Book 2. Credit Risk

FRM Part 2

CR 15. Counterparty Risk and Beyond

Presented by: Sudhanshu

Module 1. Counterparty Risk

Module 2. Managing, Mitigating and Quantifying Counterparty Risk

Module 1. Counterparty Risk

Topic 1. Counterparty Risk vs. Lending Risk

Topic 2. Transactions With Counterparty Risk

Topic 3. Institutions that take on Counterparty Risk

Topic 4. Counterparty Risk Terminology

Topic 1. Counterparty Risk vs. Lending Risk

-

Counterparty Risk

-

Risk that a counterparty is unable or unwilling to fulfill contractual obligations (i.e., counterparty defaults)

- In derivatives contracts, default occurs presettlement—after contract inception but before contract end—preventing current and future required payments

- Characterized by uncertainty in underlying instrument value (both absolute amount and which party gains/loses)

- Bilateral risk: both parties face default risk; the "winning" party faces risk that the "losing" party defaults

-

- Lending Risk

- Principal amount at risk is typically known with reasonable certainty (e.g., fixed-rate mortgage)

- Unilateral risk: only one party assumes the risk

- More straightforward than counterparty risk due to known exposure amounts and one-sided risk profile

Practice Questions: Q3

Q3. Which of the following statements regarding counterparty credit risk is most accurate?

A. Counterparty risk is unilateral.

B. Over-the-counter (OTC) derivatives contain less counterparty risk than exchange-traded derivatives because the counterparty is known.

C. The precise future value of the contract is uncertain, but the counterparties are aware of whether the future value will be positive or negative.

D. Counterparty risk is typically associated with counterparty default prior to the settlement rather than default during the settlement process.

Practice Questions: Q3 Answer

Explanation: D is correct.

Counterparty risk is a bilateral risk in that both parties are unaware of the eventual value of the contract and they do not know whether they will earn a profit or loss. For exchange-traded derivatives, the counterparty is the exchange, which effectively mitigates counterparty risk. While counterparty default can happen presettlement and during settlement, counterparty risk typically applies to the risk of default prior to settlement.

Topic 2. Transactions with Counterparty Risk

-

Exclusion of Exchange-Traded Funds: Exchange-traded derivatives do not carry counterparty risk because the exchange is usually the counterparty

-

Transactions with counterparty credit risk include securities financing transactions and OTC derivatives.

-

Over-the-Counter (OTC) Derivatives: OTC derivatives, unlike exchange-traded derivatives, carry counterparty risk.

-

Interest Rate Swaps: Counterparty risk is reduced compared to a regular loan because no principal is exchanged, and netting reduces the risk by only exchanging the net difference between payments.

-

Foreign Exchange Forwards: These carry significant counterparty risk due to the exchange of notional amounts and long maturities.

-

Credit Default Swaps (CDSs): These have large counterparty risks due to wrong-way risk and significant volatility. Wrong-way risk is an increase in exposure when the counterparty's credit quality worsens.

-

-

Securities Financing Transactions: These transactions, which include repos, reverse repos, and securities borrowing and lending, carry counterparty risk.

-

Repos and Reverse Repos: Counterparty risk exists because the seller may fail to repurchase the security. This risk is mitigated by using collateral, but a risk remains that the collateral's market value could decline. A haircut is applied to the collateral to account for this potential decline in value.

-

Topic 2. Transactions with Counterparty Risk

-

Exclusion of Exchange-Traded Funds: Exchange-traded derivatives do not carry counterparty risk because the exchange is usually the counterparty

-

Transactions with Counterparty Credit Cisk include:

-

Securities Financing Transactions: Repos and reverse repos, securities borrowing and lending

-

OTC Derivatives

-

-

Repos and Reverse Repos: Short-term lending agreements (as short as one day) where a party sells securities for cash and agrees to repurchase them later; lender receives repo rate (risk-free rate plus counterparty risk premium)

- Haircut Mechanism: Applied to mitigate borrower default risk and collateral value decline

- Example: 2% haircut on $100 million loan requires $102.04 million in securities collateral [$100M / (1 - 0.02)]

- Residual Counterparty Risk: Exists if seller fails to repurchase securities at maturity (forcing buyer to liquidate collateral) or if collateral market value declines before maturity

- Haircut Mechanism: Applied to mitigate borrower default risk and collateral value decline

- Securities Borrowing and Lending: Similar to repos but involve securities rather than cash with comparable counterparty risk profile

Topic 2. Transactions with Counterparty Risk

-

OTC Derivatives

- Interest Rate Swaps

- Market Size: Constitute the bulk of OTC derivative transactions

- Reduced Counterparty Risk: No principal exchange, only floating versus fixed cash payment exchanges

- Netting Benefit: Only net payment difference is exchanged periodically; non-defaulting party stops payments immediately upon counterparty default

- Foreign Exchange Forwards

- High Counterparty Risk Drivers: Large notional amount exchanges and long maturities increase default probability over the contract life

- Credit Default Swaps

- High Counterparty Risk Factors: Wrong-way risk and significant volatility increase probability of losing party defaulting

- Wrong-Way Risk: Exposure increases when counterparty credit quality worsens

- Example: Buying CDS on Greek sovereign debt from a Greek bank; when Greek debt rating declines, the CDS buyer benefits but the Greek bank's ability to pay deteriorates simultaneously

- Interest Rate Swaps

Practice Questions: Q1

Q1. When considering counterparty credit risk, which of the following financial products has the largest outstanding notional amount in the marketplace?

A. Credit default swaps.

B. Foreign exchange forwards.

C. Interest rate swaps.

D. Repos and reverse repos.

Practice Questions: Q1 Answer

Explanation: C is correct.

There are two classes of financial products where counterparty risk exists: over- the-counter (OTC) derivatives and securities financing transactions such as repos and reverse repos. OTC derivatives are significantly larger with interest rate swaps comprising the bulk of the market.

Topic 3. Institutions that take on Counterparty Risk

- Large Derivatives Players: Trade with each other and extensive client base with high volumes of OTC derivatives across books

- Cover very wide range of asset classes: commodities, equity, foreign exchange, interest rate, and credit derivatives

- Consistently post collateral against positions

- Medium Derivatives Players: Serve large client base and conduct high volume of OTC derivatives trades

- Cover wide asset range but less active than large players across all asset classes

- Likely (but not definite) to post collateral against positions

- Small Derivatives Players: Have specific derivatives requirements that determine trades undertaken

- Trade with only small number of counterparties with few OTC derivatives on books

- Typically specialize in single asset class

- Post collateral less frequently; when posted, often illiquid

- Third-Party Risk Management Services: Provide products and services to reduce counterparty risks and improve market efficiency

- Offerings include: clearing services, specialized software, trade compression, and collateral management solutions

Topic 4. Counterparty Risk Terminology

- Credit Loss: Loss conditional on counterparty default; occurs when one party (creditor) has positive contract value owed by the other party (debtor) who defaults

- Exposure Quantification:

- Replacement cost is more relevant than full principal amount at risk

- Must consider current exposure (claims and commitments), future exposure (potential future claims), and contingent liabilities

- Typically assumes zero recovery value in calculations

- Credit Migration: Counterparty may default or experience credit rating changes over contract term; assessment requires analyzing term structure of default probability

- Probability of Default (PD) Patterns:

- Future PD typically decreases over time (higher likelihood default occurred earlier)

- Expected credit deterioration suggests increasing PD

- Expected credit improvement suggests decreasing PD

- Empirical mean reversion: strong ratings tend to deteriorate, weak ratings tend to improve

- PD Measurement: Two approaches - real (historical) measure identifying actual PD, and risk-neutral measure computing theoretical market-implied PD

- Recovery Rate: Portion of outstanding claim recovered after default; LGD = 1 - RR

- Mark-to-Market (MtM): Sum of MtM values of all contracts with a counterparty representing current potential loss; equals PV of expected inflows - expected payments, serving as replacement cost measure but excluding factors like netting, collateral, hedging, transaction costs, and bid-ask spreads

Practice Questions: Q2

Q2. Liz Parker is a junior quantative analyst who is preparing a report dealing with credit migration. An excerpt of her report contains the following statements:

I. Future default probability will likely increase over time, especially for periods far into the future.

II. When computing the default probability of a counterparty under a risk-neutral measure, we need to first determine the actual default probability.

Which of Parker’s statements is (are) correct?

A. I only.

B. II only.

C. Both I and II.

D. Neither I nor II.

Practice Questions: Q2 Answer

Explanation: D is correct.

Future default probability will likely decrease over time, especially for periods far into the future. This is because of the higher likelihood that the default will have already occurred at some earlier point. In computing the default probability of a counterparty under a risk-neutral measure, one needs to compute the theoretical market-implied probability; the actual default probability applies under a real (historical) measure.

Module 2. Managing, Mitigating and Quantifying Counterparty Risk

Topic 1. Managing Counterparty Risk

Topic 2. Mitigating Counterparty Risk

Topic 3. Quantifying Counterparty Risk

Topic 4. OTC Derivatives Costs

Topic 5. X-Value Adjustment (xVA) Terms

- Trading with High-Quality Counterparties: Simple approach involving only AAA-rated counterparties who may not require collateral posting

- Cross-Product Netting: Aggregates derivative transactions with both positive and negative values in case of default, reducing bilateral risk

- Must consider legal risk (enforceability) and operational risks

- Close-Out: Immediate closing of all contracts with defaulted counterparty, combined with netting of mark-to-market values

- Institution offsets what it owes against what it is owed

- Results in immediate payment (if net negative) or claim (if net positive)

- Collateralization (Margining): Collateral agreement requiring sufficient collateral posting to support net exposure between counterparties

- Theoretically reduces net exposure to zero

- Involves market, operational, and legal risks plus significant administrative work

Topic 1. Managing Counterparty Risk

- Walkaway Feature: Allows non-defaulting party to cancel transactions if counterparty defaults

- Advantageous when party has negative mark-to-market position

- Diversification of Counterparty Risk: Limits credit exposure to any single counterparty based on their default probability

- Trading with multiple counterparties reduces impact of any single failure

- Exchanges and Centralized Clearinghouses: Act as counterparty to all trades, guaranteeing transactions and removing bilateral counterparty risk

- May redistribute rather than eliminate counterparty risk

Topic 1. Managing Counterparty Risk

Practice Questions: Q1

Q1. Ondine Financial, Inc., (Ondine) uses a variety of techniques to manage counterparty risk. It has entered into an interest rate swap with Scarbo, Inc. (Scarbo). Currently, Ondine’s position in the swap has a –$1 million mark-to-market value. Based on the information provided, which of the following credit risk mitigation techniques would be most advantageous to Ondine if Scarbo

defaults?

A. Close-out.

B. Collateralization.

C. Netting.

D. Walkaway.

Practice Questions: Q1 Answer

Explanation: D is correct.

Because Ondine currently has a negative mark-to-market value and the counterparty is defaulting, Ondine is able to cancel the transaction while it is “losing.” Netting and close-out would require Ondine to make a payment because it would owe a net amount of $1 million. Collateralization is not relevant in this scenario.

Topic 2. Mitigating Counterparty Risk

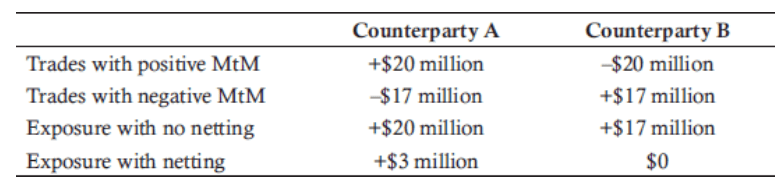

- Netting: Compute and offset each party's required payment so only the net debtor makes payment; effectiveness depends on the nature of payments and ease of offsetting

- Collateralization: Taking collateral equal to or greater than notional principal can theoretically eliminate counterparty risk

- Administrative costs and operational burden

- Liquidity risk: collateral may need to be sold at significant discount in short term

- Legal risk: title acquisition process may be lengthy and complex

- Hedging with Credit Derivatives: Reduces counterparty exposure to own clients by transferring exposure to competitor's clients; generates market risk in exchange for reduced counterparty risk

- Central Counterparties (CCPs): Exchanges and clearinghouses act as central counterparty to centralize risks, settle transactions, and reduce bilateral derivative contract risks

- Reduces incentive for parties to carefully assess and monitor counterparty risks

- Generates operational, liquidity, and systemic risks

Practice Questions: Q2

Q2. Which of the following methods of mitigating counterparty risk is most likely to generate systemic risk?

A. Netting.

B. Collateral.

C. Hedging.

D. Central counterparties.

Practice Questions: Q2 Answer

Explanation: D is correct.

Mitigating counterparty risk often leads to the generation of other types of risk. In the case of central counterparties, systemic risk is created as counterparty risk has been centralized with a limited amount of groups. If one of these groups fails, a substantial shock may be experienced by the financial system as a whole.

Topic 3. Quantifying Counterparty Risk

- Three Levels of Counterparty Risk Quantification:

- Trade level: Considers the nature of the trade and related risk factors

- Counterparty level: Accounts for risk mitigating factors such as netting and collateral for each individual counterparty

- Portfolio level: Recognizes that only a small percentage of counterparties will likely default in a given time period

- Credit Value Adjustment (CVA): The portion of derivatives pricing that accounts for counterparty risk (excluding the portion that assumes no counterparty risk); traders aim to earn returns greater than the CVA

- CVA vs. Credit Limits: CVA examines counterparty risk at trade and counterparty levels, while credit limits control exposures at the portfolio level; both tools complement each other in quantifying and managing counterparty risk

- Contrasting Objectives: CVA aims to minimize the number of counterparties to maximize netting benefits, while credit limits aim to maximize the number of counterparties to achieve greater diversification benefits

Topic 4. OTC Derivatives Costs

- The lifetime economic costs of OTC derivatives depend on whether the transaction has a positive or negative MtM.

-

Positive Mark-to-Market (In the Money)

- Counterparty risk and funding costs arise from any uncollateralized exposure

- For collateralized portion, the counterparty selects the type of collateral to post

-

Negative Mark-to-Market (Out of the Money)

- Counterparty risk stems from the party's own potential for default

- Funding benefit arises from any collateral not posted

- For collateralized portion, the party itself chooses the type of collateral to post

-

Common to Both Scenarios

- Funding costs associated with capital requirements for the transaction and initial margin apply regardless of whether MtM is positive or negative

-

Topic 5. X-Value Adjustment (xVA) Terms

- xVA Overview: Captures the impact of counterparty risk, collateral, funding, and capital; components generally represent costs but some may provide benefits

- Credit Value Adjustment (CVA): Measures counterparty credit risk from the institution's perspective

- Debt Value Adjustment (DVA): Defines counterparty risk from the counterparty's point of view; related component to CVA

- Funding Value Adjustment (FVA): Cost and benefit resulting from funding a transaction

- Collateral Value Adjustment (ColVA): Cost and benefit from embedded options in collateral agreements and additional collateral terms

- Capital Value Adjustment (KVA): Cost of holding regulatory capital over the transaction's duration

- Margin Value Adjustment (MVA): Cost of posting margin over the transaction's duration