Bristol Energy Coop Transition Lab

Not Confidential

Because nature, people and the future matters.

Tonight’s Key Topics

Optimising

- Supply

- Distribution

- Generation

- Commercial Use

- Industrial Use

Innovation in Energy

Supply & Demand

Inventing & Deploying

- Little 300

- Connected Home & Community

- Smart Grid

- Alternative Fuel Vehicles

- Distributed Generation

1st

2nd

3rd

Our Trajectory

Open Heart, Open Mind & Open Will

1

Position

2

Problem

3

Possibilities

4

Pivot

5

Proposals

6

Planning

7

Plan

The Position

Getting to where you're going requires knowing where you are.

David Allen

EVERYWHERE

Comms

IT

Music

News

Movies

Banking

Health

Apps

… and we all hate IT

At least IT doesn’t stink!

the corporation in no Board meeting or no Supervisory Board meeting has authorized this, but this was a couple of software engineers who put this in, for whatever reasons.

- 2% of green house emissions.

- c.f. Germany or Aviation.

- Rare & Expensive Minerals

- e.g. “Blood Coltan”

- Slaves to the Machine

- Child labour by Apple & others

- Labour rights e.g. Foxconn ‘interns’

- Poisoning from IT Disassembly

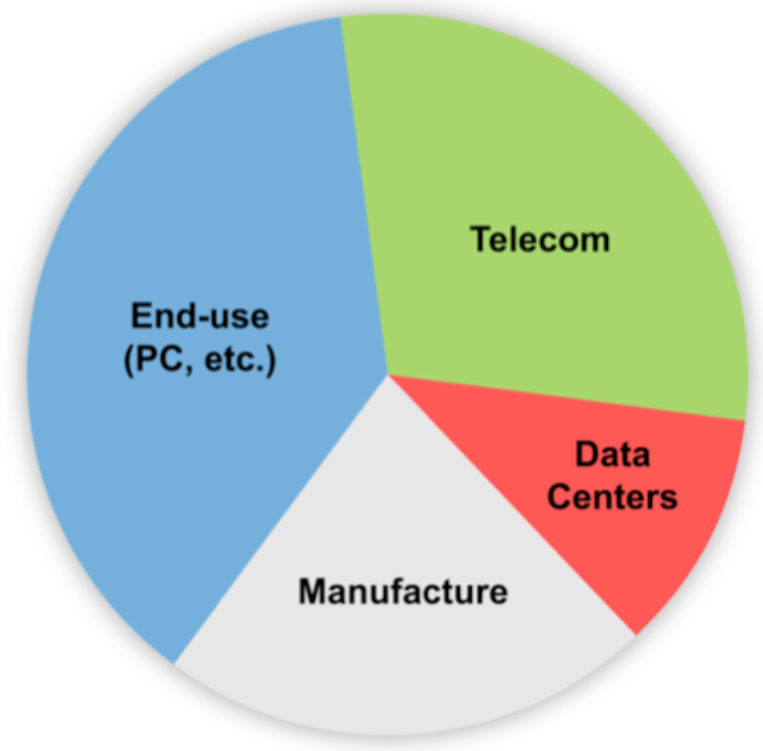

A breakdown of IT’s 2%

Source: The Cloud Begins With Coal by Mark Mills

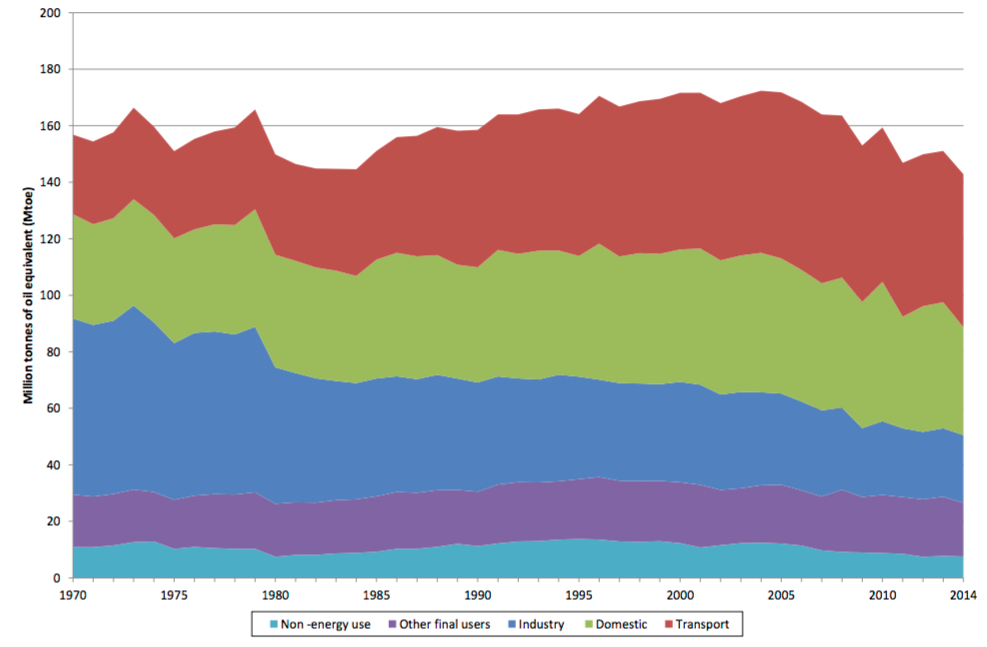

UK Energy Consumption

Source: DECC

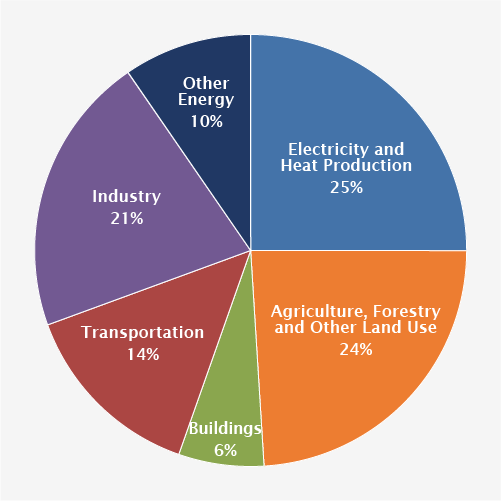

2010 Global Greenhouse

Gas Emissions

- 24% in cultivation of crops, livestock and deforestation.

- 76% of emissions are from the “energy system”.

Share of World Trade - Top Five

14.8% electrical machinery, including computers;

14.4% mineral fuels, including oil, coal, gas, and refined products ;

14.2% nuclear reactors, boilers, and parts ;

8.9% cars, trucks, and buses;

3.5% scientific and precision instruments ;

$113.7 trillion GDP ($15,800 per capita)

GDP - by end use:

- 57% household consumption

- 16.4% government consumption

- 24.9% investment in fixed capital

GDP - by sector of origin:

- 6.5% agriculture

- 31.1% industry

- 62.4% services

3.39 billion workers

- 34.6% agriculture

- 22.2% industry

- 43.1% services

While you may ignore economics, it won't ignore you.

Conclusion

IT & Energy orthodoxies are helping to

- Power Up Industry

- Over Power Nature

The Problems

The pessimist complains about the wind, the optimist expects it to change, the realist adjusts the sails

William Arthur Ward

BIG SIX strategy is to deliver annual growth in the dividend payable to shareholders through the efficient operation of and investment in, a balanced range of economically-regulated and market-based energy-related businesses.

This balance means BIG SIX has a strong and diverse group of energy assets and businesses from which to secure the revenue to support future dividend growth.

- Culture is a major root cause

- IT and energy are dominated by orthodoxy.

- Systemic 3 wise monkeys.

- The blind are leading the blind.

Big Wicked Problems

The Possibilities

To raise new questions, new possibilities, to regard old problems from a new angle requires creative imagination

and marks real advances in science.

Albert Einstein

Primary

Secondary

Tertiary

I am not an optimist. I'm a very serious possibilist. It's a new category where we take emotion apart and we just work analytically with the world.

Professor Hans Rosling

IT Reframed

Thinking differently about innovation and technology can be thoughtful & inspiring.

Technology

Innovation

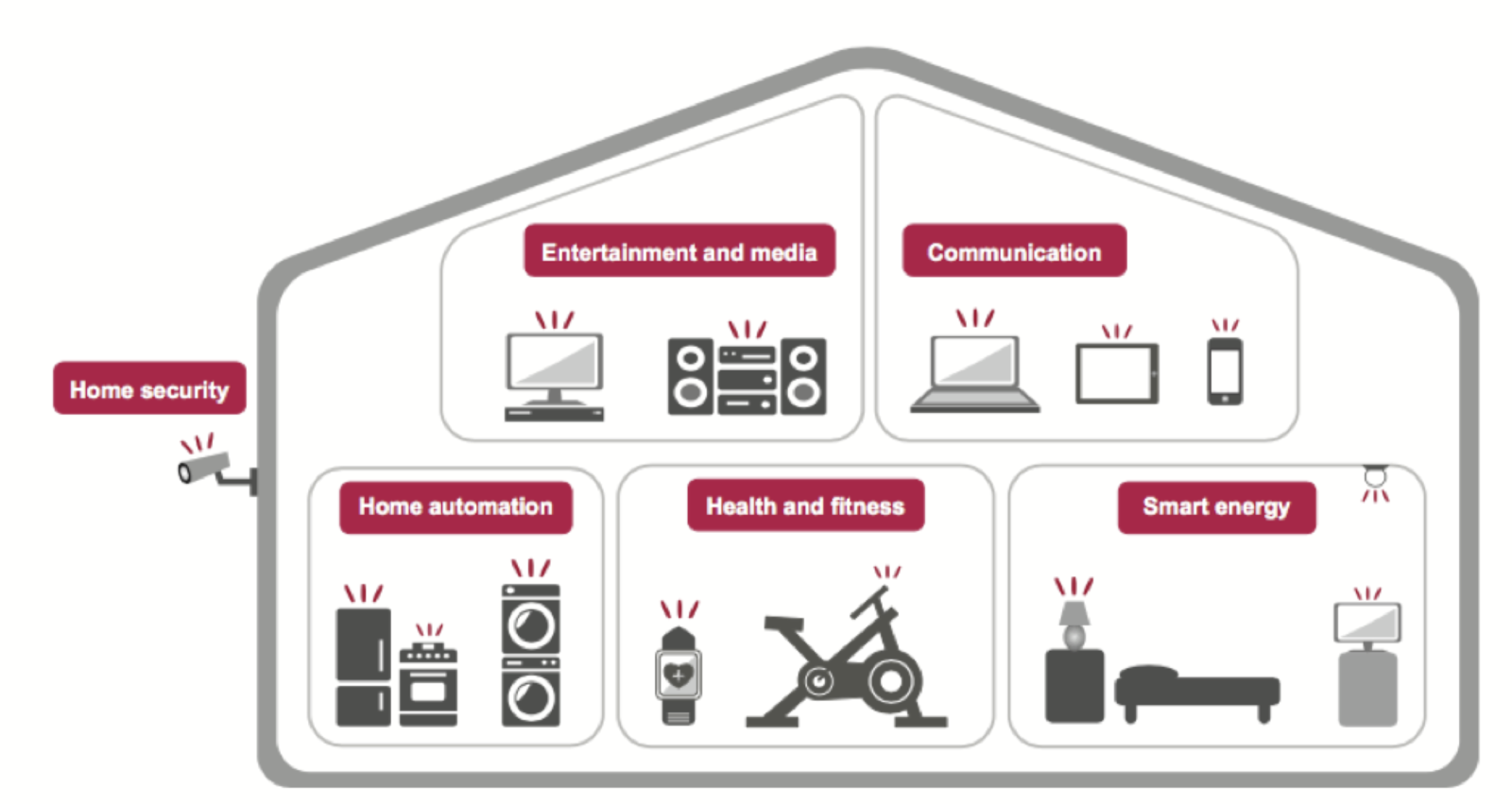

Connected Home

Many industries are converging

to satisfy our hierarchy of needs.

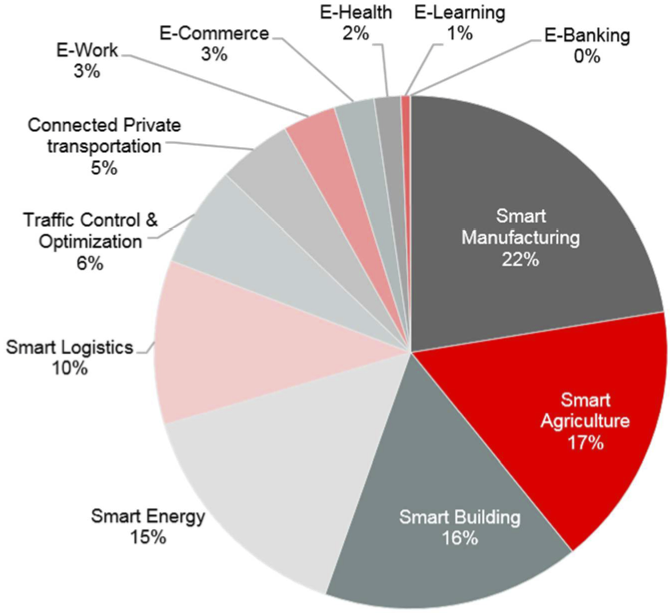

The Little 300

Renewables, smart/digital technology, big data and social media are force multipliers that can overcome the current energy orthodoxy.

Source: Ofgem

Demand Side Management

The term DSM was coined following the energy crises of the 1970s. Types of management include energy efficiency, demand response & dynamic demand.

Source: Navigant Research

Growth in Behavioural & Analytic DSM

Smart Grid

Phasor measurement units, distributed power

flow control, dynamic turn up/down,

automation, artificial intelligence, drones......

OMG!!!

Source: Navigant Research

Growth in Smart Grid Technology

Distributed Generation

Lorem ipsum .....

Connected Community

The Pivot

Retreat and reflect, allow the inner knowing to emerge.

Brian Arthur

We’re seeing a continuing sharp, exponential decline in the cost of renewable energy .....

.....in many parts of the world, renewable energy is leapfrogging fossil fuels altogether — the same way mobile phones leap-frogged land-line phones.

Al Gore, Feb 2016

Almost everything around you, was made by people that were no smarter than you.

You can change it, you can influence it, you can build your own things that other people can use.

Steve Jobs

Incumbents have to figure out different ways to use their assets, capabilities and most difficultly their cultures to compete in a very different market that is coming at them at a speed they can scarcely imagine and much faster than their cultures will find it easy to cope with.

Amory Lovins

Rocky Mountain Institute

KBO!

- On the roads

- On the grid

- In our homes

- In our offices

- In our factories

- I.T. Reframed

- Connected Home

- Connected Community

- Demand Side Management

- Smart Grid

- The Little 300

- Alternative Fuel Vehicles

- Energy Storage

- The Planning

- The Plan

Pizza & What's Next

Electric Vehicles

The time is right for electric cars.

In fact the time is critical.

Carlos Ghosn, CEO Renault & Nissan

In this section .....

Position & Problems

Possibilities

Big Auto

Gas Guzzlers

AFV Challenges

Complexity

EV or FCV?

Uniti

River Simple

Ather Energy

Tesla

Renault/Nissan

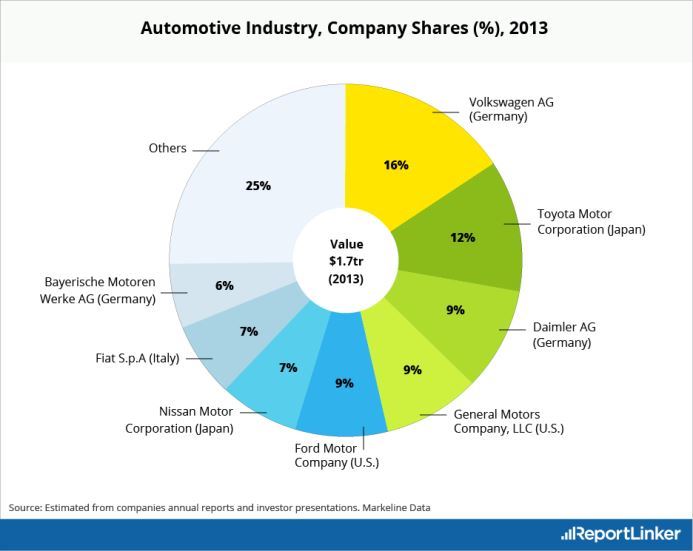

100m vehicles made per annum

- Circa 1 billion cars and light trucks on the road.

- Consuming circa 250 billion gallons fuel yearly.

- <1% of the fuel energy moves the payload

-

>90% of the mass moved is the car not the payload

- Typical car weighs 1500kg.

- Typical payload is 95kg/trip.

- >85% energy loss as heat & noise.

Source: Winning The Oil End Game, Amory Lovins

Key Considerations for AFV

.svg)

Electric Vehicles - EV

- High first cost

- Limited range

- Slow speed of recharging

Fuel Cell Vehicles - FCV

- Suffer from all 7 of the sins.

- As of 2015, two fuel cell vehicles available commercially in limited quantities.

- Difficult to engineer

- Flammability of hydrogen

- High First Cost

- High Fuel Cost

- Slow Refuelling

- Limited Range

- Limited Fuel Stations

- Safety and Liability

- Public Perceptions of Emissions

- Climate Change

Source: www.thinkprogress.org

The 7 Sins of AFVs

- 565,000 sold in 2015

- EVs have long had a per-mile fuel cost less than gasoline.

- With renewable generation, EV's have holistic low emission.

-

On going improvements in

- Range

- Recharging

- Initial Vehicle Cost

- Perceptions

There are three ways to make a living in this business: be first, be smarter, or cheat.......it sure is a hell of lot easier to just be first.

Margin Call

- Renault/Nissan - Big Auto scale

- Tesla - Silicon Valley boldness

- Ather Energy - Indian confidence

- River Simple - British quirkiness

- Uniti - Nordic efficiency & design

Some Possibilities

Big Auto Scale

-

Company Power

- Tier 1 auto maker

- 8.5M vehicles p/a (#4 globally)

- $180B revenue. 450,000 employees

-

Market Power

- A leader in the EV segment

- 85,000/565,000 EVs sold in 2015

=> 15% of niche

=> 1% of group volume

-

Offer Power

- Mid-low market vehicles.

- Cars, vans, batteries & charging.

-

Execution Power

- Early to EV market & steady growth over several years.

- Dampened by vested interest in gasoline cars.

Silicon Valley Boldness

-

Company Power

- $4B revenue. 13,000 employees.

- 125,000 cars sold in 8 years.

- 0.03% total market share

-

Market Power

- A leader in the EV segment

- 40,000/565,000 EVs sold in 2015

=> 7% of niche - 5M luxury vehicles sold per year, worth $220B

=> 0.6% of niche

-

Offer Power

- More than an auto company

- Electric luxury cars

- Automotive components

- Rechargeable energy storage systems

-

Execution Power

- Over promising & under delivering

British Quirkiness

-

Offer Power

- 300 mile range

- 3 minute recharge

- Hydrogen-fuel cell vehicle

-

Execution Power

- Rasa prototype is on road.

- Into production end of 2018.

- Roll out across the UK town by town, in tandem with hydrogen refilling stations.

-

Company Power

- Pre-revenue. Crowd funding now.

- <50 employees

-

Market Power

- Founded OScar Automotive in 2001

- Became Riversimple in 2007.

Indian Confidence

-

Company Power

- Pre-revenue.

- Circa 100 employees

-

Market Power

- Founded early 2014

- $1M seed funding Dec 2014

- $12M series A May 2015.

-

Offer Power

- Top speed of 72 kph

- Range of up to 60 km

- Charge up to 80% in 50 minutes.

-

Execution Power

- S340 unveiled on 23 Feb 2016.

- Will start taking pre-orders by Q2 end 2016. Price yet to be disclosed.

- Manufacturing will have the capacity to produce 50 scooters a day.

Nordic Efficiency & Design

-

Company Power

- Founded 2015 in Lund, Sweden

- Pre-revenue. Crowd funding soon.

- <50 employees

-

Market Power

- Underpinned by world class research, engineering & automotive capabilities.

- Tapping into open source communities.

- Strong voice in social media.

-

Offer Power

- Ultra sustainable

- Two seats in tandem (EU L7e quadricycle)

- 90km/h max speed, 150km range (weighing 400kg)

- Induction or plug-in charge. Removable battery.

- Unique driver experience

- Designed for autonomy

-

Execution Power

- Kepler Pod floor show at Cebit Feb 2016.

- Uniti Arc shipping May 2016.

- Prototype car expected end of 2016.

blog.ev-box.com

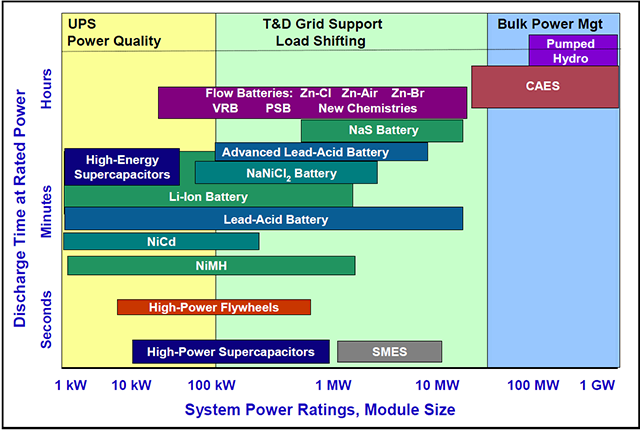

Energy Storage

Critical for Demand Side Management (DSM),

optimising renewable generation

and Alternative Fuel Vehicles (AFV).

Transmission

Distribution

Consumer

Position & Problems

Possibilities

Not enough generation

Too much demand

freq < 50Hz

Too much generation

Not enough demand

freq > 50Hz

- Optimise self consumption of renewable generation

- Store when cheap, use when expensive

- Revenues from from grid for frequency response & balancing schemes

State of art circa 2013. Things are moving on .....

Batteries

Lithium

Ionic

Lead

acid

Redox

Charge Cycles

Power Density

+

+

-

-

Flywheel ESS

- Characteristics for DR

- Short high power capability

- High cycle efficiency (up to ~95% at rated power)

- Relatively high power density

- No depth-of-discharge effects

- Easy maintenance

- Areas of differentiation

- Steel or composite flywheel (energy capacity)

- Magnetic or normal bearings (self discharge rates)

Compressed Air (CAES)

-

Typically around 60 - 90% efficient

-

Uses combination of compressors and expansion chambers to store/deliver energy.

-

Historically very large. Underground caverns and 100-300 MW units

-

Low cycle efficiency

-

High self dissipation rates

-

-

Above ground units, using air cylinders, more efficient

-

Established Players

-

LightSail

-

FlowBattery

-

-

New entrant from Adjacent market

-

Mattei

-

Text

-

Company Power

- UK private limited company

- pre-IPO

-

Market Power

- UK based, but global distribution

-

Offer Power

- Vanadium Redox Flow Battery

- Deep discharge with multiple cycles

- Domestic: 20kWh, 5kW

- SME: 300kWh, 60kW

- Modular solutions for grid

-

Execution Power

- Built in Scotland

- Incorporated 2005

-

Company Power

- Marquee investors

-

Market Power

- US based, but global distribution

-

Offer Power

- Ionic based, “Sea Water”, i.e. Na+

- Lower power density, but more sustainable than Li-Ion

- Deep discharge and high cycle count

-

Execution Power

- Initially proposing a capacity of 500 megawatt-hours per year in 2013 and 2014.

- In March 2014 they announced that commercial shipments of batteries would begin in mid-2014

- In May 2014 announced they had shipped 100 units

-

Company Power

- US based

-

Market Power

- Grid based deployments in US and Ireland

-

Offer Power

- Flywheel-based Energy Storage

-

Current offering -400 series

- 160kW units, 80kWh

- 2 year warranty

- Pricing 1.13-1.3 $/W, ex shipping + install

- Maintenance ~$6/kW per annum

- Next generation, 2017 – 450XP

-

Execution Power

-

2011, 20MW facility in NY from 200 modules for frequency regulation

-

-

Company Power

- German based company

- Spun out of fuel enrichment business

-

Market Power

- Leader in German Market

-

Offer Power

- Flywheel-based storage

- 22kW/3.6kWh units

- Built up into containers (220-616kW)

- Pricing ~£500/kW

- Aimed at grid scale

-

Execution Power

- Stadtwerke München

- 28 flywheels @ 45,000 rpm (peak)

- 100 kWh, 600 kVA.

- Stadtwerke München

-

Company Power

- UK based

- Formed in May 2015

-

Market Power

- Innovation and direct investment based

- Manufacture of newly patented storage technologies

-

Offer Power

- 0.5kW/2kWh flywheels

- Includes motors, control and inverters.

- Patents in place for novel safety system

- Pricing; £2.4/W

- Aimed at behind the meter/domestic

-

Execution Power

- Production ready, but not proven.

-

Company Power

- US based

- Founded 2009

- Marquee Investors

-

Market Power

- US Grid

-

Offer Power

- 250MW compressed air modules

- Storage based on industrial pipes

-

Execution Power

- Installing 1MW demonstrator for grid balancing in Ireland

-

Company Power

- UK based

-

Market Power

- Vertical Integration

-

Offer Power

-

Compressed air batteries

-

3kW to 200kW systems

-

100kWh max

-

-

Execution Power

- TBC but part of Flow Group

-

Company Power

- Italian, founded 1919

-

Market Power

- Specialist in Rotary Vane Technologies

-

Offer Power

- Cost effective for compression/expansion up to 250kW

- Indicative price <$500/kW

-

Execution Power

- TBC in energy storage

-

Company Power

- UK, and EU markets

- AIM listed

-

Market Power

- MoU with Good Energy

- Agreements with Shell and Toyota

-

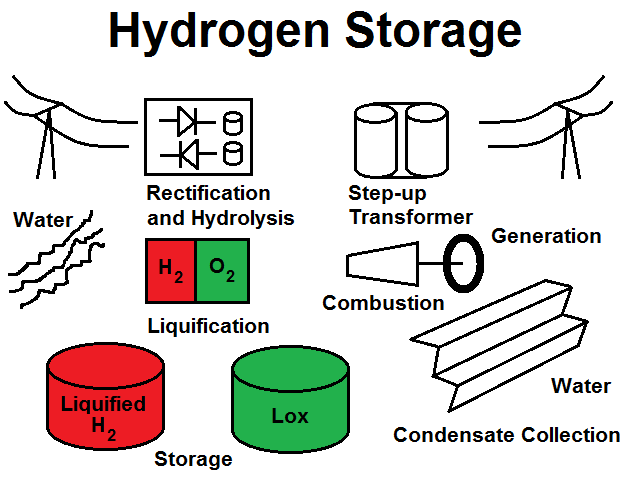

Offer Power

- Grid scale storage (HGAS)

- ReGas units (electricity to H2)

- Execution Power

- Demo units installed for Grid storage

- H2 fuelling stations deployed

Planning

Planning is everything. Plans are nothing. No plan survives contact with the enemy

Field Marshall Helmuth Graf von Molke

Natural Planning

- Purpose

- Mission

- Brainstorming

- Organising

- Next Action

Your mind's for having ideas,

not holding them

David Allen

The Plan

A good plan violently executed now is better

than a perfect plan executed next week.

General George S. Patton