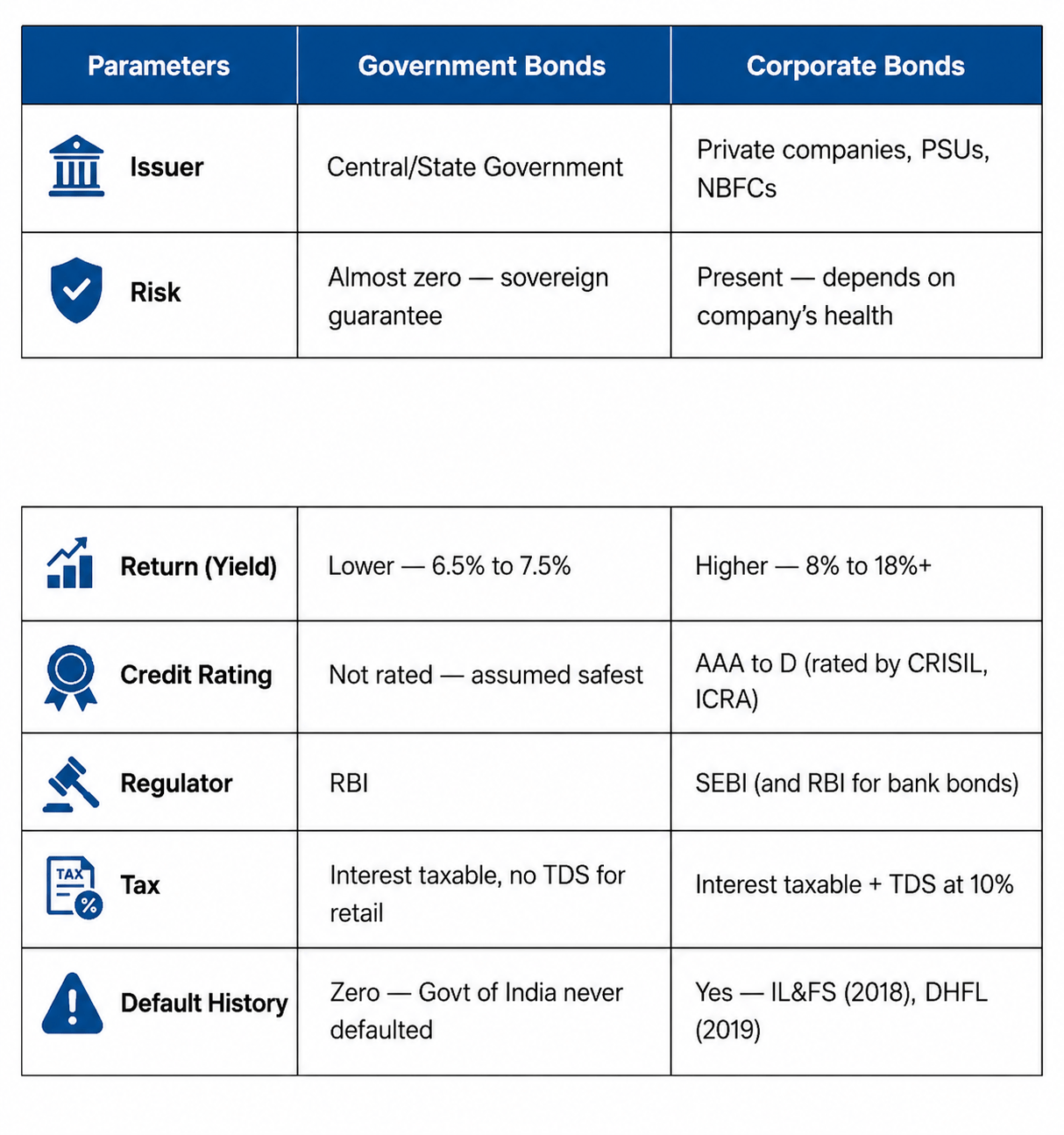

Government Bonds vs. Corporate Bonds

Summary

5

Bonds help in risk diversification.

4

Different bonds serve different investment needs.

3

Government bonds are safer than corporate bonds.

2

Bond prices and interest rates move inversely.

1

Bonds are fixed-income instruments representing loans.

Quiz

Which bond is generally safer?

A. Corporate Bond

B. Government Bond

C. Debenture

D. Commercial Paper

Quiz-Answer

Which bond is generally safer?

A. Corporate Bond

B. Government Bond

C. Debenture

D. Commercial Paper