Financial Globalisation

in

SINGAPORE

Fengyi CHAI Jianing HUANG Jiaqi WANG

Lei QIAN Sifat ISHTY

Siqi LONG Yan REN Yinjun QIU

Yining XU Yiqun ZHANG

DEFINITIONS

Financial Globalisation

Financial Liberalisation

Capital Account

Convertibility & Liberalisation

SINGAPORE'S

Economic Development

(1965-2008)

1965

Singapore was independent from Malaysia,

lacking of natural resources.

LATE 1960s

International financial centre:

outward-oriented growth and FDI

1973

MAS liberalised foreign exchange controls

1981

Adopted the exchange rate as the monetary instrument

1998

Relax its non-internationalisation policy

AFTER 1998

Banks change to risk-based management system

2008

Experience the financial crisis and MAS

re-centre the exchange rate policy band

A Glimpse of SINGAPORE’S Path to Liberalisation

From the late 1960s Singapore decided to become an international financial sector and underpinned the start of liberalisation of its capital account and financial sector.

Monetary Authority of SINGAPORE (MAS) in the 1970s began to progressively liberalise foreign exchange controls with the floating of the Singapore dollar (S$), followed by:

- (1973) Allowing Singapore residents and companies to invest in foreign currency deposits and equities

- (1975) Fixed interest rate was abolished

- (1978) All foreign exchange control regulations were lifted and Singapore residents and companies were allowed to borrow and lend in all currencies

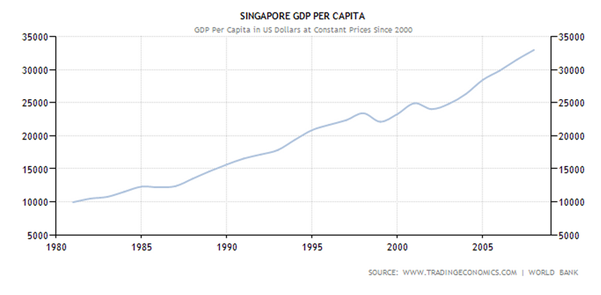

SINGAPORE’S initial phase of growth was highly dependent on FDIs

- FDIs constituted 80% of total investment in the manufacturing sector (Tan, 2000)

- Singapore’s economy started to move from labour-intensive production to more capital-intensive manufacturing industries like petroleum refining and later to higher-value-added production like electronics and chemicals

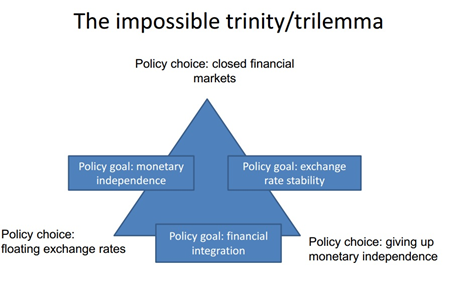

SINGAPORE'S Impossible Trinity Problem

Singapore has prioritised exchange rate stability and financial integration as a basis of economic structure and policy tool.

WHY?

Free capital mobility: Encourage more FDIs, which in-turn boosts demand and consumption and Singapore’s Comparative Advantage in the knowledge-skills sector

Exchange rate stability: Very Important for competitiveness (as it will allow to maintain a low cost of production from imports of cheaper resources with a stronger currency). Furthermore, gross exports and imports were over two times Singapore’s GDP, hence economic growth and inflation rate were highly dependent on the external sector, so a credible foreign exchange policy was pivotal to its economic health

So MAS cedes control over domestic interest rates and money supply and moved to an exchange rate centred monetary policy.

*Khor et al (2007) showed that a 1% appreciation in the exchange rate has a greater adverse effect on GDP, exports and inflation as compared to a 1% increase in interest rates)

Exchange Rate Policy

Basket, Band and Crawl (BBC) exchange regime

allows the country to manage short-term currency fluctuation and volatility as well as to adjust long-term misalignment to its macroeconomics fundamentals (MAS, 2001 ; Khor et al., 2007)

Mechanism

- S$ is managed against a basket currencies of its trading partners and competitors on a weighted basis.

- The trade-weighted exchange rate can be fluctuated within a policy band.

- The band provides a room to absorb short-term fluctuation and is reviewed periodically to ensure that it is consistent with the economic fundamentals.

Long Term Exchange Rate Policy

Singapore allows the S$ to appreciate in order to maintain price stability by dampening external demand and wage pressure through incremental increases in purchasing power of the S$, as well as to provide impetus for exporters to move up the value chain and remain competitive.

Counter-cyclical Exchange Rate Policy

MAS adopts a “ lean against the wind policy”. MAS intervened to moderate the nominal effective exchange rate appreciation, while in contrast, during the Asian crisis, it intervened to support the currency to prevent the exchange rate from falling below the policy band.

Empirical Evidences

Text

Non-internalisation of S$ to Full Liberalisation of S$ Credit Facilities

(1983)SINGAPORE discouraged internalisation of S$:

As it feared that a large offshore market in the S$ could destabilise the capital flows and cause greater exchange rate and interest rate instability.

Regulation:

Banks were required to consult with MAS before providing S$ credit facilities greater than $5 million to non-residents, or to residents where the proceeds of the loan were to be used outside Singapore.

Drawback of Non-internalisation:

- Non-internalisation of S$ was discouraging the development of the domestic bond market.

- Asian crisis (1997/98) exposed the danger of being over dependent on the banking sector for credit and growth

Hence, the government wanted to deepen and broaden Singapore’s capital markets and so it relaxed non-internalisation of S$ and moved on to greater financial and capital account liberalisation.

Mechanism of this full liberalisation policy:

Full liberalisation of the S$ credit facilities to residents and relaxing the credit facilities of S$ to non-residents for equity listing and issuance of S$ bonds. It also allowed a restrictive use of derivatives for hedging interest rate and currency risk.

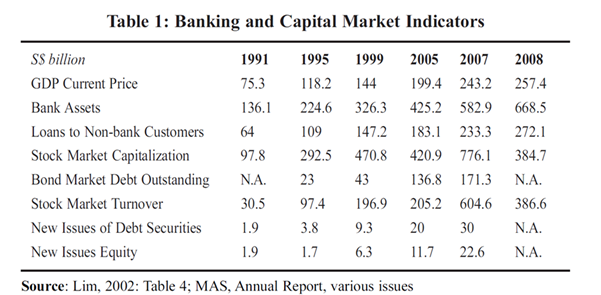

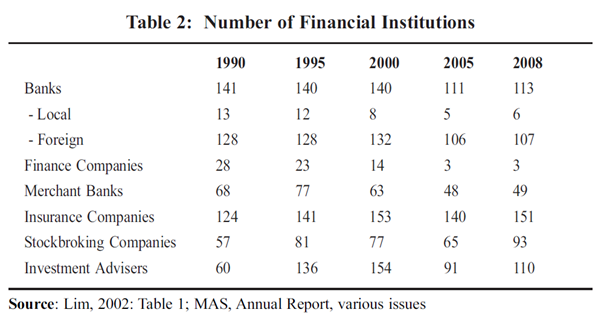

Measures in the liberalisation of the financial sector can be grouped into three categories (Lim, 2002):

- MAS moved away from regulation to supervision

- Remove the protection accorded to domestic financial institutions in order to foster competition and financial innovation

- Developed the capital markets to complement the banking loans market

An Overview of The Transition

Empirical evidences of this liberalisation can be noticed on the following slide

Empirical Evidences

Financial Crisis

&

Its Impacts

Banking Sector

Balance of Payments

Real Economy

Impact on Banking Sector

TOXIC ASSETS

Toxic structured notes sold by Singapore’s financial institutions

Text

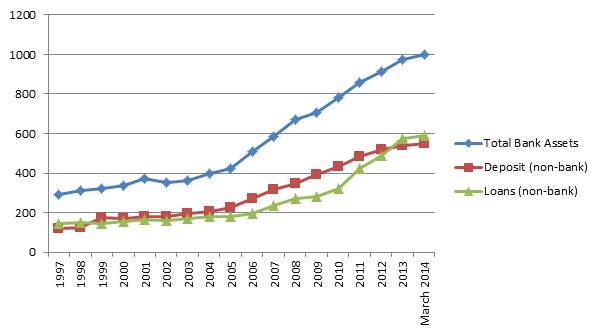

Source: MAS, Annual Report, 2013/2014

Minimal impact for a total assets of $581 billion and a capital base of $39 billion

Selected Financial Indicators, 1997-2014

Impact on Balance of Payments

Overall Balance:

Positive & Reserved Rising

- Net Direct Investment: positive and rose during crisis, foreign direct investments are more long-term-oriented

- Portfolio Investment: negative, net outflow

- Other Investments: volatile

Text

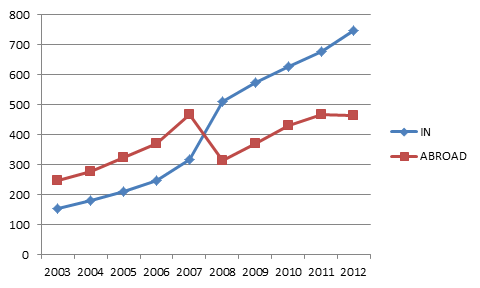

Source: Singapore Department of Statistics official website, www.singsta.gov.sg

FDI in SINGAPORE & SINGAPORE'S Direct Investment Abroad, 2003-2012

Impact on Real Economy

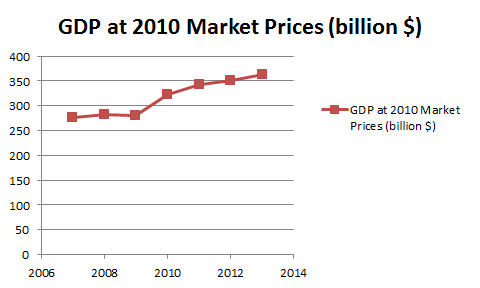

- Industrial Production Index (IPI) for the whole manufacturing sector dropped 28%

- Business confidence dimmed and investments declined

- Real GDP growth fell from 6.7% in Q1 2008 to (-10.2)% in Q1 2009

- Net exports growth fell sharply

Text

Source: MAS, Annual Report 2013/2014; Singapore Department of Statistics, Yearbook of Statistics, 2014

Policies Responses

Monetary Policy

Fiscal Policy

Monetary Policy

- April 2009: MAS decided to re-centre the S$ exchange rate band and continued with its four-year policy of gradual appreciation of the S$

Fiscal Policy

- A Stimulus package amounting to $20.5 billion: the Resilience Package

- Four Goals

(a) saving jobs

(b) enhancing competitiveness of firms and workers

(c) income relief for the lower classes

(d) strengthening physical and social infrastructure

CONCLUSIONS

- It can be concluded that instead of a big-bang approach to financial and capital account liberalization,Singapore implemented the process gradually.

-not necessarily in rigid sequential stages

-but in a pragmatic manner

- Singapore's economic growth is essentially determined by external factors-rising in times of global boom & dropping in times of world recession.

-However, having built up persistent current account surpluses and huge foreign & fiscal reserves, it is able to weather the economic & financial storms better.

REFERENCES

- Michael Lim Mah-Hui and Jaya Maru 2010 Financial Liberalization and the Impact of the Financial Crisis on Singapore

- Lim, Guan Hua, 2002. “Against the Tide? Liberalization of the Singapore Financial Sector, 1997-2000.”

- Khor, Hoe Ee, Jason Lee, Edward Robinson and Saktiandi Supaat, 2007. “Managed Float Exchange Rate System: The Singapore Experience.”

- Ngiam, Kee Jin, 2000. “Coping with the Asian Financial Crisis: The Singapore Experience.”

- Monetary authority of Singapore “Official Singapore Annual Report”

- Indicators are from http://www.tradingeconomics.com