A.I. from the Chief Investment Office to the trading desk

Disclosures: qplum LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.Gaurav Chakravorty

Chief Investment Officer at QPLUM

... continued from STAC New York keynote

where we covered

- business reasons why DL is growing now

- what sort of trades one can do with it

- how high frequency trading and DL complement each other.

- A.I. is about reducing costs and increasing transparency, not about more alpha.

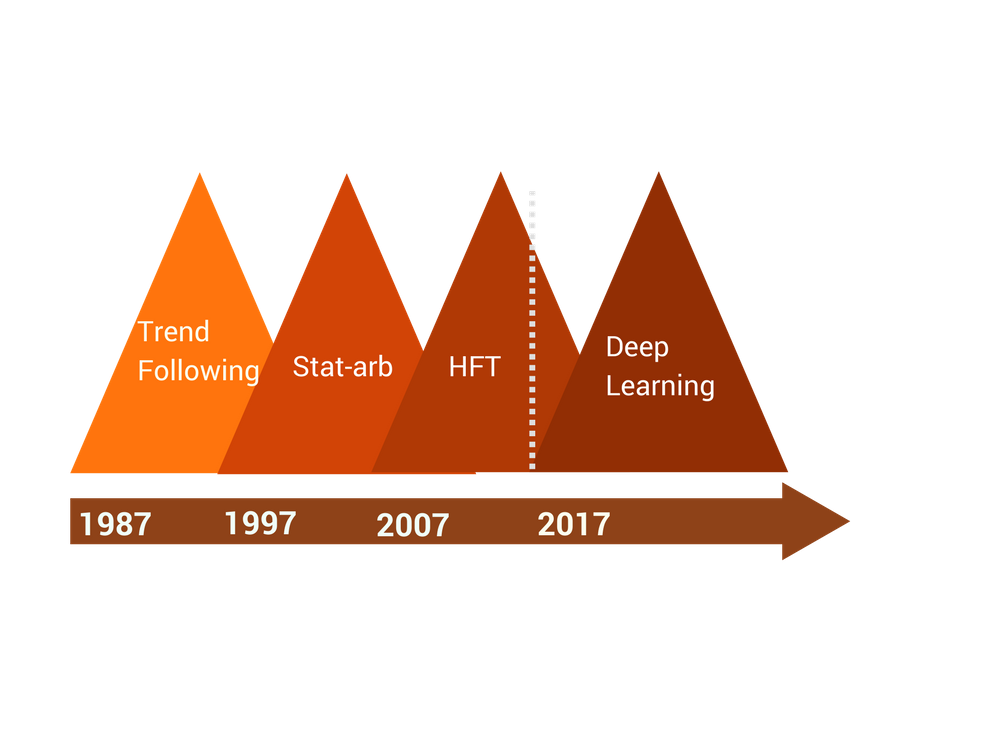

A.I. has moved out of the fringes

Real money investors are pursuing innovative investment methods

Due to innovation in "real money" investors, prop trading is dying. H.F.T is consolidating and is barely breakeven.

Institutional allocations to old-school "pedestrian" quant strategies are not yielding alpha post fees.

Jobs are telling the same story. No one wants traders any more.

What will we cover today

-

How the Chief Investment Office can use A.I. in their workflow. - Using a recommender system approach to decide strategy allocation.

(reference paper on this)

-

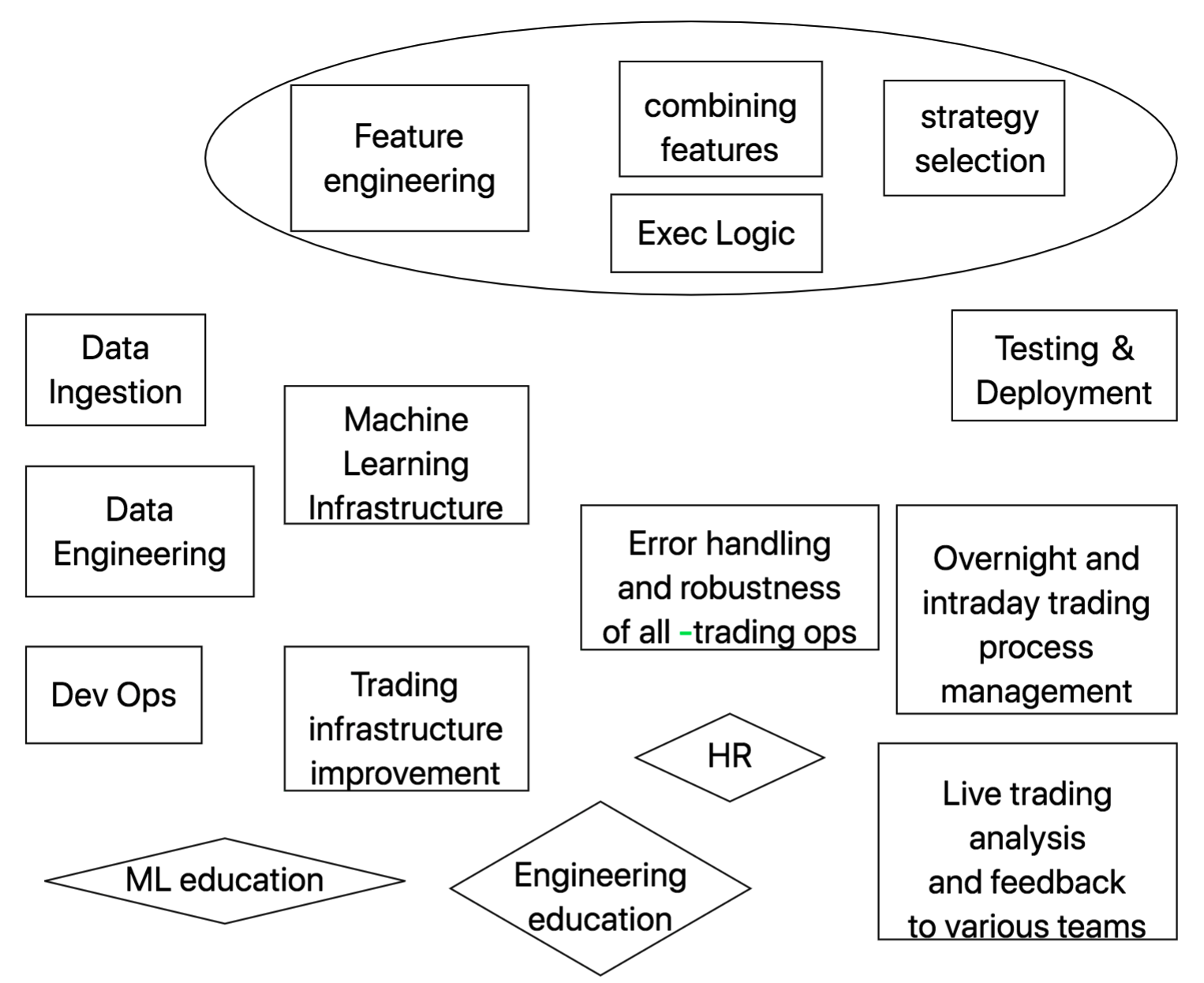

What do we need to build to implement A.I. in our organization

(teams, workflows, architecture).

Narv Narvekar

HMC

David Swensen

Yale

Warren Buffett

Berkshire

Ken Griffin

Citadel

Images may be subject to copyright

What's common to all of their work?

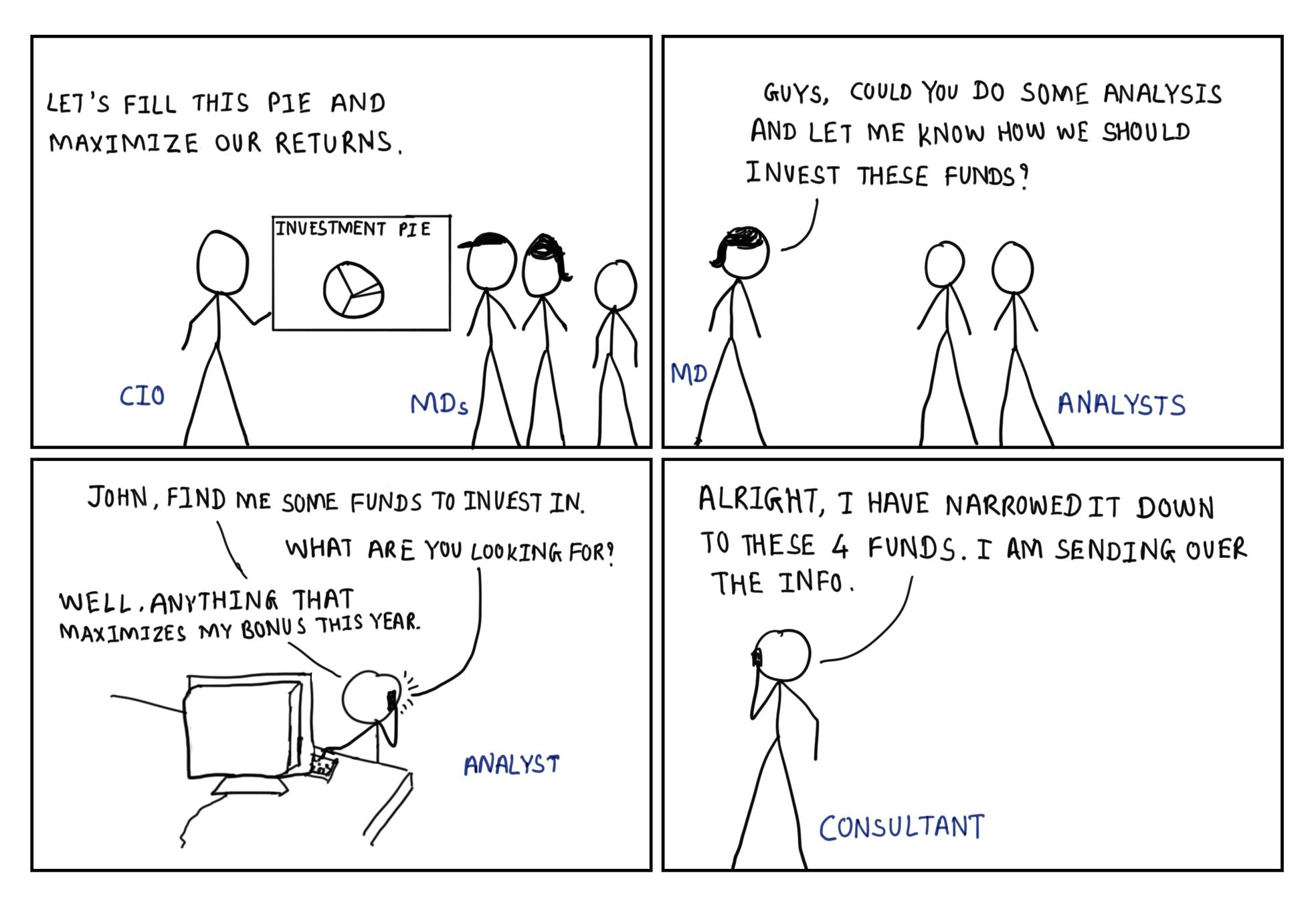

Workflow of institutional investing today

Current workflow at Chief Investment Offices is about making a pie chart and figuring out how to fill it.

Pain points of institutional investors

The need for

-

Lower fees

-

Greater transparency

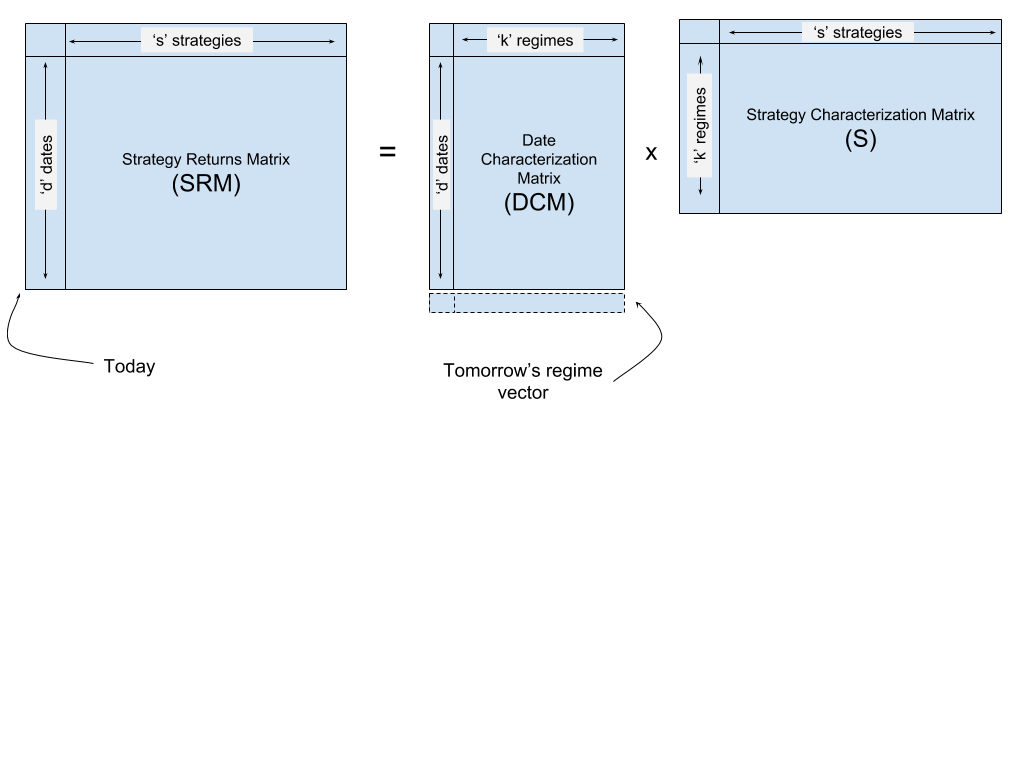

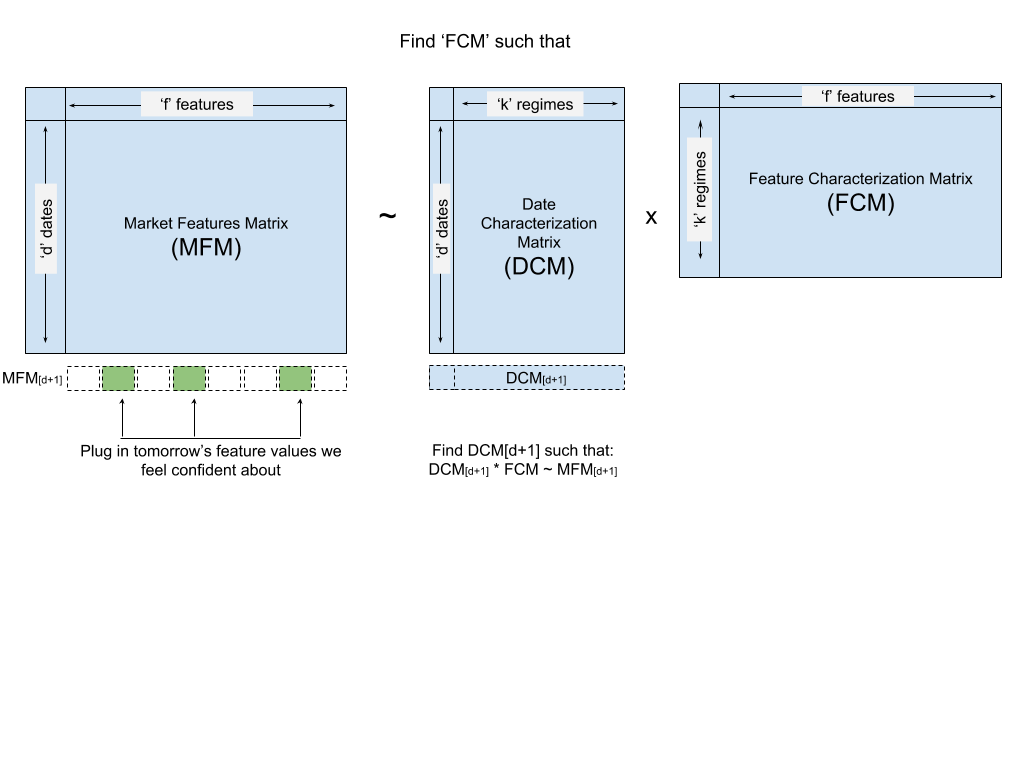

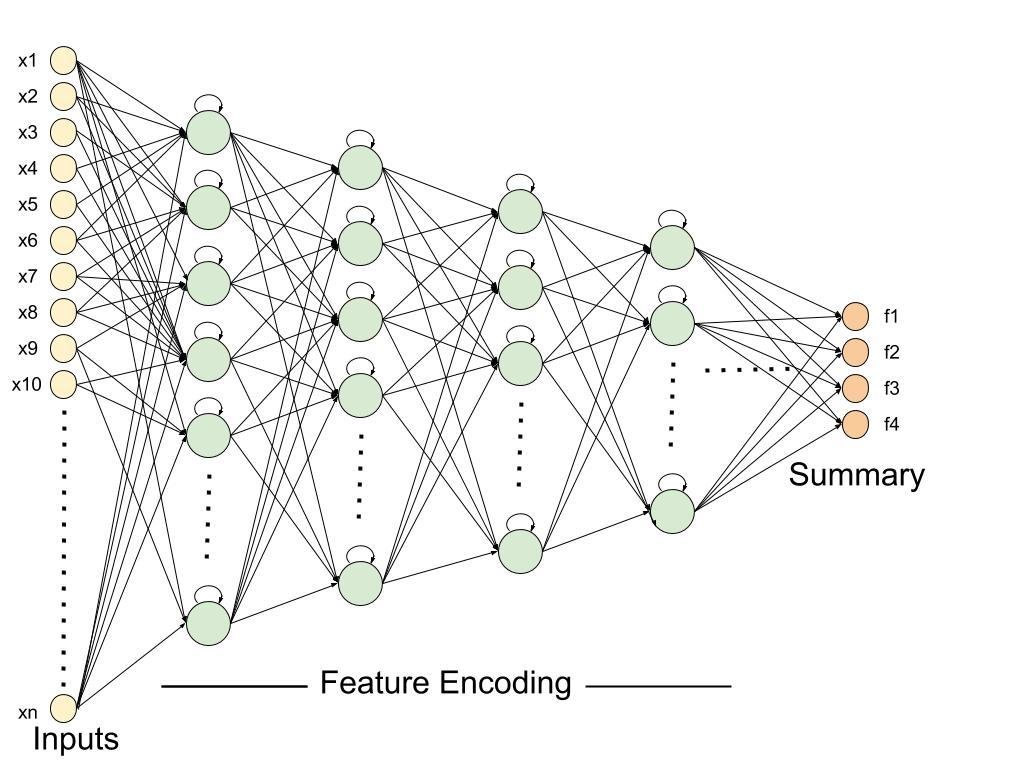

A Machine Learning approach to strategy allocation

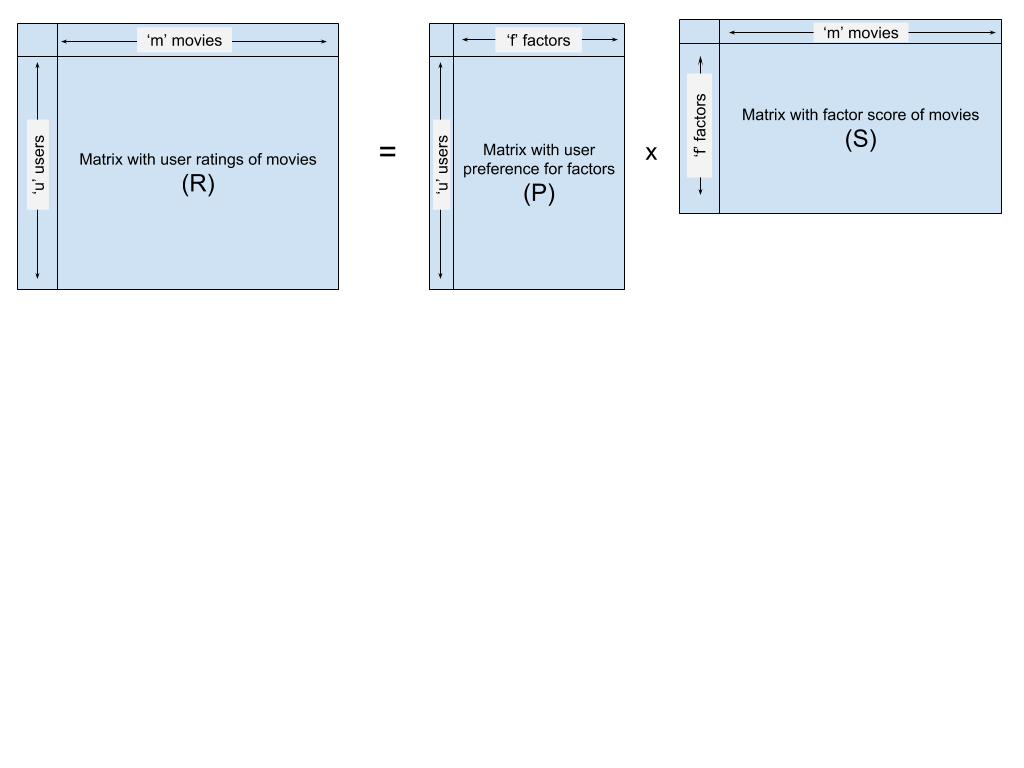

It turns out that allocating to investment strategies is very similar to recommender systems

Problem: Given a set of strategies one could allocate to, how much to allocate to each

- Figure out what is similar between the strategies.

- Figure out similarities between the days or periods you are using to backtest them.

- Figure out the easiest prediction problem you can solve that will get your job done.

- Make a walk-forward model!

Use a matrix factorization approach to learn which strategies are similar and which dates are similar

This is very similar to the movie recommendation problem

Visualization of matrix factorization based collaborative filtering

We can extend the matrix factorization approach to include predictable market features like volatility and GDP growth

The secret sauce?

Unsupervised learning

"Unsupervised learning had a catalytic effect in reviving interest in deep learning, but has since been overshadowed by the successes of purely supervised learning. Although we have not focused on it in this Review, we expect unsupervised learning to become far more important in the longer term." - Geoffrey Hinton et. al., Nature, Deep Learning

- Investment strategies that learn by themselves (article)

How to implement A.I. within an investment company

An asset management company needs to look like a tech company now

Questions?

gchak@qplum.co

Disclosures: qplum LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are never guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Appendix

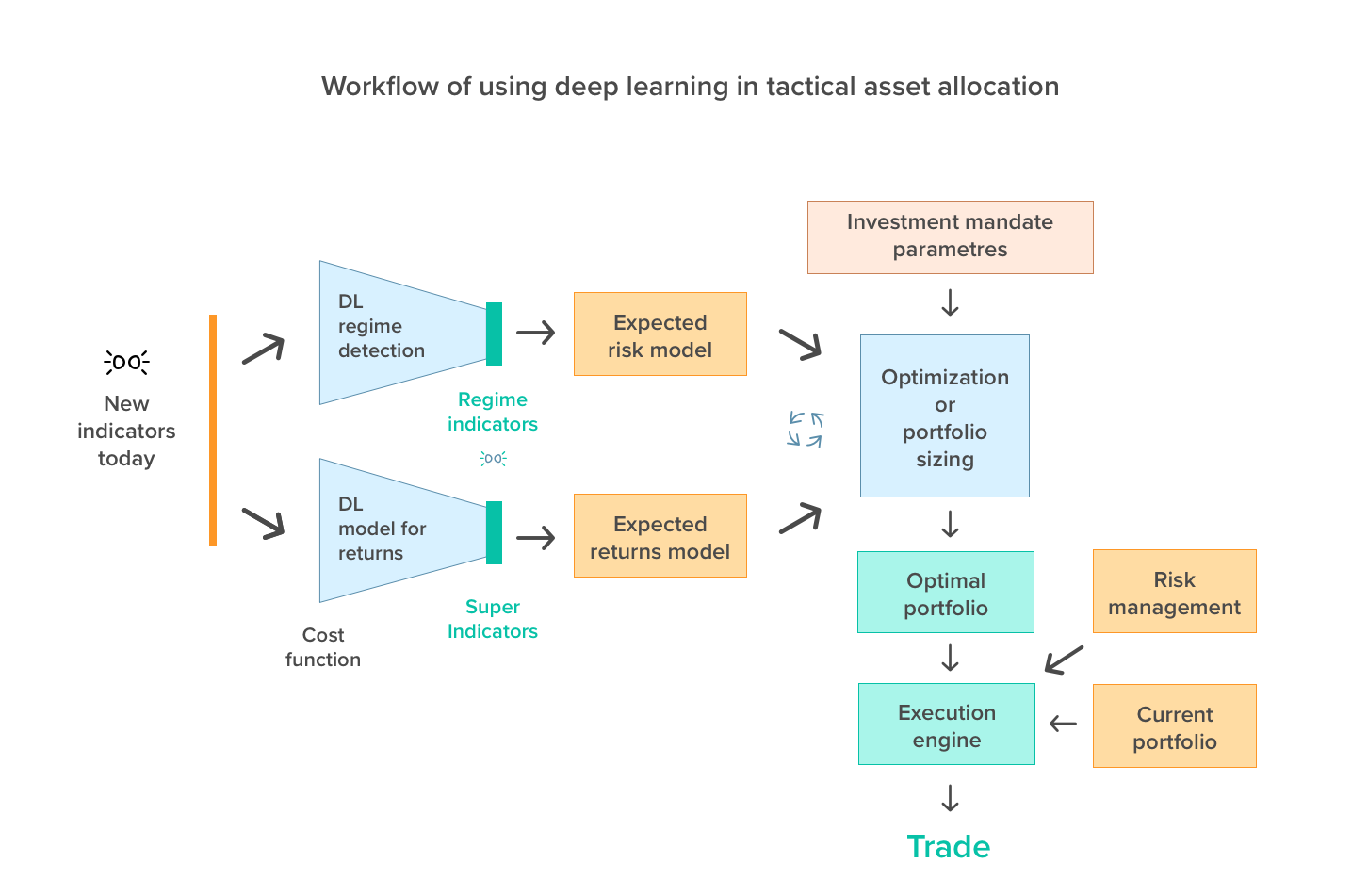

Workflow

Using unsupervised learning in the cost function

Using unsupervised learning in the cost function

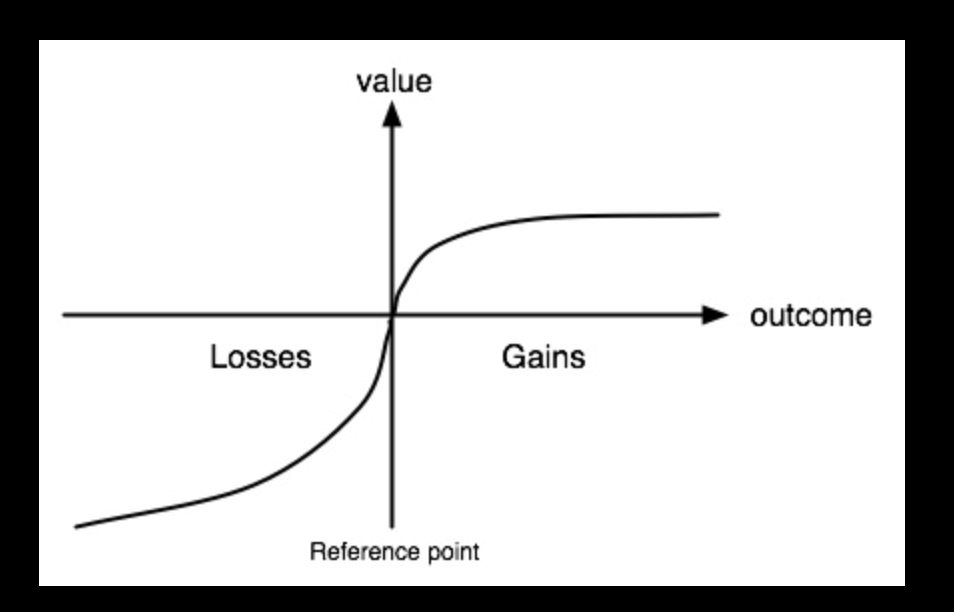

Other pain points of institutional investors

I. Aversion to losing

It is not always just about higher returns.

Utility function is not uniformly distributed.

Utility function is not the same.

II. Anchoring around a sustainability rate

Most pension funds have a nominal target yield.

Not meeting the target yield is a big deal compared to outperformance

III. Capacity:

Investments that have scale and capacity to get in and to get out

IV. Should work with illiquid assets:

Illiquid investments are a part of everyone's portfolio.

One cannot look at liquid investments without considering the illiquid assets that are a part of the portfolio already.

Asset Allocation >> Security Selection

“By choosing to place asset allocation at the center of the investment process, investors ground the decision-making framework on the stable foundation of long-term policy actions.

Focus on asset allocation relegates market timing and security selection decisions to the background, reducing the degree to which investment results depend on mercurial, unreliable factors.

Selecting the asset classes for a portfolio constitutes a critically important set of decisions, contributing in large measure to a portfolio’s success or failure. Identifying appropriate asset classes requires focus on functional characteristics, considering potential to deliver returns and to mitigate portfolio risk. Commitment to an equity bias enhances returns, while pursuit of diversification reduces risks. Thoughtful, deliberate focus on asset allocation dominates the agenda of long-term investors.”

– David Swensen

Goals of asset allocation:

(a) Target constant risk in the portfolio.

(b) Optimize portfolio for the specified utility function.

(c) Constrain any studies to a specified, systematic risk management threshold.

Investing with a trustworthy tool

"security analysis may begin--modestly, but hopefully--to refer to itself as a scientific discipline "

Imagining investing with "trustworthy tool" and not experts.

- Benjamin Graham