Learning from DeFi: Would Automated

Market Makers Improve Equity Trading?

Katya Malinova & Andreas Park

WFA 2024

Honolulu, June 28-30, 2024

| McMaster University |

University of Toronto |

|---|

- Blockchain: borderless general purpose value and resource management tool

Preliminaries

- DeFi: financial applications that run on blockchains

- \(\Rightarrow\) brought new ideas and tools

- one new market institution: automated market makers

Decentralized trading using automated market makers (AMM)

Liquidity providers

Liquidity demander

Liquidity Pool

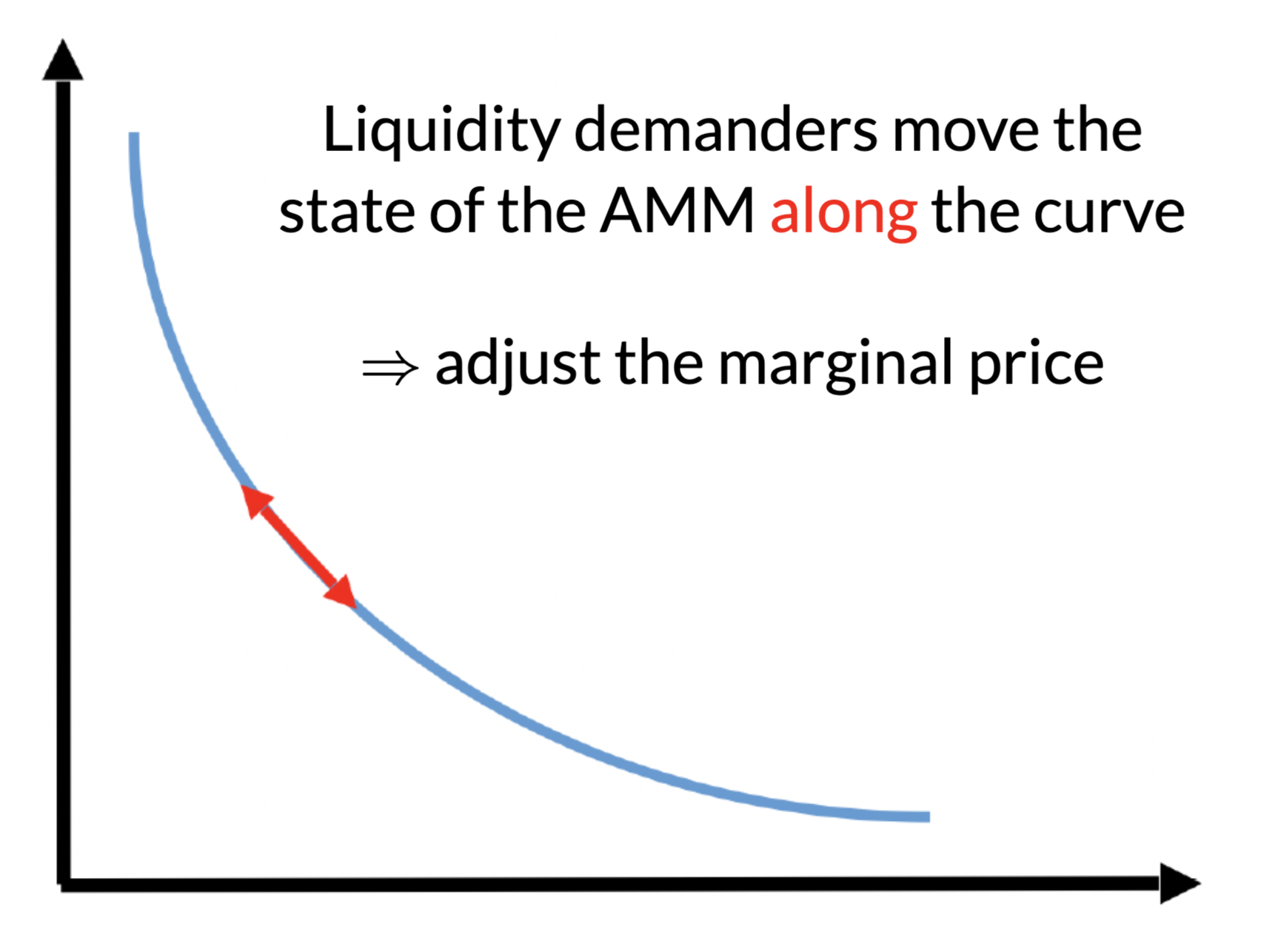

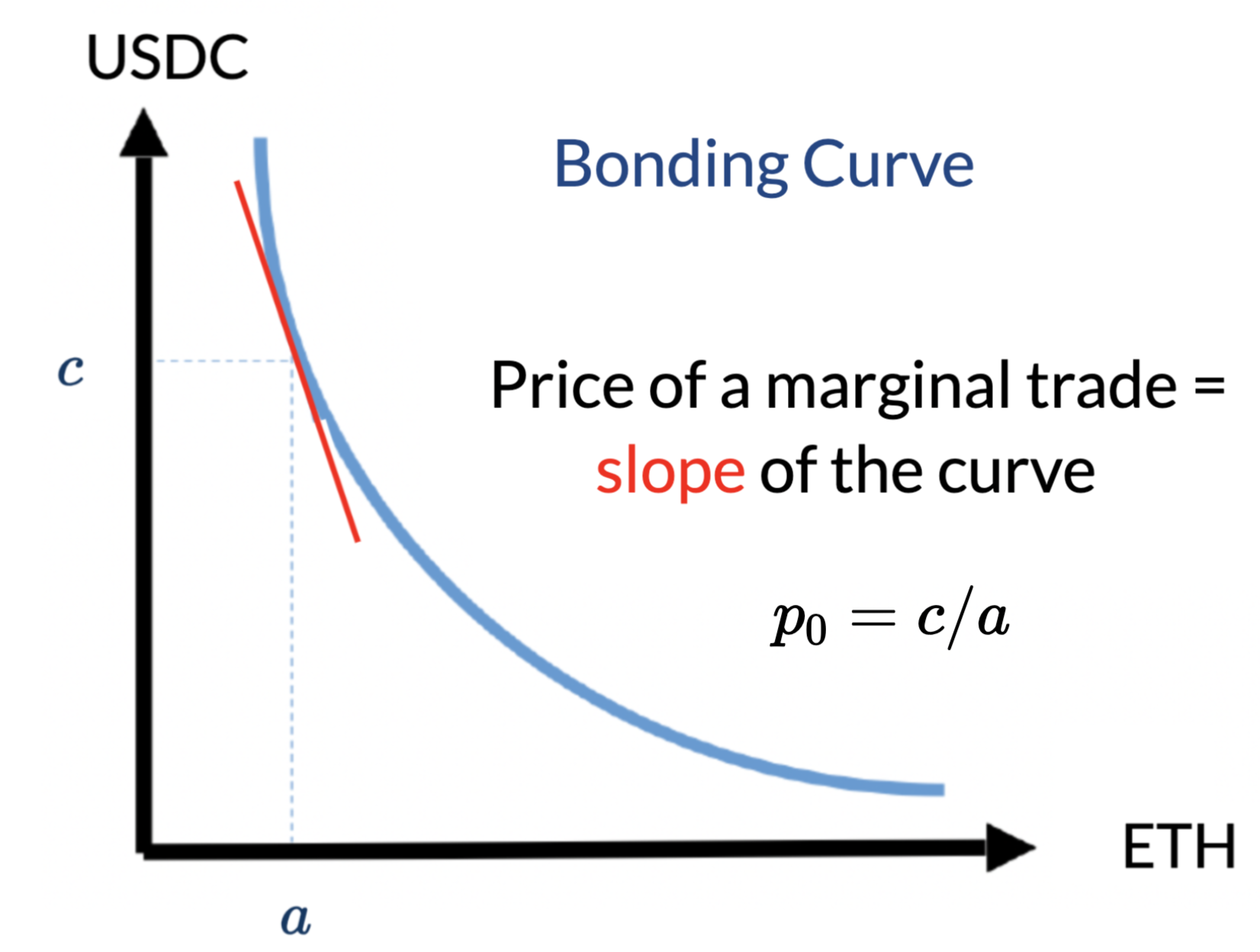

AMM pricing is mechanical:

- determined by the amounts of deposits

- most common:

- constant product

- #USDC \(\times\) #ETH = const

No effect on the marginal price

Key Components

- Our question:

- Can an economically viable AMM be designed for current equity markets?

- Would such an AMM improve current markets?

- Pooling of liquidity!

- Liquidity providers:

- pro-rated

- risk

- trading fee income

- use assets that they own to earn passive (fee) income

- retain exposure to the asset

- pro-rated

- Liquidity demanders:

- predictable price

- continuous trading

- ample liquidity

Existing asset holders, not market makers, do not aim for zero inventory!

Modelling Calibrate-able Liquidity Supply and Demand in an Automated Market Maker

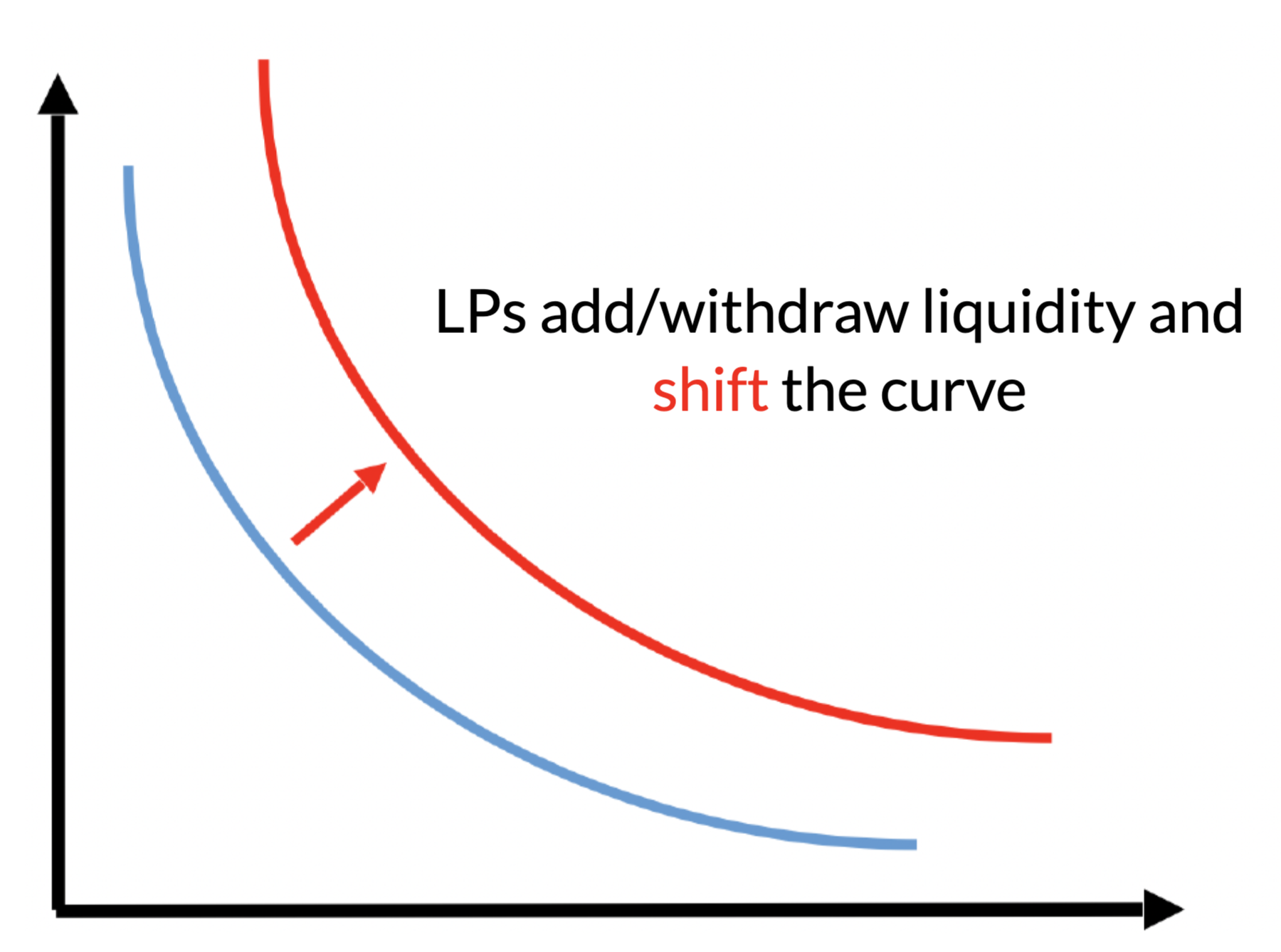

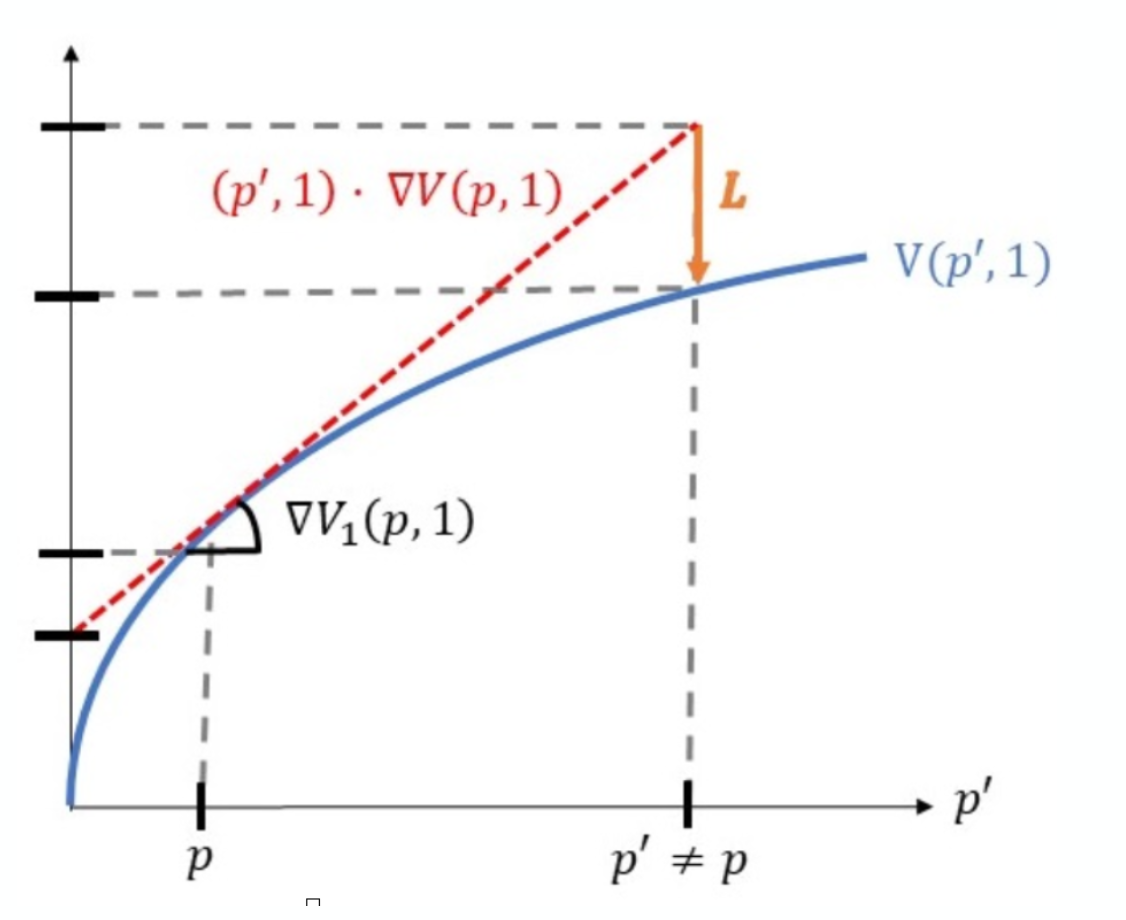

Liquidity providers

- Deposit asset & cash when the asset price is \(p\)

- While in the pool: balanced volume \(V\) + order imbalance \(p\to p'\)

- Withdraw at price \(p'\)

Buy and hold

Provided liquidity

in the pool

- \(\Rightarrow\) positional loss relative to a "buy-and-hold" when \(p'\ne p\)

- adverse selection

- Arbitrageurs monitor the pool

- \(\Rightarrow\) LPs deposit/writhdraw at efficient prices!

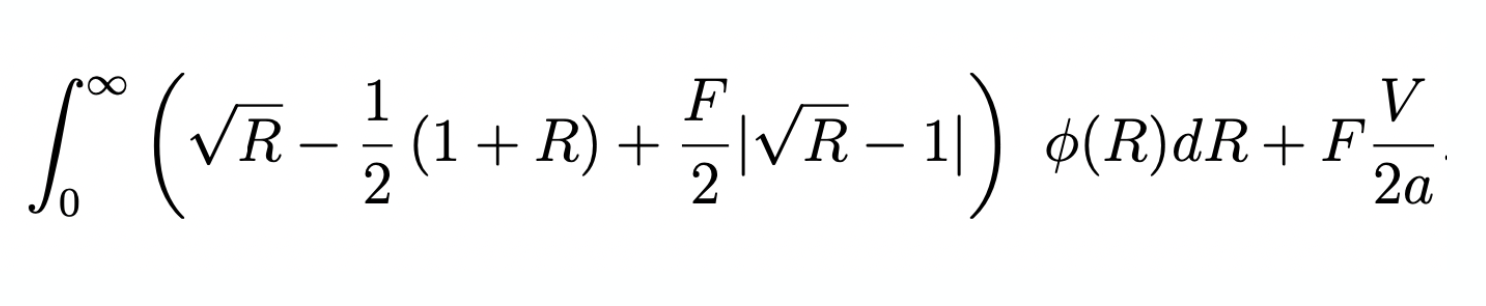

Expected returns to liquidity providers over the "deposit period"

- \(R\) = asset return

- \(F\) = trading fee

- \(V\) = balanced volume

- \(a\) = size of the liquidity pool

Similar to Lehar and Parlour (2023), Barbon & Ranaldo (2022).

(incremental) adverse selection loss \(L\) when the asset return is \(R=p'/p\)

fees earned

on informed

fees earned

on balanced flow

for reference:

- If the asset price \(\searrow\) 10% the incremental loss \(L\) for liquidity providers is 13 basis points on the deposit

- \(\to\) total loss=-10.13%

- If the asset price \(\nearrow\) 10%, the liquidity provider gains 12 basis points less on the deposit

- \(\to\) total gain =9.88%

For fixed balanced volume \(V\) & fee \(F\):

- Larger pool size \(a \to\) smaller shares of the fees

- \(\Rightarrow \) LP return \(\searrow\) in pool size

-

Competitive liquidty provision:

- \(\Rightarrow\) the upper-bound on pool size above which LPs lose money

- we characterize this by \(\bar{\alpha}\) \(=\) fraction of the asset's market cap to be deposited to the pool

\(=\) 0

Liquidity Demander's Decision & (optimal) AMM Fees

- Better off with AMM relative to traditional market if

\[\text{AMM price impact} +\text{AMM fee } F \le \text{bid-ask spread}.\]

- Two opposing forces when fee \(F\nearrow\)

- more liquidity provision

\(\to\) lower price impact - more fees to pay

- more liquidity provision

Result:

competitive liq provision\(\to\) there exists an optimal (min trading costs) fee \(F >0\)

- \(\to\) derive closed form solution

- Fee \(F\) depends on asset return distribution, balanced volume, quantity demanded

Similar to Lehar&Parlour (2023) and Hasbrouck, Riviera, Saleh (2023)

- Optimal \(F\) is asset-specific to compensate LPs for asset-specific adverse selection losses!

- Assumption: asset returns are exogenous to trading (efficient prices)

What's next?

- Calibrate to stock markets

- AMM Feasible?

- Are the AMM costs at the optimal fee \(F\) \(<\) bid-ask spread?

Approach: daily AMM deposits

- AMMs close overnight.

- Market: opening auction \(\to\) \(p_0\)

- Determine optimal fee \(F\);

LPs deposit \(a\) assets and \(c\) cash at ratio \(p_0=c/a\) until break even \(\alpha=\overline{\alpha}\)

- Liquidity locked for the day

- At EOD release deposits and fees

- Back to 1.

Background on Data

Special Consideration 1: What volume?

-

some volume may be intermediated

- with AMMs: no need for intermediation

- \(\to\) intermediated volume could disappear

- \(\to\) use volume/2

- Some caveats, e.g.

- arbitrageur volumes

- larger volume if AMM has lower trading costs

Special Consideration 2: What's \(q\) (the representative order size)?

- use average per day

- take long-run average + 2 std of daily averages

- (also avg \(\times 2\),\(\times 4\), depth)

All displayed data CRSP \(\cap\) WRDS

- CRSP for shares outstanding

- WRDS-computed statistics for

- quoted spreads (results similar for effective)

- volume

- open-to-close returns

- average trade sizes, VWAP

- Time horizon: 2014 - March 2022

- Exclude "tick pilot" period (Oct 2016-Oct 2018)

- All common stocks (not ETFs) (~7550).

- Explicitly not cutting by price or size

- All "boundless" numbers are winsorized at 99%.

Special Consideration 3:

Where to get returns and volume?

- Approach 1: "ad hoc"

- "one-day-back" look

- take yesterday's return and volume when deciding on liquidity provision in AMM

- Approach 2: estimate historical return distribution

AMMs based on historical returns

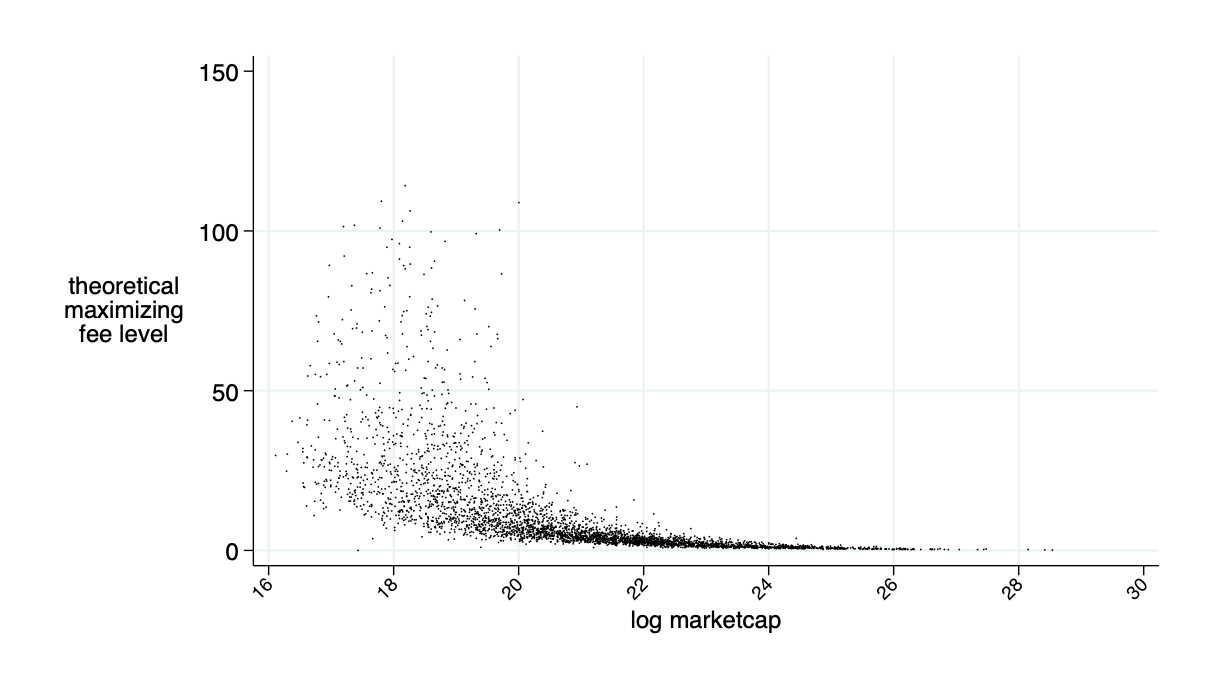

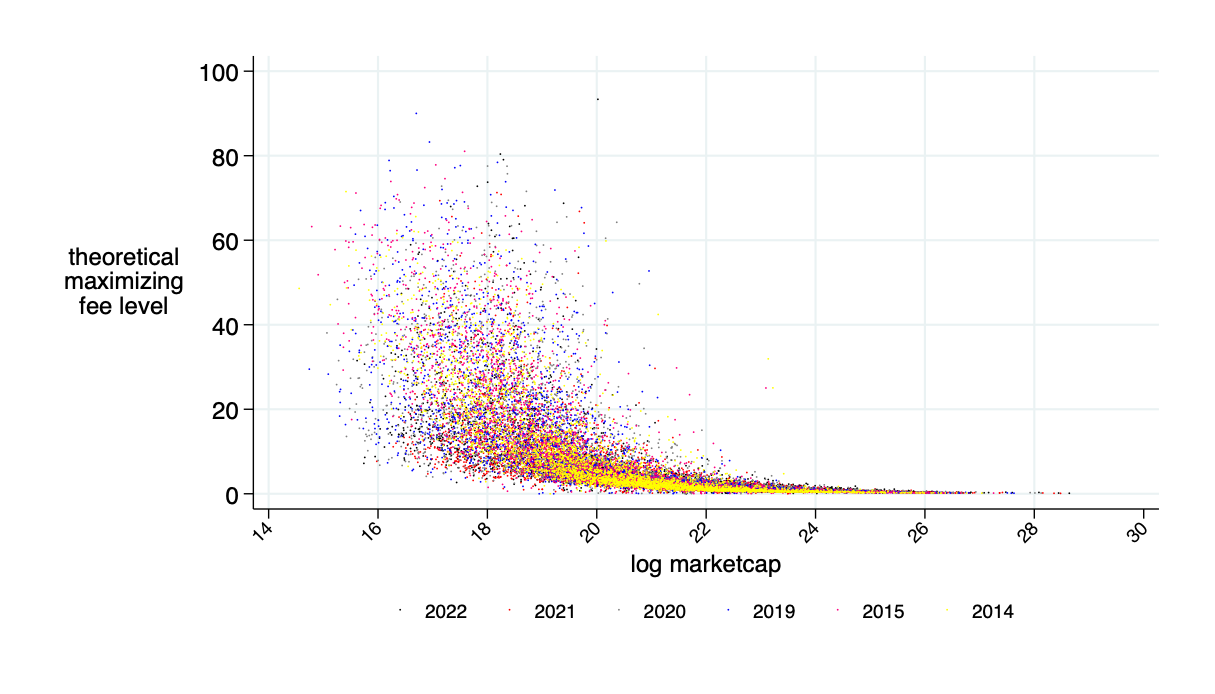

- average \(F^\pi=11\)bps

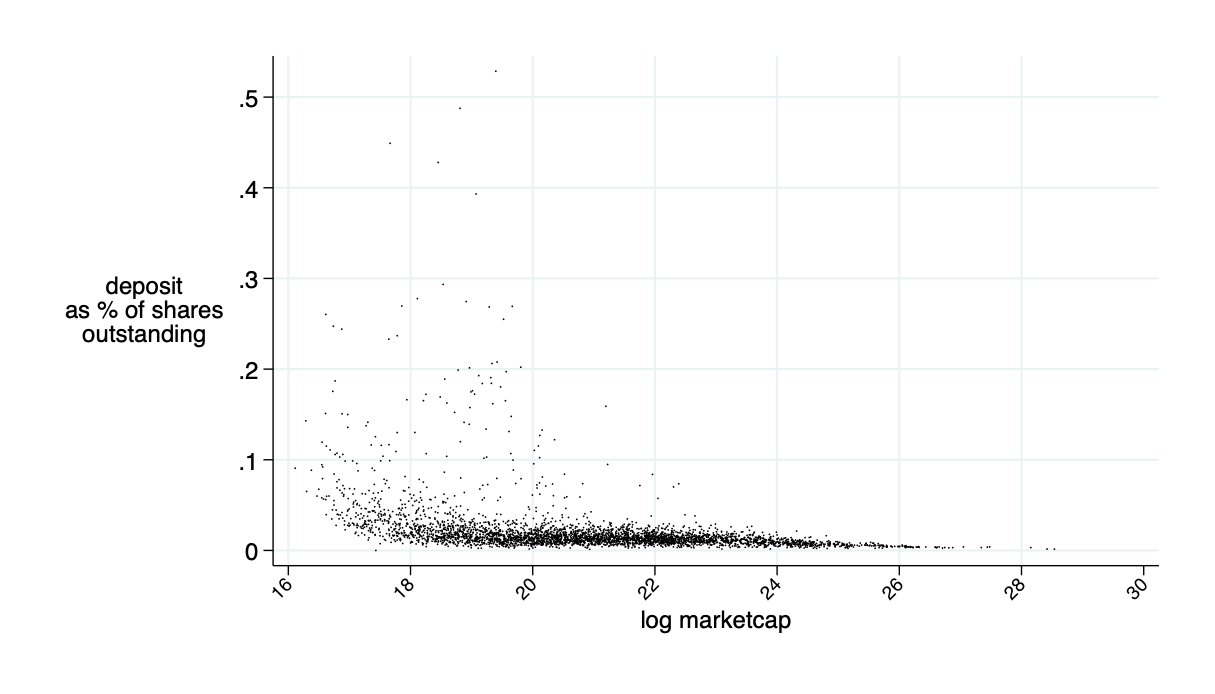

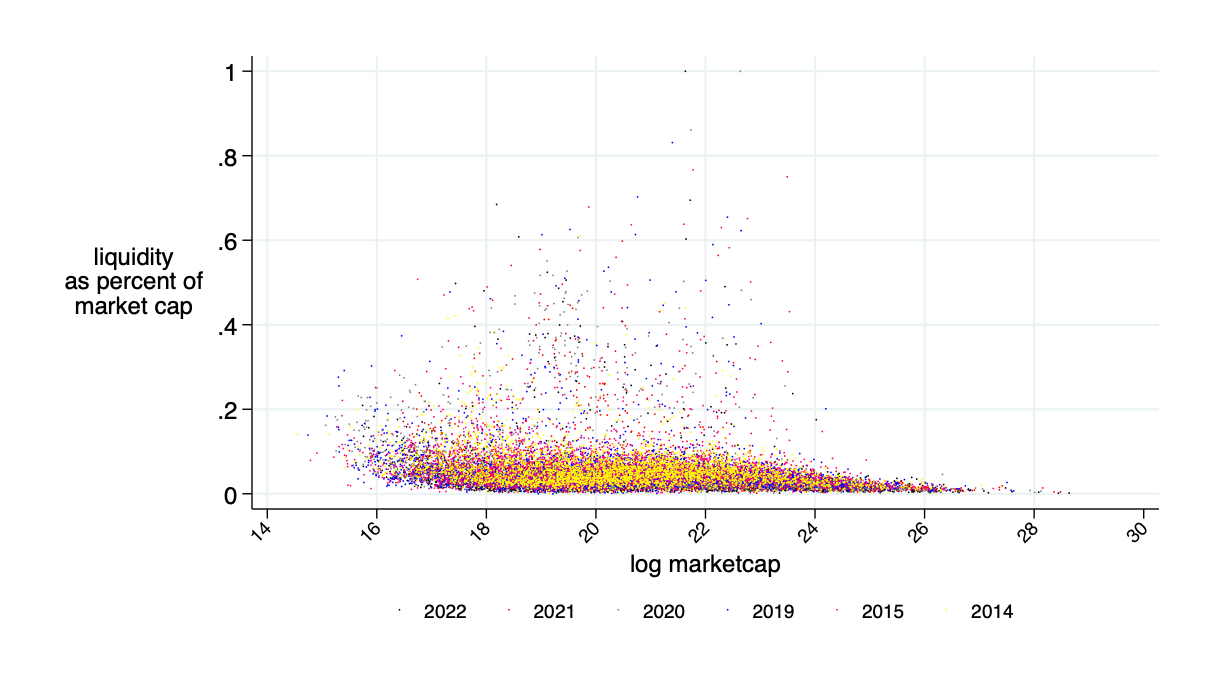

Average of the market cap to be deposited for competitive liquidity provision: \(\bar{\alpha}\approx 2\%\)

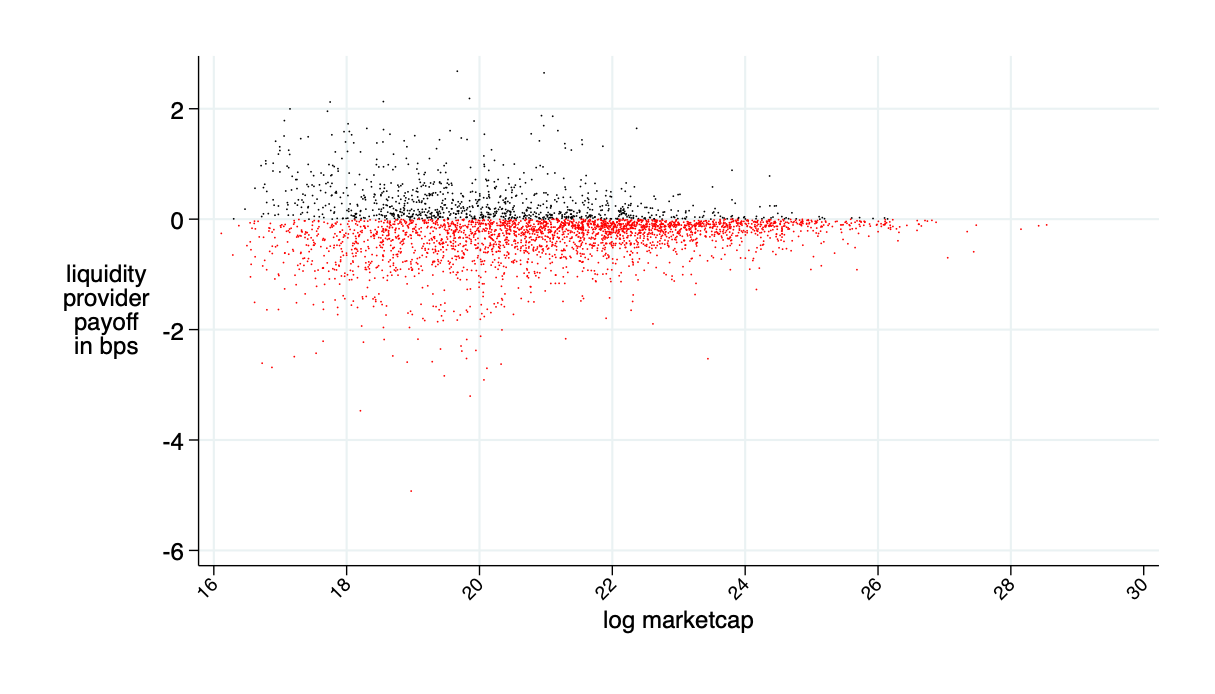

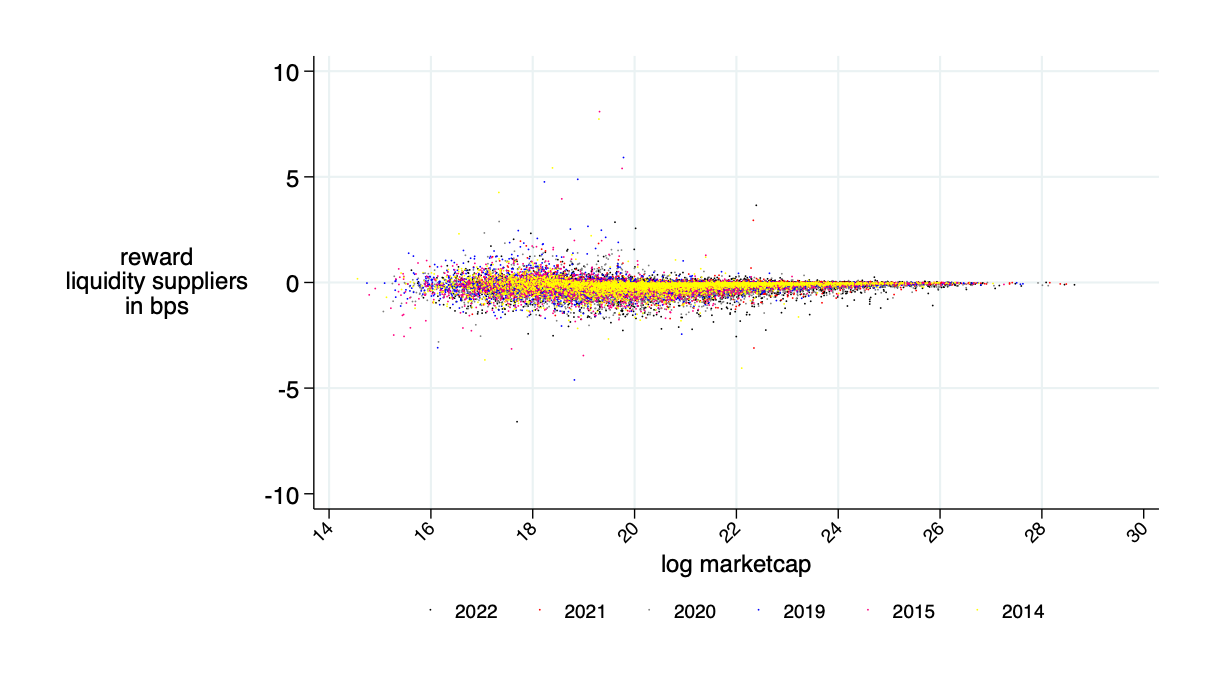

almost break even on average (average loss 0.2bps \(\approx0\))

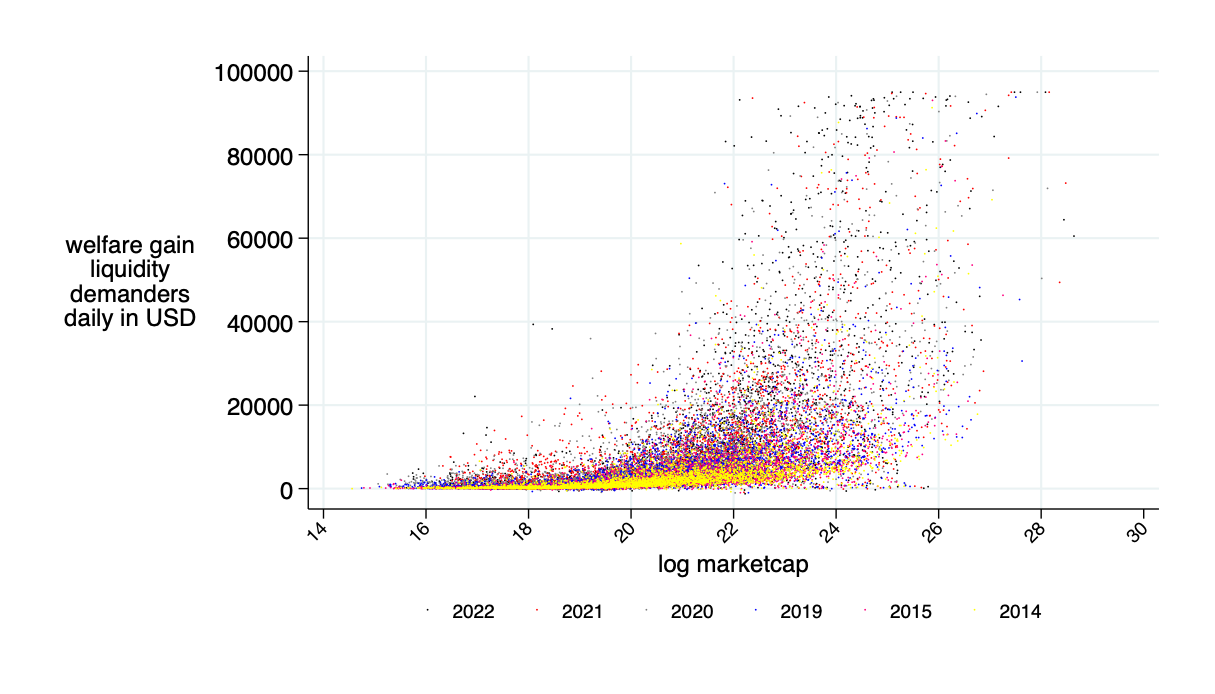

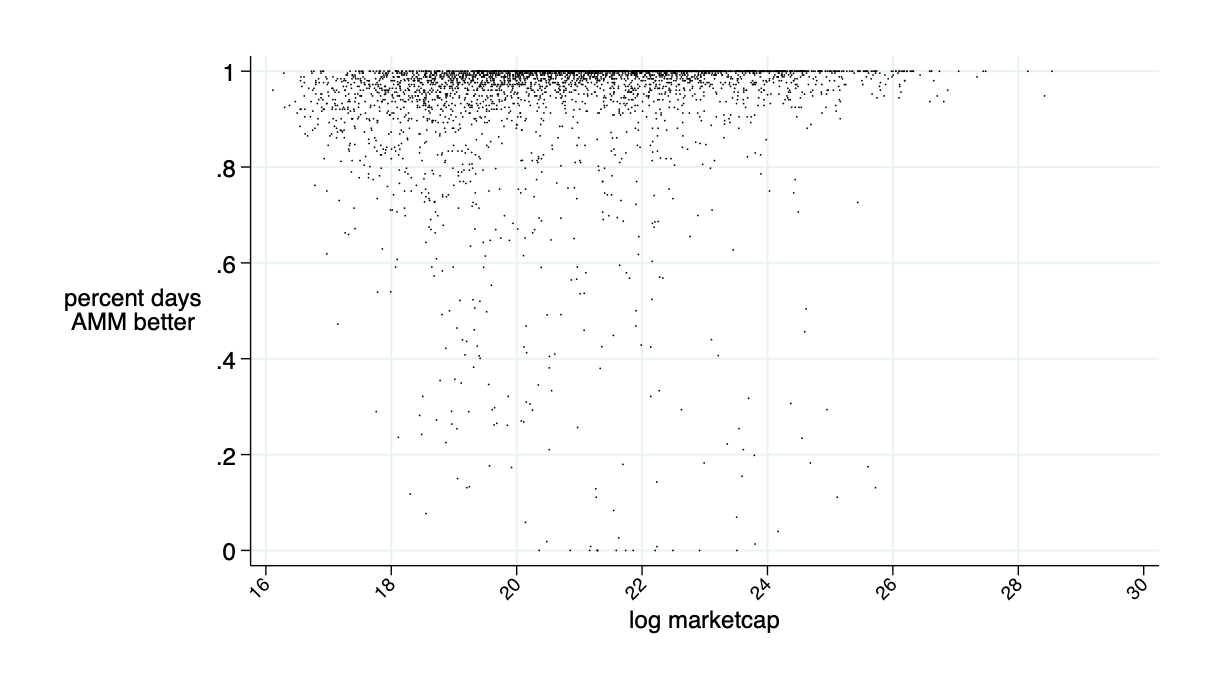

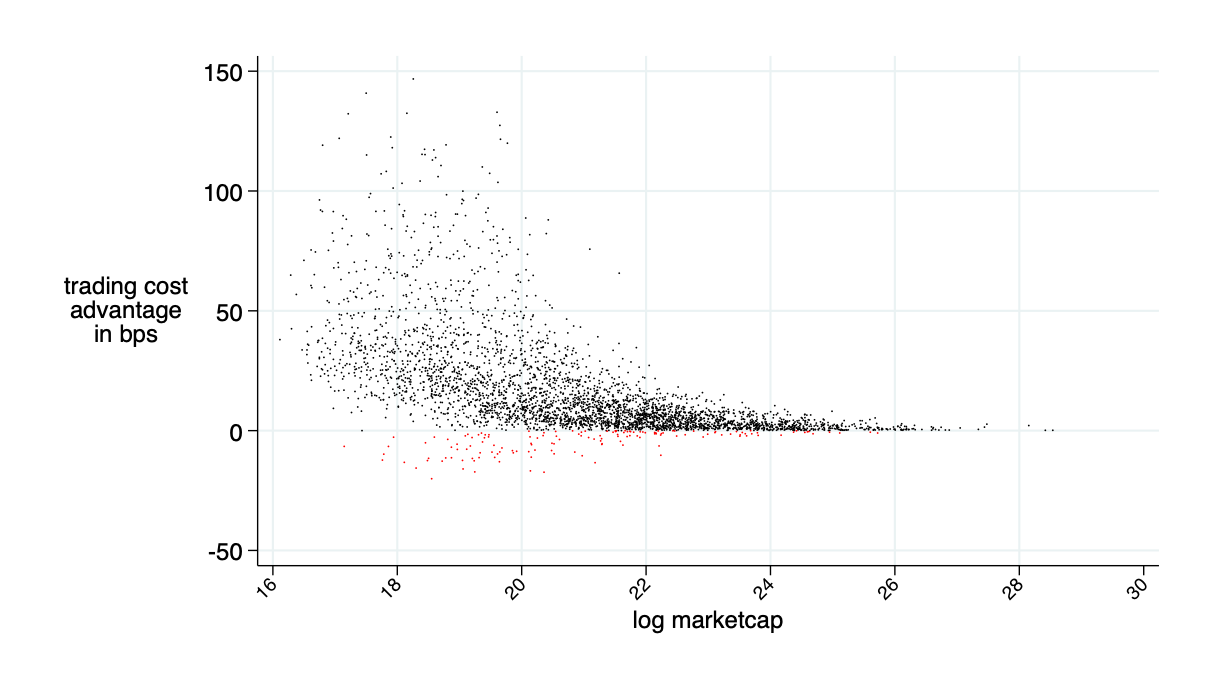

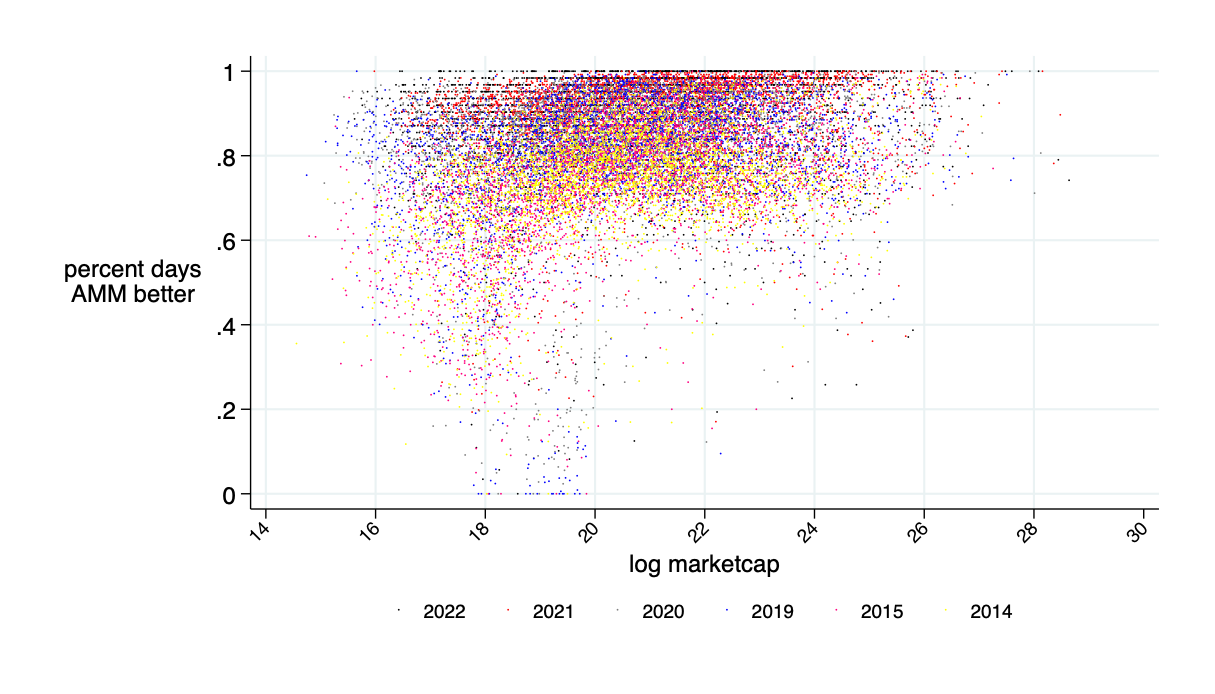

average: 94% of days AMM is cheaper than LOB for liq demanders

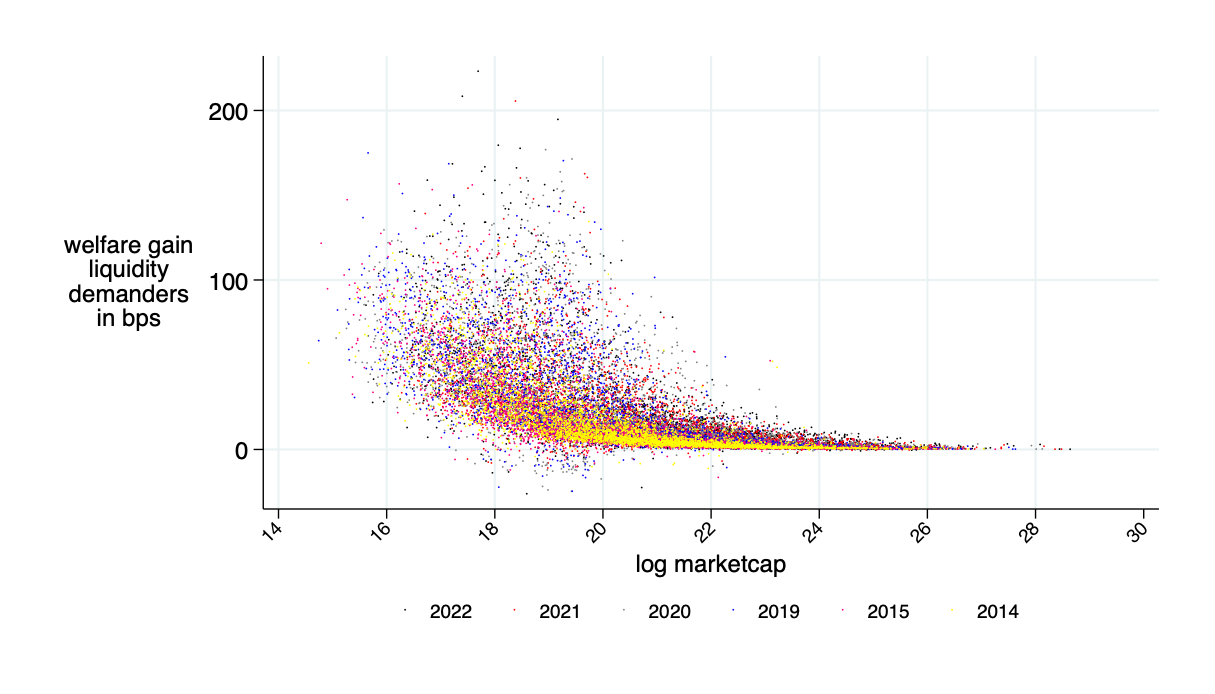

average savings: 16 bps

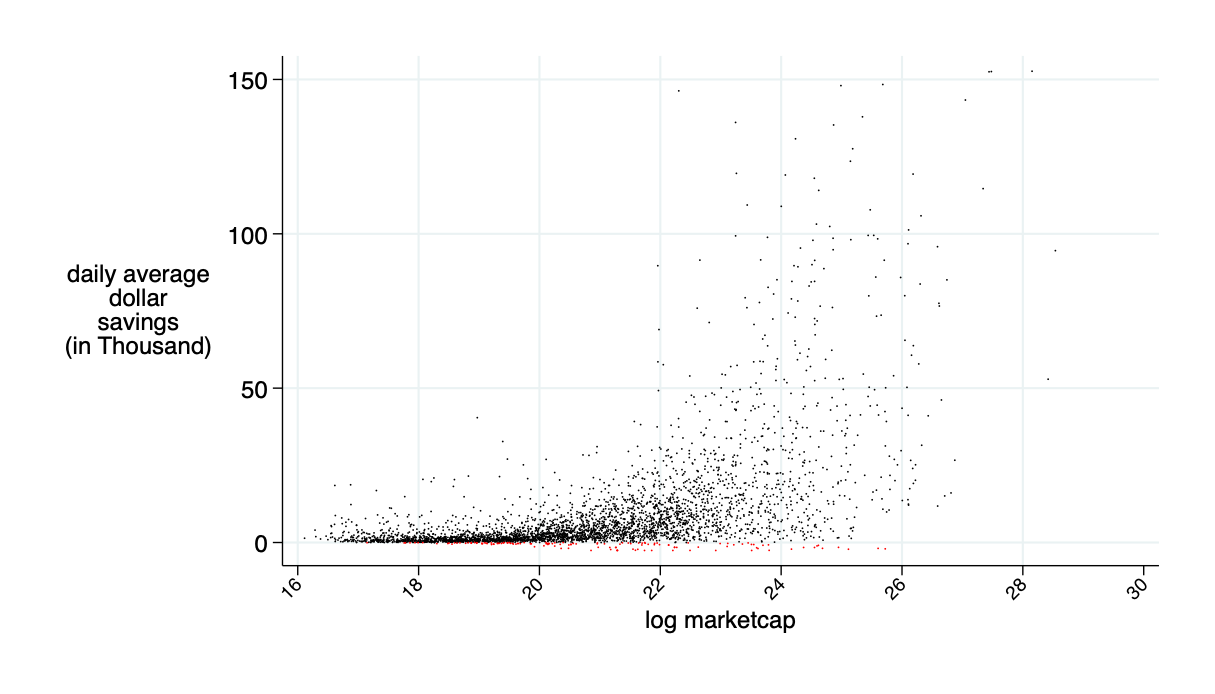

average daily: $9.5K

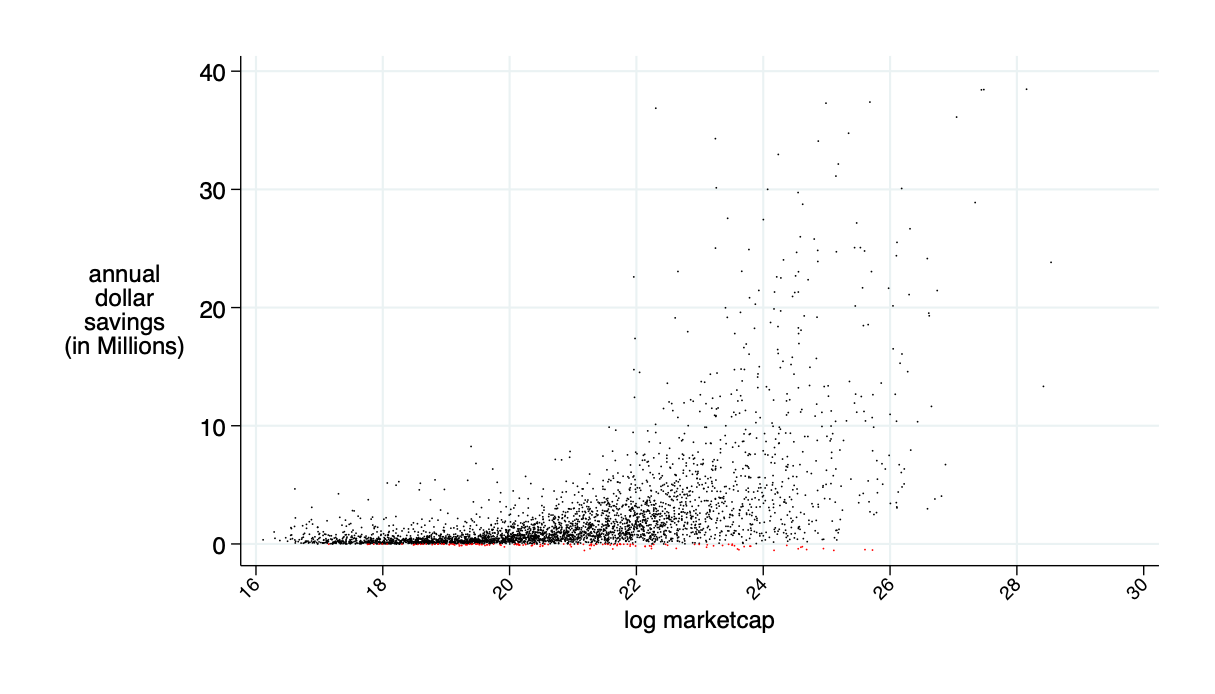

average annual saving: $2.4 million

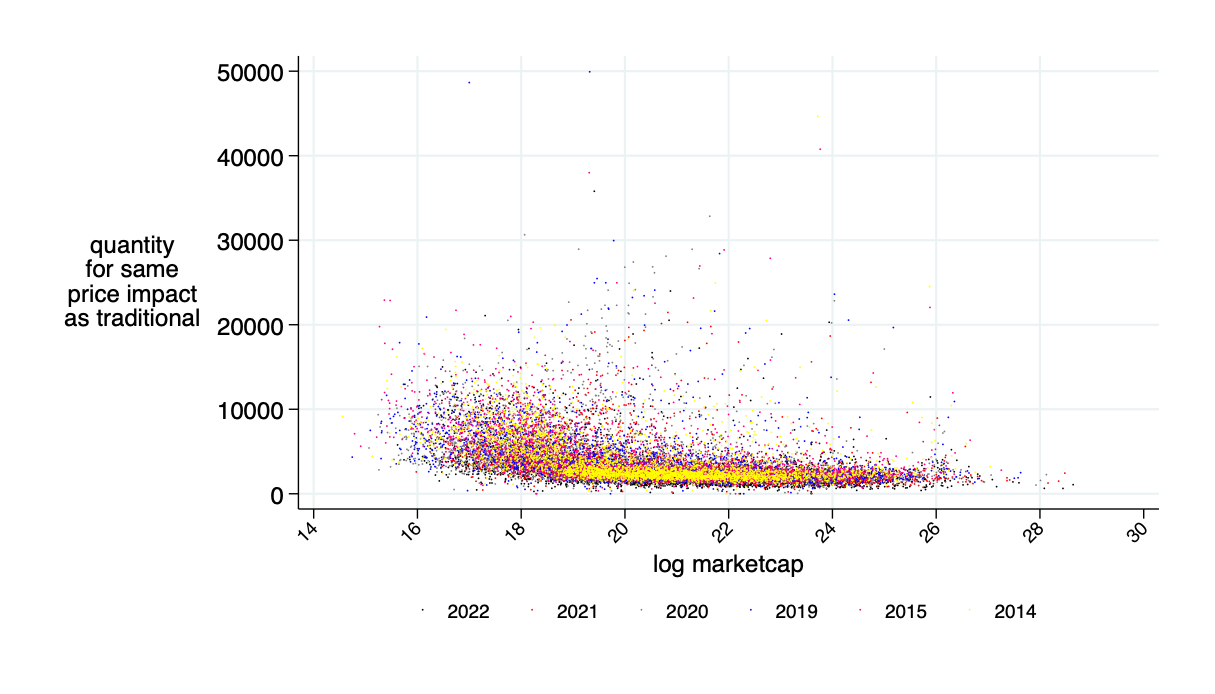

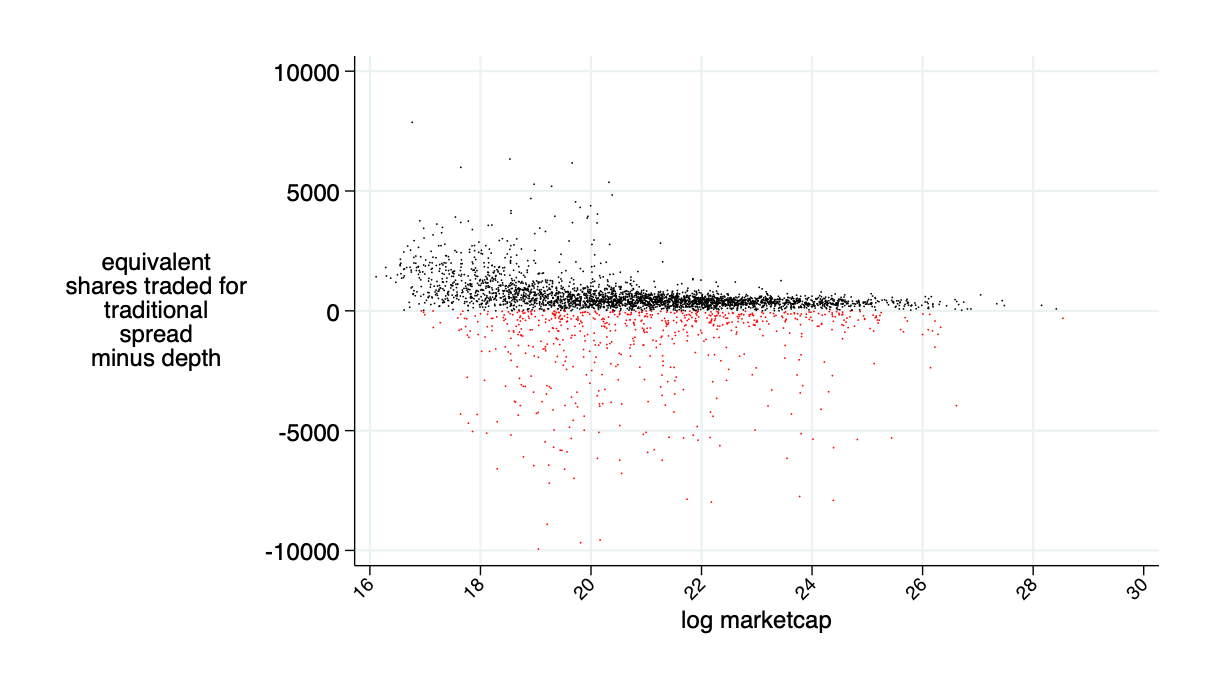

implied "excess depth" on AMM relative to the traditional market

Sidebar: Cash deposit requirements

- Asset provision is not a problem: enough idle liquidity

-

But: AMM requires off-setting cash: \(c =a\cdot p(0)\).

- Cash is not free: at 6% annual rate, 2bps per day.

- Adds to fees

- Several solutions:

- Narrow a range of returns for which to provide liquidity (akin to Uniswap V3) or circuit breakers

- Other mechanisms being developed

- Balancer protocol: same cash for many assets

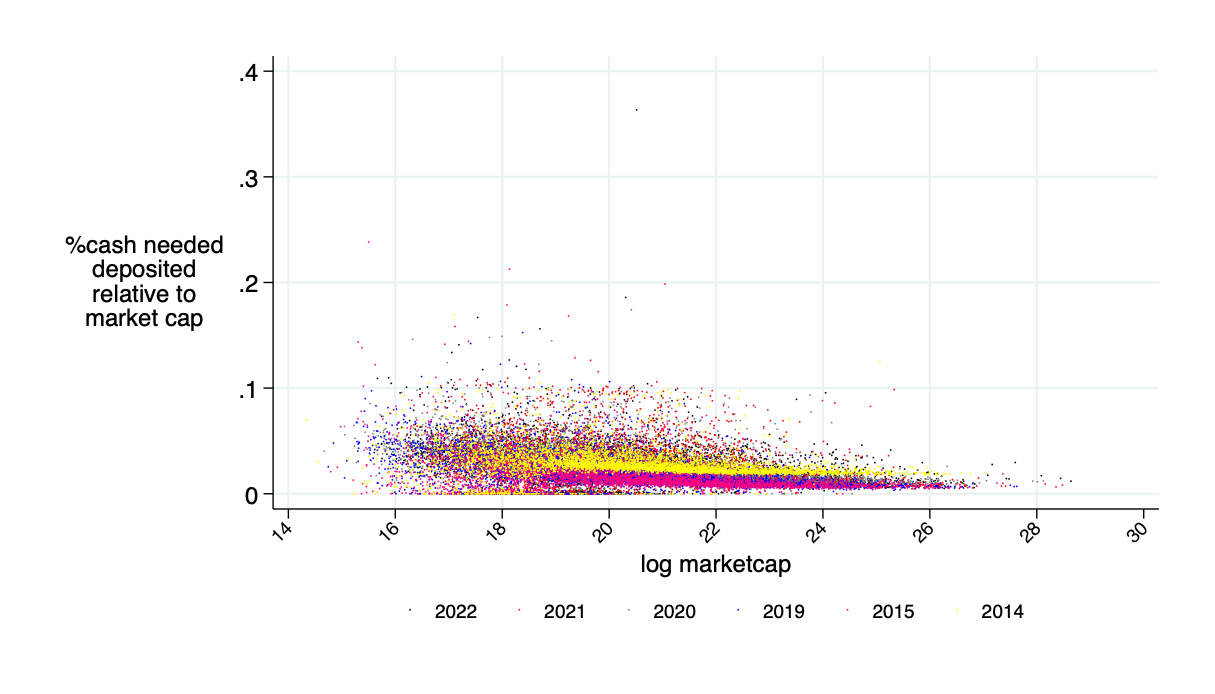

\(\Rightarrow \) Need about 5% of the value of the shares deposited -- not 100% -- to cover up to a 10% return decline

Summary

- AMMs do not require a blockchain - just a concept

- could be run in the existing world (though there are institutional and regulatory barriers)

- Our question:

- Can an economically viable AMM be designed for current equity markets?

- Would such an AMM improve current markets?

- Answers:

- Yes.

- Massively.

- Source of Savings:

- Liquidity providers \(\not=\) Citadel!

- \(\to\) no (overnight) inventory costs

- \(\to\) use idle capital

- \(\to\) + better risk sharing

@katyamalinova

malinovk@mcmaster.ca

slides.com/kmalinova

https://sites.google.com/site/katyamalinova/

Optimal fee \(F^\pi\)

average benefits liquidity provider in bps (average=0)

Insight: Theory is OK - LP's about break even

\(\overline{\alpha}\) for \(F=F^\pi\)

Need about 10% of market cap in liquidity deposits to make this work

actually needed cash as fraction of "headline" amount

Only need about 5% of the 10% marketcap amount in cash

AMMs are better on about 85% of trading days

quoted spread minus AMM price impact minus AMM fee (all measured in bps)

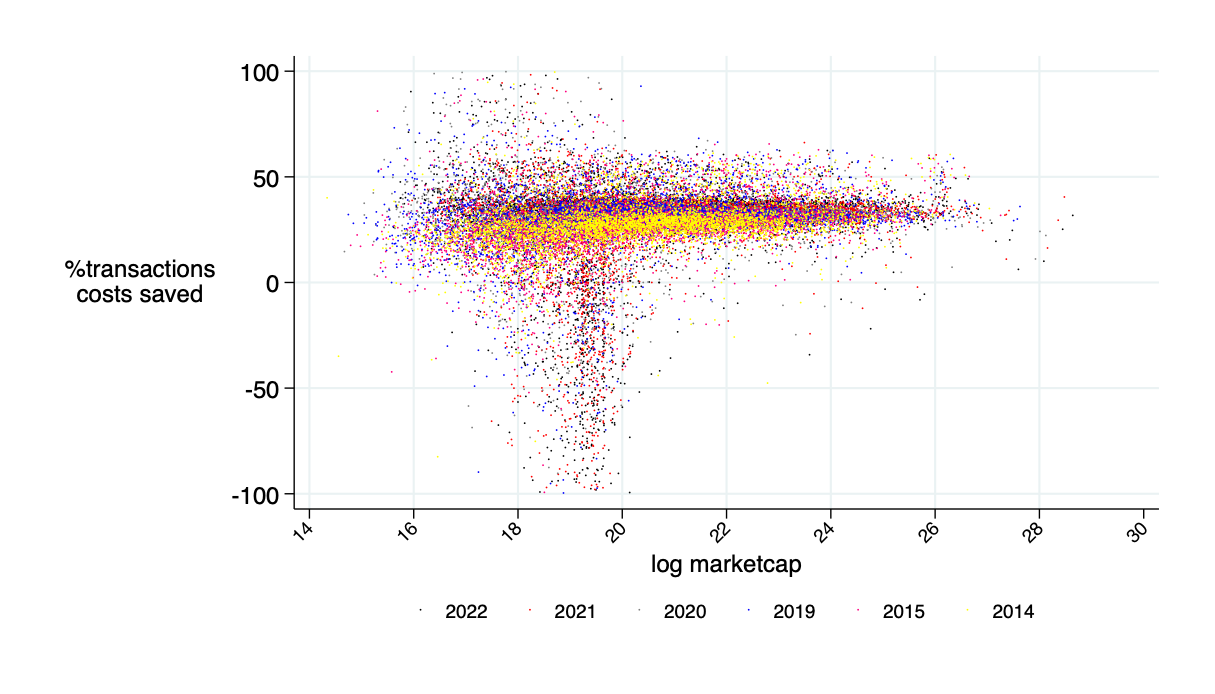

relative savings: what fraction of transactions costs would an AMM save? \(\to\) about 30%

theoretical annual savings in transactions costs is about $15B