Winter School in Political Economy

Lecture 3

Inequality

Where do we stand

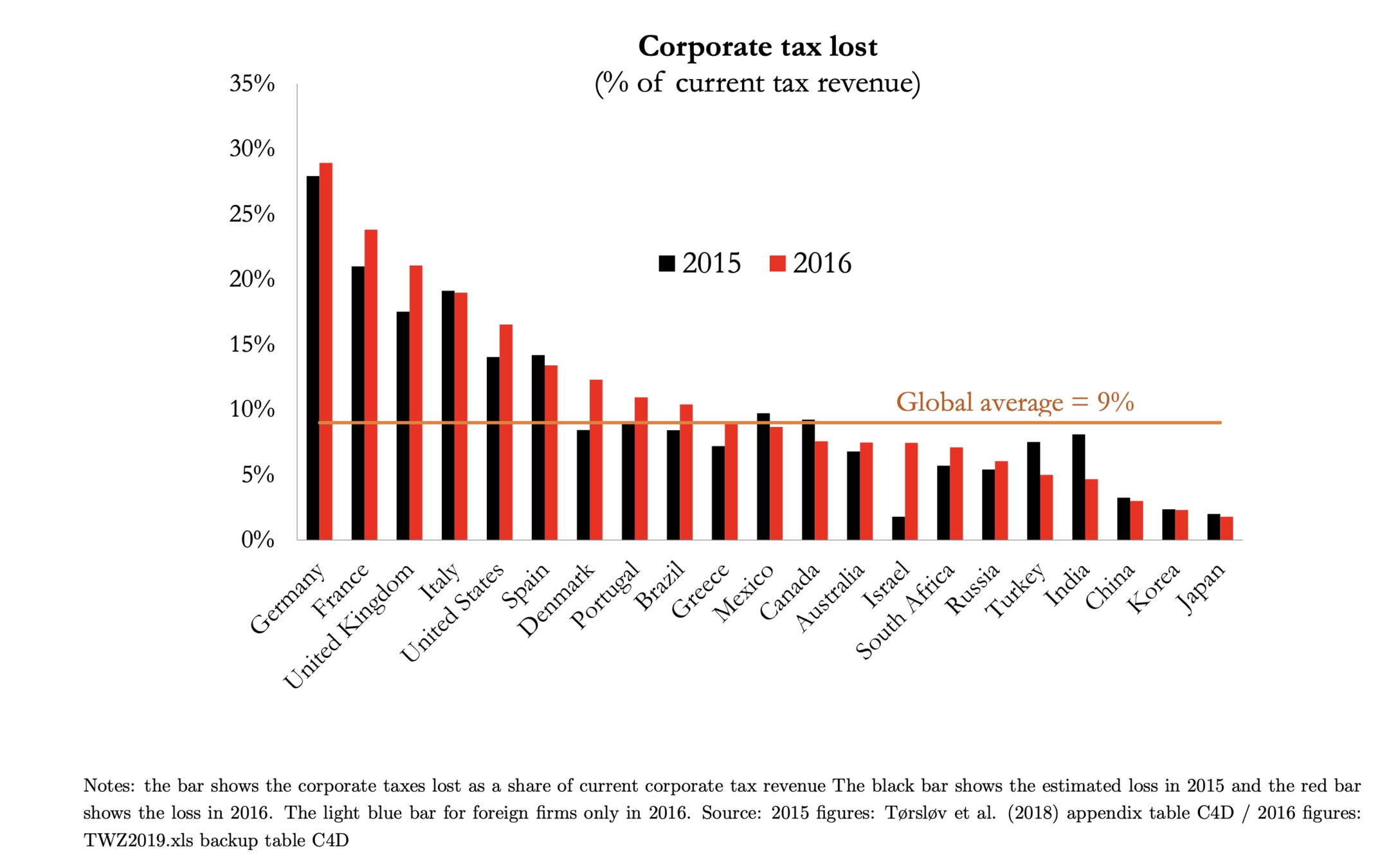

- 1985 to 2019 decrease from 49% to 23% in the global average statutory corporate tax rate

- Largely driven by tax competition – race to the bottom

- Distinction between real and nominal tax rate

- Distinction between optimisation and avoidance

- Weak international efforts

Direction of change

- Tax deficit

- as if all profits were subject to min rate

- min rate at 21% for foreign earning of US MNC

- CIT in US at 28%

- tax collector of last resort

- Coordination through OECD and G20

- moving ahead of BEPS

- Unilateral actions against non-adopting tax havens