Intro to FinTech

MBA F741

Payments Part II

Instructor: Katya Malinova

Lectures 6-7

Feb 13

Plan for today: Payments

- Finish up the "history"

- The basics of the existing payment system

- Innovations in payments (will probably spill over to Lecture 7)

History of Money (Last time)

barter

coins/commodity money

paper money

fiduciary money

Fiduciary Money

Problems?

-

Time-consuming to move/process cheques

-

No immediate use of funds

-

Costly to process paper cheques

Cheques, Drafts ... "payment from an account"

Electronic forms of fiduciary money:

- debit cards

- credit cards

- pre-paid card

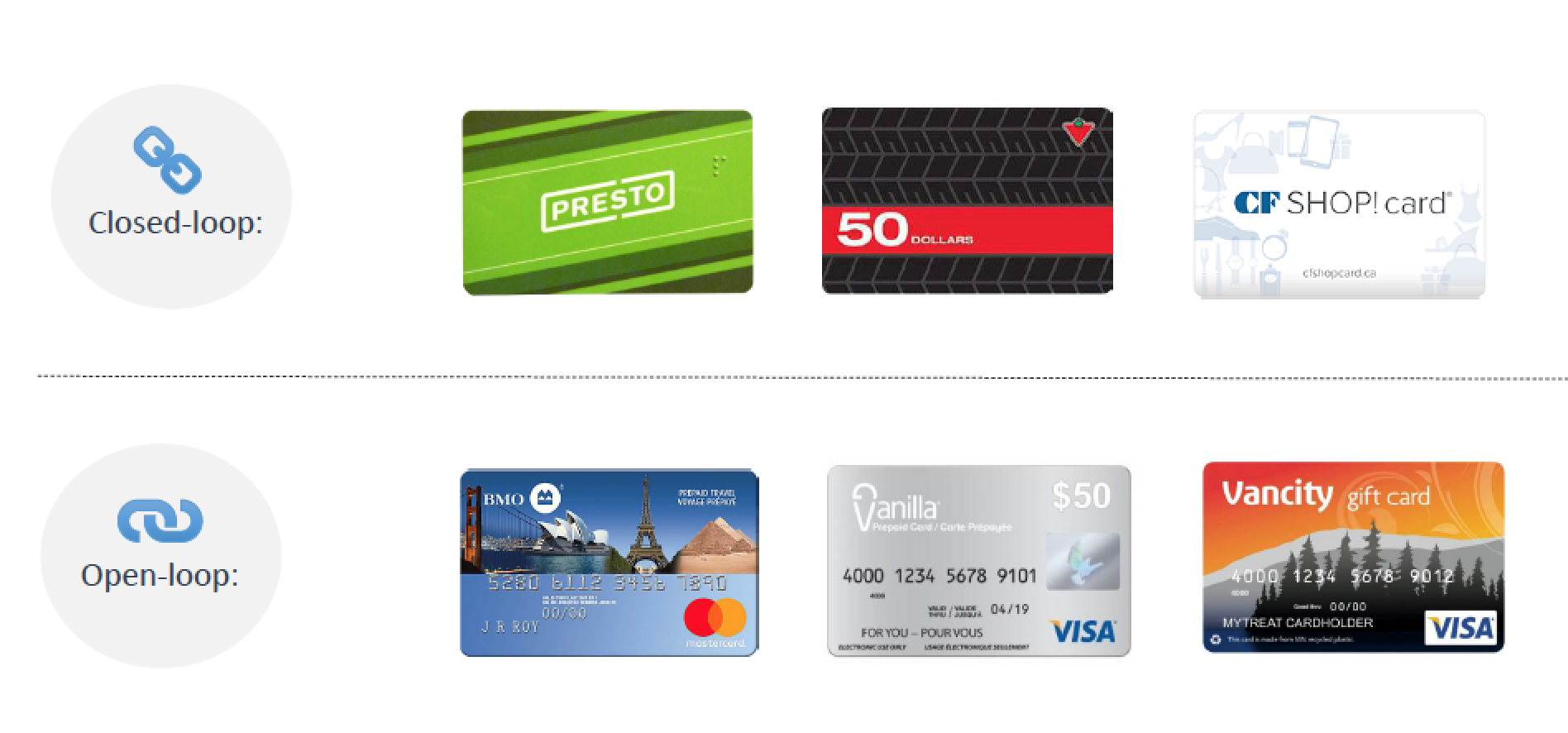

Prepaid Cards: Different Forms

Payment Basics ....

Who do you have a relationship with?

-

Visa?

-

CIBC?

What about the merchant?

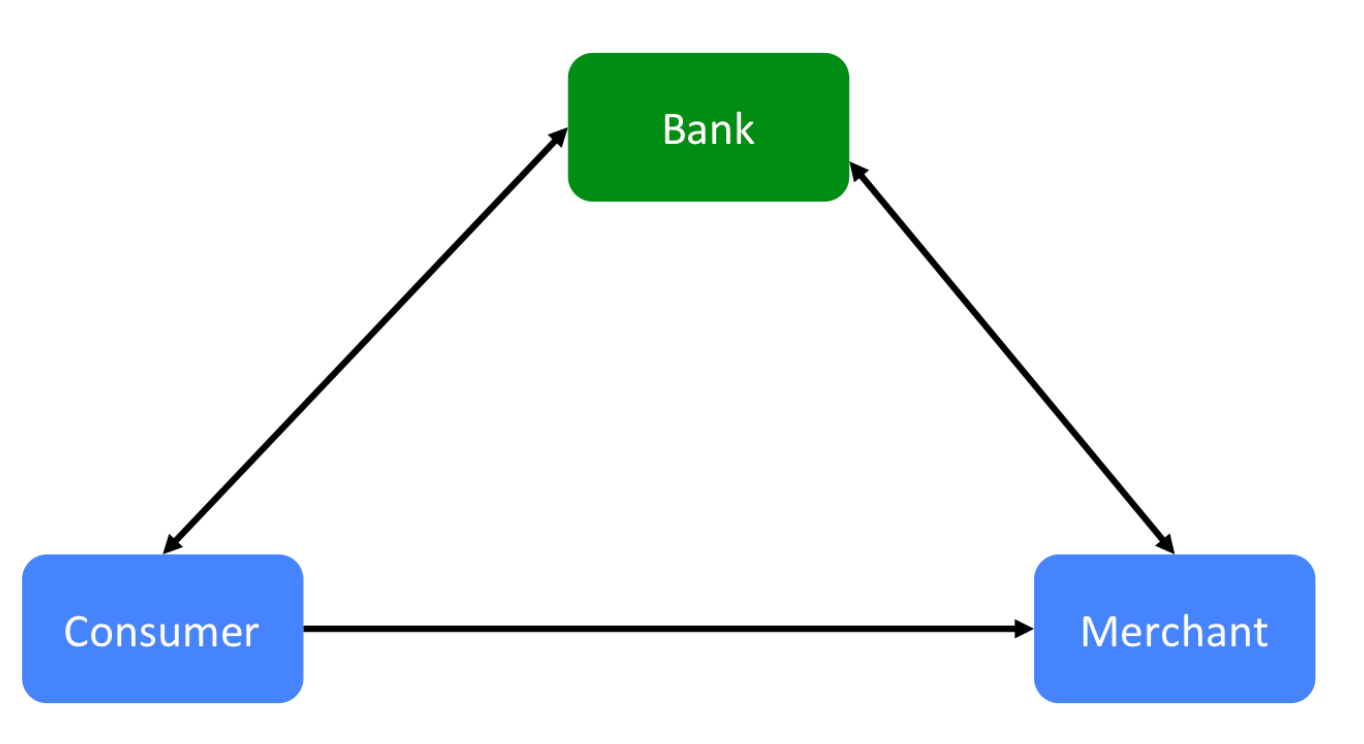

Payment Basics .... before the Visa & Mastercard...

Imagine you run a bank

Wouldn’t it be great if your customers could go to local shops and “charge” their purchases to an account that you hold for them?

Make money offering credit to the customers and make some more money charging the merchants for providing this service.

Bank of America in 1950s

Foresee any problems?

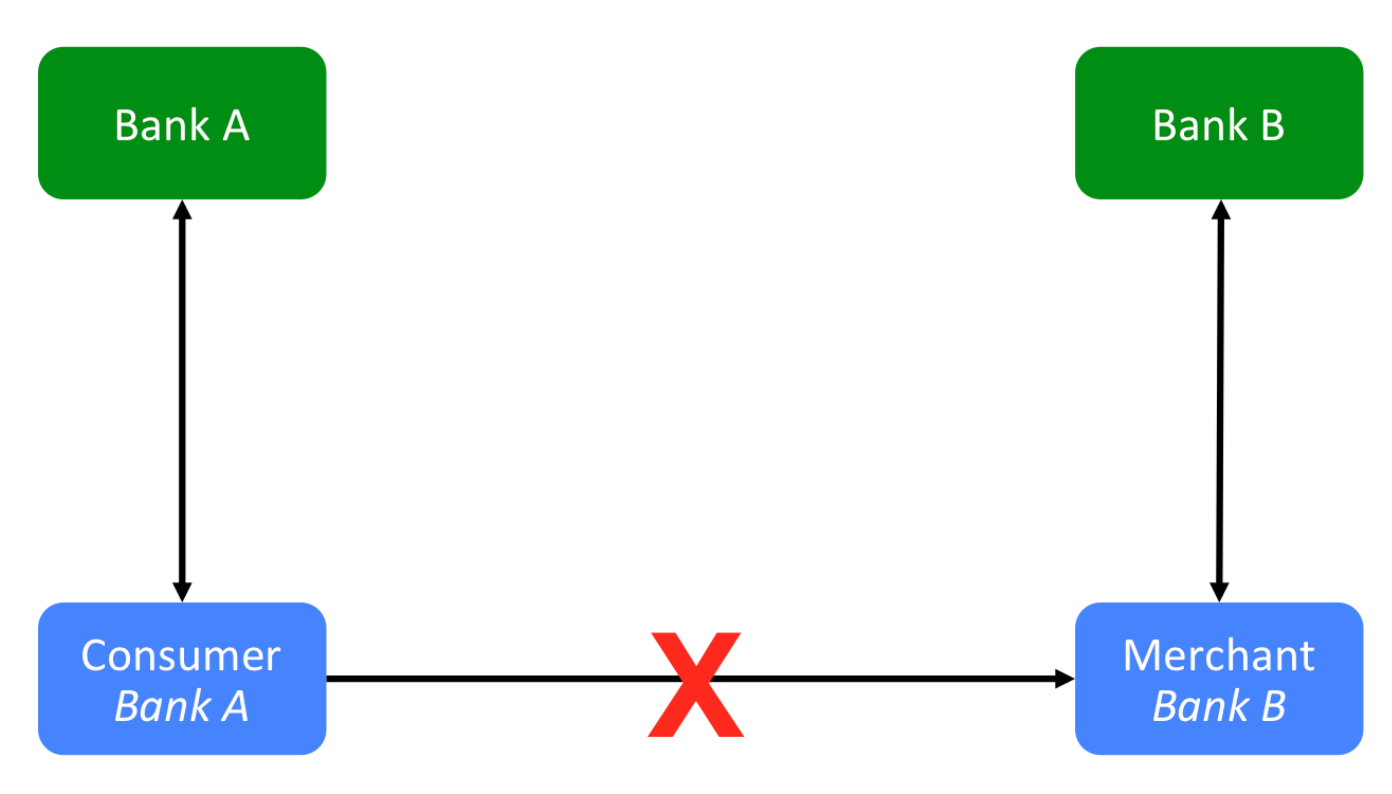

Payment Basics .... before the Visa & Mastercard...

https://gendal.me/tag/payments/

Payment Basics .... before the Visa & Mastercard...

Payment Basics .... Clever insight

Cards "business"

= TWO businesses

Business #1: offering credit to customers & processing their payments

CARD ISSUING

Business #2: enabling merchants to accept card payments & to get reimbursed

MERCHANT ACQUIRING*

*The card payment = a receivable that the processor acquires from the merchant

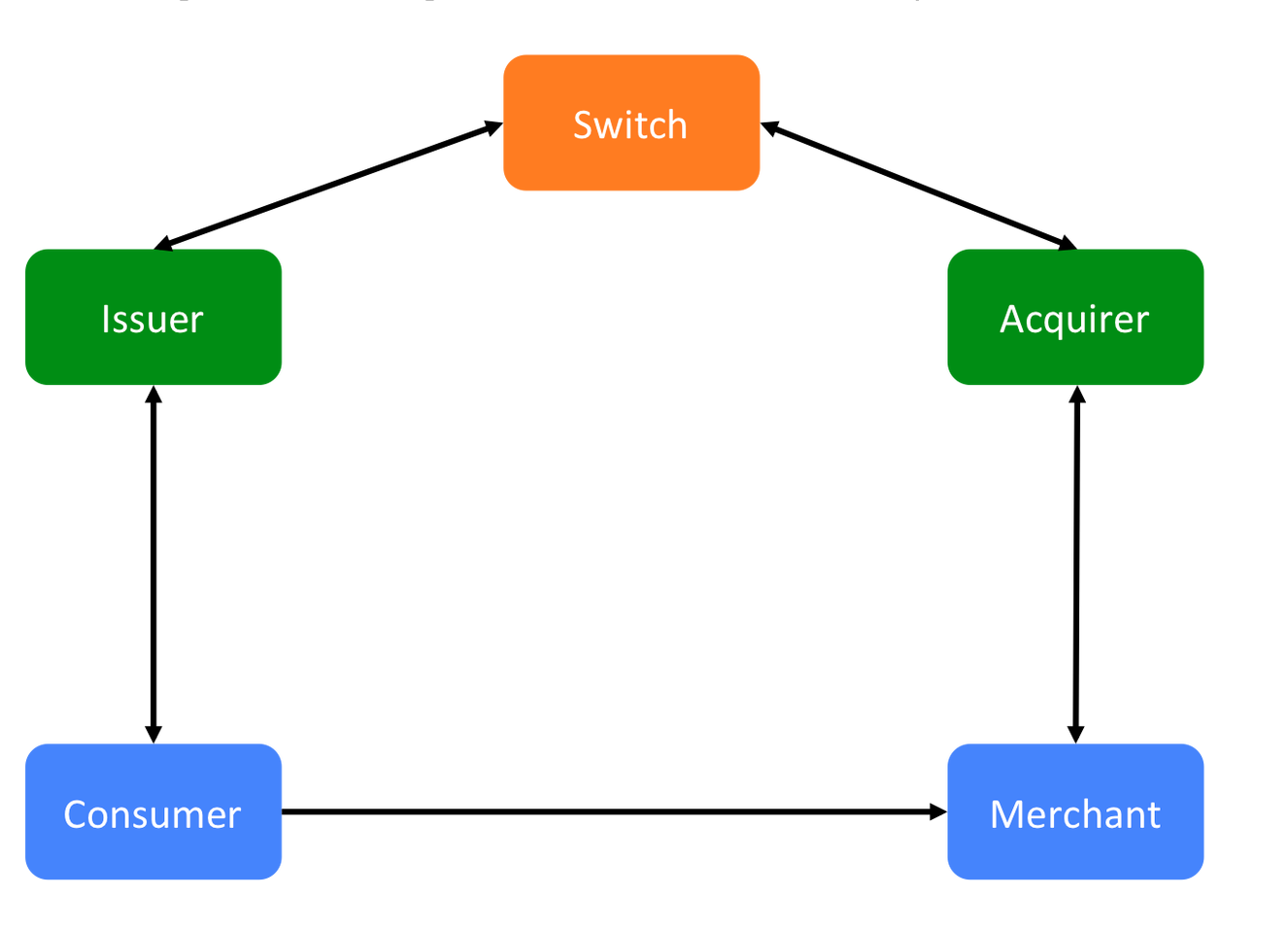

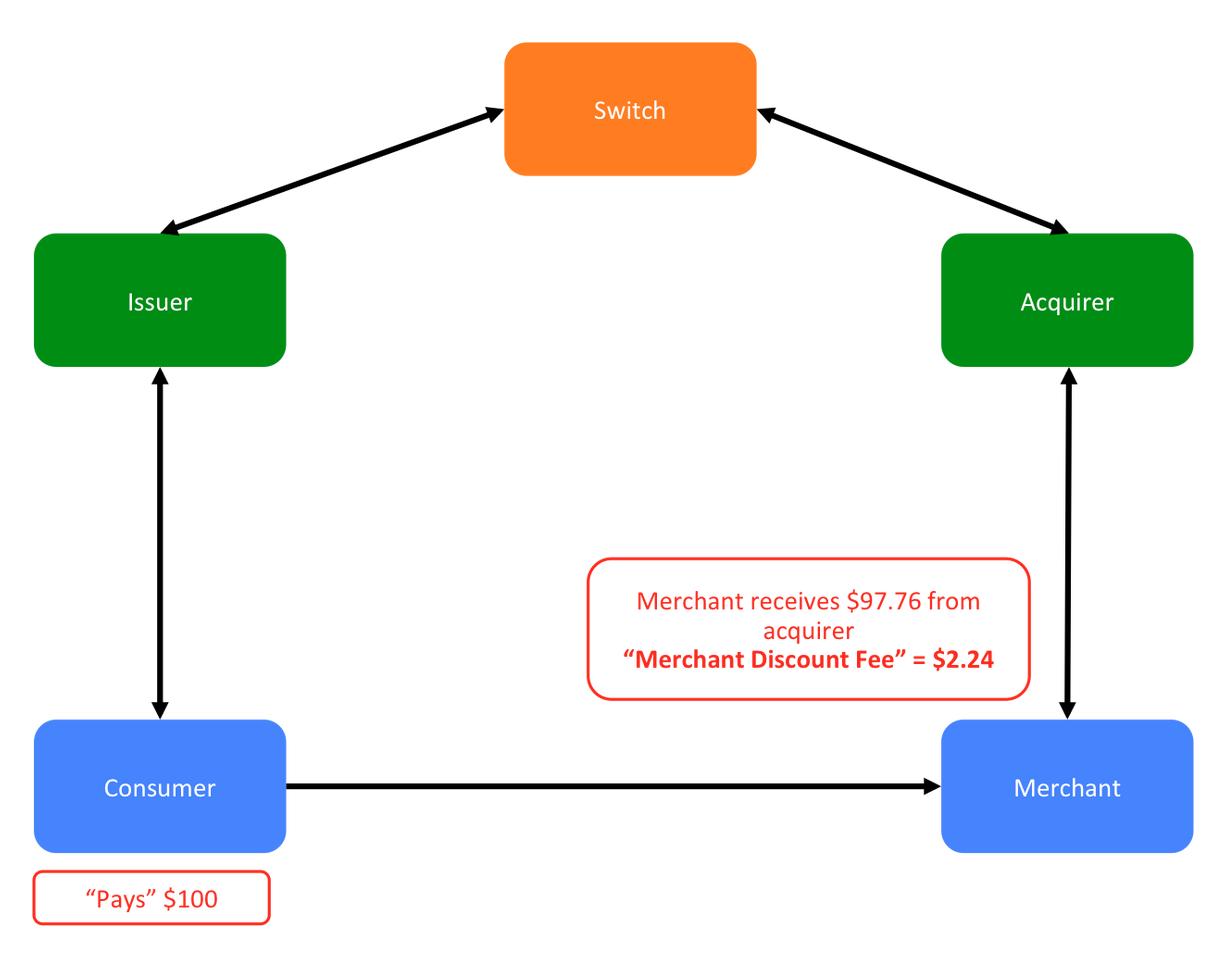

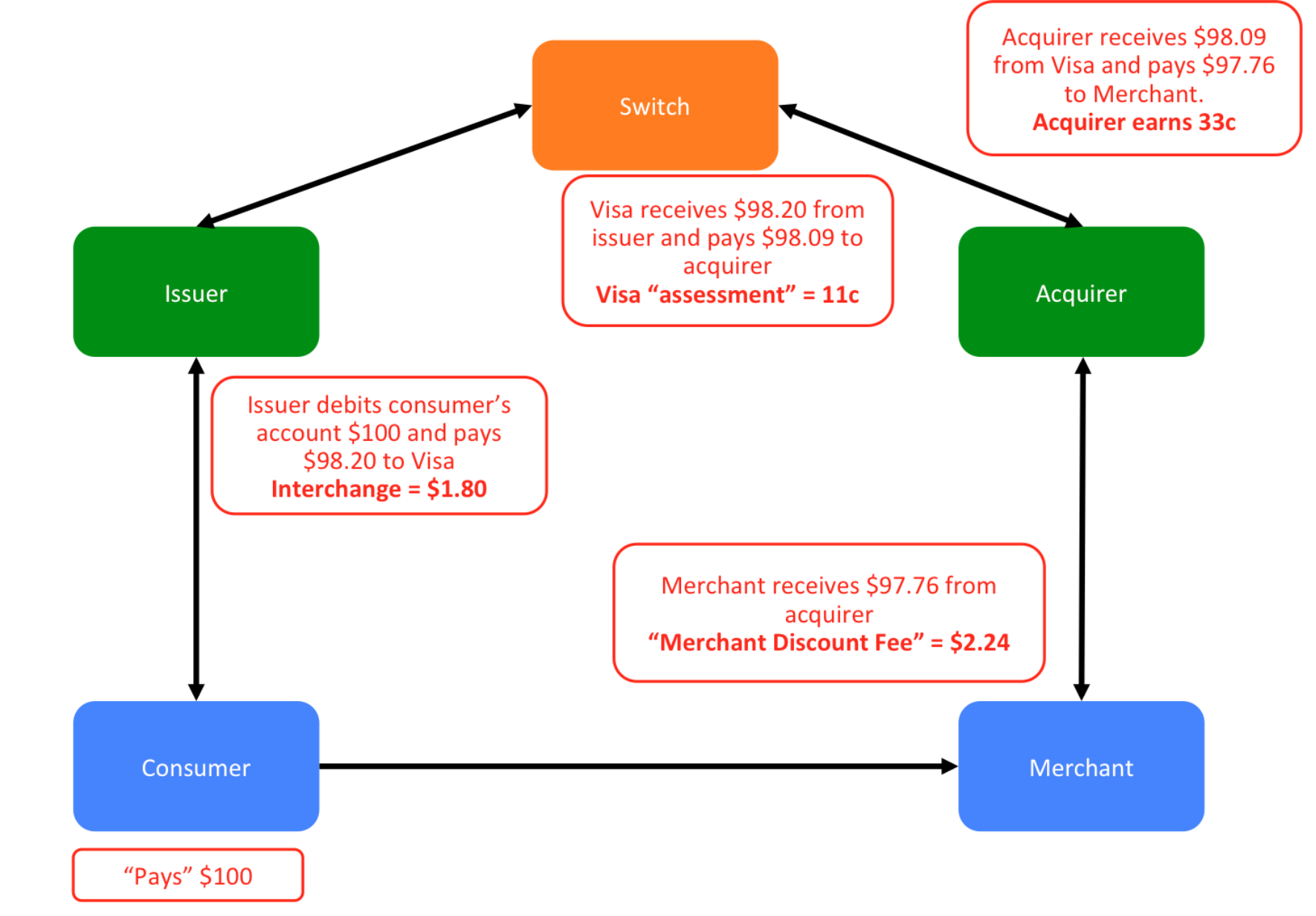

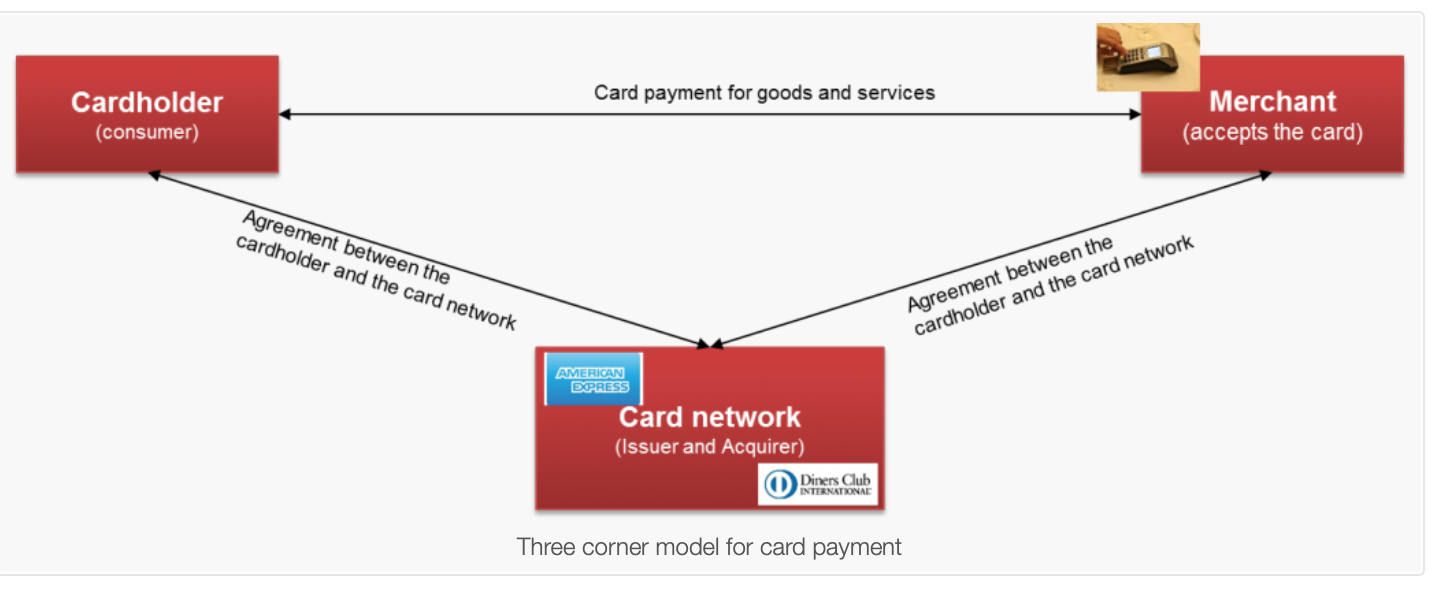

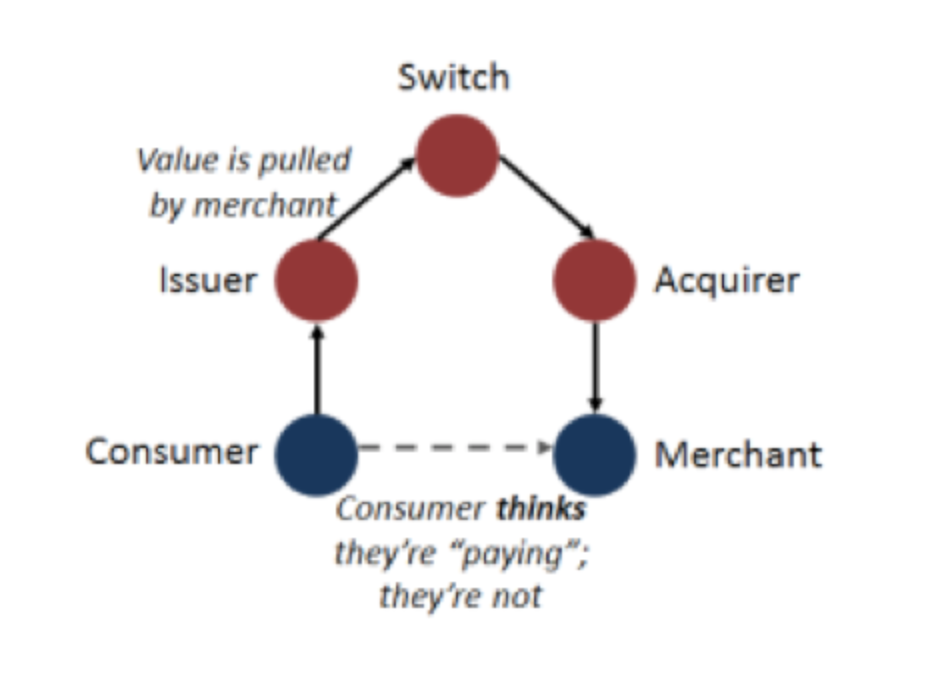

Payment Basics .... 4-party model

Or: Payment Processor

Switch = set of rules + brand recognition for the merchants and customers that are members of this arrangement

Payment Basics .... 3-party model

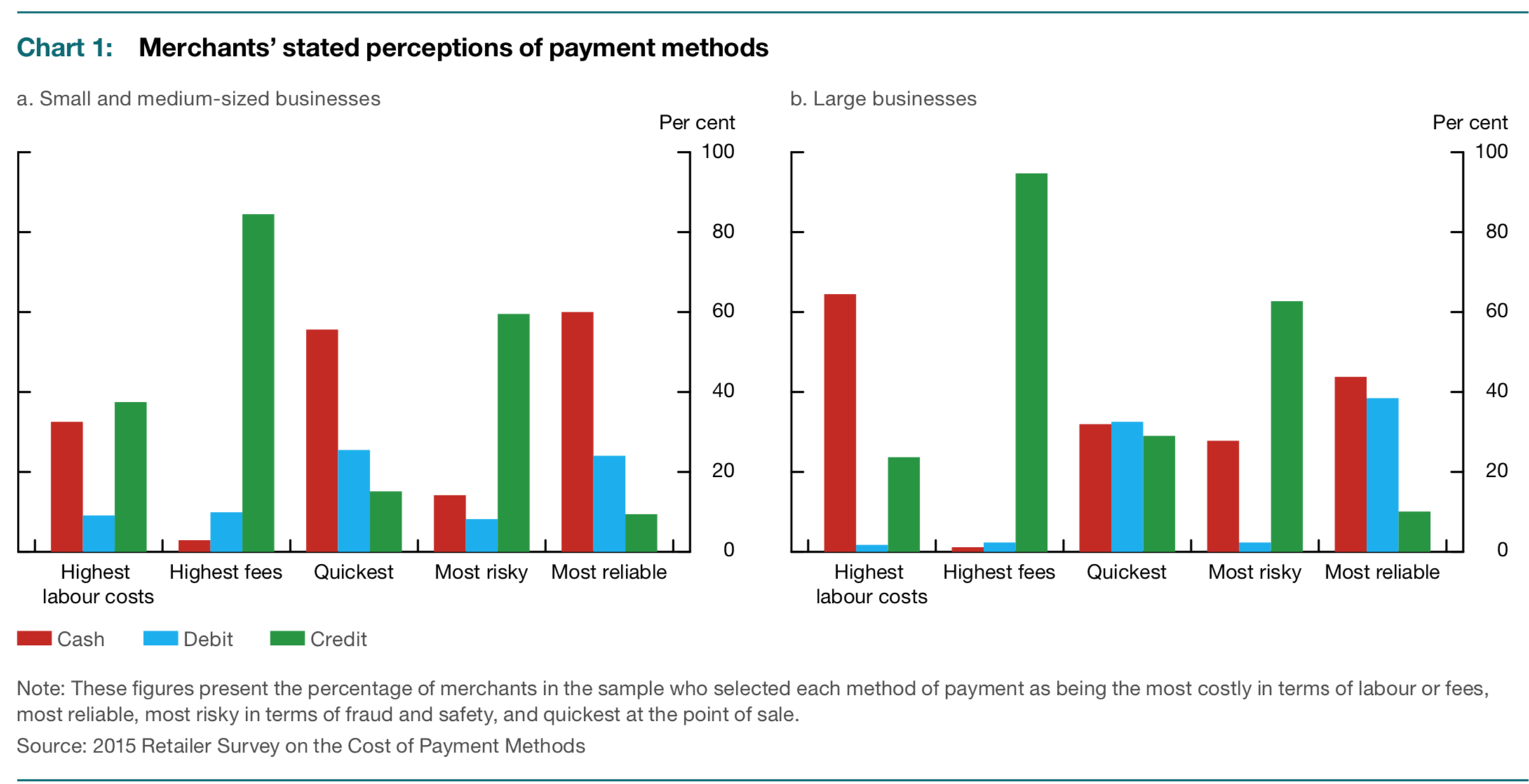

For more info on the fees

https://www.visa.ca/en_CA/support/small-business/interchange.html

https://www.cardfellow.com/blog/credit-card-processing-fees/

https://www.costcopaymentprocessing.ca/index.html

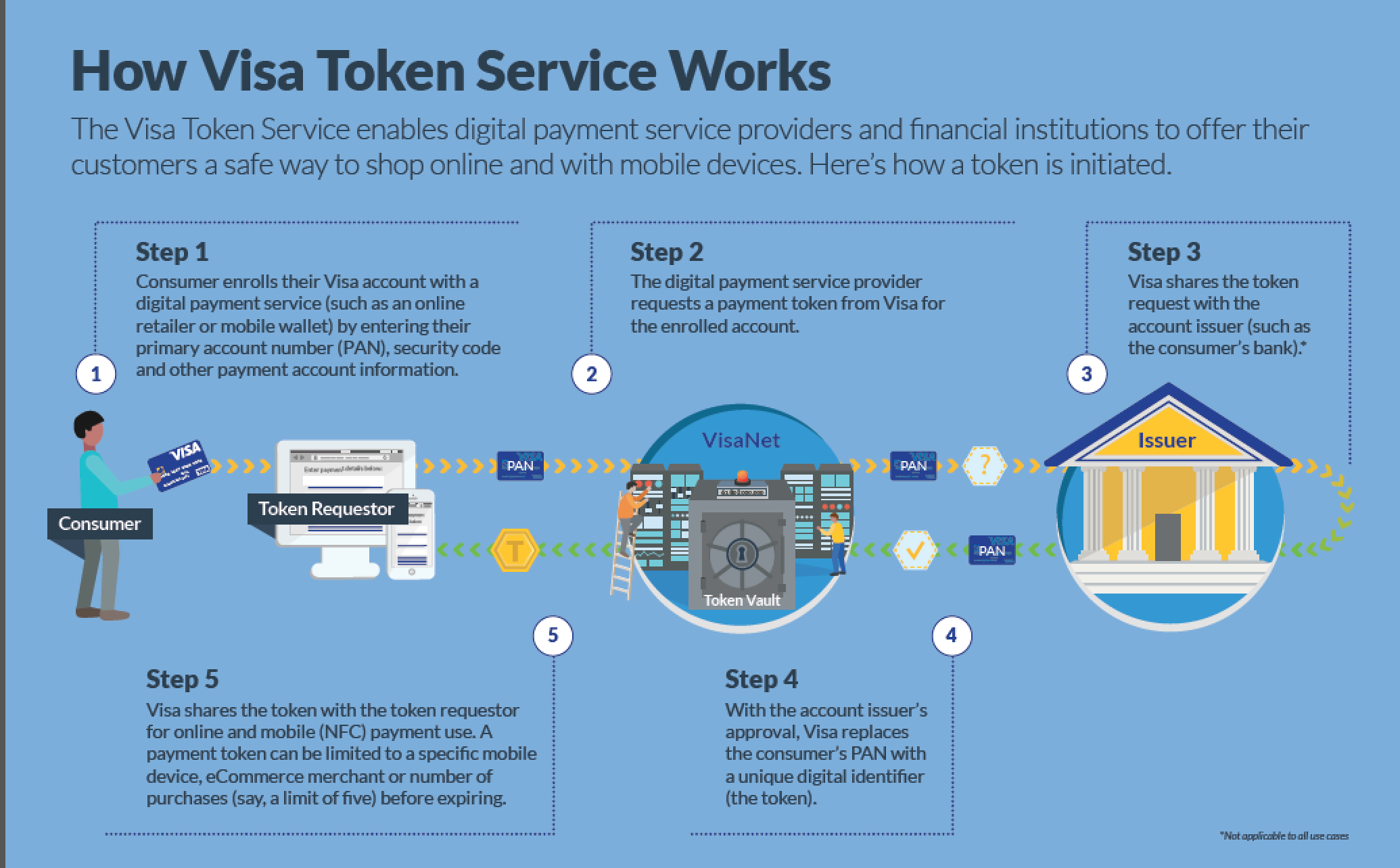

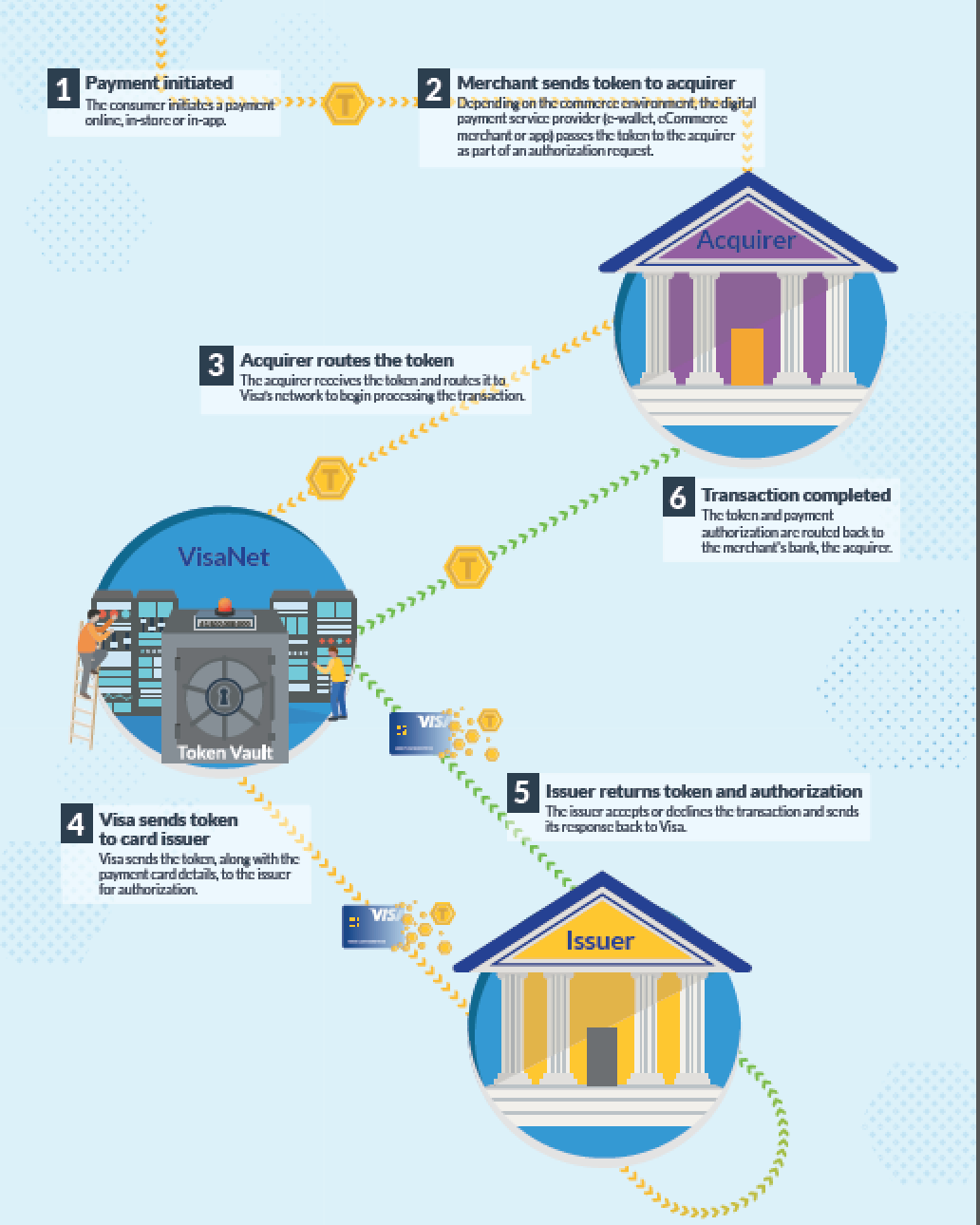

Push vs. Pull & Tokenization

Push vs. Pull & Tokenization

Push vs. Pull & Tokenization

When you allow a merchant to store your credit card details on file, you must trust all these actors "not to mess up" ...

Push vs. Pull & Tokenization

Tokenization Example: Visa Services

https://www.bhartipay.com/payment-tokenization-benefits

Let's return to discussing innovation in payments

What do we want from payments?

fritctionless

fast

open/expandable

cheap

secure

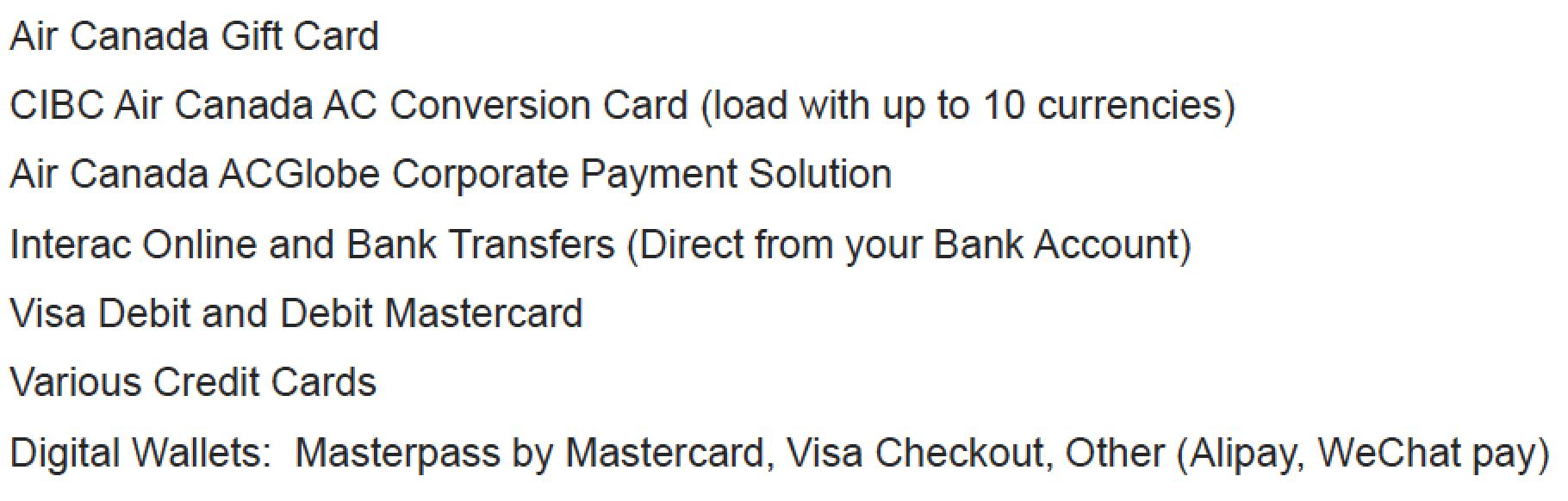

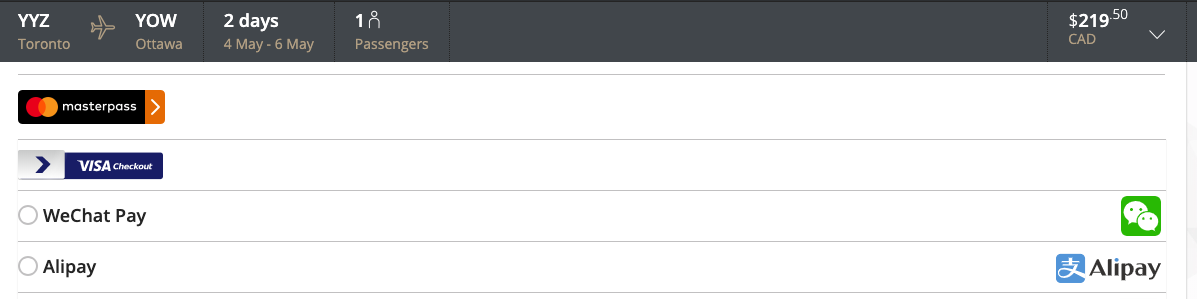

Trends? Example: Air Canada Accepted Payments

https://www.aircanada.com/ca/en/aco/home/book/payment-methods.html

What does Air Canada NOT accept (at least, not everywhere?)

CASH!

Are we becoming a cashless society? Should we?

Should we become cashless? (Discussed much of this in lectures 1-2!)

- Time savings

- Money savings

- Reduce frictions

- Reduce crime (?)

- ??

- Security/system failure concerns

- Access for everyone?

- Financial literary

- Privacy

- Loss of anonymity(?)

- ??

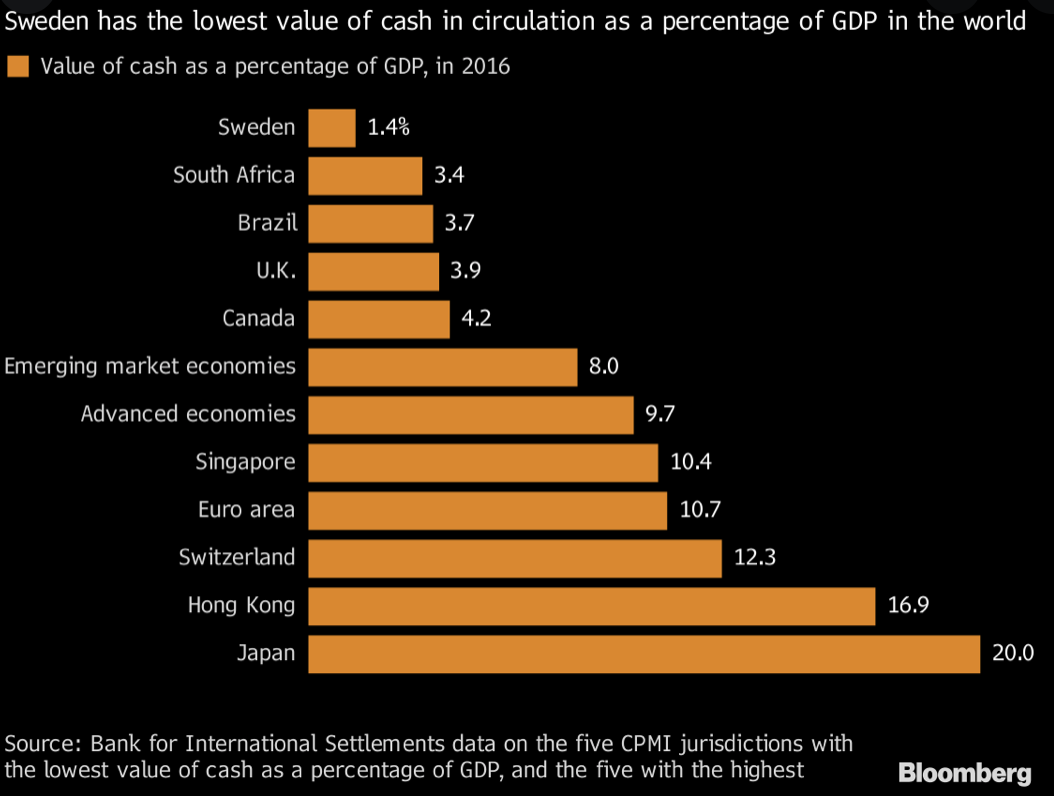

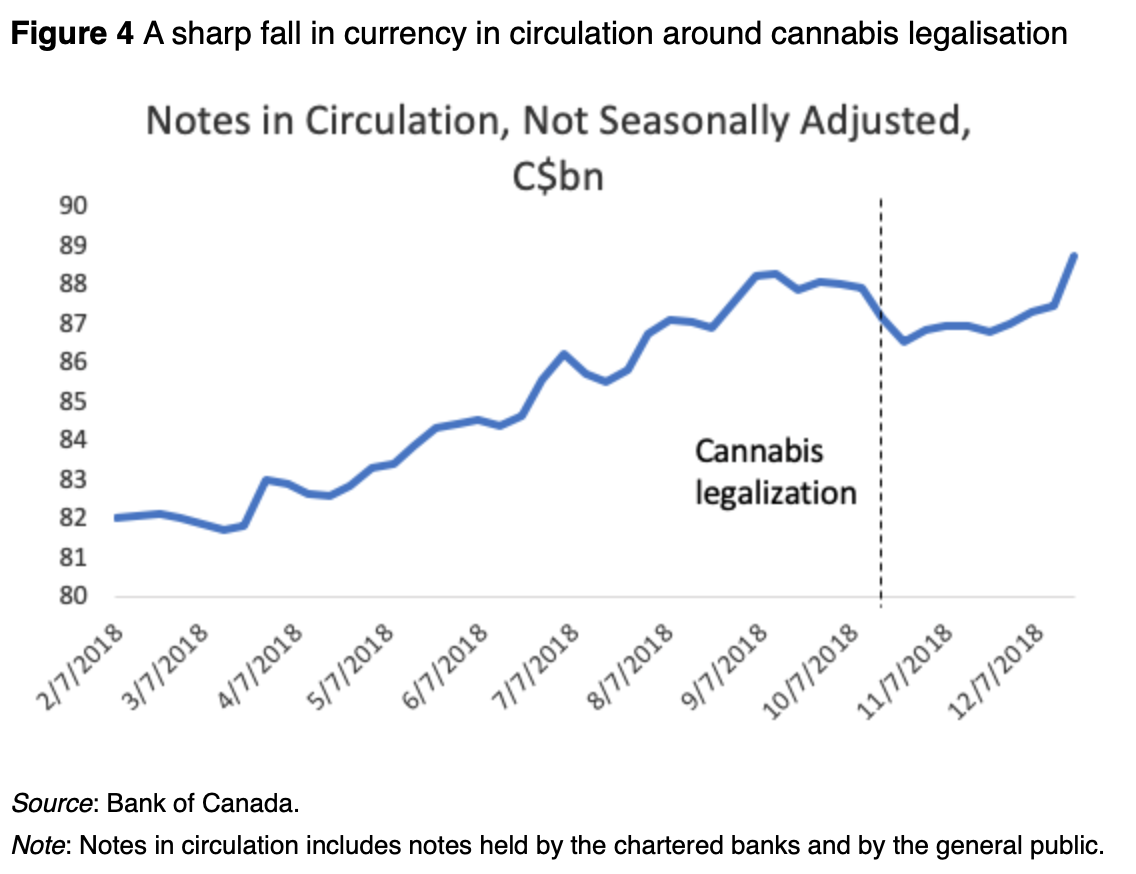

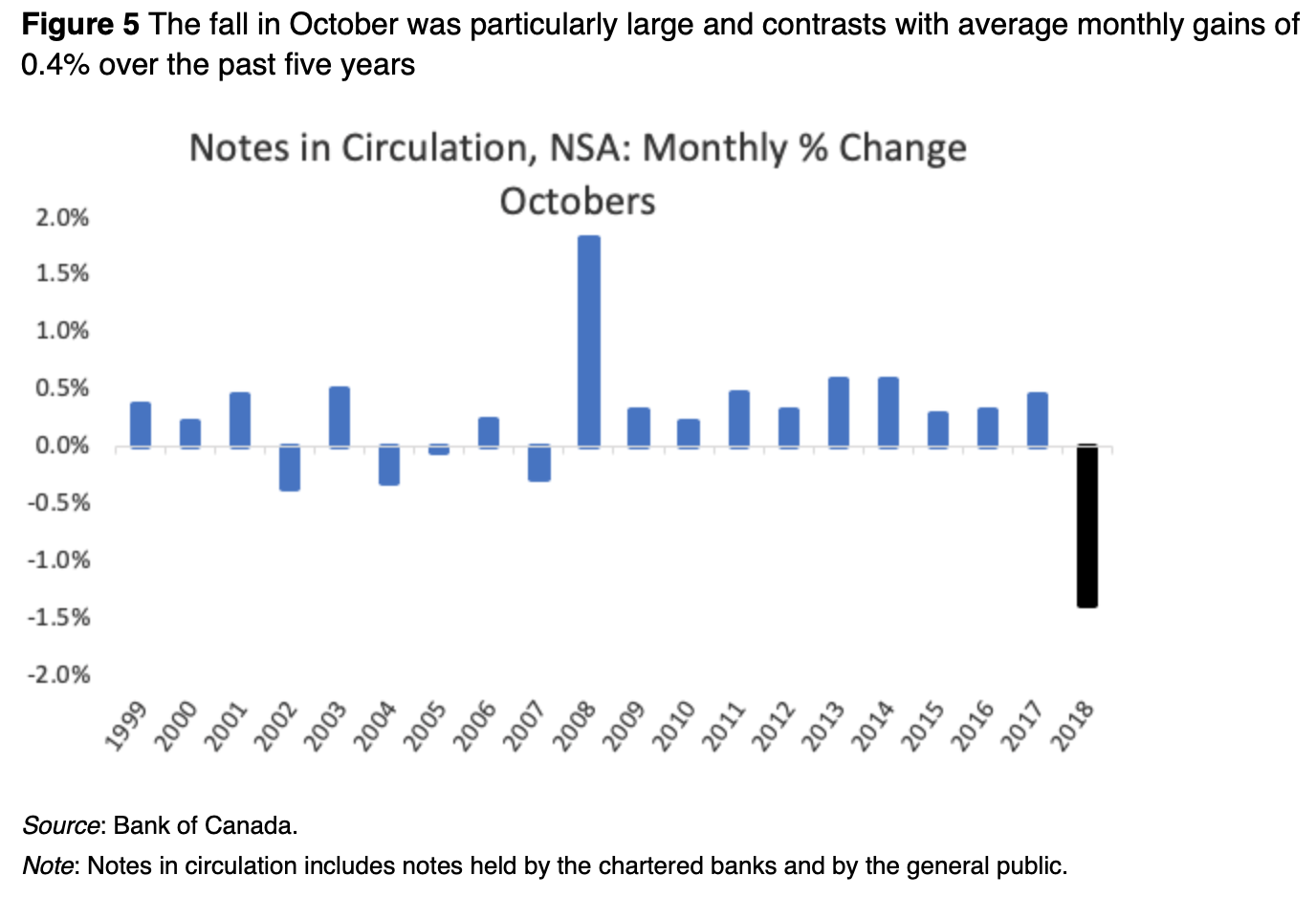

Cash and drugs: Cannabis legalization in Canada

Cash and Drugs

Pablo Escobar

80% of cocaine in the US

- accountants made allowances for the 10 percent that would rot via water damage or be consumed by rats

- US$1,000 per week purchasing rubber bands to wrap the stacks of cash

El Chapo:

$14 billion in drug profits

- private jet (to) pick up the cash at the border and fly it back to Mexico City ...$8 million or more per jet

- To much cash ....

- Solution? Pre-paid cards!

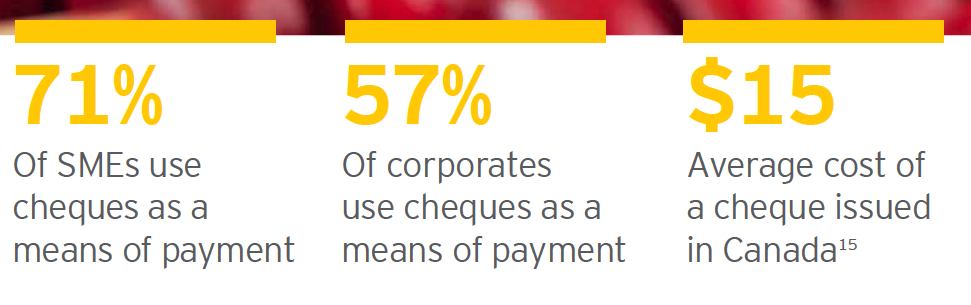

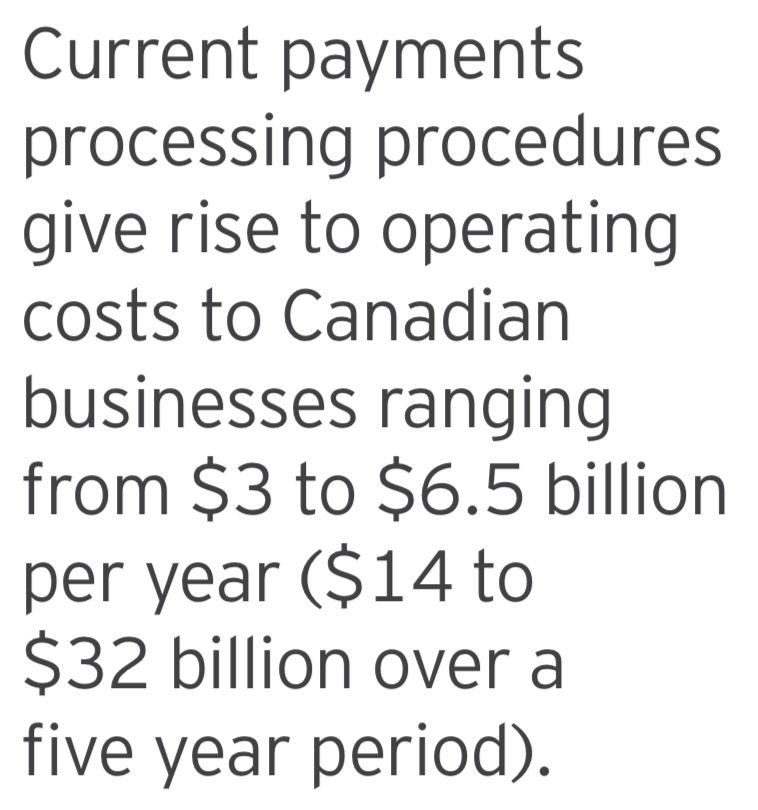

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

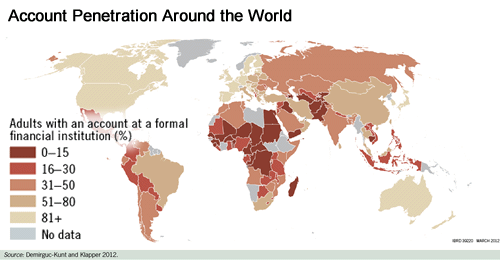

Is it a choice?

Are people well serviced?

-

student from China

-

no family in Canada

-

moves to the UK

-

needs to transfer funds and has yet to establish bank account in the UK

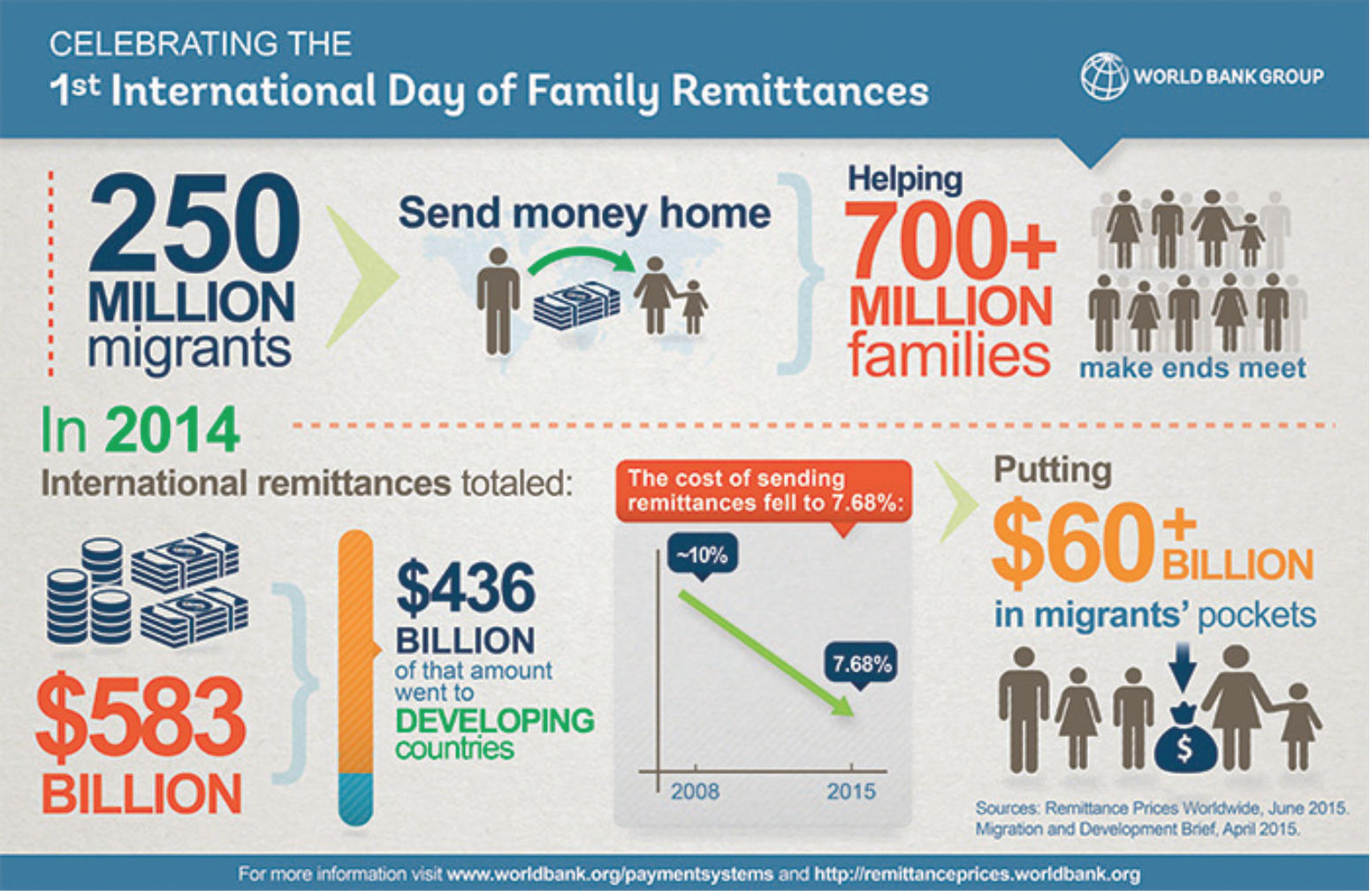

International remittances: $600B (U.S.) p.a.

all in: 10% fees

From Lecture 1: International Remittances

2015: 7.68% fees

2017: the total cost of sending remittances = $30 billion = total non-military foreign aid budget of the US!

An enormous transfer from the poor to the rich!

Not just consumers ... Anecdotally:

Credit

Financial institutions often won't offer payment solutions to small business, due to their credit risk profile.

Credit cards:

SMEs need to use owner's personal card which affects their personal credit score

Expensive B2B payments:

most financial institutions charge base fee + transaction fees

Accounting/corporate finance

Small businesses have to integrate payment activities to accounting platforms themselves.

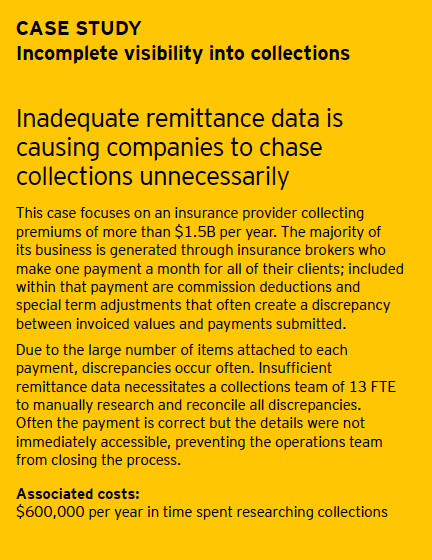

Business: Need Better Data and Faster Processes!

Where does the money go, where does it come from?

\(\Rightarrow\) inadequate cash flow information

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

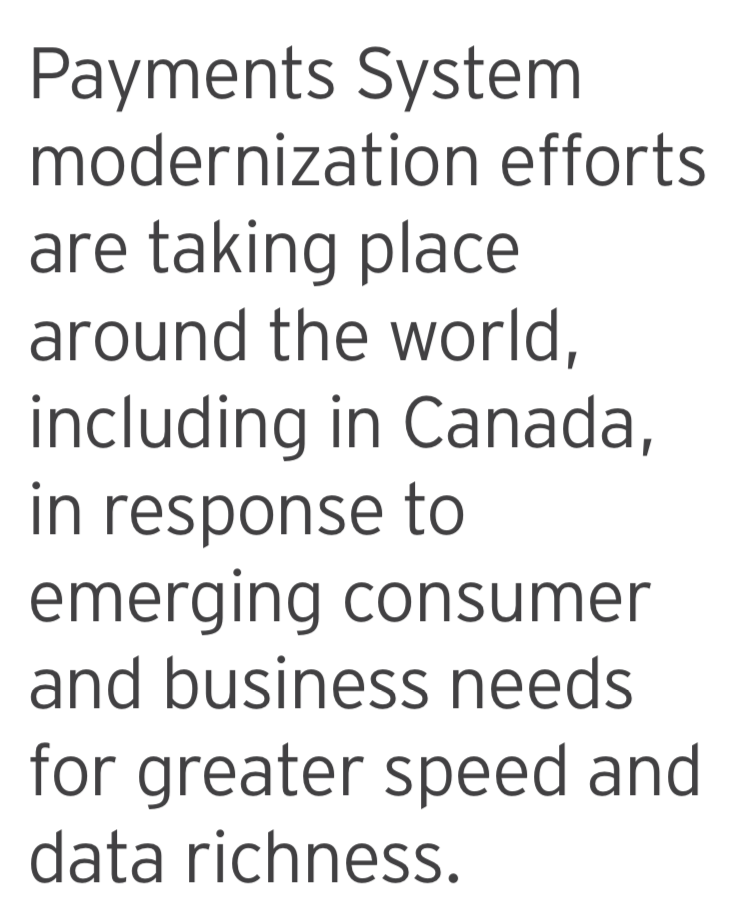

Bottom line? Not there yet!

Source: How can payments modernization benefit Canadian businesses? Evaluating the cost of payments processing; EY and Payments Canada, 2018

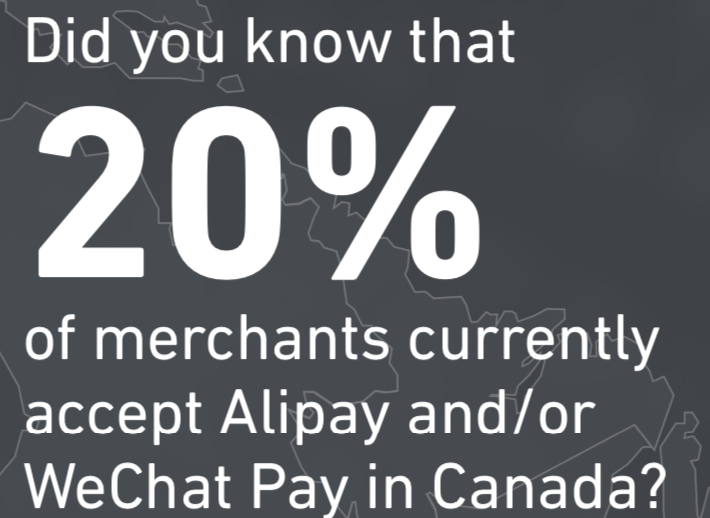

Innovations in Non-physical Payments around the world

Scandinavian Digital Payments

Mobile

Money

Mobile Apps in Emerging Economies

Danish Mobile Pay

4+ million users (population 5.7M)

235+ million transactions, 8.6Bn EUR value

launched by Danske Bank, but bank-neutral

instant payments based on mobile phone numbers

Critical PreReq for Danish Mobile Pay

government issued digital ID

available to anyone with a SIN

common login for:

civic services

banking

taxes

other businesses, e.g. telcos

Components of Danish Mobile Pay

a mobile app

links to existing bank account

uses trusted infrastructure and authentication

cleverly leverages what you have

adoption rate shows the value of form factor/frictionless experience

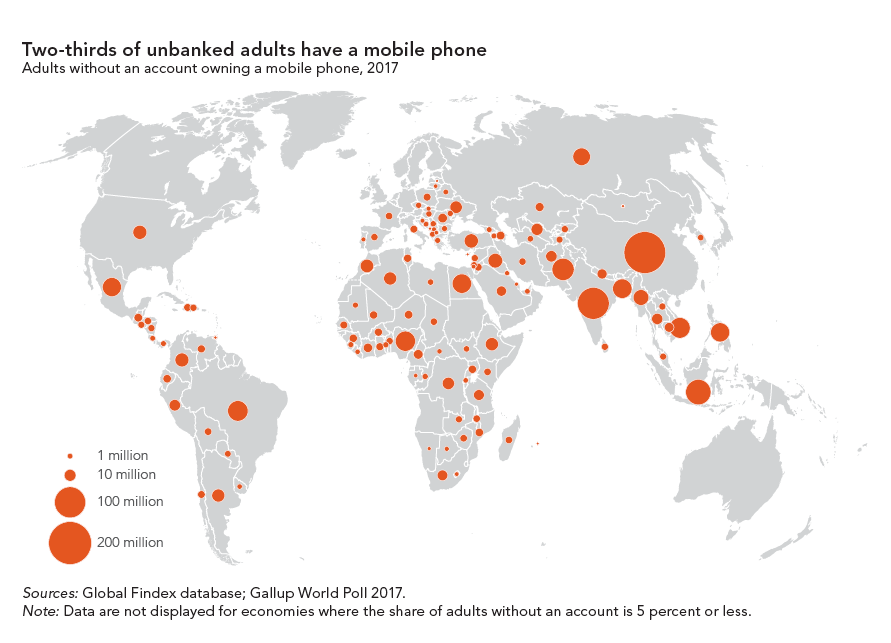

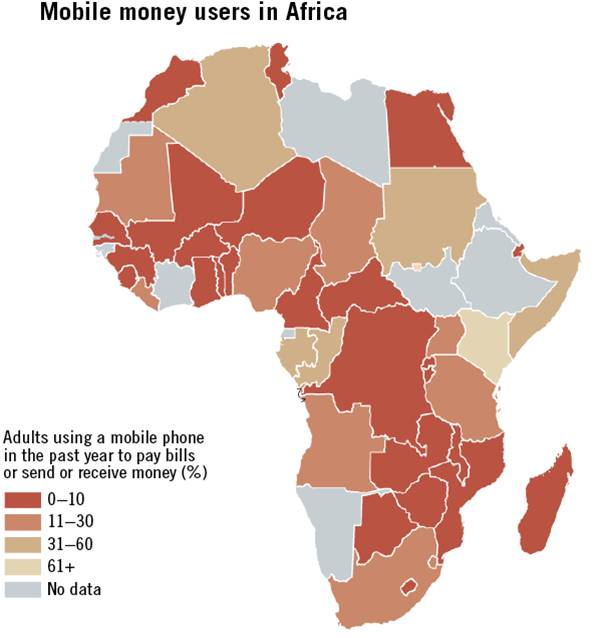

Mobile Money in the Developing World

bank account

access to saving vehicles and safe storage & transfers

better economic future

Mobile Money in the Developing World

Mobile Money

Mobile Payment

Cash-In

agent

Cash-Out

agent

Mobile Money: M-Pesa

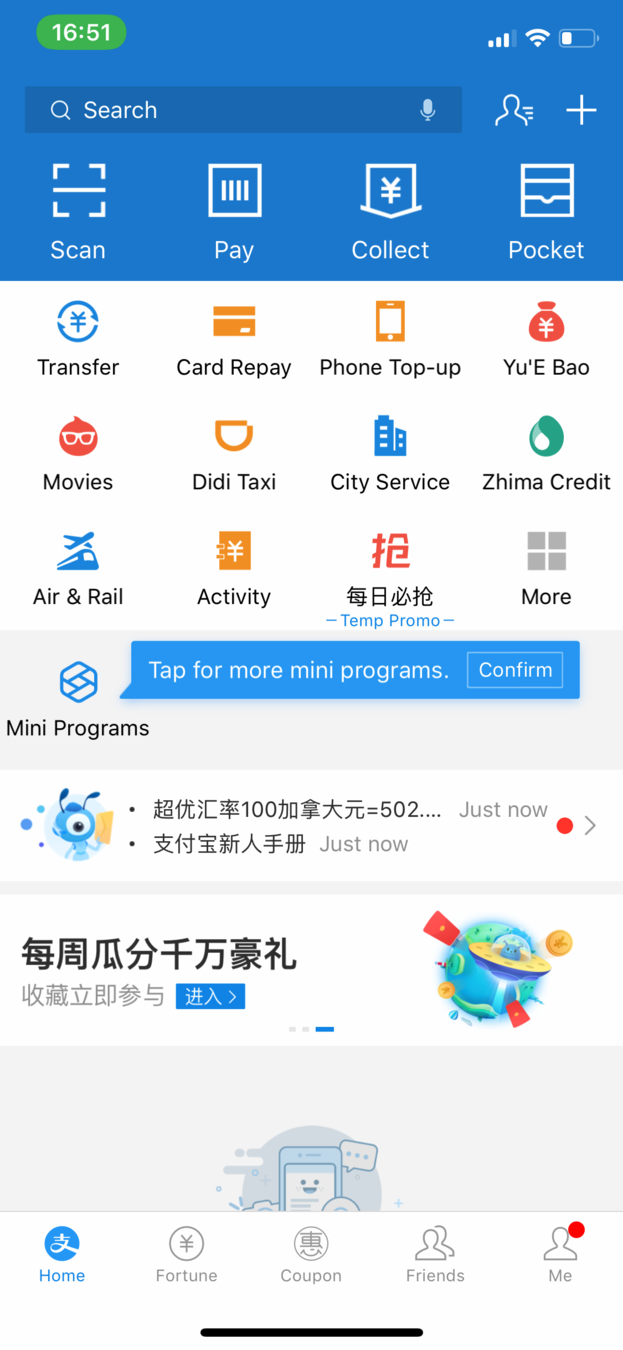

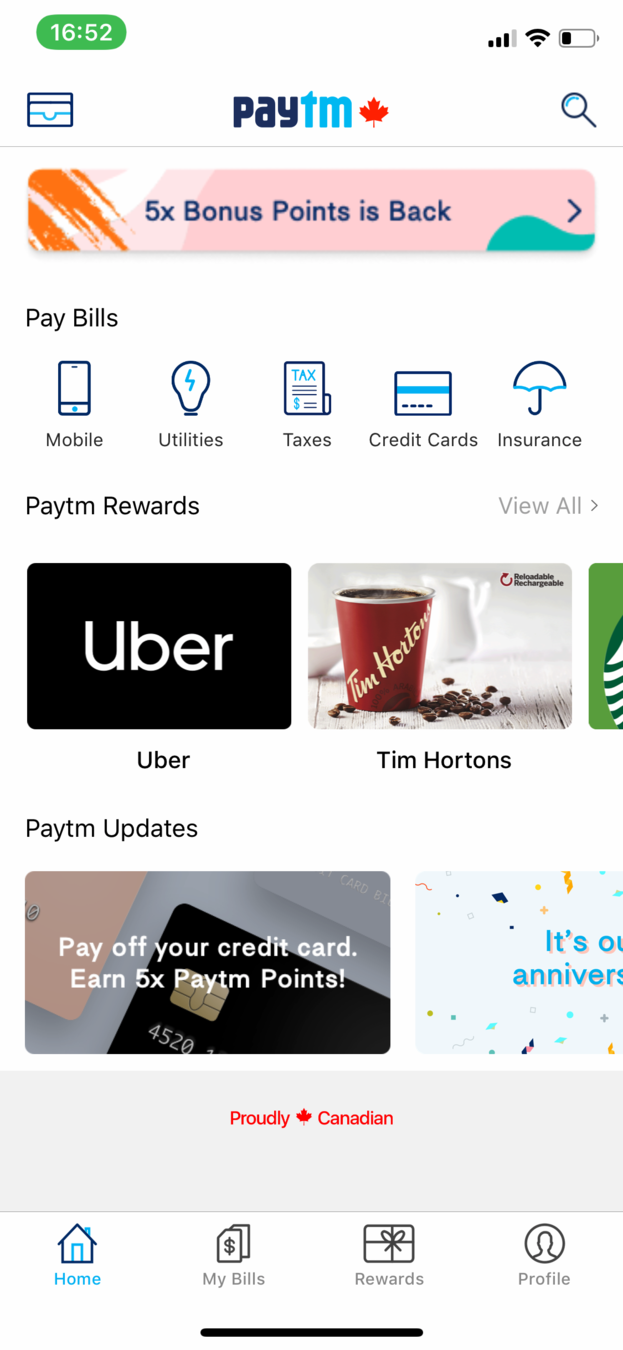

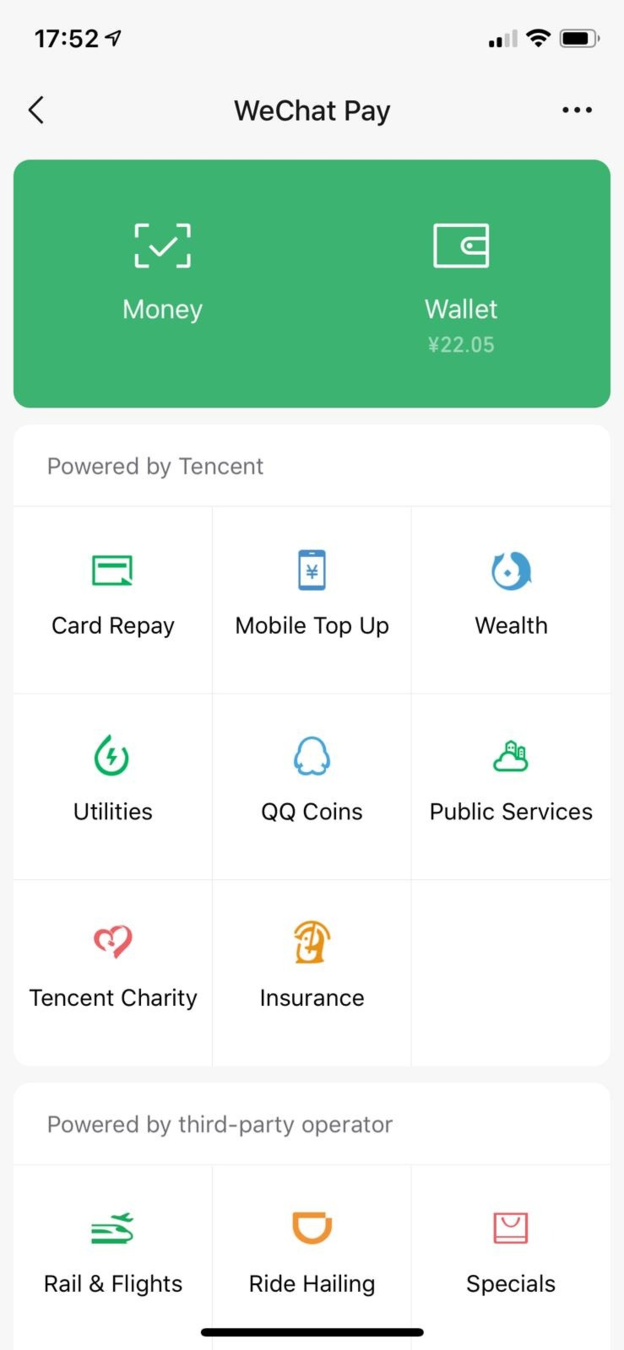

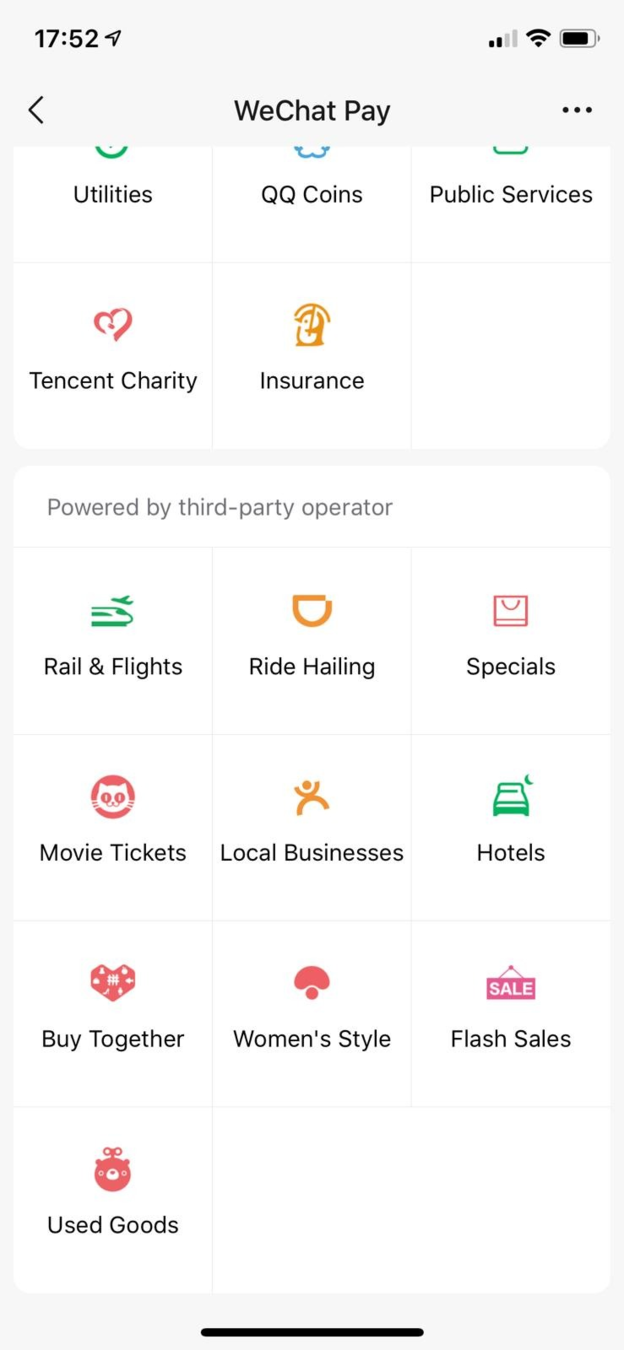

Mobile Apps in Emerging Economies

https://www.payments.ca/sites/default/files/canadianpaymentmethodsandtrendsreport_2019.pdf

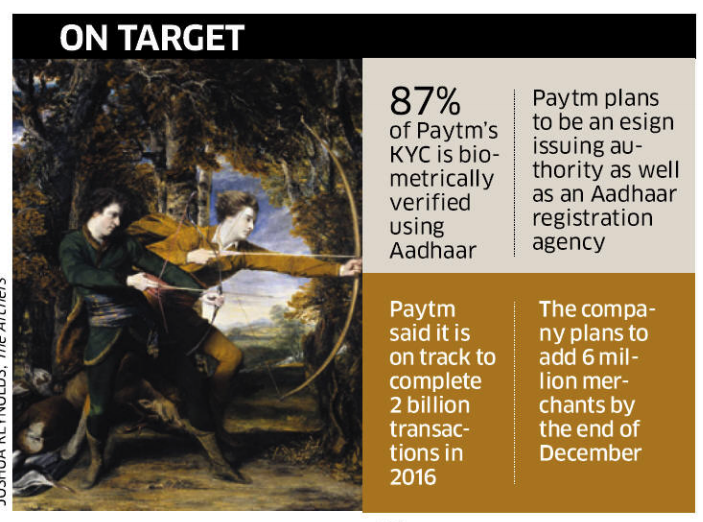

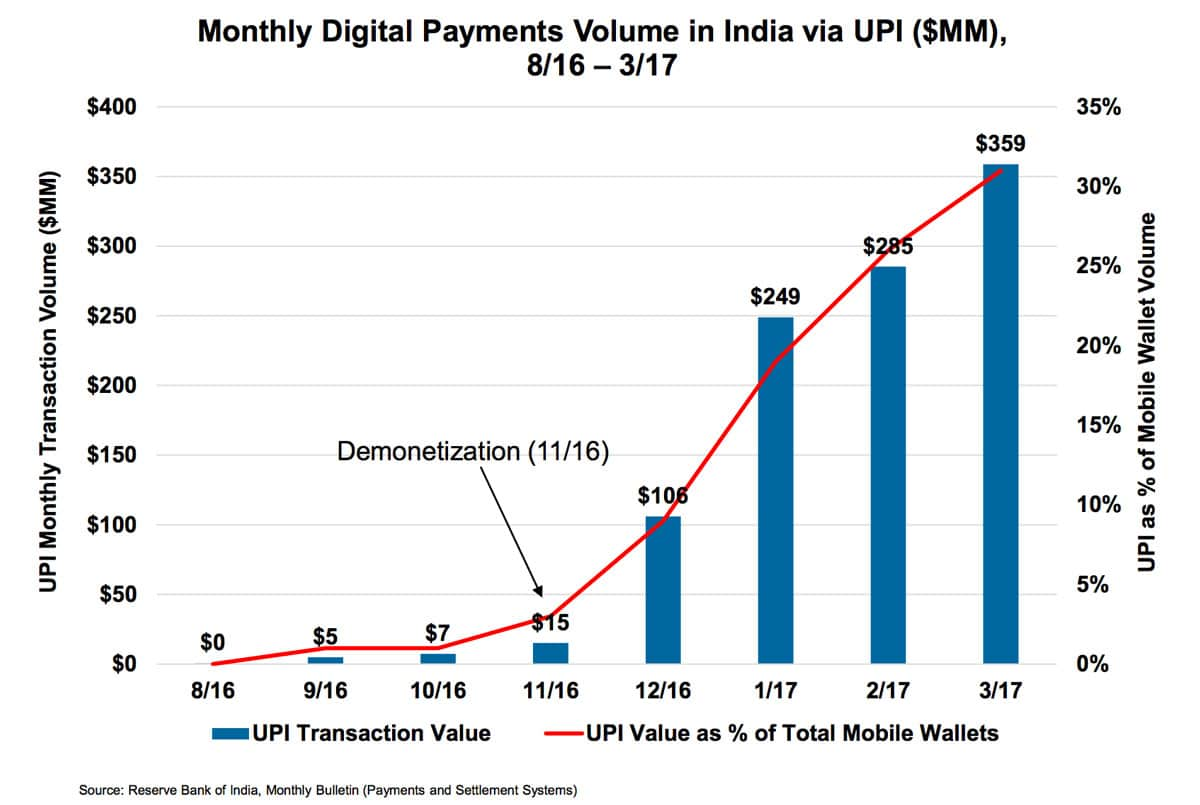

Component of : digital identity + Unified Payments Interface

"To empower residents of India with a unique identity and a digital platform to authenticate anytime, anywhere."

- "[PayTM] want[s] to become the universal payments layer on every bank account"

- "something that was going to take 3-6 years now takes 3-6 months"

UPI puts multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments under one hood.

some stats for India

-

450 million users

-

5 million transactions per day

-

over 12 million merchants

-

over $4 billion per month

These apps offer more financial services than payment

Why is this relevant (even if you aren't interested in FinTech)?

Will new students ...

-

get a bank account?

-

or just choose merchants by whether they can use WeChat pay?

How about new immigrants?

-

At what point will they simply stop using Canadian banks?

Potential problems with "outside" payment solutions?

(Until just a over a week ago?), the largest money market fund in the world was ...

Remember our discussion on crypto-exchanges taking deposits .... ?

Is PayTech a thing in Canada?

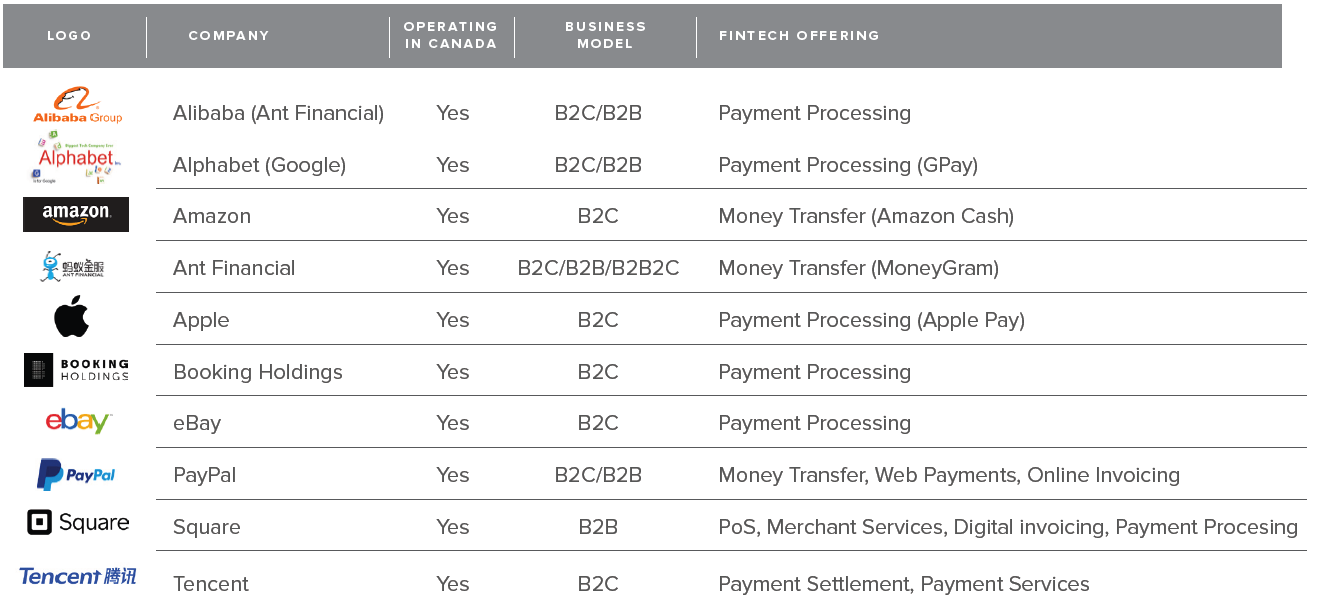

Innovations by BigTech

BigTechs operating as FinTechs in Canada

Why does BigTech enter the finance game?

Chances are: they have ZERO interest in becoming a financial institution/bank

\(\rightarrow\) no expertise

\(\rightarrow\) competitive market

\(\rightarrow\) one of the most regulated business environments

Several possible explanations:

They are trying to deal with frictions that impede their business

They aim to collect data which will vastly improve their business

Why is payments data valuable?

How much money is coming into and out of the account each month

If you had a full view of payments, what would you learn?

Spending habits: what you spend money on and where you spend it

Payment habits: Are you paying bills way ahead of deadline or tardy?

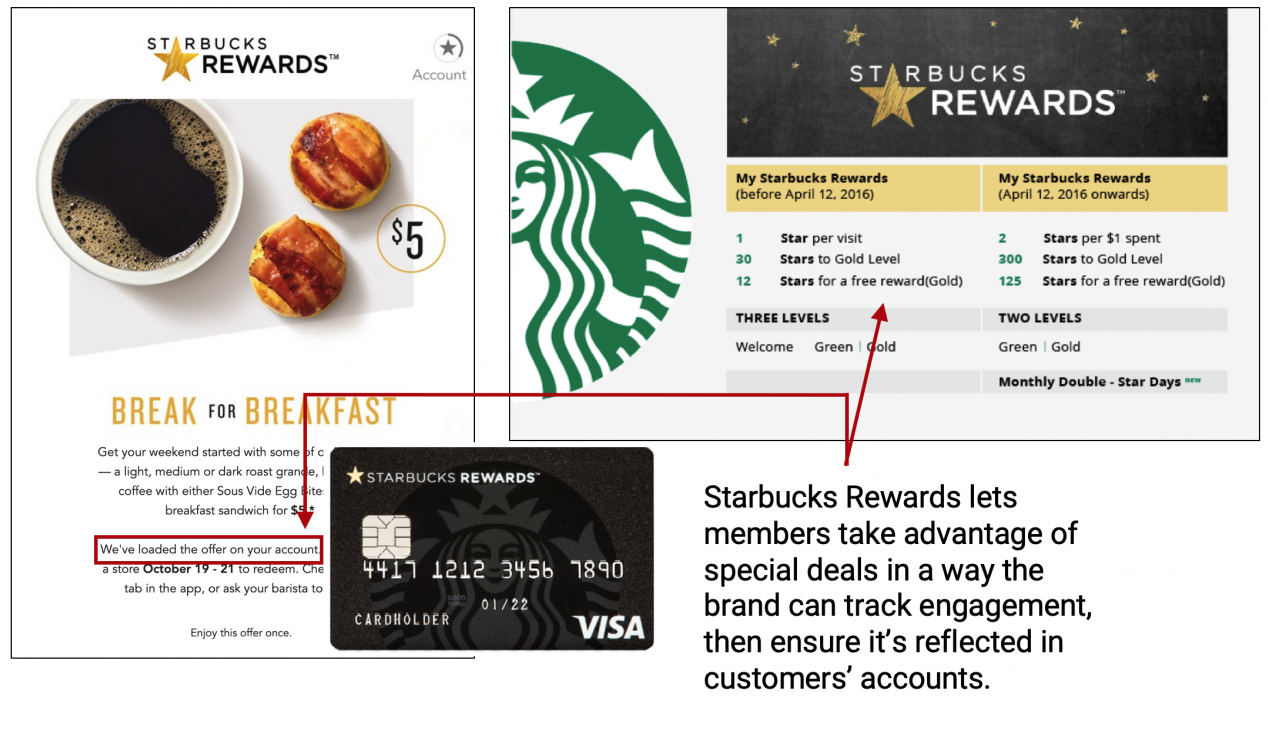

There is more to payments than payments!

There is more to payments than payments!

Loyalty rewards

is (mostly) not about rewarding loyalty.

It's DATA!

There is more to payments than payments!

Things to keep in mind? Know what the data tell you!

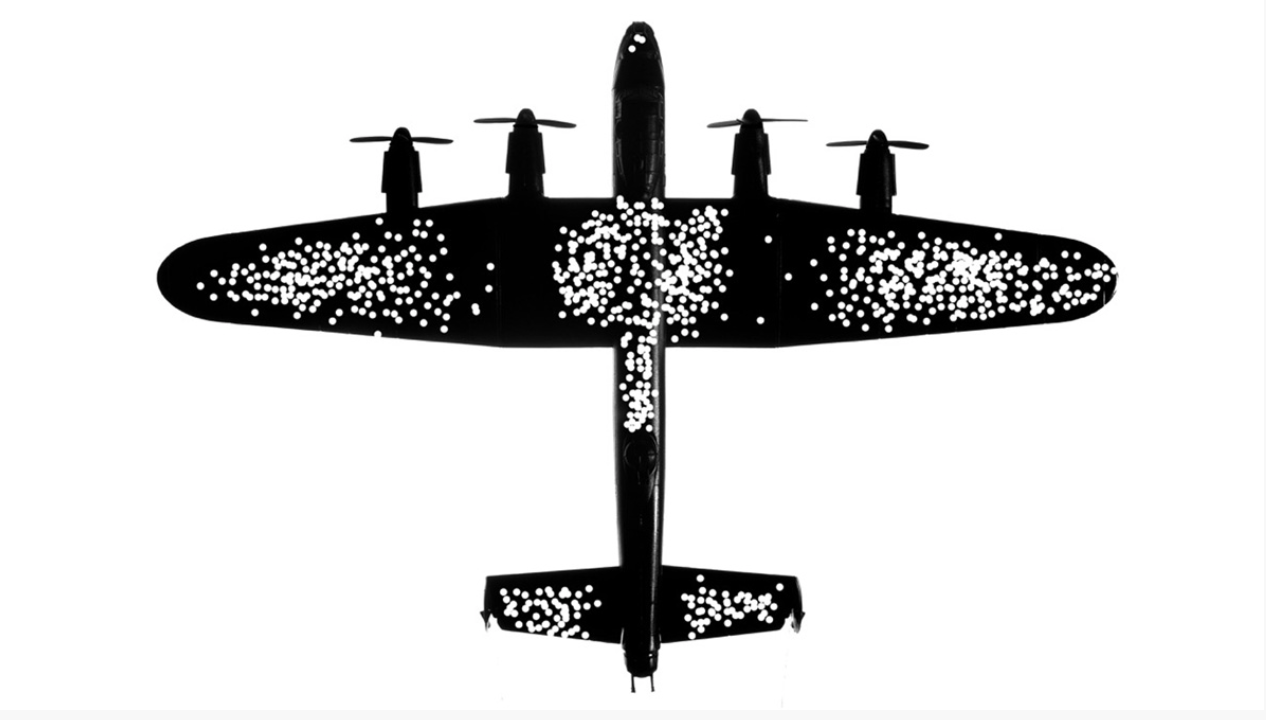

Abraham Wald: The armor should NOT go where the bullet holes are. It goes where the bullet holes aren’t!

Back during World War II, the RAF lost a lot of planes to German anti-aircraft fire. So they decided to armor them up. But where to put the armor?

Social Credit System in China

Pilot programs with various tracking metrics and consequences for violations

- Public shaming of those who don't pay the bills or behave in a socially "unacceptable" way

- “Deadbeat Debtors near me” map via WeChat