Andreas Park PRO

Professor of Finance at UofT

5th Annual Rotman GRI Finance Forum

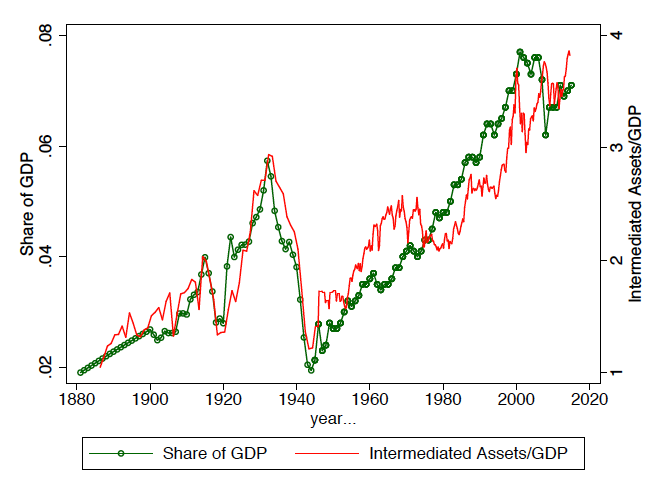

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

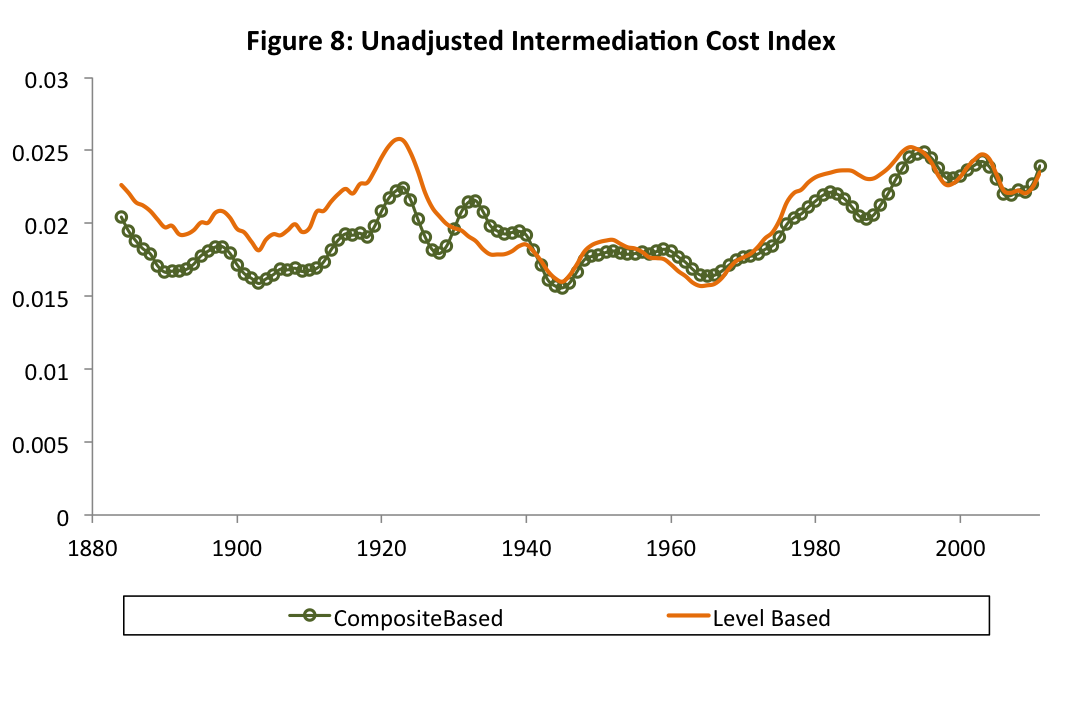

Source: Philippon (AER 2015) "Has the U.S. Finance Industry Become Less Efficient?"

Source: Bloomberg News, Feb 20, 2015

Note: The biggest disruptors (the HFTs) came from the outside of the traditional system (kinda).

Easier access and greater diversity of skills.

adapted from Philippon (2017)

=> avoid the existing, clunky infrastructure

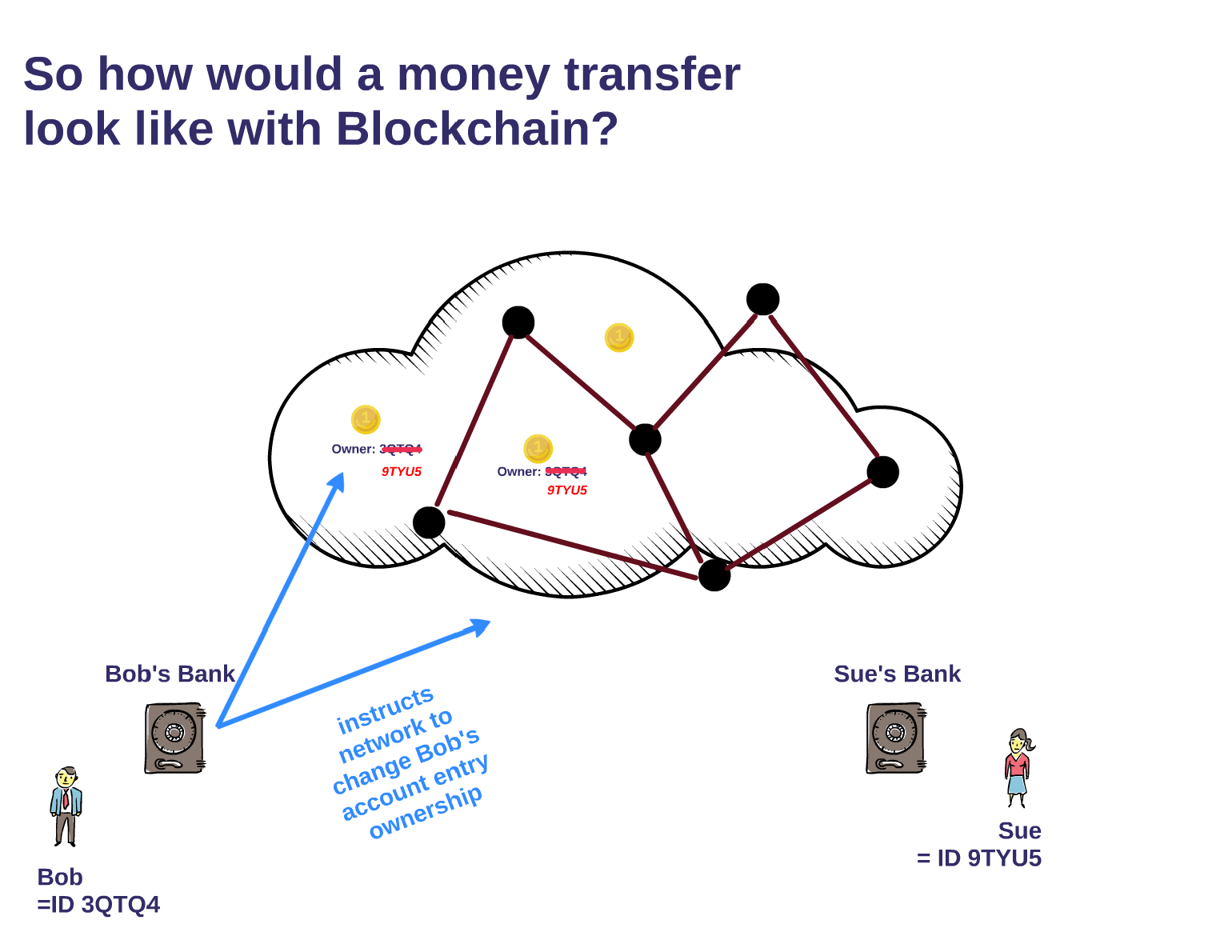

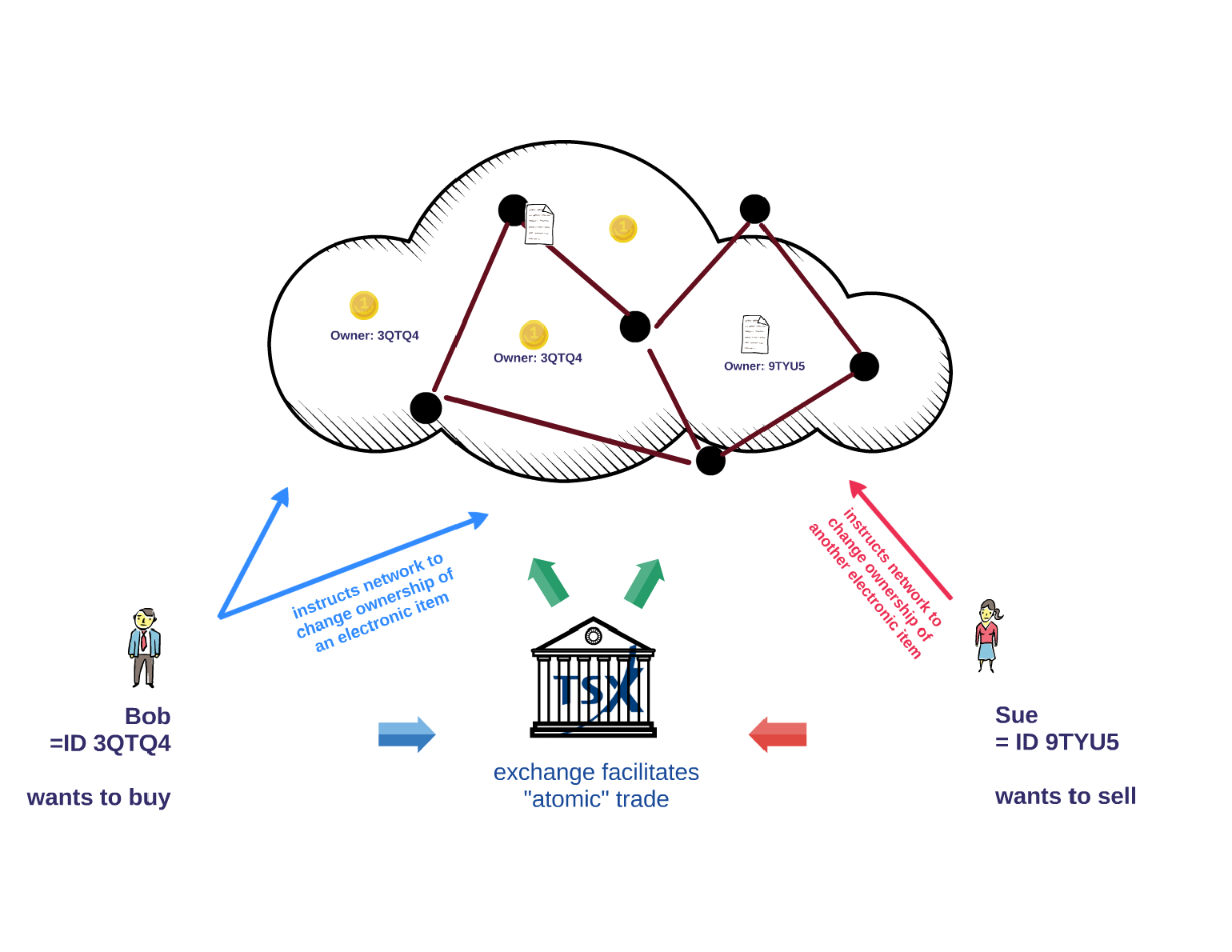

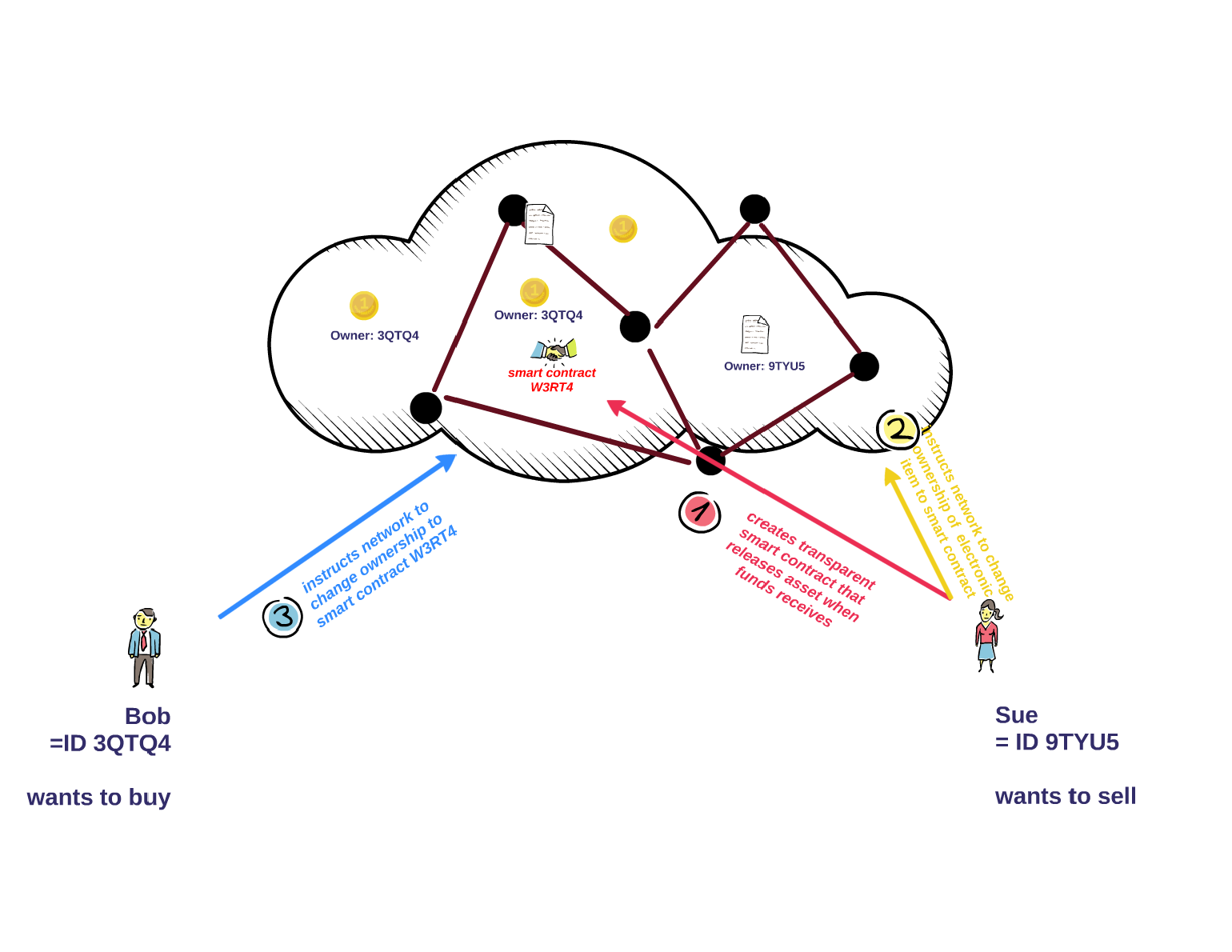

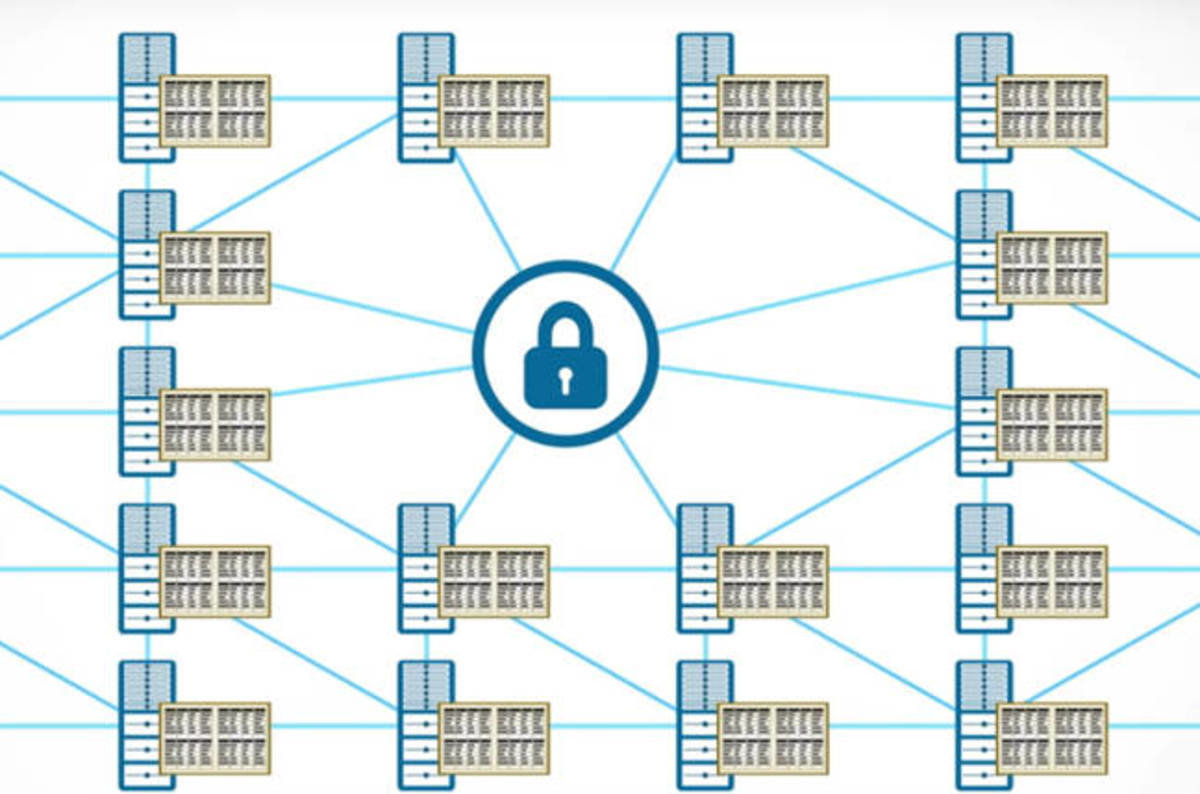

central registry

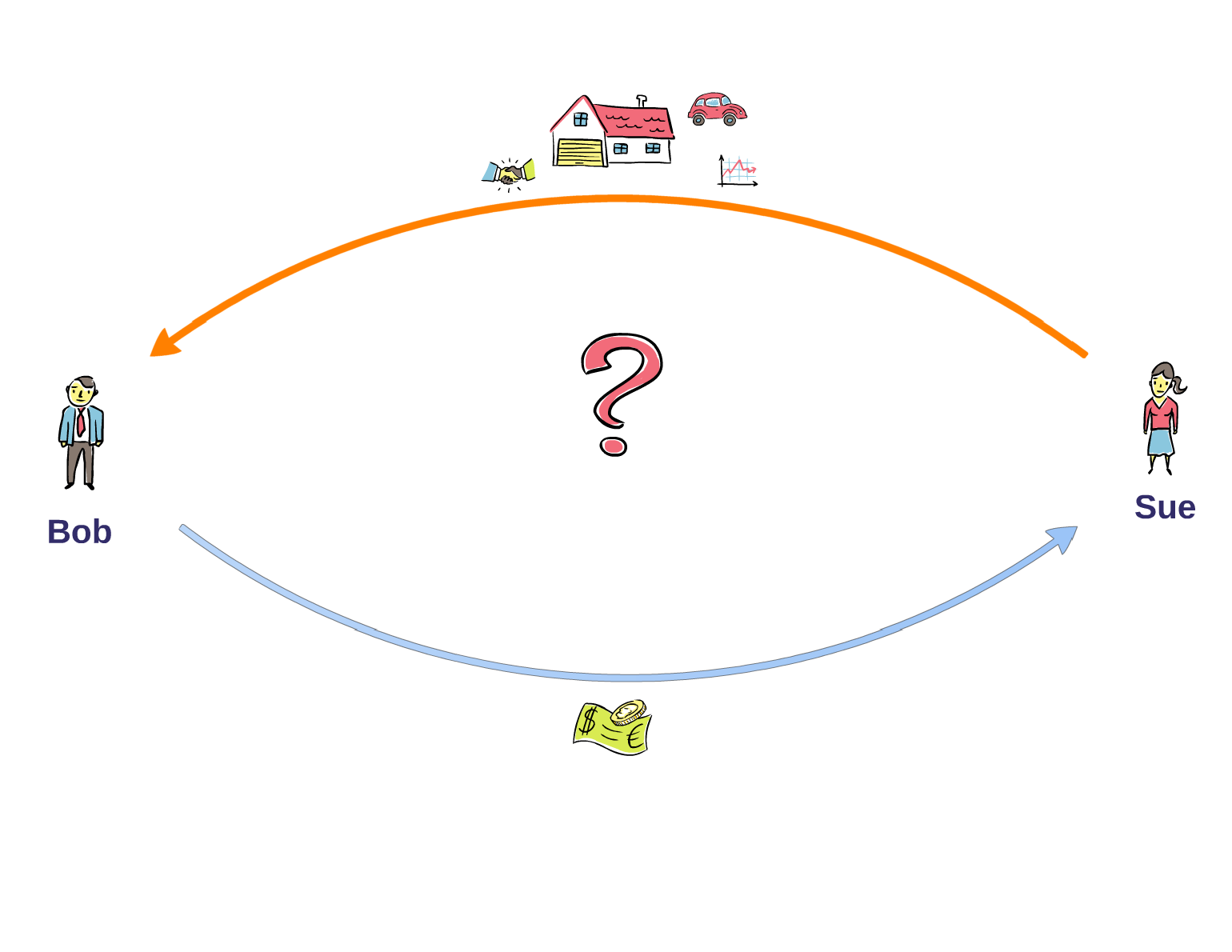

Problem:

Option 1: Centralized

Technological challenge:

Option 2: Distributed Network

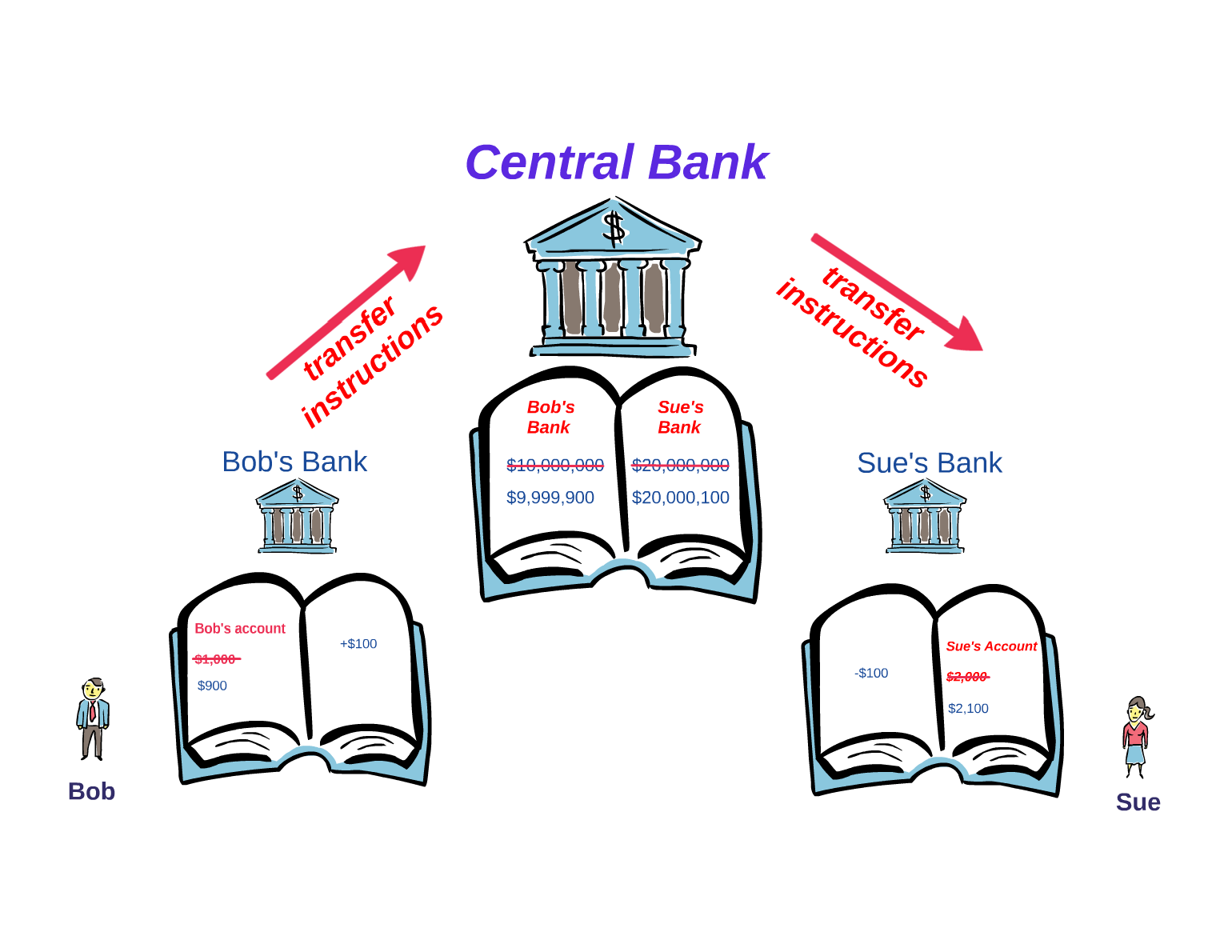

Why use banks?

frictionless electronic transfer of information

Blockchain:

frictionless electronic transfer of value

FinTech

Distributed Ledger Technology

Blockchain

My definition of FinTech: outside main financial institutions, usually post-2008

Compliance

Wealth management

Cybersecurity

payments

Data & Analytics

Cryptocurrency

crowdfunding

(120+ FinTechs)

(19 equity CF platforms)

(P2P) lending

Disclaimer: Blockchain can be used for many other non-finance applications, e.g., health records, IoT, voting, prescription drugs

5th Annual Rotman GRI Finance Forum

By Andreas Park

a set of slides that I used for a presentation at Rotman's 2017 Alumni Finance Forum