Investment Deck

Contents

- Mission

- Problem: No Whitelabel Box Office

- Solution: Disrupt Disruption

- Solution Flow

- Why Now?

- Market Size(s)

- Competitors & Our Advantages

- Product & Service

- Product Features

- Business Model

- Customer Pipeline

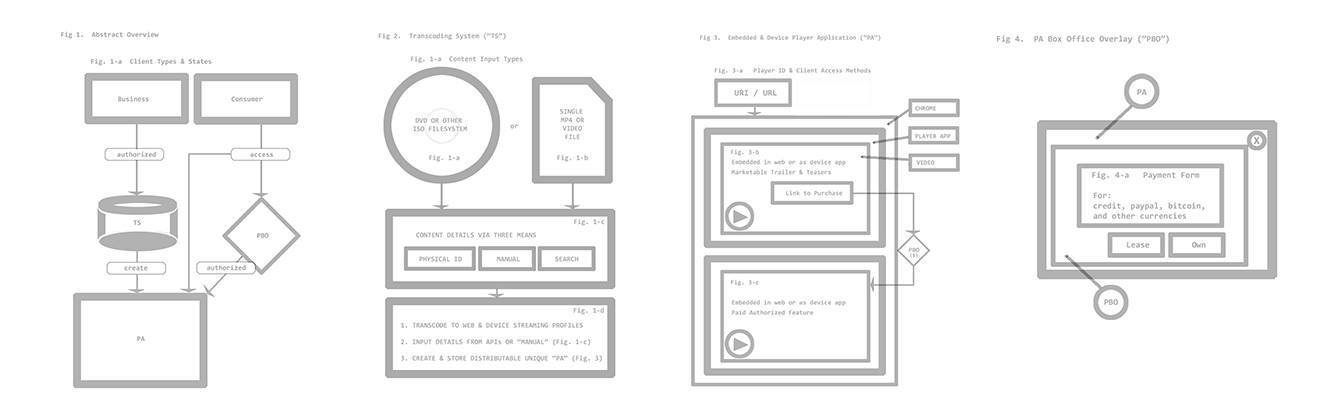

- Pending Patent Drawing

- Ingestion Video Demo

- Inventor & Noteworthy Anecdotes

- Value Proposition

- The Deal

- Contact

We want to provide any size studio & independent film maker the power to unify marketing and self-distribution for cloud-based theatrical and post-theatrical (long-tail) releases.

Also we want the film rights holder to keep

a lionshare (~95%) of generated revenue

unlike other currently available platforms.

Mission

Problem

Marketing and distribution of films on today's cloud is fragmented by third-party services and studio "+" paywalls. Their business models unoriginally fail to emulate classic and most lucrative per-title box office biz model used by conventional movie theaters.

Solution: Disrupt Disruption

Hybrid business model involving a

viral white-label box office-based player ...

Netflix (paywall) + Youtube (viral) = Cinemacloud*

(* our technology is fully derived, doesn't rely on either service)

Youtube leveraged Flash's/HTML popularity with <embed> tag allowing video to spread 'virally' in new digital consumer marketing ecosystems.

Netflix later popularized mass-licensing paywall service for flat-rate watching an ever-changing movie/show library. Now they're becoming a dominant studio themselves and are usurping Hollywood's talent pool and consumers.

Solution Flow

- Content ingested via physical ISO video_ts filesystem

- Ingest discovers film's production credits & technical A/V metadata from several disparate APIs.

- Publishers then configure box office settings like lease or own price, social network white/blacklist, and A/V transcoding settings to H.265

- Publish and take player <embed> code into native marketing context(s): film's or studio's domain, social media, any third-party site, or physical ad QR code.

Since the mid 2000's Internet video has began flourishing largely due to Youtube followed by Hulu shortly after.

Then, by turn of the decade, Netflix was rapidly redefining how production quality cinema was distributed and monetized post-theatrically and non-physically.

Since then the film industry ("biz") hasn't tended to innovate technically beyond improving the perceptual quality and special effects in films. They forfeited evolving marketing & distribution tech instead cornering just consumer tech w/ traditional licensing deals to 'disruptive' Silicon Valley-based platforms with exception being M-Go & Hulu as biz/Hollywood natives.

Why Now?

The consumer catered to is of virtually any demographic age, location, or interest spanning genres and/or topics found globally in theaters or direct-to-video.

(sources: statista, the wrap, the numbers)

TAM: ~ $42B annually

U.S. Theatrical: $12B

Global Theatrical: $32B

Physical Owning: $6B / yr (declining)

Stream Leasing: $5B / yr (growing)

SAM: $21M in 1st year, +0.1%/(yr+n) growth

If we avg. 0.05% from each TAM factor in year 1

SOM <= SAM: by 60-90%

Expect few impedances obtaining available markets

Market Size(s)

Who..

1. Netflix

2. Youtube

3. M-Go

4. Apple TV

5. Screen Room

vs. Cinemacloud

1. We sell per title anywhere

2. Box office, not ad, revenue

3. Viral not aggregated

4. Whitelabel, not proprietary

5. Not only theatrical, all phases

Competitors & Our Advantages

Our hybrid product-service begins w/ the b2b application relating to "ingest" of content into the b2c app: a marketing & distribution opportunity-creator aka "player."

In player consumer will discover, engage, and decide to lease or purchase feature after trailer(s), key art, and chapters teased.

System is trademarked & patent-pending vehicle for marketing and distributing feature film in 1080p+, on any computing, mobile, or OTT device in an <embed>, oembed, or native application context.

Product & Service

Product Features

- Automatically ingest content via physical disc

- Choose A/V & business settings for film during ingest

- H.265 HD, UHD, stereo 3D, or 360 VR (@30-60FPS)

- Markets feature with key art, trailer, & chapter teasers, production credit SEM (character, actors, chapter descr.)

- Uses LLS, rtmfp, & web-bittorrent mitigating CDN cost

- Consumer can lease, own, or gift the feature

- Physical marketing links to player via QR code

- Visitor share & comment on feature endowing its virality

1. Revenue exclusively generated box office sale conversions.

2. Prices can vary per publisher's discretion.

3. Revenue sharing is generously proportioned 95% going to publisher. Delivery cost is just a few cents/GB or less.

4. Account size is one-off purchase decision. Product life will vary depending on if leased or owned. All visitors are then retargetable leads.

5. Marketing & distribution are unified in existing digital marketing ecosystems of studios, filmmakers, or classic distributors.

Business Model

Customer Pipeline

- Native and re-targeted marketing

- Search engine marketing (SEM)

- Studio or film organic traffic and opt-in lists

- Poster & billboard direct QR link marketing

- User & commercial social media

- Physical theater value-added service

Pending Patent Drawing

Read Details in Fullscreen

Ingestion Video Demo

View Detail in Fullscreen

Inventor

- A lifetime socal resident who has worked as a video-oriented developer for 10 years, with 20 years experience in Internet programming, startup development, and Unix systems architecture.

Noteworthy Anecdotes

- Technicolor's M-Go bribed founder for IP w/ offering an architect level job for credit-only no-royalty patent filing

- Nicholas Refn discussed differences to Amazon & liked idea

- Lightspeed Ventures investor gave positive review of concept

Value Proposition

Registered approved U.S. TM #5,142,380

All systems described herein have been R&D'd by inventor using copious spare time spanning 3+ years

Estimated value of R&D efforts if compensated at fair market developer value would exceed $350k

The Deal

- Looking for active angel or silent equity partner(s) at

$150k per 5% (max 30%) per SEC's Reg. D - Investment use to free & focus founder's full time to support launch & immediate growth in ~ 6 months, small office lease & supplies, buying CDN access & servers, buying direct marketing data for biz dev, completing patent/SLA (lawyer), and accountant.

- Or trade equity for a committed strategic relationship i.e. with a studio, distributor, or connected celebrity.

Contact

- invest@cinemacloud.co

- Peter @ (424) 285-5045

- Email questions, offer, or schedule visit with

founder at Santa Monica office