Tutorial 1

Explain risk in a financial industry’s perspective. How do risks arise through a bank’s course of business?

In the financial industry, the risk is the exposure to the uncertainty of loss that has adverse consequences on the organisation.

Risk arises from the bank’s exposure to financial markets. Its investments, transactions, operations and its level of reliance on processes, system and people.

(Highlight to students that for exposure to financial markets, any dramatic change in financial prices (like interest rates, exchange rates and commodity prices) can increase costs, reduce revenues, or otherwise adversely impact the profitability of an organisation.)

Discuss with an example of how financial risk arises due to mergers/acquisitions?

Mergers and acquisitions (M&A) is a general term that refers to the consolidation of companies or assets through various types of financial transactions. Financial risk arises when the uncertainty of return of investments in the financial market, that could result in both positive or negative consequences.

DBS Bank took over the wealth management and retail banking business of ANZ in 5 markets in Oct 2016. DBS must be ready to take on the credit risk, debts, interest payment and all related financial obligation from this merger/acquisition.

Do management, operational staff, stakeholders, and the board of directors have to be involved in the management of financial risk? Why?

Yes, they should be involved so that they are in agreement on key issues of the risk the organisation is faced with. Management, stakeholders and even the board of directors will be able to determine the level of risk tolerance.

Operational staff’s awareness and involvement can help to avoid/prevent operational risks and to report the risks encountered.

Briefly explain the ‘Three Lines Of Defence’ Model in your own words.

The model illustrates how controls, processes and methods are aligned in organisations.

Lines of business

Commonly referred to as the front office, where it makes up the first line of defence. Their primary responsibility is the day-to-day risk management by identifying, measuring and managing all risks within their scope of business.

Lines of business periodically prepares self-assessment reports that identify the status of risk issues, including mitigation plans to the central risk department.

Central risk function

Standard practices require a separation between risk-taking business lines and risk supervising departments (i.e. central risk department). The department is responsible for the guidance and implementation of risk policies, for monitoring the proper execution that complies with documented risk processes.

Corporate audit and compliance functions

This is typically the third line of defence where internal and external auditors provide an independent review of the effectiveness and compliance to risk policies of the risk processes to the senior committee (board of directors). The auditors have the capacity to make recommendations and supervise the execution of the policies.

Explain with an example, one possible financial risks that will arise when banks are dealing with:

a. Other financial institutions

Market risk – due to change in interest rate (lower profit margin if interest expenses on borrowed money increase more rapidly than interest revenues on loans and security investments) or exchange rate (value of financial institution’s assets denominated in foreign currency may fall). Or any possible risks.

b. Bank customers

Credit risk – due to default loan payment

Briefly explain and elaborate the process of risk management.

The process of risk management is:

• Identify and prioritize key financial risk

• Determine an appropriate level of risk tolerance

• Implement risk management strategy in accordance with policy

• Measure, report, monitor and refine as needed

Tutorial 2

- What is interest rate risk? Explain how Interest rate risk affects organisations (both borrowers and investors) in particular to capital-intensive industries and sectors. Discuss how interest rates can affect companies and governments.

Interest rate risk is the probability of an adverse impact on profitability or asset value as a result of interest rate changes.

The reasons are due to the following:

* Most companies and governments require debt financing for expansion and capital projects and interest rates affect the cost of capital.

* When interest rates increase, the impact can be significant on borrowers.

* For e.g., a corporate borrower that utilizes floating interest rate debt is exposed to rising interest rates that could increase the cost of funds.

* A portfolio of fixed income securities has exposure to interest rates through both changes in yield and gains or losses on assets held.

2. Identify and explain (with examples) the four ways that organisations can reduce interest rate exposure without the use of derivatives?

Netting

* Organizations having cash flows in multiple currencies

* On centralize basis, pool funds from divisions or subsidiaries and make them available to other parts of the organization.

Intercompany lending

* A long-term approach to manage fund shortages and surpluses across an organization.

Changes to payment schedules

Supplier/vendor schedules

Customer payment schedules

Contractual long-term payments

2. Identify and explain (with examples) the four ways that organisations can reduce interest rate exposure without the use of derivatives?

Asset-Liability Management

For financial institutions, pairing and matching of customer loans and mortgages (assets) and customer deposits (liabilities)

Asset Liability Management (ALM) Asset/liability management is technique designed in managing the use of assets and focuses on the timing of cash flows to meet an organisation's obligations in order to reduce the firm’s risk of loss from not paying a liability on time.

Liquidity is an institution's ability to meet its liabilities either by borrowing or converting assets readily.

3. Forward rate agreement (FRA) is one of the derivatives that companies can use to reduce their interest rate exposure. Assume Company A enters into an FRA with Company B in which Company A locked in a fixed rate of 3%pa for 9 months on a loan principal of $1 million in 3 months time. The agreement will mature in 9 months. If the market rate is at 5%pa after 3 months, calculate the amount of settlement between company A and B.

Since the interest rate is 5% after three months, the settlement to the agreement will require that Company B to pay Company A. This is because the market rate is higher than the fixed rate.

$1 million at 3% interest is $30,000 pa for Company A x 6/12 = $15,000

$1 million at 5% interest is $50,000 pa for Company B x 6/12 = $25,000.

Ignoring present values, the net difference between the two amounts is $10,000, which is paid to Company A annually.

(Note: For FRA, only the difference will be paid when the agreement matures.)

4. Explain two factors that influence the market interest rates.

Inflation

The higher the inflation rate, the more interest rates are likely to rise. This occurs because lenders will demand higher interest rates as compensation for the decrease in purchasing power of the money they will be repaid in the future.

Monetary policy

The government has a say in how interest rates are affected. The U.S. Federal Reserve (the Fed) often makes announcements about how monetary policy will affect interest rates.

The rate that institutions charge each other for extremely short-term loans, affects the interest rate that banks set on the money they lend. That rate then eventually trickles down into other short-term lending rates. When the government buys more securities, banks are injected with more money than they can use for lending, and the interest rates decrease. When the government sells securities, money from the banks is drained for the transaction, rendering fewer funds at the banks' disposal for lending, forcing a rise in interest rates.

4. Explain two factors that influence the market interest rates.

Demands for loans

Interest rate levels are a factor of the supply and demand of loan: an increase in the demand for money or credit will raise interest rates, while a decrease in the demand for credit will decrease the rates. Conversely, an increase in the supply of credit will reduce interest rates while a decrease in the supply of credit will increase them.

Foreign exchange (FX) market activity

When the interest rates rise, investors will want to capitalize high returns and they channel money into that country with high interest. When one country's interest rates rise, their currency is seen as being stronger than other currencies. This happens because investors seek more of that currency to profit more. Otherwise, it is seen as a good thing when interest rates rise and a bad thing when they fall.

Foreign investor demand for debt securities

Higher interest/yield offered for debt securities will attract foreign investors to invest as this means that the debt securities are cheaper.

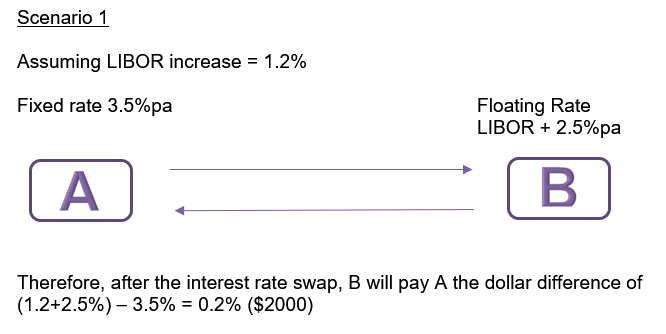

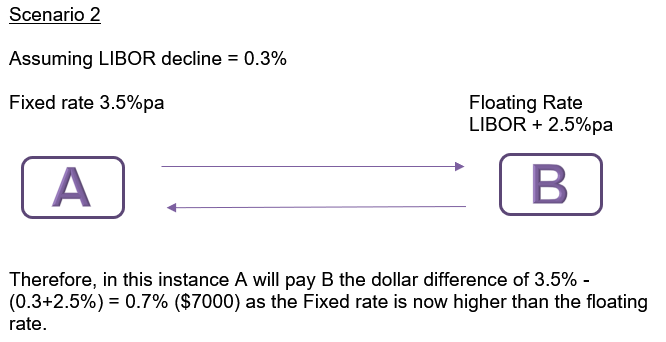

5. Illustrate and explain how an interest rate swap works.

5. Illustrate and explain how an interest rate swap works.

Tutorial 3

- Explain with example how does FX risk affect a foreign trade?

When a company does business with overseas suppliers, the transaction is usually completed in the domestic currency of the suppliers. Therefore, when the Singapore Company makes a payment to the US company, a conversion from SGD to USD is required. As FX rates fluctuate, the required amount needed to convert from SGD to USD also fluctuates. This will essentially affect the revenue of the Singapore company if their products are sold in SGD.

2. Exchange rates could have an effect on business’ competitiveness even if a company does not trade overseas. Do you agree and why?

Agree.

If a company imports supplies from the US, it will need to sell SGD for USD. When SGD loses value against the USD, imports from the US become more expensive. Local companies have to respond to aggressive pricing from other local competitors who source from the US.

3. A US company receives quarterly business revenues from its international customers, mostly in £ (GBP). The company’s primary cost is in US$ (USD). Owing to the business deals are denominated in £ (GBP), the company is faced with foreign exchange risk arises from transaction exposure.

As shown below, the GBP weakened against USD from Quarter 1 to Quarter 4.

|

Quarter |

Revenues (GBP) |

Bid |

Ask |

Revenues (USD) |

|

1st |

1,380,000 |

1.5807 |

1.5811 |

|

|

2nd |

1,420,000 |

1.4954 |

1.4959 |

|

|

3rd |

1,470,000 |

1.4065 |

1.4072 |

|

|

4th |

1,510,000 |

1.3204 |

1.3206 |

|

3a. What is transaction exposure? Give an example of a transaction with such exposure.

It is the exposure arises from ordinary business transactions denominated in a foreign currency. Some examples of such transactions are:

- Purchases from suppliers and vendors,

- Contractual payments in other currencies or

- Sales to customers in foreign currencies.

3b. From Quarter 1 to Quarter 3, there is an increase in revenues (GBP) received. Is the company making a profit or loss over this period? Comment on the impact of exchange rates on the company.

|

Quarter |

Revenues (GBP) |

Bid |

Revenues (USD) |

|

1st |

1,380,000 |

1.5807 |

2,181,366 |

|

2nd |

1,420,000 |

1.4954 |

2,123,468 |

|

3rd |

1,470,000 |

1.4065 |

2,067,555 |

|

4th |

1,510,000 |

1.3204 |

1,993,804 |

There is a decline exchange rate in GBP/USD from Quarter 1 to Quarter 3 that resulted in a difference of US$113,811 in revenue between those two quarters. It is unlikely that the company expenses would have a similar decline over that period. Therefore, the company could potentially suffer a loss if the rates continue to decline.

Even when there is an increase in revenue (GBP) received from Quarter 1 to Quarter 3, the exchange rate has caused the company to receive less in USD over that period.

4. Unlike a forward contract, where the initial premium is zero, to buy an option contract, the buyer has to pay a premium to the seller of the contract. Why?

In the option agreement, the buyer has the liberty to decide whether to exercise the option or not at the expiration of the contract. If the buyer chooses not to exercise the option, the seller will not be able to make money. Hence, the seller must be able to benefit from the contract in order for it to take place. Therefore, this initial payment of premium compensates the seller for being at a disadvantage at expiration if the buyer chooses not to exercise the option.

5. What are Call and Put options, and how do they differ from each other?

In options, an investor is given a non-obligated right to transact in the underlying asset, the right can take on two different forms. That is, he may either have the non-obligated right to buy (Call) the underlying asset, or he may have the non-obligated right to sell (Put) the underlying asset.

6. Suppose a European manufacturing firm is expecting to be paid US$600,000 for a piece of medical equipment to be delivered in 90 days. If the USD weakens against the EUR over the next 90 days the European firm will lose money, as it will receive less EUR when the US$600,000 is converted into EUR. The firm decided to hedge the fund by paying a premium to buy a USD put option (EUR call) that provides the right to sell US$ with a strike price of EUR/USD 1.1650. Assume that option premium will not be considered in the calculation.

a. If the spot rate is EUR/USD 1.1580 after 90 days, should the firm exercise the put option? Show calculation to support your answer.

At EUR/USD 1.1650 strike price, US$600,000 is equivalent to EUR515,021.

At EUR/USD 1.1580 spot rate, US$600,000 is equivalent to EUR518,134.

No, since the firm will receive less GBP after converting US$600,000. For not exercising the put option, the firm will only lose the premium paid.

7

i. What is the value of the forward contract if the spot rate is at 2.0 at the end of 3 months?

If spot exchange rate is at 2.0, the forward contract will have a positive value of 1,000,000 * (2.1356 – 2.0) = S$135,600.

ii. What is the value of the forward contract if the spot rate is at 2.2 at the end of 3 months?

If spot exchange rate is at 2.2, the forward contract will have a negative value of 1,000,000 * (2.2 - 2.1356) = S$64,400

iii. What rate is the company hoping in order to be successfully hedged?

The company is hoping for the spot rate to be below the 3-month forward bid rate of 2.1356.

Tutorial 4

- What is commodity risk and how will market participants

exposed to the risk be affected? Give an example for each of the participants

It refers to the uncertainties of future market values and future size of income caused by fluctuation in the prices of commodities.

The market participants are:

- Commodity consumers such as car manufacturers. They are exposed to rising steel prices which increase manufacturing and production cost, thus reduce profit.

- Commodity suppliers such as steel producers. Steel price reduction, for example, caused by the global crisis at the end of 2008, was hurting the steel industries as revenue was reduced.

- Commodity dealers such as commodity trading house will be affected by the price movement of the commodity in their derivative trades. In Singapore, it is SMX (Singapore Mercantile Exchange).

2. How can supply and demand of commodity cause prices to change?

Supply of commodity

Maybe reduced if problems with delivery occur, such as crop failures or labour disputes -> commodity price will increase

Cost of production such as an increase in interest rate -> commodity price will increase

Demand for commodity

May be affected if final consumers are able to obtain substitutes at a lower cost -> commodity price will decrease

Major shifts in consumer taste over the long term if there are supply or cost issues -> commodity price will decrease

3. Commodity forward is one of the strategies used to manage commodity risk. Explain how do commodity (Agricultural) consumers use forwards to reduce commodity risk?

Commodity (e.g. corn) price fluctuates due to the supply, demand and quality of the commodity. With the certainty the price increase during the winter in the later part of the year. The consumers enter into a forward contract to lock in the forward price at which the corn can be purchased during the winter.

This will ensure when supply is low during winter, the increase in corn price will not affect the consumer who has locked in the price for use in winter to buy the corn.

4. Why is a future contract different from a forward contract?

A futures contract is a standardized forward contract that can trade on an exchange.

5. A farmer bought 10 live-cattle futures contract at a price of $0.7455 per kg. In each future contract, there was an agreement to buy 40,000 kg of live cattle in 6 months time.

a. Based on the futures contract price of $0.7455 per kg, Calculate the value of the contracts.

0.7455 x 40,000 x 10 = $298,200.

b. Is there a gain or loss in the value of position for getting the futures contract if the spot price is $0.7435 per kg in 6 months time?

The spot price will be 0.7435 x 10 x 40,000 = $297,400.

$298,200 – 297,400 =$800

There is a loss of $800.

6. Royal Mill buys wheat to make flour. In 6 months Royal plans to buy 50,000 bushels of wheat, and they want to lock in a price now. Royal bought 10 wheat futures contracts at the Minneapolis Grain Exchange with a delivery price of $3.00. Each contract guarantees the delivery of 5000 bushels of wheat in 6 months for $3.00 per bushel. Note: In the futures contract, there is no physical delivery of wheat but cash settlement.

a. Royal Mill can now expect to pay a net total price of how much for their wheat?

Net total price = 5000 x 3 x10 = $150,000

b. What happens to the future position of Royal Mill, if the spot price is $3.50 per bushel?

The total value of Royal Mill’s futures position on 50,000 bushels, with an original delivery price of $3.00 has risen by 50,000 x 0.5 = $25,000.

c. Explain whether Royal Mill has successfully hedged against the price increase of wheat.

Yes, Royal Mill has successfully hedged against the price increase of wheat. Royal Mill buys 50,000 bushels from their regular supplier at $3.50 or $175,000 altogether. The net price of Royal Mill’s wheat purchase is $175,000 less the $25,000 future gain or $150,000 as desired.

Tutorial 5&6

1. Operational risk is the loss resulting from any inadequate or failed internal processes or from external events. Identify and explain an example of internal process that constitute as operational risk to an organisation?

Any example of internal process failure.

1a. DBS Bank Ltd (DBS) acquired the wealth management and retail banking business of ANZ in five markets for approximately SGD 110 million. The acquisition had tremendously increased the wealth management business of the banking group.

Impact on management information needed for decision making. Risk often increases during the post-deal period, when working practices, systems and corporate cultures not designed to work together are suddenly thrown together. Regulatory risk also arises due to the 5 markets of acquisition.

1a. DBS Bank Ltd (DBS) acquired the wealth management and retail banking business of ANZ in five markets for approximately SGD 110 million. The acquisition had tremendously increased the wealth management business of the banking group.

Impact on management information needed for decision making. Risk often increases during the post-deal period, when working practices, systems and corporate cultures not designed to work together are suddenly thrown together. Regulatory risk also arises due to the 5 markets of acquisition.

1b. A restaurant decided to use a FinTech company service to process Point of Sale instead of running its own cash management system to reduce the high operating cost.

The impact is that the restaurant must change to use outsource services and to manage the service level agreement (SLA) signed with the FinTech company to ensure that the service stays in line with the service standards of the restaurant.

1c. Company XYZ globalisation has resulted in increasing business transaction volumes arising from increased market activity. This can put pressure on company XYZ to perform and to manage the increase impact of disruption.

The impact on company XYZ is that it is facing an increasing competition when its business begins to operate across geographical borders and time zones. The time can become a new constraint or a window for problem solving.

2a. Operational risk can break into categories of people risk, process risk and systems & technology risk.

People are critical to the functioning of an organisation but they often represent one of its most significant risks due to frauds. Describe with an example each for internal fraud and external fraud arising from people risk.

- Internal fraud, i.e. Staff stealing clients information and sell it to third parties.

- Losses due to intentional acts with intention to defraud, property misappropriation, circumvention of regulations, law or company policy involving at least one internal party.

- External fraud, i.e. Phishing website to steal bank customer’s login information with the intention to steal funds from customer’s account.

- Losses due to intention acts with intention to defraud, property misappropriation, circumvention of law by a third party.

2b. U.S. Securities and Exchange Commission announced its decision to loosen restrictions on the use of Twitter and other social media by companies, a hacker from Associated Press Tweeter account announced to the world that the White House was under attack, the reaction from the market was instantaneous as the Dow declined 150 points and several billions dollars of market value was wiped out in a few seconds. Is this considered an internal or external fraud? Why?

- It is an internal fraud. The hacker is from the company.

3. The Monetary Authority of Singapore (MAS) issued a set of guidelines for financial institutions to develop and to adopt Business Continuity Management in their environment. This is to ensure business continuity and prompt recovery when the needs arise.

a. What are the objectives of business continuity planning? Explain the purpose of each objective.

The objectives are to:

- identify the organization’s exposure to internal and external threats

- provide effective prevention and recovery of organization assets

- maintain competitive advantage and value system integrity

Students are to explain/elaborate the purpose of each objective.

3. The Monetary Authority of Singapore (MAS) issued a set of guidelines for financial institutions to develop and to adopt Business Continuity Management in their environment. This is to ensure business continuity and prompt recovery when the needs arise.

b. What are the key drivers of business continuity planning? Why do they differ from organisation to organisation?

The key drivers for business continuity planning are how much of a disruption to your business is tolerable and what are you able and willing to spend to avoid disruption.

Organisation have different level of tolerance level to ops risk and the budget willing to spend differ as well.

4. Describe disaster recovery planning and how does it compliment BCP?

- Disaster recovery is part of business continuity

- Deal with the immediate impact of an event e.g. server outage, security breach

- Stop the effects of the disaster quickly and address the immediate aftermath

DRP is part of BCP which address the post disaster event. It works concurrently with BCP to get the business back up after a disaster strike the company.

5. When managing operational risk, why is it important to ensure that duties and procedures have been clearly established, documented and followed?

During a crisis,

- reduce the possibility of chaos

- instructions can be followed closely

- avoid confusing processes

- proper delegation of duties

6. Identify 2 methods to manage operational risk. Explain how the methods help to manage the operational risk.

Any 2 methods below:

- Manage financial risk with respect to financial market performance

- Clear financial risk management policy

- Documentation of policies and procedures

- Adequate risk oversight

- Segregation of duties

- Employee compensation

- Education and training

- Holidays

- Job rotation

7. What can corporations do to offset or compensate for their losses due to operation risks? Give an example.

In some cases, operational risk may be partially offset by insurance designed to meet the needs of specific operational failures of breakdown.

Tutorial 7

1. State whether the following is a trade credit, bank credit or neither. Explain your answer.

a. In the manufacturing industry, where it is common practice for manufacturers to extend long-term, low-interest payment scheme to their clients.

It is a trade credit as it involves a supplier providing the buyer with good or services in which the buyer will repay the goods with interest over a long term.

b. Individuals obtained funding from government stimulus programme.

Neither a trade credit nor bank credit because the government is neither a company nor a bank providing a loan.

1. State whether the following is a trade credit, bank credit or neither. Explain your answer.

c. A company obtain a business loan, from the bank, to be used for their day-to-day business operations and working capital requirements.

It is a bank credit as the bank has provided a loan to the company in return for the promise of interest and capital repayment in the future.

d. Money obtained from the funds that are pool together from company divisions or subsidiaries for use by any division or subsidiaries.

Neither a trade credit nor bank credit because the company divisions or subsidiaries are drawing their own funds.

2. In your own words, explain Pre-settlement and Concentration Risk. Give an example for each.

The pre-settlement risk is the risk that a counterparty of a contract, will not or unable to settle or honour their end of the deal during the contractual period but before the settlement date.

Concentration risk is describing the exposure of loans that are poorly diversified. E.g. loan issuance is focused heavily on an industry only.

3. From the following scenarios, identify the likely type/s of credit risk face.

a. On 15th September 2008, the bankruptcy of Lehman Brothers had affected many bank customers around the world. Many of them who bought the Mini-bond Notes were facing total losses of the money invested. The bank customers, including swap counterparties, were unable to receive their scheduled interest payment due to the collapse of Lehman Brothers.

It is a credit default risk.

b. For many years, company ABC has been investing in various types of business in Japan, China and Australia. Owing to the strong economic recovery, especially China, company ABC has decided to invest wholly in China.

It is a concentration risk and country risk.

3. From the following scenarios, identify the likely type/s of credit risk face.

c. XYZ Corporation has many businesses in Indonesia, due to the new ad-hoc government regulation on the foreign-owned businesses transaction in Indonesia, XYZ corporation is suddenly faced with many fund flow issues.

It is a legal risk.

4. What are some of the reasons that increase the likelihood of an organization to default?

Some of the reasons are:

- poor economic conditions and high-interest rates

- when an organization has accumulated large losses

- owes many other counterparties

- when an organization’s creditors or counterparties have financial difficulty or have failed.

5. When banks provide housing loan to their customers, their credit risk will increase if the property valuation goes down by 20%.

a. Explain why the credit risk exposure of banks will increase.

Credit risk will increase is due to the banks are facing a higher risk exposure. The property is currently worth 20% less in value and the banks have previously provided the loan based on a higher valuation.

b. What will banks do to reduce this risk?

One of the possible action is banks will need their customers to reduce their loan amount, e.g. by topping-up with cash.

6. A risk event may give rise to both market and credit risks. Credit risk often does not occur in isolation. Discuss.

- When interest rates rise, it could impair the creditworthiness of the bond issuer thereby increasing the credit risk to an institution holding those bonds. At the same time, the fall in the value of the bond raises the market risk for the institution.

- Similarly, if an institution holds many an obligor’s shares as collateral for loans granted, a deterioration in the obligor’s credit standing could result in lower share prices, causing an increase in both market and credit risks.

Tutorial 8

1. a. What is the use of a risk management framework? And how does it relate to risk management policies?

A risk management framework attempts to identify, assess, measure risk and then develop countermeasures to mitigate its impact. Sound governance, constant reporting and monitoring help in the integrity of the framework.

An effective risk management framework can protect an organization's capital base and earnings without hindering growth.

Usually, investors are also more willing to invest in companies with good risk management practices.

RM policies are designed to address the risks identified in the framework.

1. b. In a risk management framework, an organization may include “risk management practices” as one of the basic components. What are the other two basic components? Briefly explain the components.

The other two basic components are:

- Governance framework

- Ensures all company employees perform their duties in accordance with the risk management framework.

- Senior executives have the overall responsibility for monitoring and reporting of risk management in the organization.

- Risk management knowledge and skills development

- Develop the skills of managers and their staff so to increase their knowledge and understanding of the application of their risk management accountabilities and responsibilities.

2. A risk management policy is a framework that allows an organization to grow by building decision-making processes to manage risks.

a. What are the three major reasons for an organization to adopt a risk management policy?

Three major reasons are to:

- provide a framework for decision-making

- mandate a policy for controlling risk

- facilitate measurement and report of risk

b. What should a risk management policy support?

A risk management policy should support the financial risk management of an organization like

- how the organization is at risk

- identify an acceptable level of risk

- what is the cost to manage risk

- what are the risk management policies and how to manage within them

- how information will be communicated timely and accurately

3. Why is the role of management and board members of an organization important to the development of a risk management policy?

Risk Management policy is developed by a risk management team and usually must be approved by the board of directors before implementation.

The constant evolution of business and its environment requires review and updates of such policies to maintain validity from time to time.

An independent risk oversight function can be one of the requirements in the risk management policy.

a. Why is an independent risk oversight function necessary?

It is necessary because an independent risk oversight function (Risk Management Team) formed will ensure management that risk is being looked after. Usually led by the board or senior management group members.

b. In most companies, finance and treasury activities are overseen by senior management. Why is it important for senior management to report to board members and stakeholders of the company?

It is important because:

- a good understanding of financial risk faced helps to provide leadership to ensure the development of policies to measure and manage risk

- it helps to ensure management executes the plans effectively

4. Why is it important to understand the risk profile of an organization when developing a risk management policy?

When developing a risk management policy, it is important to understand the risk profile of an organization because it is:

- made up of attributes such as:

- risk tolerance

- financial position within the industry

- management culture

- stakeholders

- competitive landscape

- unique to each organization due to the different business, products and people that make up the organization

5. What are the reasons that risk profile will influence the organization’s exposure to risk differently?

The reasons are due to:

- specific exposures that impact an organization

- the market in which an organization operates

- the risk tolerance of the organization

- management, stakeholders and the board

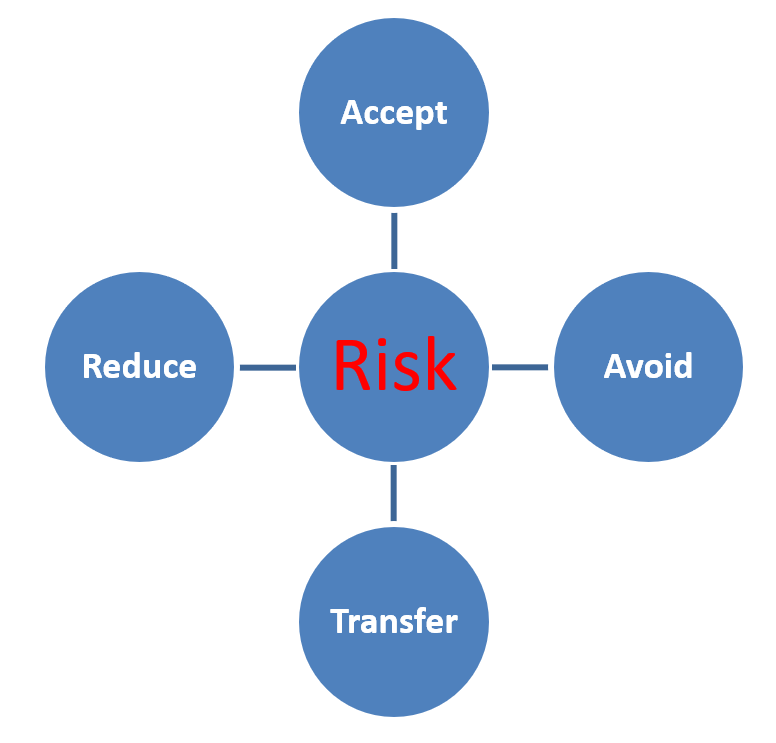

6. Discuss what does the below diagram implies and explain the various components found in the risk management practices below:

Risk management practices typically include identify risks, analyze risks, estimate risk level, evaluate risks and treat the risks.

The above illustration can be focusing on “treat the risks”. It is looking at whether the risk identified can be acceptable (or as to what level), can be avoided (perhaps to change in the way businesses are carried out), can be reduced and transferred (by hedging or sharing risks with a third party like insurance).

Tutorial 9

1. a. What is the purpose for organisation to measure credit risk?

It is to measure how a transaction, when defaulted, can potentially affect the organization overall performance.

b. Why is there an increase in emphasis in measuring risk?

Increase complexity of Financial Risk

Credit providers are exposed to a broad range of financial risks that can result in large financial losses and that need to be managed in part by quantifying and measuring the potential risk exposures. Many credit providers, e.g. banks, have invested in investment products that are evolving into very complex products.

Extend credit expose to market and operational risks

Extending credit intimately related to market and operational risks, because with an extended credit exposure, companies operations are open to volatile market conditions, which in turn may affect its operational cash flow.

2. What are the three main goals of measuring credit risk? Briefly explain each.

They are to help to:

- limit credit risk exposure

- use of collaterals covers all parties and areas

- ensure lender will be adequately compensated for the specific risks of extending credit

- the interest rates derived for facilities should allow for maximum earnings and profitability

- mitigate credit risk from economic loss

- Using techniques like hedging, collateralization, netting, guarantees

3. Name 4 of the common techniques used to mitigate credit risk? Briefly explain each technique.

The common techniques are:

- Collateralization

- Guarantees

- Hedging

- Netting

4. Suppose a bank wants to determine the expected loss on a $4,500,000 unsecured term loan to a machinery company. Assume the bank maps its internal credit ratings to that of a rating agency to give the Probability of Default at 1.6%. As the five-year term loan is fully drawn, the Exposure at Default is 100% and Loss Given Default is estimated to be 40%. Calculate the expected loss of the facility.

Note: The expected loss (EL) is a risk measure of the possibility or likelihood of a credit loss that could be incurred should an event of default occur.

Expected Loss (EL) = Principal x Probability of Default (PD) x Exposure at Default (EAD) x Loss Given Default (LGD)

= $4,500,000 x 0.016 x 1 x 0.40

= $28,800

Ans: Expected Loss is $28,800

5. Briefly explain why the formal risk rating scales used in risk rating systems have become the primary source for credit risk identification and monitoring?

It is because formal risk rating scales can help to:

- improve the precision and effectiveness of managing credit risk exposure and made the process more efficient and less time-consuming.

- provide a conceptual credit risk framework for transactions and facility structures by summarizing risks and measurable outcomes of credit default loss.

- meet regulatory requirements such as by monitoring exposure concentration limits, allocating loan loss reserves, and managing capital requirements.

6. For each of the following, identify whether it is specifically occurred from operating, operational or operations risk:

a. Nicholas W. Leeson traded on Asian futures markets in 1995 ran up debts of $1.4 billion, which brought down Britain's oldest merchant bank and landed him in a Singapore jail.

Operational (failure) – Fraud by an employee

b. PayNow system collapsed and delayed 80,000 fund transfer transaction.

Operations (processing) risk – Failure of a computer system

c. A trader buys 100,000 shares instead of 10,000 shares.

Operations (processing) risks – Incorrect entering trades

Video

List of Trading Losses

Game

Cryptogram

Cryptogram