Time Series Analysis

Quest for Stationarity: Analyzing Stationarity in Time Series

Learning Outcome

5

Apply techniques to convert non-stationary data → stationary

4

Use statistical tests (ADF & KPSS)

3

Understand types of stationarity

2

Identify visual signals of non-stationary data

1

Understand what stationarity means in time series.

Recall

Before this topic we learned:

- Time Series data

- Trend

- Seasonality

- Forecasting models

- ARIMA basics

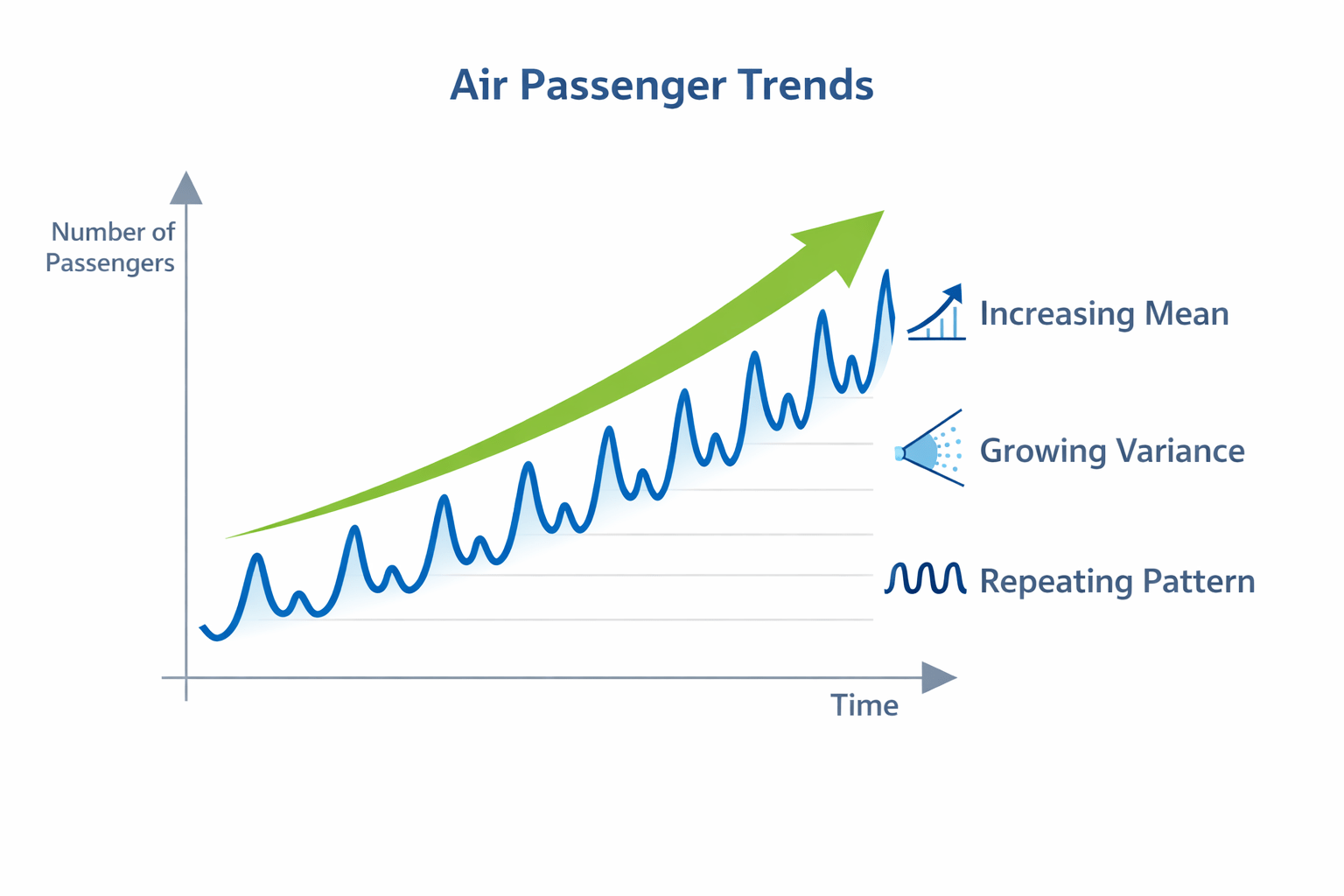

Why do many models fail when the data keeps changing its behavior?

Hook Story

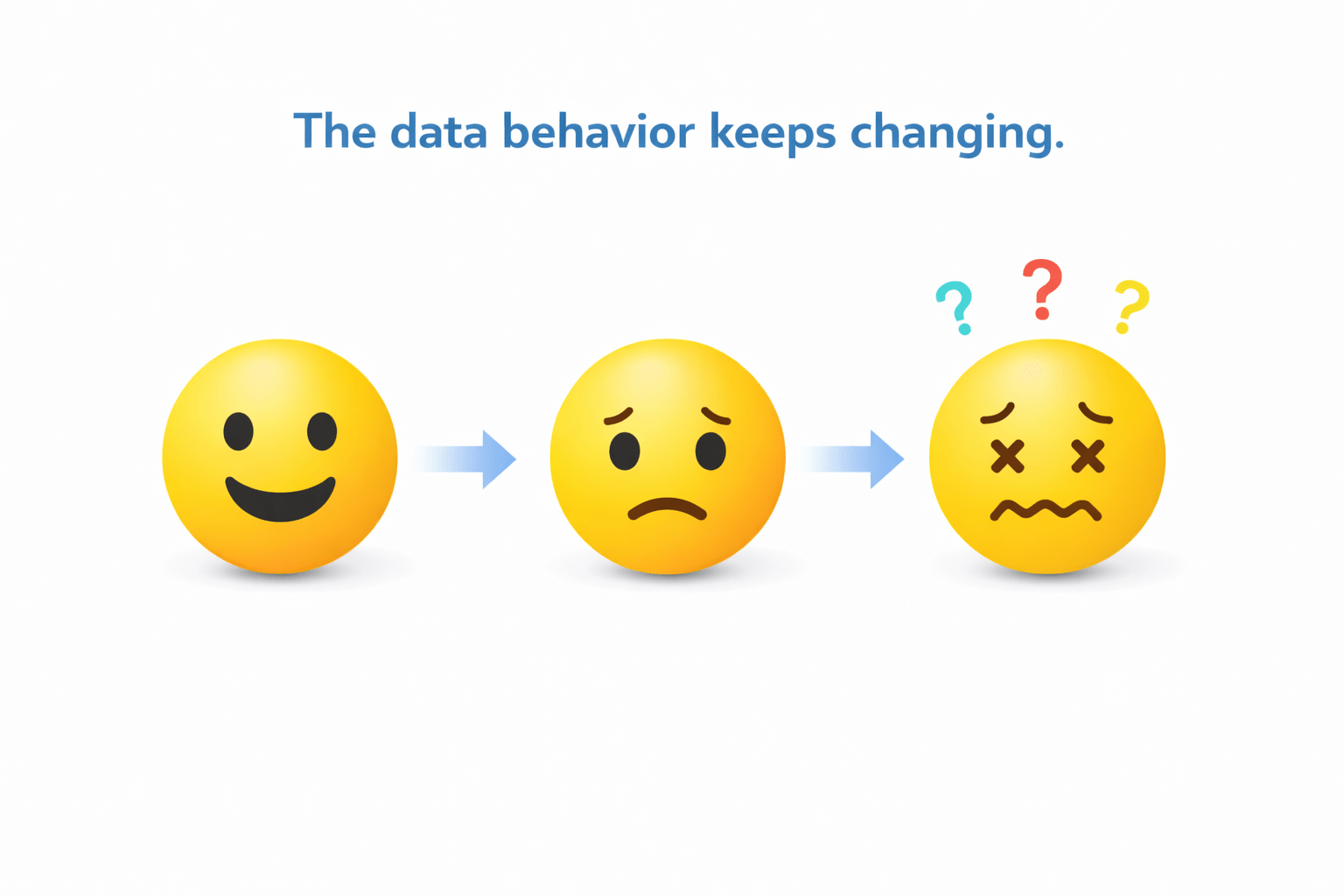

The Stock Market Problem

- Yesterday average price = ₹100

- Next year average price = ₹300

This is the core problem of non-stationary data.

The data behavior keeps changing.

Transition to Concept

Why Models Need Stable Data

Machine learning models assume: Future behaves similar to past

But if:

- Mean changes

- Variance changes

- Patterns change

→ Model fails

Solution: Make the data stationary

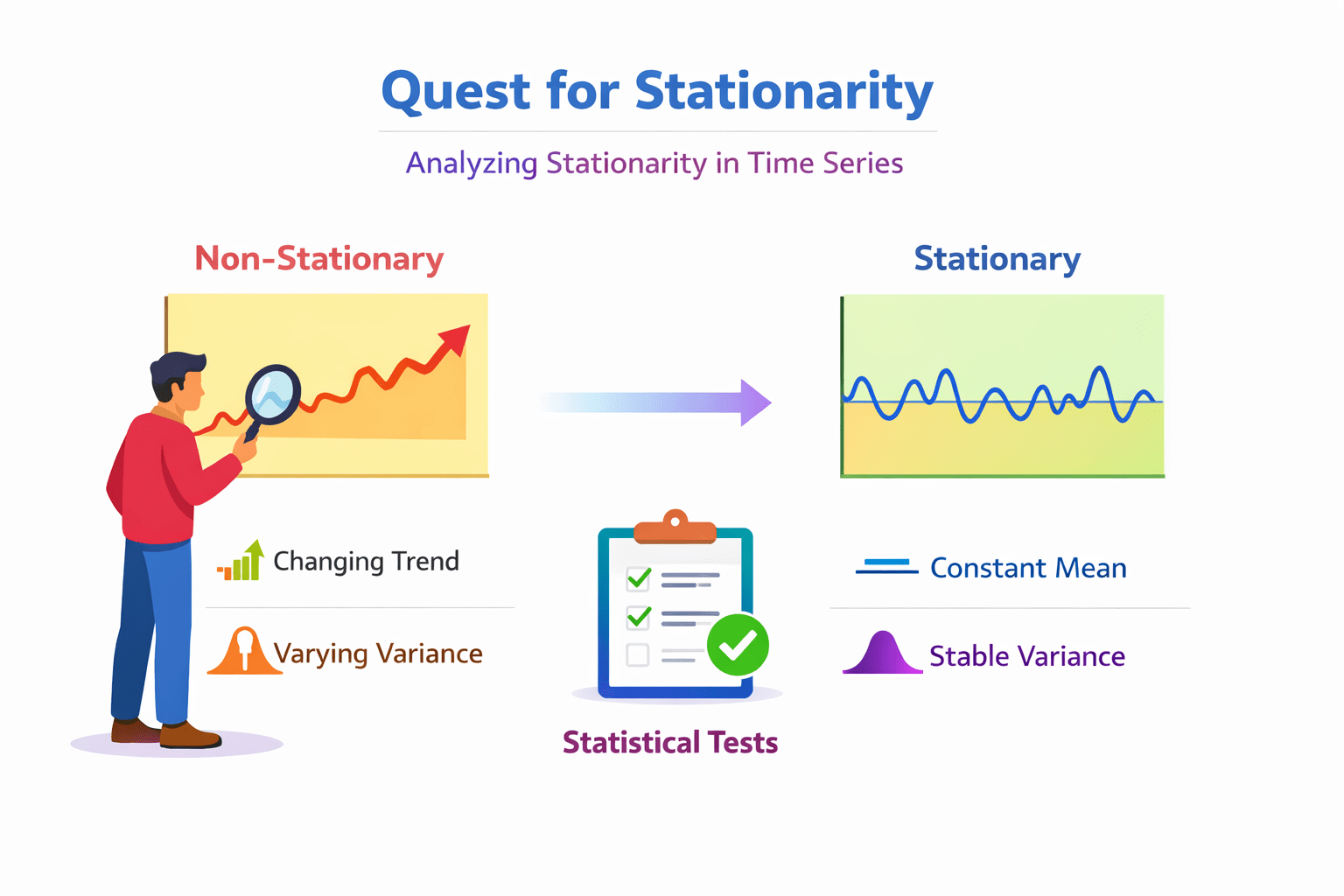

What is Stationarity?

A time series is stationary when its statistical properties do not change over time.

Mean

Mean

📊

Variance

Variance

📉

Autocorrelation

Autocorrelation

🔁

Models like ARIMA require stationarity

Stable properties include:

Stationary vs Non-Stationary

Key Difference:

Stationary Data

- Constant mean

- Constant variance

- No trend

Non-Stationary Data

- Changing mean

- Trend or seasonality

- Changing variance

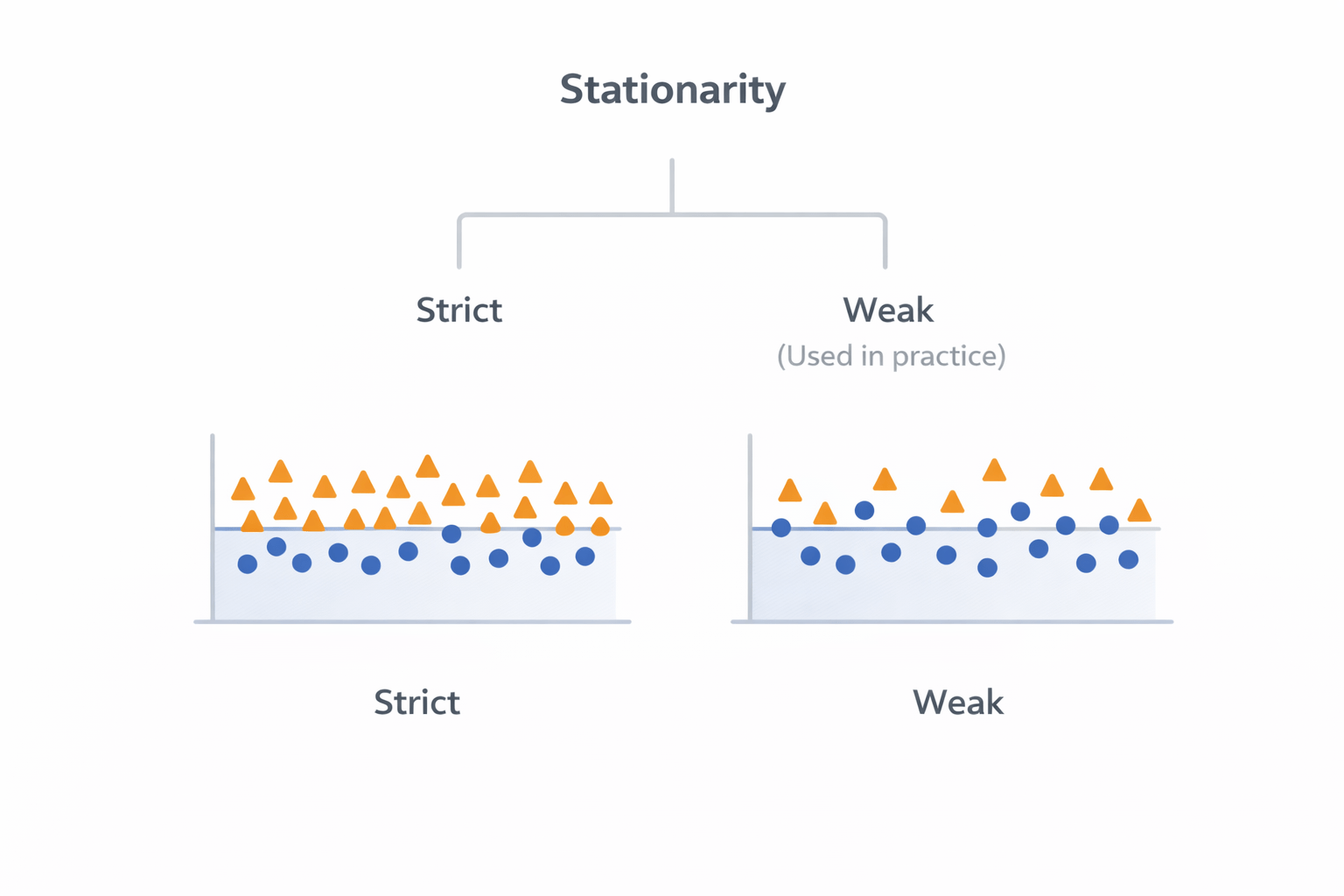

Types of Stationarity

Two Types of Stationarity

Strict Stationarity:

- Entire distribution constant

Weak (Covariance) Stationarity:

- Mean constant

- Variance constant

- Covariance constant

Most models assume weak stationarity in time series data.

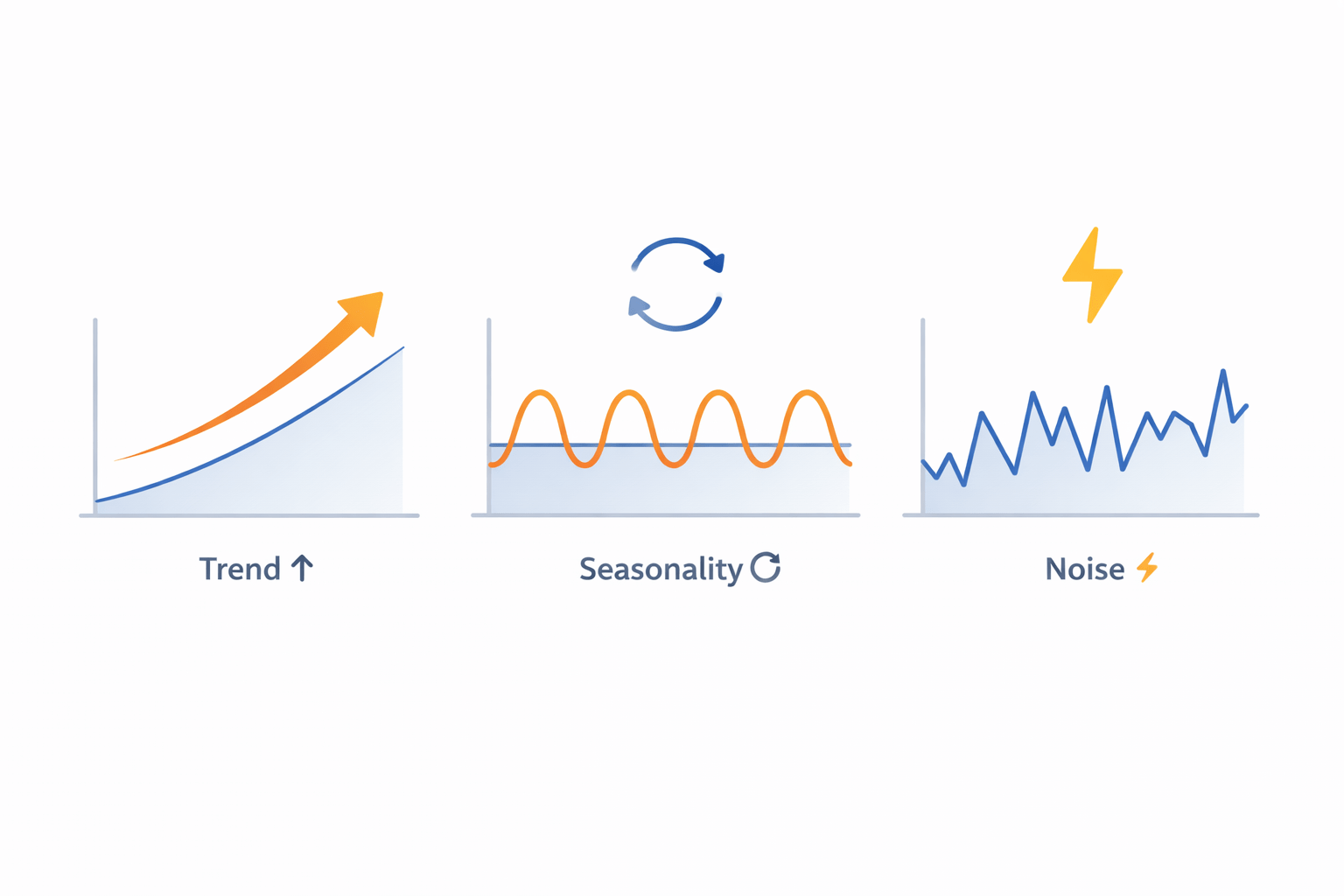

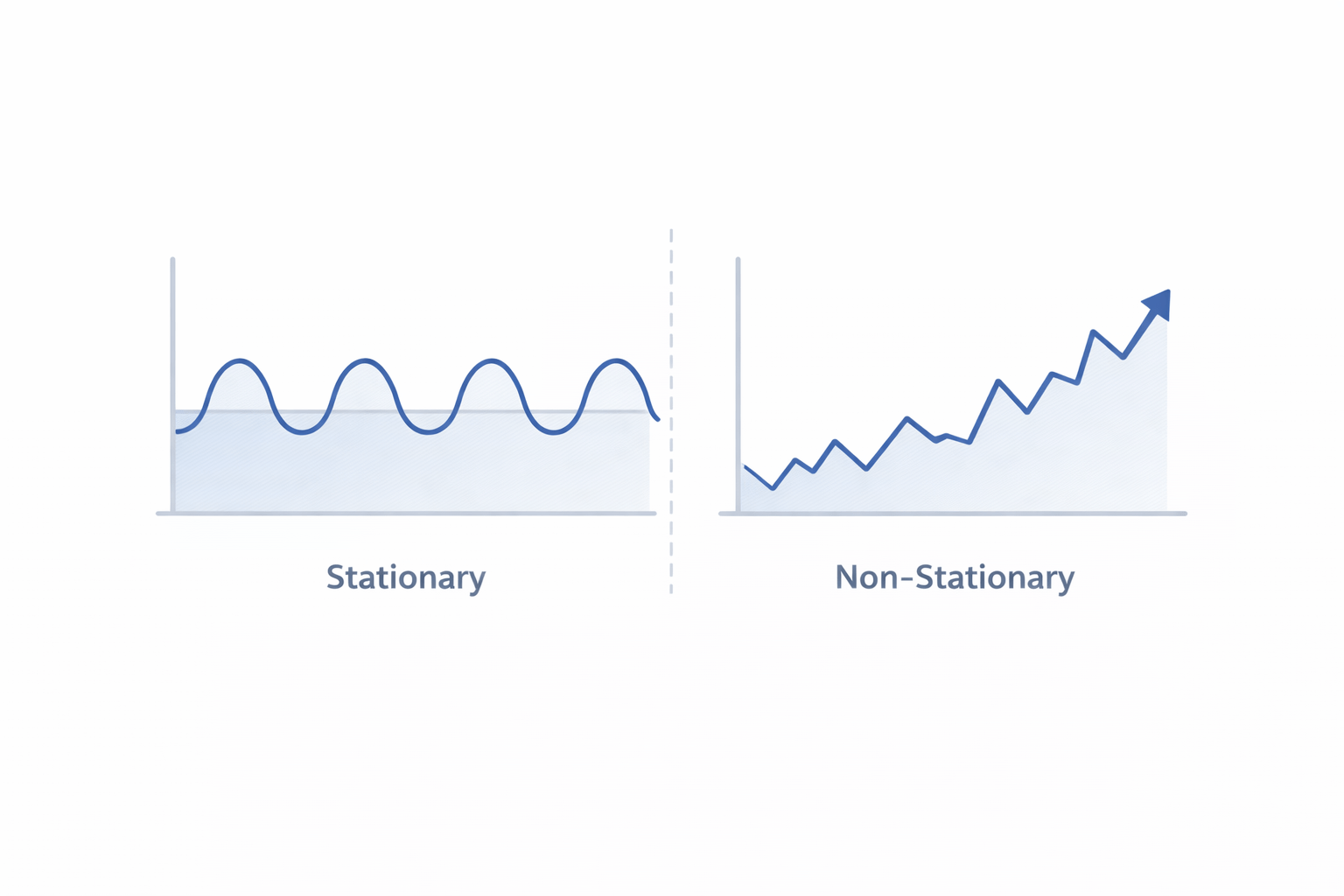

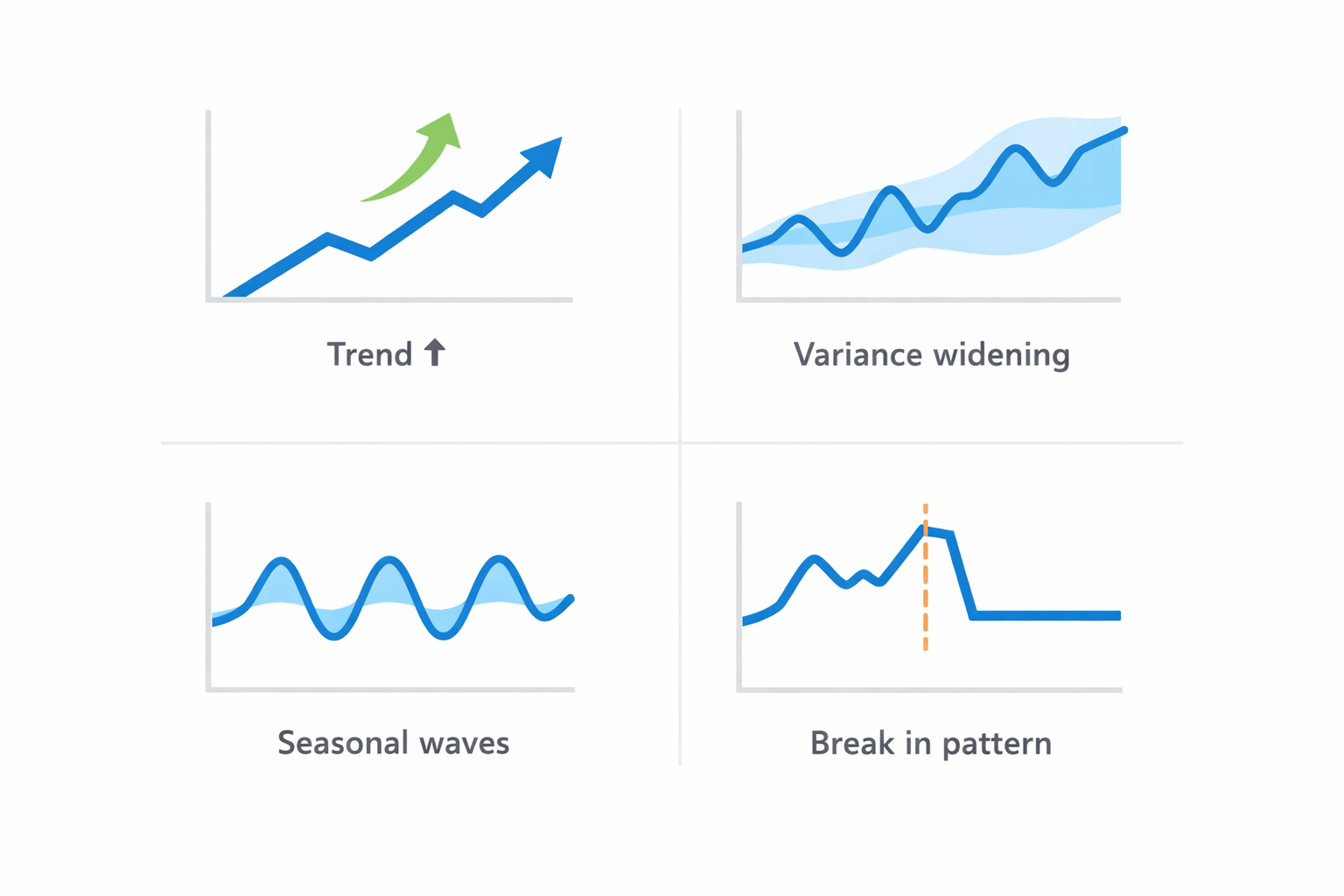

Visual Indicators

How to Visually Detect Non-Stationarity ?

Look for:

- Trend

- Changing spread

- Seasonal patterns

- Structural breaks

Example Plot:

Original Time Series Plot

Formal Tests for Stationarity:

Two popular tests:

- ADF Test

- KPSS Test

These tests check whether data is stationary using hypothesis testing.

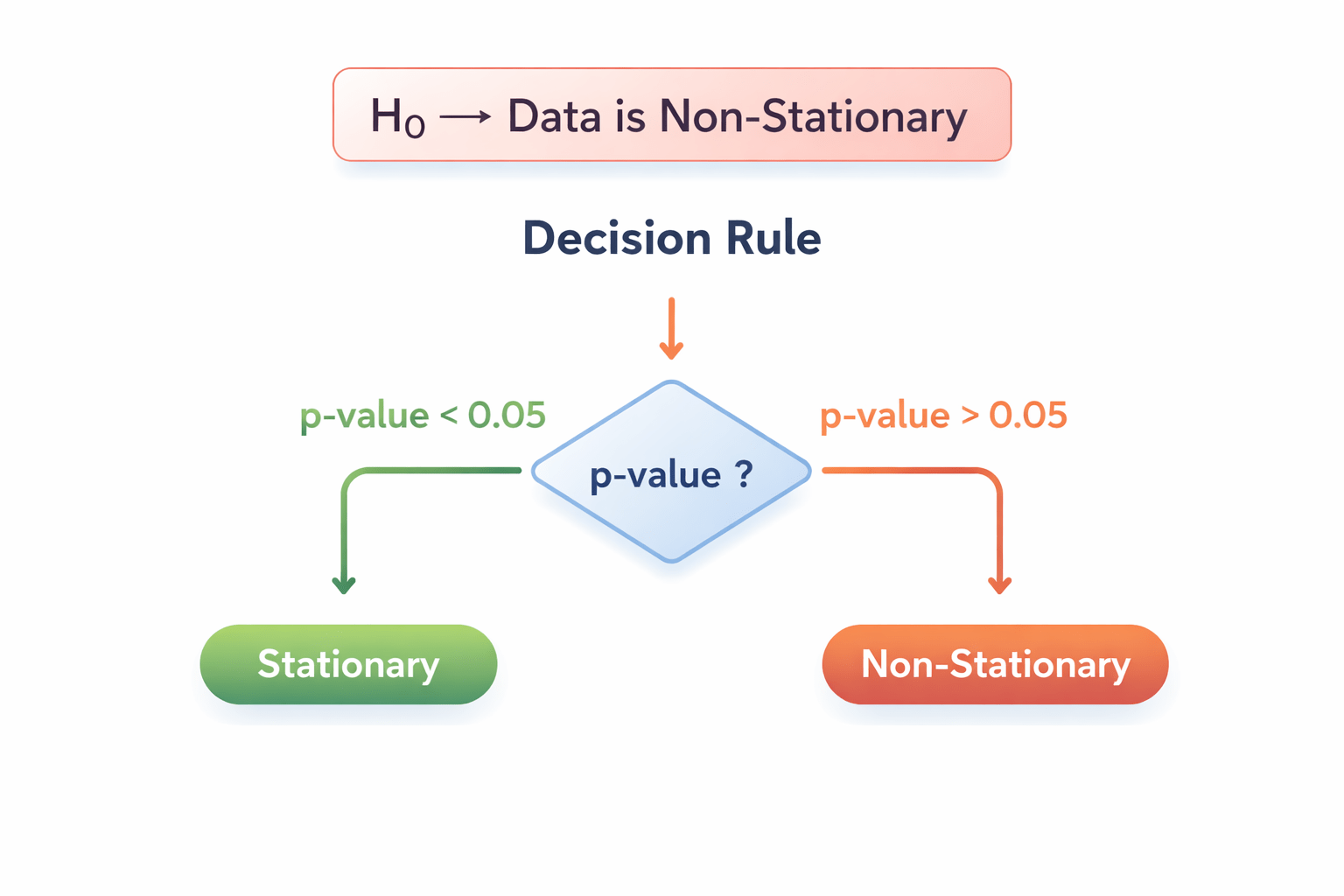

Augmented Dickey Fuller Test

ADF Test

H₀ → Data is Non-Stationary

Decision Rule:

p-value < 0.05 → Stationary

p-value > 0.05 → Non-Stationary

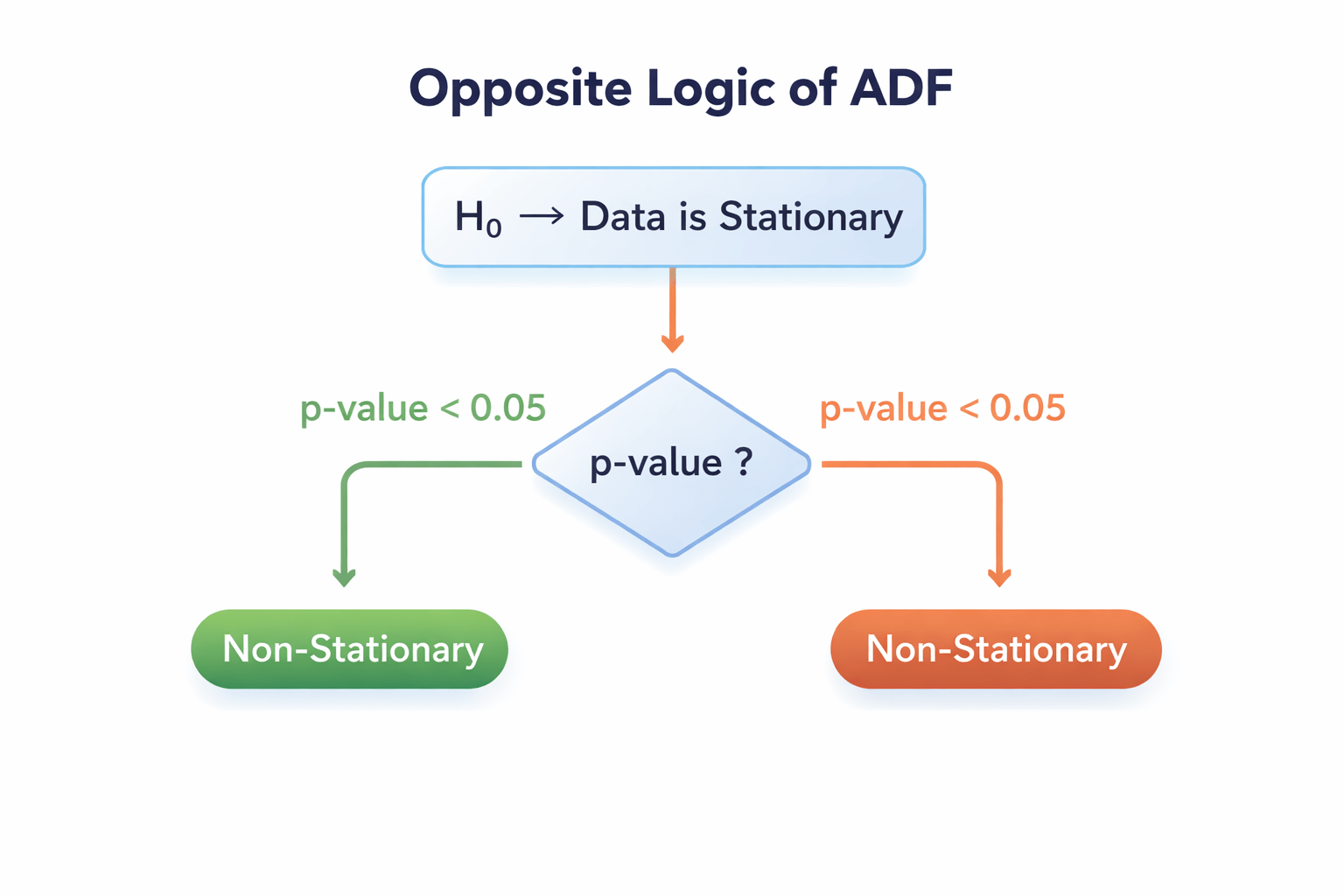

KPSS Test (Opposite logic of ADF)

H₀ → Data is stationary

Decision Rule:

p-value < 0.05 → Non-Stationary

p-value > 0.05 → Stationary

KPSS Test

Python Example

ADF Test in Python

from statsmodels.tsa.stattools import adfuller

result = adfuller(series)

print(result[1]) # p-valuep-value < 0.05 → Stationary

Techniques to Achieve Stationarity

- Differencing

- Log Transformation

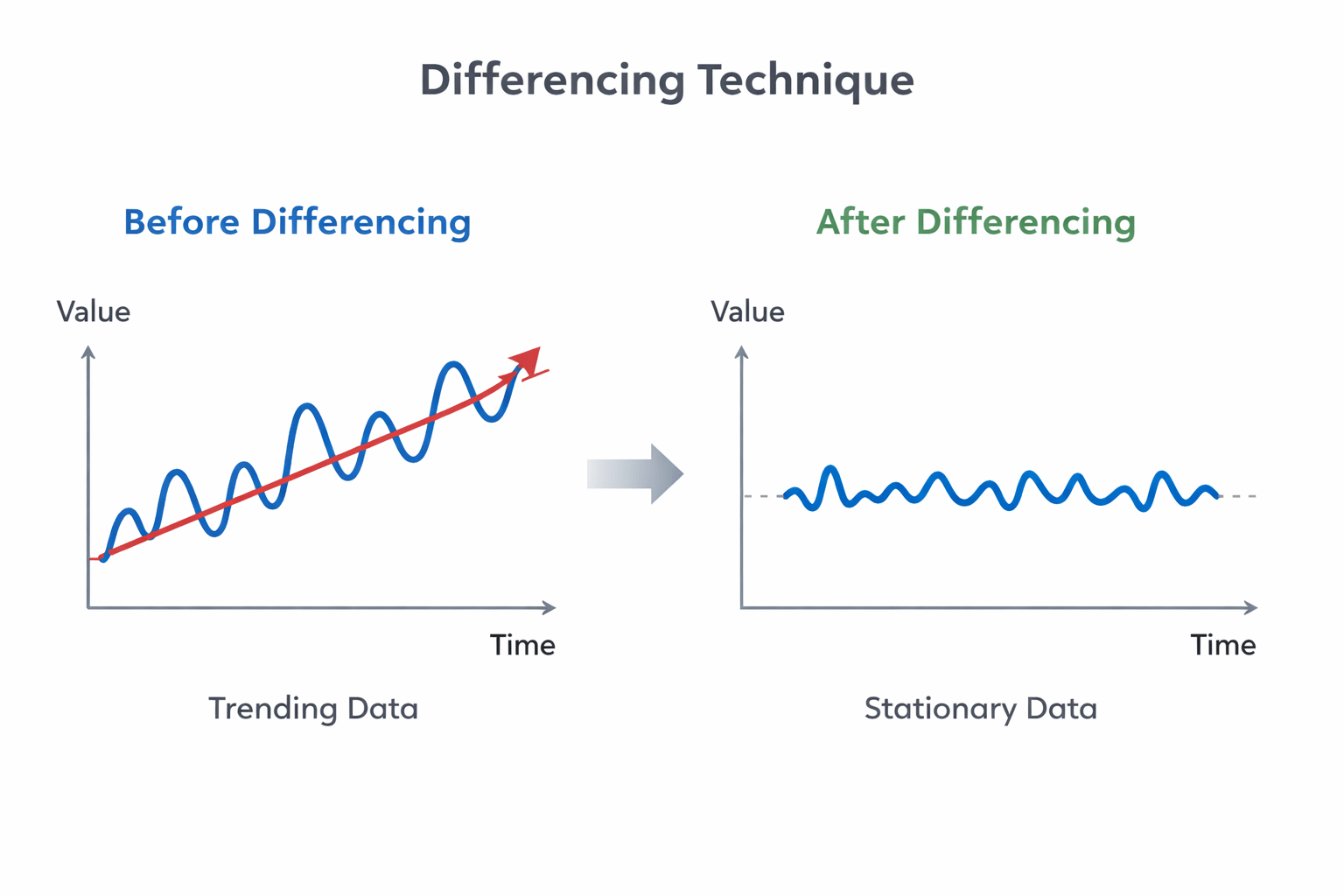

Differencing Technique:

Formula: Yt − Y(t−1)

Purpose:

- Removes trend

- Stabilizes mean

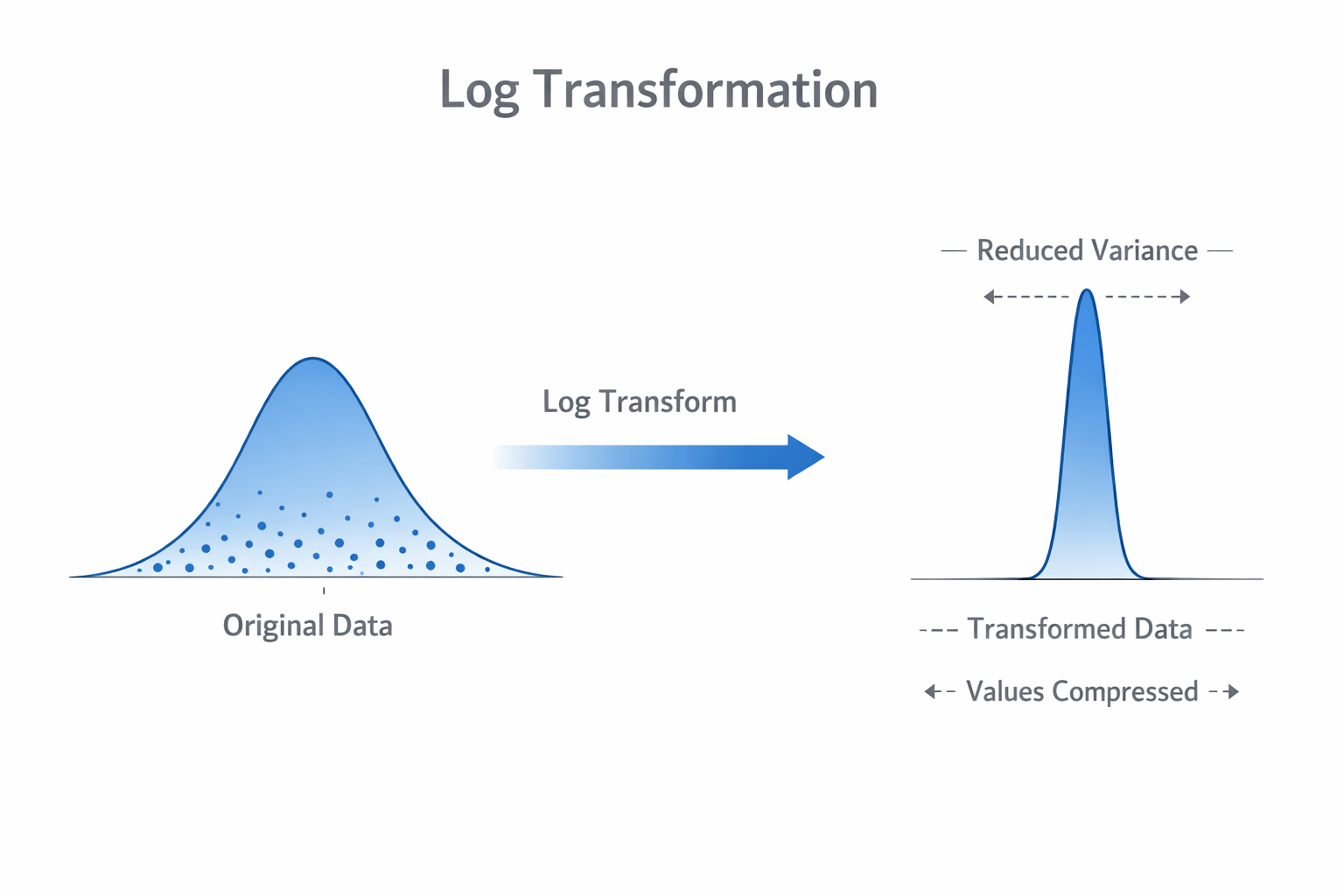

Log Transformation:

Formula: log(Y)

Used when:

- Variance increases over time.

Effect:

- Stabilizes variance

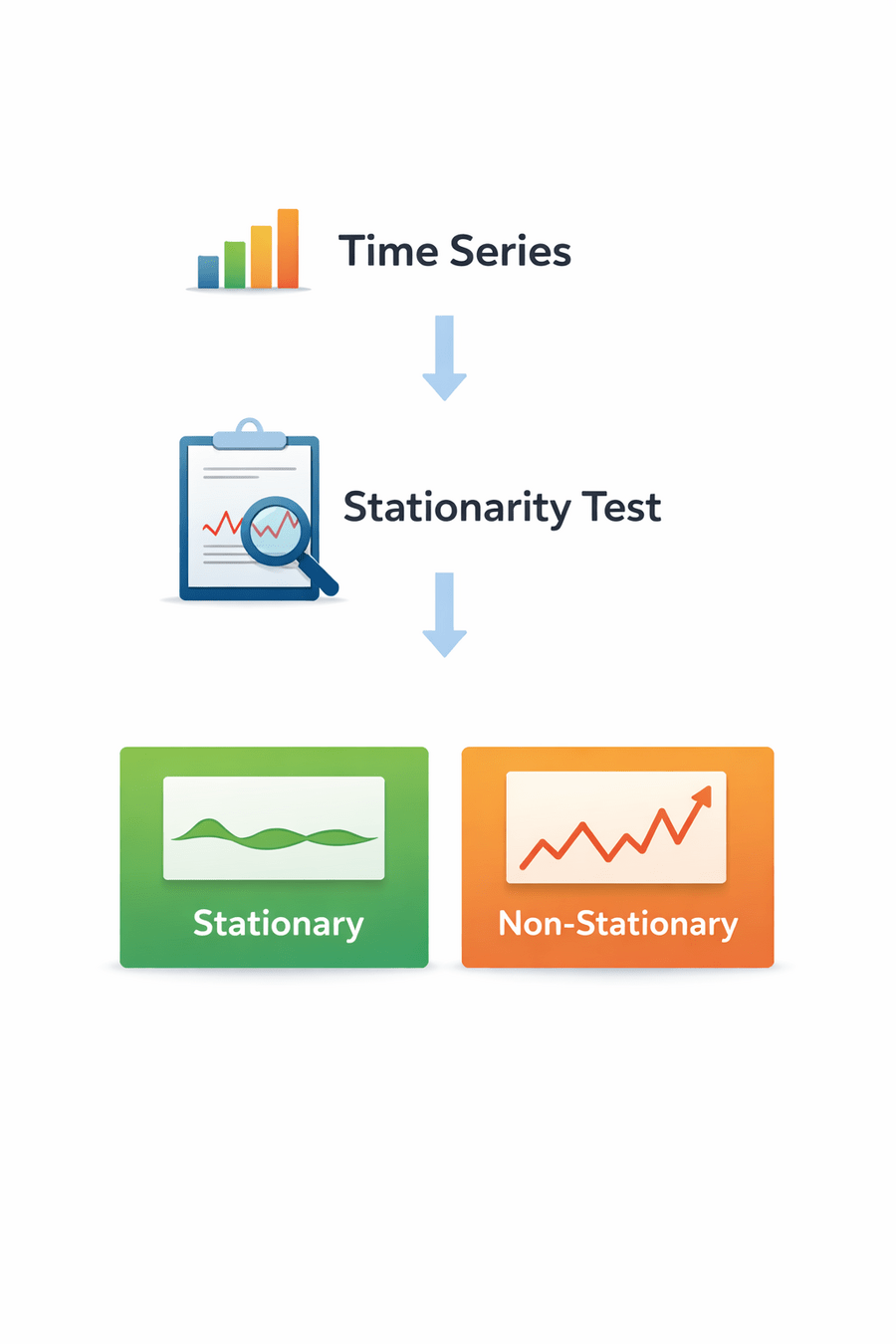

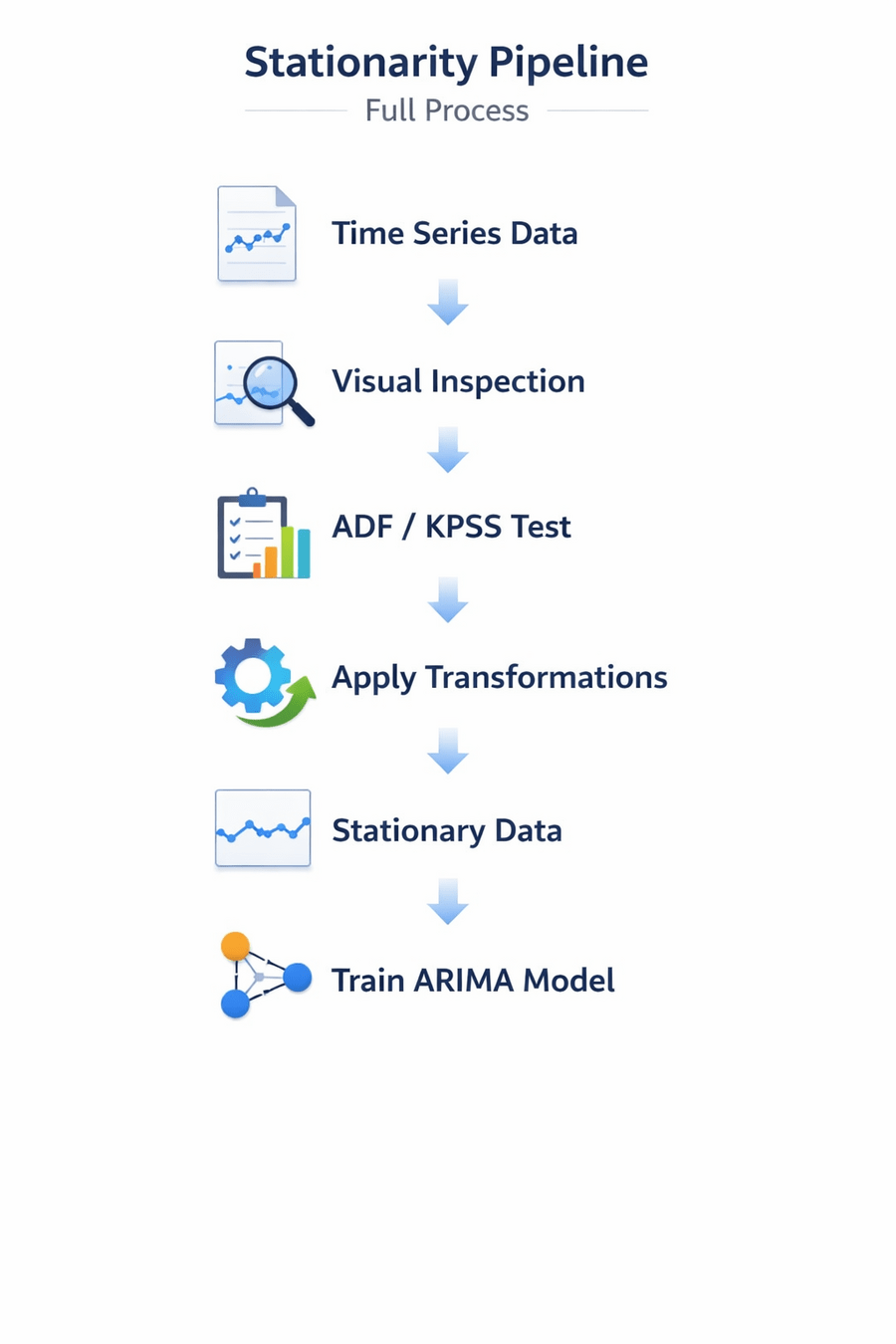

Complete Workflow

Time series → check stationarity → transform if needed → train ARIMA for forecasting.

Summary

5

Techniques like differencing and log transformation convert data to stationary

4

ADF and KPSS tests help statistically detect stationarity

3

Non-stationarity appears as trend, changing variance, or seasonality

2

Many forecasting models like ARIMA require stationary data

1

Stationarity means statistical properties remain constant over time

Quiz

Which statement about the ADF test is correct?

A. Null hypothesis: Data is stationary

B. Null hypothesis: Data is non-stationary

C. Used only for classification

D. Used to detect seasonality

Quiz

Which statement about the ADF test is correct?

A. Null hypothesis: Data is stationary

B. Null hypothesis: Data is non-stationary

C. Used only for classification

D. Used to detect seasonality