Book 3. Operational Risk

FRM Part 2

OR 22. Solvency, Liquidity, and Other Regulation After the Global Financial Crisis

Presented by: Sudhanshu

Module 1. Stressed VaR, Incremental Risk Capital Charge and Comprehensive Risk Charge

Module 2. Basel III Capital Requirements, Buffers and Liquidity Risk Management

Module 3. Contingent Convertible Bonds and Dodd-Frank Reform

Module 1. Stressed VaR, Incremental Risk Capital Charge, and Comprehensive Risk Charge

Topic 1. Introduction

Topic 2. Stresses VaR Overview

Topic 3. Stresses VaR Calculation

Topic 4. Incremental Risk Charge

Topic 5. Comprehensive Risk Charge

Topic 1. Introduction

- Post-Crisis Capital Reforms: Following the 2007-2009 financial crisis, Basel Committee implemented Basel 2.5 and Basel III reforms to increase bank capital, tighten capital definitions, and create protective buffers against stress period losses.

- Key Capital Regulation Changes: Major changes include incremental risk capital charge, comprehensive risk capital charge, stressed value at risk (VaR), capital conservation buffer, and countercyclical buffer requirements.

- Liquidity Risk Management: Basel III requires banks to maintain liquidity coverage ratios and net stable funding ratios to better manage liquidity risks and ensure adequate funding stability.

- Alternative Funding Sources: Higher capital requirements encourage banks to use less mainstream funding sources, such as contingent convertible bonds (CoCos), to meet regulatory capital standards.

- Critical Ratio Calculations: Key regulatory ratios include leverage ratio, liquidity coverage ratio, and net stable funding ratio, all calculable from bank balance sheet information.

- Institutional Reform Creation: Major post-crisis reforms established new regulatory bodies including the Financial Stability Oversight Council and Consumer Financial Protection Bureau.

- Comprehensive Regulatory Framework: Reforms address capital adequacy in normal periods, stress period protection, liquidity management, and broader systemic risk oversight through coordinated regulatory changes.

Topic 2. Stressed VaR Overview

- Basel II implementation coincided with the 2007-2009 financial crisis, leading to criticism that it enabled banks to underestimate risks through self-regulation

- Advanced IRB approach allowed banks to use their own estimates for probability of default (PD), loss given default (LGD), and exposure at default (EAD)

- Basel Committee responded with Basel 2.5 changes to market risk capital calculations, implemented December 31, 2011

-

Three primary changes include:

-

The calculation of a stressed value at risk (SVaR)measure.

-

The implementation of a new incremental risk change (IRC).

-

A comprehensive risk measure (CRM) for instruments sensitive to correlations between default risks of various instruments (e.g., securitizations and related instruments).

-

Topic 3. Stressed VaR Calculation

- Banks historically used historical simulation method to calculate VaR for market risk capital charges, assuming next-day % changes in market variables are random samples from the previous 1-4 years

- Pre-crisis period (2003-2006) had low market volatilities, resulting in low VaR calculations that persisted even after the financial crisis began due to models still using historical low-volatility data

- Basel 2.5 addressed this problem by requiring banks to calculate two VaRs: regular VaR using historical simulation and stressed VaR using a 250-day period of stressed market conditions

- Regulators initially considered 2008 as the ideal stressed period for all banks

- Current requirements mandate banks identify their own one-year stressed period within the most recent seven years when their actual portfolios performed poorest

- This individualized approach means stressed periods may differ across banks based on their specific portfolio performance history

-

-

Previous day's VaR (10-day horizon, 99% confidence).

-

VaRavg: Average VaR over past 60 days (10-day horizon, 99% confidence level).

-

mr: Multiplicative factor (supervisor-determined, minimum 3).

-

SVaRt−1: Previous day's stressed VaR (10-day horizon, 99% confidence).

-

SVaRavg: Average stressed VaR over past 60 days (10-day horizon, 99% confidence level).

-

ms: Stressed VaR multiplicative factor (supervisor-determined, minimum 3).

-

-

The capital charge for MR under Basel 2.5 is at least twice that under Basel II due to the addition of SVaR.

Practice Questions: Q1

Q1. Which of the following statements about a stressed value at risk (VaR), required under Basel 2.5, is correct?

A. Basel 2.5 has established the year 2008 as the “stress” period. All banks use data from 2008 to calculate the stressed VaR.

B. The stressed VaR replaces the “normal” VaR for the purpose of calculating capital for credit risks.

C. Market risk capital under Basel 2.5 should be at least double that of market risk capital under Basel II due to the addition of the stressed VaR.

D. The stressed VaR must be calculated using a 99.9% confidence interval.

Practice Questions: Q1 Answer

Explanation: C is correct.

Basel 2.5 required banks to calculate two VaRs, the usual VaR, using the historical simulation method, and a stressed VaR, using a 99% confidence level, 250-day period of stressed market conditions. The total market risk capital charge is the sum of the usual bank VaR and the stressed VaR.

Initially, regulators thought the year 2008 would be ideal for stressed market conditions. However, banks are now required to identify a one-year period when their portfolios performed poorly. This means the stressed period may be different across banks.

Topic 4. Incremental Risk Charge

- Pre-crisis capital charges were lower for trading book exposures (bonds, equity securities, derivatives held for trading) than banking book exposures (loans, investment securities), creating regulatory arbitrage opportunities

- Trading book used 10-day 99% VaR with multiplier while banking book required one-year 99.9% confidence level VaR, leading banks to shift illiquid default-prone instruments to trading book

- Basel Committee proposed incremental default risk charge (IDRC) in 2005, requiring 99.9% confidence level, one-year VaR for trading book instruments sensitive to default risk

- IDRC effectively equalized capital requirements between trading and banking books by making trading book capital the greater of market risk capital and banking book capital

- 2007-2009 crisis losses came primarily from downgrades, credit spread widening, and liquidity losses rather than actual defaults, exposing IDRC limitations

- IDRC was revised to incremental risk charge (IRC) covering all credit-sensitive instruments, requiring banks to consider rating change sensitivities and expected portfolio rebalancing to reduce default risk

Topic 4. Incremental Risk Charge

- Banks must estimate a liquidity horizon for each instrument in their IRC portfolio calculation, with Basel Committee setting minimum horizon at three months

- Rebalancing assumption requires banks to replace downgraded or defaulted instruments with comparable instruments of original rating at the end of each liquidity horizon period

- Example: AA-rated bond with six-month liquidity horizon gets replaced with new AA-rated bond if downgraded or defaulted, with loss recorded on the sale

- This "constant level of risk assumption" maintains portfolio quality through periodic rebalancing at three-month, six-month, or other intervals based on estimated liquidity horizons

- Rebalancing creates small losses from downgrades but reduces default likelihood, generally lowering the one-year 99.9% VaR calculation

- Specific risk charge (SRC) separately captures changing credit spreads beyond the IRC framework

Practice Questions: Q2

Q2. Banks are required to rebalance their portfolios as the creditworthiness of bonds decline, leading to losses over time but generally not to outright default. This requirement to specify a liquidity horizon for each instrument in the portfolio and rebalance at the end of the liquidity horizon is part of the:

A. incremental risk charge calculation.

B. net stable funding charge formula.

C. countercyclical buffer estimation.

D. comprehensive risk charge calculation.

Practice Questions: Q2 Answer

Explanation: A is correct.

As part of the incremental risk charge (IRC) calculation, banks are required to estimate a liquidity horizon for each instrument in the portfolio. For example, assume an AA+-rated bond in the portfolio has a liquidity horizon of three months. If, at the end of three months, the bond has defaulted or has been downgraded, it is assumed that the bank will replace the bond with an AA+-rated bond comparable to the one held at the start of the period.

This rebalancing is assumed at the end of each three-month period (or six months, nine months, etc., depending on the estimated liquidity horizon). Rebalancing allows banks to take losses as instruments are downgraded but generally allows the bank to avoid defaults.

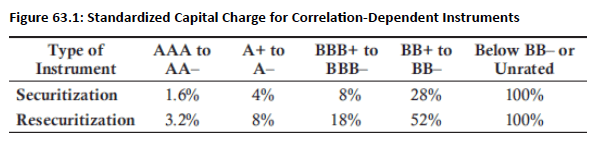

Topic 4. Comprehensive Risk Charge

-

Purpose: The Comprehensive Risk (CR) charge is a single capital charge for correlation-dependent instruments, replacing the Specific Risk Charge (SRC) and the IRC for these instruments.

-

"Correlation Book" Instruments: Applies to instruments sensitive to correlations between default risks of different assets, such as Asset-Backed Securities (ABSs) and Collateralized Debt Obligations (CDOs).

-

Crisis Experience: In normal times, highly-rated tranches of these instruments have little risk. However, during stress periods (e.g., 2007-2009 crisis), correlations increase, making even high-rated tranches vulnerable.

-

Standardized Approach for Rated Instruments:

-

Unrated/Low-Rated Instruments: For instruments rated below BB- or unrated, banks must hold dollar-for-dollar capital (100% capital charge).

-

Internal Models: With supervisory approval, banks can use internal models for CR charge, but these require rigorous stress tests and must capture:

-

Credit spread risk.

-

Multiple defaults.

-

Volatility of implied correlations.

-

Relationship between implied correlations and credit spreads.

-

Costs of rebalancing hedges.

-

Volatility of recovery rates.

-

Topic 4. Comprehensive Risk Charge

Module 2. Basel III Capital Requirements, Buffers and Liquidity Risk Management

Topic 1. Basel III Capital Requirements

Topic 2. Capital Conservation Buffer and Countercyclical Buffer

Topic 3. Liquidity Risk Mangement

Topic 1. Basel III Capital Requirements

- Basel III responded to the 2007-2009 financial crisis by increasing capital requirements for credit risk, tightening capital definitions, and eliminating Tier 3 capital, with proposals published in 2010-2011 and later amended

-

The crisis revealed weaknesses in the Basel II framework, including:

-

Market participants during the crisis focused exclusively on tangible Tier 1 common equity capital as the only capital type capable of maintaining banks as going concerns

- Regulators recognized that distress at certain banks posed greater systemic threats to society, leading to the creation of systemically important financial institution (SIFI) categories

- Banks appeared able to manipulate risk-based capital requirements, necessitating leverage ratios as backup measures that market participants also began monitoring

- Banks required substantial capital after absorbing losses to remain going concerns, not merely to stay technically solvent

- Some solvent banks experienced runs and failed due to unstable wholesale funding and inadequate liquid reserves, prompting new liquidity requirements

- Lehman and other banks failed to honor derivatives contract commitments, highlighting the need for capital to cover counterparty credit risk

- Large exposures framework (LEF) established global standards limiting single counterparty concentrations at 15% of capital for global SIFIs and 25% for other institutions

-

Topic 2. Tier 1 Capital

-

Tier 1 capital (or core capital) includes:

-

Common equity including retained earnings (called Tier 1 equity capital or Tier 1 common capital).

-

A limited amount of unrealized gains and losses and minority interest.

-

-

Tier 1 core capital does not include:

-

Goodwill and other intangibles.

-

Deferred tax assets.

-

Changes in retained earnings arising from securitized transactions.

-

Changes in retained earnings arising from the bank’s credit risk, called debit (debt) value adjustment (DVA).

-

-

Additional Tier 1 capital includes:

- Noncumulative perpetual preferred stock (additional Tier 1 capital is part of total Tier 1 capital).

- Debt with triggers that cause conversion to equity or write-downs.

- Approved minority interest not included in Core Tier 1.

Topic 3. Tier 2 Capital

-

Tier 2 capital (or supplementary capital) is designed to absorb losses after failure. It is meant to protect depositors and other creditors. It includes:

-

Debt subordinated to depositors with an original maturity of five years or more.

-

Some preferred stock, such as cumulative perpetual preferred.

-

General loan loss reserves, not allocated to absorb losses on specific positions. Reserves may not exceed 1.25% of standardized approach risk-weighted assets (RWAs), or 0.6% of IRB RWAs.

-

-

Capital is adjusted downward to reflect:

- Debt subordinated to depositors with an original maturity of five years or more.

-

Some preferred stock, such as cumulative perpetual preferred.

-

General loan loss reserves, not allocated to absorb losses on specific positions. Reserves may not exceed 1.25% of standardized approach risk-weighted assets (RWAs), or 0.6% of IRB RWAs.

-

Common equity is known as going-concern capital. It absorbs losses when the bank has positive equity (i.e., is a going concern).

-

Tier 2 capital is known as gone-concern capital.

-

When the bank has negative capital and is no longer a going concern, Tier 2 capital absorbs losses.

-

Depositors are ranked above Tier 2 capital in liquidation so theoretically, as long as Tier 2 capital is positive, depositors should be paid in full.

Practice Questions: Q1

Q1. Under Basel III, capital must be adjusted downward to reflect which of the following?

A. Planned bonuses for managers.

B. Deficits in defined benefit pension plans.

C. Corporate convertible debt.

D. There is no requirement under Basel III to adjust capital downward for anything.

Practice Questions: Q1 Answer

Explanation: B is correct.

Capital is adjusted downward to reflect:

- Defined benefit pension plan deficits (but is not adjusted upward for surpluses).

- Certain cross-holdings within a group.

- Mortgage servicing rights greater than 10% of common equity.

Topic 4. Total Capital Requirement

-

Capital requirements for each tier and for total capital are:

-

Tier 1 equity capital must be 4.5% of RWAs at all times.

-

Total Tier 1 capital (i.e., equity capital plus additional Tier 1 capital such as perpetual preferred stock) must be 6% of RWAs at all times.

-

Total capital (total Tier 1 capital plus Tier 2 capital)must be at least 8% of RWAs at all times. This requirement was left unchanged.

-

-

By comparison, under Basel I, the equity capital requirement was 2% of RWAs and the total Tier 1 capital requirement was 4% of RWAs.

-

The new requirements are significantly more rigorous because:

-

the percentages are higher

-

the definition of what qualifies as equity capital has been tightened.

-

-

The 8% total capital requirement is the same as under Basel I and Basel II but the stricter definition of equity capital applies under Basel III.

Topic 5. Capital Conservation Buffer (CCB)

- CCB Motivation: Protect banks during financial distress, similar to U.S. Prompt Corrective Action (PCA) system.

-

Requirement: Banks must build a buffer of Tier 1 equity capital equal to 2.5% of RWAs in normal times.

-

Normal Times Minimums:

-

Tier 1 equity capital ratio: 4.5% (base) + 2.5% (CCB) = 7.0%.

-

Total Tier 1 capital: 6.0% (base) + 2.5% (CCB) = 8.5%.

-

Total capital: 8.0% (base) + 2.5% (CCB) = 10.5%.

-

-

Dividend Restrictions: When the CCB is used, dividend payments are constrained (e.g., 60% earnings retention if Tier 1 equity is 6%).

-

Motivation: Prevent government bailouts of Global Systemically Important Banks (G-SIBs) due to their significant societal cost if they fail.

-

Requirements: Additional capital ranging from 1% to 3.5% for G-SIBs (e.g., HSBC, JPMorgan Chase have been in 2.5% category).

-

Leverage Ratio Buffer: Introduced for G-SIBs (e.g., half of risk-based G-SIB buffer, or half the sum of CCB and G-SIB risk-based buffer).

-

Total Loss-Absorbing Capacity (TLAC): Proposals for G-SIBs to use TLAC instruments (equity, subordinated debt) to absorb losses and recapitalize, potentially converting debt to equity (CoCos).

-

Topic 6. G-SIBs CCB Requirements

Practice Questions: Q2

Q2. The capital conservation buffer:

A. is intended to protect banks from the countercyclical nature of bank earnings.

B. can be set between 0.0% and 2.5% of risk-weighted assets, and is at the discretion of the regulators in individual countries.

C. causes the Tier 1 equity capital ratio requirement to increase to 7% of risk-weighted assets in normal economic periods.

D. requires that total capital to risk-weighted assets must be 10.5% at all times.

Practice Questions: Q2 Answer

Explanation: C is correct.

The capital conservation buffer is meant to protect banks in times of financial distress. Banks are required to build up a buffer of Tier 1 equity capital equal to 2.5% of risk-weighted assets in normal times, which will then be used to cover losses in stress periods. This means that in normal times, a bank should have a minimum 7% Tier 1 equity capital to risk-weighted assets ratio, an 8.5% total Tier 1 capital to risk-weighted assets ratio, and a 10.5% Tier 1 plus Tier 2 capital to risk-weighted assets ratio. The capital conservation buffer is a requirement and is not left to the discretion of individual country regulators. It is not a requirement at all times but is built up to that level in normal economic periods and declines in stress periods.

-

Countercyclical Buffer (CCyB): Motivation: Protect against cyclicality of bank earnings and dampen credit cycles.

- Requirement: Discretionary for individual country supervisors, can range from 0% to 2.5% of RWAs. Must be met with Tier 1 equity capital.

- Countries requiring the CCyB may impose dividend restrictions on banks subject to this requirement

- International banks face complexity as CCyB requirements vary by country, with their overall requirement calculated as a weighted average of CCyB rates across all nations where they operate

-

Rationales:

-

Overheating: Higher capital requirements restrict credit supply, reducing potential for overheated credit markets and financial crises.

-

Cost-of-capital: Easier/less costly to raise capital in good times, allowing financial stability to be achieved at lower cost by adjusting CCyB.

-

Topic 7. Countercyclical Buffer (CCyB)

Topic 8. Liquidity Risk Management

-

Crisis Lessons: The 2007-2009 financial crisis highlighted that solvent banks could fail due to liquidity issues (e.g., Northern Rock). Basel III aimed to improve liquidity risk management.

-

Minimum Leverage Ratio:

-

Requirement: Basel III specifies a minimum leverage ratio of 3%.

-

Calculation: Capital / Total Exposure.

-

Total Exposure: Includes all on-balance sheet items (not risk-weighted) and some off-balance sheet items (e.g., loan commitments).

-

-

Mismatched Financing Issue: Banks often finance long-term obligations with short-term funds (e.g., commercial paper, repurchase agreements), which creates liquidity risk during stress periods when short-term financing becomes difficult to roll over.

-

Two Key Liquidity Ratios: Basel III requires banks to meet:

-

Liquidity Coverage Ratio (LCR)

-

Net Stable Funding Ratio (NSFR)

-

-

Focus: Bank's ability to withstand a 30-day period of reduced/disrupted liquidity.

-

Stress Scenarios: Includes events like a three-notch downgrade, loss of deposits, complete loss of wholesale funding, increased "haircuts" on collateral, and potential drawdowns on credit lines.

-

Goal: Banks should be able to sell liquid assets to meet liquidity demands during the 30-day period while restoring confidence.

-

LCR= high-quality liquid assets/ net cash outflows in a 30-day period ≥100%

-

High-Quality Liquid Assets (HQLAs):

-

Examples: Deposits at central banks, zero-risk-weight government securities (no haircuts).

-

Haircuts: Corporate debt and equity have a 50% haircut (e.g., $100M corporate debt counts as $50M HQLA). Individual mortgage loans are excluded.

-

Implementation Complexity: While the definition is simple, implementation is complex due to varying withdrawal speeds of different liabilities (e.g., 3% run-off for insured retail deposits vs. 100% for non-operational wholesale funding).

-

Topic 9. Liquidity Coverage Ratio (LCR)

-

Focus: Bank's ability to manage liquidity over a period of one year.

-

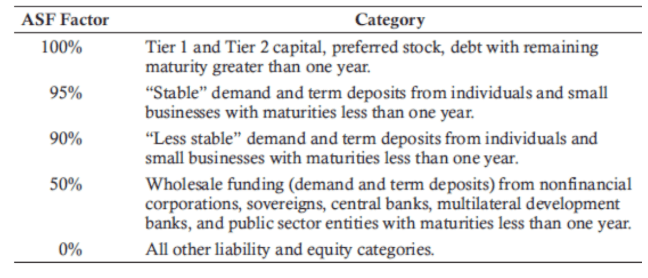

NSFR = amount of available stable funding/amount of required stable funding ≥100%

-

Available Stable Funding (ASF): Higher factor = more illiquid/less likely to leave the bank (similar to haircuts).

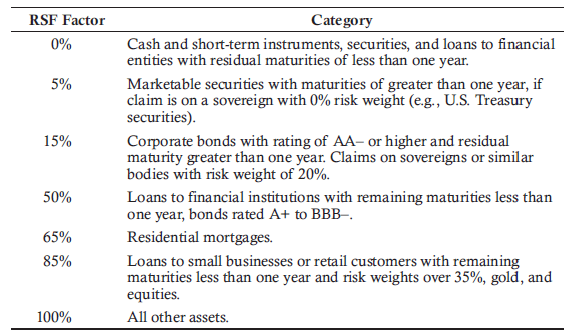

- Required Stable Funding (RSF): reflects permanence of the funding required

- NSFR is calculated by multiplying each funding source (retail deposits, repurchase agreements, capital) by a factor reflecting its stability - ASF in numerator and RSF in denominator.

Topic 10. Net Stable Funding Ratio (NSFR)

Practice Questions: Q3

Q3. Highlands Bank has estimated stable funding in the bank to be $100 million. The bank estimates that net cash outlows over the coming 30 days will be $137 million. The bank has capital of $5

million and a total exposure of $140 million. The bank estimates that it has high-quality liquid assets of $125 million. What is the bank’s liquidity coverage ratio (LCR)?

A. 89.3%.

B. 91.2%.

C. 73.0%.

D. 3.6%.

Practice Questions: Q3 Answer

Explanation: B is correct.

Basel III requires a minimum liquidity coverage ratio of 100%. The LCR focuses on the bank’s ability to weather a 30-day period of reduced/disrupted liquidity.

LCR is computed as follows:

LCR= high-quality liquid assets / net cash outflows in a 30-day period

LCR = $125 million/$137 million = 0.912 or 91.2%

In this case, Highlands Bank does not meet the minimum 100% requirement and is in violation of the rule.

Module 3. Contingent Convertible Bonds and Dodd-Frank Reform

Topic 1. Contingent Convertible Bonds (CoCos)

Topic 2. Reforms After the Global Financial Crises

Topic 1. Contingent Convertible Bonds (CoCos)

- Traditional convertible bonds convert to equity at the bondholder's option when stock price exceeds specified thresholds in the indenture

- Contingent convertible bonds (CoCos) automatically convert to equity when predetermined conditions are met, typically during financial stress periods

- CoCos function as debt during normal periods, avoiding negative impact on return on equity (ROE) calculations

- During financial distress, CoCos convert to equity providing loss-absorbing capital cushion to help prevent bank insolvency

- CoCos enable banks to obtain needed capital from private bondholders rather than government bailouts during crisis periods

-

Potential triggers that activate conversion are:

- Tier 1 Capital Ratio Trigger: Conversion activates when Tier 1 equity capital to risk-weighted assets falls below specified threshold, as seen in Credit Suisse's 2011 CoCo issuance

- Supervisory Judgment Trigger: Automatic conversion occurs when bank supervisors determine the institution requires public sector equity capital injection to avoid insolvency

- Market Capitalization Ratio Trigger: Conversion based on minimum ratio of bank's market capitalization to total assets, which may reduce balance sheet manipulation but could introduce stock price manipulation risks

Practice Questions: Q1

Q1. Which of the following statements is correct regarding the mechanics and motivations of contingent convertible bonds (CoCos)?

I. During normal financial periods, CoCos are debt and do not drag down return on equity.

II. During periods of financial stress, CoCos convert to equity, providing a cushion against loss, which helps prevent insolvency.

A. Statement I only.

B. Statement II only.

C. Both Statements I and II.

D. Neither Statement I nor II.

Practice Questions: Q1 Answer

Explanation: C is correct.

Contingent convertible bonds (CoCos), unlike traditional convertible bonds, convert to equity when the company or bank is experiencing financial strains. During normal financial periods, the bonds are debt and thus do not drag down return on equity (ROE).

- Financial Stability Oversight Council (FSOC) established to monitor systemic risks across the entire financial system and identify systemically important financial institutions (SIFIs)

- SIFI Requirements: Systemically important institutions must create "living wills" for safe wind-down procedures and may face additional capital requirements

- Executive Compensation Reform: Post-crisis changes discourage short-term performance incentives that increase risk-taking, with shareholders gaining nonbinding votes on compensation and independent directors required on compensation committees

- OTC Derivatives Regulation: Standardized derivatives between financial institutions must be cleared through exchanges or CCPs, with swap execution facilities (SEFs) mandated for price transparency

- Rating Agency Oversight: Increased transparency requirements for rating assumptions and methods, creation of Office of Credit Ratings for monitoring, and enhanced legal liabilities under Dodd-Frank

- Consumer Protection: Consumer Financial Protection Bureau created within Federal Reserve to ensure clear loan terms and prevent financial firm abuses

- Mortgage Standards: Banks must assess borrower repayment ability, with potential foreclosure restrictions if good faith effort to verify repayment capacity is not made

- Risk Management Governance: At least one board member must have risk management experience at large, complex organizations

- Securitization: Firms must retain minimum 5% of assets they securitize, with limited exceptions

- Volcker Rule: Prohibits proprietary trading by deposit-taking institutions, though distinguishing between speculative trading and legitimate hedging remains challenging