The monetary policy transmission

mechanism in China

BB30414

Cao Ying

Author‘s Background

Yi Gang

- Former Director of the State Administration of Foreign Exchange.

- Deputy Governor of the People's Bank of China.

- He has published more than 40 articles in Chinese and 20 academic papers in English.

-

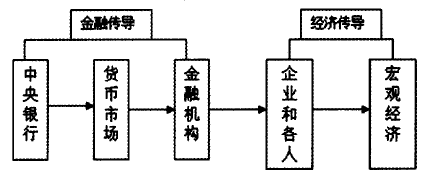

Evolution of monetary policy transmission mechanism

-

Monetary policy transmission relies mainly on an indirect management mechanism

-

A further improvement of the monetary policy transmission mechanism

EVOLUTION OF MONETARY POLICY TRANSMISSION MECHANISM

Time Period:

- 1984-1990 :direct credit controls were used in the conduct of monetary policy

- After 1990 :monetary policy operations moved from direct credit control to indirect measures.

EVOLUTION OF MONETARY POLICY TRANSMISSION MECHANISM

- 1984-1990 :direct credit controls were used in the conduct of monetary policy

The People’s Bank of China (PBC) began functioning as the central bank in 1984. At the time, direct credit controls were used in the conduct of monetary policy.

EVOLUTION OF MONETARY POLICY TRANSMISSION MECHANISM

- After 1990 :monetary policy operations moved from direct credit control to indirect measures.

It came with the abolition of credit ceilings and the expansion of open market operations.

And the intermediate and operational targets also switched to money supply and base money, with the adoption of a combination of monetary policy

instruments.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

Recent years have seen the transformation from direct control through direct control through administrative measures to indirect controls through economic measures, while greater priority has been given to building a mechanism for macro-management.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

- First, monetary policy instruments have been further improved.

The open market operations is the major instrument.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

2. Second, interest rate system reform has been pushed forward, with the role of interest rates strengthened.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

3. Third, the flexibility of the RMB exchange rate has increased as market supply and demand have played a bigger role in the formation of the RMB exchange rate.

On July 21, 2005, China adopted a managed floating exchange rate regime based on market supply and demand, putting an end to a basically fixed RMB exchange rate.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

4. Fourth, financial markets have developed stably and the monetary policy transmission mechanism has further improved.

The development of financial markets not only directly impacts the transmission of monetary policy but also to a large extent determines the transition toward indirect approaches.

MONETARY POLICY TRANSMISSION RELIES MAINLY ON AN INDIRECT MANAGEMENT MECHANISM

5. Fifth, there has been a breakthrough in financial institution reforms, resulting in heightened incentives for profit maximization and sensitivity to the indirect approach of monetary policy.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

- Some problems still remain in the monetary policy transmission mechanism.

- First, the independence of monetary policy in macroeconomic management has been constrained to some extent.

- Second, it is more difficult for monetary policy to be conducted with money supply as the intermediate target.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

- In order to solve the existing problems, in addition to domestic economic structural adjustment, we need to promote a shift from quantitative instruments to price instruments.

- And continue to push ahead steadily with market-based interest rate reform, so as to enable price instruments to play a sufficient role in monetary policy transmission.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

1. First, improving the RMB exchange rate formation regime.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

2. Second, steadily advancing market-based interest rate reform.

The recent development of Shibor (Shanghai interbank offer rate) is an encouraging sign for interest rate liberalisation.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

3. Third, pushing forward the reform of state-owned commercial banks and rural credit cooperatives.

A FURTHER IMPROVEMENT OF THE MONETARY POLICY TRANSMISSION MECHANISM

4. Fourth, promoting further financial market development.

Thank you!

Reference

http://www.bis.org/publ/bppdf/bispap35h.pdf

(<The monetary policy transmission mechanism in China> Yi Gang)

http://www.cnfinance.cn/magzi/2010-04/02-8694.html

(《中国货币政策传导机制的现状、问题与改革》 王煜)