Random walk, Markov chain and Brownian motion

Trang Le, PhD

2020-04-15

Guest lecture, Fundamentals of AI

Concepts

- Random walk

- Stochastic processes

- Markov chain

- Martingale

A stochastic process

is a collection of random variables indexed by time.

\(X_0, X_1, X_2, X_3, \cdots\) discrete time

\(\{X_t\}_{t\geq 0}\) continuous time

Alternatively, ...

a stochastic process is a probability distribution over a space of paths; this path often describes the evolution of some random value/system over time.

- Dependencies in a sequence of values?

- Long term behavior?

- Boundary events (if any)?

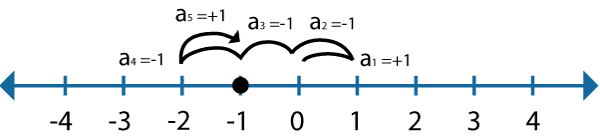

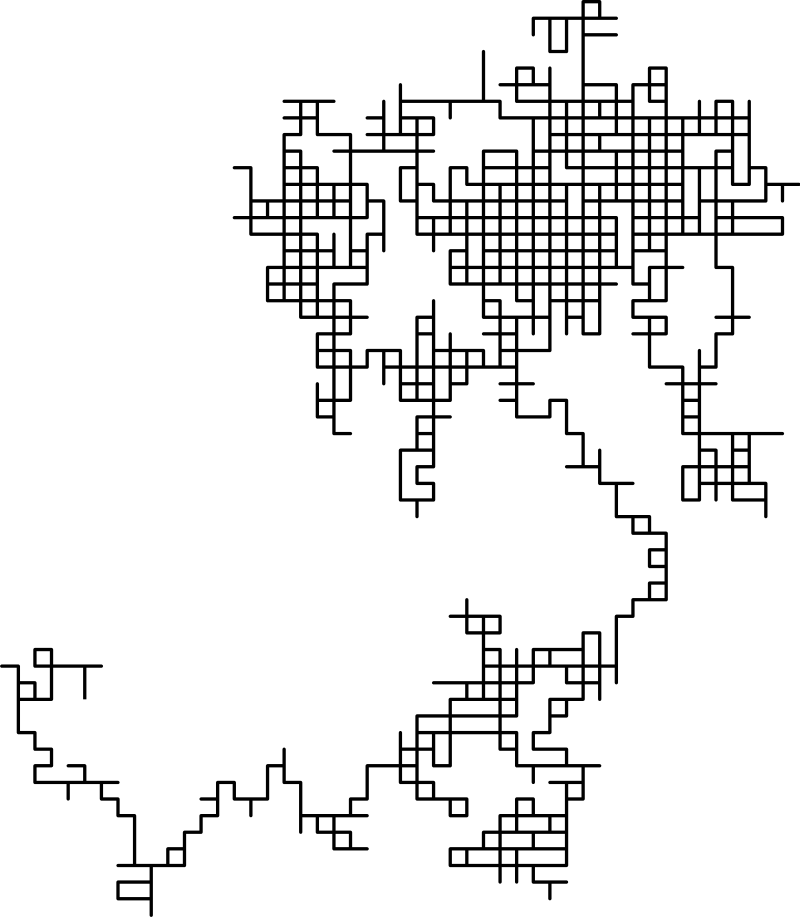

Simple random walk

\(Y_i\) i.i.d random variables \( \begin{cases} 1 & (\textrm{prob} \frac{1}{2}) \\ -1 & (\textrm{prob} \frac{1}{2}) \end{cases} \)

\(X_0, X_1, X_2, ...\) is called simple random walk.

hard to visualize the time component

2-D simple random walk

Long term behavior?

Some properties

If \(0 = t_0\leq t_1 \leq \cdots \leq t_k\)

then \(X_{t_{i+1}}- X_{t_i}\) are mutally independent.

- \(E(X_k) = 0\)

- Independent increment

- Stationary

For all \(h \geq 1, t \geq 0\), the distribution of \(X_{t+h} - X_t\) is the same as the distribution of \(X_h\).

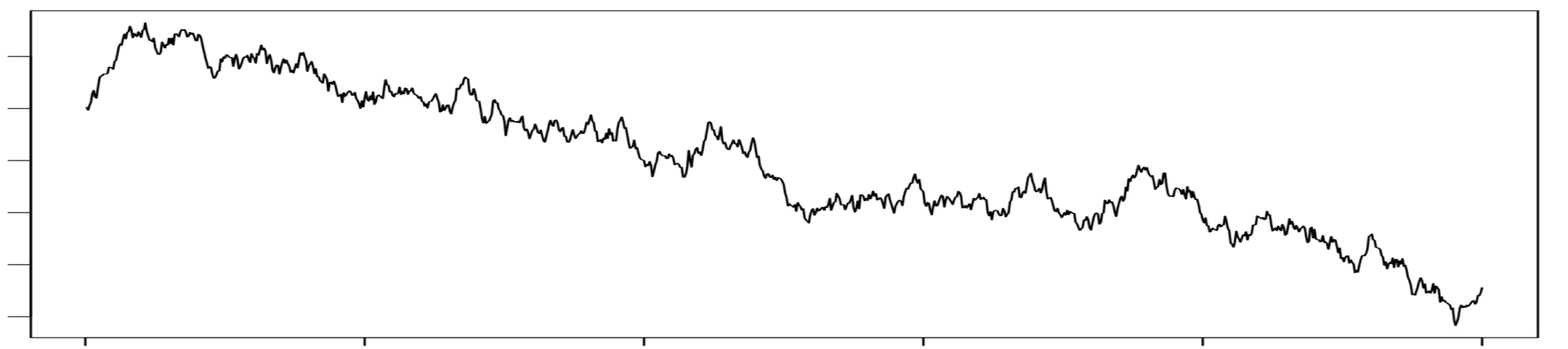

Example. A coin toss game...

At each turn, my balance goes up by $1 or down by $1.

My balance = Simple random walk

If I play until I win $100 or lose $100,

what is the probability of me winning?

If I play until I win $100 or lose $50,

what is the probability of me winning?

Code...

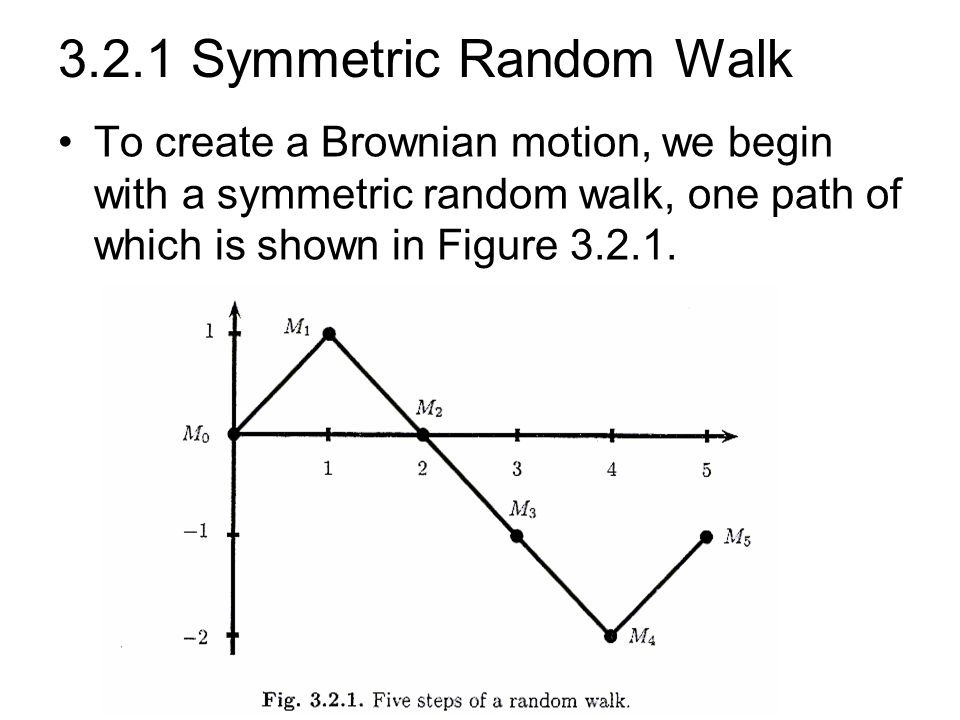

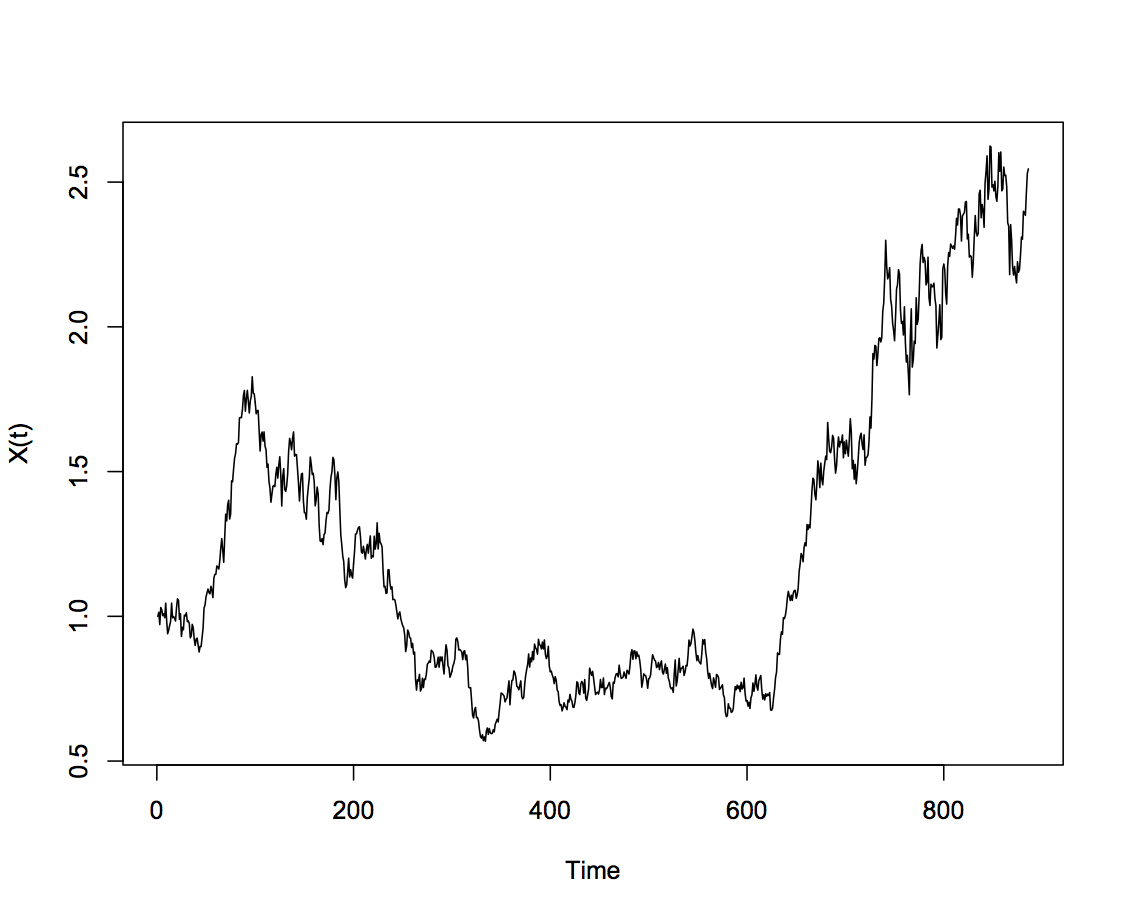

Brownian motion

is the "limit" of simple random walks.

Let \(Y_0, Y_1, ..., Y_n\) be a simple random walk.

\[Z\left(\frac{t}{n}\right) = Y_t\]

Interpolate linearly and take \(n \to \infty\).

Then, the resulting distribution is the Brownian motion.

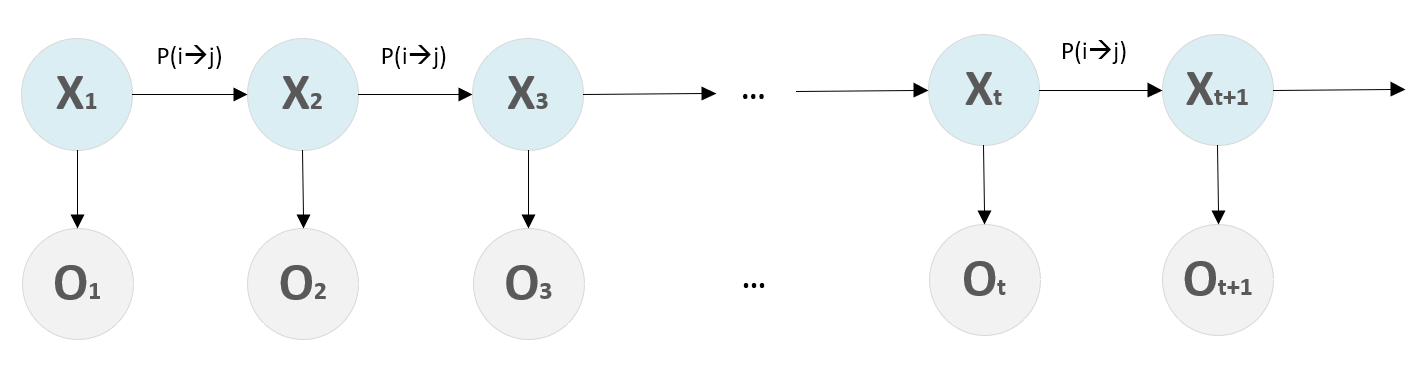

A Markov chain

is a stochastic process where effect of the past on the future is summarized only by the current state.

Formally, ...

A discrete-time stochastic process \(X_0, X_1, X_2, ...\) with state space \(S\) has Markov property if

If the state space \(S\) (\(X_t \in S\)) is finite,

all the elements of a Markov chain model

can be encoded in a transition probability matrix.

Why?

transition probability

(jumping from state i to state j)

Is simple random walk a Markov chain?

Does simple random walk have a transition probability matrix?

This matrix contains all the information about the stochastic process.

Why?

What is the probability of going from state 7 to state 9 in one steps?

What is the probability of going from state 7 to state 9 in two steps?

\[P_{79}\]

\[P^2_{79}\]

What is the probability of going from state 7 to state 9 in \(n\) steps?

An unrealistic example...

What is our transition probability matrix?

state

state

Stationary distribution

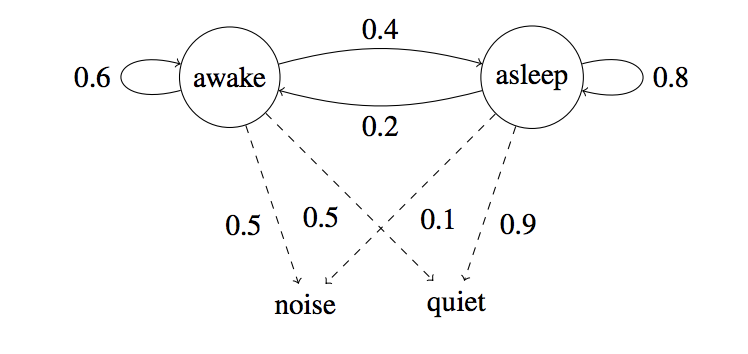

Hidden Markov Model (HMM)

Hidden Markov Model (HMM)

Hidden Markov Model (HMM)

Speech recognition

- Observation: sounds

- hidden states: words

Face detection

- Observation: overlapping rectangles of pixel intensities

- hidden states: facial features

DNA sequence region classification

- Observation: nucleotides

- Hidden states: introns, exons

A few words on

Markov Chain Monte Carlo method (MCMC)

A martingale

is a stochastic process which is "fair game".

Formally, ...

A discrete-time stochastic process \(X_0, X_1, X_2, ...\) is a martingale if

i.e., expected gain in the process is zero at all times.

Is a random walk a martingale?

A random variable \(X\) is distributed according to either \(f\) or \(g\). Consider a random sample \(X_1, \cdots, X_n\). Let \(Y_n\) be the likelihood ratio

\[Y_n = \prod_{i = 1}^n \frac {g(X_i)}{f(X_i)}\]

If X is actually distributed according to the density \(f\) rather than according to \(g\), then \[\{Y_n: n = 1, 2, 3, \cdots\}\] is a martingale with respect to\(\{X_n: n = 1, 2, 3, \cdots\}\).

Likelihood-ratio testing

Review

- Random walk

- Stochastic processes

- Markov chain

- Hidden Markov model

- MCMC

- Martingale