Autoencoder Asset Pricing Models

Gu, Kelly, and Xiu

Motivation

- The IPCA model (a latent factor conditional asset pricing model) is powerful.

- However, it assumes the factor exposures are a linear function of the covariates.

- Existing literature suggests their relationship might be nonlinear.

Objective

- Create a nonlinear version of IPCA using autoencoders

Results

- Reduces out-of-sample pricing errors (predictive \(R^2\))

- Imposes economic restriction of no-arbitrage (no intercept)

Background

A model of returns

\[r_{i,t+1}=\alpha_{i,t}+\beta'_{i,t}f_{t+1}+\epsilon_{i,t+1}\]

- \(r_{i,t+1}\): return for stock \(i\) at time \(t+1\)

- \(f_{t+1}\): systemic risk factors at time \(t+1\)

- \(\beta'_{i,t}\): exposure of stock \(i\) at \(t+1\) to systemic risk factors

- \(\alpha_{i,t}\): intercept term (perhaps set to 0)

- \(\epsilon_{i,t+1}\): error

A model of returns

\[r_{i,t+1}=\alpha_{i,t}+\beta'_{i,t}f_{t+1}+\epsilon_{i,t+1}\]

-

\(f_{t+1}\): systemic risk factors at time \(t+1\)

- These are the "factors" in a factor model

- Systemwide: no \(i\) subscript

- Can be pre-specified or latent

- We will use latent factors

IPCA

- From "Characteristics are covariances" by KPS

- Idea: characteristics proxy for exposure to risk factors

- Momentum, volatility, bid-ask spread

- Conditional exposures: \(\beta(z_{i,t})'=z'_{i,t}\Gamma_\beta\)

- \(z_{i,t}\): vector of characteristics of asset \(i\)

IPCA

- Provides robust interpretation of returns

- If characteristics proxy for risk factors, then \(\beta\neq 0\) and \(\alpha=0\)

- If not, then characteristics can be used for compensation without risk, so \(\beta=0\) and \(\alpha\neq 0\)

- This is an "anomaly" (arbitrage)

IPCA Analysis

- \(R^2_{total}\): fraction of variance in \(r_{t+1}\) explained by \(\hat{\beta}_{i,t}'\hat{f}_{t+1}\)

- Ability of model to explained realized variation in returns (systemic risks)

IPCA Analysis

- \(R^2_{predictive}\): fraction of variance in \(r_{t+1}\) explained by \(\hat{\beta}_{i,t}'\hat{\lambda}\)

- \(\hat\lambda\): vector of estimated risk factor prices

- \(\hat{\beta}_{i,t}'\hat{\lambda}\): model-based conditional expected return on asset \(i\) given \(t\) information

- Measures the accuracy of model-implied conditional expected returns

- Ability to describe differences in average returns (risk compensation).

IPCA Results

- Achieves similar \(R^2_{total}\) to Fama-French (in sample)

- Better \(R^2_{total}\) out of sample

- More than double Fama-French in \(R^2_{predicitve}\)

-

\(\alpha\) usually insignificant from zero for 5-factor

- If significant, returns are small

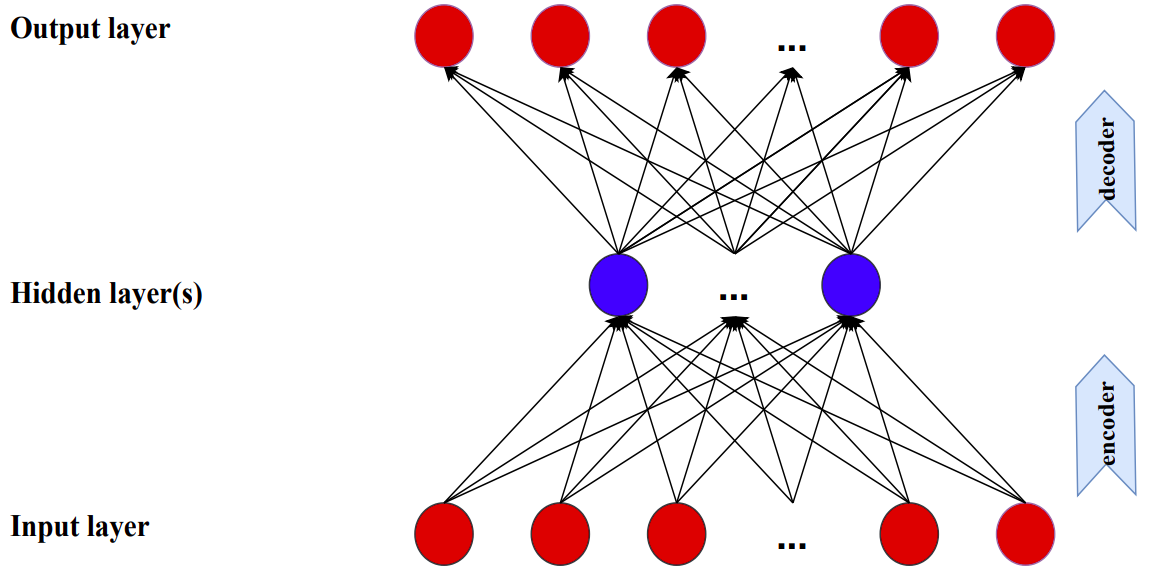

Autoencoders

- Neural network for dimension reduction

- Output layer is the same as input layer

- Hidden layer(s) have fewer neurons

New Model

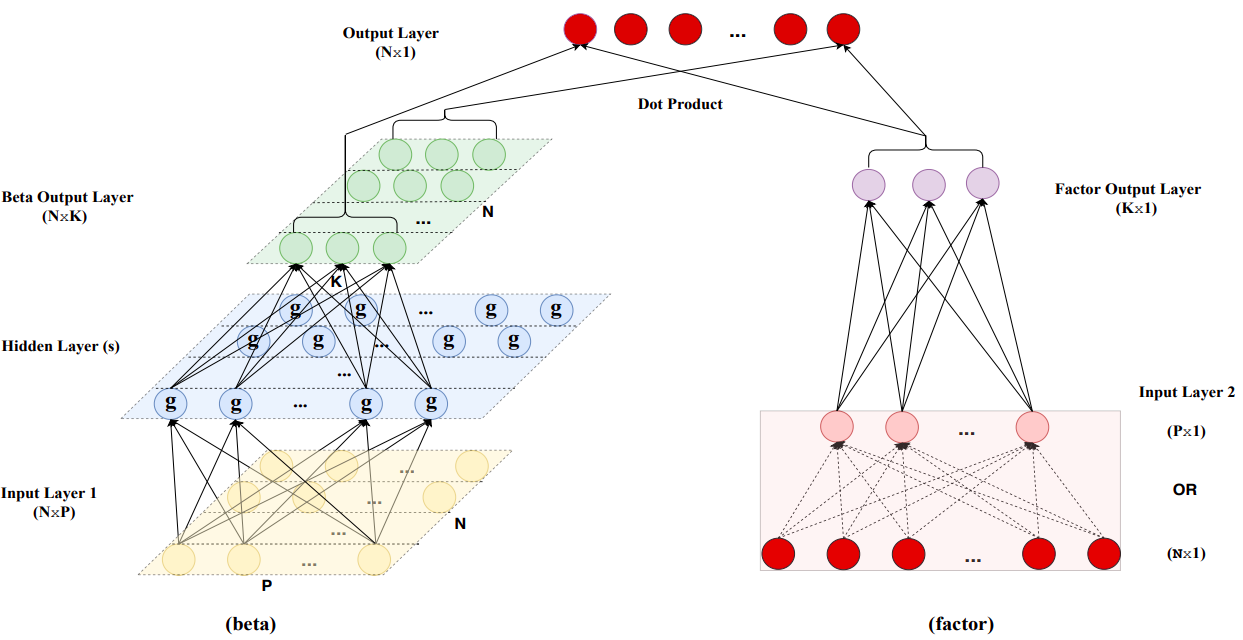

Conditional Autoencoder

- Covariates improve estimates of factor loadings and latent factors

- Design new neural network structure by augmenting a standard autoencoder to incorporate covariates

- \(r_{i,t}=\beta'_{i,t-1}f_t+u_{i,t}\)

Conditional Autoencoder

Beta (left side)

- Neural network to compute betas:

z^{(0)}_{i,t-1} = z_{i,t-1} \\

z^{(l)}_{i,t-1} = g\left(b^{(l-1)}+W^{(l-1)}z^{(l-1)}_{i,t-1}\right),\quad l-1,\dots,L_\beta \\

\beta_{i,t-1}=b^{(L_\beta)}+W^{(L_\beta)}z^{(L_\beta)}_{i,t-1}

Factor (right side)

- Neural network to compute betas:

r^{(0)}_{t} = r_t \\

r^{(l)}_t = \widetilde g\left(\widetilde b^{(l-1)}+\widetilde W^{(l-1)}r^{(l-1)}_t\right),\quad l-1,\dots,L_f \\

f_t=\widetilde b^{(L_f)}+\widetilde W^{(L_f)}r_t^{(L_f)}

- \(L_f=1\)

- This makes the factors interpretable as portfolios

Factor (right side)

- Difficult to use full cross section of individual stock returns

- Many weight parameters: 30,000 firms, 720 months

- Panel is unbalanced: only 6,000 stocks/month

- Solution: initialize network with set of portfolios

- \(x_t=(Z'_{t-1}Z_{t-1})^{-1}Z_{t-1}r_t\)

- Set of portfolios dynamically re-weighted by characteristic

- \(j^{th}\) element: return of long-short portfolio constructed by sorting stocks based on \(j^{th}\) characteristic

Objetive Function

- \(\theta\): summarizes weight parameters

- \(\phi(\theta)\): penalty function for regularization

- Use LASSO (\(l_1\))

- \(\phi(\theta;\lambda)=\lambda \sum_j |\theta_j|\)

- Set coefficients on a subset of covariates to exactly zero

- Imposes sparsity on weights

\mathcal L(\theta;\cdot) = \frac{1}{NT}\sum_{t=1}^T\sum_{i=1}^N ||r_{i,t}-\beta'_{i,t-1}f_t||^2+\phi(\theta;\cdot)

Other Regularization Techniques

- Early stopping: stop when validation sample errors begin to increase

- Usually occurs before errors minimized in training

- Ensemble: train 10 networks and use average prediction

Optimization Algorithn

- Stochastic gradient descent

- Adam optimizer

- Batch normalized: for each hidden layer in each training step (batch), cross-sectionally de-mean and standardize

- Motivated by internal covariate shift: inputs of hidden layers follow different distributions than their counterparts in the validation sample

- Should restore representation power of the unit

Data

Dataset

- Source: CRSP monthly data from NYSE, AMEX, and NASDAQ

- Range: March 1957 to December 2016 (60 years)

- 30,000 total stocks, ~6,200 per month

- Training: 1957-1974 (18 years)

- Validation: 1975-1986 (12 years)

- Testing: 1987-2016 (30 years)

Characteristics

- 94 characteristics

- 61 updated annually

- 13 updated quarterly

- 20 updated monthly

- Delay characteristics to avoid forward looking bias:

- Monthly by 1 month

- Quarterly by 4 months

- Annually by 6 months

- Avoid recursively refitting model each month

- Refit annually (most signals annual)

Characteristics

- Missing characteristics replaced by cross-sectional median of that characteristic for that month

- Distributions can be skewed and leptokurtic

- Rank-normalize characteristics

- Create 94 managed portfolios

- Also include one equal weighted market portfolio

- No filters based on prices or share types

Experiment

Model Set

- PCA: linear, constant betas, no conditioning

- IPCA: linear, conditional betas

- CA0: conditional autoencoder, single layer in both beta and factor networks (similar to IPCA)

- CA1: add hidden layer with 32 neurons to beta

- CA2: add second hidden layer with 16 neurons to beta

- CA3: add third hidden layer with 8 neurons to beta

- FF: Fama-French model with observable factors

- Try each model with 1 to 6 factors

Metrics

R^2_{total} = 1-\frac{\sum_{(i,t)\in OOS} (r_{i,t}-\hat\beta'_{i,t-1}\hat f_{t})^2}{\sum_{(i,t)\in OOS}r^2_{i,t}}

R^2_{pred} = 1-\frac{\sum_{(i,t)\in OOS} (r_{i,t}-\hat\beta'_{i,t-1}\hat \lambda_{t-1})^2}{\sum_{(i,t)\in OOS}r^2_{i,t}}

- \(\hat\lambda_{t-1}\): sample average of \(\hat f\) up to month \(t-1\)

Results

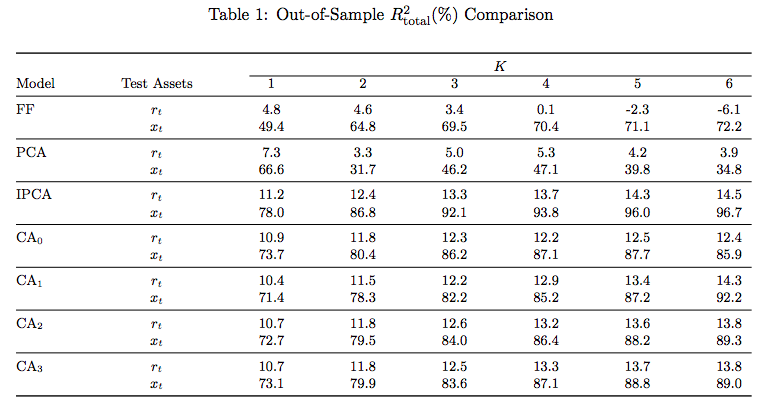

OOS \(R^2_{total}\)

- IPCA with 6 factors top performing

- Closely followed by CA networks

- FF models worst:

- Infrequent re-estimation of parameters

- Much larger cross-section of stocks than normal

OOS \(R^2_{total}\)

OOS \(R^2_{total}\)

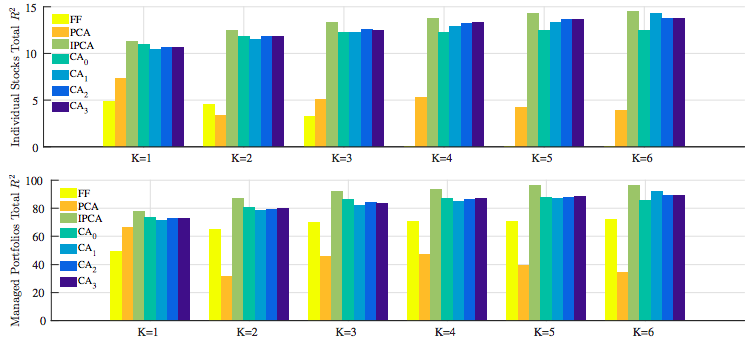

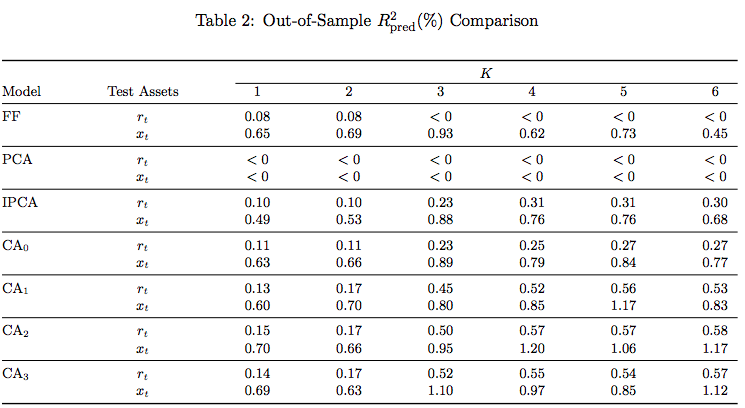

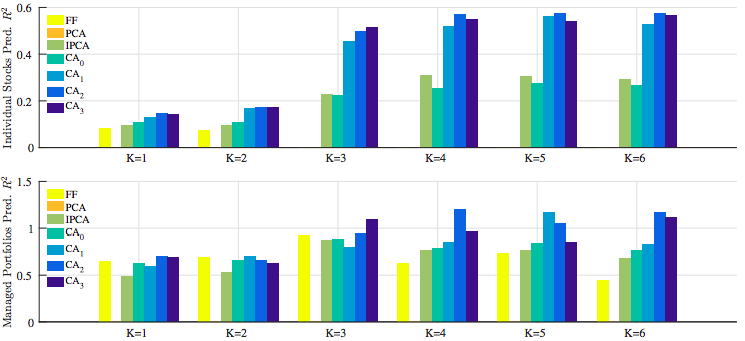

OOS \(R^2_{pred}\)

- CAs did much better than IPCA

- Static models did poorly

OOS \(R^2_{pred}\)

OOS \(R^2_{pred}\)

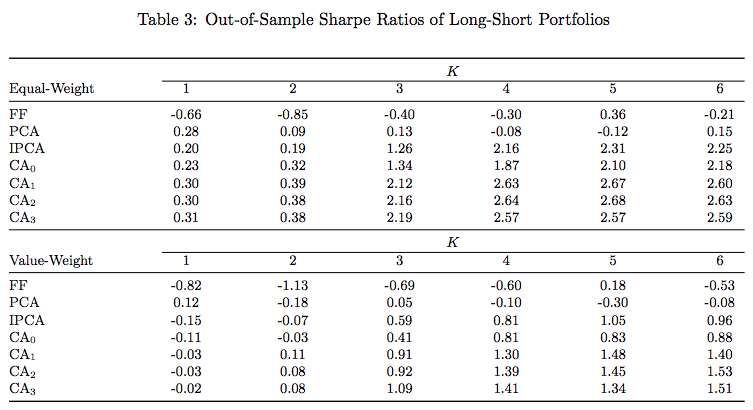

Economic Performance

- Sort stocks based on OOS forecast

- Create zero-net investment portfolio

- Buy top 10%

- Sell bottom 10%

- Equal-weighted and value-weighted portfolios

- CA2 top performing

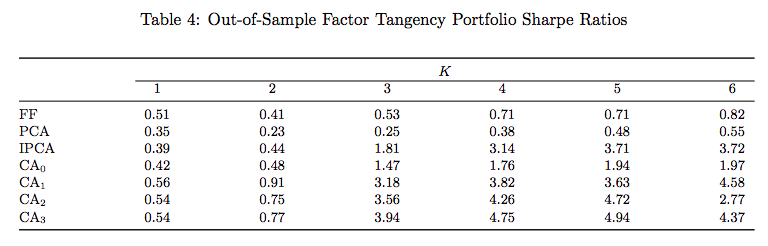

Economic Performance

Economic Performance

- Constructed using mean and covariance matrix of estimated factors through \(t\) and tracking the post-formation \(t+1\) return

- CA3 5-factor top performing

- Not necessarily implementable strategies

Risk Premia vs. Mispricing

- Models above specified with no intercept (\(\alpha\))

- Imposes no arbitrage

- Stock characteristics proxy for compensated factor risk exposures

- Should there be an intercept?

Risk Premia vs. Mispricing

- If zero-intercept is correct model, time series average of model residuals for each asset should be statistically indistinguishable from zero

- \(\alpha_i := E[u_{i,t}]=E[r_{i,t}]-E[\beta'_{i,t-1}f_t]\)

- Use \(t\)-tests

Risk Premia vs. Mispricing

- Magnitude of alphas less for CA

- Fewer are significant

- Those that are have small magnitude (7 bps/mo)

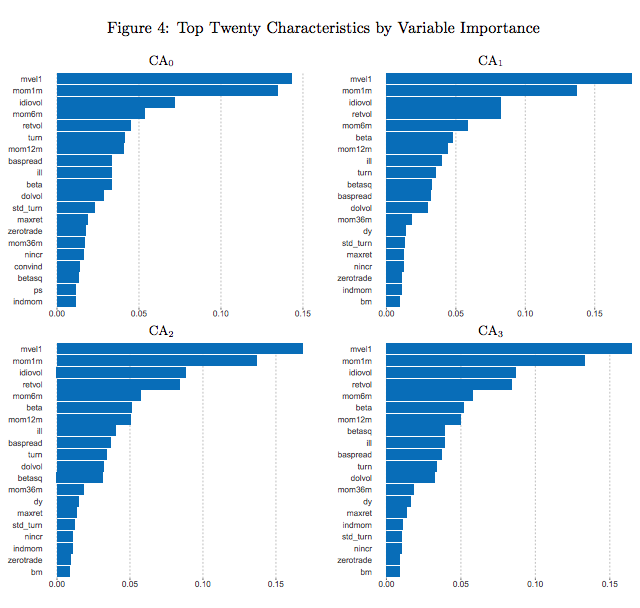

Characteristics Importance

- Variable importance by reduction in \(R^2_{total}\) when removed

- Top 20 characteristics contributed 90% for CA1-3

- Three influential categories:

- Price trend: reversal, momentum

- Liquidity: turnover, dollar volume, bid-ask spread

- Risk measures: volatility, market beta

Robustness Check

- Rerun on random subsamples

- Still performs well

Monte-Carlo Simulations

- Construct a dataset and test on it

- Performs well

Conclusion

- New nonlinear conditional asset pricing model

- Embeds economic restriction of no-arbitrage

- Dominates other asset pricing models

- Especially in predictive power

Analysis

- Well written and robust

- Like that they note perhaps not implementable

- Powerful framework for evaluating all characteristics

- Personally biased against monthly studies

- Need to look back far

- Market much different 50 years ago

- Their model can handle daily data/characteristics

- Would like to see study with short return periods and higher frequency characteristics