Book 2. Credit Risk

FRM Part 2

CR 18. Central Clearing

Presented by: Sudhanshu

Module 1. Central Counterparties

Module 2. CCP Risk Management

Module 3. Central Clearing Market Impact

Module 1. Central Counterparties

Topic 1. Central Counterparty (CCP)

Topic 2. Mechanics of Central Clearing

Topic 3. Novation

Topic 4. Netting, Multilateral Offset and Compression

Topic 1. Central Counterparty (CCP)

- CCP Purpose: Central counterparties serve as a solution for systemic risk mitigation by providing clearing services for various types of financial transactions between member firms

- Complete Clearing Process: CCPs engage in "complete clearing" by standing in the middle of previously bilateral over-the-counter (OTC) transactions, operating as the buyer for every seller and seller for every buyer

- Counterparty Risk Transfer: Through the clearing process, the original counterparty is no longer a direct risk as the CCP becomes the new counterparty for all transactions

- Bilateral Structure Replacement: Traditional bilateral counterparty structures where default risk is directly borne by individual counterparties are replaced by centralized clearing

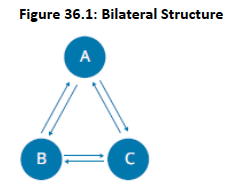

- Example: Fig 36.1 shows a traditional bilateral counterparty structure where default risk is directly borne by the individual counterparties.

Topic 1. Central Counterparty (CCP)

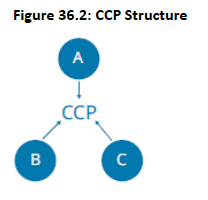

- CCP as Middleman: The CCP acts as the central intermediary in all risk transactions, fundamentally changing the traditional bilateral risk structure shown in Fig 36.2

- Reduced Interconnectedness and Enhanced Transparency: CCPs reduce market interconnectedness because Party A is no longer directly exposed to the full losses of Party B or Party C; the CCP gains complete visibility of all member positions, increasing market transparency

- Indirect Access Complexity: Some counterparties (non-members like Party D) access the CCP indirectly through member firms acting as conduits (e.g., Party D clears transactions through member firm Party C)

- Added Operational Layers: Indirect access arrangements introduce additional complexity in margin transfer processes and default management scenarios, as the CCP must manage relationships through intermediary member firms rather than directly with all participants

Topic 1. Central Counterparty (CCP)

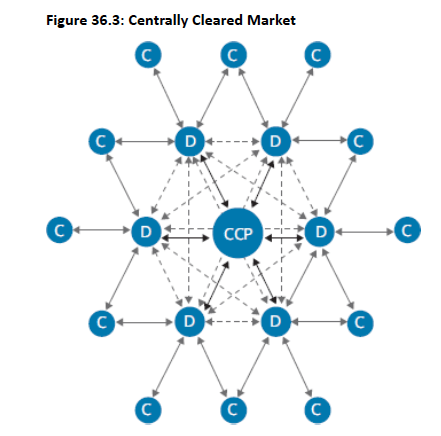

- Centrally Cleared Market: Fig 36.3 shows a centrally cleared market with bilateral transactions (dotted lines), directly-cleared transactions (black lines), and non clearing members (C) who must clear with the assistance of clearing members (D) (gray lines).

- Some OTC derivatives that cannot be centrally cleared can only exist as bilateral transactions.

- Interconnectedness Concerns: Members may participate in multiple CCPs, creating cross-CCP interconnectedness that must be monitored

- Concentration Risk: Despite clear advantages, central clearing creates significant concentration risk where a major error or failure at the CCP level could prove disastrous for all involved members

Topic 2. Mechanics of Central Clearing

-

CCP Business Model and Optimal Number:

- Revenue Sources: CCPs operate primarily by charging fees on all trades, with secondary income from earning returns on assets in their possession

- Monopolistic vs. Competitive Structure:

- Arguments for fewer CCPs: Multilateral netting benefits reduce risk exposures and provide economies of scale; monopolistic control avoids concerns about CCP credit quality competition

- Arguments for more CCPs: Jurisdictional fragmentation, product variety, need for competition, and mitigation of severe systemic risk from single CCP collapse

- Jurisdictional and Product Considerations: Local currency clearing requirements (e.g., USD, EUR) and regulatory mandates for national/regional CCPs support multiple entities; wide range of OTC derivatives requires product-specialized CCPs

-

CCP Ownership Models:

- Vertical Scheme: Exchange owns the CCP, which operates as a unit clearing only products associated with that specific exchange

- Horizontal Scheme: Clearing members collectively own the CCP without ties to a specific exchange, enabling transactions across wider range of markets and asset classes; works best for bilateral OTC derivatives and promotes greater competition, lower costs, and higher clearing service standards favored by regulators

Topic 2. Mechanics of Central Clearing

-

Derivatives Products Characteristics for CCP Clearing

- Standardization: OTC derivatives (e.g., credit default swaps) must be standardized to enable CCP legal liability for all cash flows and facilitate netting of same or similar contracts

- Complexity: Only non-exotic, less complex derivatives are clearable; exotic derivatives' unique features create valuation difficulties affecting initial and variation margin computations and increase under-margining or over-margining risks

- Liquidity: CCPs can only clear liquid products; illiquid products create pricing issues due to limited information and historical data, complicate valuation model calibration, and extend time horizons for replacing defaulted positions

- Wrong-Way Risk (WWR): Products with WWR (positive correlation between default risk and credit exposure) are not optimal for CCPs; increases complexity and risk exposures from CCP member defaults

- Market Volume: Sufficient market volume is necessary to justify upfront costs of developing product-clearing expertise

Practice Questions: Q1

Q1. There are numerous challenges when clearing over-the-counter (OTC) derivative products through a central counterparty (CCP). Which of the following lists best summarizes the key challenges for central clearing of OTC derivative products?

A. Illiquid products, jurisdictional fragmentation, presence of wrong-way risk, and legal concerns.

B. Lack of standardization, increased counterparty risk, increased dependency risk, and less transparency.

C. Jurisdictional fragmentation, increased counterparty risk, less transparency, and standardization.

D. Product complexity, illiquid products, presence of wrong-way risk, and lack of standardization.

Practice Questions: Q1 Answer

Explanation: D is correct.

Lack of standardized products, complexity, illiquid products, and the presence of wrong-way risk are characteristics of OTC derivative products that make CCP clearing challenging. OTC derivative products need to be standardized before they can be cleared through a CCP. More complex and illiquid derivative products are problematic for CCPs because their unique features make them difficult to value. Products with wrong-way risk are also more complex and create additional concerns for CCPs in the event of default.

- Novation Process: In the event of default, a CCP replaces nonperforming contracts by closing out the bilateral contract and substituting itself as the new counterparty capable of meeting obligations; original parties no longer have contractual obligations to each other as the CCP assumes counterparty risk

- Market Neutrality and Matched Book: CCPs maintain market neutrality by netting buy-side transactions with offsetting sell-side transactions, creating a matched book; transactions are guaranteed once buyers and sellers are matched

- Default-Induced Market Risk: Market risk emerges upon party default because the matched book is disrupted; CCP may sell off the defaulting party's positions to restore balance

- Loss Mutualization: CCPs require default fund contributions from all member firms to mutualize losses and spread them across many market participants rather than concentrating risk with a single party

Topic 3. Novation

- Bilateral Market Redundancy: The bilateral derivatives market contains significant redundant transactions that elevate counterparty risk levels

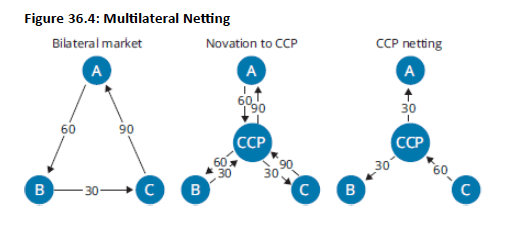

- Netting and Multilateral Offset (Fig 36.4): shows the progression from bilateral market liabilities to CCP novation to final netted positions, demonstrating risk reduction through multilateral offset

- Bilateral Market Example: Total liabilities of 180 (30 + 60 + 90); if Party C defaults on 90 owed to Party A, Party A may also default on 60 owed to Party B due to insufficient funds

- CCP Novation: CCP steps into the middle of all parties enabling transaction netting; Party A's two CCP transactions (60 and 90) net to 30

- Risk Reduction: Party C's liability reduced from 90 to 60; Party A no longer owes 60 to Party B but is instead owed 30 by the CCP

- Key Advantage: CCPs achieve multilateral offsets for cash flows and margins without canceling transactions

Topic 4. Netting, Multilateral Offset and Compression

- Compression: Cancellation of offsetting contracts on a gross basis, replacing multiple contracts with fewer ones while maintaining net exposures

- Example: 10 offsetting transactions between Parties A and B with $1 million gross exposure and $250,000 net exposure to Party A can be compressed to 5 transactions with $350,000 gross exposure, maintaining the same $250,000 net exposure

- Benefits: Reductions in initial margin requirements, regulatory capital, and administrative work for margin calculations and reporting

- Compression vs. Multilateral Offset: Multilateral offset compresses risk without canceling transactions, whereas compression actively cancels and substitutes contracts; both can be used together with central clearing for maximum efficiency

- Market Trends: Notional amounts cleared continue to increase for interest rate swaps while total outstanding notional remains stable; compression techniques are becoming more sophisticated, including ability to compress positions with identical cash flow dates but different fixed rates

Topic 4. Netting, Multilateral Offset and Compression

Module 2. CCP Risk Management

Topic 1. Margin and Default Funds

Topic 2. CCP Risks Management

Topic 3. CCP Loss Waterfall

Topic 4. CCP Losses Absorption

Topic 1. Margin and Default Funds

- Initial Margin: Beginning deposit required from all members to cover future potential default losses in a worst-case scenario; depends primarily on market risk rather than clearing member credit quality

- Variation Margin: Additional margin required to account for daily price changes in asset positions

- Intraday margin calls used during periods with large market movements

- Similar to initial margin, based on market risk rather than credit quality

- Initial Margin Determination Factors:

- Time period of CCP exposure to a position

- Required confidence level (percentage of default scenarios covered, usually 99% or higher)

- Goal is sufficient loss provision so defaults don't require coverage by other members

- Loss Mutualization: Members contribute to CCP's default fund at a level covering potential losses with high confidence, rather than prohibitively high 100% coverage of individual potential losses

- Indirect Liability: Members may be liable for a share of default losses through the loss allocation process even without direct dealings with the defaulting member or net position with the CCP

Topic 2. CCP Risks Management

-

Membership Requirements

-

Risk-Based Criteria: CCPs impose requirements focusing on creditworthiness (low default likelihood), liquidity (ability to cover margin calls quickly), and compliance with CCP rules

- Ongoing Requirements: Accepted clearing members must maintain minimum capital base, contribute to default funds, and participate in default management

-

-

Margin Requirements

- Variation Margin: Typically only cash is accepted; netting possible in single currency but not across different currencies

- Initial Margin: Cash and highly liquid government securities accepted; calculated using complex scenarios of price changes during a specified trade horizon

- Margin Investment: CCPs hold significant margin amounts and must conservatively invest these funds in low-risk investments to generate income for paying interest on excess cash deposited

Topic 2. CCP Risks Management

-

Member Default Management

-

Primary Risk: Default creates unmatched book when defaulting member (with losses) fails to make variation margin payment; CCP must pay instead to members with gains

- Macro-Hedging: Default management group aims to significantly reduce portfolio exposure to major market risks (e.g., interest rate volatility) quickly

- Auction Process:

- CCP liquidates defaulted member's portfolio through auctions of subportfolios to members

- Members incentivized to participate to minimize collective loss and avoid loss waterfall

- Macro-hedges reduce market risk in subportfolios, increasing attractiveness and bid prices

- Porting Option: Most efficient approach is porting defaulted member's trades to surviving member on "as is" basis; if unsuccessful, proceeds to default management using initial margins to cover losses

-

Topic 2. CCP Risks Management

-

Margin Period of Risk (MPoR)

-

Definition: Also known as liquidation period; lowered through frequent (at least daily) cash collateral calls and rapid position close-out

- Three Distinct Periods:

- Predefault: From member's most recent margin posting until CCP declares default

- Macro-Hedging: Most important market risks reduced substantially and quickly using liquid hedges

- Auctions: Defaulting member's portfolio sold off with risk decreasing to zero as each auction concludes and positions close

-

Practice Questions: Q1

Q1. Which of the following statements regarding risk management by central counterparties (CCPs) is most accurate?

A. Netting in different currencies is possible.

B. Only cash is accepted as variation margin.

C. An important source of returns for CCPs is the interest earned on held assets.

D. During the margin period of risk (MPoR), most of the risk is reduced with auctions where the defaulting member’s portfolio is sold off.

Practice Questions: Q1 Answer

Explanation: B is correct.

Usually, only cash is accepted as variation margin. Netting in a single currency is possible but not in different currencies. CCPs operate primarily by charging fees on all trades and to a lesser extent by earning income on the assets in their possession. The most important risks are reduced substantially and quickly using liquid hedges via macro-hedging.

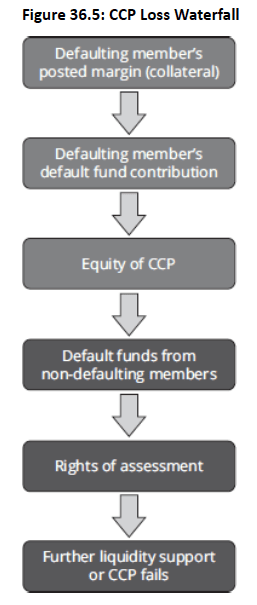

Topic 3. CCP Loss Waterfall

-

Illustration: Fig 36.5 illustrates how CCP member defaults are absorbed in a loss waterfall.

-

Stage 1-2: Defaulting Member's Contributions

- Initial margin posted by the defaulting member when the transaction was initiated

- Daily variation margin from mark-to-market adjustments

- Defaulting member's default fund contributions

- Stage 3: CCP's Own Capital ("Skin in the Game")

- CCP deploys its own equity capital to cover remaining losses

- Limited to an amount that allows the CCP to continue functioning normally

- Incentivizes CCP to set sufficiently high initial margins and default fund requirements

- Stage 4: Loss Mutualization - Surviving Members

- Default fund contributions from non-defaulting (surviving) members are utilized

- Loss allocation may be pro rata or favor members who participated successfully in the auction of the defaulted portfolio

-

Practice Questions: Q2

Q2. Given the following three events, what is the proper order of the CCP loss waterfall?

I. Non defaulting member’s default fund contributions are exhausted.

II. Defaulting member’s collateral and default fund contributions are exhausted.

III. CCP taps an amount of its equity that enables them to function normally.

A. I, II, III.

B. II, I, III.

C. II, III, I.

D. III, II, I.

Practice Questions: Q2 Answer

Explanation: C is correct.

The first layer in the loss waterfall is for the defaulting member’s collateral and default fund contributions to be exhausted. The next layer is for the CCP to tap into its own equity to the point where it could still function normally. Non defaulting members will then have their default funds exhausted before moving to the rights of assessment.

Topic 4. CCP Losses Absorption

-

Rights of Assessment

- Additional contributions required from member firms when default fund is significantly depleted (e.g., 25% liquidated) to restore the fund and prevent CCP collapse

- Usually limited to a specific amount per period to avoid onerous cash outflows during economic downturns when members are least able to contribute

-

Variation Margin Gains Haircutting (VMGH)

- CCP "discounts" incremental margin paid to members with gains, providing only partial payment while requiring full satisfaction of amounts owed to the CCP

- Assumes losses from defaulting members have corresponding gains for other members

- Success depends on CCP's ability to transact at midmarket prices; may fail if forced to transact at large premiums above midmarket

-

Tear-Up

- CCP cancels unmatched contracts with clearing members to restore a matched book by eliminating trades opposite to those of the defaulting member

- Key advantage: CCP avoids paying risk premiums that could occur with auctions

- Partial or complete tear-ups possible; complete tear-ups favor the CCP but impose losses and residual market risk on clearing members

Topic 4. CCP Losses Absorption

-

Forced Allocation

- Requires members to take specific positions at amounts specified by the CCP

- Similar end result to tear-up but existing trade is not canceled; member may be forced into reverse trades

- Does not require member to already have relevant trades in place (unlike tear-ups)

- Financial impacts cannot be passed to clients (unlike tear-ups which may allow this)

- Requires members to take specific positions at amounts specified by the CCP

-

Further Liquidity Support

- Loss allocation methods like tear-up and forced allocation impose potentially infinite liability on members, risking their survival if CCP needs are excessive

- CCP may require external liquidity support from well-capitalized entities like central banks, bank credit lines, or insurance company guarantees

- Full movement down the loss waterfall is an extremely low probability event

- Initial margin of non-defaulting members cannot be touched (initial margin haircutting prohibited), though infinite liability from other methods may make this protection ultimately irrelevant

Module 3. Central Clearing Market Impact

Topic 1. Bilateral Clearing

Topic 2. Central Clearing

Topic 3. Initial Margin and Default Fund

Topic 4. Advantages of Central Clearing

Topic 5. Disadvantages of Central Clearing

Topic 1. Bilateral Clearing

- Counterparty: Original counterparty remains in effect for the duration of the contract

- Available Products: No product limitations; any contract can be created as long as both parties agree to terms

- Eligible Participants: Open to all market actors; only exclusion is entities with credit so weak that no counterparty will trade with them

- Contract Netting: Must be manually and intentionally arranged; typically trades are not offset as participants are betting on specific events rather than seeking market neutrality

- Margining: Counterparties negotiate customized collateral arrangements with significant flexibility, though new regulatory rules are moving toward standardization

- Close-out of Default Positions: Can be messy; entirely between two counterparties and may quickly escalate to default of entire counterparty, not just the isolated transaction

- Loss Absorbency Cost: Primarily through capital, increasingly through initial margins

Topic 2. Central Clearing

- Counterparty: CCP replaces original counterparty by stepping into the middle of transactions; CCP becomes new counterparty with other CCP members as secondary counterparties

- Available Products: Limited to standardized, plain-vanilla (non-exotic), and liquid financial products to limit specialized contract risk

- Reduces loss potential but limits contract flexibility

- Eligible Participants: Restricted to clearing members (typically large financial institutions); other entities may clear through members if they post necessary collateral and find a willing sponsor

- Contract Netting: CCPs naturally maintain market neutrality by netting financial transactions, further spreading risk across the system

- Margining: Transparent, static, and non-negotiable collateral requirements and margin rules with daily or intra-day posting requirements for all member firms

- Close-out of Default Positions: Coordinated default process centered on loss waterfall mechanism

- Prevents single asset default from causing complete member firm default

- Minimizes internal operational costs and legal risk through rules-based relationship structure

- Loss Absorbency Cost: Primarily through initial margin and clearing member contributions to the default fund

Practice Questions: Q1

Q1. Which of the following statements is not an improvement that centrally cleared markets offer relative to bilateral markets? Centrally cleared markets:

A. remain market neutral by netting trades.

B. formalize the default workout process by using a loss waterfall structure.

C. offer more flexibility in contract selection because of their collateral collecting process.

D. improve the counterparty risk picture by replacing the original counterparty with a series of counterparties.

Practice Questions: Q1 Answer

Explanation: C is correct.

Bilateral markets permit any type of customized financial contract and customized collateral that is freely negotiated between the two bilateral parties. In a centrally clearedmarket, flexibility is reduced because contracts must be standardized, and collateral rules are fixed and nonnegotiable.

Topic 3. Initial Margin and Default Fund

- Initial Margin: Designed to provide very high likelihood (e.g., 99%) of sufficient coverage for losses from a member default; however, possibility remains that extreme losses may exceed initial margin coverage

- Default Fund: Covers losses not covered by initial margin through a risk pooling system that mutualizes large losses from one CCP member across all other members

- Provides greater loss absorbency than initial margin alone due to mutualization

- Allows relatively small contributions from each member while creating substantial total coverage

- Large Initial Margin / Small Default Fund Approach: Higher clearing costs but stronger risk discipline

- More consistent with "defaulter pays" principle, encouraging better member behavior

- Lower moral hazard incentivizes clearing members to provide portability (allowing clients to move portfolios to other clearing members)

- Small Initial Margin / Large Default Fund Approach: Lower clearing costs but elevated moral hazard

- Greater likelihood that losses are mutualized through default funds rather than borne by defaulter

- Discourages portability as insufficient initial margin may require clearing members to contribute additional amounts to default funds

Topic 3. Initial Margin and Default Fund

- Default Fund Sizing: Optimal size is difficult to compute due to extreme complexities; CCPs estimate size using stress tests

- Typically expressed as number of defaults the CCP can absorb (e.g., one or two major defaults)

- Loss allocation follows straightforward methods such as pro rata based on position size or initial margin contributions

Topic 4. Advantages of Central Clearing

- Transparency: CCPs can see aggregate risk concentrations across member firms' transactions, enabling early identification and mitigation of potential risks

- Multilateral Offset: Transparency enables risk offsetting, eliminating the need for members to monitor each other's creditworthiness and lowering margin costs for member firms

- Loss Mutualization: When a member defaults, the CCP manages it through a loss waterfall where losses may be shared by all members, reducing market impact and systemic risk

- Legal and Operational Efficiency: Netting and collateral policies increase operational efficiency and lower costs; rules-based structure minimizes legal costs

- Liquidity: Enhanced ability for members to trade and use multilateral offset improves market transparency and liquidity

- Default Management: CCPs manage defaults through orderly auctions of the defaulted member's positions, bringing market stability and securing optimal pricing

Topic 5. Disadvantages of Central Clearing

- Moral Hazard: Member firms have little incentive to vet other members' creditworthiness due to netting, collateralization, and loss mutualization processes

- Adverse Selection: CCP members often have superior knowledge on pricing and risk of derivative contracts compared to the CCP, leading members to trade with CCPs offering the best prices due to incomplete information

- Bifurcations: Requirement to clear only standard contracts creates a bifurcated market where some trades are cleared and others are not, reducing multilateral offset benefits

- Procyclicality: CCPs typically increase collateral requirements during volatile markets and economic stress, which can exacerbate potential default scenarios

Practice Questions: Q2

Q2. Following the financial crisis of 2007–2009, the roles of central counterparties (CCPs) were increased to reduce systemic risk through a centralized clearing process. Which of the following actions is not an advantage of the CCP in the centralized clearing process?

A. Increase transparency.

B. Manage loss mutualization.

C. Eliminate counterparty risk.

D. Improve operational efficiency.

Practice Questions: Q2 Answer

Explanation: C is correct.

CCPs reduce counterparty risk, but they do not eliminate this risk. Improved legal and operational efficiencies, increased transparency, and loss mutualization are major advantages of the CCP central clearing process.