Do Proprietary Traders Provide Liquidity?

Bergman, Kadan, Michaely, and Moulton

Discussion by Marius Zoican

Answer: yes, but not where it matters (?)

- Proprietary traders provide liquidity in:

- large,

- low-volatility,

- high-volume,

- ... and already liquid stocks.

- Liquidity provision by prop traders is constrained in "bad times," when they scale down risk-taking.

- Proprietary traders "follow the market," in that they amount for 25% of volume in all but the smallest stocks.

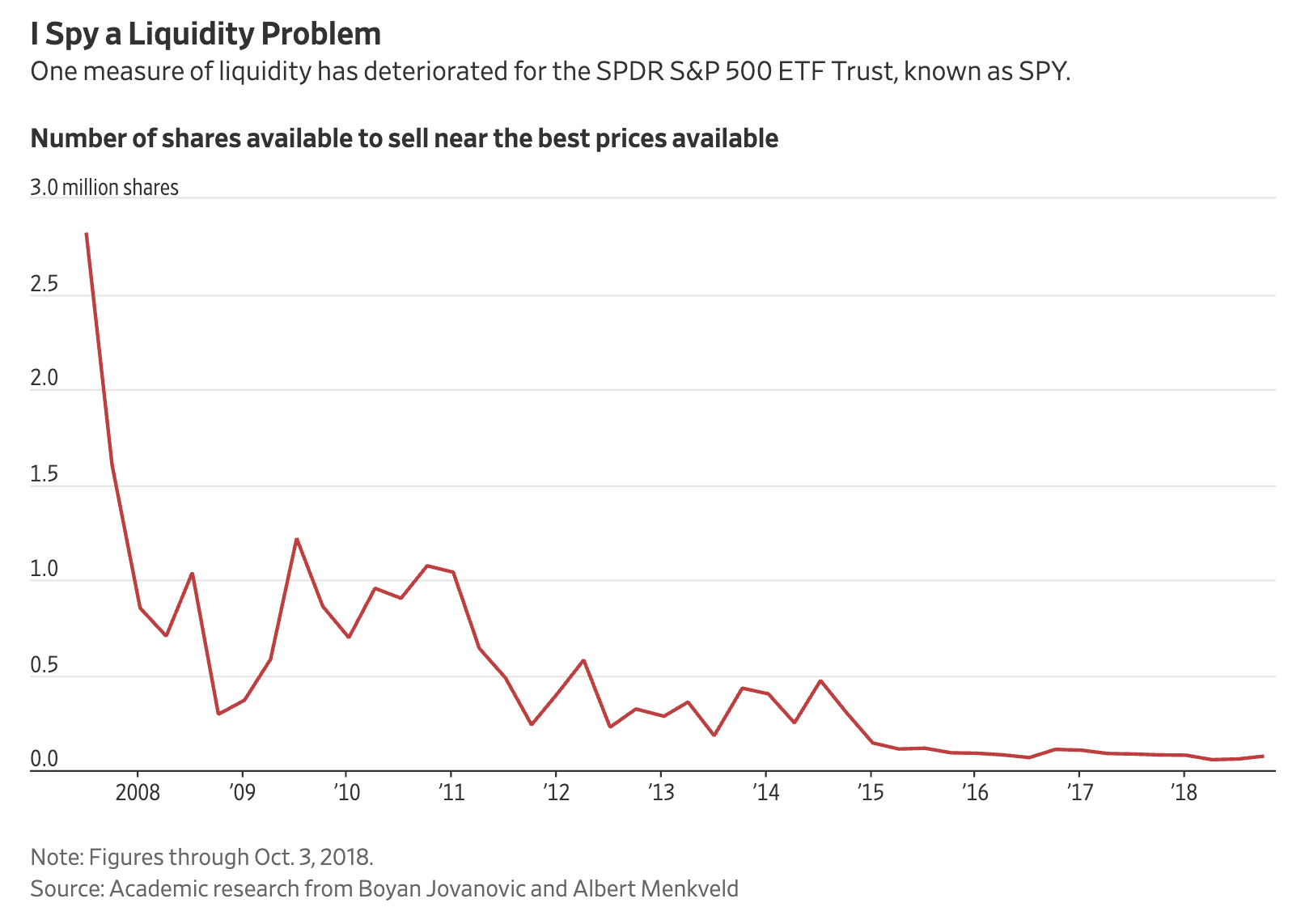

Main findings

Source: Jovanovic and Menkveld (2020)

Restrictions on prop traders matter!

we show that the illiquidity of stressed bonds has increased after the Volcker Rule. Dealers regulated by the rule have curtailed their market-making activities and non-Volcker-affected dealers have not offset the decreased activities of Volcker-affected dealers.

The paper has a normative undertone

- Prop traders do not help level the liquidity playing field.

- Should we expect them to do that? No have a fiduciary duty, after all.

- Should we mandate DMMs for small stocks? (since private incentives seemingly do not work)

- If risk-taking capacity is limited, is it socially optimal to "lock it down" in small stocks? Probably yes, to allow small companies to raise capital.

(I would like to see more on the implications)

How to measure liquidity?

- Price pressures: liquidity providers trade "against the wind" (buy when there is selling pressure).

- Is daily measure too "low-res"? (especially with trade-granular data & large influence of prop traders on prices)

| Price decomposition | Order book data |

|---|---|

| Kalman filter: decompose price in permanent (martingale ) and transitory component (AR process : |

Build an intra-day measure of order book imbalance (e.g., top 5 levels) |

| Do prop traders trade against the sign of ? | Do prop traders buy when there is sell (buy) pressure at the ask (bid)? |

p_t=m_t+\epsilon_t

m_t

\epsilon_t

\epsilon_t

Magnitude of the effect

- It is not straightforward to interpret the regression coefficient.

- A negative beta implies some degree of liquidity provision.

- How to translate this number to an explicit transaction cost? (e.g., implementation shortfall)

- Can I compare liquidity provision across trader groups?

- I.e., since imbalances from prop- & non-prop sum up to zero, should I expect that:

\beta_{1,\text{prop}}\approx -\beta_{1,\text{non-prop}}

Intermediary Capital Risk Factor and Liquidity

- The result that ICRF matters for liquidity provision is neat, and in line with the literature.

- ICRF only varies in the time series. Can you directly look at spreads/market depth as a function of ICRF?

Results on negative returns

- The paper shows prop traders do not provide liquidity in low-return periods.

- Is this an issue of negative returns, or extra risk? (e.g., if the return distribution is skewed)

Other comments

Is prop trading activity relatively stable over time?

If yes, wouldn't lagged stock liquidity/volatility be endogenous to prop trader presence? (25% of trading for most stocks)