Behavioral Researcher at the Center for Advanced Hindsight

PRESENTED BY

Hi there, my name is Allison White and in this Habit Weekly PRO case study, I hope to help you uncover the following insights and tools 💡🛠

Introducing Behavioral Mapping 💡

5.

4.

1.

2.

3.

The Behavioral Map Checklist ✅

How to Build Your First Behavior Map From Scratch 🛠

Going a Few Layers Deeper With Behavior Blueprints 🕵️♀️

Special Downloadable Gift 🎁

Case Study Overview

This is the map we'll use to take us through the first section of this case study. Let's get to the first checkpoint!

From chefs👩🍳 to architects 🏢, nearly every discipline has its own unique method for organizing information.

Making sense of information

CHECKPOINT #1

Unfortunately, we often miss out on opportunities to improve our own methods by learning from other disciplines.

Making sense of information

CHECKPOINT #1

Maps are an exceptional way to visualize information 👀.

CHECKPOINT #2

If there's a map there's a way

They have the potential to break down siloed thinking, allow their viewers to grasp interlocking relationships, and mobilize teams towards a shared purpose.

If there's a map there's a way

CHECKPOINT #2

Within applied behavioral science, some organizations use a method called “behavior mapping”.

If there's a map there's a way

CHECKPOINT #2

We've made our ways to my office at the Center for Advanced Hindsight. Let's see how behavior mapping fits into our process!

A behavior map is typically created during the first phase of a project - often called a behavioral diagnosis or behavioral audit.

Identify barriers to positive behaviors and the challenges that make decision-making difficult.

Behavioral Diagnosis

Intervention Design

Implement the interventions in ways that allow for rigorously evaluating their impact

Testing

Multiply impact by sharing lessons learned form the partnership with the broader community

Sharing

Center for Advanced Hindsight Process Model

Design or modify products and services that leverage behavioral science to improve behaviors

Before we design a solution, we need to identify the root of the problem - and the diagnosis phase is dedicated to doing exactly that.

Identify barriers to positive behaviors and the challenges that make decision-making difficult.

Behavioral Diagnosis

Intervention Design

Implement the interventions in ways that allow for rigorously evaluating their impact

Testing

Multiply impact by sharing lessons learned form the partnership with the broader community

Sharing

Center for Advanced Hindsight Process Model

Design or modify products and services that leverage behavioral science to improve behaviors

Ideas42 describes behavior mapping as as “a systematic approach to identifying candidate bottlenecks… each of which is a possible intervention point.”

CHECKPOINT #4

Opening those bottlenecks

Behavior Mapping

"a systematic approach to identifying candidate bottlenecks... each of which is a possible intervention point."

The goal is to reveal “behavioral stress points,” and each of these stress points could be a promising place to design an intervention.

CHECKPOINT #4

Opening those bottlenecks

Behavior Mapping

"a systematic approach to identifying candidate bottlenecks... each of which is a possible intervention point."

But if you Google the term “behavior mapping”, you’ll likely have a hard time finding much information about how to create one 🤔 🤷🏼♀️

CHECKPOINT #4

Opening those bottlenecks

Behavior Mapping

"a systematic approach to identifying candidate bottlenecks... each of which is a possible intervention point."

So - I’m going to teach you how to make a behavior map, and also how we can make them even better by borrowing some ideas from service design 🙌🏼 (which I’ll tell you about later).

Different organizations follow slightly different steps when creating behavior maps.

But I’m going to walk you through the ones the Center for Advanced Hindsight typically use.

Before we get into the details, let's get a quick overview of all of the steps.

CHECKPOINT #5

The behavior map checklist

First, define the target behavior. This is the specific behavior you want your customers or users to perform.

Define the target behavior

Second, establish the starting point. This is the spot in the customer or user journey where you want to begin your behavior map.

Define the target behavior

Establish the starting point

Then, write down every discrete behavioral step between your starting point and your target behavior.

Write discrete behavioral steps

Define the target behavior

Establish the starting point

Next, for each step in your behavior map, state all the potential barriers your customers or users might face when trying to complete it.

Define the target behavior

State all potential barriers

Write discrete behavioral steps

Establish the starting point

And lastly, for each step, identify and brainstorm potential opportunities to reduce friciton and increase motivation of the behavior.

Define the target behavior

State all potential barriers

Write discrete behavioral steps

Establish the starting point

Identify potential opportunities

The first step is to define a target behavior 🎯- this is a specific and measurable action you want a user or customer to perform.

Let's take "I want customers to be healthier" as an example.

CHECKPOINT #6

Example: Let's get healthy

The first common mistake people make is being too outcome focused, rather than translating it into an actionable behavior.

Step 1: Define the target behavior

"I want my customers to be healthier."

"I want my customers to be healthier" is a noble goal, but there are many ways to be healthier, and even more behaviors on the path to get there. So let's choose one particular behavior.

Step 1: Define the target behavior

"I want my customers to be healthier."

A better diet can lead to better health outcomes. So let's refine our outcome down to something like "I want my customers to eat more vegetables." It's a good start, but we can do even better!

Step 1: Define the target behavior

"I want my customers to be healthier"

"I want my customers to eat more vegetables"

👉

Step 1: Define the target behavior

"I want my customers to eat more vegetables"

This leads to the second common mistake in establishing a target behavior 🎯, leaving it too broadly defined.

Step 1: Define the target behavior

"I want my customers to eat more vegetables"

It needs to be specific enough to meaningfully measure 📏.

Step 1: Define the target behavior

"I want my customers to eat more vegetables"

Although "eating more vegetables" is technically measurable, it isn't meaningfully so if we don't know our customers' baseline consumption and how much more they are or aren't eating.

Step 1: Define the target behavior

"I want my customers to eat more vegetables"

"I want my customers to eat two servings of vegetables every day"

👉

So instead of this vague behavior, let's refine it further. We know that this specific behavior results in positive health outcomes and it is relatively easy to measure.

Step 1: Define the target behavior

"I want my customers to eat two servings of vegetables every day"

And now we know how to define a meaningfully measurable target behavior 🎯!

Once you have a target behavior 🎯, which is the end point of your map, it’s time to pick the starting point.

CHECKPOINT #7

Post-it-mania

Step 2: Establish the starting point

Let's change gears to a financial target behavior 🎯, "A credit union member rounds up their loan payment into a savings account."

TARGET BEHAVIOR

Credit union member rounds up their loan payment into a savings account.

Step 2: Establish the starting point

Credit union member rounds up their loan payment into a savings account.

Pick a starting point that’s far enough upstream in the process that you don’t miss barriers that could affect downstream choices.

STARTING POINT

Credit union member inquires about qualifying for a loan.

TARGET BEHAVIOR

Step 2: Establish the starting point

But not one that is so far back that you’re mapping steps outside of your scope of influence.

STARTING POINT

Credit union member inquires about qualifying for a loan.

Credit union member rounds up their loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

In this case, if your starting point includes something like "person signs up to be a credit union member", you've probably gone too far back. This behavior may warrant its own entire behavior map.

STARTING POINT

Credit union member inquires about qualifying for a loan.

Credit union member rounds up their loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

Now let's get a little more specific about our target customer segment.

STARTING POINT

Credit union member inquires about qualifying for a loan.

Credit union member rounds up their loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

Users or customers can be segmented according to many different characteristics.

STARTING POINT

Credit union member inquires about qualifying for a loan.

Credit union member rounds up their loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

But what’s most important for a behavior map is to segment users on dimensions that affect how they behave when interacting with your product or service.

STARTING POINT

Credit union member inquires about qualifying for a loan.

Credit union member rounds up their loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

In my case, I’m only concerned about members who are applying for an auto loan - not those applying for other types of loans.

STARTING POINT

Credit union member inquires about qualifying for an [auto] loan.

Credit union member rounds up their [auto] loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

This is because I think the loan term and regular payment amounts are optimal for trying out round-ups.

STARTING POINT

Credit union member inquires about qualifying for an [auto] loan.

Credit union member rounds up their [auto] loan payment into a savings account.

TARGET BEHAVIOR

Step 2: Establish the starting point

Now that we have a target behavior and a starting point for our map we can move on to the next step, writing all the discrete behavioral steps between them.

STARTING POINT

Credit union member inquires about qualifying for an [auto] loan.

Credit union member rounds up their [auto] loan payment into a savings account.

TARGET BEHAVIOR

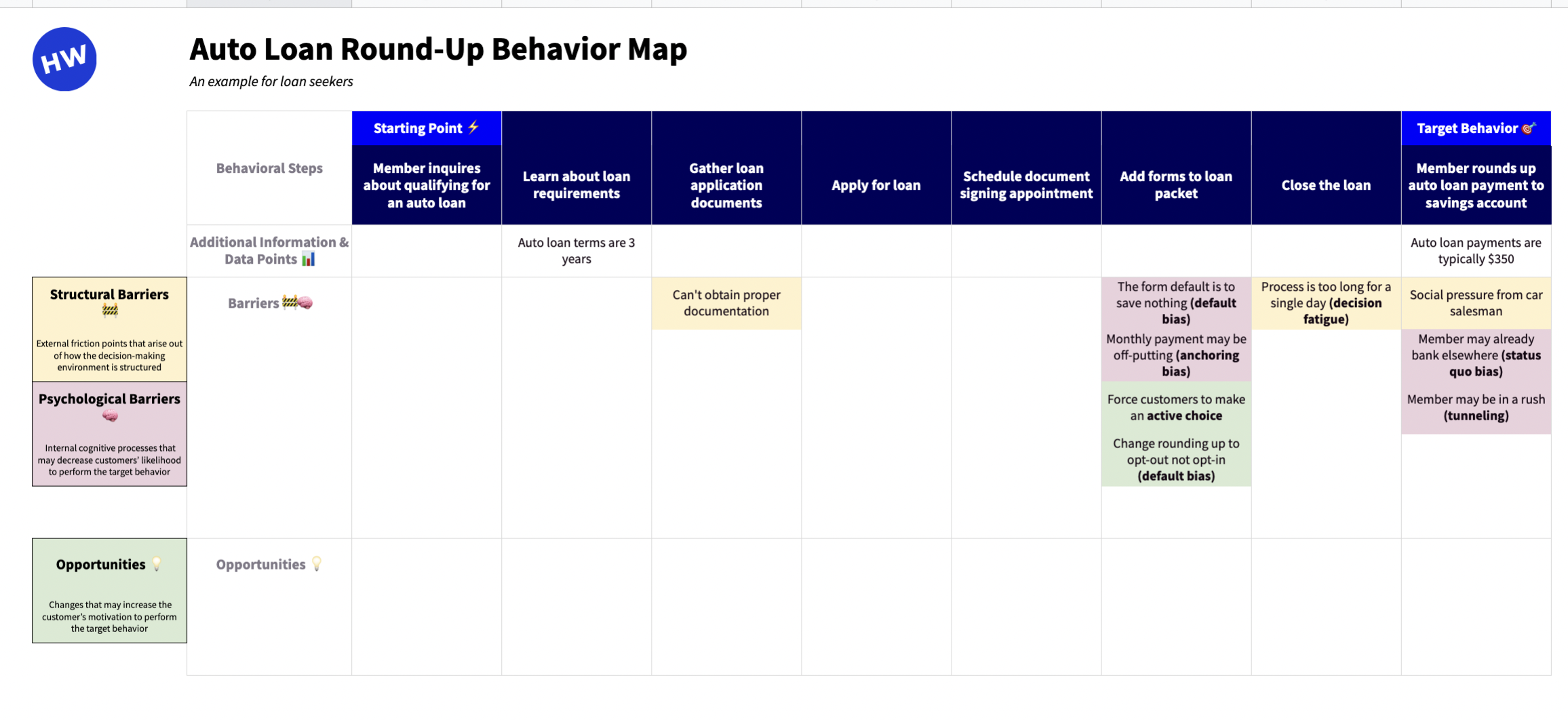

Map the end-to-end behavioral steps that an individual in your customer segment would need to perform to reach this target behavior.

Step 3: Write discrete behavioral steps

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Step 3: Write discrete behavioral steps

At this stage it can be helpful to bring in stakeholders at different levels of the process (like loan officers) to help bridge any knowledge gaps you might have. If you are an outside consultant, you may not have necessary domain-specific knowledge to accurately represent the entire behavior map.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Step 3: Write discrete behavioral steps

Also, If you have any useful data about the current state of this behavioral process, it can be helpful to represent that information on your map as well.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

Step 3: Write discrete behavioral steps

This could be data about how the process works, or engagement metrics for a more digital experience.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

Step 4: State all potential barriers

At this point you can begin to state all the potential barriers to each behavioral step in your map.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

Behavioral science typically buckets improvement hypotheses into two categories: (1) barriers, and (2) benefits - which I prefer to call opportunities.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

Barriers are the real or potential friction points that could be keeping a customer from performing the target behavior.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

These can be further broken down into two types of barriers.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Auto loan payments are typically $350

First, structural barriers 🚧 have to do with how the decision-making environment is structured; barriers that are external to the customer or user's cognition, like the way a form is designed, or the user's social environment.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Auto loan terms are 3 years

Social pressure from car salesman

Auto loan payments are typically $350

Can't obtain proper documentation

Process is too long for a single day, may experience decision fatigue

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Second, psychological barriers 🧠 are part of the customer or user's internal cognition. Psychological barriers are best identified through a review of the academic literature. These can be things like self-efficacy or identity, but here are a few examples based on cognitive biases.

Step 4: State all potential barriers

Auto loan terms are 3 years

Can't obtain proper documentation

Social pressure from car salesman

Auto loan payments are typically $350

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

The form default is to save nothing

(default bias)

Monthly payment may be off-putting

(anchoring bias)

Member may already bank elsewhere

(status quo bias)

Member may be in a rush

(tunneling)

Process is too long for a single day, may experience decision fatigue

For organizations without a behavioral scientist to help with this piece, lists of biases like this one can serve as a helpful starting point.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Auto loan terms are 3 years

Can't obtain proper documentation

Social pressure from car salesman

Auto loan payments are typically $350

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

The form default is to save nothing

(default bias)

Monthly payment may be off-putting

(anchoring bias)

Member may already bank elsewhere

(status quo bias)

Member may be in a rush

(tunneling)

Process is too long for a single day, may experience decision fatigue

Once we’ve mapped all the barriers (structural + psychological), it’s time to add the opportunities 💡.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Auto loan terms are 3 years

Can't obtain proper documentation

Social pressure from car salesman

Auto loan payments are typically $350

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

The form default is to save nothing

(default bias)

Monthly payment may be off-putting

(anchoring bias)

Member may already bank elsewhere

(status quo bias)

Member may be in a rush

(tunneling)

Process is too long for a single day, may experience decision fatigue

What opportunities exist to increase the customer’s motivation to perform the target behavior? Here are a few examples also based on cognitive biases.

Step 4: State all potential barriers

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Auto loan terms are 3 years

Can't obtain proper documentation

Social pressure from car salesman

Auto loan payments are typically $350

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Force customers to make an active choice

Change rounding up to opt-out, not opt-in

(default bias)

The form default is to save nothing

(default bias)

Monthly payment may be off-putting

(anchoring bias)

Member may already bank elsewhere

(status quo bias)

Member may be in a rush

(tunneling)

Process is too long for a single day, may experience decision fatigue

Step 4: State all potential barriers

With the behavior map finished, the team relies on research – most commonly surveys – to try to identify the most important barriers to remove, or opportunities to increase motivation.

Force customers to make an active choice

Change rounding up to opt-out, not opt-in

(default bias)

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Learn about loan requirements

Auto loan terms are 3 years

Can't obtain proper documentation

Process is too long for a single day, may experience decision fatigue

The form default is to save nothing

(default bias)

Monthly payment may be off-putting

(anchoring bias)

Member may already bank elsewhere

(status quo bias)

Member may be in a rush

(tunneling)

Social pressure from car salesman

Auto loan payments are typically $350

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Now that you know the basics to creating a behavior map, you have a choice. You can stop now and keep all the knowledge you've retained, or you can take a leap and dive with me into the deep end.

CHECKPOINT #8

The choice

Are you ready to see how deep the rabbit hole goes? Time to make your decision.

You've chosen well. Now, let's get going on our second map!

While behavior maps are a valuable tool, they do not capture the behind the scenes systems, actors, touchpoints, and policies that help shape the customer’s decision-making environment.

Behavioral interventions are often implemented by changing something about how an organization delivers an experience to end-customers.

CHECKPOINT #9

The levers of power

CHECKPOINT #9

The levers of power

Understanding the organizational context unveils what levers would need to be pulled, and where, to make an intervention happen.

So - how can we bolster behavior maps to include more of this organizational context, and help us both choose the right intervention, and plan appropriately for how to implement it?

🤔 By borrowing some tools from service design.

Service design is a human-centered design approach that places equal value on the customer experience and the business process, aiming to create quality customer experiences, and seamless service delivery.

CHECKPOINT #10

Service design

Service blueprints, the most powerful tool in a service designer's toolkit, were first described by G. Lynn Shostack in 1984.

Faced with service problems, we tend to become somewhat paranoid. Customers are convinced that someone is treating them badly; managers think that recalcitrant individual employees are the source of the malfunction. Thinly veiled threats by customers and managers are often first attempts to remedy the problem; if they fail, confrontation may result.

But these remedies obscure the basis for a lasting “cure.” Even though services fail because of human incompetence, drawing a bead on this target obscures the underlying cause: the lack of systematic method for design and control.

https://hbr.org/1984/01/designing-services-that-deliver

To be able to manage services effectively, she argued, requires better service design.

Faced with service problems, we tend to become somewhat paranoid. Customers are convinced that someone is treating them badly; managers think that recalcitrant individual employees are the source of the malfunction. Thinly veiled threats by customers and managers are often first attempts to remedy the problem; if they fail, confrontation may result.

But these remedies obscure the basis for a lasting “cure.” Even though services fail because of human incompetence, drawing a bead on this target obscures the underlying cause: the lack of systematic method for design and control.

https://hbr.org/1984/01/designing-services-that-deliver

The current work flow design and quality control methods used on the operations side of the service were not adequate in that they failed to capture a key, missing component – the customer’s relationship to and interaction with the service.

CHECKPOINT #11

Blueprints

Service blueprints are designed to capture exactly that. They use the customer experience as starting point...

...but then unpack it to expose how the organization supports that journey.

Customer Experience

Organizational Support

Credit: Illustration from Practical Service Design

Customer Experience

Organizational Support

Since Shostack’s original development of the concept, there have been many iterations and additions to service blueprints.

Credit: Illustration from Practical Service Design

But we’re going to fast-forward to 2015 when Erik Flowers and Megan Erin Miller founded Practical Service Design in an effort to integrate service design concepts into practical work contexts.

CHECKPOINT #12

To the theater

CHECKPOINT #12

To the theater

Erik and Megan describe service blueprints’ unique value add through the metaphor of a theater production.

Rather than focusing only on the end-to-end experience from the customer’s point of view, service blueprints map out a process both from end-to-end, and from surface-to-core.

Credit: Illustration from Practical Service Design

This is the term Flowers and Miller use to discuss blueprints’ ability to capture the layers of relevant information one could see if one were to pull back the curtain.

Credit: Illustration from Practical Service Design

The back stage is where all the support processes that produce the front stage live; the lights, the sets, the crew – it’s the organization and all the things we do to make that front stage happen.

Behind-the-scenes are all the intangible things that influence the front and back stage, but aren’t really part of either - such as rules, regulations, policies, and budget.

The front stage is where the action happens and what the audience can see; for us, customers act on the front stage. This is where the end-to-end steps in a normal behavior map live.

Credit: Illustration from Practical Service Design

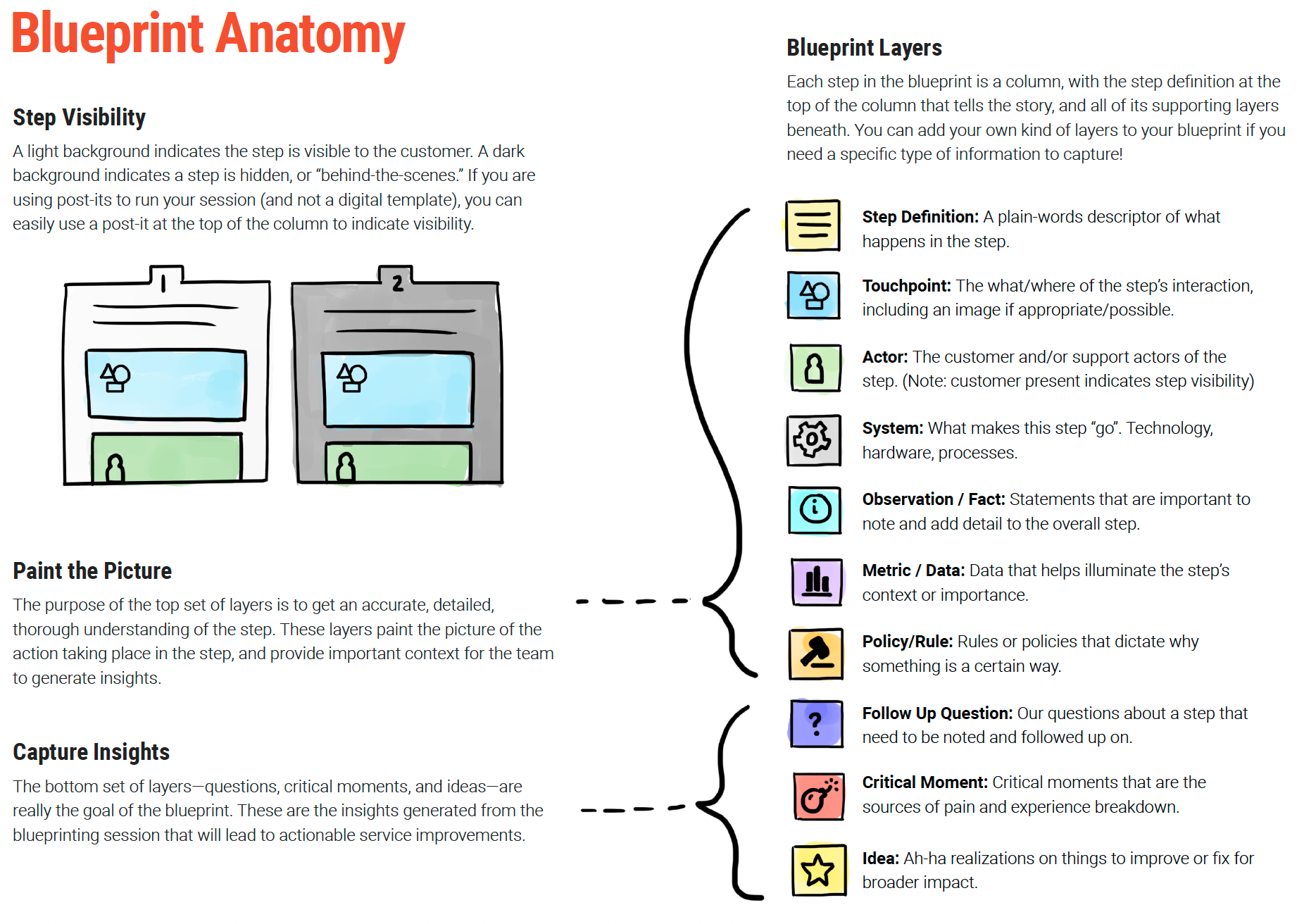

Layers

CHECKPOINT #13

Service blueprints add unique value in the depth of layers they bring to mapping out an experience.

Layers

CHECKPOINT #13

To leverage that unique value for our behavior maps, we need to understand what, exactly, those layers look like.

The initial layers of a current state blueprint seek to capture relevant details about the current state scenario.

Credit: Illustration from Practical Service Design

These layers make up the front stage, back stage, and behind-the-scenes.

Credit: Illustration from Practical Service Design

Blueprints also distinguish between process steps that the customer can see, versus ones they can’t.

Credit: Illustration from Practical Service Design

This allows for capturing the full end-to-end process - as steps happening behind the scenes can often cause implementation snags for behavioral interventions.

Credit: Illustration from Practical Service Design

Additional layers are used to capture questions, insights, and critical moments.

Credit: Illustration from Practical Service Design

It’s incredibly helpful to capture questions right underneath the process step in question - it allows us to easily fill in that relevant information once we have it.

Credit: Illustration from Practical Service Design

Critical moments are similar to barriers - except the language of “barrier” implies a target behavior, and service blueprints don’t necessarily hinge on a target behavior.

Credit: Illustration from Practical Service Design

“Ideas” are also similar to what we referred to earlier as “opportunities.”

Credit: Illustration from Practical Service Design

CHECKPOINT #14

Sources of pain

Service designers typically identify critical moments – sources of pain and experience breakdown – through contextual inquiry, user interviews, and/or focus groups.

CHECKPOINT #14

Sources of pain

While this bottom-up approach to research can be incredibly helpful for contextualizing problem framing, it can also limit the understanding of the problem.

To adapt service blueprints to a behavioral science context, we can split critical moments into the categories we discussed before - structural barriers and psychological barriers.

⚡️ Critical moment

Sources of customer pain and experience breakdown

Structural barriers

External friction points that arise out of how the decision-making environment is structured

Psychological barriers

Internal cognitive processes that may decrease customers’ likelihood to perform the target behavior

Structural barriers

Now that we understand the surface-to-core layers of a service blueprint, what does it look like to combine the best of both concepts into one, cohesive map?

External friction points that arise out of how the decision-making environment is structured

Psychological barriers

Internal cognitive processes that may decrease customers’ likelihood to perform the target behavior

⚡️ Critical moment

Sources of customer pain and experience breakdown

The steps to create one are fairly similar - with a few differences I’ll walk you through.

A behavioral blueprint is a map that captures the details of a customer’s experience from end-to-end, and surface-to-core, while also identifying potential barriers to remove and opportunities to leverage to increase the number of customers exhibiting a target behavior.

Define the target behavior

Choose your customer segment

Establish the starting point

Blueprint Checklist

You’ll still start by identifying an action-based and specific target behavior, a starting point, and a customer segment you want to target.

Next, you’ll list actions that customers need to perform to reach the target behavior.

Starting Point ⚡️

Target Behavior 🎯

Starting Point ⚡️

Target Behavior 🎯

Blueprints are also meant to capture organizational backstage processes and systems.

I find it helpful to map out steps beyond the customer target behavior itself that could end up having an impact on the intervention design.

Starting Point ⚡️

Target Behavior 🎯

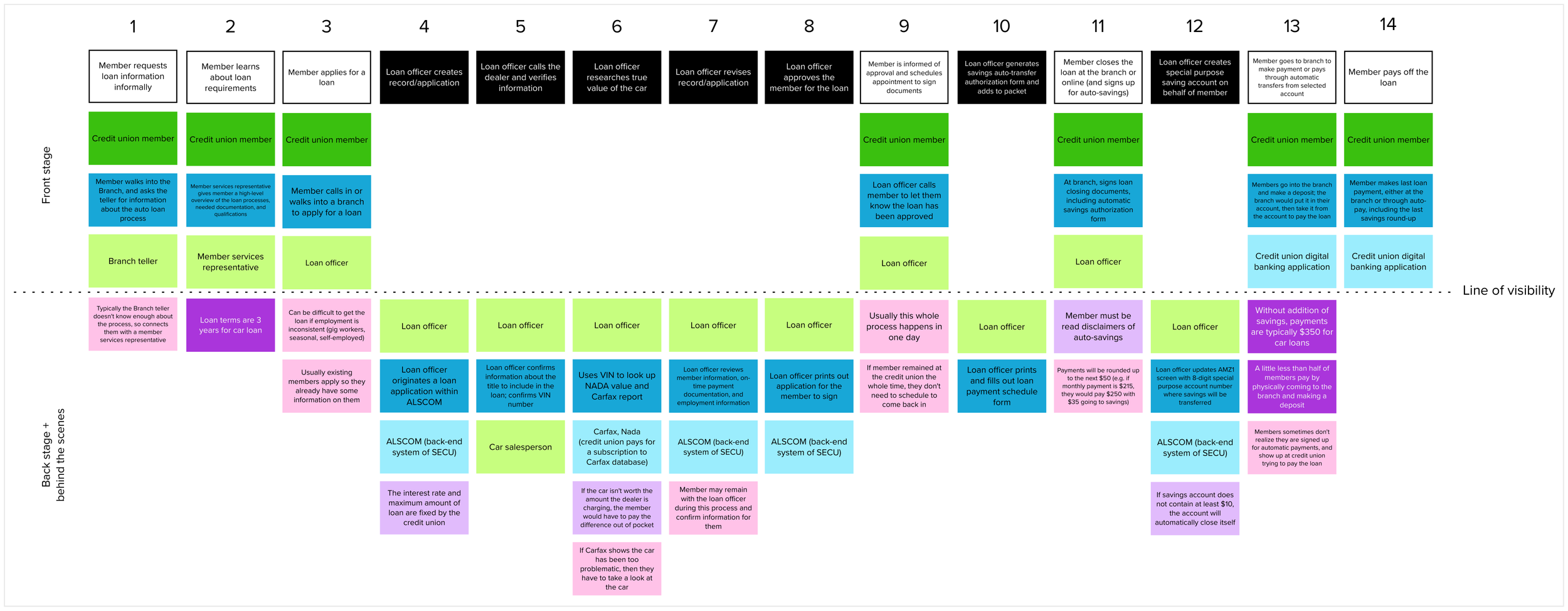

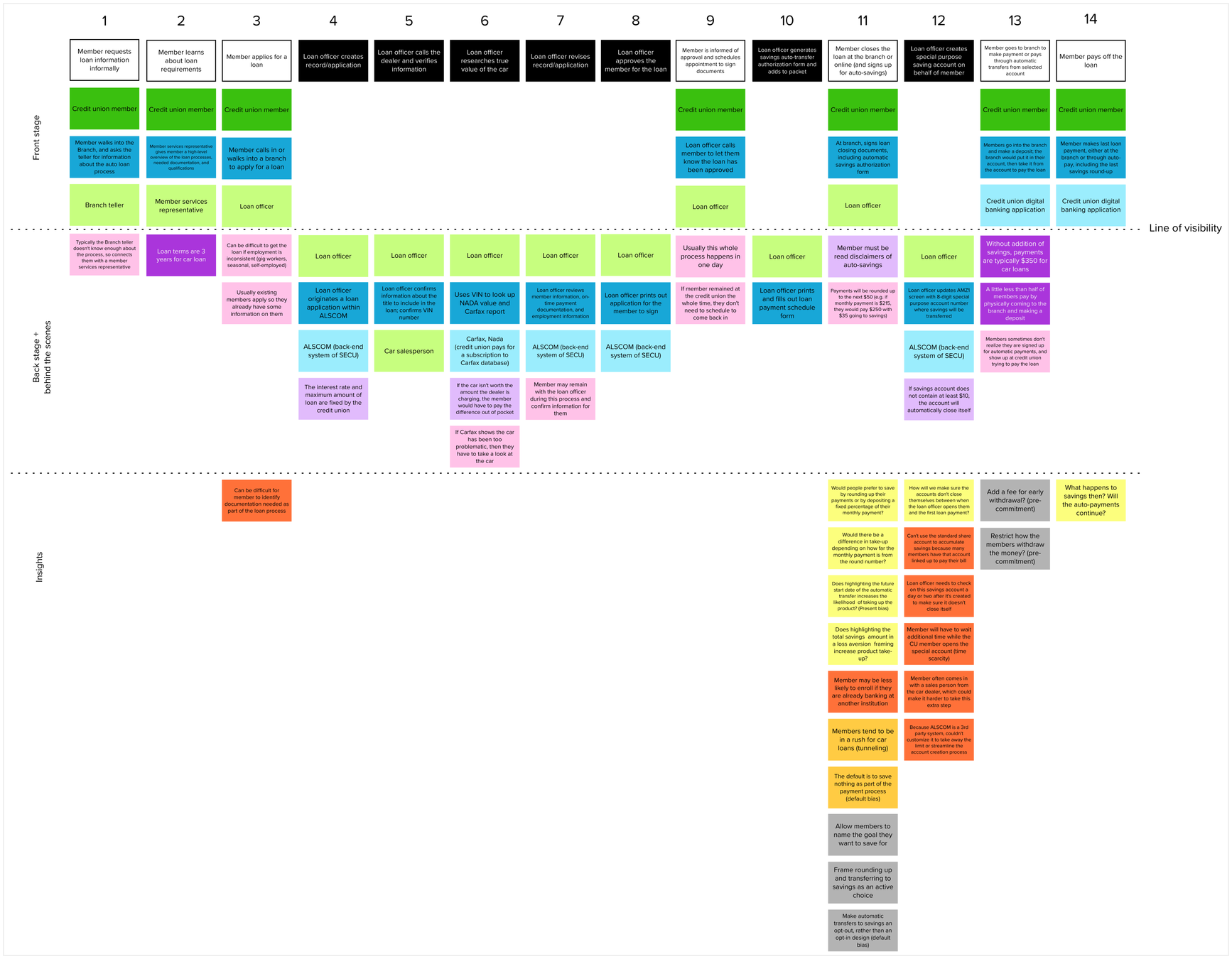

Once you’ve captured the top-level steps, use them as a checklist to add the surface-to-core detail to each step. Click on the magnifying glass to zoom in 🔎.

Here you can see that the blueprint includes the individuals involved in each step, the system that handles the step, and other relevant internal organizational factors involved in operating it.

Alright, ready to go down one more final set of layers?

Great! Now we add the final layers, including the step's barriers and opportunities. Woah, quite the map we got here! Let's zoom in.

Here you can see that the blueprint includes each step's structural and psychological barriers and its opportunities, as well as any questions about system operations or intervention design.

It can be helpful to track the outstanding questions you have about the process within each step as a reminder to the team to answer them and refine the map accordingly.

You might still be asking - do I really need all of these layers of information? What do they do for me? Here’s an example of why they matter.

Preventing an accident

CHECKPOINT #15

The Center for Advanced Hindsight worked with a credit union to design a two-condition experiment to reduce the number of members opting out of an auto loan round-up savings program.

640

Loss Aversion Condition

Control Condition

The experiment was fairly successful with enrollment rates in the round-up savings program increasing from 28% to 36% by highlighting the “loss” of not having savings at the end of the loan.

640

Loss Aversion Condition

Control Condition

26% enrollment

36% enrollment

640

Loss Aversion Condition

Control Condition

26% enrollment

36% enrollment

The round-up savings program, along with the embedded experiment, were rolled out as a pilot.

Based on a traditional behavior map, there were no indications that the pilot would be difficult to scale.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Auto loan terms are 3 years

Can't obtain proper documentation

The form default is to save nothing

Process is too long for a single day

Auto loan payments are typically $350

Social pressure from car salesman

Member may already bank elsewhere

Member may be in a rush

Change rounding up to opt-out, not opt-in

Force customers to make an active choice

Monthly payment may be off-putting

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Behavior map

Qualitative interviews with loan officers conducted after the pilot revealed some new information.

Gather loan application documents

Apply for loan

Schedule document signing appointment

Add forms to loan packet

Close the loan

Auto loan terms are 3 years

Can't obtain proper documentation

The form default is to save nothing

Process is too long for a single day

Auto loan payments are typically $350

Social pressure from car salesman

Member may already bank elsewhere

Member may be in a rush

Change rounding up to opt-out, not opt-in

Force customers to make an active choice

Monthly payment may be off-putting

Learn about loan requirements

Member rounds up their auto loan payment into a savings account.

Credit union member inquires about qualifying for an auto loan.

Behavior map

The intervention design had loan officers open a special purpose savings account the same day they closed the loan, but these savings accounts were designed to close automatically if they did not contain a minimum of $10.

This became problematic because members did not make their first deposit until the first loan payment was due.

But the 3rd party system used by the credit union barred them from removing this $10 account minimum.

During the pilot, loan officers went in and manually overrode this minimum for each member who signed up for the savings program, but this workaround was not feasible at scale.

The blueprint layers serve as a checklist to gather this kind of behind-the-scenes information.

And likely would have revealed the special purpose savings account minimum, the inability to customize the system easily, the need to create a workaround, and ultimately, the fact that the intervention design was not scalable.

Taken together, the behavior map's focus on identifying barriers and opportunities rooted in behavioral science research paired with service design’s surface-to-core layers that provide important context, provide a more holistic approach to performing a behavioral diagnosis.

A behavioral blueprint :

1

2

3

Provides a team with a complete picture of which pieces of the product or service experience are fairly set-in-stone due to actors or systems outside of their control, technical constraints, or policy constraints.

Provides a sense of which steps in the process are the biggest problem areas based on funnel metrics (when available), and it documents hypotheses about possible bottlenecks.

Reduces the number of surprises, misaligned assumptions, and implementation hiccups experienced by the team in subsequent stages of the project.

Well done, you've made it to the end of this Behavioral Mapping case study! 🎉

Thank you for diving into this Habit Weekly PRO case study with me. I hope you enjoyed it and that you learned something! Here's a summary + a special downloadable gift 🎁

1.

2.

3.

When creating a behavior map 🗺️ follow these steps:

CHECKPOINT #16

Case Study Takeaways 🚀

a.

Define a target behavior 🎯

b.

Establish a starting point ⚡

c.

Write all discrete behavioral steps 🦶

d.

State all potential barriers 🚧

Similar to behavior maps, service design blueprints 🟦 add a focus on an organization's behind-the-scenes processes.

Maps and blueprints are important because they provide a systematic method for identifying bottlenecks and limiting preventable mistakes with service delivery.

e.

Idenitfy potential opportunities 💡

🛠 Behavioral Mapping Templates

Exclusive templates for PRO members to make it easier to put your new insights to practice.

Allison is a Behavioral Researcher in the Common Cents Lab at Duke University's Center for Advanced Hindsight. At the lab, she designs and tests solutions to improve the financial well-being of low- to moderate-income individuals. Prior to joining the lab, Allison spent four years as a User Experience Designer at Deloitte Consulting. She enjoys finding intersection points between behavioral science and experience design, and exploring what the two disciplines have to offer one another.