Andreas Park PRO

Professor of Finance at UofT

Some AMM Theory

Basic Requirements

Some Pricing Rules from Traditional Markets: Uniform Price

\(q=2\)

\(\Delta c(q)= q\times p^m(q)=2\times 15.5\)

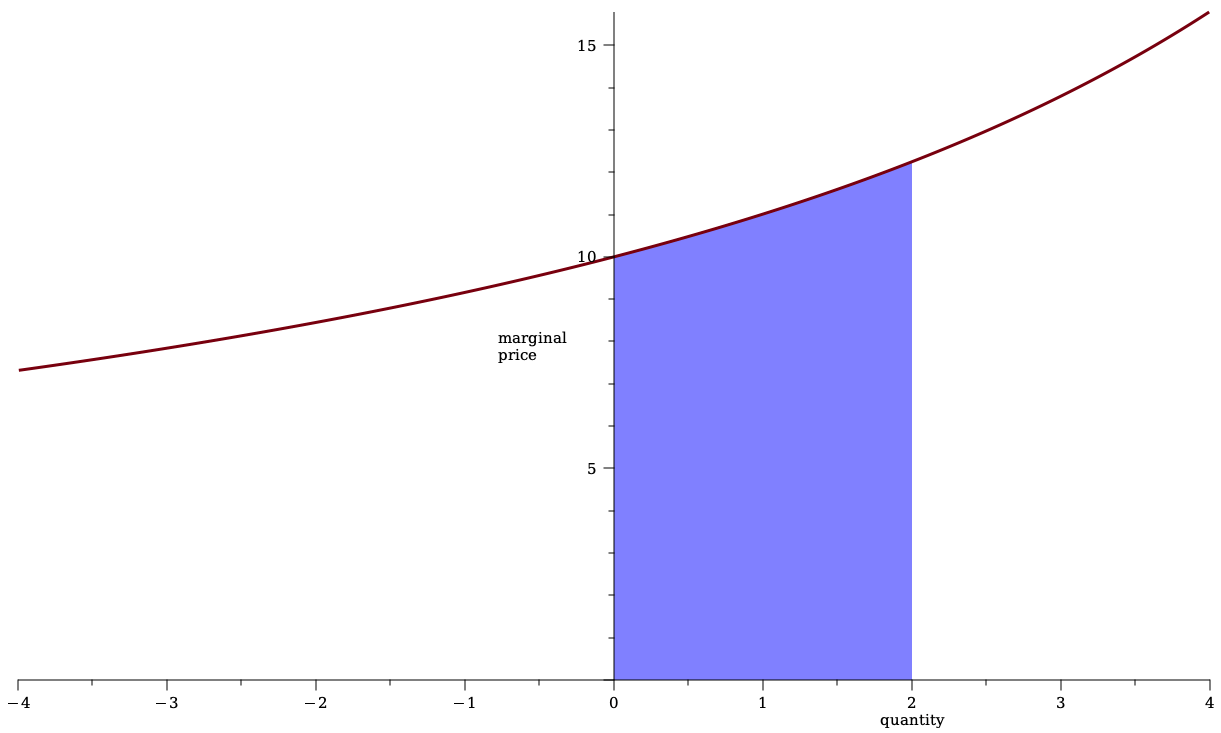

Some Pricing Rules from Traditional Markets: Limit Order Book

\[\Delta c(q)=\int_0^q\rho(s) ds.\]

Some Pricing Rules from Traditional Markets: Limit Order Book

note: if you do uniform pricing and split your order into infinitesimal units, then you pay the limit order price

Most Common Pricing Rule in DeFi: Constant Product

Insight: AMM pricing function is the same as a limit order book when we require

By Andreas Park

some general thoughts on AMMs vs TradFi