Indicator of Economic Uncertainty for Brazil

Motivation

- In view of the negative consequences uncertainty shocks have for the economic activity of a country, an in-depth study of this subject in the context of Brazil seemed relevant.

- Therefore, the Economic Uncertainty Indicator for Brazil (IIE-Br) was developed following the best current academic practices. It seeks to measure the level of economic uncertainty in Brazil over time.

Methodology

The indicator is mainly built using web-scraping techniques in which news are extracted from online information sources, such as newspapers, and the extracted text is analyzed to produce measures related to uncertainty movements. It also combines information on stock market volatility and expectations.

IIE-BR = 0.7 x Media + 0.2 x Expectation + 0.1 x Stock Market Volatility

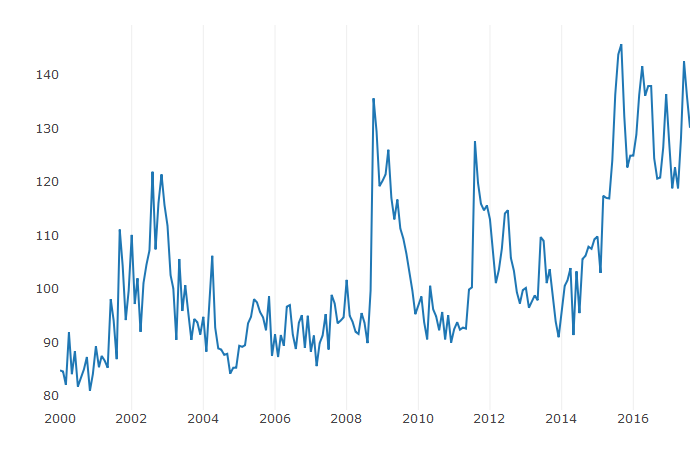

IIE-BR

Oct/02

Presidential Election

Oct/08

Collapse of Lehman Brothers

Aug/11

US credit-rating downgrade

Aug/15

BR credit-rating downgrade

General Idea

Use the same methodology applied on the development of the Indicator to generate an Indicator via Facebook Data.

Test the hypothesis that the Indicador generated by FB is comparable to the one developed by FGV.

Verify whether social media react to uncertainty or predict it.

Methodology

- The same two groups of terms would be used here: one related to ”economy”, and another related to uncertainty, which consisted of the terms ”uncertainty”, ”instability” and ”crisis”.

- In order to ensure that words related to the selected terms would also be included in the search (e.g., ”uncertain” as well as ”uncertainty”), a type of lemmatization would be performed, in which words would be reduced to their roots: ”ECON” for economy and ”INSTAB”, ”UNCERT” and ”CRISIS” for the uncertainty terms.

Nicholas Bloom, 2009. "The Impact of Uncertainty Shocks," Econometrica, Econometric Society, vol. 77(3), pages 623-685, 05]

References

[2] Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593-1636.

[1] Bloom, N. (2009). The impact of uncertainty shocks. econometrica, 77(3), 623-685.