Building data set pipelines for

deep learning strategies

See important disclosures at the end of this presentation.

Ankit Awasthi

Quantitative Portfolio Manager

The Trading Show NY, September 26th, 2018

Outline of the talk

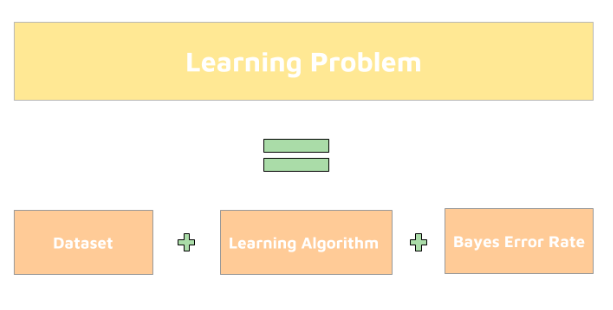

Breaking down a generic learning problem

Criteria for selecting datasets

Improving deep learning strategies using hypothetical data

Future Testing Strategies

Breaking down a general machine learning problem

Illustrative and Representative Only

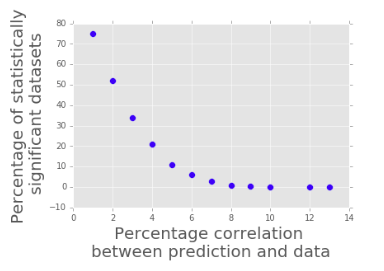

Hard problems are easy (to overfit)!

Here, for a dataset of 1,000 data points, given an expected correlation of 1%, around 75% of datasets could appear to be statistically significant, whereas for expected correlation values of 13%, it is close to 0.

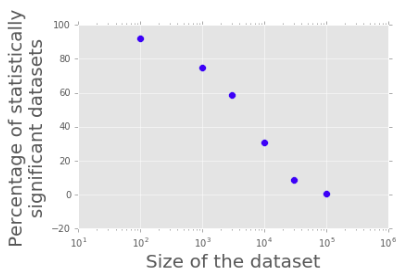

Hard problems are easy (to overfit)!

Given expected correlation of 1%, as the size of the dataset increases from 100 data points to 100,000 data points, the chances of a random dataset appearing statistically significant goes from around 92% to close 0%

Select a dataset that...

Is clean and reliable

Has high coverage

Has long history

Is predictive over long horizons

Data Cleaning and Validation

Addressing look-ahead bias

Filling in missing data

Outlier Detection

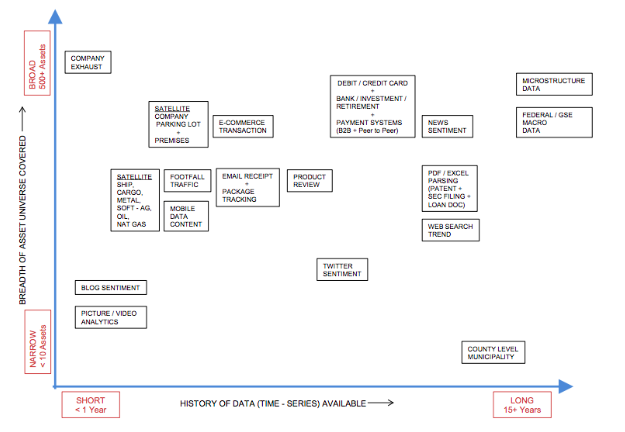

Datasets : Coverage vs History

Source : JP Morgan

Macro data and price volume data have the highest coverage with longest history!

Tremendous Success of Deep Learning

Image

Text

Speech

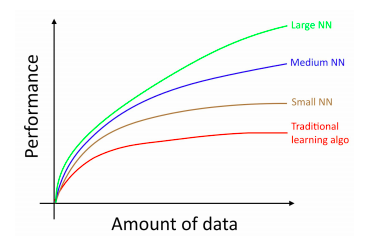

Abundance of Data!

Deep learning scales with data

Source : Andrew Ng, Coursera Deep learning specialization

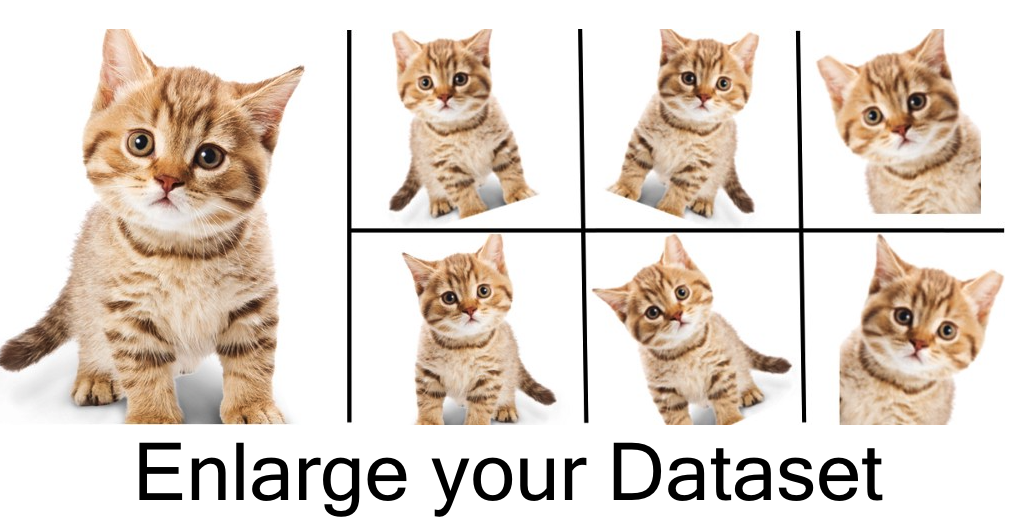

Data Augmentation for Deep Learning

Even more data!

Source : Bharat Raj, Data Augmentation | How to use Deep Learning when you have Limited Data

Much harder in Finance!

Generating Hypothetical Data for Trading

Adding noise or transformations

Theoretical models

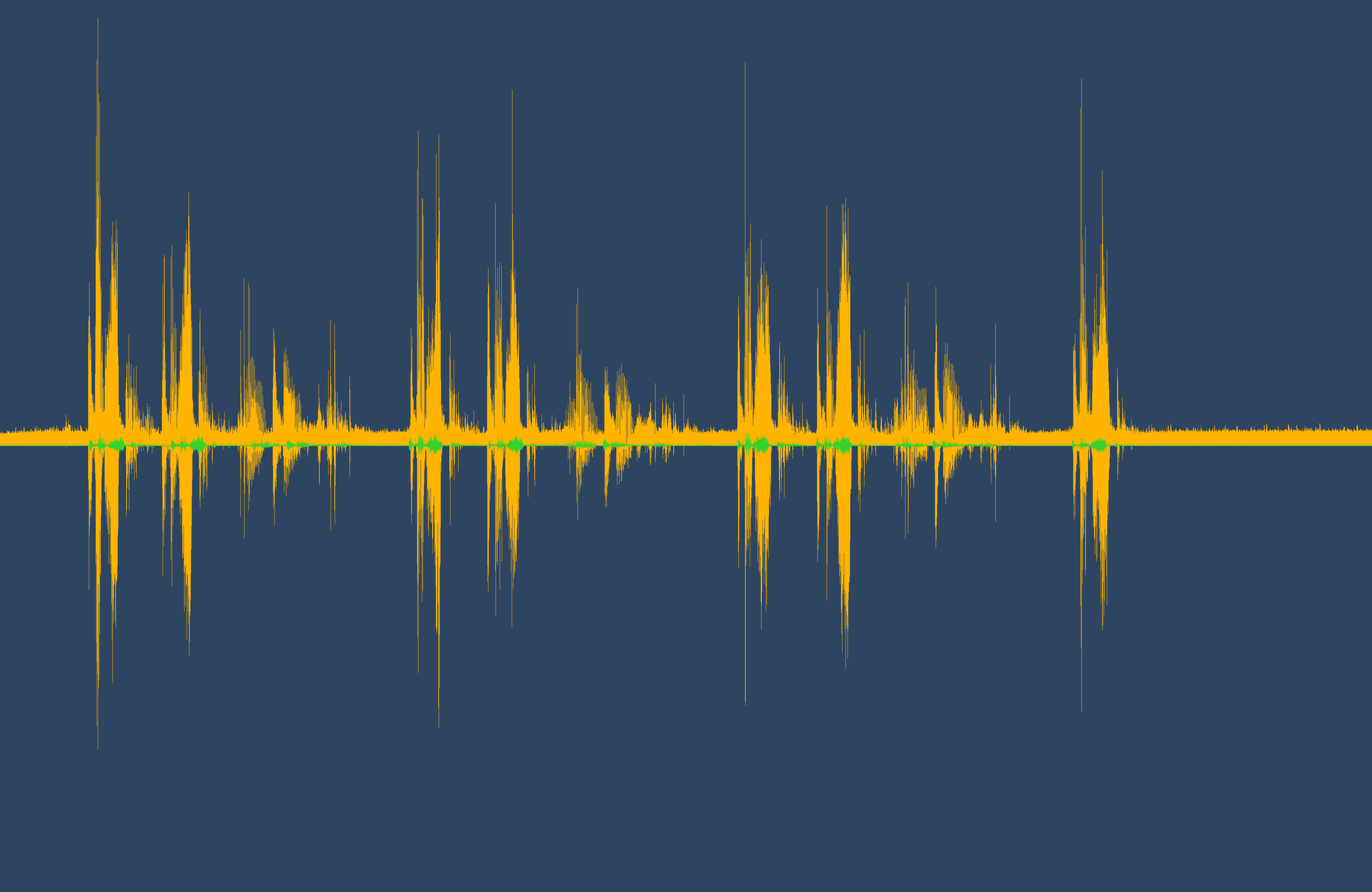

Appropriating High Frequency Data

Stylized Effects of Financial Time Series

Absence of Autocorrelations

Heavy Tails

Volatility Clustering

Leverage Effect

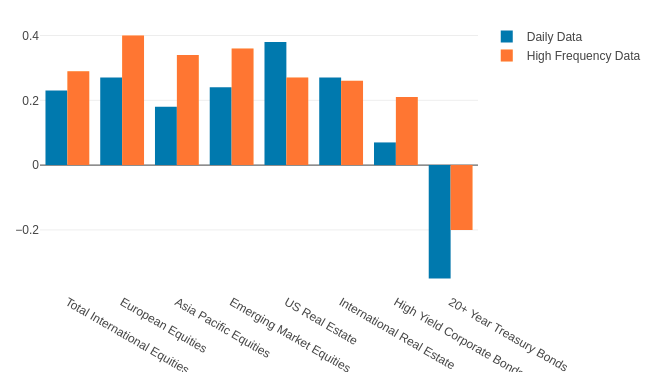

Cross Correlation vs Volatility

Reference : Empirical properties of asset returns: stylized facts and statistical issues, Rama Cont

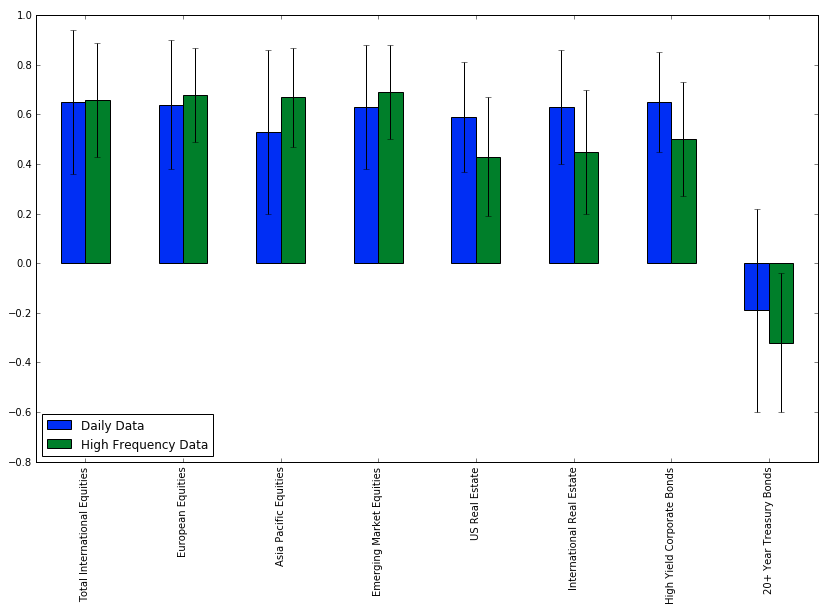

Cross-Correlation Vs Asset Volatility

Mean of 30-day rolling correlation of different assets with US Total Stock Market (VTI)

Standard Deviation is shown as error bars.

Correlation (Mean and Variance)

Correlation increases with volatility

Correlation of 30-day rolling correlation of log returns of different assets vs US Total Stock Market against the volatility of US Total Stock Market.

Correlation

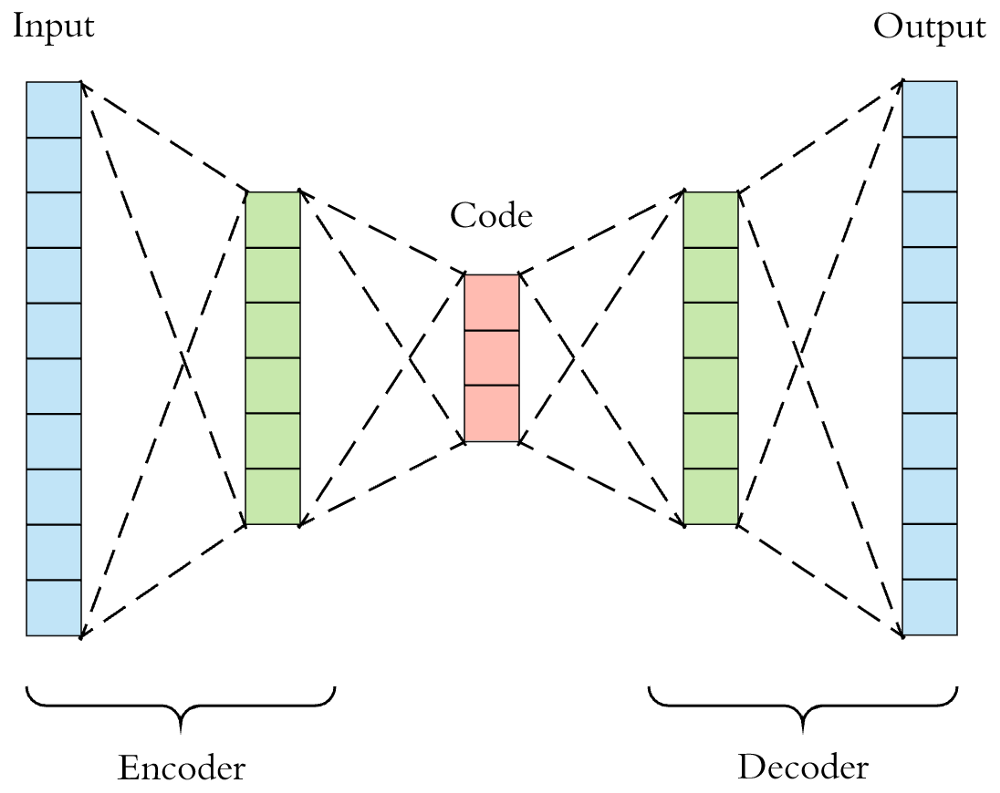

A simple example - Autoencoders

Source : Arden Dertat, Applied Deep Learning

Experimental Setup

Daily EOD Data

Training

3000 pts

Validation

1000 pts

Testing

1000 pts

Large High Frequency Data Corpus

( 32000 pts )

Training

(High Frequency + Daily)

Validation

Out of Sample

Evaluation

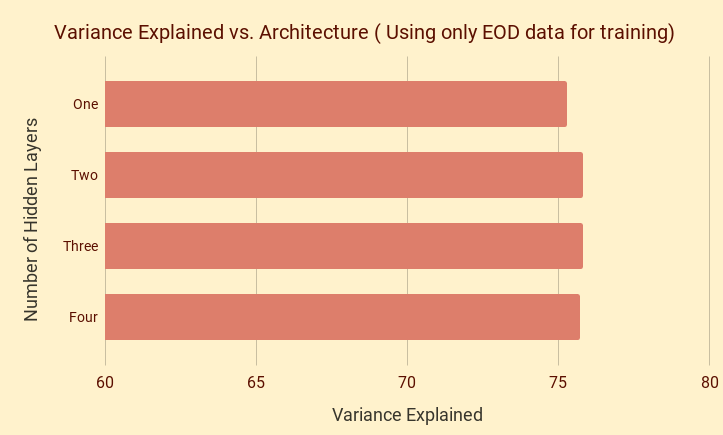

Model complexity alone doesn't help much!

One Hidden Layer : 62 -> 3 -> 62

Two Hidden Layers : 62 -> 10 -> 3 -> 10 -> 62

Three Hidden Layers : 62 -> 20 -> 10 -> 3 -> 10 -> 20 -> 62

Four Hidden Layers : 62 -> 100 -> 20 -> 10 -> 3 -> 10 -> 20 -> 100 -> 62

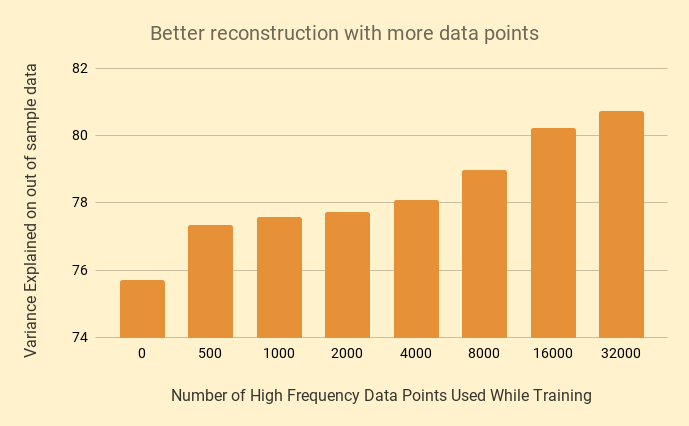

However....more data does!

Architecture Used : 62 -> 100 -> 20 -> 10 -> 3 -> 10 -> 20 -> 100 -> 62

Stress / Future Testing Investment Strategies

Helps to be data-driven with more data!

Scenario Analysis

Cross-Validating Hyperparameters

Future performance under different capital market assumptions

Key Takeaways

Overfitting is one of the biggest concerns when working with financial datasets

Deep learning works best when you have lots of data and it's the same for finance

Hypothetical data can be used to develop better and more robust data driven strategies

Questions?

contact@qplum.co

ankit@qplum.co

Important Disclaimers: This presentation is the proprietary information of qplum Inc (“qplum”) and may not be disclosed or distributed to any other person without the prior consent of qplum. This information is presented for educational purposes only and does not constitute and offer to sell or a solicitation of an offer to buy any securities. The information does not constitute investment advice and does not constitute an investment management agreement or offering circular.

Certain information has been provided by third-party sources, and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind. Past performance is not a guarantee of future results. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.