Applied

Microeconomics

Lecture 18

BE 300

Plan for Today

Finish up Coase theorem

Introduction to Game Theory

Coming Up

Pricing Games case is due next Thursday.

Ch 12.1-12.3

Ch 13 intro, Ch 13.1-13.2, 13.5-13.6 (will likely continue into next week)

Externalities

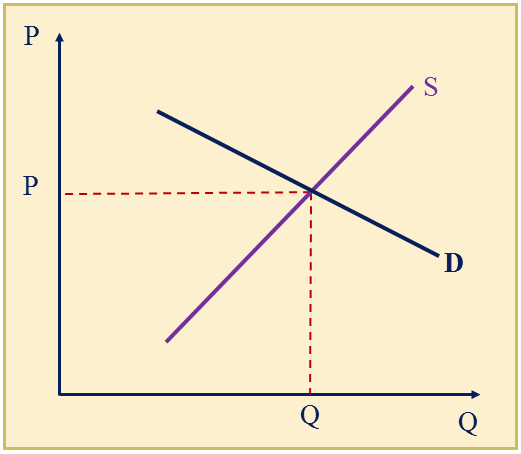

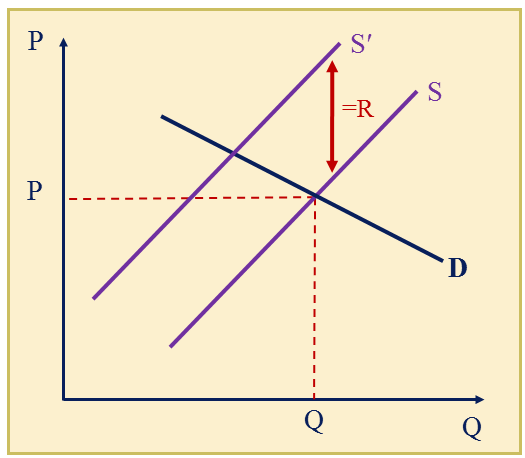

Supply curve represents ∑MC for all producers. These are private costs. But suppose there is an external cost to production, R. What is the "real" marginal cost?

Externalities

Suppose production generates pollution = a social cost of R per unit

- the supply curve that includes all costs is S′

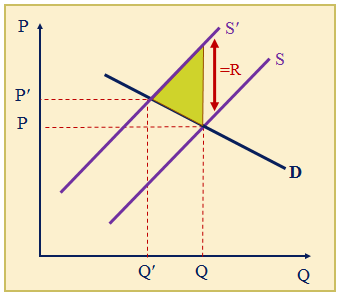

Externalities

Private parties would reach Q and P as an outcome. But accounting for the full social cost, Q′ and P′ are optimal, i.e., max social.

Externalities

Charge a price/make sure the producer pays something commensurate with the cost they impose (the externality)

- One possible approach: charge producers an emission fee (= R) per unit of output that approximates the external cost they generate

- Or impose a tax (t = R) on the good that is being produced (note: pay producers a subsidy if they generate a positive externality)

- If set at right level, then get P′ and Q′

Likely problem : what is R?

Externalities

•Government creates a market

•It either auctions off pollution permits (“emissions allowances”) or allocates permits to firms

•After the initial allocation, firms can buy and sell these permits

Enormous benefit: Allows firms, rather than government, to determine the least-cost way of reducing pollution.

What are the problems?

Coase Theorem

Ronald Coase, 1991 Nobel Prize

•Cattle from farm A damages fields of farm B…

•What can we do?

~Put up a fence? Who pays for it?

•Surprise: irrespectively of the allocation of property rights, the fence will be built.

~Efficiency doesn’t suffer

~What does?

Coase Theorem

•Under the assumption of zero transaction costs, the initial allocation of property rights does not affect the final outcome (though it does affect the distribution of welfare).

•There should be some contractable solution that allows one or both parties to internalize the externality, leading us to the socially optimal (efficient) outcome.

•When trade in an externality is possible and there are no transaction costs, bargaining will lead to an efficient outcome, regardless of the initial allocation of property rights.

Coase Theorem: Application

•The upstream factory emits discharges that harm the citizens who live downstream. The economic cost of this pollution to the citizens is $500. The factory can eliminate this pollution through primary treatment at the plant for a cost of $100. The citizens can eliminate this damage by constructing a water purification system for a cost of $300.

•What is the bargaining solution if the citizens have the property rights?

•What is the bargaining solution if the factory has the property rights?

Coase Theorem: Application

•Bargaining with victim-assigned property rights:

~Max offer by company: $100

~Min acceptance by citizens: $300

~Outcome: company installs controls, no cash transfer

•Bargaining with polluter-assigned property rights:

~Max offer by citizens: $300

~Min acceptance by company: $100

~Outcome: citizens pay company

–$100 to install controls

Limitations of Coase Theorem

1.Transactions are “often extremely costly, sufficiently costly at any rate to prevent many transactions that would be carried out in a world in which the pricing system worked without cost.” Coase (1960)

2.Property rights are not always well-defined

~Limited enforcement, due to imperfect information

~Free-riding

2.Competing effects & complex ramifications of externalities

This provides another economic rationale for regulation (and give a reference framework for developing a regulatory policy)

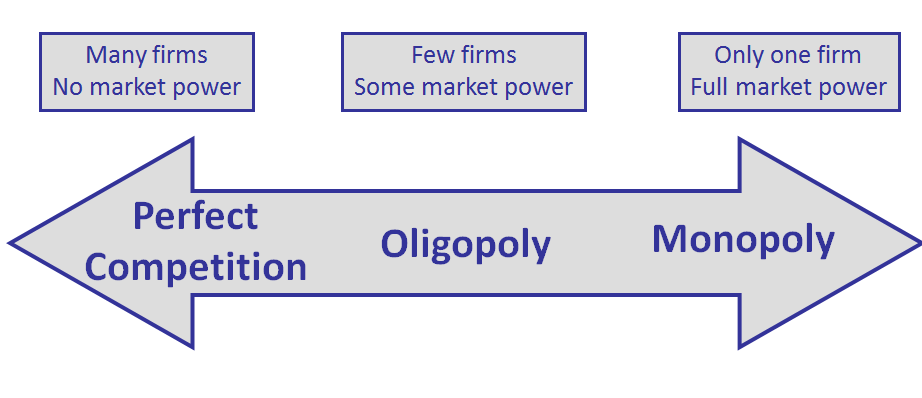

Oligopoly: Strategic Interaction

An oligopoly is a market where

- there are a few sellers, many buyers

- the product may or may not be homogeneous

- there is no entry (can be relaxed)

Oligopoly: Strategic Interaction

With relatively few firms, it becomes important to behave strategically and consider your rivals' incentives.

Oligopoly: Strategic Interaction

Because there are few sellers, firms must be concerned with actions of their competitors, and their competitors’ reactions to own decisions.

- Profit of each firm in the industry is affected by the actions of each of the others; nothing is independent.

-

You can choose your strategy, but not your profits.

-

Firms must be aware of (and plan for) potential reactions by rival firms when choosing a strategy.

Oligopoly: Strategic Interaction

Gasoline pricing:

Two identical gas stations, A and B, are located directly across from one another on a long isolated (but not divided) highway.

Price is currently $3, but you can increase or decrease it.

- If your price is above your rivals, you risk losing a significant portion of your demand!

Oligopoly: Strategic Interaction

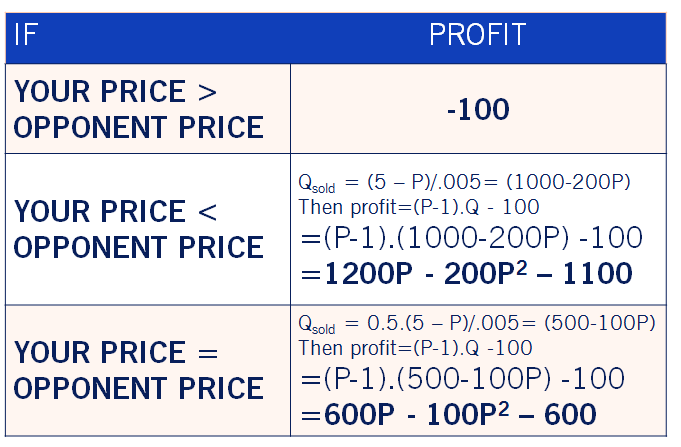

Daily demand for gasoline on this stretch of highway is

P = 5 − .005Q, where Q is gallons per day

•Currently, P = $3.00/gallon at both gas stations.

•Marginal cost is $1.00/gallon and fixed costs are $100/day.

•When the price is the same at both stations, they divide the market equally; otherwise the lower priced station gets all the demand.

Oligopoly: Strategic Interaction

Oligopoly: Strategic Interaction

Game theory is the best tool we have to model interactions among oligopolists. It allows us to:

- describe how the choices of one firm affect where it and all the other firms in the industry end up (e.g. their profits)

- identify ways that a firm can influence its rivals' decisions, as well as see how its own decisions are affected by its rivals’

Oligopoly: Strategic Interaction

"Games": Situations where mutually aware players/firms interact.

Strategies: Choices available to players

- May depend on what other players and self have done so far

- Need not at all be the same across players

Payoffs: A scale to measure how well off players are.

- For firms, profit is the standard measure

Oligopoly: Strategic Interaction

Retail gasoline pricing "game":

Two identical gas stations, A and B, are located directly across from one another on a long isolated (but not divided) highway

Daily demand for gasoline on this stretch of highway is

P = 5 - .005Q, where Q is gallons per day.

MC = $1, fixed costs are $100/day

Currently, P = $3.00/gallon at both gas stations.

When the price is the same at both stations like that, they divide the market equally; otherwise the lower priced station gets all the demand.

Oligopoly: Strategic Interaction

What is the set of strategies available to the players in this game?

What is the price that maximizes the sum of their profits?

What is the minimum price they should be willing to charge?

Oligopoly: Strategic Interaction

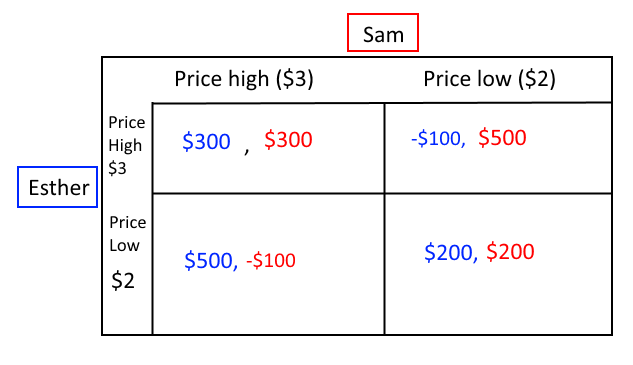

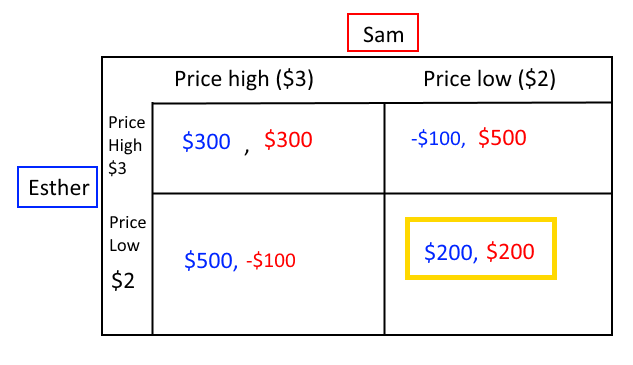

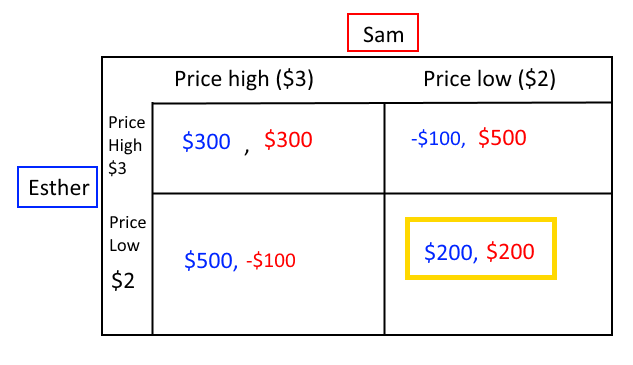

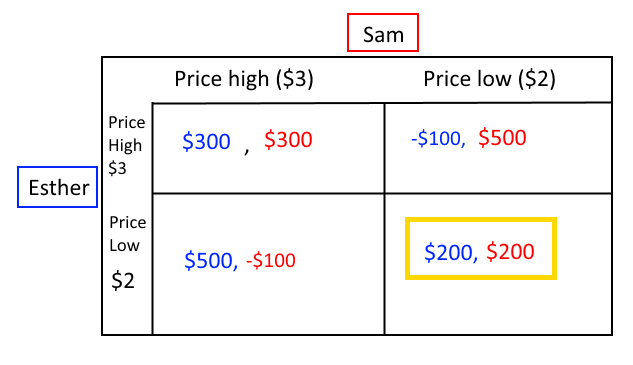

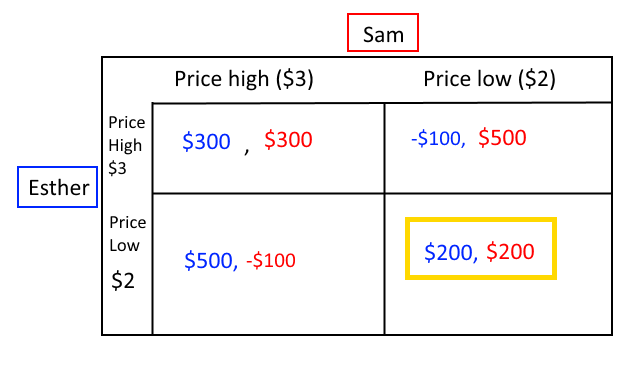

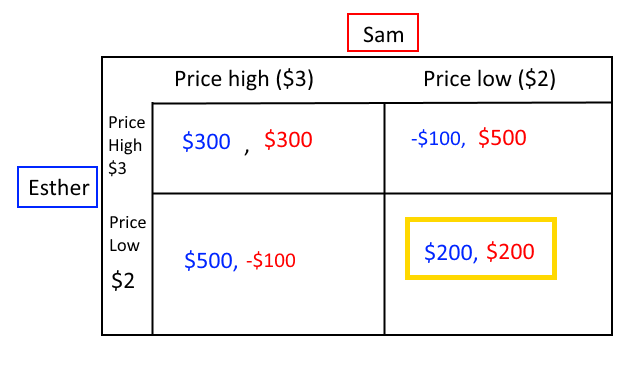

For now, let's just think about two possible prices: high price ($3) and low price ($2).

Imagine they are both charging $3. Can one of them do better by cutting the price?

Oligopoly: Strategic Interaction

For now, let's just think about two possible prices: high price ($3) and low price ($2).

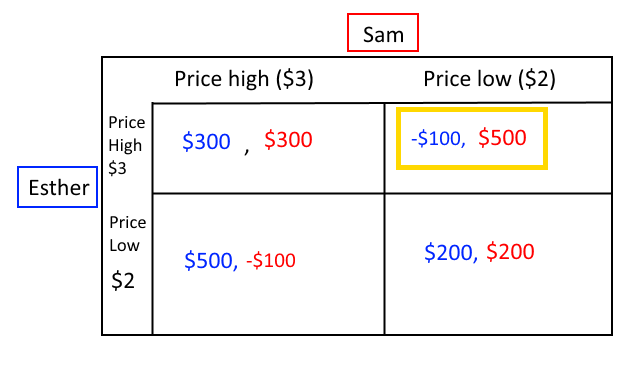

Say Sam decides to lower the price on Esther. Will Esther keep the price the same, or will she make a change?

Oligopoly: Strategic Interaction

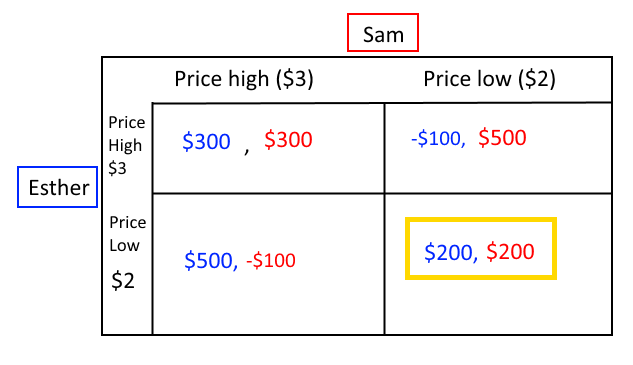

Now they are both charging $2. Does either party have an incentive to change?

Oligopoly: Strategic Interaction

Charging a low price is a Nash equilibrium.

No player has an incentive to unilaterally deviate. Is an equilibrium outcome always the best outcome?

Oligopoly: Strategic Interaction

Nash equilibrium.

A set of strategies for all players at which no player has an incentive to unilaterally deviate (i.e. equilibria are stable).

This does not mean that total profits (payoffs) are maximized, only that a player cannot unilaterally make him or herself better off

Oligopoly: Strategic Interaction

If Sam commits to always pricing high ($3), what should Esther do?

What about if Sam always prices low ($2)?

Oligopoly: Strategic Interaction

Because it is always best for Esther to price low, no matter what Sam does, pricing low is a dominant strategy.

Oligopoly: Strategic Interaction

Dominant strategy: A strategy that always turns out to be in your best interest, no matter what the other player does. If the equilibrium occurs when both players have dominant strategies, we call that a dominant strategy equilibrium.

Oligopoly: Strategic Interaction

Dominant strategy: A strategy that always turns out to be in your best interest, no matter what the other player does. If the equilibrium occurs when both players have dominant strategies, we call that a dominant strategy equilibrium.

Oligopoly: Strategic Interaction

Basic Problem: in the retail gasoline game there are huge incentives for each gasoline station to undercut the other. By undercutting, you steal all the demand from the other station. This puts lots of downward pressure on prices.

How might the bad outcome be avoided in the retail gasoline game?

Some things that limit incentives to undercut and thus limit downward pressure on prices are:

- Product differentiation (branding, advertising, quality differences, different locations)

- Repeated interaction and tacit collusion (more to come later)

- Price matching (or price beating) guarantees

Oligopoly: Strategic Interaction

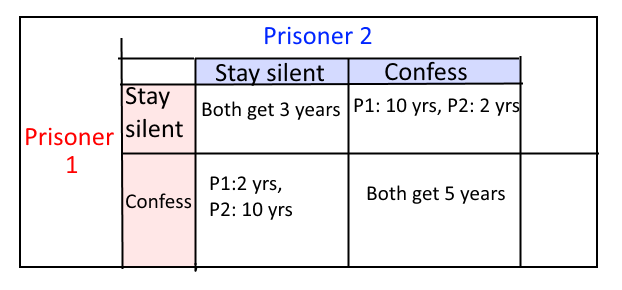

This is actually a version of a very old "game" called The Prisoner's Dilemma. We call all games of this form "prisoner's dilemma" games.

Prisoners in separate cells and must make their decision at the same time (can't wait to see what the other guy does). This is called a simultaneous move game.

Oligopoly: Strategic Interaction

What is Prisoner 1's dominant strategy?

Remember: dominant strategy means this strategy gives you the best outcome no matter what the other guy does.

Oligopoly: Strategic Interaction

What is the equilibrium in this game?

Oligopoly: Strategic Interaction

The payoff structures of the two games we’ve seen so far (simplified retail gas, prisoners’ dilemma) are very similar.

In both games, there are dominant strategies, a dominant strategy equilibrium, and the equilibrium is worse for both players than another possible outcome (e.g. both price high).

These are all what we call “Prisoners’ Dilemma” type games -- but not all games need to have a dominant strategy.

Oligopoly: Strategic Interaction

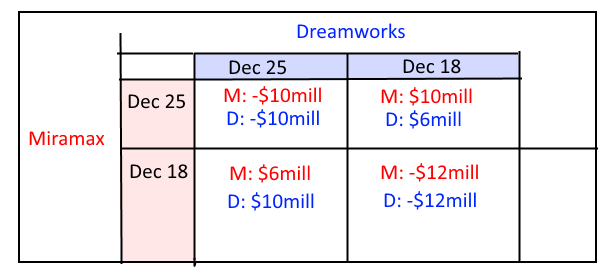

LA Times (2002): "Scorsese-Spielberg Match Called Off"

Miramax is releasing Scorcese’s “Gangs of New-York.”

Dreamworks is releasing Spielberg’s “Catch me if You Can.”

Both movies star DiCaprio and both were planning to release on Christmas day.

Oligopoly: Strategic Interaction

This type of game is called a coordination game.

Is there a dominant strategy?

Oligopoly: Strategic Interaction

This type of game is called a coordination game.

Is there a dominant strategy?

Oligopoly: Strategic Interaction

Best response strategy:

What is best for a player to do – makes him or her as well off as possible - given what the other is doing.

By definition, a dominant strategy is also a best-response strategy

Oligopoly: Strategic Interaction

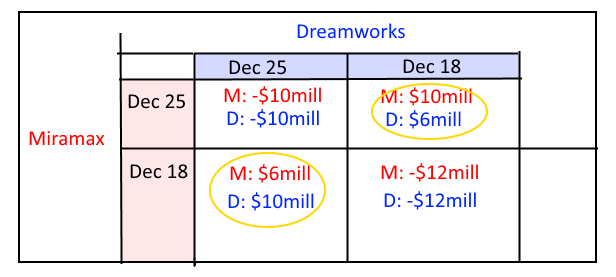

What is the Nash equilibrium in this game?

Oligopoly: Strategic Interaction

Actually there are two equilibria.

Oligopoly: Strategic Interaction

A Nash equilibrium occurs when both players are doing what is best for themselves given what the other player is doing.

- This is an equilibrium because players have no incentive to unilaterally deviate from their chosen strategy – they are doing what is best for them.

- Games can have 0, 1, or several Nash equilibria.

Oligopoly: Strategic Interaction

If games have several Nash equilibria, sometimes it takes a commitment or signal to choose among the equilibria.

If Dreamworks can credibly commit to releasing "Catch Me If You Can" on December 25th, it is in Miramax's best interest to release on December 18th.

Oligopoly: Strategic Interaction

"Miramax has decided to move Martin Scorsese's costly and long-in-the-making epic "Gangs of New York,"

which features DiCaprio in a central role, from Dec.

25 to an earlier date in December.... That means Scorsese's gritty tale of gang warfare in 19th century

Manhattan will not go head-to-head with Steven Spielberg's "Catch Me if You Can," a holiday confection

that also stars DiCapri." -LA Times (2002)

Oligopoly: Strategic Interaction

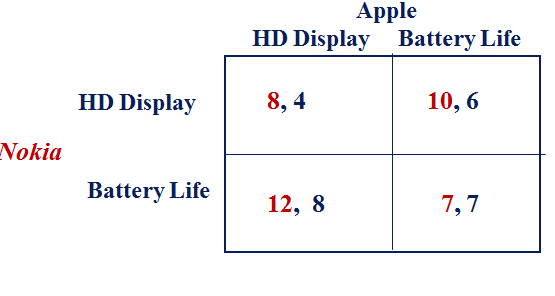

Nokia and Apple are making design decisions for next-generation smartphones. Different attributes will lead to less elastic demand curves facing each firm. The payoffs are profits for each firm.

What is (are) the Nash Equilibrium (ia)? Does either firm have a dominant strategy?

Oligopoly: Strategic Interaction

A Japanese Company (Maspro Denkoh) wanted to sell its $20 million art collection.

Couldn’t decide which auction house to use (Christie’s or Sotheby’s).

Told the to compete by playing “rock, paper, scissors.”

Does this game have a Nash Equilibrium?

Christie’s consulted an expert who recommended scissors.

Christie’s won.

Sequential Games

Sequential games are those where players get to play one after the other (as in chess).

An empty threat: a “promise” that you will do something later which, when it comes time to do it, you will not want to go ahead with.

A commitment or pre commitment: An action a player/firm can take to change its future incentives so it will want to do what it says it will do

- it changes what might have been an empty threat into a credible threat

Sequential Games

Strategic commitments are decisions that have long-term impacts and are difficult to reverse.

Examples :

- investments in capacity

- investments in inflexible technologies

- long-term contracts, with suppliers or customers

- R & D investments

- investments in the positioning of a brand

- Such commitments are valuable, they can help solve prisoner’s dilemma help solve coordination problems

improve outcomes (e.g. from bargaining, competition, etc)