Michael Brolley and Marius Zoican

3rd Toronto FinTech Conference November 5, 2020

Liquid speed:

a congestion fee for low-latency exchanges

Who really needs to trade at warp speed?

- HFTs provide price discovery as both makers and takers

- However, they also to capture latency arbitrage rents.

- Speed inequality can adversely effect liquidity (Shkilko & Sokolov, 2020).

- Should we tinker with or overhaul our market design? (Baldauf & Mollner 2020; Brolley & Cimon 2020; Haas,Khapko, & Zoican 2020).

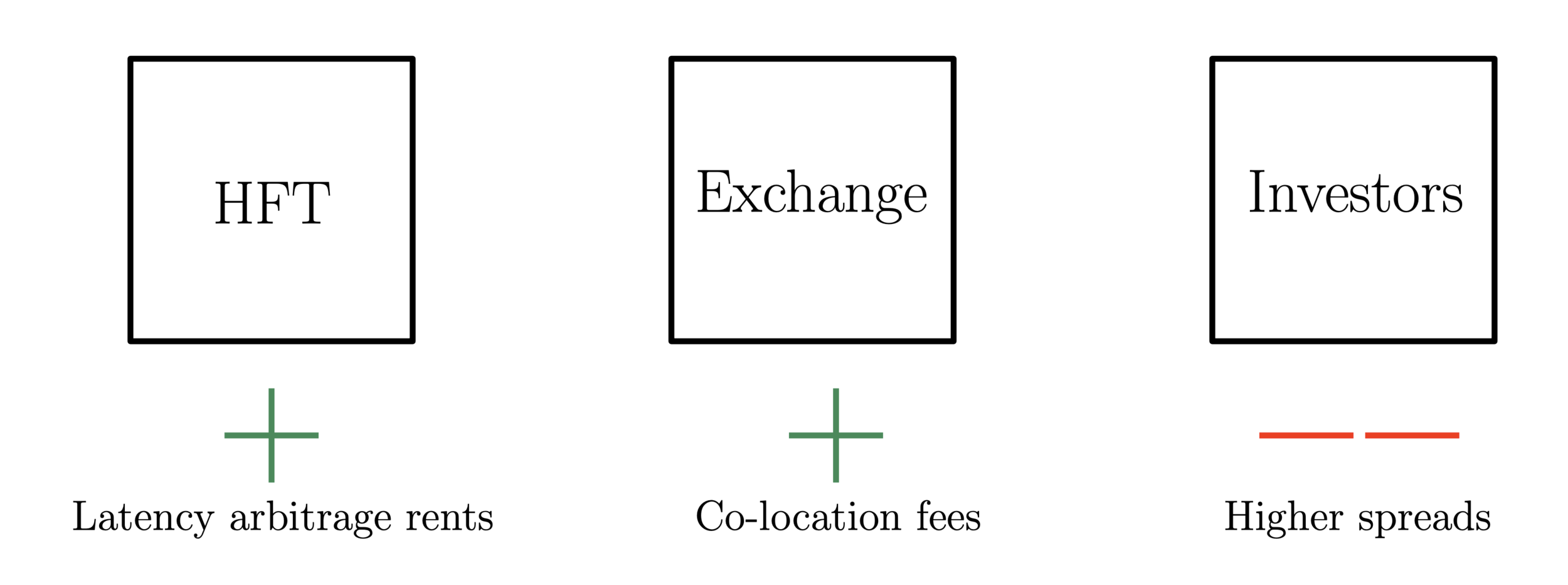

- Exchanges charge HFTs for "co-location": revenues between $874M-$1024M in 2018

- Co-location revenue on par with trading fees revenue.

How much speed do we really need?

Our paper

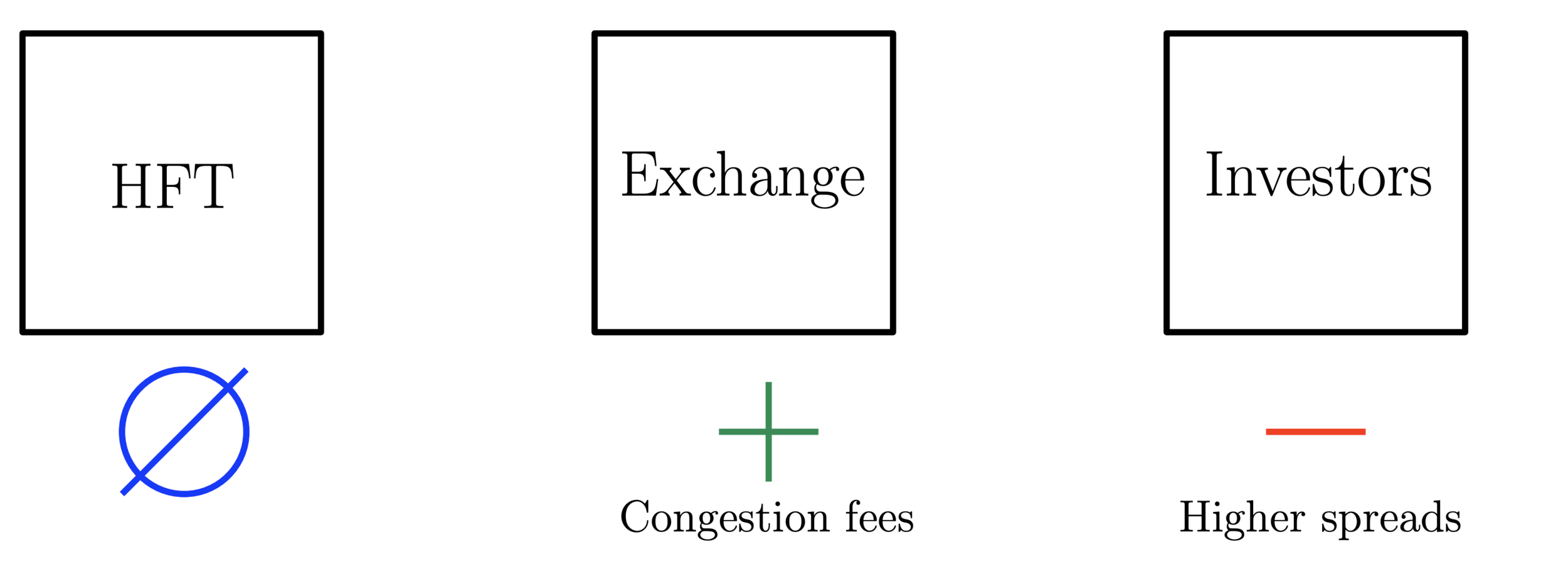

- Main idea: Surge pricing of speed (à la Uber).

- How? Implement a congestion fee on liquidity taking orders.

- Charge a uniform fee to each liquidity-taking order message whenever there are multiple take orders in a short time interval.

- Fee level the number of take orders, surging during micro-bursts.

- Latency arbitrage externalities are (partially) priced in.

- A system that is incentive-compatible for exchanges.

\uparrow

Status quo: Latency arbitrage rent-sharing

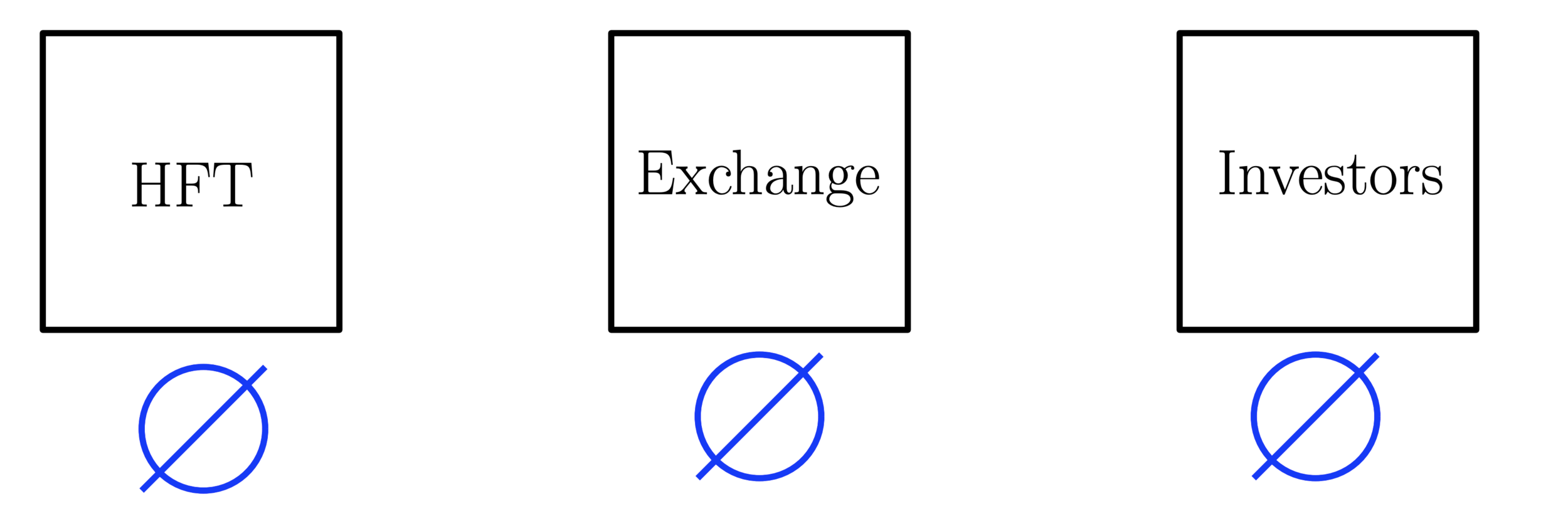

Ideal world: No latency arbitrage rents

Our idea: Incentive-compatible rent transfer from HFTs to investors

Asset

- One risky asset, for which news arrives with probability .

- It pays off:

\delta

\tilde{v}=\begin{cases}

v+\sigma, & \text{if ``good news'' arrives} \\

v-\sigma, & \text{if ``bad news'' arrives} \\

v, & \text{if no news arrives}.

\end{cases}

Traders

- risk-neutral high-frequency traders (HFT) who submit market or limit orders.

- Liquidity investors (also risk neutral), arrive at the market with probability .

- Liquidity investors only submit market orders are equally likely to buy/sell.

H\geq 3

1-\delta

Congestion fee

If HFT "snipers'' submit a marketable order simultaneously, each is charged a fee

k\geq 2

f\left(k\right)=\begin{cases}

\phi \left(k-1\right) & \text{ if } k\geq 2 \\

0 & \text{ if } k=1.

\end{cases}

- Congestion fee number of liquidity-taking orders received by the exchange in a short time interval (100 s to 10 ms).

- Single marketable order arrives congestion fee is zero.

- Congestion fees are computed from intraday, but charged daily (or monthly, even).

- Unlikely that liquidity traders pay congestion fees. Estimated total duration of HFT races in FTSE100 stocks:

\propto

\mu

\Rightarrow

537 \text{ races/day} \times 81 \text{ $\mu$s/race} = 0.043 \text{ seconds/day}.

Impact of fee on liquidity and race intensity

A larger congestion fee leads to:

- Narrower spreads;

- Lower sniping probability

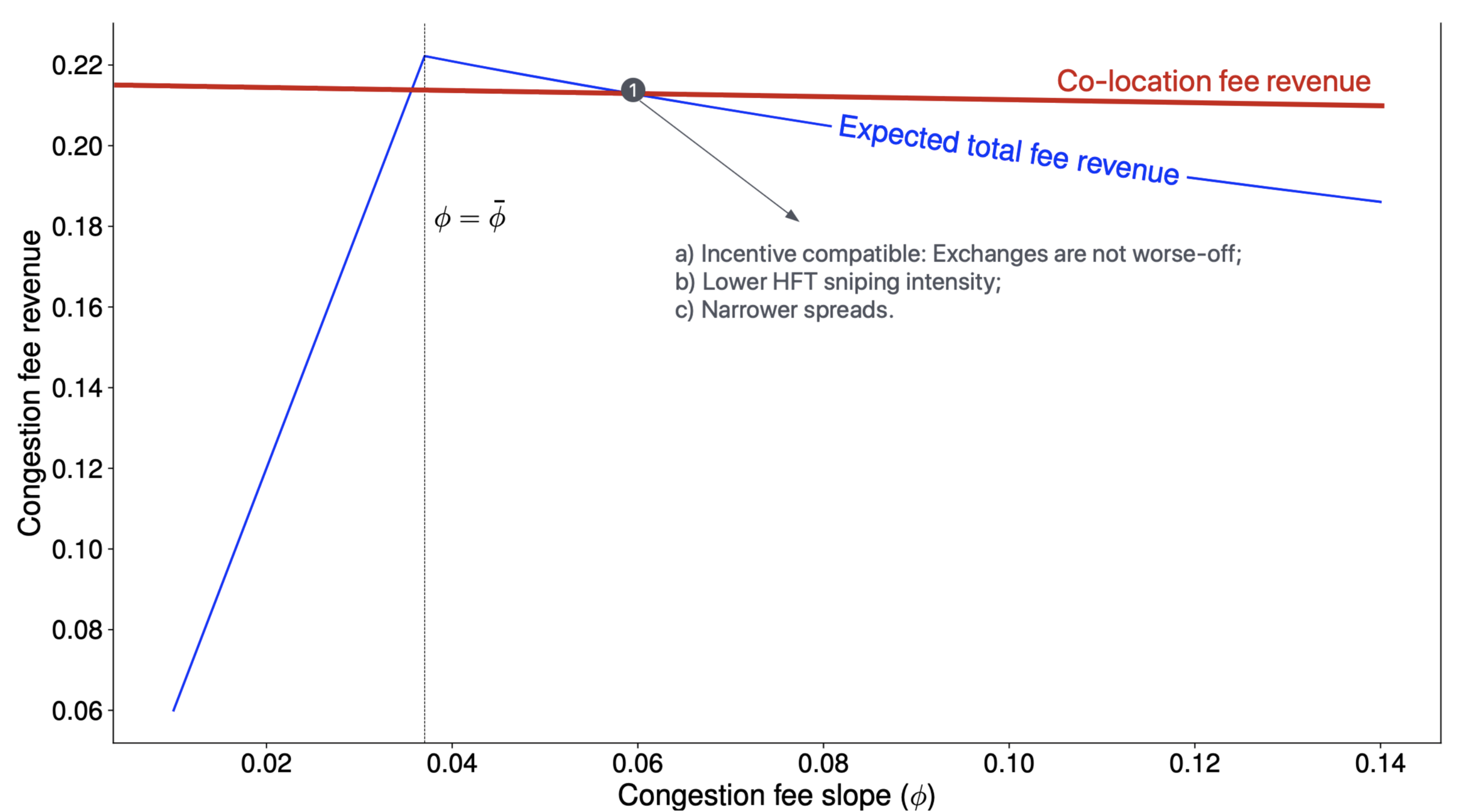

What about fee revenues?

- Direct effect: implies higher revenues for each trade;

- Indirect effect: reduces HFT incentives to snipe less intense races.

\phi \nearrow

\phi \nearrow

\Longrightarrow

A regulator’s optimal fee choice

- Implement a "surge pricing of speed'' (a la Uber) on liquidity taking orders.

- Charge HFTs a fee whenever there are multiple liquidity-taking orders in a short time interval.

- Quick calibration indicates fee in the range of 15%-35% relative to the average arbitrage opportunity. (using Aquilina, Budish, and O'Neill, 2020).

- Latency arbitrage externalities are (partially) priced in.

- Incentive-compatible for exchanges (i.e., competition-proof vs. co-location fees).