Financial Instruments:

Bonds and Futures

Christopher Makler

Stanford University Department of Economics

Econ 50: Lecture 13

Warm-Up Exercise: Expected Value

If a random variable \(X\) takes on values \(x_1,x_2,x_3,...,x_n\) with probabilities \(\pi_1,\pi_2,\pi_3,...,\pi_n\), where the \(\pi\)'s all add up to 1, then the expected value of \(X\) is

\mathbb{E}[X] = \sum_{i = 1}^n \pi_i x_i

= \pi_1x_1 + \pi_2x_2 + \pi_3x_3 + \cdots + \pi_nx_n

Example:

Suppose there is a 50% chance it will rain tomorrow,

If it rains, there is an 80% chance it will rain 10mm,

and a 20% chance it will rain 20mm.

What is the expected value of the amount of rain?

pollev.com/chrismakler

Applications of Uncertainty and Intertemporal Choice

Futures

Buying money in states of the world

Prediction Markets

Problems of insider trading and market manipulation

Bonds

Duration

Inflation

Risk of Default

Futures and Prediction Markets

\text{Expected consumption: }\mathbb{E}[c] = \pi_1 c_1 + \pi_2 c_2

\text{Expected of the lottery: }\mathbb{E}[v(c)] = \pi_1 v(c_1) + \pi_2 v(c_2)

\text{Utility from having }\mathbb{E}[c]\text{ for sure: }v(\mathbb{E}[c]) = v(\pi_1 c_1 + \pi_2 c_2)

Risk Aversion

\text{Risk averse: }v(\mathbb{E}[c]) > \mathbb{E}[v(c)]

You prefer having E[c] for sure to taking the gamble

\text{Risk neutral: }v(\mathbb{E}[c]) = \mathbb{E}[v(c)]

\text{Risk loving: }v(\mathbb{E}[c]) < \mathbb{E}[v(c)]

You're indifferent between the two

You prefer taking the gamble to having E[c] for sure

Marginal Rate of Substitution

u(c_1,c_2) = \pi v(c_1) + (1-\pi) v(c_2)

MRS =

MU_1 = \text{MU from another dollar in state 1} =

MU_2 = \text{MU from another dollar in state 2} =

\pi \times v'(c_1)

(1-\pi) \times v'(c_2)

Where do the values of \(c_1\) and \(c_2\) come from?

- Up to now, we've been talking about your preferences over lotteries.

- What if you could buy a lottery in the same way as you could buy a bundle of goods?

Prediction markets like Kalshi and Polymarket let you buy a contract that pays $1 if an event occurs.

You can either buy a contract saying the event will occur, or that it will not occur. These must add up to 1, with possible rounding errors.

So, if \(c_1\) is your consumption if the event occurs, and \(c_2\) is your consumption if it doesn't occur, these prices are \(p_1\) and \(p_2\)!

\mathbb{E}[v(c)] = \pi c_1^r + (1-\pi) c_2^r

Your value function for money in any state of the world is \(v(c) = c^r\).

Suppose you have $300 in your pocket, and you believe Gavin Newsom will win with some probability \(\pi > 0.25\).

You can buy money in state of the world 1 for \(p_1 = 0.25\). How much should you buy?

Prediction Markets: The Good, the Bad, and the Ugly

- Good: Information has economic value, and prediction markets can provide real-time data on the "wisdom of crowds."

- Bad: insider trading - traders know whether an event will happen

- Ugly: Risk of market manipulation - traders can influence the odds of an event happening

Lest you think this is a new phenomenon...

An important note

Prediction markets walk a fine line between investing, risk hedging, and gambling.

Markets for risky assets are a core subject of econ; but gambling addiction is a serious problem.

If you or someone you love has a problem with gambling, there is help. Reach out.

Bonds

c_2 = m_2 + (1 + r)(m_1 - c_1)

Inflation and Real Interest Rates

Suppose there is inflation,

so that each dollar saved can only buy

\(1/(1 + \pi)\) of what it originally could:

c_2 = m_2 + \left({1 + r\over 1 + \pi}\right)(m_1 - c_1)

Up to now, we've been just looking at

dollar amounts in both periods

\text{let }\rho = {1 + r \over 1 + \pi} - 1

c_2 = m_2 + (1 + \rho)(m_1 - c_1)

We call \(r\) the "nominal interest rate" and \(\rho\) the "real interest rate"

For low values of \(r\) and \(\pi\), \(\rho \approx r - \pi\)

c_1 + \frac{c_2}{1+r} = m_1 + \frac{m_2}{1 + r}

"Present Value" for two periods

Beyond Two Periods

If you save \(s\) now, you get \(x = s(1 + r)\) next period.

The amount you have to save in order to get \(x\) one period in the future is

s(1 + r) = x

s = {x \over 1 + r}

Remember how we got this...

If you save \(s\) now, you get \(x = s(1 + r)\) next period.

The amount you have to save in order to get \(x\) one period in the future is

s(1 + r) = x

s = {x \over 1 + r}

If you save for two periods, it grows at interest rate \(r\) again, so \(x_2 = (1+r)(1+r)s = (1+r)^2s\)

Therefore, the amount you have to save in order to get \(x_2\) two periods in the future is

s(1 + r)^2 = x_2

s = {x_2 \over (1 + r)^2}

If you save for two periods, it grows at interest rate \(r\) again, so \(x_2 = (1+r)(1+r)s = (1+r)^2s\)

Therefore, the amount you have to save in order to get \(x_2\) two periods in the future is

s(1 + r)^2 = x_2

s = {x_2 \over (1 + r)^2}

If you save for \(t\) periods, it grows at interest rate \(r\) each period, so \(x_t = (1+r)^ts\)

Therefore, the amount you have to save in order to get \(x_t\), \(t\) periods in the future, is

s(1 + r)^t = x_t

s = {x_t \over (1 + r)^t}

Therefore, the amount you have to save in order to get \(x_t\), \(t\) periods in the future, is

s(1 + r)^t = x_t

s = {x_t \over (1 + r)^t}

We call this the present value of a payoff of \(x_t\)

PV(x_t) = {x_t \over (1 + r)^t}

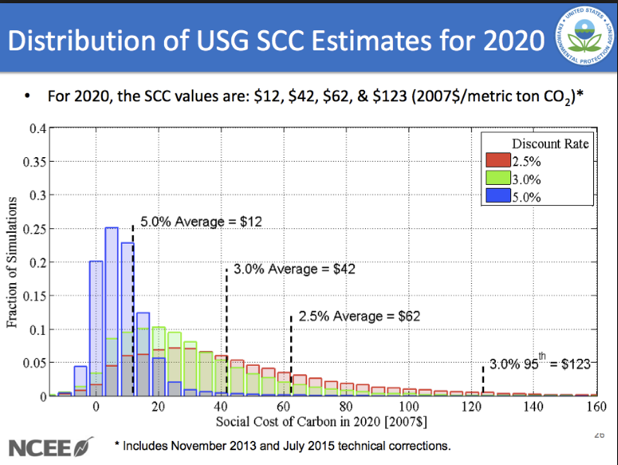

Application: Social Cost of Carbon

Obama Admin: $45

Uses a 3% discount rate; includes global costs

Trump Admin: less than $6

Uses a 7% discount rate; only includes American costs

PV of $1 Trillion in 2100:

$86B for Obama, $4B for Trump

Risky Assets and Optimal Portfolio Theory

Two Kinds of Optimization

Tradeoffs between two goods

Optimal quantity of one good

🍎

(not feasible)

(feasible)

🍌

Optimal choice

🙂

😀

😁

😢

🙁

🍎

benefit and cost per unit

Marginal Cost

Marginal Benefit

Optimal choice

Tradeoffs between two goods

Optimal quantity of one good

Checkpoint 1: April 20

Model 1: Consumer Choice

Model 2: Theory of the Firm

Checkpoint 2: May 4

WEEK 1

WEEK 2

WEEK 3

Modeling preferences with multivariable calculus

Constrained optimization when calculus works

Constrained optimization when calculus doesn't work

WEEK 4

WEEK 5

Consumer Demand

Applications: Financial Economics

Checkpoint 3: May 18

Final Exam: June 5

WEEK 6

WEEK 7

WEEK 8

Production and Costs for a Firm

Profit Maximization

When markets work

WEEK 9

WEEK 10

When markets need a little help

When markets fail

Model 3: Market Equilibrium

Econ 50 | Lecture 13 | Futures and Bonds

By Chris Makler

Econ 50 | Lecture 13 | Futures and Bonds

We apply the framework of consumer choice theory to the choice of how to allocation money across time, investigating saving and borrowing.