Book 2. Credit Risk

FRM Part 2

CR 6. Credit Scoring and Rating

Presented by: Sudhanshu

Module 1. Credit Scoring and Rating Systems

Module 2. Credit Rating Agency Methodologies

Module 1. Credit Scoring and Rating Systems

Topic 1. Credit Scoring and Credit Rating Systems

Topic 2. Types of Credit Rating Systems

Topic 3. Credit Scoring and Rating Models

Topic 4. Social Lending

Topic 1. Credit Scoring and Credit Rating Systems

-

Purpose of credit assessment: Lenders, investors, and regulators use standardized measures to quantify a borrower’s creditworthiness.

-

Credit scores: Individuals and small firms are typically assessed using credit scores ranging from 300-850 (higher scores indicate stronger repayment ability).

-

Credit ratings: Corporates and governments are evaluated using letter-grade credit ratings (e.g., AAA, AA, BBB), where higher grades imply lower default risk.

-

Agency-specific conventions: Rating agencies use different notation systems, including uppercase or lowercase letters and plus/minus modifiers, to refine credit distinctions.

-

Key Benefits of credit scoring/rating systems:

-

Reduces subjectivity in loan evaluation and acceptance

-

Enables analysis in credit risk management (e.g., scenario analysis and stress testing)

-

Promotes transparency and consistency through a common framework

-

Reduces time for and cost of appraisal

-

-

Banks may develop internal or external credit scoring/rating systems:

-

Internal credit systems: Proprietary credit scoring or rating models to approve or reject loans, leveraging internal historical data and past performance insights.

-

External credit providers: Credit scores and ratings can also be sourced from external parties such as credit rating agencies, credit bureaus, and consulting firms The primary external vendors - Standard & Poor’s, Moody’s, and Fitch- sell credit ratings to banks, corporations, and investors.

-

Practice Questions: Q1

Q1. ABC Bank needs to conduct a risk assessment for a large manufacturing firm that is publicly traded. Which of the following statements regarding this assessment is correct? The bank should use a:

A. credit score to reduce subjectivity.

B. credit score to enhance transparency.

C. credit rating to reduce the cost of appraisal.

D. credit rating despite the limitations for stress testing.

Practice Questions: Q1 Answer

Explanation: C is correct.

Borrowers that are large firms (especially those that are publicly traded) should use credit ratings. Smaller firms and private individuals should be assessed using credit scores. The advantages to using credit scores/ratings include reduced subjectivity, reduced time/cost of appraisal, enabling analysis (e.g., scenario analysis or stress testing), and promoting transparency and consistency.

Topic 2. Types of Credit Rating Systems

-

(BCBS) has distinguished two types of credit rating philosophies as follows:

-

Through-the-Cycle (TTC) Approach:

-

Long-term orientation covering at least one full business cycle

-

Ratings updated infrequently and less sensitive to short-term events

-

Commonly used by external rating agencies

-

Better suited for longer-term loans

-

-

Point-in-Time (PIT) Approach:

-

Focuses on current conditions, typically over horizons up to one year

-

Ratings are more volatile and driven by short-term developments

-

Commonly used in banks’ internal credit processes

-

Better suited for short-term loans

-

-

Topic 3. Credit Scoring and Rating Models

-

Issuer vs issue ratings: Credit scores and ratings can be assigned at either the issuer level (borrower) or the issue level (specific loan or bond).

-

Motivation for ratings: Issuers typically seek credit ratings when they plan to access capital markets to raise debt financing.

-

There are two different scoring methods commonly used:

-

Behavioral scoring (consumer loans):

-

Based on observed historical financial behavior of existing customers.

-

Short-term and dynamic, updating in real time with new information (e.g., payments, spending, default signals).

-

Commonly used for credit limit management, collections, and targeted marketing.

-

-

Profit scoring:

-

Focuses on the estimated profitability of a loan, incorporating pricing, operational decisions, credit risk, and default predictions.

-

Implemented via:

-

Account-level models: Profit calculated separately for each account, ignoring links across accounts.

-

Customer-level models: Profit aggregated across all accounts held by the same customer.

-

-

-

Practice Questions: Q2

Q2. A lender is considering using a through-the-cycle approach when assessing the creditworthiness of a potential borrower. Which of the following statements regarding this approach is correct? This method:

A. will capture default risk in the best way possible.

B. should be used if the loan is short-term in nature.

C. should be used if the loan is long-term in nature.

D. is a robust option because it relies on internal data only.

Practice Questions: Q2 Answer

Explanation: C is correct.

Through-the-cycle approaches are used by credit ratings agencies, not by internal models. They consider data from an entire business cycle, which is long-term in nature. For this reason, this method is best suited for long-term loans. Point-in time assessments use short-term data, and they capture real-time default risk better than the long-term focused through-the-cycle approach.

Topic 4. Social Lending

-

Rise of social lending: Advances in AI and fintech have enabled peer-to-peer lending, allowing borrowers and lenders to transact directly without traditional financial intermediaries.

-

Credit risk challenges: While credit decisions can be made rapidly, credit risk modeling in social lending is still evolving and requires deeper understanding.

-

Higher default risk: Social lending platforms often exhibit higher default rates compared to intermediated loans.

-

Governance concerns: Responsible use of big data and transparency in credit decisions remain key concerns with this innovation.

Practice Questions: Q3

Q3. A risk analyst is considering the best method to generate a credit score that updates in near real-time while considering the payment and purchase history of a customer. Which of the following methods for developing credit risk scoring and rating models should he use?

A. Behavioral scoring.

B. Social lending scoring.

C. Account-level profit scoring.

D. Customer-level profit scoring.

Practice Questions: Q3 Answer

Explanation: A is correct.

Behavioral scoring updates a credit score in near real-time with factors such as a customer’s payments, purchases, and probability of default. The two profit scoring approaches (account-level and customer-level) offer different vantage points on a method focused on profitability rather than on the behavior of a customer. Social lending is an emerging innovation with a credit risk scoring system still in its infancy.

Module 2. Credit Rating Agency Methodologies

Topic 1. Regulatory Requirements (Basel Committee)

Topic 2. Credit Risk Scoring/Ratng Development Process

Topic 3. Data Collection and Preprocessing

Topic 4. Model Fitting

Topic 5. Model Validation

Topic 6. Definition and Validation of Ratings

Topic 7. Implementation, Monitoring and Review

Topic 8. Criticisms of Credit Rating Agencies

Topic 1. Regulatory Requirements (Basel Committee)

-

The Basel Committee outlines five basic requirements for credit scoring and rating systems to ensure proper governance and integrity:

-

Meaningful Differentiation of Risk:

-

Credit grades must be based on genuine risk differences, not designed to manage regulatory capital requirements.

-

Borrowers in the same grade may be treated differently based on transaction-level factors.

-

There must be a reasonable dispersion of borrowers across credit grades to avoid concentration.

-

-

Continuous Evaluation of Borrowers: Borrower ratings should be updated regularly, with annual reviews as a minimum.

-

Operational Oversight: Systems should be continuously monitored for integrity, proper functioning, and adequate controls (e.g., stress testing).

-

Correct Selection of Risk Assessment Metrics: The risk factors used must adequately predict a borrower's creditworthiness, aiming for estimates that are as close as possible to actual outcomes.

-

Collecting Substantial Data: The data must accurately represent reality and should incorporate historical data, past scores/ratings, prior default estimates, and payment history.

-

-

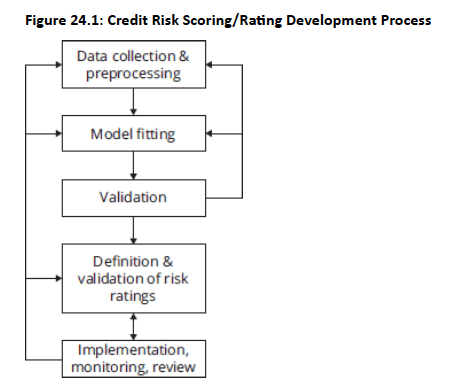

Figure 24.1 provides an overview of the rating development process.

Topic 2. Credit Risk Scoring/Ratng Development Process

Topic 3. Data Collection and Preprocessing

-

Data collection: The first step in credit scoring/rating development is gathering relevant data and consider any preprocessing needs.

-

Dataset: The dataset includes both performing loans and loans that have been nonperforming for more than 90 days.

-

Data preprocessing: Data is cleaned and prepared by removing outliers, selecting appropriate risk attributes, and transforming variables as needed, using a combination of algorithms, statistical tests, and expert judgment.

-

Data types and consistency: The dataset includes both quantitative and qualitative information, with an emphasis on minimizing subjectivity and ensuring consistency in inputs.

-

Typical consumer loan inputs: Key variables may include borrower income and assets, existing debt obligations, payment history, employment status, collateral or guarantees, and loan type (e.g., auto loan, credit card, mortgage).

Topic 3. Data Collection and Preprocessing

-

Typical corporate loan inputs:

-

Financial data analysis: Review corporate financial statements (balance sheet, income statement, cash flow) and compute ratios to assess point-in-time strength and historical trends.

-

Profitability ratios: ROA, ROE, and profit margins to evaluate repayment capacity.

-

Solvency ratios: Debt burden and debt-servicing ability (e.g., D/E ratio, interest coverage).

-

Liquidity measures: Working capital, current ratio, and quick ratio to assess short-term obligations.

-

Management efficiency ratios: Inventory, receivables, payables, and total asset turnover to gauge operational performance.

-

- Transaction-level data: Analyze recent transactions and payment behavior to obtain a more current view of credit quality, including debt balances, delinquencies, and credit limit usage.

-

Firm size and age: Larger firms generally exhibit lower default risk due to better access to capital and greater shock-absorption capacity; size is proxied by market capitalization (public firms) or total assets/revenues (private firms).

-

Market conditions and competitive position: Assess industry and economic conditions, market share and intensity of competition, barriers to entry, sector outlook, competitive advantages (e.g., technology or supply chain), and supplier

-

Topic 3. Data Collection and Preprocessing

-

Typical corporate loan inputs (...continued):

-

Financial market data: For publicly traded firms, use market-based indicators such as stock prices, return volatility, and valuation metrics (P/E, P/B, EPS), which are more informative for short-term horizons, while accounting data is better suited for longer-term loans.

-

Corporate governance: Evaluate board composition and independence, executive qualifications, accountability, ethical standards, and shareholder protections as indicators of long-term corporate health.

-

Corporate news and analytics: Incorporate insights from press releases, traditional media, social media, and alternative data sources to enhance credit assessment when applied responsibly.

-

Topic 4. Model Fitting

-

The second step in the process is model fitting, which involves identifying model parameters with the best descriptive ability (i.e., fit) for the model training data.

-

Assume the following linear model:

- In this formula, the vector includes a constant term and a series of coefficients for various risk attributes.

-

The goal is to provide the best fit (i.e., optimized estimates for β) such that:

-

-

-

-

Optimization objective: The model estimates the optimal parameter vector β* by minimizing a loss function LLL that measures the discrepancy between model predictions and observed classifications in the training data, serving as an empirical proxy for minimizing true default losses.

-

Binary-response modeling: The formula represents a regression-like approach with a binary dependent variable (e.g., default vs nondefault) rather than a continuous outcome, with model fitting using algorithms that draw on statistical methods, data mining, and operations research tec

Topic 5. Model Validation

-

Purpose of model validation: Validation evaluates the fitted model on a new dataset not used in training, making it an out-of-sample test.

-

Validation data requirements: The validation sample should share the same risk characteristics as the training data but consist of different cases (e.g., borrowers or loans).

-

Iterative development: Poor validation results require revisiting model fitting or data collection and preprocessing, and the early stages of credit model development often need multiple iterations to succeed.

-

Key Validation Techniques:

-

Backtesting: Uses historical data to simulate how the model would have performed in the past. It includes both out-of-sample and out-of-time tests.

-

Walk-Forward Testing: A systematic process that evaluates the model's stability by moving the test period forward in time.

-

Rolling testing window: Testing at time ttt uses data from periods t−1t-1t−1 and t−2t-2t−2, with the observation window advancing one period at a time.

-

Forward update: The next testing period t+1t+1t+1 incorporates data from ttt, t−1t-1t−1, and t−2t-2t−2.

-

Model robustness: Additional robustness can be achieved through resampling techniques such as bootstrapping and cross-validation.

-

-

Benchmarking: As a qualitative alternative to backtesting, benchmarking compares model outputs to external references (e.g., rating agency ratings) to identify deviations and inform recalibration and model improvements.

-

Practice Questions: Q1

Q1. Moody’s is considering a revision to their credit rating model. When they checked the model derived from model training data against out-of-sample data, they found a few issues to address. Which of the following steps in the credit rating development process were they likely on when they noticed this issue?

A. Model fitting.

B. Preprocessing.

C. Model validation.

D. Validation of the risk rating.

Practice Questions: Q1 Answer

Explanation: C is correct.

The credit score/rating process has five steps:

(1) data collection and preprocessing,

(2) model fitting,

(3) model validation,

(4) definition and validation of the risk rating, and

(5) implementation.

Step 3, model validation, involves checking the model developed in Step 2 with out-of-sample data.

Topic 6. Definition and Validation of Ratings

-

After data collection/preprocessing, model fitting, and model validation, the credit scores are mapped to a specific risk rating class (e.g., A, B, C).

-

The goal is to ensure:

-

PD calibration: Each rating class should be linked to empirically observed probability of default (PD) estimates.

-

Class differentiation: Rating classes should be well diversified and clearly separated from neighboring classes in terms of risk.

-

Avoid concentration: Borrowers within a rating class should not be overly concentrated in a single risk grade.

-

Topic 6. Definition and Validation of Ratings

-

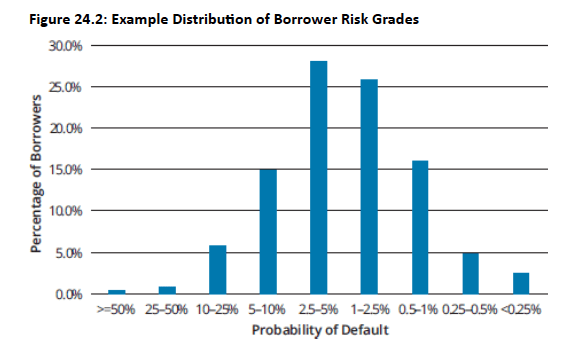

Fig. 24.2 shows a distribution of borrowers given their level of risk.

-

In this example, borrowers are organized into nine risk grades. The lowest risk has less than a 0.25% PD and the highest risk has more than a 50% PD.

-

The middle four risk grades have the highest concentration with two of them having over 25% concentration of borrowers.

-

This is considered an acceptable risk concentration (i.e., no excess concentration).

-

The mapping should be monitored over time for consistency amid rating migration, and re-evaluated and adjusted if results are inadequate.

-

Topic 7. Implementation, Monitoring and Review

-

Implementation: The developed system is integrated into lending operations to provide real-time risk estimates for loan applications and existing accounts.

-

Monitoring: The model's performance should be continuously monitored to detect any degradation in its predictive accuracy.

-

Review and Recalibration: Periodic, comprehensive reviews are necessary to ensure the model remains accurate and relevant. If performance degrades, the model needs to be recalibrated using new data.

Topic 8. Criticisms of Credit Rating Agencies

-

Lack of Transparency: The models used are proprietary and not publicly disclosed, making it difficult to verify their fairness or accuracy.

-

Potential Conflicts of Interest: A significant conflict exists because agencies are paid by the very entities they rate, raising questions about objectivity.

-

Promoting a Debt Explosion: By providing an illusion of risk management and reducing risk premiums, CRAs may encourage excessive borrowing and increase systemic risk.

-

Poor Predictive Ability: CRAs have been widely criticized for failing to predict major financial crises and corporate failures (e.g., Enron, Lehman Brothers).

-

Procyclicality: Despite their stated "through-the-cycle" approach, ratings have been shown to be overly optimistic during economic booms and overly pessimistic during downturns.