Investor Attention and the Cross-section of Analyst Coverage

Charles Martineau and Marius Zoican

Bank of Lithuania October 16, 2020

Motivation

Analyst coverage across stocks (2017Q4)

What drives the demand for information?

- Investors need information to choose portfolios.

- Limited attention can lead to suboptimal investment decisions:

- Portfolio under-diversification

- Home bias

What drives the supply for information?

- A key source of information comes from equity analysts, who disseminate financial information through reports.

How does investor attention impact analyst coverage choices?

Analyst objective

Maximize trading volume & revenue for brokerage house.

(Groysberg, Healy, and Maber, 2011)

Research question

This paper

- Empirical: How much does investor attention matter for analyst coverage choices?

- Theory: Build a noisy REE model to understand how attention constraints drive analyst coverage.

Contributions

Results

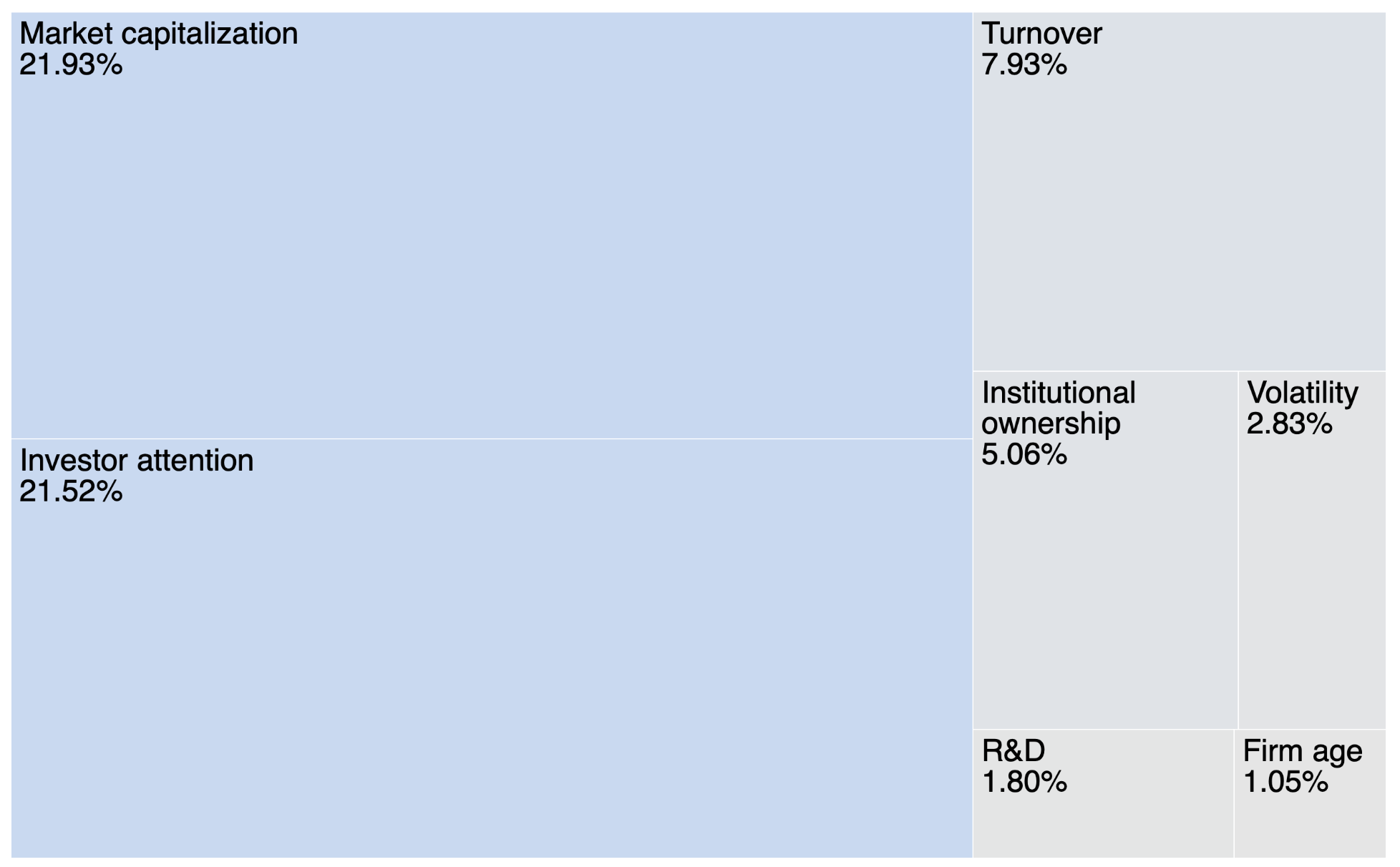

- Investor attention explains 21.52% of cross-sectional variation in analyst coverage -- second only to firm size.

- Model predicts coverage clustering, consistent with the data.

- Coverage clustering first , then in attention capacity.

- Relaxing cognitive constraints may not lead to more balanced coverage.

Literature

A growing literature shows that investor attention plays an important role in asset pricing at determining, e.g.,:

- price efficiency (Hirshleifer and Teoh, 2009)

- risk premium (Andrei and Hasler, 2015)

- return predictability (Da, Engelberg, and Gao, 2011)

- comovement (Peng and Xiong, 2006)

However, we know little on how investor attention influence information supply in financial markets.

Empirical results

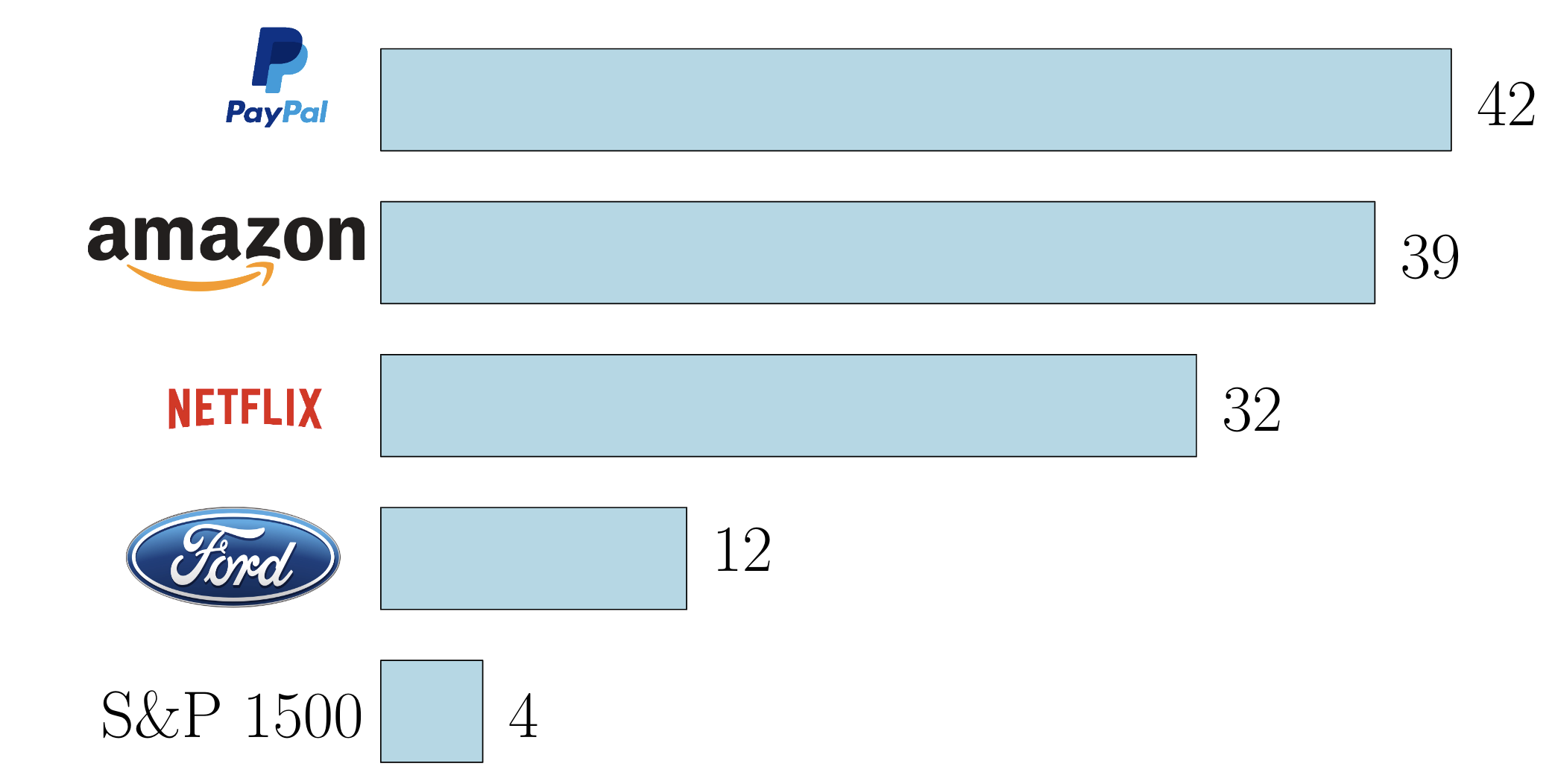

A measure of attention

- Bloomberg provides a daily score, ranging from 0 to 4, to reflect the (abnormal) investor attention.

- We follow Ben-Rephael, Da, and Israelsen (2017).

- The score measures the number of times terminal users actively search and read articles about a particular stock.

- We collect the score between 2012-2017 and take yearly averages.

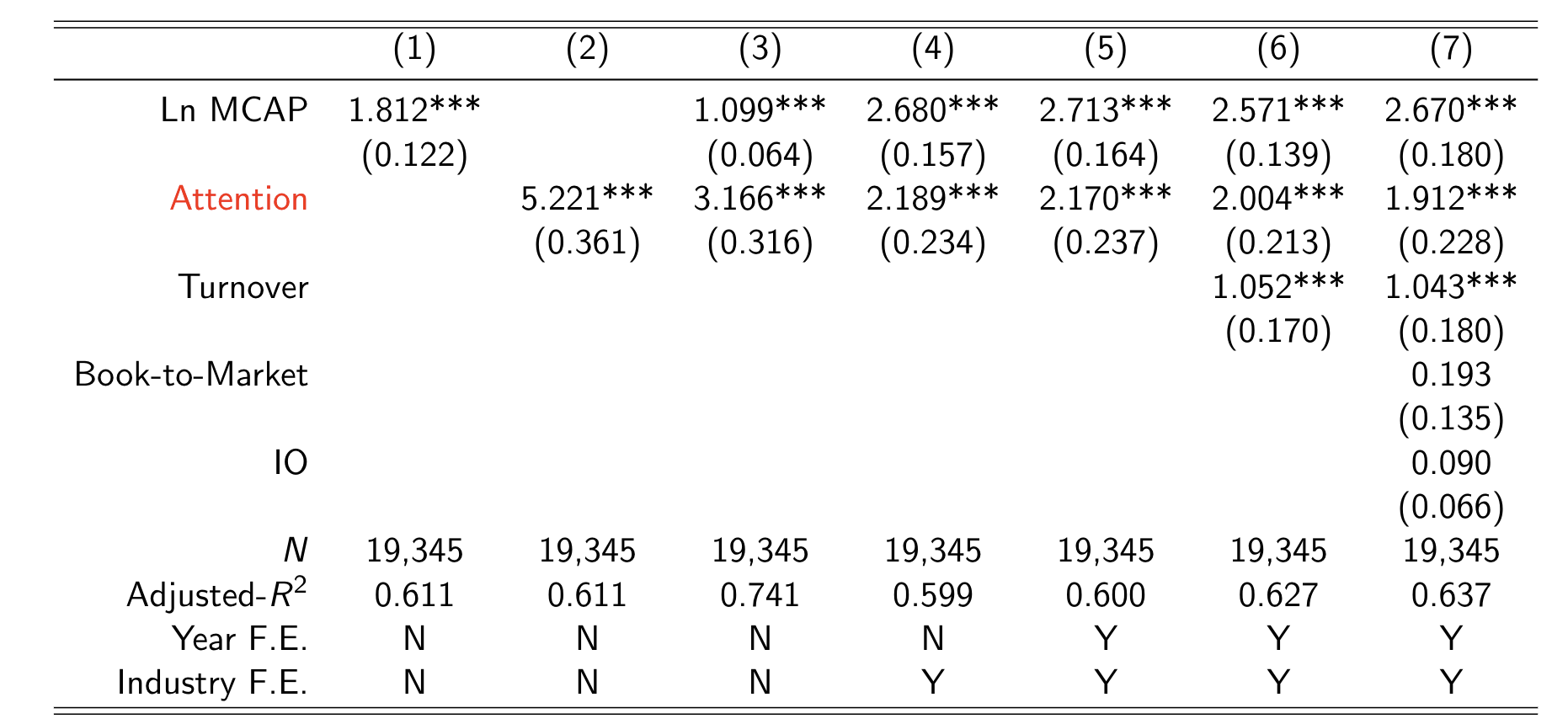

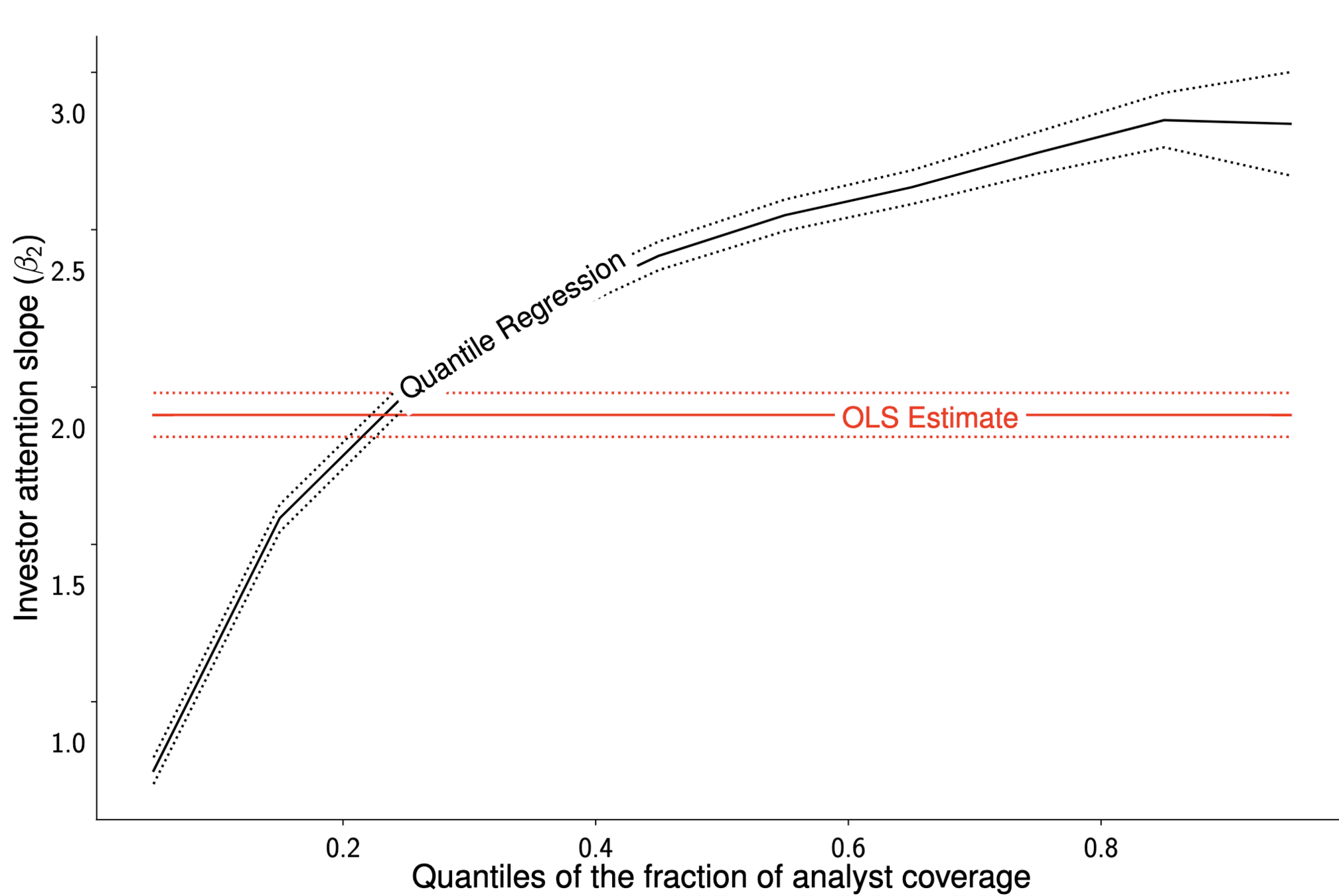

Investor attention and analyst coverage

*using Shapley-Owen decomposition

Analysts are more sensitive to attention for well-covered stocks

Model

Model ingredients

Assets

Two risky-assets in zero net supply, paying off at t=2

1. A high-precision asset H:

2. A low-precision asset L:

- Continuum of investors I with unit endowment and CARA preferences:

- Noise traders (i.i.d. across stocks) with variance

- Two analysts (k) who provide a public signal for one asset:

Agents

Investor attention and learning

Each investor j can acquire unbiased signals about stock i:

Investors choose the signal precision, but have finite learning (attention) capacity K:

Learning cost is lower if more analysts cover stock i

(through a "familiarity" argument):

(note decreasing returns to scale)

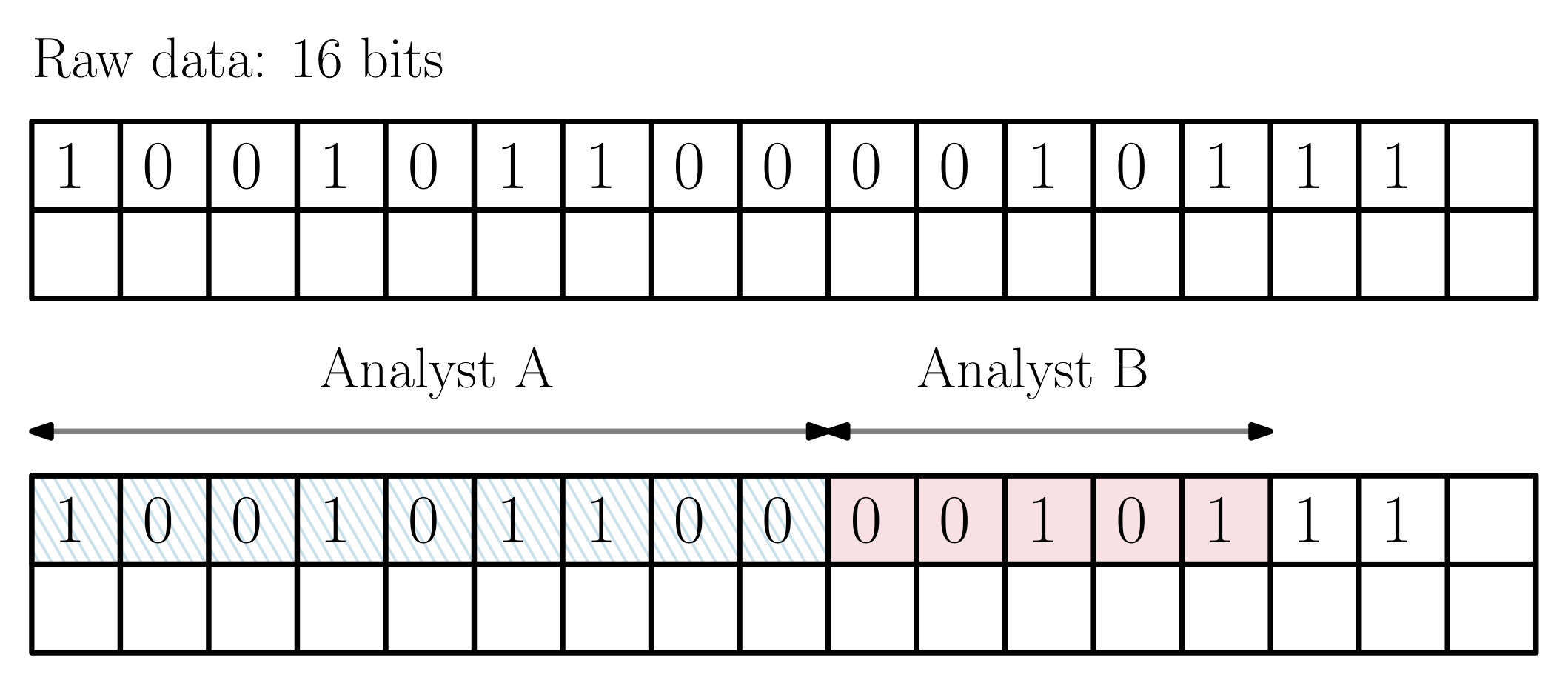

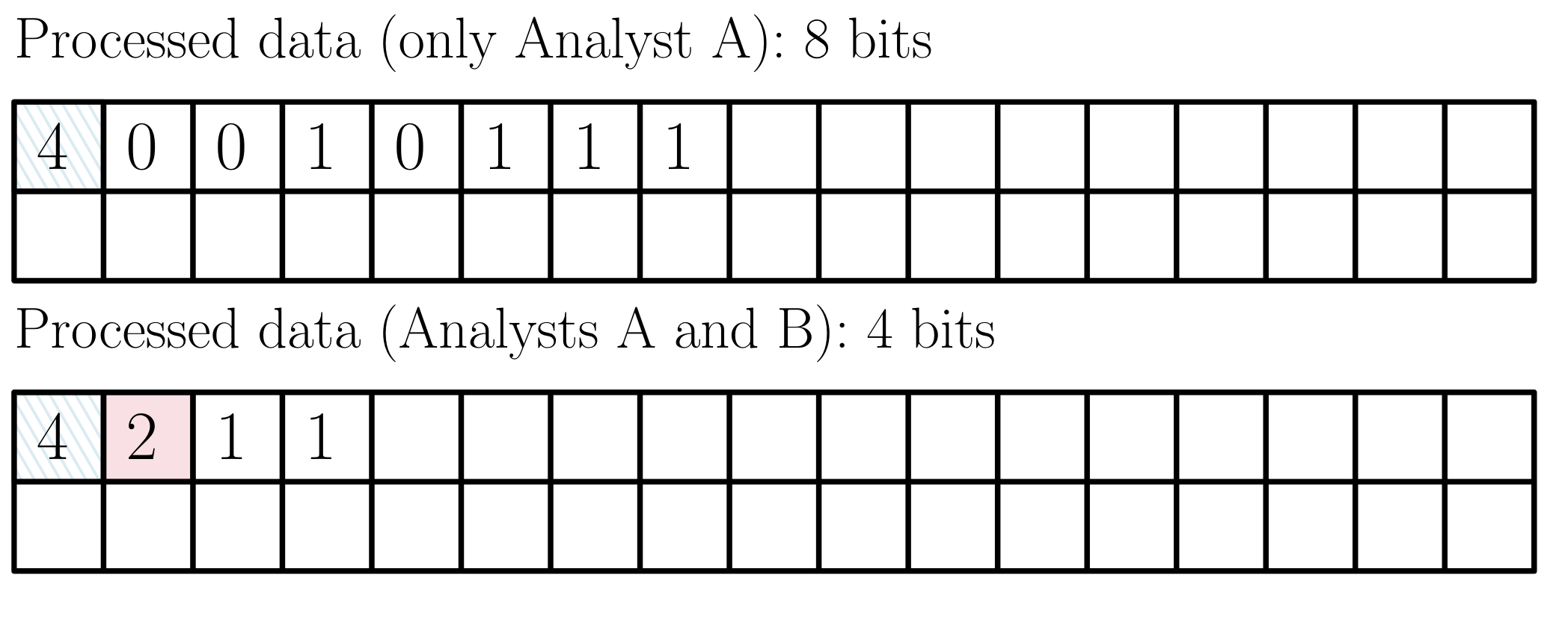

Analyst coverage as data compression

Analyst coverage as data compression

Analyst objective

- Sell-side analysts work for brokerage houses.

- Brokerage houses charge a fee f per unit of traded volume.

- Therefore, analysts choose to cover stocks to maximize expected volume for their brokerage house:

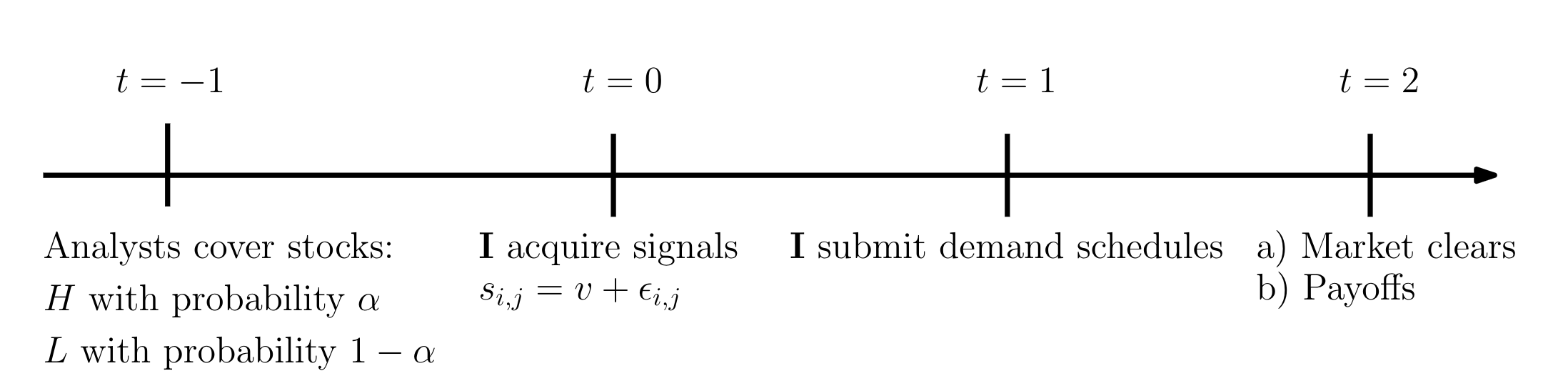

Model timing

Solving for equilibrium: Market clearing

(i) Conjecture linear price:

(ii) Optimal demand from investor j, conditional on signal:

(iii) Market clearing condition:

(iv) Clearing price:

Solving for equilibrium: Private signals

Following Verrecchia (1982), problem boils down to:

Posterior precision

A measure of price impact

Investors have zero mass so take price as given.

Problem becomes:

Text

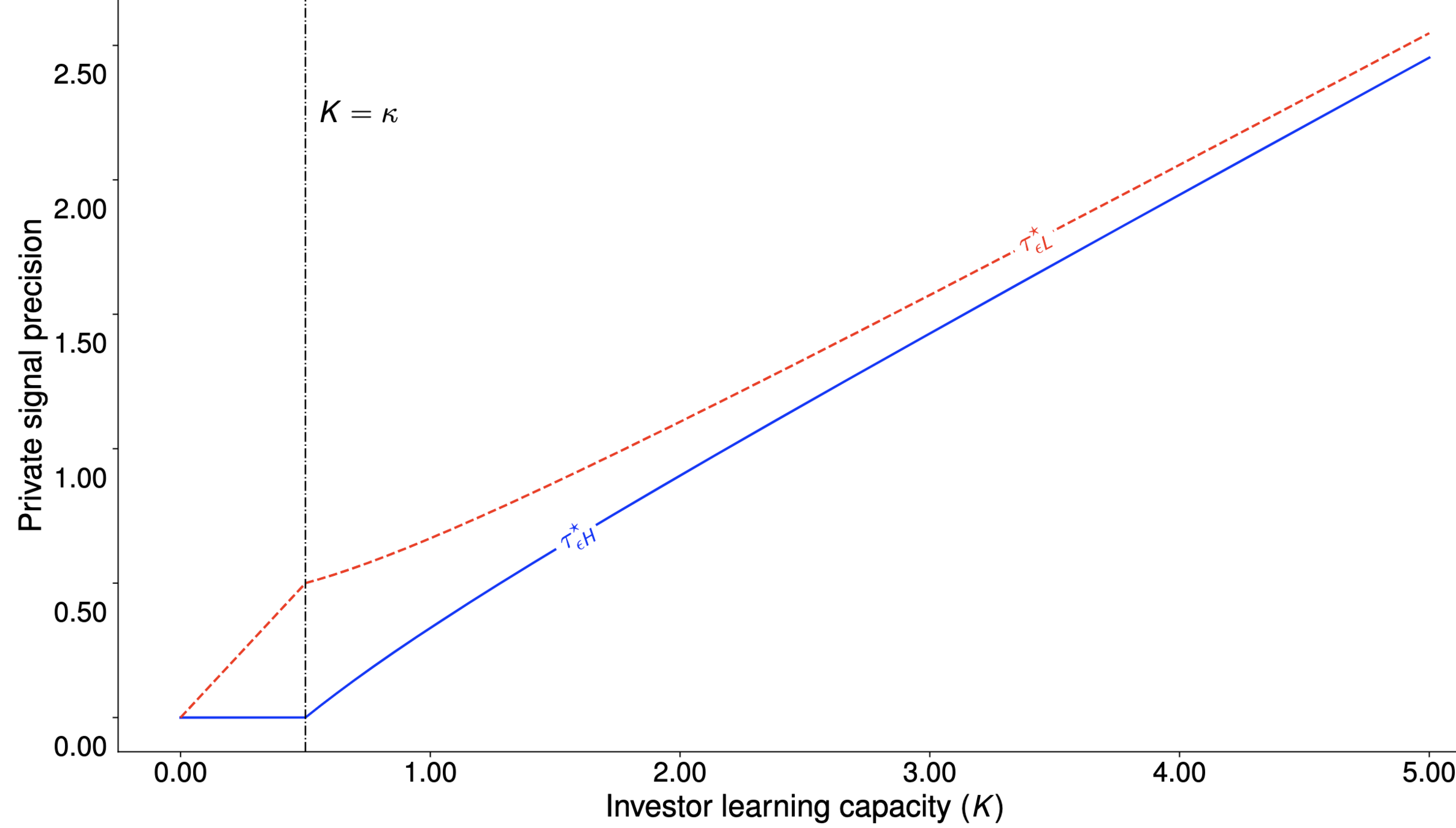

Attention constraint

Investors only learn about H if capacity is large enough

Optimal signal acquisition and coverage

Solving for equilibrium: analysts' problem

The expected volume in a given stock i is:

Mechanism

- Coverage Private learning Confidence in signal Volume

- Public forecasts are common knowledge influence prices, but not volumes.

Analyst choice

If analyst j covers stock H, her utility is:

If analyst j covers stock H, her utility is:

If analyst j covers stock L, her utility is:

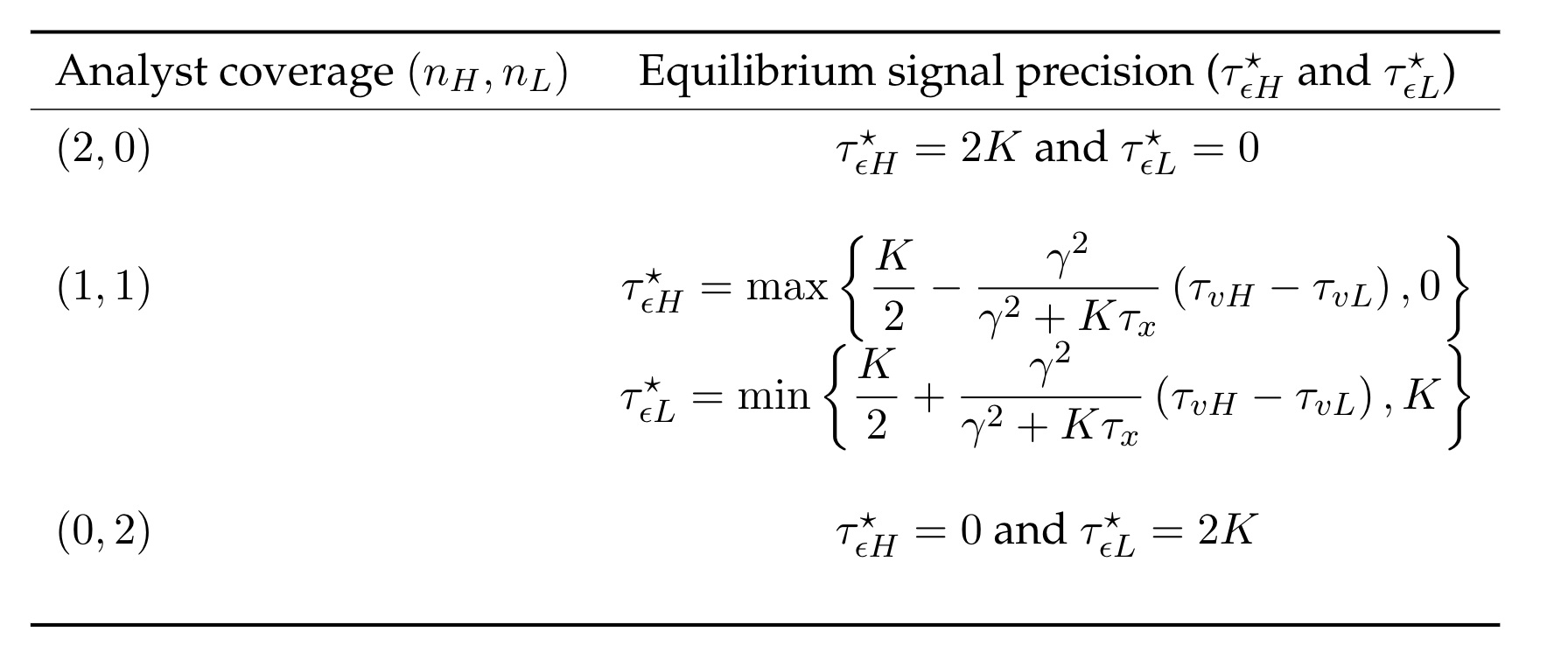

The equilibrium probability to cover stock H is:

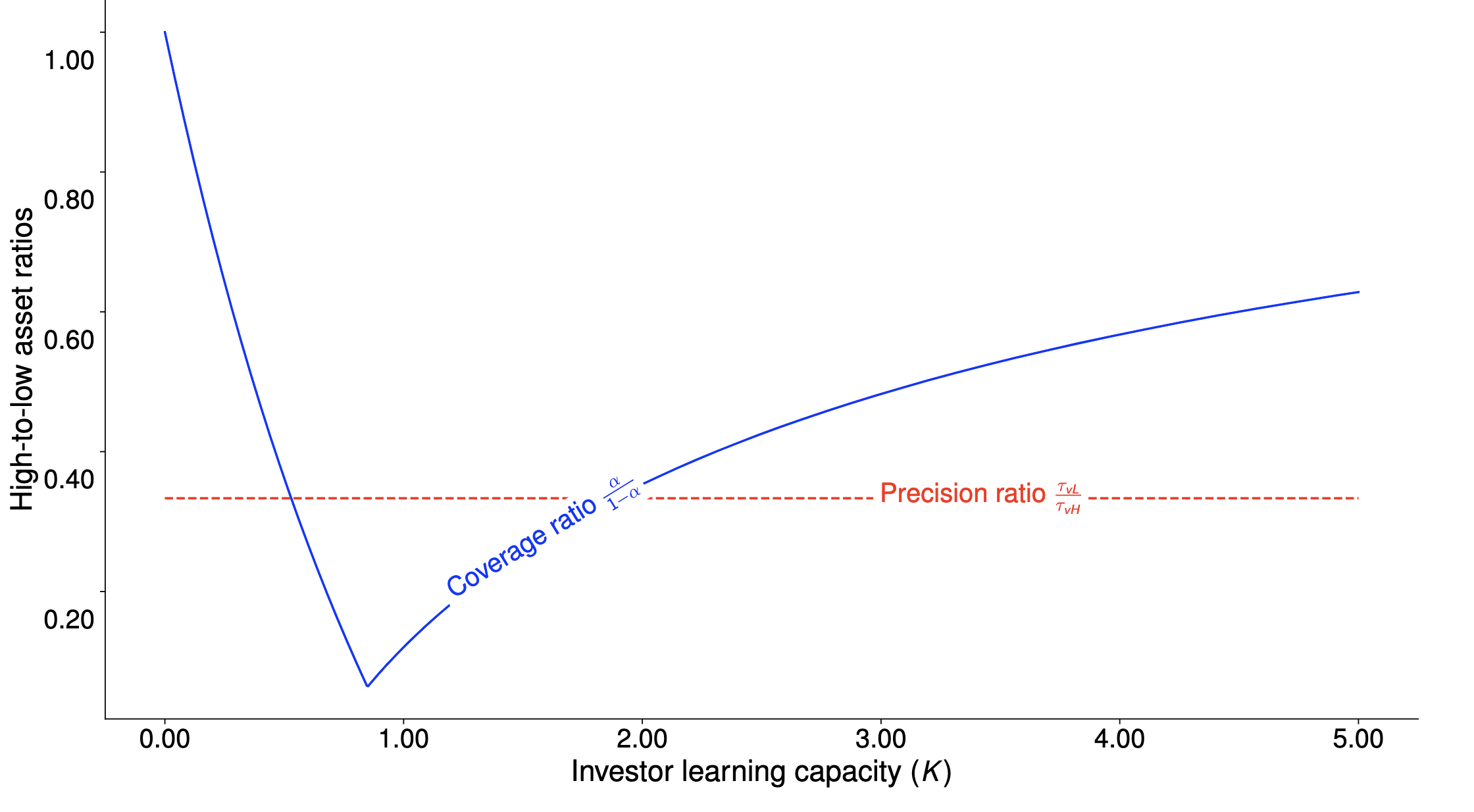

Equilibrium analyst coverage distribution

Coverage odds-ratio can exceed risk odds-ratio

Example: If stock L has a payoff variance 3x that of stock $H$, it can have up to 10x more analyst coverage in expectation

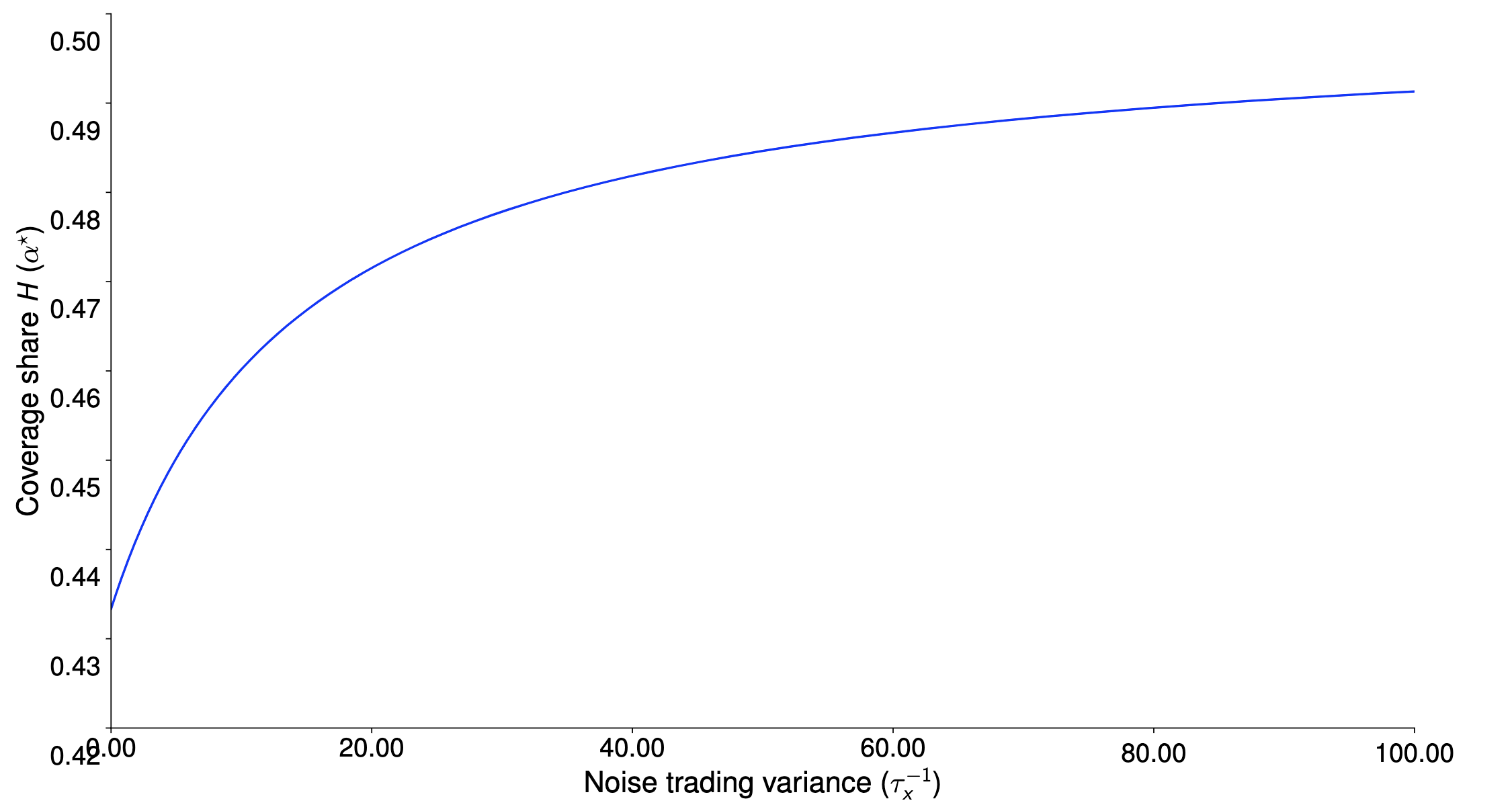

Analyst coverage and noise trading

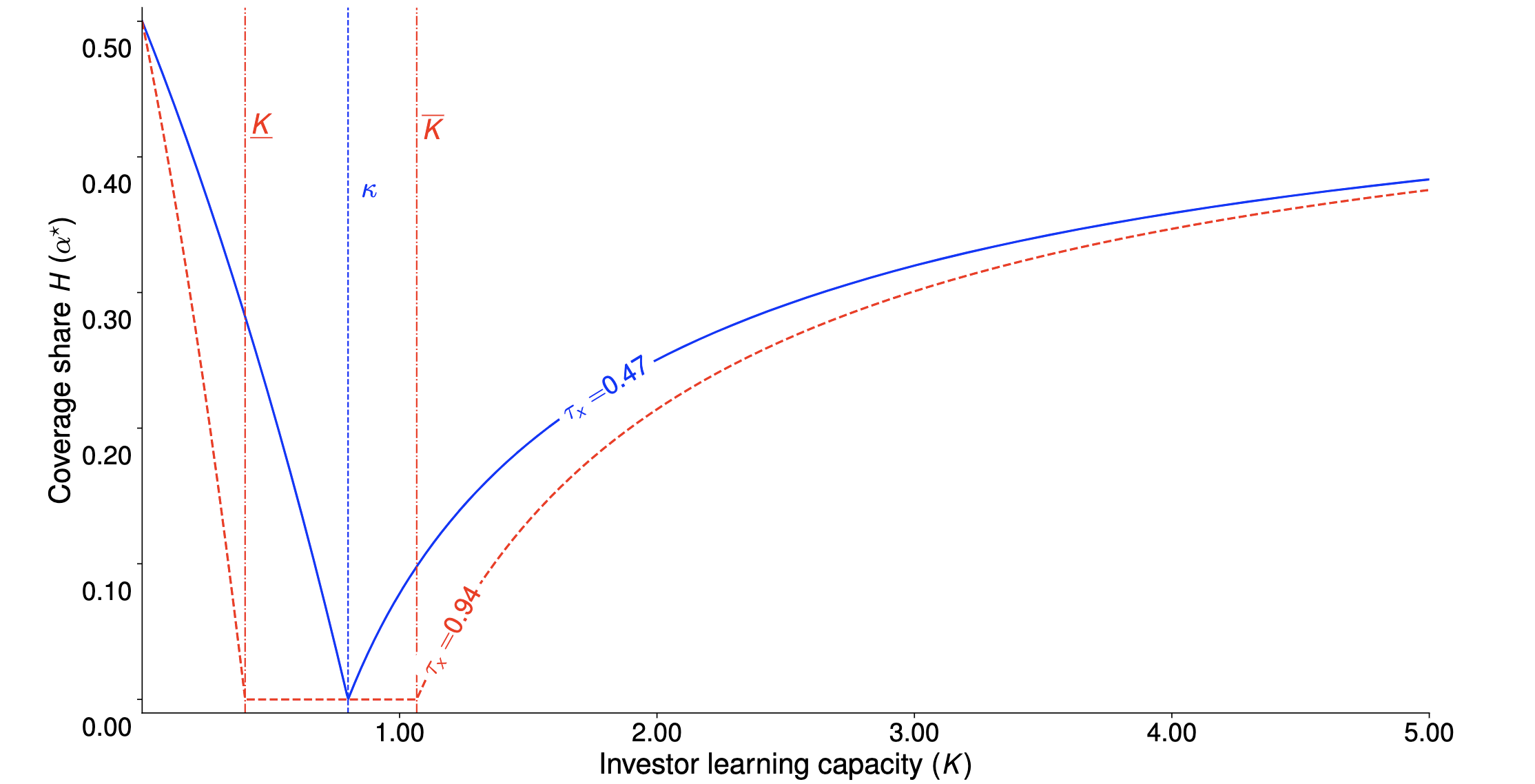

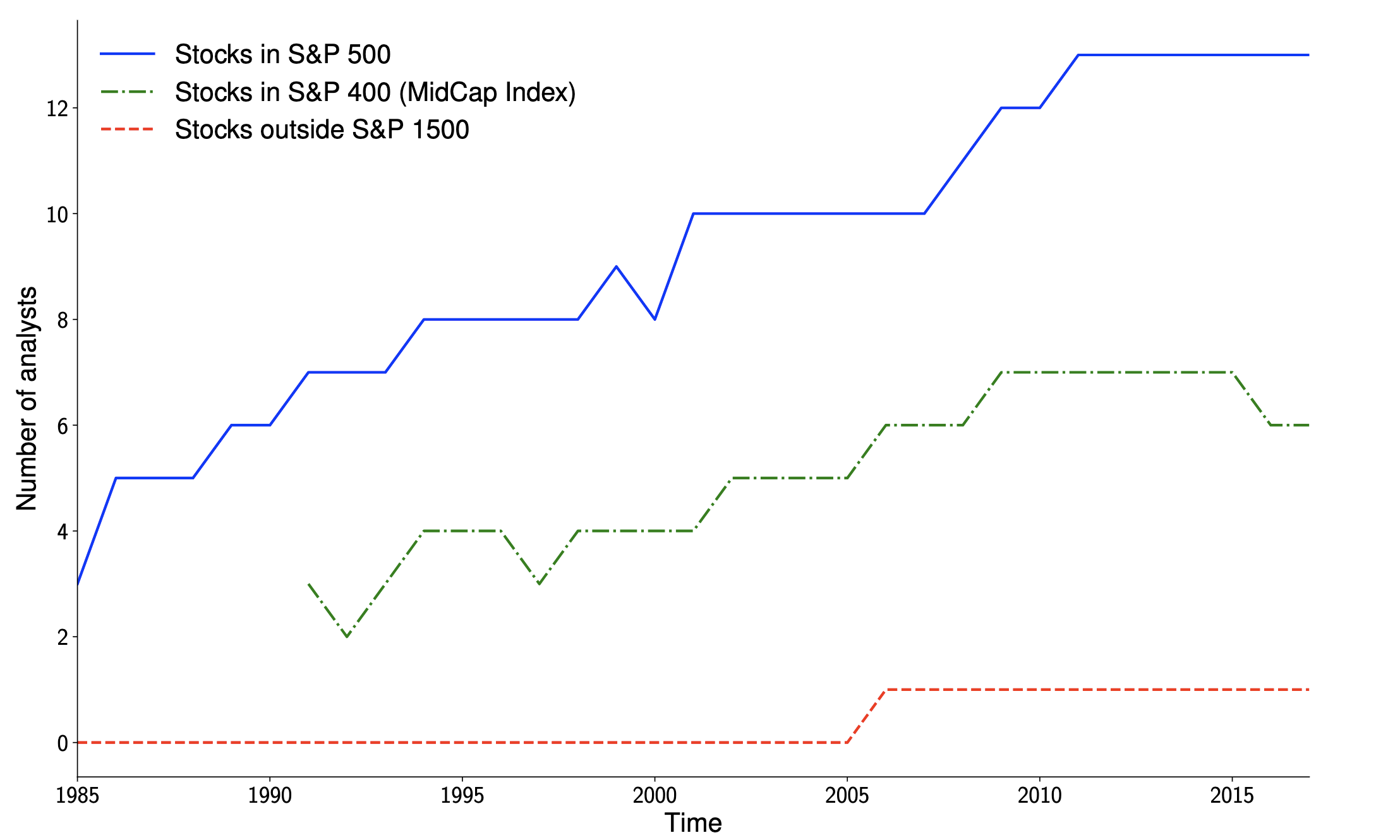

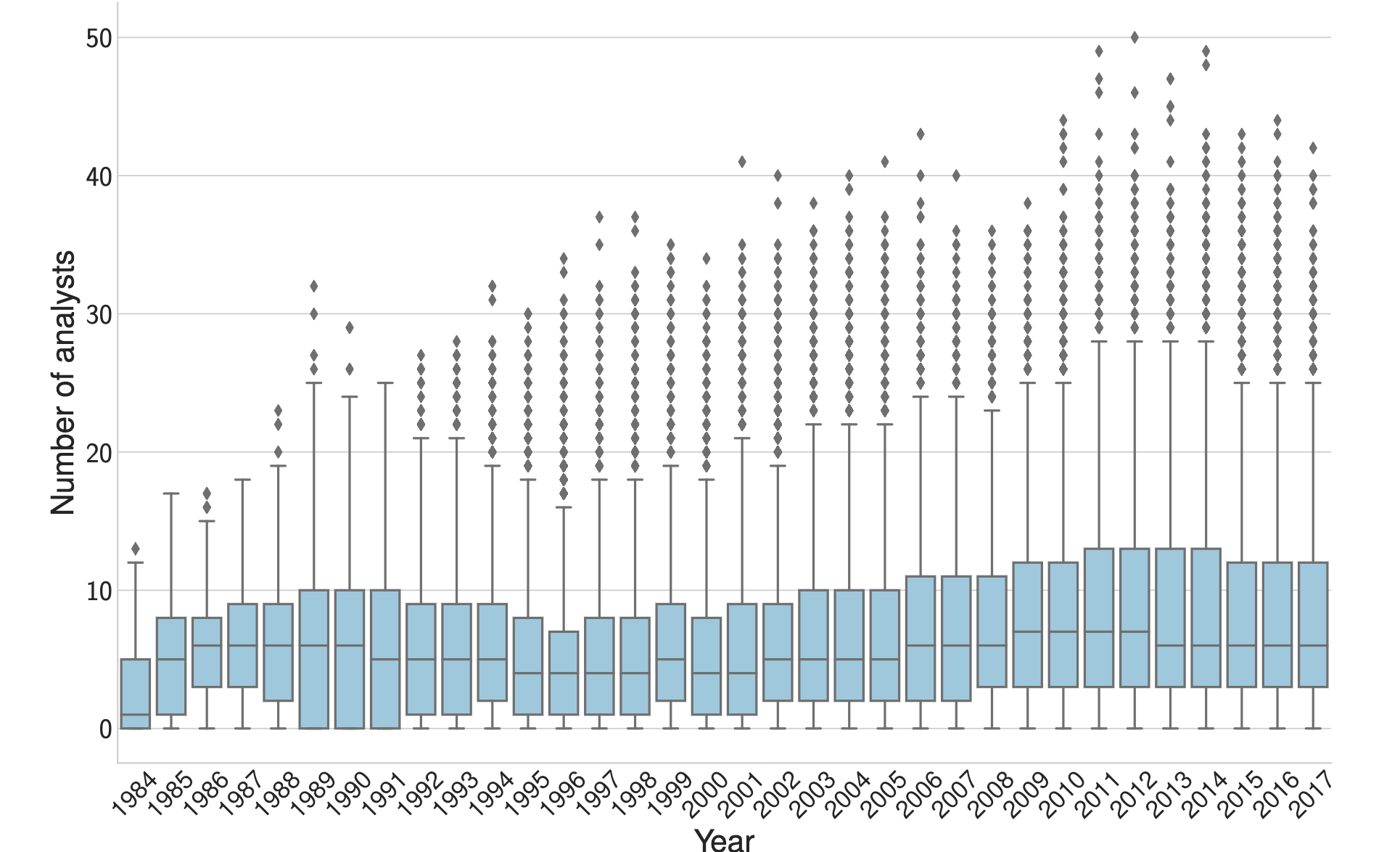

Coverage clustering

empirical evidence

Median coverage in the cross-section of stocks

A closer look at coverage clustering

Conclusions

- Investor attention explains 21.52% of cross-sectional variation in analyst coverage -- second only to firm size.

- For very limited investors attention, analysts are better off sharing a crowded space rather than trying to differentiate and cover neglected stocks.

-

The implications of our model match empirical patterns: the significant analyst coverage clustering in U.S. equities.

- A skewed information supply can disproportionately benefit large firms to the expense of small, "neglected" firms.