Machine Learning Approach for

Systematic Global Macro Strategies

See important disclosures at the end of this presentation.

Ankit Awasthi

Quantitative Portfolio Manager

October 25, 2018

Outline of the talk

Global Tactical Asset Allocation

Why Asset Allocation

Macroeconomic Data

Why Deep Learning

Case Study

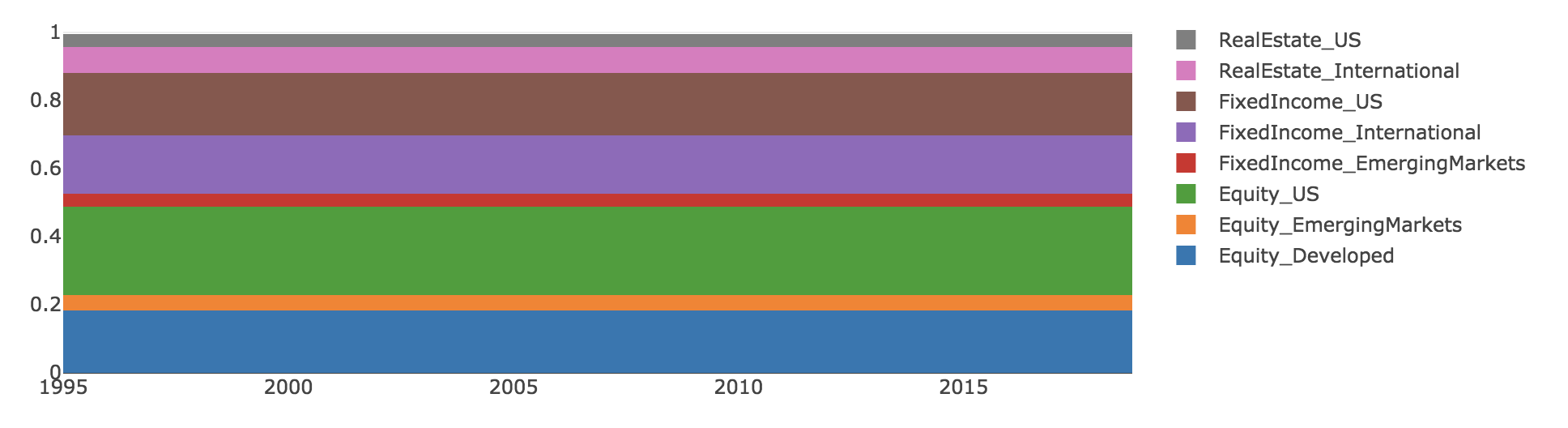

Global Strategic Asset Allocation

Based on Long Term Capital Market Assumptions

Incorporates Desired Risk and Return Profile

Asset allocation remains unchanged over time

Salient Features

Source: Qplum Research

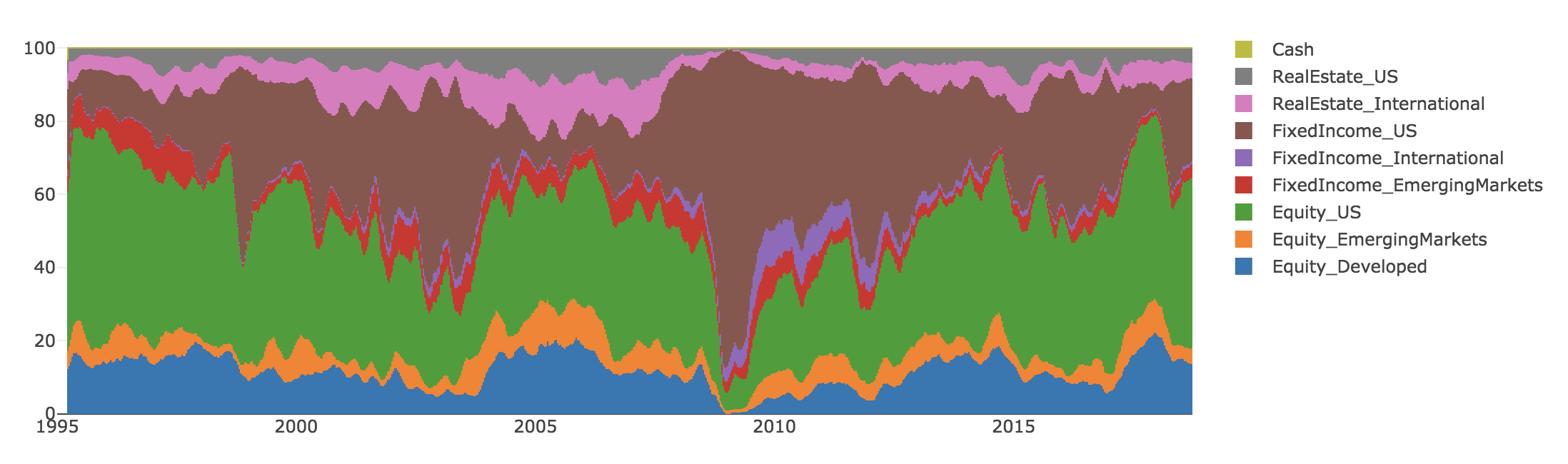

Global Tactical Asset Allocation

Salient Features

Based on Long Term and Short Term Capital Market Assumptions

Incorporates Desired Return and Risk Profile

Dynamic Asset Allocation

Average Asset Allocation over long periods is similar to strategic allocation

Source: Qplum Research

Why Asset Allocation ?

More than 90% of the variance in returns

can be attributed to

Asset Allocation vs Security Selection

Source : CFA Institute Blog

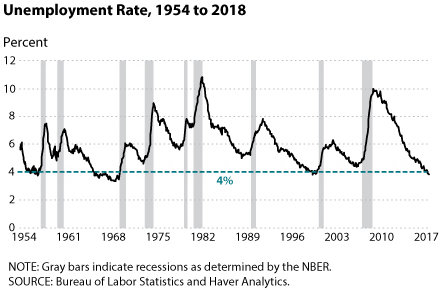

Macro Data for Business Cycle Detection

Source : Federal Reserve Bank of St. Louis

Troughs of Unemployment Rate turn out to be fairly robust predictors of recession.

Current unemployment rate is 3.7% which is the lowest since 1969.

Plot of Unemployment Rate OverTime

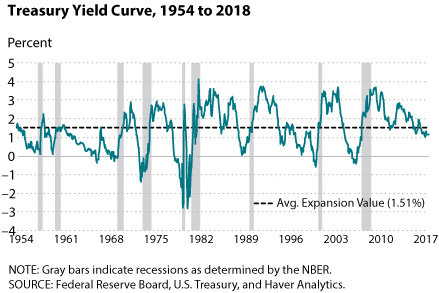

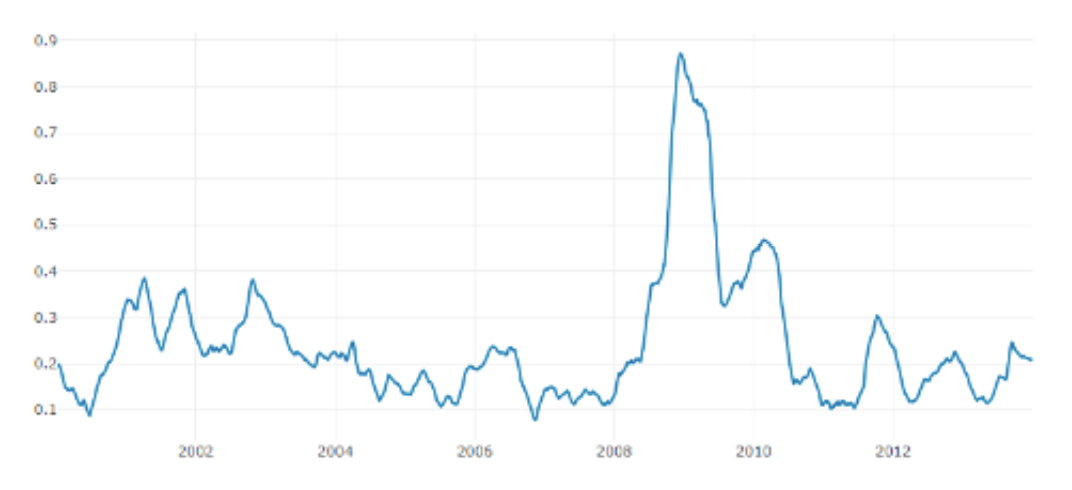

Macro Data for Business Cycle Detection

Source : Federal Reserve Bank of St. Louis

Yield Curve Inversion is another variable which has successfully predicted recessions.

Plot of difference of 10 year yields - 3 month yields over time

Why Deep Learning ?

Deep learning models excel at...

Capturing highly non-linear relationships

Combining disparate sources of information

Bayesian Deep Learning

Signal to Noise ratio is low in financial time series data

Point estimates of expected returns can have significant errors

Important to estimate model uncertainty along with expected returns

Dropout as a bayesian approximation

Source : Yarin Gal et. al. 2016

Case Study

The model or backtested portfolio and performance data provided in this presentation is theoretical and is not based on the performance of actual portfolios. It does not reflect trading in actual accounts; actual results may significantly differ from the theoretical returns being presented It is provided for informational purposes to illustrate use of deep learning only. Any interpretation of the results should take into consideration the limitations inherent in the results of the model. Backtested performance is developed with the benefit of hindsight, including the ability to adjust the method for selecting securities until returns for the past period are maximized, and has inherent limitations. Actual performance may differ significantly from backtested performance.

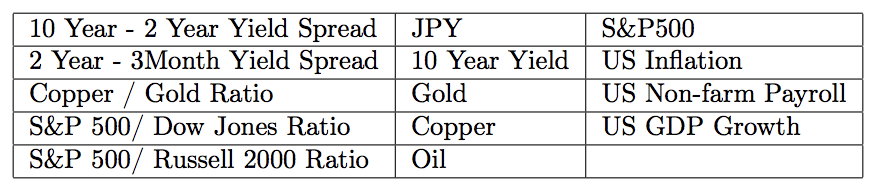

Macro-economic Indicators

Sample List of macro-economic indicators

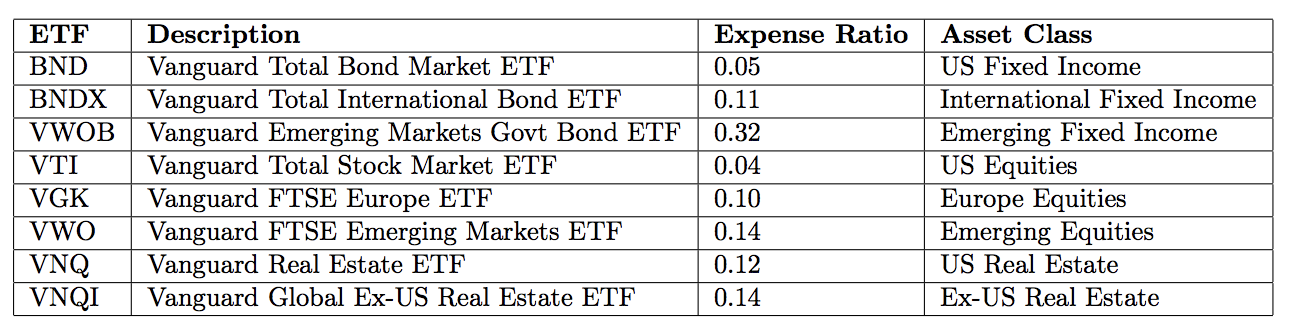

Traded Securities

Sample list of ETFs used as proxies for different asset classes

ETFs chosen such that the...

Expense ratio is low

Cover important asset classes

AUM is high

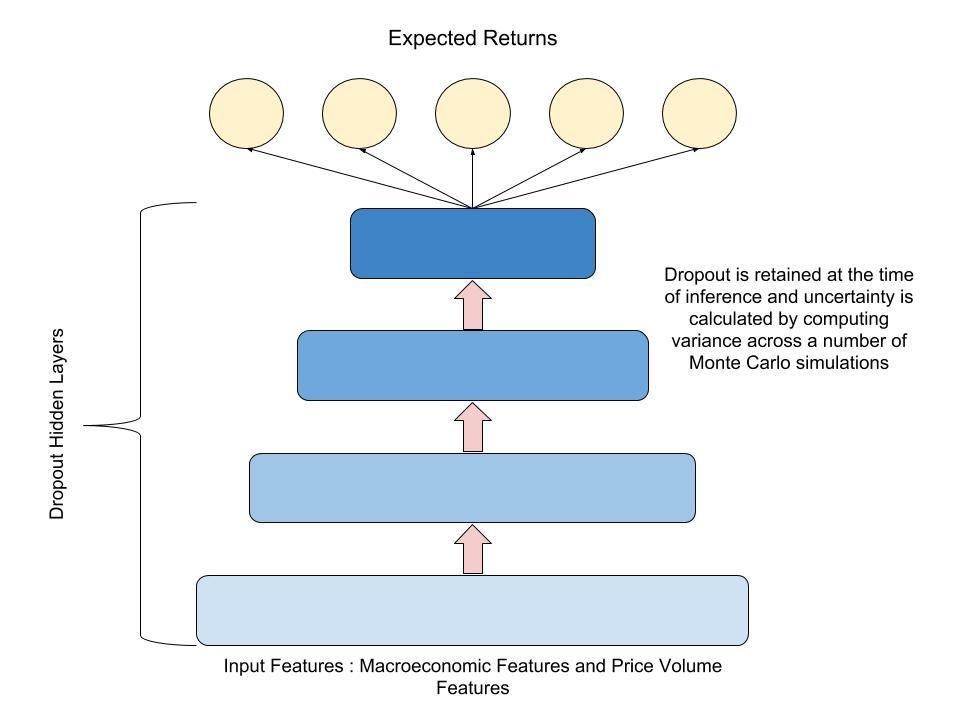

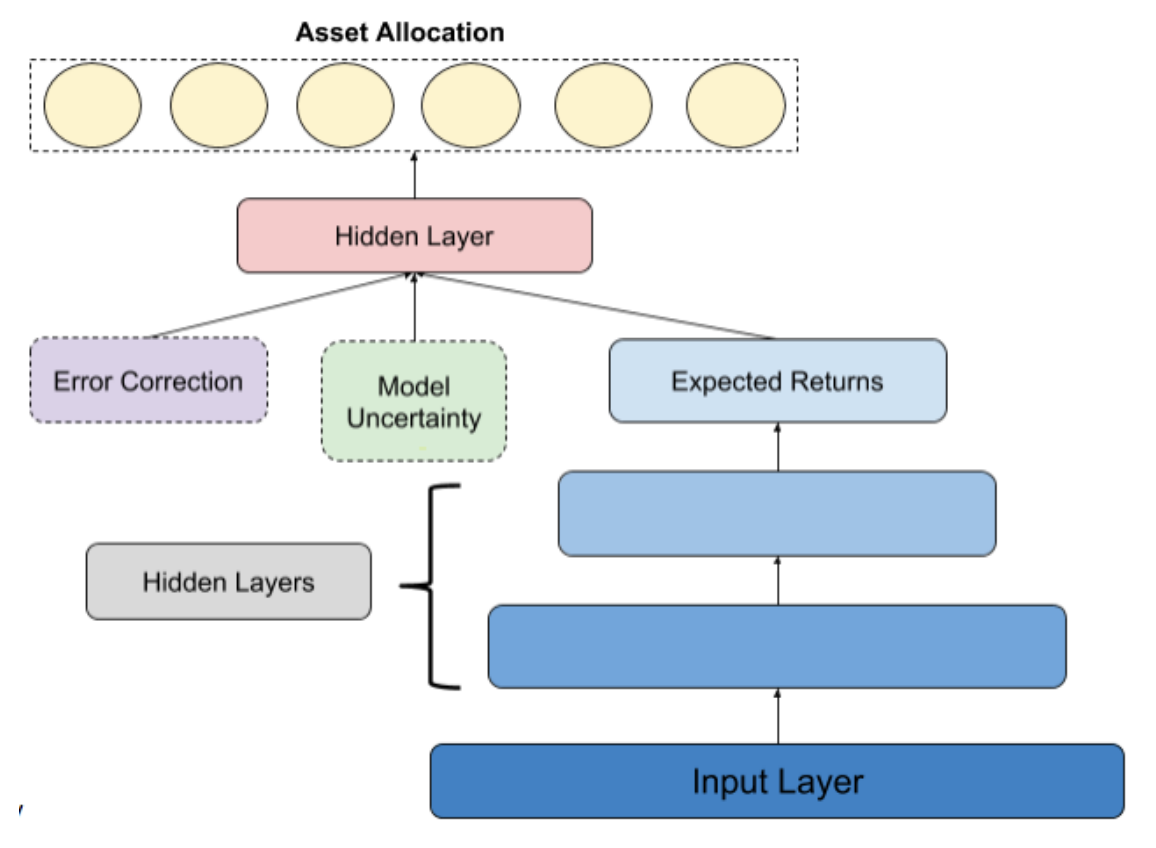

Expected Returns Model

Architecture for the feed-forward neural network for computed expected returns and expected model uncertainty

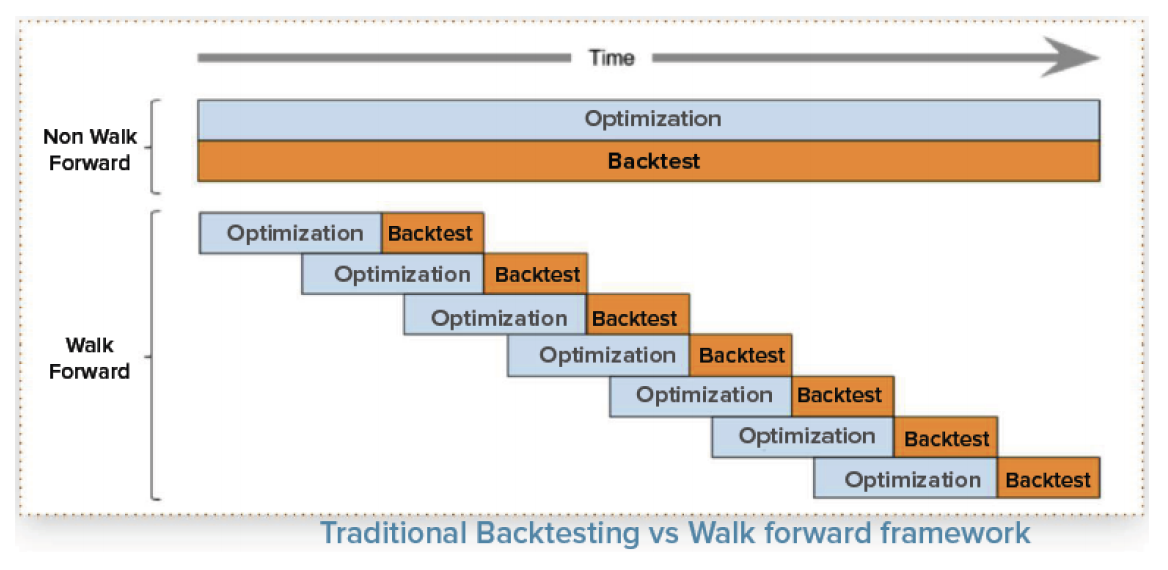

Walk-forward Training and Testing

Walk-forward Optimization helps in....

Better performance in out of sample data

Higher conviction in backtested results

Expected Returns Model

Mean exponentially weighted MAE (mean absolute error) across all assets (scaled between 0 and 1)

Source: Qplum Research

Model Uncertainty vs Volatility

Correlation between uncertainties obtained from the model using dropout approximation and uncertainty obtained using volatility in different asset classes.

Asset Class |

Security |

Correlation b/w Dropout Uncertainty and Volatility Uncertainty |

|---|---|---|

US Fixed Income |

BND |

0.08 |

International Fixed Income |

BNDX |

-0.16 |

Emerging Markets Fixed Income |

VWOB |

-0.17 |

US Equities |

VTI |

0.36 |

EU Equities |

VGK |

0.30 |

Emerging Markets Equities |

VWO |

0.15 |

US Real Estate |

VNQ |

0.50 |

International Real Estate |

VNQI |

0.54 |

Utility Function based Position Sizing

Architecture for position sizing based on the utility function. The basic idea is to learn the allocations directly based on the performance metric such as sharpe ratio. It uses the expected returns model, an error correcting feedback and the uncertainty of the expected returns model

Softmax

Utility Function

Sharpe Ratio ( net of all trading and slippage assumptions )

+

Entropy of allocations to different asset classes

Easy to extend to other objective functions capturing different investor preferences

CAGR |

Worst Drawdown |

Sharpe Ratio |

Sortino Ratio |

|

|---|---|---|---|---|

Run 1 |

8.4 |

23.8 |

0.95 |

1.30 |

Run 2 |

8.4 |

25.2 |

0.89 |

1.22 |

Run 3 |

8.8 |

27.0 |

0.99 |

1.35 |

Run 4 |

8.9 |

26.3 |

0.98 |

1.36 |

Run 5 |

7.2 |

29.9 |

0.79 |

1.07 |

Risk Parity |

8.9 |

27.8 |

0.87 |

1.20 |

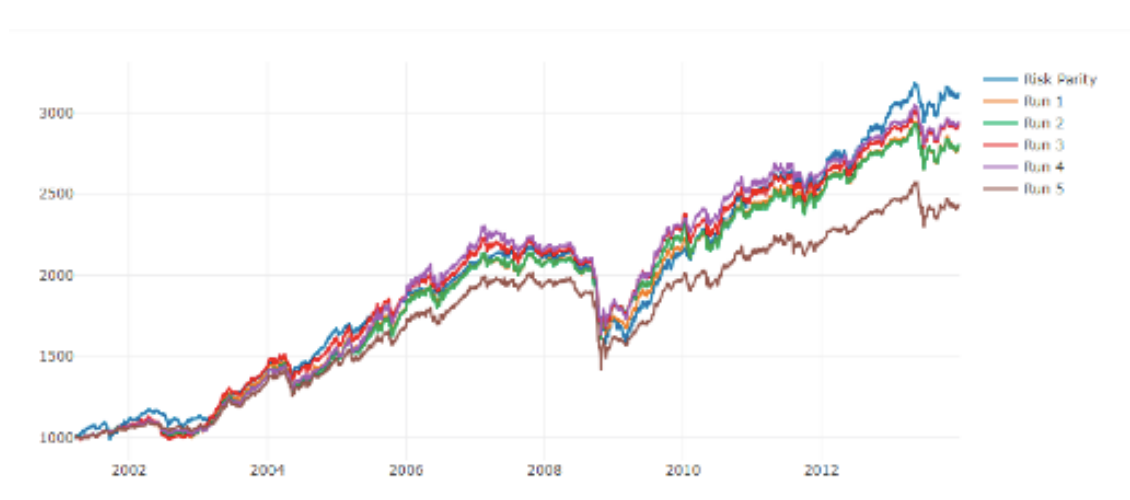

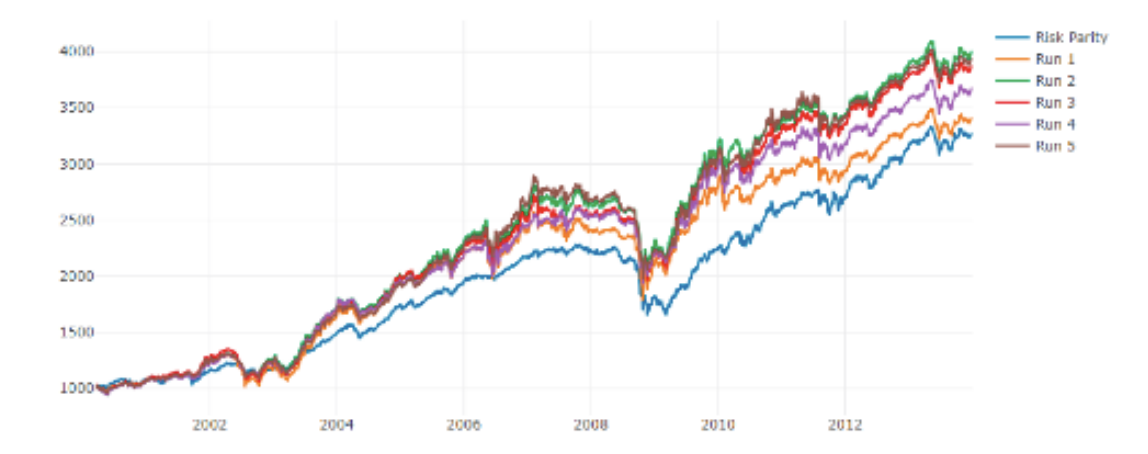

Backtested cumulative returns of the strategy across different runs against risk parity in the observation period. The variation in performance comes from different initializations of the neural network

Performance statistics for different runs and risk parity

Cumulative Performance

Uncertainty estimate based on realized volatility

Source: Qplum Research

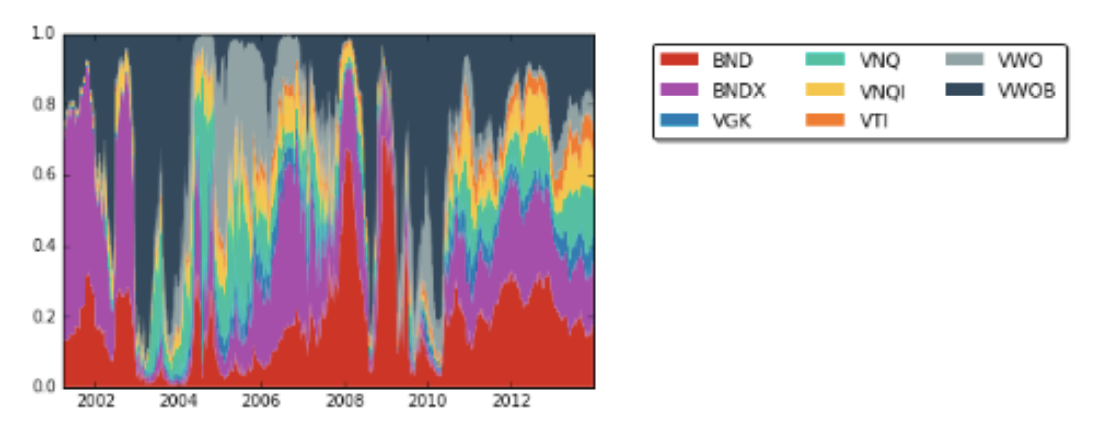

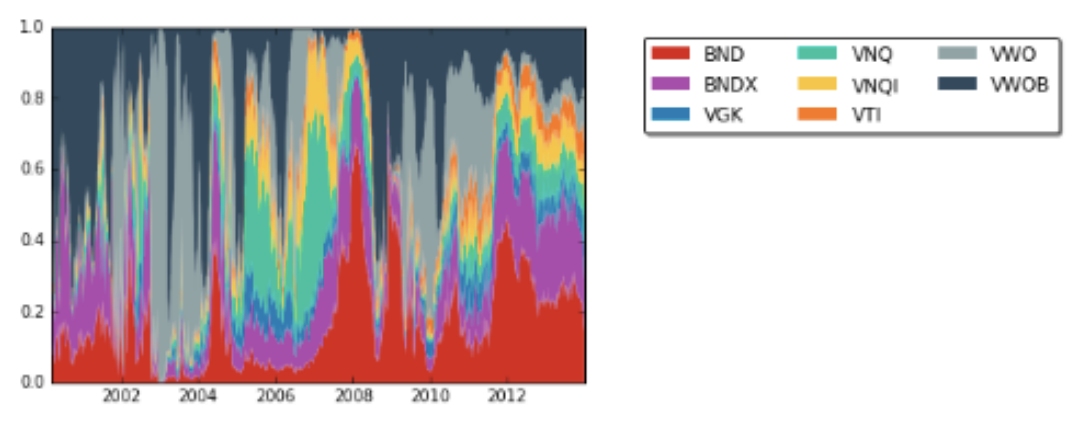

Asset Allocation

Asset allocation over time for utility based position sizing logic over time

Uncertainty estimate based on realized volatility

Source: Qplum Research

CAGR |

Worst Drawdown |

Sharpe Ratio |

Sortino Ratio |

|

|---|---|---|---|---|

Run 1 |

9.3 |

30.7 |

0.74 |

1.03 |

Run 2 |

10.6 |

29.9 |

0.87 |

1.23 |

Run 3 |

10.3 |

28.9 |

0.84 |

1.19 |

Run 4 |

9.9 |

26.3 |

0.84 |

1.18 |

Run 5 |

10.5 |

32.0 |

0.87 |

1.22 |

Risk Parity |

8.9 |

27.8 |

0.87 |

1.20 |

Backtested cumulative returns of the strategy across different runs against risk parity in the observation period. The variation in performance comes from different initializations of the neural network

Performance statistics for different runs and risk parity

Cumulative Performance

Uncertainty estimate based on model uncertainty

Source: Qplum Research

Asset Allocation

Asset allocation over time for utility based position sizing logic over time

Uncertainty estimate based on model uncertainty

Source: Qplum Research

Strategy |

CAGR |

Worst Drawdown |

Sharpe Ratio |

Sortino Ratio |

|---|---|---|---|---|

Utility Function (MC) |

4.3 |

17.2 |

0.44 |

0.58 |

Utility Function (Vol) |

5.2 |

12.9 |

0.62 |

0.82 |

Expected Returns |

2.0 |

8.3 |

0.37 |

0.50 |

Risk Parity |

4.6 |

9.3 |

0.76 |

1.03 |

Performance of different formulations against risk parity in out of sample period

Performance stats of different formulations against risk parity in out of sample period

Cumulative Performance

Source: Qplum Research

Future Improvements

Increase the coverage of macro-economic variables

Better estimates of model uncertainty

Use hypothetical data to learn price-volume features

Explore other neural network architectures

Key Takeaways

Systematic walk-forward training of deep neural networks for financial time series data

Bayesian deep learning could be helpful in applications where signal to noise ratio is low such as capital markets

Utility function as an objective function for training to directly determine allocation

Deep neural networks are a flexible and powerful framework to do tactical asset allocation

Questions?

contact@qplum.co

ankit@qplum.co

Important Disclaimers: This presentation is the proprietary information of qplum Inc (“qplum”) and may not be disclosed or distributed to any other person without the prior consent of qplum. This information is presented for educational purposes only and does not constitute and offer to sell or a solicitation of an offer to buy any securities. The information does not constitute investment advice and does not constitute an investment management agreement or offering circular.

Certain information has been provided by third-party sources, and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. The information is furnished as of the date shown. No representation is made with respect to its completeness or timeliness. The information is not intended to be, nor shall it be construed as, investment advice or a recommendation of any kind. Past performance is not a guarantee of future results. Important information relating to qplum and its registration with the Securities and Exchange Commission (SEC), and the National Futures Association (NFA) is available here and here.