Book 2. Credit Risk

FRM Part 2

CR 13. Credit Derivatives

Presented by: Sudhanshu

Module 1. Credit Default Swaps

Module 2. CDS Extensions and Credit Indices

Module 3. Total Return Swaps and Collateralized Debt Obligations

Module 1. Credit Default Swaps

Topic 1. Credit Derivative Products

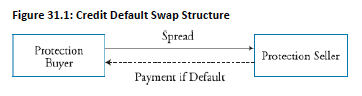

Topic 2. Credit Default Swap Structure

Topic 3. CDS Valuation

Topic 2. Credit Default Swap Structure

- CDS Definition: Contract where a protection buyer pays periodic CDS spreads to a protection seller for protection against default on a reference obligation; payments continue until maturity or default, whichever occurs first

- Premium Payment Structure: CDS premiums are paid in arrears (at the end of settlement periods), unlike regular insurance policies paid upfront

- Upon default, an accrual payment is due for the period between the last settlement date and default date

- Example: In a 5-year CDS with annual settlement, if default occurs three months after the first payment, the protection buyer owes a pro-rata premium for those three months

- Standardization: Many CDS contracts follow ISDA terms with common maturities of 1, 3, 7, and 10 years and quarterly settlements on March 20, June 20, September 20, and December 20

- First payment covers the period from initiation date to first settlement date

Topic 2. Credit Default Swap Structure

- CDS-Bond Basis Relationship: N-year CDS premium should approximately equal the risk premium on an N-year risky bond over the benchmark rate

- CDS-bond basis = CDS spread – bond yield spread

- Basis should be close to zero for swaps with same maturity as reference obligation to prevent arbitrage

- Recovery Rate and Settlement: Recovery rate is the percentage of par value at which a bond trades immediately after default

- CDS contracts allow delivery of any bonds with same seniority from same issuer

- Protection buyer delivers the cheapest-to-deliver (CTD) bond for full face value

- Example: If CTD trades at $53 for $100 par value bond, recovery rate is 53%

Practice Questions: Q1

Q1. Modus Corp's 7 -year, 5 % coupon bond is rated AA. The annual CDS spread on a 7 -year bond is 3 %. The swap spread is flat at 25 bps, while the swap fixed rate is 3 % for 5 years and 4 % for 7 years. To prevent arbitrage, Modus Corp's bond should most likely yield:

A. 7.00 %.

B. 7.25 %.

C. 7.75 %.

D. 8.00 %.

Practice Questions: Q1 Answer

Explanation: A is correct.

Arbitrage-free conditions indicate that:

CDS-bond basis = CDS spread – bond yield spread = 0

Thus, CDS spread = bond yield spread = 3% (given).

Bond yield spread = bond yield – swap fixed rate

3% = bond yield – 4% (make sure to use the 7-year swap fixed rate)

Therefore, the bond yield = 7%.

Topic 3. CDS Valuation

-

CDS Spread: CDS valuation involves determining the CDS spread (s), which serves as the compensation for bearing credit risk.

-

Inputs: CDS spread (s) is calculated using four primary inputs:

-

the swap maturity,

-

the risk-free rate,

-

the hazard rate (default intensity), and

-

the recovery rate.

-

-

Key Valuation Formulas: To value a CDS, we must first determine the probability that the reference entity will survive or default over a specific period.

-

Hazard Rate ( ): A constant parameter representing default intensity.

-

Probability of Survival (PS): The probability that the entity has not defaulted by time t is calculated as:

-

-

-

Probability of Default (PD): The probability of defaulting specifically within year t is the difference between the survival probability at the end of the previous year and the current year:

-

-

-

PS_{t} = e^{-\lambda \times t}

PD_{t} = (PS_{t-1} - PS_{t})

\lambda

Topic 3. CDS Valuation

-

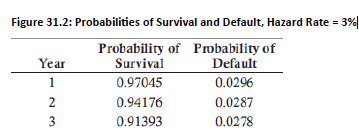

CDS Valuation Example: Consider a 3-year CDS with a hazard rate of 3%, a recovery rate of 35%, and a continuously compounded risk-free rate of 4%. We assume annual settlements and that defaults occur in the middle of the year.

-

The probabilities of survival for each year of the swap are computed as follows:

-

Year 1:

-

Year 2:

-

Year 3:

-

-

The probability of survival at t = 0 = 100%, or 1. Therefore

-

PD in Year 1 = 1 - 0.97045 = 0.0296

-

PD in Year 2 = 0.97045 − 0.94176 = 0.0287

-

PD in Year 3 = 0.94176 − 0.91393 = 0.0278

-

(e^{-1 \times 0.03})=0.97045

(e^{-2 \times 0.03})=0.94176

(e^{-3 \times 0.03})=0.91393

Topic 3. CDS Valuation

-

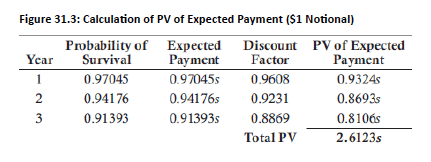

Suppose that the CDS spread = s%. Fig 31.3 shows the expected payment for each of the three years in the swap. Note that the payment is made only if there is no default:

-

-

-

We discount the expected payment at the risk-free rate of 4%. For example, the discount factor at t=1 is: The PV of the expected payment is then computed as:

-

-

-

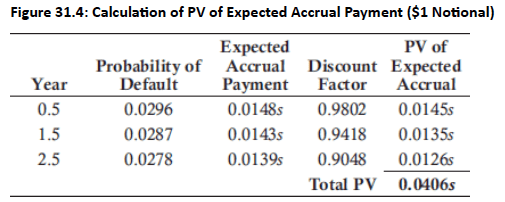

As the protection buyer makes the payments in arrears and because the default is assumed to occur in the middle of the year, there is a final payment (i.e., accrual payment) that the protection buyer needs to make in the year of the default

(representing the CDS spread for half the year or s/2).

-

Fig 31.4 presents the present value of expected accrual payments, using default probabilities since these payments occur only if a default happens.

-

Therefore, the total PV of expected payments made by the protection buyer over the life of the swap = 2.6123s + 0.0406s = 2.6529s.

\text {Expected Payment }=\text { Probability of Survival } \times \text { Notional Principal } \times s

e^{-0.04 \times 1}=0.9608.

\text { PV of expected payment }=\text { discount factor × expected payment }

Topic 3. CDS Valuation

-

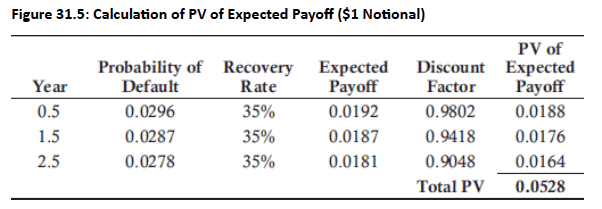

Now, we calculate the PV of the expected payoff paid by the protection seller under the assumption of a 35% recovery rate. Recall the assumption that default occurs in the middle of the year and the payoff would occur at that time. (Calculations in Fig. 31.5)

-

-

-

Assuming default in Year 2 (or Year 1.5, because default is assumed to occur in the middle of the year):

-

-

-

Then, the PV of the expected payoff = expected payoff multiplied by the discount factor.

-

The CDS spread for this 3-year deal is computed using the following equation and solving for s:

-

-

-

-

\text { expected payoff }=(1 \text { - recovery rate }) \times \text { PD } \times \text { notional principal }

\text { expected payoff }=0.65 \times 0.0287 \times \$ 1=0.0187

\begin{aligned}

& \text { PV of E(payments) }=\text { PV of E(payoff) } \\

& 2.6529 s=0.0528 \\

& s=0.0528 / 2.6529=0.0199, \text { or } 1.99 \%, \text { or } 199 \mathrm{bps}

\end{aligned}

Practice Questions: Q2

Q2. Xeta Corp's hazard rate is estimated to be 2 % over the next five years. The probability of default in Year 2 for Xeta is closest to:

A. 1.94 %.

B. 1.98 %.

C. 2.00 %.

D. 2.23 %.

Practice Questions: Q2 Answer

Explanation: A is correct.

The probability of survival in Years 1 and2

and

The probability of default in Year 2 = 0.9802 – 0.9608 = 0.0194, or 1.94%.

e^{-0.02 \times 1}=0.9802

e^{-0.02 \times 2}=0.9608

Practice Questions: Q3

Q3. CDS spreads are calculated such that the PV of:

A. accrual payments is zero.

B. expected payoff is less than the PV of expected payments during the life of the CDS.

C. expected payoff is equal to the PV of expected payments during the life of the CDS.

D. expected payoff is greater than the PV of expected payments during the life of the CDS.

Practice Questions: Q3 Answer

Explanation: C is correct.

The CDS spread is set such that the PV of expected payoff is equal to the PV of

expected payments during the life of the swap. The PV of expected payments

includes the PV of expected periodic swap spread payments plus the PV of

expected accrual payments.

Module 2. CDS Extensions and Credit Indices

Topic 1. Default Probabilities Used to Value a CDS

Topic 2. Marking a CDS to Market

Topic 3. Binary CDS

Topic 4. Credit Indices

Topic 5. Fixed Coupons

Topic 6. CDS Forwards and Options

Topic 1. Default Probabilities Used to Value a CDS

- Risk-Neutral vs. True Probability: The probability of default (PD) used in CDS pricing is the risk-neutral (RN) probability, not the true/actual PD; RN probability is implied from the CDS spread quoted in the market

- Calibrating Hazard Rate: If actual market CDS spread is 2.75% but assumed hazard rate of 3% is too low, trial-and-error methods or Excel SOLVER can determine the correct hazard rate (approximately 4.15% in this example)

- Recovery Rate (RR) Impact:

- When calculating using RN probability implied by market price, the estimated RR does not affect final market spread calculations

- RN probability of default is approximately proportional to 1/(1-RR)

- Higher assumed RR leads to higher RN probability of default while keeping actual market CDS spread constant

Topic 2. Marking a CDS to Market

- Daily MtM Process: CDS contracts are marked to market daily to reflect current market conditions and fair value changes.

- Spread Movement Impact:

- Narrowing spreads: Protection buyer loses value; protection seller gains value

- Widening spreads: Protection buyer gains value; protection seller loses value

- MtM Calculation: The MtM value to the protection seller is computed as:

-

-

-

Example: Consider a 3-year swap that was originally part of a 3.5-year swap initiated 6 months ago at a spread of 1.50%. With 3 years remaining, the PV of expected payments and the PV of payoff were 2.6529s and 0.0528, respectively, and s was equal to 1.99%. Calculate the MtM value of the swap to the protection seller with a notional principal of $1million.

-

Answer: Using the 1.50% original spread, the PV of expected payments = 2.6529 X 0.015 = 0.0398 per $1 notional. The PV of the expected payoff with three years remaining is unchanged at 0.0528 per $1 notional.

-

Value of protection seller = PV of expected payments - PV of expected payoff =0.0398 - 0.0528 = -0.013 per $1 notional principal

-

Swap value to protection seller = -0.013 X $1,000,000 = -$13,000

-

Swap value to protection buyer = +$13,000

-

-

As the swap spread has widened from 1.50% to 1.99% in the six months since inception, the protection buyer gains, and the protection seller suffers a loss.

-

\text{MtM value to protection seller} = \text{PV of expected payments} - \text{PV of expected payoff}

Practice Questions: Q1

Q1. Banko, Inc., entered into a $5 million notional, 5-year CDS as a protection buyer two years ago at a spread of 1.85%. The current 3-year CDS spread for the same reference entity is 2.30% based on the PV of expected payoff of 0.0312 per $1 notional. The value of the CDS to Banko, Inc., is closest to:

A. -$ 45,000.

B. -$ 30,900.

C. +$ 30,500.

D. +$ 53,000.

Practice Questions: Q1 Answer

Explanation: C is correct.

Recognize that the value of the CDS is calculated such that:

- current PV of expected payments = current PV of expected payoff = 0.0312

Using the current spread of 2.30%,

- current PV of expected payments = 0.023 ×s

- s = 0.0312/0.023 = 1.3565

Applying this value to the initial CDS spread of 1.85% yields:

- PV of expected payments (based on 1.85%) = 0.0185 × 1.3565 = 0.0251

Value to the protection buyer = PV of expected payoff − PV of expected payments

- Value to the protection buyer= 0.0312 – 0.0251 = 0.0061 per $1 notional

The swap value for the $5 million notional = 0.0061 × 5,000,000 = $30,500.

Because the spread has widened, the protection buyer gains.

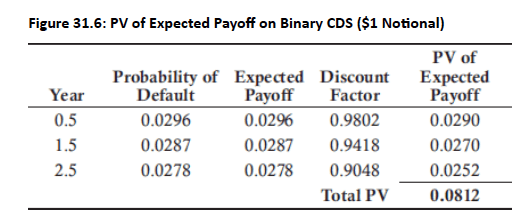

Topic 3. Binary CDS

-

Binary CDS: The payoff on default is full notional, regardless of recovery rate (RR).

-

Payoff: The payoff calculation changes only at last step, where RR is updated to 0%.

-

Updated Calculations: Fig 31.6 shows the new calculations using the data from the previous example. The sum of the PV of expected payments remains 2.6529s.

-

The spread on this binary CDS to computed as:

-

s = 0.0812/2.6529 = 0.0306 = 3.06%

-

-

Using the original RR of 35%, the spread on a binary CDS is calculated as:

-

-

-

-

-

As expected, with a 0% recovery assumption, the calculated spread of 3.06% for a binary CDS is higher than the 1.99% spread for a vanilla (or regular) CDS. Therefore, the price to purchase protection in a binary CDS is higher.

\text{binary CDS spread} = \frac{\text{vanilla CDS spread}}{(1 - RR)} =\frac{1.99}{1-0.35}=3.06\%

Topic 4. Credit Indices

- Overview: CDS indices provide exposure to credit risk of multiple issuers simultaneously (similar to equity indices), with equal protection weight for each issuer and total notional equal to the sum of all individual protections

- Major Index Examples:

- CDX NA IG covers 125 equally-weighted North American investment-grade companies

- iTraxx Europe covers 125 equally-weighted European investment-grade companies

- Similar indices exist for high-yield issuers

- Payment Calculation Example: For CDX NA IG at 50 bps spread with $100,000 notional per company, annual payment = 125 × 0.005 × $100,000 = $62,500 ($500 per company)

- Default Mechanics: When an index company defaults:

- Contract continues with remaining companies (e.g., 124 after one default)

- Protection seller pays (1 – Recovery Rate) × $100,000 notional

- Annual payment adjusts downward (e.g., to $62,000, reducing by $500)

- Index Spread and Updates: Index spread approximately equals the average credit spread of constituents; indices update semi-annually with companies downgraded below investment grade replaced by other investment-grade companies (applies only to new contracts post-update)

Practice Questions: Q2

Q2. If one of the entities in the CDX NA IG index defaults, the CDS index would most likely:

A. make a payoff and be discontinued.

B. continue with a replacement entity, with no change to the notional principal.

C. continue with 99 entities, and the notional principal of each entity would be reduced by 1%.

D. continue with 124 entities, and the notional principal of each entity would remain the same.

Practice Questions: Q2 Answer

Explanation: D is correct.

The CDX NA IG index has 125 equally-weighted entities. When one of these

entities defaults, the existing CDS would continue with 124 entities with the same notional per entity.

Topic 5. Fixed Coupons

-

Market Liquidity: CDS contracts are standardized to improve market liquidity such that the protection buyer pays fixed coupon rates instead of the actual market CDS spread.

-

Up-front Premium: The difference between the coupon rate and the spread is settled at initiation using an up-front premium

-

-

where:

-

D = CDS payment duration (e.g., 2.6529 in the 3-year example).

-

s = Quoted CDS spread

-

c = Fixed coupon rate

-

-

- The price of the CDS contract is computed from spread price as:

-

-

Example: A 5-year CDX NA IG CDS has a fixed coupon of 100 bps (0.01). The current market CDS spread is 65 bps (0.0065), and the duration is 4.125.

-

Answer:

-

As the price is > 100, the protection seller pays the protection buyer. This makes sense, given that the protection buyer is committing to paying a higher coupon of 100 bps compared to the justified spread of 65 bps. The amount that the protection seller pays to the buyer is computed as:

-

-

-

\text{up-front premium \%} = D \times (s - c)

\text{Price} = 100 - [100 \times D \times (s - c)]

\text { Price }=100-[100 \times 4.125 \times(0.0065-0.01)]=101.44 \text {, or up-front premium }=1.44\%

\text { up-front payment by seller }=125 \times 100,000 \times 0.0144=\$ 180,000

Topic 6. CDS Forwards and Options

-

CDS Forwards

- Structure: Contract allowing a party to enter a specific CDS as protection buyer or seller at a fixed spread and term, starting at a specified future date

- Example: Enter a 5-year CDS at 100 bps spread starting one year from today

- Default Impact: Forward contract terminates if the reference entity defaults before the forward start date

- Structure: Contract allowing a party to enter a specific CDS as protection buyer or seller at a fixed spread and term, starting at a specified future date

-

CDS Options

- Structure: Grant the holder the right to enter a CDS at a strike spread (protection buyer or seller) in exchange for an option premium

- Example: Option to enter 2-year CDS as protection buyer at 100 bps strike is exercised when current CDS spread exceeds 100 bps

- Default Impact: Option ceases to exist if the reference entity defaults before option maturity

- Structure: Grant the holder the right to enter a CDS at a strike spread (protection buyer or seller) in exchange for an option premium

Practice Questions: Q3

Q3. Which of the following statements about CDS forwards and CDS options is most accurate?

A. CDS forwards entered at market rates require a premium payment, while CDS options do not.

B. CDS options entered at market rates require a premium payment, while CDS forwards do not.

C. Both CDS forwards entered at market rates as well as CDS options require a premium payment.

D. Neither CDS forwards entered at market rates nor CDS options require a premium payment.

Practice Questions: Q3 Answer

Explanation: B is correct.

CDS forwards entered at market rates do not require a premium payment.

However, CDS options do require a premium payment to the option writer who is willing to take the risk of option exercise.

Module 3. Total Return Swaps and Collateralized Debt Obligations

Topic 1. Total Return Swap (TRSs)

Topic 2. Collateralized Debt Obligations (CDOs)

Topic 3. Synthetic CDOs

Topic 4. Synthetic CDO Valuation: Spread Payments Approach

Topic 5. Synthetic CDO Valuation: Gaussian Copula Approach

Topic 6. Implied Correlation

Topic 7. Gaussian Copula Model Alternatives

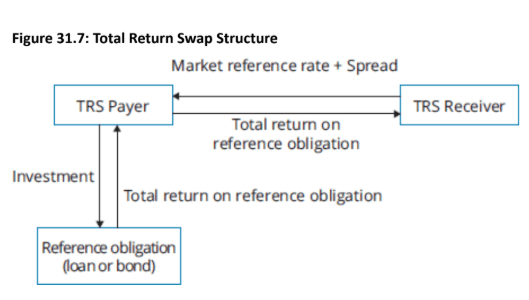

Topic 1. Total Return Swaps (TRSs)

- TRS Structure: One party pays the total return (coupon/dividend plus price change) of an asset in exchange for a fixed or floating rate

- Dual Risk Coverage: For risky bonds, TRSs are not pure credit derivatives as they hedge both credit risk and interest rate risk simultaneously

- Financing Mechanism: TRSs allow investors to indirectly fund the purchase of risky bonds without direct ownership

- Example: Consider an investor wanting to purchase $20million worth of a corporate bond. The investor enters into a TRS.

- Investor receives total return on the bond with notional amount ($20million)

- Investor pays market reference rate plus a spread (e.g., 50 bps)

- Effectively, the investor borrows funds at reference rate plus spread to finance the bond purchase

- Spread Components: The 50 bps spread compensates the TRS payer for:

- Credit risk of the TRS receiver

- Correlation between the corporate bond's credit risk and the TRS receiver's credit risk

- Settlement at Maturity:

- TRS payer pays any bond price appreciation to TRS receiver

- TRS receiver pays any bond price depreciation to TRS payer

Topic 1. Total Return Swaps (TRSs)

Topic 2. Collateralized Debt Obligations (CDOs)

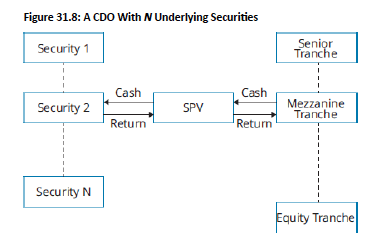

- CDO Structure: Claims against a portfolio of risky debt securities, divided into tranches with varying levels of credit risk

- Tranche Hierarchy: Senior tranches bear lower credit risk compared to junior tranches, reflecting different priority levels in the capital structure

- Distribution Waterfall: Specifies the order and allocation of cash flows generated from the underlying portfolio to the various CDO tranches

Topic 3. Synthetic CDOs

- Synthetic CDO Definition: Similar credit risk exposure to cash CDOs but assembled using credit default swaps (CDS) rather than actual debt securities; protection sellers gain credit risk exposure without purchasing bonds, with notional principal equal to the sum of all CDS contract notionals

- Cash Flow Mechanics: Originator receives CDS spreads from protection buyers and pays out default losses; example: $100 million notional CDO with 25 bonds ($4 million each) at 2% average spread generates $2 million annual spread cash flow

- Tranche Structure (Waterfall Distribution):

- Equity Tranche (5% / $5M): Absorbs first 5% of credit losses; receives highest return of 10% annually ($0.5M); return paid on reduced principal as losses absorbed; wiped out once losses exceed 5%

- Mezzanine Tranche (20% / $20M): Bears losses from 5% to 25% after equity exhausted; earns 5.625% return ($1.125M) annually

- Senior Tranche (75% / $75M): Bears losses exceeding 25% of total notional; receives lowest return of 0.5% ($0.375M) annually; structured for very high credit rating

- Funding and Collateral: Synthetic CDOs are unfunded as there is no cash outlay to purchase debt; tranche investors post collateral and make deposits to meet obligations if credit losses occur requiring payments

- Market Liquidity: Individual tranches trade separately with liquid markets existing for standard tranches on synthetic CDOs based on credit indices

Topic 4. Synthetic CDO Valuation: Spread Payments Approach

-

Valuation Approaches: The two approaches for valuing synthetic CDOs (i.e., calculation of the CDS spread) are:

-

Spread Payments Approach: Based on the PV of expected payments and the PV of expected payoff

-

Gaussian copula model.

-

- Spread Payments Approach

- Spread Calculation Method: Calculate the spread on a single synthetic CDO tranche by setting the present value (PV) of expected inflows equal to the PV of expected outflows

- Expected Inflow Dependency: For a single tranche, PV of expected inflows depends on spread payments, which are determined by the outstanding principal amount of the tranche

- Settlement Assumptions:

- Model assumes annual settlement for simplicity, though it can be generalized for other time periods

- Losses are assumed to occur midway through each settlement period

- Principal Dynamics: As the tranche experiences losses, its outstanding notional principal declines, directly affecting future spread payment calculations

Topic 4. Synthetic CDO Valuation: Spread Payments Approach

-

Expected Loss: The expected loss at time t is calculated as:

-

- Expected Payoff: The CDO tranche expected payoff is:

-

The of $1 received at time t. We subtract 0.5 from t to account for losses occurring midway through the time period. For example, if a loss occurs in the second year, we are discounting the loss for 1.5 years.

-

The total spread payments to be received during the life of the CDO = , where:

-

-

The final accrual period (because of the assumption of a loss midway through the

settlement period) = , where:

-

-

Note that the accrual period payment is only for the loss amount. The remaining notional was already accounted for as part of the calculation for A.

E L_t=E\left(N P_{t-1}\right)-E\left(N P_t\right)

\mathrm{C}=\sum_{\mathrm{t}} \mathrm{EL}_{\mathrm{t}} \times \mathrm{DF}_{\mathrm{t}-0.5}

DF_t=PV

A \times s

\mathrm{A}=\sum_{\mathrm{t}} \mathrm{E}\left(\mathrm{NP}_{\mathrm{t}}\right) \times \mathrm{DF}_{\mathrm{t}}

B \times s

\mathrm{B}=\sum_{\mathrm{t}} \mathrm{EL}_{\mathrm{t}} \times \mathrm{DF}_{\mathrm{t}-0.5}

Topic 4. Synthetic CDO Valuation: Spread Payments Approach

-

The total PV of expected cash inflow to tranche investors = , and the total PV of expected cash outflows on account of credit losses = C

- Breakeven Spread: Setting these equations equal results in the breakeven spread:

-

For tranches with a standard coupon (spread) s*, the up-front premium of NP is:

-

-

s=\frac{C}{A+B}

s \times (A+B)

\text{up-front premium}=\left[\mathrm{C}-s^* \times(\mathrm{A}+\mathrm{B})\right]

Topic 5. Synthetic CDO Valuation: Gaussian Copula Approach

- Copula Function: A copula joins a multivariate distribution of time to default (for numerous debt obligations in a CDO collateral pool) to its one-dimensional marginal distribution functions

- One-factor Gaussian Copula Model: Homogeneous model assuming identical time-to-default probability distribution Q(t) for all reference entities in the CDO collateral pool

- Popular methodology for pricing CDS tranches

- Assumes constant copula correlation between any pair of companies

- Conditional Probability of Default: Given unconditional PD of Q(t), the conditional PD Q(t|F) in a one-factor Gaussian copula model is expressed as:

- Unconditional PD Calculation: Computed using constant hazard rate λ (risk-neutral probability implied in market price):

- Binomial Distribution Application: 2 possible outcomes per period (default/no default)

- Probability of exactly k defaults out of n companies by time t:

-

- Probability of exactly k defaults out of n companies by time t:

- Tranche Loss Estimation: Expected values of notional principals and losses absorbed in each time period for each tranche are computed using the estimated probability of default

\rho

Q(t \mid F)=N\left(\frac{N^{-1}[Q(t)]-\sqrt{\rho} F}{\sqrt{1-\rho}}\right)

Q(t)=1-\mathrm{e}^{-\lambda \times t}

P(k, t \mid F)=\frac{n!}{(n-k)!k!} Q(t \mid F)^k[1-Q(t \mid F)]^{n-k}

Practice Questions: Q1

Q1. At inception, the tranches in a synthetic CDO are priced to earn a spread that is:

A. equal for each tranche.

B. consistent with their seniority.

C. aggregate in amount to the premium paid to binary CDSs.

D. higher for senior tranches, as they represent a larger notional principal.

Practice Questions: Q1 Answer

Explanation: B is correct.

At inception, the tranches in a synthetic CDO are priced to earn a spread that is

consistent with their risk level (i.e., seniority in the distribution waterfall). The

aggregate spread amount is set equal to the premium received as a protection

seller in a vanilla CDS. While senior tranches normally have a higher notional

principal, the spread (as a rate) is lower due to the lower credit risk of the senior

tranches.

Topic 6. Implied Correlation

- Model Inputs and Calibration: Using industry standard 40% recovery rate, the missing input for estimating tranche spread is copula correlation; similar to calculating implied volatility in Black-Scholes-Merton model, market-implied correlation can be derived

- Compound (Tranche) Correlation: The correlation value that equates model-calculated tranche spread to market-quoted spread for a specific tranche; determined through iterative search process

- Base Correlation: Derived from compound correlations using an iterative process to determine present value of expected loss for each CDO tranche consistent with current market prices

- Compound Correlation Pattern - "Correlation Smile":

- Starts high for junior tranches

- Declines initially, then rises again with seniority

- Base Correlation Pattern - "Correlation Skew": Correlations rise monotonically with tranche seniority

- Model Limitations: If one-factor Gaussian copula model were consistent with market prices, implied correlations should be identical across all tranches; pronounced smile or skew patterns reveal inconsistency with market pricing and expose limitations of the one-factor model

Practice Questions: Q2

Q2. Base correlation and compound correlation are both:

A. tranche correlations.

B. implied correlations.

C. not relevant for synthetic CDOs.

D. exhibiting a skew with correlations rising with tranche seniority.

Practice Questions: Q2 Answer

Explanation: B is correct.

Compound (or tranche) correlation and base correlation are implied correlations

that are calculated differently. While compound correlations exhibit a smile

pattern, base correlations show a skew pattern.

Topic 7. Gaussian Copula Model Alternatives

-

Limitations of One-Factor Gaussian Copula:

- Does not account for fat tails in real-world probability distributions for time to default

- Fails to capture the observed correlation smile/skew phenomenon

-

Alternative Models:

- Heterogeneous Models: Allow specification of different distributions for time to default across different reference entities in the collateral pool; significantly more complex and cannot use binomial model for probability of k defaults at time t

- Alternative Copulas: Include Student's t copula, Archimedean copula, Clayton copula, and Marshall-Olkin copula

- Random Recovery Rates and Factor Loadings: Based on the negative relationship between default rates and recovery rates

- Implied Copula Model: Derived directly from market prices

- Dynamic Models: Include structural and reduced-form models that measure the evolution of loss on a collateral pool over time

Practice Questions: Q3

Q3. The structural model of credit risk is most likely a(n):

A. dynamic model.

B. heterogenous model.

C. implied copula model.

D. random recovery rate model.

Practice Questions: Q3 Answer

Explanation: A is correct.

Dynamic models, including structural and reduced-form models, capture the

evolution of loss on a collateral pool over time. Heterogenous models allow for

specification of different distributions for time to default for different reference

entities included in the collateral pool. Random recovery rates and factor loadings

are based on the negative relationship between default rates and recovery rates.

The implied copula model is derived from market prices.

CR 13. Credit Derivatives

By Prateek Yadav