Book 2. Credit Risk

FRM Part 2

CR 3. Credit Risk Management

Presented by: Sudhanshu

Module 1. Credit Risk Policies and Credit Asset Classification

Module 2. Loan Loss Provisioning and Credit Risk Assessment

Module 1. Credit Risk Policies and Credit Asset Classification

Topic 1. Elements of an Effective Lending Policy

Topic 2. Setting Exposure and Concentration Limits

Topic 3. Lending Policy and Credit Risk Reduction

Topic 4. Review of Loan Portfolio

Topic 4. Review of Bank's Policy

Topic 6. Credit Asset Classification

Topic 7. Nonperforming Loans (NPLs)

Topic 1. Elements of an Effective Lending Policy

-

Credit Risk and Bank Failure: Credit risk, or counterparty risk, is the chance a borrower will be late on or completely miss payments.

-

Credit risk is a major cause of bank failures, linked to about 70% of a bank's balance sheet.

-

-

Effective Lending Policy

-

A good lending policy should detail the bank's credit facilities and how risk is managed, including

-

origination,

-

appraisal,

-

internal supervision, and

-

collection procedures.

-

-

It's essential for policies to be flexible and adaptable to changing conditions.

-

Risk managers must have direct access to the board of directors for special issues.

-

Lending standards: Regulators require minimum lending standards covering risk identification, the bank’s credit risk philosophy, and clearly defined credit risk limits.

-

Policy categories: Lending policies generally fall into three groups:

-

reducing or limiting credit risk,

-

classifying assets by credit quality and collectability, and

-

establishing provisions for potential credit losses.

-

-

Practice Questions: Q1

Q1. Within their credit risk management plan, banks are either required to include, or at least should strongly consider including, a:

A. classification of risks organized by collectability.

B. loan loss provisions equal to at least 8 % of their loan portfolio.

C. duration target for the bank's portfolio that is not higher than 10.

D. rigid set of policies designed to address every possible risk source.

Practice Questions: Q1 Answer

Explanation: A is correct.

All banks should have a well-developed series of policies to manage credit risk

exposures. Policies should include recognizing and managing known risks. They need to be flexible to adapt to changing conditions. While regulators like to see established loan loss provisions and risk parameters, the specific targets are at the discretion of each bank because risk exposures are unique.

Topic 2. Setting Exposure and Concentration Limits

-

Concentration Limits

-

Definition: Concentration limits cap exposure to a single client, region, or sector, typically as a percentage of bank capital or reserves, with many jurisdictions setting client limits between 10% and 25% of capital.

-

Measurement challenges: Exposure sizing becomes complex for indirect credit forms (e.g., guarantees, letters of credit, contingent liabilities), and collateral is generally excluded when measuring exposure.

-

Single-client aggregation: A “single client” includes individuals, entities, or connected groups under common control, requiring aggregation of exposures.

-

Risk management concern: Large single-client exposures can bias risk assessment and create vested interests, so risk managers must continuously monitor events affecting major clients regardless of current payment performance.

-

-

Related Parties

-

Related-party influence risk: Related parties (such as parent or subsidiary entities, major shareholders, affiliated firms, directors, and executives) may exert undue influence over bank credit decisions.

-

Internal limits: To prevent preferential lending and policy violations, regulators typically cap related-party exposures as a percentage of Tier 1 capital; in the absence of such rules, banks should establish equivalent internal limits.

-

Practice Questions: Q2

Q2. A risk analyst is reviewing his bank's credit risk management policies. He notes that banks have limits on related-party financing decisions. His colleague agrees and correctly adds that:

A. the term single client only refers to a legal person.

B. all banks have a limit of 10 % of capital for a single client.

C. loan collateral should be included in exposure sizing using mark-to-market principles.

D. acceptances and letters of credit should be factored into the risk exposure of a single client.

Practice Questions: Q2 Answer

Explanation: D is correct.

Credit risk management should consider both related-party financing and concentration limits. The concern with a related-party transaction is either that a credit decision may be biased, or the loan terms may be more favorable than market norms. Concentration limits should be imposed to protect against overexposure to single client, region, or sector of the economy. Alternative credit (e.g., acceptances, lines of credit, guarantees, etc.) should be factored in as well, but collateral should not be considered when sizing risk exposures.

Topic 3. Lending Policy and Credit Risk Reduction

- Scope: A bank's credit facility scope should cover how loans are originated, appraised, supervised, and collected, with flexibility for changing market conditions.

-

Factors related to lending policy and risk reduction are as follows:

-

Lending authority: Lending policies should define approval limits for lending officers, with higher limits for more experienced staff or longer tenure, and be centralized in smaller banks or decentralized by geography, product, or customer type in larger banks.

-

Types and distribution of loans: Policies should specify permitted credit instruments based on officer expertise, deposit structure, and credit demand, with category limits (e.g., commercial, real estate, consumer) and Board approval required for exceptions.

-

Appraisal process: Risk is reduced by formally defining appraisal standards, including appraisal limits by credit type, reappraisal requirements for renewals, cases requiring independent appraisals, and maximum loan-to-value ratios.

-

Loan pricing: Loan rates should reflect cost of funds, supervision and administrative costs, expected loss, and a reasonable profit margin, with periodic reviews to adjust for market and competitive conditions.

-

Maturities: Policies should set maximum maturities by loan type, aligned with realistic repayment schedules, repayment sources, and the useful life of collateral.

-

-

Factors related to lending policy and risk reduction are as follows (...continued):

-

Geographic and sector concentration: Lending policies must address concentration risk by region or sector, including additional risks from international lending such as political and exchange rate risk.

-

Financial information requirements: Policies should define required borrower financial information, use of external credit checks, audit requirements, and alignment of financial projections with loan maturities.

-

Monitoring and collections: Policies should establish clear processes for ongoing monitoring of loans and management of collections.

-

Limits on total loans outstanding: Policy limits should link total lending to capital, deposits, or total assets, while also factoring in deposit volatility and known credit risks to control overall risk.

-

Loan-to-value and margin requirements: Maximum loan-to-market-value ratios should be set for pledged securities, with clear margin requirements and periodic collateral repricing to reduce risk.

-

Impairment recognition and restructured debt: Loan impairments must be identified and renegotiated debt (excluding simple extensions) should be closely monitored, as frequent restructurings signal elevated credit risk.

-

Documented policies: All lending policies and procedures must be documented through written internal guidelines rather than informal understanding.

-

Topic 3. Lending Policy and Credit Risk Reduction

Practice Questions: Q3

Q3. A regional bank wants to decrease risk in their lending practices. They are considering several lending policy changes. Which of the following items should be included in this new risk-reductionfocused direction?

A. All loans should have a maximum maturity schedule of 10 years.

B. The Board should approve all individual delinquency workout plans.

C. Financial projections from business clients should match the maturity of their loan.

D. Credit officers should have the flexibility to extend any type of credit that a customer needs as long as they find it to be a reasonable risk for the bank.

Practice Questions: Q3 Answer

Explanation: C is correct.

Some lending policy practices that reduce risk are matching the length of financial projections to loan maturities, only offering loans that match the bank’s targeted products, matching maturity to the type of loan and the source of funds for repayment, and having a formal delinquency workout policy. The Board should be aware of delinquency issues, but they do not need to approve each individual

workout plan when a solid policy is in place.

Topic 4. Review of Loan Portfolio

-

The bank’s loan portfolio should reflect the market demand for loans, the bank’s business and risk strategy, and its ability to extend credit.

-

Periodic reviews of the loan portfolio should include a random sample covering

-

at least 75% of the total loan portfolio by dollar amount,

-

at least 30% of the number of loans,

-

at least 50% of the number of all foreign loans, and

-

all loans with a maturity greater than one year

-

-

Additionally, loan portfolio reviews should include the following:

-

All loans to single clients whose aggregate exposure for the bank exceeds 5% of bank capital

-

All loans to related parties and shareholders

-

All loans whose terms have been altered since loan inception

-

All loans that are delinquent beyond 30 days

-

All loans classified as substandard, doubtful, or loss

-

Topic 4. Review of Loan Portfolio

-

Each individual loan review should include detailed documentation about:

-

the customer,

-

the loan terms,

-

the use of funds,

-

the structure of any collateral, any noted delinquencies,

-

descriptions of the borrower’s financial condition, and

-

an itemization of any monitoring efforts conducted

-

-

If the amount borrowed exceeds 5% of the bank’s capital, then consideration is given to the associated business plan and debt service capacity.

-

The loan review should be conducted with input from the assigned credit loan officer.

Topic 5. Review of Bank's Policy

-

Risk managers should also periodically review the bank’s policy for loan loss allowances.

-

This review should include the following:

-

A survey of the existing policy for allowances

-

An overview of the asset classification process

-

An assessment of the current risk factors that may lead to losses; the focus should be on the current factors that are different from historical ones

-

A trend analysis of historical losses

-

A statement of the adequacy of the current policy

-

-

Interbank deposits and off-balance-sheet commitments should also be considered with respect to credit risk.

Topic 6. Credit Asset Classification

-

Classification Process: Asset classification is the process of assigning bank assets to credit risk grades based on their likelihood of repayment.

-

Assets should be classified at loan origination and then periodically reviewed and reclassified.

-

The review should consider the client's financial condition, loan performance, economic trends and market changes.

-

-

Regulators use five categories for asset classification:

-

Standard (Pass): Delinquency is not a concern, and loans secured by cash equivalents typically fall into this category.

-

Specially Mentioned (Watch): Assets with potential weaknesses that could affect the borrower's ability to repay.

-

Substandard: Loans with defined credit weaknesses that could jeopardize repayment. The primary source of repayment has often failed, and the bank is looking to secondary sources like collateral. Nonperforming loans over 90 days delinquent are typically in this category.

-

Doubtful: These assets have the same concerns as substandard assets, but the expectation of loss is more significant. Nonperforming loans over 180 days delinquent are placed here unless they are well-secured.

-

Loss: Delinquency is considered highly probable, and the loan should be written off. Nonperforming loans over one year delinquent are categorized as a loss unless they are sufficiently secured.

-

Practice Questions: Q4

Q4. Three and a half months ago, XYZ Manufacturing lost their single largest customer, and the company stopped service of all debt payments to ABC Bank. The bank has seized some collateral, but they are working with XYZ as they form plans to find new customers and build a better future. For now, the loans to XYZ Manufacturing should most likely be classified as:

A. loss.

B. doubtful.

C. substandard.

D. specially mentioned.

Practice Questions: Q4 Answer

Explanation: C is correct.

XYZ Manufacturing is approximately 105 days delinquent on debt service payments. ABC Bank has begun to access secondary sources of capital (i.e., collateral), but XYZ has hope for repayment. There is a path for them to move forward. A renegotiation may be needed down the line, but for now, this loan should be classified as “substandard.” They are not as severe as “doubtful” or “loss,” and they are a bigger concern than merely being classified as “specially mentioned.”

Topic 7. Nonperforming Loans (NPLs)

-

Definition of nonperforming loans (NPLs): NPLs do not generate interest or principal income for the lender and are typically identified when payments are more than 90 days past due.

-

Beyond payment status: Loan classification also considers the borrower’s cash flows and expected ability to repay, even if repayment is delayed.

-

Analysis of nonperforming loans should include the following considerations:

-

Age: This is how long delinquency has existed (e.g., 30 days, 90 days, 180 days, one year).

-

Reasons: As with any trouble spot, it is helpful to understand why the trouble is present (i.e., the root cause). It is possible that the bank could help get the borrower back on track.

-

Case-by-case assessment: Each individual delinquency case should be reviewed, not just in aggregate. Incremental improvements may be possible.

-

Set provision levels: The bank needs to set thresholds for each classification with consideration of the bank’s overall stability.

-

Module 2. Loan Loss Provisioning and Credit Risk Assessment

Topic 1. Loan Loss Provisions and Reserves

Topic 2. Expected Loss vs. Unexpected Loss

Topic 3. Expected Loss Under IFRS 9

Topic 4. Managing Loss Assets

Topic 5. Credit Risk Analysis

Topic 6. Credit Risk Management Capacity

Topic 7. Key Question for Board of Directors

Topic 1. Loan Loss Provisions and Reserves

-

Loan Loss Provisions: These are resources that a bank sets aside to cover potential future losses. The asset classification process helps banks determine these provisions.

-

Loan Loss Reserves: These represent the accumulation of loan loss provisions over multiple years, and they are recorded on a bank's financial statements.

-

Loan loss provisions and reserves are typically counted as Tier 2 capital.

-

-

Factors for Determining Reserves: Banks should consider below factors to decide an appropriate reserve level:

-

Credit quality policies and procedures.

-

Previous loss exposures.

-

Growth in the bank's loan portfolio.

-

The quality of management in charge of lending.

-

Loan collection and recovery policies.

-

Changes in the economic environment and business conditions.

-

Practice Questions: Q1

Q1. Two senior credit managers are reviewing their bank's loan loss reserve procedures. Which of the following elements is most important when determining the appropriate level of reserves?

A. Current loan loss reserves.

B. The bank's experience with previous losses.

C. The current number of nonperforming loans in aggregate.

D. A list of all loans that are delinquent for more than 180 days.

Practice Questions: Q1 Answer

Explanation: B is correct.

It is important to include the bank’s previous experience with loan losses. Loss provisions should not be biased by the number of aggregate losses already on the books (i.e., reserves). Loss provisioning needs to consider the bank’s policies at a high level and not focus on classification issues (i.e., the number of days delinquent). If they did factor delinquency, then 180 days is too long.

Topic 2. Expected Loss Vs Unexpected Loss

-

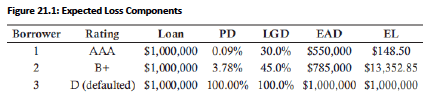

Expected Loss (EL): This is the expected dollar loss if a borrower defaults on a loan. EL is a quantitative measure of counterparty risk.

-

Components of Expected Loss:

-

Probability of Default (PD): The likelihood that a borrower will fail to make timely payments. PD considers observations from historically similar customers, observed degradation on credit default swaps, information from credit rating agencies, and personalized credit scores for each customer. PD also considers the counterparty in the loan.

-

Loss Given Default (LGD): The percentage capital at risk in the event of a default. LGD considers the product used for credit risk.

-

Exposure at Default (EAD): An estimate of the dollar loss exposure for the bank when a borrower defaults. EAD considers the duration of loan origination.

-

-

Formula: EL($)=PD(%)×LGD(%)×EAD($)

-

Unexpected Loss: This is the loss not captured by the expected loss formula. It is typically considered a tail risk event, such as a 99th percentile event.

Practice Questions: Q2

Q2. Which of the following components of expected loss considers the product that was used for the loan?

A. Unexpected loss.

B. Loss given default.

C. Exposure at default.

D. Probability of default.

Practice Questions: Q2 Answer

Explanation: B is correct.

The component of expected loss that considers which loan product was used is loss given default (LGD). The probability of default (PD) considers which client is associated with the loan while the exposure at default (EAD) considers how long the loan has been outstanding.

Topic 3. Expected Loss Under IFRS 9

-

IFRS 9 Model: Since January 1, 2018, IFRS 9 requires a three-stage expected loss model, replacing the incurred loss model of IAS 39.

-

Stage 1: For all performing (non-delinquent) assets, provisions for expected loss are calculated using a 12-month expected loss methodology. This includes effective interest based on the gross amount.

-

Stage 2: Assets with any level of delinquency require a lifetime expected loss model, also including effective interest based on the gross amount.

-

Stage 3: Nonperforming assets also use a lifetime expected loss model, but the effective interest is based on the net (carrying) amount.

-

Practice Questions: Q3

Q3. A bank's loan asset is considered delinquent, but not yet nonperforming. There is a short-term macroeconomic event that is temporarily preventing repayment. According to IFRS 9, which "stage" is required for this specific loan?

A. Stage 1.

B. Stage 2.

C. Stage 3.

D. Stage 4.

Practice Questions: Q3 Answer

Explanation: B is correct.

IFRS 9 requires three stages of reporting.

- Stage 1 is for performing assets. They can apply a 12-month expected loss methodology using effective interest computed based on the gross amount.

- Stage 2 is for assets with some level of delinquency. They can apply a lifetime expected loss methodology using effective interest computed based on the gross amount.

- Stage 3 is for nonperforming assets. They can apply a lifetime expected loss methodology using effective interest computed based on the net amount.

Topic 4. Managing Loss Assets

-

Loan Workout Procedure: This process involves reviewing historical attempts to collect and the success rate. A common workout procedure can include these four steps in any order:

-

Reducing the bank's credit risk exposure by getting additional capital, collateral, or guarantees.

-

Working with the borrower to identify areas for improvement, such as providing advice, developing a plan to cut costs and increase earnings, selling assets, or restructuring the loan. This option is close to consulting.

-

Introducing a third party as a potential joint venture partner or for a takeover.

-

Liquidation through an out-of-court settlement, which may involve foreclosure, liquidating collateral or calling on guarantees.

-

-

Approaches to Managing Loss Assets: From a balance sheet perspective, there are two ways to handle loss assets:

-

Retaning loss assets: Common in the British tradition, this method keeps loss assets on the balance sheet to allow time for collection attempts. This makes the loss reserve appear larger.

-

Writing-off loss asset: Common in the U.S. model, this method immediately writes off losses, which removes them from the loan loss reserves account. This makes the reserves appear smaller in relation to the loan portfolio size.

-

Practice Questions: Q4

Q4. A financial analyst for ABC Bank notices that loan loss reserves are fairly small relative to the size of the bank's loan portfolio. He tells his coworker that this is a red flag for him. However, his coworker tells him that there could be an easy explanation that could be cleared up by asking management. The coworker is suggesting that ABC Bank could be following the:

A. British model and using the retention model for addressing loss assets.

B. U.S. model and using the write-down model for addressing loss assets.

C. U.S. model and providing internal consulting to help the borrower enhance their ability to pay.

D. U.S. model and allowing more time for collection efforts or collateral enhancement to work out.

Practice Questions: Q4 Answer

Explanation: B is correct.

The U.S. model involves immediate write-down. This method allows for the option of repayment but treats it as unlikely. It will make the loan loss reserves appear smaller on the balance sheet. The British model uses retention of loss assets, which will make the loan loss reserves appear much larger on the balance sheet than the write-off model. While loss assets are retained on the balance sheet, managers give more attention to loss workout options.

Topic 5. Credit Risk Analysis

-

Components: Credit risk analysis should evaluate:

- the lending products used,

- the customer base, and

- the loan terms.

-

Key components of credit risk analysis include:

-

A summary of major loan types, including details like number of customers, the average maturity and the average rate charged.

-

The distribution of the loan portfolio, including the number of loans, the amount lent, and segment information (e.g. currencies, maturities, and economic sectors). The category of the borrower (e.g., state-owned, private borrowers, corporations, and retail-customers) should also be identified.

-

A list of all loans with guarantees from government bodies or other entities.

-

A thorough review of loans by their risk classification.

-

An analysis of nonperforming loans with reference to their vintage year (the year they were originated).

-

Practice Questions: Q5

Q5. Portfolio-level credit risk analysis should include:

A. customer segmentation data.

B. current macroeconomic conditions.

C. commentary from the credit risk officer.

D. details on the bank's interest rate hedging policy.

Practice Questions: Q5 Answer

Explanation: A is correct.

Portfolio-level credit risk analysis should include a summary of major loan types, customer segmentation data, a list of loans with guarantees, a review of loans by risk classification, and an analysis of nonperforming loans. Because this is a portfolio-level analysis, credit officer commentary is not needed.

Topic 6. Credit Risk Management Capacity

- The board of directors is ultimately responsible for the credit risk management capacity of a bank. Their main lending objectives are to make loans that are sound and collectible, profitable, and meet the legitimate lending needs of society.

-

Key Components of Review: A review of a bank's credit risk management capacity should include:

-

Lending Process: This review should evaluate the origination, appraisal, approval, monitoring, and collection procedures. It should also cover the criteria for loan approval, lending limits at various management levels, and the collateral review process. The review should also consider the volume of credit applications appraised versus approved over the last 6-12 months.

-

Staffing: The review should list the staff involved in credit origination, appraisal, supervision, and risk monitoring. It should detail the number of staff, their experience, qualifications, and specific responsibilities. An essential part of this is detailing all staff training, including its frequency and adequacy.

-

Information Flows: The review needs to assess how lending information reaches senior managers, the board, and the risk committee in a timely manner.

-

-

Key Questions for the Board of Directors: With respect to credit risk management, the board of directors should be asking a number of key questions, including:

-

Are the bank's loans and deposits priced competitively?

-

Are the sources of interest income well-diversified?

-

How secure is the income from the loan portfolio, and do investment returns reflect the level of risk taken?

-

Can the bank's liquidity position survive stressed scenarios?

-

Which internal rating models does the bank use? Are PD (Probability of Default), LGD (Loss Given Default), and EAD (Exposure at Default) estimates historically accurate?

-

How frequently is the loan portfolio stress-tested?

-

Are all concentration risks adequately disclosed?

-

Does the bank have the required information, such as exposure trends, concentration trends, loss provisions, and delinquency trends?

-

Topic 7. Key Question for Board of Directors

Practice Questions: Q6

Q6. The credit risk management capacity review process should include:

A. staff diversity metrics.

B. information available to credit loan officers.

C. a list of all loans denied in the last three months.

D. timeliness of information flows from loan officers to the Board.a

Practice Questions: Q6 Answer

Explanation: D is correct.

The credit risk management capacity review process should include the lending process, staffing, and information flow concerns. Census data should be gathered on staff including the number of people in the risk management function, their ages, their experience, and their specific responsibilities. Diversity metrics may be captured by human resources but not in this review. Within the lending process, it is useful to understand credit applications relative to approvals over the last 6–12 months. The key part of information flow analysis is to understand if accurate, timely, and cost-effective data is making its way to the senior managers and the Board.