Book 5. Risk and Investment Management

FRM Part 2

IM 11. Private Markets Investing

Presented by: Sudhanshu

Module 1. Motivations and Access to Private Markets

Module 2. Perfomance and Risk Measurement in Private Markets

Module 3. Private Market Co-Investing And Intermediated Vehicles

Module 1. Motivations and Access to Private Markets

Topic 1. Private Market Investment Overview

Topic 2. Private Market Investment Motivations

Topic 3. Private Market Investment Structures

Topic 4. Equity and Debt Investments in Private Market

Topic 1. Private Market Investment Overview

-

Overview: Private markets facilitate capital raising for private companies through various securities, including equity, convertible debt, and traditional debt.

-

Private Markets Securities: These investments are generally categorized as:

- Private Equity (PE): Equity investments in private firms that may eventually become publicly traded through listing

- Private Debt (PD): Debt investments in private companies, including convertible and traditional debt

- Private Real Assets (PRA): Investments in privately held real assets

- Private Investments in Public Equities (PIPEs): Private placements in publicly traded firms with limited trading volume

-

A private equity investment may eventually become publicly traded through a listing on public markets.

Topic 2. Private Market Investment Motivations

-

Investors motivations for private market investments include six major categories:

-

Performance and diversification: Private market investments can offer higher returns than public assets and provide diversification during periods of market uncertainty.

-

Control and value creation: Private investors can actively monitor and influence company performance, contributing capital, industry networks, and operational expertise—levels of control rarely available in public markets.

-

Access to a broader investment universe: Private markets offer broader diversification because there are far more private firms than public ones—over 300 million globally compared to about 52,000 listed companies. This provides exposure to a wider range of industries, business models, and companies at different lifecycle stages.

-

Potential for absolute returns: Many investors pursue private investments in search of absolute returns that are less correlated with public market performance.

-

Wider geographic reach: Private investments provide access to regions with limited or no public markets, expanding diversification and reducing home-country bias.

-

Specialized investment structures: Some investors seek specialized risk exposures that can be accessed through structures like private funds of funds and co-investments.

-

Practice Questions: Q1

Q1. Which of the following statements best explains why investors may prefer private investment vehicles over public markets? Private investment vehicles:

A. require less expertise from investors.

B. harness the power of home country bias.

C. guarantee higher returns than in public markets.

D. offer investors greater control over the value creation process.

Practice Questions: Q1 Answer

Explanation: D is correct.

Investors are attracted to private investment vehicles because they provide broader diversification, the opportunity for active involvement in value creation, and access to specialized structures. These benefits are generally not available in public markets and allow investors to pursue unique opportunities while managing risk more effectively.

-

An investment structure is the framework that determines how capital is pooled, managed, and governed.

-

An investment structure also defines the specific rights and obligations of both the managers and the investors.

-

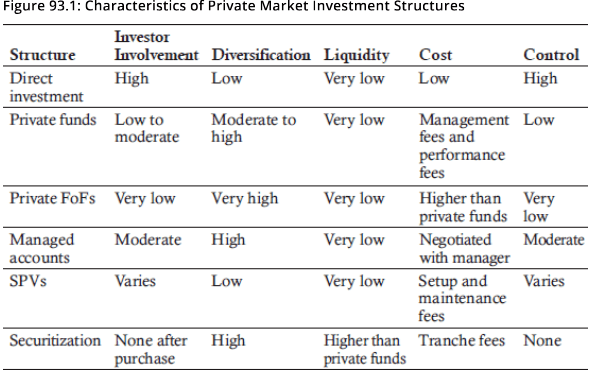

The main investment structures used in private markets are shown in below figure.

Topic 3. Private Market Investment Structures

-

Direct Investment: In this structure, an investor acquires an ownership interest in a specific private company or asset directly.

-

Requirements: Demands significant expertise, active involvement, and strong networks to source local opportunities.

-

Risks: Carries high concentration risk and provides limited diversification unless a large number of positions are held.

-

Common Users: Often used by entrepreneurs, family offices, buyout investors, and through crowdfunding.

-

Limitations: Certain strategies, like leveraged buyouts or distressed debt, are generally not accessible in this format.

-

-

Private Funds: This is the most common structure for institutional investors. Capital is pooled and managed by specialized general partners (GPs) who make all oversight decisions.

-

Benefits: Provides professional management and diversification.

-

Legal Form: The most common format is a closed-end limited partnership.

-

Costs: Investors pay both management fees and performance-based fees (carried interest).

-

Topic 3. Private Market Investment Structures

-

Private Funds of Funds (FoFs): A FoF is a fund that invests in a portfolio of other private market funds rather than direct assets.

-

Best For: Investors with limited experience or those who prioritize maximum diversification.

-

Trade-off: While it offers the highest diversification, it introduces an additional layer of management fees, making it more expensive than single funds.

-

Nature: It is the closest approximation to a passive investment approach in private markets.

-

-

Managed Accounts: These are separate accounts tailored to a specific investor's mandate.

-

Types of Mandates:

-

Discretionary: The manager makes all decisions; usually involves performance-based fees (carried interest).

-

Advisory: The investor retains veto authority; often does not include performance fees.

-

-

Key Feature: Offers high customization and transparency but requires a substantial capital commitment.

-

Topic 3. Private Market Investment Structures

-

Special Purpose Vehicles (SPVs): An SPV is a legal entity created specifically to hold a single asset or a small group of assets.

-

Use Case: Often used to facilitate investments in Private Real Assets (PRAs) or to give sophisticated investors targeted exposure to a single deal.

-

Flexibility: Can be structured using either equity or debt.

-

-

Securitization: This involves pooling assets (typically debt) and dividing them into "tranches" with varying risk and return profiles.

-

Advantage: Offers higher liquidity than traditional private funds and allows investors to target specific risk profiles.

-

Disadvantage: Introduces complexity and reduces transparency.

-

-

Private investments are further defined by the type of security used:

-

Private Equity: Can be structured as common shares or preferred shares. Preferred shares are often negotiated to include specific protections or rights.

-

Private Debt: Can be convertible or nonconvertible.

-

Convertible Debt: Offers a hybrid profile.

-

-

Value=Downside Protection (Debt Component) + Upside Potential (Equity Option)

Topic 3. Private Market Investment Structures

Practice Questions: Q2

Q2. Which of the following private market investment structures requires the highest level of investor expertise and involvement, offers high control, but results in concentrated risk and low diversification unless many positions are held?

A. Private funds.

B. Direct investment.

C. Managed accounts.

D. Private funds of funds.

Practice Questions: Q2 Answer

Explanation: B is correct.

Direct investment requires substantial investor expertise and active involvement while offering a high degree of control. However, it exposes investors to significant concentration risk and provides limited diversification unless many positions are held.

-

Private investments are further defined by the type of security used:

-

Equity Investments (Private Equity):

-

Common vs. Preferred Shares: Can be structured as either common shares or preferred shares

- Preferred Share Variations: Negotiable to include specific rights and protections; features and level of influence vary significantly across different preferred share agreements

-

-

Debt Investments (Private Debt):

- Convertible vs. Nonconvertible: Debt can be structured as convertible or nonconvertible with varying degrees of seniority in the capital structure

- Convertible Debt Benefits: Provides downside protection through the debt component while offering upside potential through the embedded option to convert into equity

- Seniority Arrangements: Debt can be organized with different levels of seniority, affecting priority in claim on assets and cash flows

-

Topic 4. Equity and Debt Investments in Private Market

Module 2. Perfomance and Risk Measurement in Private Markets

Topic 1. Internal Rate of return

Topic 2. Multiple of Invested Capital (MOIC)

Topic 3. Public Market Equivalent (PME)

Topic 4. Common Limitation of PE Performance Metrics

Topic 5. Major Risk Categories

Topic 6. Measuring Private Market Risks

Topic 1. Internal Rate of return

-

Primary Metrics: The three primary metrics for measuring private equity performance are the internal rate of return (IRR), the multiple of invested capital (MOIC), and the public market equivalent (PME).

- IRR Definition and Strengths: Reflects the annualized return on invested capital incorporating the timing of cash flows; well-suited for multi-year investment projects and comparing competing investments

- Timing Bias Limitation: Early cash flows can artificially inflate IRR, potentially encouraging fund managers to favor short-term gains over higher long-term returns

- Mitigation: Use time-zero IRR (also known as Modified IRR or MIRR) to address timing distortions

- Risk Blindness: IRR does not incorporate risk considerations, which can incentivize managers to pursue riskier deals to achieve higher reported returns

- Capital Call Gaming: Managers may delay capital calls by drawing on credit lines to shorten holding periods, artificially boosting reported IRRs

- Industry Usage: The IRR is the most widely used performance metric in the private equity industry.

Topic 1. Internal Rate of return

-

Advantages of IRR

-

Intuitive and easy to interpret

-

Incorporates time value of money

-

Widely accepted and used by industry participants

-

-

Disadvantages of IRR

-

Measures only deployed capital (not committed capital)

-

Not adjusted for risk

-

Highly sensitive to timing of cash flows, creating potential for manipulation

-

Assumes reinvestment at the IRR

-

Can overstate performance when credit lines are used to accelerate distributions

-

Does not incorporate explicit benchmarks or broader market context

-

Topic 2. Multiple of Invested Capital (MOIC)

-

Definition: MOIC measures value generated relative to capital invested;

-

MOIC Calculation: MOIC = (Total Distributions + Current Value of Remaining Assets)/(Total Capital Invested);

-

Interpretation: MOIC of 1.0x indicates breakeven (capital recovered equals original investment)

- Total Value to Paid-In (TVPI): Primary MOIC measure

- Calculated as: TPVI (MOIC) = (Distributions + Residual Value)/(Capital Called)

- Can be expressed as DPI + RVPI

- Limitation: Subject to manipulation if fund managers inflate asset valuations since it includes residual value

- Distributed to Paid-In (DPI):

- Calculated as: DPI = Distributions/(Capital Called)

- Based entirely on realized cash flows, making it immune to valuation manipulation

- Often preferred measure when sufficient realizations (cash exits) have occurred

- Limitation: Realized cash flows may reflect economic conditions different from those affecting remaining unrealized assets

- Residual Value to Paid-In (RVPI):

- Calculated as: RVPI = (Residual Value)/(Capital Called)

- Increases naturally as fund invests in appreciating assets

- Limitation: Like TVPI, can be manipulated if residual values are overstated

Topic 2. Multiple of Invested Capital (MOIC)

-

Advantages of MOIC

-

Focuses on absolute performance

-

Independent of dollar size, making comparisons across funds straightforward

-

Less susceptible to manipulation than the IRR

-

Cash-based submetrics (such as DPI) are robust

-

-

Disadvantages of MOIC

-

Measures only deployed capital (not committed capital)

-

Not adjusted for risk

-

Ignores time value of money, including holding periods

-

Cannot be annualized

-

Does not incorporate explicit benchmarks or broader market context

-

Topic 3. Public Market Equivalent (PME)

- PME Methodology: Compares private equity investment performance against public market benchmarks by discounting all fund cash flows using returns of an index (e.g., S&P 500)

- PME Calculation: PME = (Sum of Discounted Distributions)/(Sum of Discounted Capital Calls)

- PME Interpretation: A PME > 1 indicates outperformance relative to the benchmark

- Implementation Requirements:

- Works best with fully realized funds

- Requires matching each distribution with its associated capital call to reflect correct holding period

- Modified PME (mPME): Developed by Cambridge Associates to approximate the PME calculation

- Provides a more robust measure of manager value creation and is less prone to manipulation

Topic 3. Public Market Equivalent (PME)

-

Advantages of PME

-

Incorporates explicit benchmarking to provide market context

-

Helps neutralize the impact of market cycles on performance evaluation

-

Measures manager value creation in a way that is less prone to manipulation

-

-

Disadvantages of PME

-

Measures only deployed capital (not committed capital)

-

Sensitive to the choice of benchmark

-

Suitable benchmarks may not always exist

-

Most reliable when applied to fully realized funds

-

Practice Questions: Q1

Q1. Which of the following performance metrics for private equity best incorporates the timing of cash flows but can be artificially inflated by early distributions or the use of credit lines?

A. Internal rate of return (IRR).

B. Residual value to paid-in (RVPI).

C. Public market equivalent (PME).

D. Multiple of invested capital (MOIC).

Practice Questions: Q1 Answer

Explanation: A is correct.

The IRR incorporates the timing of cash flows, making it useful for evaluating multiyear private equity investments. However, it can be artificially inflated through early distributions or by using credit facilities to delay capital calls, which shortens the measured holding period and boosts reported performance.

Practice Questions: Q2

Q2. Which of the following private market performance metrics is most useful for assessing absolute performance without regard to holding periods?

A. Distributed to paid-in (DPI).

B. Internal rate of return (IRR).

C. Public market equivalent (PME).

D. Multiple of invested capital (MOIC).

Practice Questions: Q2 Answer

Explanation: D is correct.

MOIC measures the total value created relative to the capital invested. It provides an absolute performance multiple without adjusting for holding periods, making it especially useful for comparing outcomes across private market funds.

Topic 4. Common Limitation of PE Performance Metrics

- Common Disadvantage - Deployed vs. Committed Capital: All three performance metrics measure only deployed capital rather than committed capital, creating significant analytical gaps

- Cash Drag Issue: Ignores the negative impact (cash drag) from uncalled capital sitting idle and earning minimal returns

- Over-Commitment Strategy: Creates challenges for investors who intentionally commit more capital than they plan to deploy, exploiting the trend of funds not calling full committed amounts

- Example: Investor commits 110% of desired allocation expecting only ~60% to be called, helping reach target exposure but creating risks

- Risks of Over-Commitment Practice:

- Overallocation Risk: Investor may end up with more deployed capital than desired if call rate exceeds expectations

- Default Risk: Investor faces potential inability to meet capital calls if the fund unexpectedly calls the full committed amount

Topic 5. Major Risk Categories

-

Investors in private markets face both traditional financial risks and risks specific to private assets. These risks are grouped into the following broad categories:

-

Traditional and Specific Risk Categories:

-

Systematic Risk: Private assets remain exposed to macroeconomic risks (economic downturns, inflation shifts, interest rate changes) despite low correlations with public indices; interest rate risk particularly affects leveraged strategies; illiquidity complicates hedging (e.g., foreign exchange risk); monitored through scenario analysis, stress testing, and public market equivalent comparisons

- Illiquidity Risk: Investments locked up for long periods with limited exit opportunities; measured by investment duration, time until expected liquidity (funding liquidity risk), and opportunity cost implications

- Credit Risk: Most relevant for private debt; includes two components:

- Recovery risk: potential capital loss from borrower default (critical for distressed investors)

- Credit event risk: spillover from negative developments in public credit markets

- Settlement Risk: Present in counterparty transactions; reduced relative to public markets through extensive due diligence conducted by private market investors

-

Topic 5. Major Risk Categories

-

Information and Valuation Challenges:

-

Information Asymmetry: Private investments face less regulation than public firms, limiting information availability and quality; mitigated through rigorous due diligence, frequent reporting, and regular auditing

- Valuation Risk: Arises from infrequent transactions and limited comparable data; concerns include stale pricing and valuation subjectivity; denominator effect occurs when outdated private valuations are compared with liquid public asset values; assessed through third-party appraisals, DCF analysis, comparables, and IPEV Guidelines adherence

-

-

Allocation and Strategic Risks:

-

Strategic Asset Allocation (SAA) Risk: Long-term allocation deviations from market-neutral benchmarks; complicated by investability constraints, access limitations, and unique private asset characteristics; slow private asset value adjustments versus public markets can create artificial weighting differences and unnecessary rebalancing; significant SAA deviations may challenge fundraising

- Tactical Asset Allocation (TAA) Risk: Market timing challenges; capital commitments may not deploy for years; procyclical behavior (increasing allocations after strong performance); mitigated through co-investments, secondary transactions, and time diversification across 5-7 vintage years

-

Topic 5. Major Risk Categories

-

Operational and Manager-Related Risks:

-

Agency Risk: Introduced by delegating control to fund managers; assessed through fee structures (including carried interest), potential conflicts of interest, and governance framework strength

- Operational Risk: Particularly relevant for private debt and PRA investors; relates to default risk, recovery challenges, and company/asset-level operational failures; assessed using historical default/loss statistics, covenant compliance, and operational due diligence

- Selection Risk: Risk of choosing wrong manager or deal; asymmetric with substantial performance dispersion between top and bottom performers; wide top 5% to bottom 5% spread creates Monte Carlo simulation challenges due to non-normal return distributions

- Reporting Risk: Performance metrics and valuations may not reflect economic reality due to intentional manipulation or measurement limitations; driven by limited transparency, infrequent reporting, less oversight, and NAV subjectivity; DPI less exposed than TVPI or RVPI as it's based on realized cash flows

-

Topic 6. Measuring Private Market Risks

-

Performance Dispersion: Monitor spread between highest and lowest pooled average TVPI to assess macro risk

- Use multiyear rolling averages to reduce outlier effects; large spreads suggest greater macroeconomic influence on returns

- Compare individual fund TVPI with pooled category average to evaluate selection risk

- DPI vs. TVPI Comparison: Compare distributions to paid-in (DPI, based on realized cash flows) with total value to paid-in (TVPI, based on manager-determined NAV estimates); substantial gaps may indicate potential reporting risk

- Portfolio Weight Reviews: Compare investor's portfolio weights against target allocation or market-neutral portfolio (reflecting geographic and strategy mix of relevant private market allocation) to assess strategic asset allocation (SAA) risk

- Value at Risk (VaR) and Stress Testing: Model worst-case outcomes for strategy-specific risks, including macroeconomic shocks and periods of reduced liquidity

- Vintage Year Analysis: Compare returns across vintage years to evaluate market timing and risk variation across economic cycles.

- Due Diligence Reviews: Qualitative review to confirm whether materialized risks align with expectations at investment time; identified gaps strengthen future due diligence processes

- Default and Loss Rates: For private debt investments, track historical default rates and loss statistics as benchmarks for assessing recovery risk

Practice Questions: Q3

Q3. Which of the following metrics best helps investors monitor the impact of macro risks and selection risk in private market performance?

A. Value at risk (VaR).

B. Default and loss rates.

C. Performance dispersion.

D. Strategic asset allocation (SAA) weights

Practice Questions: Q3 Answer

Explanation: C is correct.

Performance dispersion evaluates the spread between the highest and lowest pooled average TVPI, making it useful for assessing how much macroeconomic conditions and manager selection contribute to differences in private market returns.

Module 3. Private Market Co-Investing And Intermediated Vehicles

Topic 1. Private Market Co-Investing

Topic 2. Intermediated Private Market Investment

Topic 1. Private Market Co-Investing

- Definition and Access: Private investor directly invests in a specific deal alongside a private market fund, typically by invitation from the fund manager; access is usually restricted to large, established investors with strong manager relationships

- Fee Advantage: Co-investing generally offers lower fees compared to investing through the fund itself, as it bypasses typical fund management fee structures

- Manager Motivations: Fund managers extend co-investment opportunities when additional capital is needed to complete deals that exceed their usual investment limits or fund capacity

- Operational Considerations: Opportunities often arise on short notice, requiring accelerated due diligence and decision-making and investors must be prepared to evaluate and commit to investments quickly

- Structured Access: Some managers offer dedicated co-investment vehicles that formalize and streamline access to co-investment deals for qualified investors

- Advantages of Co-Investing:

- Lower Fees: Co-investors typically pay reduced or no management fees and carried interest compared to primary fund investors; transaction and due diligence costs are still shared

- Greater Control: Enables investors to target specific deals, allowing precise shaping of exposures and desired portfolio weights

- Potential for Higher Net Returns: Lower fee structure often produces higher after-fee returns than primary fund investments

- Learning and Access: Provides valuable deal experience, strengthens GP relationships, and offers exposure to opportunities unavailable through traditional fund commitments

Topic 1. Private Market Co-Investing

- Disadvantages of Co-Investing:

- Adverse Selection:

- May receive less attractive opportunities or deals outside fund manager's core expertise

- Deal flow can be procyclical, appearing when valuations are already elevated

- Speed and Complexity: Often requires accelerated due diligence and rapid decision-making with less preparation time than primary fund commitments

- Resource and Expertise Requirements: Demands significant internal resources, specialized expertise, and quick deal evaluation capabilities; investors lacking these often underperform

- Concentration and Diversification Risk:

- Typically larger, more concentrated positions than standard fund exposures

- Portfolios may become less diversified and more sensitive to deal-specific risks

- Many involve leveraged buyouts or infrastructure projects, increasing unintended concentration risk

- Legal and Governance Risks: Co-investors are usually passive participants with limited influence over deal structure, management decisions, or exit timing; often accept fewer legal protections than primary fund limited partners

- Adverse Selection:

Practice Questions: Q1

Q1. Which of the following is a key advantage of co-investing compared with investing as a limited partner in the primary fund?

A. Increased legal protections.

B. Reduced management fees.

C. Reduced need for due diligence.

D. Increased portfolio diversification.

Practice Questions: Q1 Answer

Explanation: B is correct.

Co-investing typically offers investors the opportunity to participate in specific deals while paying reduced, or sometimes no, management fees or carried interest. This can lead to higher net returns compared with investing solely through the primary fund.

Topic 2. Intermediated Private Market Investment

-

Investing in private markets through an intermediated vehicle, such as a private equity or private debt fund, involves numerous benefits as well as several challenges.

-

Benefits of using Intermediated Vehicles in Private Markets:

- Expertise: Fund managers provide specialized capabilities in sourcing, due diligence, structuring, monitoring, and exiting investments; valuable for navigating private market complexity and reducing operational risk for investors lacking specialized skills

- Risk Reduction:

- Diversification through pooled capital enables access to wider range of deals, sectors, and geographies

- Professional management may achieve lower loss ratios, further mitigating investment risk

- Deal Flow Access: Managers maintain access to attractive investment opportunities unavailable to most individual investors; particularly critical as private markets become increasingly competitive and specialized

- Cost and Resource Sharing: Asset pooling allows investors to share substantial costs of sourcing, analysis, and ongoing oversight that would otherwise prevent individual participation in private markets

Topic 2. Intermediated Private Market Investment

-

Challenges of using Investment Vehicles in Private Markets:

- High Fees: Professional management is expensive; investors pay both management fees and carried interest, creating a performance hurdle that reduces net returns

- Principal-Agent Risk: Misalignment between general partner goals and limited partner interests can create governance and performance concerns, including potential for abuse or misconduct

- Lack of Transparency: Multiple intermediation layers between investors and underlying assets limit monitoring and influence capabilities; information asymmetry arises from limited disclosure, infrequent valuations, proprietary practices, and uncertain cash flow timing

- Blind Pool Risk: Investors commit capital before knowing specific asset acquisitions; while strategy guidelines are provided, fund managers ultimately control deployment, potentially resulting in unwanted exposures

- Illiquidity Risk: Long-term capital commitments with no redemption rights and limited secondary market options; investors needing liquidity may face significant discounts to NAV

- Due Diligence Demands: Investors must conduct extensive due diligence on fund strategies, manager track records, governance structures, and operational processes to mitigate underperformance or misconduct risks

- Potential Conflicts of Interest: Conflicts arise in multiple forms, such as funds investing in both equity and debt of the same company facing competing debtholder versus equity holder incentives, or allocation disputes over co-investment opportunities

Practice Questions: Q2

Q2. Which of the following is a key benefit of investing in private markets through intermediated vehicles such as private equity or private debt funds?

A. Access to expertise.

B. More access to liquidity.

C. Elimination of management fees.

D. Increased transparency and control.

Practice Questions: Q2 Answer

Explanation: A is correct.

Intermediated vehicles provide investors with access to the specialized expertise of professional fund managers who source, evaluate, structure, monitor, and exit private market investments. This expertise is valuable given the complexity of private markets and helps reduce operational risk for investors who may lack these capabilities.

Practice Questions: Q3

Q3. Which of the following is a key challenge of investing in private markets through intermediated vehicles such as private equity or private debt funds?

A. Reinvestment risk.

B. Low information asymmetry.

C. Increased concentration risk.

D. Performance hurdle from fees.

Practice Questions: Q3 Answer

Explanation: A is correct.

High fees are a major challenge of intermediated private market investing. Investors must overcome both management fees and carried interest before earning positive net returns, which creates a significant performance hurdle.